Abstract

In the current venture capital climate, it is easier to secure funding for late-stage, next-in-class therapeutic agents than for early-stage opportunities that have the potential to advance basic science and translational medicine. This funding paradigm is particularly problematic for the development of “dual-use” biothreat countermeasures such as antibiotics, vaccines, and antitoxins that target pathogens in novel ways and that have broad public health and biodefense applications. To address this issue, we propose the creation of the Drug Development Incentive Fund (DDIF), a novel funding mechanism that can stimulate the development of first-in-class agents that also possess the capability to guard against potential biothreats. This program would also support greater synergies between public funding and private venture investment. In a single act, this organization would secure science of national importance from disappearing, invest in projects that yield significant public health returns, advance the promises of preclinical and early phase research, revitalize biopharmaceutical investment, and create valuable innovation-economy jobs.

In recognition of the high cost, high risk, and low profit margins associated with vaccine and antibiotic development, the U.S. government has undertaken several measures to improve its level of preparedness and to encourage the development of medical countermeasures (MCMs) for procurement. An incentive for companies to develop products, the Project BioShield Act of 2004 was passed with a $5.5 billion appropriation primarily to create a market for chemical, biological, radiological, and nuclear (CBRN) responses; it offers a guarantee that the U.S. government would procure successfully developed countermeasures for the Strategic National Stockpile (SNS). While the enactment of this program reduced some market risk, it did very little to help reduce development risk. The belief that the U.S. government could create or somehow guarantee a market for these products was later undermined when large sums of the appropriated monies were part of Congressional rescissions. Project BioShield also established a process for the Department of Health and Human Services (HHS) to award grants and contracts to prospective developers of these responses, and the authority for the agency to administer unapproved therapies deemed to be efficacious for emergency use authorizations. The Pandemic All-Hazards Preparedness Act of 2006 was passed later to widen the agency's authorities and to create the Biomedical Advanced Research and Development Authority (BARDA) to oversee HHS's Project BioShield and to address other public health priorities.4,6

To date, these legislative efforts have had some success in procuring MCMs for the SNS that are reasonably advanced in the development pipeline. In 2007, for example, the federal government invested $505 million under Project BioShield for the development, manufacture, and purchase of 20 million smallpox vaccines for immune-compromised populations. 7 * However, despite this and similar stockpiling achievements, significant gaps remain in the government's ability to swiftly respond to emergent biothreats. These deficiencies came to light during the 2009 H1N1 influenza pandemic, as HHS procured and tested a successful vaccine candidate for H1N1 but was unable to distribute it before the virus had spread widely in the general population. Another problem specific to Project BioShield has been its inability to expand the nation's pool of anthrax vaccine suppliers beyond a single manufacturer. These and other shortcomings have cast doubt even in the White House about the ability of these government programs to meet the nation's biodefense needs.8,9

Given the deficiencies in the current framework, we believe that the potential exists for an alternative funding structure that can achieve greater synergy between the public and private sectors and foster a more robust development of agents that possess dual-use capabilities in both biodefense and translational medicine. As we have seen in aerospace, microelectronics, and other high-tech fields, leading-edge advances in science and technology for defense purposes often lead to broader commercial applications. We believe that similar results can be experienced in the domain of biotechnology. With continued research and partnerships between the public and private sectors, advances made for purposes of biodefense can readily be leveraged into broader medical applications, resulting in a tremendous benefit to public health and vice versa. †

Current Funding Models for Early-Phase Companies

Drug development is a high-risk, high-cost enterprise. The cost of developing each newly FDA-approved drug (taking into account development costs of failed agents) is approximately $1.3 billion (USD), with elapsed time from identifying a new molecule to approval taking 10 to 15 years. For every 5 drugs that enter into clinical trials, only 1 is eventually approved and only 2 out of 10 generate sufficient revenue to recover the cost of their development. 10

There is a perception that large pharmaceutical companies are powerhouses for advancing first-in-kind therapeutics based on novel technology. That is not the case. These large, publicly held companies are driven by financial metrics such as quarterly earnings-per-share. Risky or overly expensive research and development efforts adversely affect these metrics and are avoided. Thus, instead of focusing on critically needed R&D breakthroughs, large pharmaceutical companies have concentrated their efforts on increasing market size and share of existing drugs and biologics to meet their earnings goals.

In the absence of “big pharma financing,” venture capital (VC) investments are widely considered to be one of the most important avenues to new drug and technology development. In 2007, healthcare venture financing accounted for 31% of the $30 billion in total venture investments.1,11 Within the pharmaceutical sector, venture capital–backed biotechnology acquisitions accounted for more than two-thirds of big pharma product pipelines, in essence supplanting in-house research and development efforts. 12 This phenomenon is so pronounced that approximately 26.1% of sales from the 20 largest pharmaceutical companies will be derived from in-licensed products in 2010. 1 According to the data, venture capital has become the de facto engine of product development for the majority of biopharmaceutical agents and, as a direct consequence, significantly guides the course of science and discovery, thereby directly determining the pool of new products and technologies that can be evaluated for biodefense and used for public health.

The strict dependence on VC investment to drive biopharmaceutical development is particularly problematic in the current economic climate as VCs struggle to meet their fund-raising objectives. Total U.S. healthcare venture investment dropped by 25% to 50% in the final quarter of 2008. Similarly, first round VC deals in biotechnology decreased by 40% from 130 to 78 deals between 2008 and 2009 (Figure 1). Total biotechnology VC deals, including follow-on round offerings, also decreased over the same period, from 501 to 406 deals. 13 Though 2008 and 2009 were unusual recession years, a poll conducted by the National Venture Capital Association revealed that 90% of venture capitalists believe the number of VC firms will decline over the next 5 years, further reducing the availability of private capital to fund product development. 14

VC Investment in Biotech by Number of Deals 2000-2009. Color images available online at www.liebertonline.com/bsp.

In addition to bringing about an absolute reduction in venture financing within the biopharmaceutical space, the recession also highlighted how the profit maximizing objectives of VCs do not necessarily overlap with the government's interest in developing genuinely novel products or diverse, sustainable product pipelines. This notion is apparent as venture investors have recently sought to maximize their returns by shifting investments toward start-ups with immediate clinical assets. In 2004, 77% of the 26 biotech/biopharmaceutical companies that completed IPOs (initial public offerings) had already developed a late-stage (Phase 2) lead drug, whereas only 12% were still at the preclinical stage with their most advanced product. 15 In the last quarter of 2008 and the first 2 quarters of 2009, only approximately $323 million was invested by healthcare venture capitalists in early-stage biopharmaceutical start-ups. 16

VC firms have also become increasingly conservative in their risk tolerance. 17 Inherently higher risk practices associated with funding seed or early-stage research, which lack either proven efficacy or proven market viability, are more likely to be rejected in favor of later-stage opportunities with defined markets and predictable annual sales.2,17 Next-in-class drugs, in which the regulatory environment is relatively well defined, are also more likely to be supported rather than programs that rethink basic science and explore potentially new biological pathways. As a result, the chance that an investment will be made in a new therapeutic area has decreased in comparison to the likelihood that it will be made in a “me-too” product space.

From the standpoint of scientific discovery, this approach is detrimental, because it channels resources toward single, incrementally advanced technologies instead of research that has the potential to yield completely new treatment modalities and generations of rich product pipelines. This paradigm also limits the development of products for biodefense, since the expected profits resulting from government consumption may not justify the opportunity cost of forgoing the development of next-in-class drugs with a wider consumer base.3,18 Furthermore, this strategy effectively reduces the diversity of technologies that can be procured by the U.S. government, since only those companies that satisfy the risk profile and profit generation potential of private investors are given the opportunity to mature and develop.

A Novel Funding Source for Early-Phase Research

In light of the VC paradigm described above, innovative research and development programs that generate novel biothreat countermeasures, especially those with dual-use potential for broader public health applications, must be identified, funded, and supported financially and structurally early in the development cycle so they have the opportunity to advance to market. Otherwise, vital scientific research and development will continue to diminish. Ideally, such a funding vehicle must also save and create the type of high-tech, innovation economy jobs the U.S. needs to remain globally competitive in the biopharmaceutical space.

After researching several models of current and historical government R&D incentive programs (DeVenCI, OnPoint, Red Planet, and In-Q-Tel) and grant-based financing, we believe that a U.S. government–funded Drug Development Incentive Fund (DDIF) should be created to provide risk-capital to privately held or publicly traded early-stage biotechnology and pharmaceutical companies with novel agents or technologies. We believe that the DDIF should follow the venture model as it mirrors the natural pathway for biopharmaceutical development in the U.S. and provides an opportunity for government to synergistically link with private venture firms, albeit through an intermediary. We also favor this approach in contrast to the traditional government grant structure that is commonly used to fund and advance basic science. While it is true that grants encourage scientific innovation, they do not facilitate the translation of that innovation into a commercialized product and are, at best, a passive form of investment. From our experience, a company with good science but led by managers with poor business acumen and little experience in clinical development is unlikely to successfully bring a product to market.

A structure like the DDIF is also preferred to programs such as the Defense Venture Catalyst Initiative (DeVenCI), which provides no funding at all. 19 Rather, the objective of DeVenCI is to increase Department of Defense (DoD) awareness of emerging technologies developed outside traditional DoD procurement. It acts solely as a conduit to improve communication among innovators, private venture capital, and the DoD. Without funding, it does little to change the risk calculus associated with private investment and does not motivate venture capital to look beyond the portfolio of companies that are already considered viable investments.

Better incentive models, such as the On Point program developed by the U.S. Army and the CIA's In-Q-Tel, provide funding for technologies that directly benefit the objectives of its target organization and have wide applicability in the commercial sector. Of the two models, In-Q-Tel is of particular interest, since it has enjoyed considerable success 20 and because its investment strategy assures that demand for a technology by its primary government client, the CIA, already exists. Given the clear demand expressed by the DoD and HHS for biopharmaceutical agents that act both as a safeguard against bioterrorism and to protect against infectious agents, we believe that the In-Q-Tel model is one that should serve as the structural framework for the creation of the DDIF. We also note the investments of Silicon Valley venture capital firm Kleiner Perkins Caufield & Bauer's (KPCB) Pandemic and Biodefense Fund, a $200 million source of private capital for the sector. As we have calculated, KPCB's Biodefense Fund has to date made investments in at least 5 companies with applicable technologies in the space, investing heavily in vaccine technology and microbial detection device companies. 21 While these are important investments, a major differentiating characteristic of the DDIF would be its ability to take positions in companies with riskier technologies in support of novel therapies and potentially breakthrough platforms that may require longer time horizons. Additionally, the DDIF's sole focus would center on the needs of its government clientele, and one of its primary directives would be to build substantial relationships with partnering VC's in similar endeavors, encouraging other VCs to follow the example of KPCB (see Table 1).

Funding Structures

In-Q-Tel and Government Precedent for the DDIF

In-Q-Tel is a strategic venture capital and incubation fund brought into existence in 1999 by the CIA to provide the agency with advanced communication and information technologies vital to the U.S. strategic national interest. Backed by funding appropriated by Congress, In-Q-Tel is structured as an independent, not-for-profit corporation that identifies and invests in companies developing these technologies. 20 Through its investment strategies, In-Q-Tel is able to protect and nurture technologies otherwise overlooked and undeveloped by companies pursuing wider consumer markets. By building a network of more than 150 venture capital firms, maintaining affiliations with national laboratories, and fostering university outreach programs, In-Q-Tel is strategically positioned to access new technologies and explore seeding of new start-ups.

Logistically, In-Q-Tel typically takes an interest in emerging companies at the early stage of investment, acquiring equity positions or warrants in investment targets in exchange for capital infusion. With annual appropriations of approximately $30 million, the organization is able to leverage its venture pool by attracting partnering VCs to its deals, thereby inviting more dollars to the table and creating a competitive funding environment. The majority of the companies that In-Q-Tel invests in are small, privately held organizations with advanced technologies with commercial applications. All investments center on a working plan that links the disbursement of investment capital to mutually agreed upon milestones of product development. Furthermore, In-Q-Tel takes observer seats or full positions on the boards of its portfolio companies. This maneuver facilitates the transfer of knowledge about the product space and the special needs of the consumer.

To ensure that target investments meet the specific needs of its client, In-Q-Tel also makes use of an Interface Center (QIC), which is comprised of CIA employees. The QIC provides a direct link to the agency and supplies a list of specific, unclassified technology needs that serve as a general focus for In-Q-Tel's investments. Perhaps more so than any other component of the In-Q-Tel structure, the direct communication established by the QIC ensures that the fund's investment philosophy remains contemporary to the immediate needs of the client and improves the chances that the right solutions are fully developed and ultimately purchased.

The Drug Development Incentive Fund

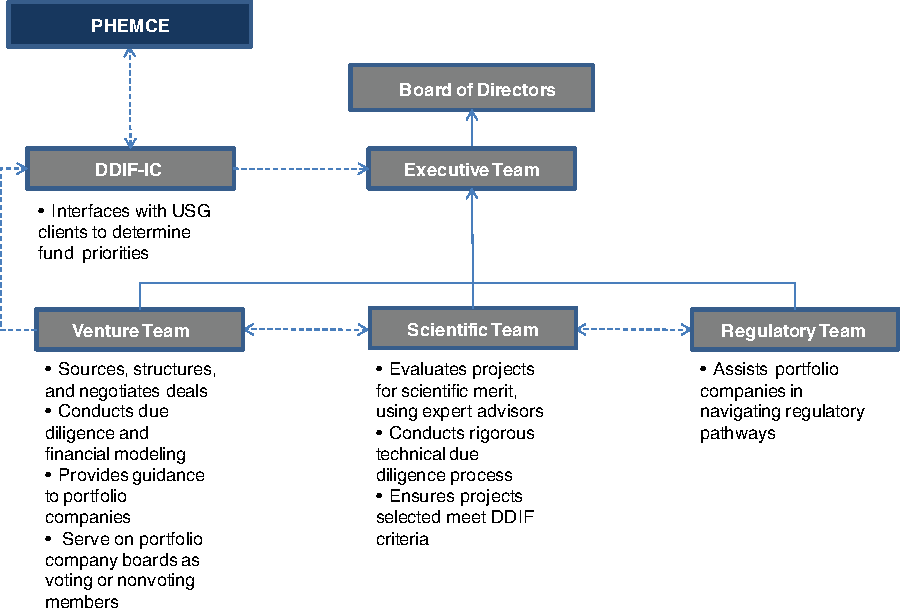

Modeled after In-Q-Tel, the DDIF would function as an independent, nonprofit organization that would be a strategic biodefense and drug development venture fund. The DDIF would follow a directive for funding set by the needs of its government clients, which would include HHS BARDA, NIH/NIAID, and potentially the DoD. The work of the Public Health Emergency Medical Countermeasures Enterprise (PHEMCE)—composed of members from various agencies involved in biodefense preparedness, including the Centers for Disease Control and Prevention, the Food and Drug Administration, and the National Institutes of Health—could be used to establish the problem sets the DDIF would seek to address. PHEMCE, as a planning nexus, continuously manages HHS's priorities for countermeasure development. However, the DDIF would have latitude in the strategies it would employ to meet these needs. ‡

Primarily, the DDIF would be charged with generating new development programs that can seek assistance from agencies such as BARDA once they mature. While the NIH can invest in early-stage technologies, and authorities such as BARDA can continue to provide financial support for more developed technologies, we believe the DDIF, a new, potentially sustainable funding source that targets early-stage development, can provide both investment capital and strategic guidance to target companies, which government agencies are restricted in their ability to do. As a result, DDIF investment would bridge the gaps in federal funding to more aggressively promote first-in-class therapeutics and technologies with potential collateral benefits for biodefense while simultaneously imparting strategic leadership to create a business infrastructure that can sustain product development. This secondary mandate is crucial since, in many instances, the development of novel biopharmaceutical technologies is not hindered by scientific or technical issues alone, but also by a failure of the underlying company to function successfully as a business or navigate the complex regulatory processes involved in drug development.

A second and collateral objective of the DDIF could be to fund early-phase R&D for novel therapeutics for public health. These opportunities (eg, new classes of antimicrobials or orphaned antimicrobials) may or may not have overlapping utility and dual use with biothreat defense, but they should demonstrate some significant benefit to translational medicine. With an emphasis on investing in technologies and biopharmaceutical agents that can successfully transition to BARDA, as well as addressing other unmet public health needs, we believe that investment by the DDIF can reduce the risk profile of its targets and attract leveraged financing from sources of private investment. Because the multiplicative effect of capital from both the federal government and private institutions will support ventures that are currently overlooked by both funding sources, we believe that the government can be more nimble in its ability to produce a robust pipeline of medical countermeasures and revolutionary biopharmaceuticals that advance translational medicine and benefit public health. Culturally, the organization should be agile and free from bureaucracy, but it must remain process oriented and results driven. Additionally, the DDIF would retain transparency and interface with government agencies that have specific, predefined objectives for biodefense, thereby increasing the likelihood that products are developed with significant procurement potential and with wider translational applicability.

To gain public acceptance and industry legitimacy, the DDIF would be established through legislative action. In conjunction with the DDIF, a QIC-like structure (the DDIF-IC) would also be created as an internal mechanism to interface with PHEMCE and other government clients of the DDIF. This apparatus would provide the DDIF with an internal “problem set” of highly specific strategic needs pertaining to biothreat defense and public health that would guide the investment strategy adopted by the fund. Facilitated communication through an Interface Center would also minimize DDIF funding of potential investments that duplicate the ventures of other government-backed programs.

Given the exorbitant costs associated with product development, the DDIF would seek to leverage its capital investment by attracting traditional VCs and pharma venture arms to co-invest in opportunities that were thoroughly evaluated by the DDIF. To maximize the likelihood of follow-on capital, the DDIF would promote transparency in its investments by specifying how a target organization and its technologies meet the needs of the problem set advanced by the DDIF-IC and outline potential transition strategies of these technologies to BARDA or other strategic partners within the federal government should a viable product emerge. Using In-Q-Tel as a guide, the DDIF would attempt to leverage its initial risk capital by at least 5 to 1. As a percentage of the early-stage companies become successful and seek exits, the fund would be repaid like any other investor, recouping its initial investment—perhaps by as much as 10 to 1 in certain circumstances—and thereby replenish and grow the fund for the future. §

Subsequent rounds of financing from the DDIF would not be required if other VCs and government R&D programs are used for continued development. BARDA, for example, provides funding for companies with late-stage technologies and can provide contracts with milestone provisions for purchase and procurement. Cash rich and R&D poor pharmaceutical companies, starved for breakthrough discoveries, would also be logical strategic partners once promising candidates have been brought by DDIF companies to later stages, if not lured earlier by the DDIF, especially if those drugs or the platforms that were developed have applications that are relevant to broader public health needs.

After sufficient initial appropriations, the DDIF would attempt to become a self-sustaining fund. It would receive stock and warrants or hold debt like any other investor through such equity or equity-like instruments. The DDIF would experience a return on investment to be used for future investments when a portfolio company achieved a significant monetizing event such as being acquired by a larger pharmaceutical company, issuing an initial public offering, or exercising open market exit strategies. This is a significant distinguishing characteristic of the DDIF that the NIH/NIAID and BARDA lack: its ability to take an ownership and, consequently, a leadership position in a company.

Like its deal structure, the DDIF's operational structure would follow industry practice, with a board of directors composed of well-respected members from the investment, academic, pharmaceutical regulatory, and drug development fields; a Venture Team, charged with sourcing, structuring, and negotiating deals, financial modeling, conducting due diligence, guiding companies, and protecting DDIF investments by serving on portfolio company boards as observer or voting members; a Scientific Team to evaluate projects, conduct a rigorous technical due diligence process, and ensure projects selected meet the criteria of the DDIF; and a Regulatory Team, assigned to assist portfolio companies in navigating the regulatory pathway (Figure 2). Each team would be kept small to promote operational efficiency. These teams would provide valuable insight and leadership to target investment companies and further enhance the likelihood of successful product development, thus making target investments more appealing to private VCs.

DDIF Organizational Structure. Color images available online at www.liebertonline.com/bsp.

The value of the regulatory component of the DDIF should not be underestimated. Private investors meet the regulatory process with open skepticism, discounting investment potential significantly by the hurdles the FDA evaluation process may include. If early in the process and short on resources, the regulatory process around drug candidates is not clearly known by company management. Companies at this stage usually outsource such functions to outside consultants who have varying degrees of expertise. DDIF's experienced regulatory guidance would provide early-stage companies with a capability that otherwise would be very costly and, depending on who is selected by companies to provide regulatory guidance, risky. A DDIF Regulatory Team would reduce the risk associated with regulatory processes that the investment community uses to discount the investment potential of biotechnology and pharmaceutical targets, adding an additional layer of comfort for sources of private capital.

With these mandates and an appropriate structure, we believe that the DDIF is capable of altering the current funding paradigm associated with the development of novel biopharmaceuticals. Transparency in the funding process, DDIF guidance for business development, and the potential to produce technologies with broader commercial applicability would lower the risk calculus for private VCs and facilitate follow-on investment. Investment by the DDIF would also be attractive to development/early-stage companies themselves. DDIF endorsement would carry significant weight in the investor and scientific communities, validating the scientific merit and commercial potential of portfolio assets and attracting VCs and pharmaceutical venture arms to take part in the funding process. While there can never be a guarantee of product procurement, the likelihood that BARDA or some other agency will use the product for the SNS or that that the product itself has viability within broader commercial markets would be enhanced. Furthermore, DDIF endorsement would provide easier funding for early-stage companies with innovative therapeutics that otherwise would have difficulty raising capital.

Conclusion

Ultimately, by establishing a relatively modest-sized fund to stimulate early development of treatments, the U.S. government can both meet the national defense objective of creating biothreat countermeasures and stimulate development of first-in-class therapeutics that will benefit public health. With sufficient appropriations, the DDIF could invest $100 million a year for 3 years with partial exit strategies starting as early as year 4, followed by reinvestment of newly available funds. Individual investments by the DDIF would be made in the range of $2 million to $10 million in co-investment opportunities potentially as high as $50 million to $100 million, with participating VCs providing the additional funding.

Creation of the DDIF would result in significant dividends. In a single act, this organization would secure science of national importance from disappearing, invest in projects that yield significant public health returns, advance the promises of preclinical and early phase research, revitalize biopharmaceutical investment, and create valuable innovation-economy jobs. The externality of job creation would not be trivial: venture-financed life science companies supported 493,800 jobs in 2006 and generated more than $132 billion in revenue.22,23 Some projections indicate that for every job in biopharmaceuticals, an additional 6.7 jobs are created in other sectors of the economy, yielding a total employment of 3.3 million jobs in the sector (2.1% of total U.S. employment). 22 Most important, more than 250 biotechnology products have been approved by the FDA with more than 600 new drugs in clinical trials today.2,24

We note in closing that the idea of a government-backed venture fund is beginning to gain traction among policymakers in Washington, DC. In the recent HHS Public Health Medical Countermeasures Review, published in August 2010, HHS reviewed and identified several barriers to the development of a robust arsenal of medical countermeasures, including regulatory limitations, manufacturing capacity, financial incentives, and the like. In postulating a multiplicity of solutions to this problem, the review recommended that HHS consider establishing and sponsoring an independent strategic investment firm and seek any required statutory authority to implement this initiative. 25 This idea is the very essence of the DDIF that we have espoused in this article.

In summary, the DDIF provides an opportunity for advancing early medical breakthroughs where a dangerous healthcare and national security fault now exists. Using a strategy of public/private leverage, a relatively modest government investment could address this dangerous shortcoming. The original tactic of leveraging was a useful tool to increase profit and reduce risk in investments. Unfortunately, recent Wall Street abuses have made leveraging a pejorative term. With successful execution of the DDIF program, the strategy of leveraging could begin its needed rehabilitation. If the fund's investments were to result in a single drug that significantly improved the quality of health care, the total investment program could be justified even without the consideration of pharmacoeconomics.

Footnotes

*

Delivery of the first million doses into the SNS occurred in May 2010. The remaining doses are expected by 2013.

†

As an example, one of the strategic goals of BARDA has been the identification of broad-spectrum antibiotics and antivirals that combat bioterrorism. Developments in this area can be leveraged to fight antibiotic resistant strains of bacteria (eg, Methicillin-resistant Staphylococcus aureus, or MRSA), which have emerged as a significant risk to public health.

‡

The DDIF would have wide-ranging discretion in its strategy to meet these objectives. The DDIF may be charged not only with the task of producing a medical countermeasure to a specific threat, but also for a more effective and efficient means of production and manufacture of that response, which may require strategic investments across disciplines.

§

Despite the current state of diminished VC interest in new therapeutic areas, we believe that leverage ratios at least as high as 5 to 1 are possible for several reasons. First, we are informed by the In-Q-Tel model. During the first 5 years of its existence, In-Q-Tel was able to leverage its government investment by raising $300 million from private sources to co-invest in its projects. 20 Second, initial investment by the DDIF lowers the risk profile of a company and demonstrates a clear customer demand for its biopharmaceutical agents. Third, the imprimatur of DDIF investment would mean that the company's technologies have undergone intense due diligence, thus further increasing the likelihood that private capital would experience significant returns from the commercial potential. High-yield opportunities with 10 to 1 returns currently exist in the market, but their risk profile, sometimes by virtue of novelty, acts as a barrier to entry for private investment.