Abstract

Abstract

Section 527 of the Internal Revenue Code generally exempts political organizations from federal income tax, but not on their net investment income. Section 527(f) imposes a similar tax on the “political activity” of Section 501(c) tax-exempt organizations like trade associations, labor unions, and tax-exempt lobbying organizations, in order to discourage use of such organizations to avoid the Section 527 investment income tax. The definition of “political activity” for these purposes was clarified in 1980, when Treasury promulgated regulations under Section 527(f). These regulations left the door open for future investigation and regulation in the form of “Reserved Regulations,” and Treasury assured taxpayers that any adverse changes to the regulations would be prospective. The Reserved Regulations remain reserved to this day.

The “reserved” gap in the regulations did not matter much for the first thirty years. Section 501(c) organizations, which are usually corporations (or unincorporated labor unions), were already constricted in their conduct of Section 527-type political activity by federal election laws that prohibited them from making independent expenditures supporting or opposing candidates. When the Citizens United decision came down, the first wave of reaction concerned the potential uses and perceived abuses of this new freedom by business corporations. Quickly, however, commentators noted that the Supreme Court had also created an opportunity for Section 501(c) organizations—free from income taxation, and (if careful) free from disclosure obligations—to engage in heretofore unprecedented levels of independent, expressly political activity. In theory, Section 527(f) and its Treasury Regulations discouraged this free-for-all by taxing the political expenditures of such entities, except that until the Reserved Regulations are promulgated, any political expenditures “allowed” by the FECA escape the tax. After Citizens United, what is “allowable” has mushroomed: A literal reading of the existing regulations renders all of those independent expenditures untouchable under Section 527(f).

While some practitioners and their clients may be willing to operate as if this literal, but in our view unreasonable, outcome is the best interpretation under the circumstances, others may prefer a more nuanced and, we believe, credible approach. In this article we examine the background of Section 527(f) and the Reserved Regulations, summarize the Internal Revenue Service's few attempts to interpret the latter, and then present our proposal for a revised interpretation of the current regulations. We hope this proposed framework will be helpful both to practitioners and counsel who are wrestling with similar matters, and to Treasury, should it decide it is finally time to promulgate the Reserved Regulations.

I. Introduction

A. Section 527: The intersection of election and federal tax law

Until 1975, election lawyers had little reason to consider how federal tax law affected their clients. No provisions of the Internal Revenue Code addressed the tax status of essentially political entities; such entities fell through the statutory cracks, neither clearly taxable nor tax-exempt. In practice, political parties, candidate campaign committees, and political action committees paid no tax on their income from any source,1 and as an administrative matter, the Internal Revenue Service (IRS) did not require them to file returns.2 However, all good things must end. In 1973 the IRS proposed to tax political organizations on their net investment income,3 and in 1975, Congress responded by enacting Section 527,4 bringing federal tax status issues directly into the election law world.5

Section 5276 exempts political organizations7 from tax on their income from political contributions, dues, political fundraising events or sales, and bingo games, provided the income is used only for the political organization's “exempt function.”8 Section 527(e)(2) defines politics—the “exempt function” of a political organization—as legally9 influencing or attempting to influence the selection, nomination, election, or appointment of any individual to any federal, state, or local public office or office in a political organization, or the election of presidential or vice presidential electors,10 abbreviated in Treasury Regulations (Regulations)11 as “the selection process.”12 Section 527 is thus the source of tax-exempt status for political organizations ranging from political parties and candidate campaign committees, to affiliated and freestanding political action committees, all of which share “politics” as their “exempt function.”13

Under Section 527, if a political organization's income is derived from traditionally political sources, it is generally exempt from income tax. Political contributions and gifts, dues directed to political activity or ticket sales made in response to political fund raising efforts, and sales of political campaign materials (outside the context of a trade or business) are all political sources that fall within this Section 527's concept of “exempt function income.” What does not qualify as “exempt function income” is revenue earned by the political organization on its investments or through a trade or business. All of a political organization's net income from these sources in excess of $100 per year must be reported to the IRS14 and is taxed under Section 527, generally at the then-highest corporate rate.15 Given the way most political organizations operate, in practice the effect is to tax their net investment income.

Once an incoming dollar meets the “exempt function income” test because it arises from a political source, that dollar must still be “segregated for use only for the exempt function of the political organization.”16 This means that that dollar must be kept in a separate bank account and eventually spent by the political organization on an “exempt function” activity; otherwise (the statute implies), that dollar will be taxed.

B. Section 527(f): Taxing the political activities of non-political tax-exempt organizations

To this point, this overview has focused on entities that Section 527 exempts from federal income taxes, i.e., political parties, candidate campaign committees, and independent or affiliated political committees. This article, however, is concerned with Section 527(f), the section of Section 527 directed at levying a tax not on political organizations described in Section 527, but on organizations exempt from federal income tax under Section 501(c).17 These tax-exempt organizations include labor unions (under Section 501(c)(5)), trade associations and chambers of commerce (both under Section 501(c)(6)), and social welfare organizations (under Section 501(c)(4)). Such entities are taxed by Section 527(f) if they make political expenditures within the meaning of Section 527. The Section 527(f) tax is levied on the lesser of such an entity's political expenditures or its net investment income.18 In other words, the net investment income is treated as if it had been spent on the political expenditures up to the amount of those expenditures, and so is taxed as if it had been earned by a Section 527 political organization, instead of by a Section 501(c) that would be otherwise exempt from tax on investment earnings. When codified, the intent of Section 527(f) was to equalize the treatment of Section 527 political organizations and Section 501(c) organizations to the extent that the latter behave like political organizations, thus discouraging the use of Section 501(c) organizations to avoid the taxes imposed by Section 527.

As an alternative to paying the Section 527(f) tax, a Section 501(c) organization can form a separate segregated fund (SSF) with as little formality as opening a bank account and notifying the IRS19 and perhaps the Federal Election Commission (FEC) or the applicable state agency,20 and make its 527-type expenditures strictly through the SSF. The SSF will be treated as a separate Section 527 political organization and taxed accordingly, including only owing income tax if the SSF had investment income or other non-“exempt function income,” instead of taxing the investment income of the affiliated Section 501(c) organization.21

There is little evidence in the legislative history to show how Congress intended Section 527 to relate to the federal or state election laws applicable to political organizations. The statute does explicitly refer to election laws twice: once to define what qualifies as an SSF of a Section 501(c) organization,22 incorporating both federal and state election law provisions, and again to define “principal campaign committee,” incorporating the federal election law definition.23 One commentator has opined that while “[l]ittle thought was given [by Congress] to the relation between [S]ection 527 and the [then] new [Federal Election Campaign Act24 (FECA)]… there appears to have been at least an implicit assumption that [S]ection 527 organizations would be subject to the FECA.”25 This assumption can explain the minimalist nature of the tax law under Section 527; Congress might have feared that detailed tax law provisions for political organizations would increase the potential for inconsistencies between the tax law and the FECA.26 It also highlights the focus on the FECA at the expense of attention to the breadth and variety of approaches used by the states to regulate elections and campaign finance, thereby creating some of the problems addressed in this article.

As noted above, the net effect of Section 527(f) is to tax labor unions, trade associations, social welfare organizations, and other 501(c)-tax-exempt organization that engage in politics on the lesser of their 527-type expenditures or their net investment income. Assuming most large, well-established Section 501(c) organizations are difficult to operate prudently without generating significant net investment income in the normal course of their operations, their 527-type expenditures (up to the extent of their investment income) will be taxed at the highest corporate rate. Any exception to what is included in the definition of a (taxable) political expenditure for such organizations is therefore a source of potentially significant tax savings.

C. The exception that swallowed the rule: The Reserved Regulations after Citizens United

This article focuses on two major exceptions found in the Regulations implementing Section 527. These exceptions render otherwise taxable 527-type expenditures nontaxable where the Section 501(c) organization (1) pays certain “indirect expenses” of a political organization27 or (2) makes certain expenditures that are “allowable” under the FECA or “similar State statute”28—but, in each case, the exception applies “only to the extent”29 provided in two other provisions of the Regulations. Unfortunately, those two provisions have been “reserved” by the Treasury since first promulgated in 1980 and they, together with the two exceptions that refer to them, are therefore often called, and will be called throughout this article, the “Reserved Regulations.” The scope of each exception in the Reserved Regulations has been frozen in limbo for decades, and pending the issuance of final Regulations, these exceptions remain frustratingly unclear. Frankly, however, that frustration might have remained the bane of a few law school academics and fewer tax practitioners, having only modest significance for election lawyers and their clients, if not for the Supreme Court's January 2010 decision in Citizens United v. Federal Election Commission.30

Prior to Citizens United, all corporations (for-profit and nonprofit) and labor organizations were prohibited under the FECA from making independent political expenditures (except for the limited “MCFL” exception for section 501(c)(4) nonprofit corporations that do not receive corporate, union, or business income31). The Court's decision lifted that prohibition. Since it was not mentioned in the oral argument or in the Court's opinion, it is probably safe to assume that the effect of Citizens United on the interpretation of the Reserved Regulations was not considered by the Justices. That effect was arguably enormous. Pre-Citizens United, a well-advised Section 501(c) organization (other than one within the narrow MCFL exception) would never make an independent federal political expenditure, since the FECA prohibited it from doing so; campaign finance law counsel therefore did not have to consider the tax consequences to their Section 501(c) clients of expenditures those clients were not permitted to make in the first place. After Citizens United, however, those same Section 501(c) clients are at liberty to make such expenditures without limit, and the only fly in the ointment is a federal tax statute, Section 527(f), that many such organizations may never have previously considered. With the lifting of the independent expenditure prohibition, “allowable under [the FECA]” took on a whole new meaning, as did “or under similar State statute,”32 leaving only the Section 527(f) tax—if it applies—to rein in such activities. The Reserved Regulations, and how to make practical sense of them in the post-Citizens United world of campaign finance, are the focus of this article.

Part II outlines the relevant legal authority underpinning the Reserved Regulations and identifies serious obstacles to their interpretation and practical application. Part III suggests a new interpretative framework for deploying the Reserved Regulations that takes into account the more permissive scope of election-related activity newly sanctioned for corporations and labor unions by Citizens United. Part IV applies this proposed framework to three categories of expenditures by hypothetical Section 501(c) organizations working on both federal and state elections. These examples highlight the difficulty of a literal interpretation of the Reserved Regulations and underscore the value of the interpretive methodology we propose. We look forward to Treasury's development of substantive Regulations to implement the Section 527(f) tax in a manner consistent with and cognizant of the revised campaign finance disclosure laws. In addition to assisting practitioners counseling clients under the current Reserved Regulations regime, we hope the framework presented here, as well as the demonstration of its application to hypothetical organizations and their expenditures, may prove useful in that endeavor, if and when it occurs.

II. Background of the Reserved Regulations

A. The Reserved Regulations: What we know and what we do not know

We know that the current Regulations indicate that, in determining which of their expenditures are nontaxable indirect expenses, Section 501(c) organizations may rely on the definition of “indirect expenses” applicable to Section 527 organizations as a starting point.33 Using this definition, Section 501(c) organizations may count as nontaxable indirect expenses any expenses “necessary to support the directly related activities of [a] political organization,” and activities that “must be engaged in to allow [a] political organization to carry out the activity of influencing or attempting to influence the selection process,” and specifically, overhead, recordkeeping, and fundraising expenses of a Section 527 political organization.34 The only limitation on the use of this definition of “indirect expense” is a proviso that gives to the Reserved Regulations the authority to make exceptions to the exception. In the absence of the Reserved Regulations, the definition of “indirect expenses” borrowed from Section 527 appears to be the operative one for 501(c) organizations.

We also know that the Regulations permit a Section 501(c) organization to carve out from Section 527(f) taxation expenditures that “are otherwise allowable under [FECA] or similar State statute,” and that there is a similar proviso granting authority to the Reserved Regulations to limit this exception.35

The bottom line is that without substantive Regulations to replace the Reserved Regulations, we do not know to what extent the current Regulations are meant to limit the application of the “indirect expenses” exception, or how best to interpret the “allowable under [the FECA] or similar State statute” exception.

B. Existing regulatory authority interpreting the Reserved Regulations

Despite the lack of positive authority defining the scope of the Reserved Regulations exceptions, taxpayers and the IRS have operated under certain provisional principles since section 1.527-6 of the Regulations was promulgated in 1980, most of which follow from a few statements made by the Treasury and the IRS. This section summarizes the limited existing regulatory authority. The first subpart summarizes guidance applicable to both Reserved Regulations; the second subpart focuses on authority specific to the indirect expenses exception; and the third subpart addresses the “allowable under the FECA or similar State statute” exception.

1. Regarding the Reserved Regulations generally

There is very little existing guidance regarding the interpretation of the Reserved Regulations. The preamble to the final Regulations under Section 527, issued December 30, 1980 (Preamble),36 is the only available precedential authority. The Preamble sets forth the position of commentators on the proposed Regulations and the Treasury's provisional acquiescence to certain of those comments. As described in the Preamble, commentators suggested that certain types of indirect expenditures, which would, if made by a Section 527 organization, be 527-type expenses not taxable to such political organization, should not be characterized as taxable expenses under Section 527(f) if made by a Section 501(c) organization. Commentators also recommended that certain activities of Section 501(c) organizations that are not considered “political activities” under federal or state election laws should not be treated as taxable 527-type activity to such Section 501(c) organizations. In particular, commentators urged that expenditures to fund the following three activities should not be considered “exempt function” expenditures when made by a Section 501(c) organization:

In response to these comments, the Treasury agreed to reserve Regulations “pending resolution of the relationship between Section 527 and the FECA and similar State statutes.” Importantly, the Preamble states that when amendments to the Reserved Regulations are adopted and promulgated, they “will apply on a prospective basis if the commentators' position is rejected and taxpayers are thereby adversely affected.” The Preamble constitutes the only guidance issued by the Treasury with respect to the Reserved Regulations.

There are two resources intended to be internal to the IRS that also address the Reserved Regulations. From time to time, the IRS has published continuing professional education (CPE) texts for Exempt Organizations Division personnel, although it recently discontinued that practice. In 2002, the most recent year in which the IRS published a CPE text on election year issues, the authors included in that text a section that posed the following question:

Are [a Section] 501(c) organization's expenditures allowed by the FECA (2 U.S.C. §441b(b)(2)(C)) and its indirect expenses relating to political campaign activity considered exempt function expenditures?

The CPE text has a lengthy answer to the question, acknowledging that, “[b]oth issues are unresolved.”39 The answer first addresses expenditures allowed by the FECA:

[The FECA] specifically permits labor unions and trade associations to spend money for (1) internal communications with members, stockholders, and their families (but not to the general public) that might involve support of particular candidates; (2) the conduct of nonpartisan registration and get-out-the-vote campaigns aimed at their members, stockholders, and families; and (3) the establishment, administration, and solicitation of contributions to separate segregated funds to be used for political purposes. As a result, when the [R]egulations under [Section] 527 were published in proposed form, several commentators suggested that these expenditures, which are made routinely by some [Section] 501(c) organizations and are regarded as appropriate under the FECA for such organizations, should be treated differently from identical expenditures made by political organizations. In other words, the commentators suggested that such expenditures continue to be treated as “exempt function” activities for political organizations (including separate segregated funds of [Section] 501(c) organizations) but not for [Section] 501(c) organizations. No final determination of the issue was made; therefore, the treatment of expenditures allowed by the FECA is reserved in the final regulations. [Regulations section] 1.527-6(b)(3).40

The CPE text then turns to indirect expenses:

[I]ndirect expenses are defined in [Regulations section] 1.527-2(c)(2) as expenses, such as overhead and record keeping, that are necessary to support directly related exempt function activities. . . . [A Section] 501(c) organization may pay for the indirect expenses of [a Section] 527 organization without incurring tax under [Section] 527(f). However, to take advantage of this situation, [a Section] 501(c) organization must actually pay the indirect expenses.41

This CPE text provides a liberal reading of the Reserved Regulations: It suggests that “allowable” means “permitted,” and relies on the prospective nature of any final Regulations to render irrelevant the difference, if any, between its permissive interpretation and any more narrow construction that may be required under the final Regulations. We think this reading, while supportable by nonprecedential authority, ignores the practical difficulties with equating “allowable” and “permitted,” discussed in more detail below.

Perhaps more importantly, this CPE text predates the U.S. Supreme Court's January 2010 decision in Citizens United v. Federal Election Commission.42 In light of Citizens United, a more permissive interpretation of “allowable” could open the door for Regulations potentially sanctioning substantial tax-free express advocacy expenditures for Section 501(c) organizations.43 Since the 2002 CPE text has not been revisited since Citizens United, it is difficult to construe the two together with any certainty. We also note that CPE texts, although written by IRS personnel who are expert in the subject matter covered and intended to guide IRS staff interpretations of applicable law, are not precedential authority and may not be relied upon by a taxpayer in an audit or in any judicial proceeding.

The other internal source is the Internal Revenue Manual (IRM). The IRM is the IRS's guidebook for its examining agents. It provides both a digest of the relevant law and guidelines for agents pursuing audits and undertaking other review functions. Although, like the CPE text, it is not precedential authority, the IRM provides a window on the IRS's positions with respect to application of federal tax law. IRM Section 7.27.4.2 provides in whole:

Indirect or FEC Allowed Expenses Regulations sections 1.527-6(b)(2) and (3) have been reserved with regard to the treatment of certain indirect expenses and expenditures by a corporation with a connected [political organization] that are permissible under [the FECA]. Until final regulations are issued on the treatment of these expenditures, these items are not to be treated as exempt function expenditures when made by [Section] 501(c) organizations. Final regulations, if adverse, will be applied prospectively.44

Although the IRM does not mention the “or other similar State statute” provision of Regulations sections 1.527-6(b)(1) and (3), there is no reason to believe that the IRM's silence on this point affects the IRS's view of the application of that regulatory provision to current Section 501(c) organizations.

2. Indirect expenditures exception: Additional guidance and interpretation

A series of private letter rulings in the early- to mid-1980s reflected IRS difficulties with the meaning of “indirect expenses” under Section 527(f) and how to apply the Reserved Regulations to Section 501(c) organizations. Ten years later, in another private letter ruling, the IRS appeared to have clarified its analysis, but some ambiguities remain. Private letter rulings are issued to specific taxpayers and are only precedential with respect to those taxpayers, but they are made available to the public in redacted form and so provide useful insights into current IRS thinking on the issues addressed. The relevant rulings are summarized below.

A 1983 private letter ruling determined that the provision by a Section 501(c)(8) police beneficiary society of its facilities, including office space, meeting halls, and related facilities, to candidates for public office or to an SSF established by the Section 501(c)(8) organization, was not subject to Section 527(f) tax because the provision of such facilities was an indirect expense to the Section 501(c)(8) organization. In concluding that either candidates or the fund could use the facilities without subjecting the Section 501(c)(8) society to Section 527(f) tax, the ruling does not appear to draw a line between providing such facilities to candidates versus to the affiliated political organization, even though the Section 501(c)(8) society, in its initial ruling request, offered to require the SSF to pay rent to the Section 501(c)(8) for any use by candidates of the Section 501(c)(8) society's facilities. The ruling also does not mention whether state or federal election law applied to the SSF's proposed activities, and does not cite to Regulations section 1.527-6(b). However, it twice mentions that the rulings regarding the use of facilities by candidates and by the SSF were “issued with the understanding that final regulations dealing with ‘indirect expenses' of an organization exempt under Section 501(c) for an ‘exempt function’ will provide that such expenses will not be taxable as ‘exempt function’ expenditures.”45 While we agree that use by the connected Section 527 organization of the society's facilities for administrative or fundraising endeavors could be a nontaxable indirect expense to the Section 501(c)(8) organization, there is nothing in the ruling that limits this “use of facilities” to activities necessary to support the directly related activities of a political organization, or other purposes described in Regulations section 1.527-2(c)(2). The Regulations, the Preamble, and later rulings appear to require such a limitation, so we are wary of reading “indirect expenses” as broadly as this early ruling.

A year later, the IRS pivoted to interpret the Preamble and the Reserved Regulations very narrowly, not shedding much light on the meaning of “indirect,” but nonetheless suggesting that only indirect expenses (and not even the direct expenses explicitly named in the Preamble) could be nontaxable under the exceptions provided by the Reserved Regulations. In Private Letter Ruling 8502003, a Section 501(c)(5) labor union made direct contributions to candidates for state political office. State law did not require such contributions to come from SSFs and did not impose any limit on the amount of contributions that could be made for political purposes. The union made the contributions from its general checking account (the only account used for receiving and disbursing member dues for political contributions), from which it also made expenditures not connected to candidate campaign intervention. It used fund accounting and tracked candidate campaign intervention expenditures separately from other expenditures. The ruling does not indicate whether a state statute similar to the FECA affirmatively permitted the direct contributions, or if instead there existed no state law on point. The union argued that because the contributions were only made for state candidates, the Reserved Regulations should apply, but could only be applied prospectively after promulgation. The IRS disagreed, and stated:

Although Congress was aware that certain problems existed in defining the relationships between State Statutes and Section 527[,] the tax was clearly imposed upon generally all direct expenditures for political purposes whether on the Federal or local level. Therefore, we can see no reason to conclude that anything other than indirect political expenditures would be covered by [Regulations] section 1.527-6[(b)](2) or (3).46

The problem with this statement is that it goes too far, ignoring the fact that communications with the Section 501(c) organization's members—a direct expense of the Section 501(c) organization—are explicitly included in the list of expenditures blessed by the Preamble as not subject to the Section 527(f) tax unless and until the Reserved Regulations are amended to the contrary. While we agree that the direct contributions by the union in this ruling were taxable under Section 527(f) if there was no state statute akin to the FECA that explicitly “allowed” (as we define that term below) such contributions by the union, we believe that, to reach the ruling's conclusion, the IRS should have made (but failed to make) an inquiry into applicable state law, and the expenditures should have been nontaxable if there was such a statute on point that “allowed” the union to make such contributions.

Not long after that September 1984 ruling, the IRS issued another ruling concerning a Section 501(c)(6) trade association that made a contribution to a Section 527 organization that supported the election of both national and state candidates for political office.47 The political organization had two accounts: one for “hard money,” which was used for the support of candidates and came only from individual contributors, and one for “soft money,” which funded the political organization's “necessary administrative expenses, telephone, postage, stationery, and other expenses” and consisted of money given by associations.48 The trade association contributed money to the soft money account of the political organization, and asked the IRS: (1) whether the contribution was a “‘directly related’ expenditure for an ‘exempt function’”; and (2) whether the contribution met the definition of “indirect expense” under Regulations section 1.527-6(b)(2), “which is now reserved and therefore, for administrative purposes, is not subject to tax at this time.”49 The IRS acknowledged that a contribution made by a Section 501(c) organization to a political organization “but only to be used by the political organization for necessary administrative expenses of the organization, rather than the direct support of the candidate, cannot be considered a ‘direct expense’ of an exempt function.”50 However, because Section 1.527-6(b)(2) of the Regulations had been reserved, the IRS refused to answer the indirect expense question, saying that it was “unable to determine whether the contribution represents an amount to be used by [the political organization] for an exempt function. . . . If, when final regulations are published, the subject organization is adversely affected thereby, the regulations will apply on a prospective basis only.”51 The IRS's reticence is confusing here, because the soft expenses seem completely consistent with the meaning of “indirect expenses” suggested by the Preamble and Regulations, and the IRS could have gotten to the same result through straightforward reliance on existing Regulations.

Ten years later, another private letter ruling took a more reasonable approach to the meaning of “indirect.” In Private Letter Ruling 9433001, a Section 501(c)(6) trade association contributed funds to an affiliated Section 527 organization, calculating the contribution at $1 per member. The ruling states that the trade association “intended the money to be used to pay administrative expenses of the political organization.”52 Although the IRS ultimately determined that the trade association had made a taxable “exempt function” expenditure because it did not take any steps to ensure that amounts it paid to a political organization would be used only for administrative expenses, the IRS noted:

[Regulations] section 1.527-6(b)(1)(i) . . . provides that indirect expenses paid by a Section 501(c) organization are only considered exempt function expenditures to the extent provided in [Regulations] section 1.527-6(b)(2). Since that section has not yet been promulgated and will only be applied prospectively, we are unable to determine the extent to which indirect expenses paid by the Section 501(c) organization will be considered exempt function expenditures. Therefore, if [the Section 501(c)(6) trade association] had directly paid the indirect administrative expenses of the political organization, it would not be liable for the tax under Section 527(f)(1). . . . 53

This approach, if it had been applied a decade earlier in Private Letter Ruling 8516001,54 may have resulted in no taxation to the trade association in that ruling. Note that this 1994 ruling emphasizes Regulations section 1.527-6(b)(1)(ii), which states that although a Section 501(c) organization will not be directly liable for amounts transferred to an individual or organization that are ultimately used for an “exempt function,” the organization is “required to take reasonable steps to ensure that the transferee does not use such amounts for an exempt function.” It appears, therefore, that had the trade association in the 1994 ruling transferred the funds to the Section 527 political organization with enforceable restrictions on the use of the funds for only administrative purposes, the IRS might not have assessed tax.

Beyond these rulings and the Regulations themselves, there is limited guidance regarding the definition of indirect expenses of a Section 501(c) organization. Nonetheless, we think it is relatively safe to assume that expenditures by a Section 501(c) organization that are within the definition of “indirect expenses” under Regulations section 1.527-2(c)(2) (except for being made by a Section 501(c) organization and not a Section 527 political organization) will not be subject to Section 527(f) tax as long as the Section 501(c) organization itself is paying the indirect expenditure for the benefit of a political organization. As a policy matter, we believe the indirect expenditure exception should not be read too broadly, risking the rule-swallowing referred to earlier, but we believe the IRS should have little choice but to accept a fairly literal reading of the Section 1.527-2(c)(2) definition until the Reserved Regulations are amended to narrow its scope. If an expense of a Section 501(c) organization on behalf of a political organization is “necessary to support the directly related activities of the political organization,” i.e., is necessary to support activities of the Section 527 organization that “must be engaged in to allow the political organization to carry out the activity of influencing or attempting to influence the selection process,” such expenditures by the Section 501(c) organization on behalf of the political organization should be nontaxable “indirect expenses” within the meaning of the Reserved Regulations.55

3. “Allowable under the FECA or similar state statute” exception

As discussed above, Regulations Section 1.527-6(b)(1)(i) provides that expenses “allowable under the FECA or similar state statute” are excepted from the Section 527(f) tax. Beyond the Preamble and the IRM, there is no Treasury or IRS guidance expanding upon the meaning of “allowable under [the FECA] or similar State statute,” so we are left with the plain meaning of the phrase and logical reasoning.56 Part III presents an interpretative framework that is consistent with the authorities described above and also provides reasonable defensible outcomes in light of the post-Citizens United expansion of the permitted electoral activities of corporations and labor unions.

III. A New Interpretation of “Allowable Under [The FECA] or Similar State Statute”

The “allowable under [the FECA] or similar State statute” exception hinges upon the meanings of “allowable” and “similar” in the context of the Reserved Regulations. The following sections focus upon possible meanings of these two simple words and the consequences of adopting one meaning over another, which in turn facilitates our construction of the interpretive framework outlined in Parts III.C and IV.

A. “Allowable”

There is no Treasury or IRS guidance regarding the proper interpretation of the word “allowable” in the Reserved Regulations; unfortunately, using the plain dictionary meaning of the term, i.e., “not prohibited,” would drive an interpretation of the Reserved Regulations that is both improbably permissive in scope (especially when applied to many states' campaign finance disclosure laws, examples of which are discussed below) and inconsistent with the policy rationales underlying Section 527(f), at least as we understand them. In our view, part of Congress' intent with Section 527(f) was to “piggy back” onto existing FEC and state campaign finance disclosure law in determining what campaign-related activity should and should not be burdened by regulation. By relying primarily on election laws for this purpose, the IRS avoids imposing two separate, potentially inconsistent sets of Regulations on the same activity. In some states (like California), political activity is monitored and subject to disclosure, but rarely prohibited; such a reporting regime does not suggest that reportable activities are not political, only that they are insulated from penalty or limit if properly reported.

We therefore interpret “allowable” to mean that applicable election law permits the Section 501(c) organization in question57 to make the expenditure not only without prohibition, but also without burden, i.e., without disclosure. In other words, to the extent that the organization is permitted to engage in the activity or expenditure without reporting it, that amount of activity and expenditure is “allowable” under Regulations section 1.527-6(b)(3).58

Likewise, if the expenditure relates to an election at the state or local level, we interpret “allowable under…similar State statute” to mean that the applicable statute permits the expenditure without requiring the organization to report the specific expenditure. To the extent that the organization is required to report an expenditure (which could be required from the first dollar spent or only in excess of a prescribed limit for a particular type of expenditure), our framework would treat the reported amounts as not “allowable” within the meaning of the Reserved Regulations.

In the event that the expenditure relates to a non-federal election in a state without any applicable statute governing campaign finance, there is no “similar State statute,” and therefore the Regulations section 1.527-6(b)(3) exception could not apply. We acknowledge that this outcome is somewhat ironic: It means that the lack of any state regulation of an electoral activity whatsoever will result in taxation of more expenditures for that activity. Since it has not to our knowledge been tested in any jurisdiction, perhaps one could argue for the reverse outcome (i.e., not taxing such expenditures) by reasoning that the intent of the Reserved Regulations is not to require affirmative permission by the state law but rather not to contradict such permission if it exists; exploring that argument is beyond the scope of this article and the framework it proposes.

We recognize that our interpretation of “allowable” substantially alters application of the Reserved Regulations when compared to other possible interpretations of the term. Nonetheless, we conclude that under current circumstances, our interpretation is the most reasonable given the apparent legislative intent underlying Section 527(f), the newly sanctioned freedom of Section 501(c) corporations and labor unions to engage in unlimited 527-type independent expenditures, and the diversity of election laws among the states that regulate political activity. Plausible alternative meanings produce irrational results. For example, a simple interpretation of “allowable” as “not prohibited” is reasonable on its face, but such an interpretation would render exempt from Section 527(f) tax almost all expenditures supporting or opposing non-federal candidates in states (like California) that have substantial campaign finance disclosure requirements but minimal prohibitions. On the other hand, it would be unreasonably narrow to define “allowable” to mean, categorically, “not subject to reporting,” since many categories of expenditure are subject to reporting, but only if in excess of an established threshold. For example, some campaign finance disclosure regulators have established certain de minimis levels under which expenditures are beneath their notice; if those levels are exceeded, reporting is required. In describing such a category of expenditure, one would have to say that the category is subject to reporting regulations, even if the reporting obligation does not attach from dollar one. If “allowable” meant “an expense in a category of expenditure not subject to reporting,” then even those de minimis expenditures would nonetheless be taxable under Section 527(f).

We believe the requirement to disclose an expenditure is the manner in which campaign finance regulators (both federal and state) generally indicate what types and amounts of expenditures are considered by them to be political activity properly regulated by applicable election laws; therefore it is appropriate, and consistent with the Preamble, to impose tax on a Section 501(c) organization under Section 527(f) if it makes such expenditures.

In the absence of congressional, Treasury, or IRS guidance, we cannot assume without caveat that our interpretation of the term “allowable,” which is admittedly somewhat outcome-driven, is correct. Throughout the remainder of the article, we will use the capitalized term “Allowable” to underscore that our use of this term carries our defined meaning, and that it is not a definition explicitly dictated by statute or regulation. This constructed definition is summarized in the last column of Table 1 (“Never reportable or only reportable above reporting threshold (and not prohibited)”). For comparison, the first two columns of Table 1 include two of the other possible interpretations and the effect of each on the application of Regulations section 1.527-6(b)(3). As mentioned above, depending on jurisdiction, expenses may be categorically permitted or impermissible under campaign finance disclosure laws, and may require reporting or not require reporting. In some categories of expenditure, the existence of a prohibition or reporting requirement may depend on the amount of the expenditure. For each possible combination of “permitted/not permitted” and “reporting required/reporting not required,” the table indicates whether that type of expense would be allowable (i.e., tax-free) or not, depending upon the interpretation chosen. The purpose of the table is to contrast the results of the first two interpretations with the more balanced outcome under the interpretation advocated here.

Y=Allowable not taxed N=not Allowable; taxed Y/N=Allowable up to reporting threshold; not Allowable above threshold.

As noted earlier, there is additional uncertainty since the Supreme Court's January 2010 decision in Citizens United v. Federal Election Commission59 struck down the prohibition on expenditures by corporations on public communications expressing support or opposition to political candidates. Arguably, any such independent expenditure in support of or in opposition to a federal candidate that is no longer prohibited (i.e., it is permitted) under federal law, would be nontaxable.60 Using our interpretation of Allowable, however, any such expenditure that must be reported to the FEC would not be Allowable, even if permitted.

B. “Similar”

For the reasons we describe below, we interpret “similar State statute” to mean (1) similar to the FECA in purpose and scope and (2) applicable to the Section 501(c) organization making the expenditure. In other words, in the case of any given expenditure, we do not believe that it is necessary for the relevant specific provisions of the federal and state statutes to be substantially or even materially similar, or in fact for parallel provisions to exist with respect to that category of expenditure. Since no individual 527-type expenditure will be governed simultaneously by both federal and state election laws, we do not believe that it is necessary to the meaning of “similar” in Regulations section 1.527-6(b)(3) for a given expenditure to be blessed by both statutes, as long as it is Allowable under the statute that applies to that expenditure, by the organization making that expenditure, at the time the expenditure is made.

There are other ways in which one could interpret “similar State statute” beyond the macro approach that we propose here, ranging from slightly less macroscopic to very precise. For example, “similar” could mean that, for a given expenditure, both the federal and state statutes include provisions concerning that category of expenditure (i.e., both have provisions regarding expenses of communication with members), regardless of what those provisions actually say about the expenditure and to whom those provisions apply. Alternatively, “similar” could mean that both the FECA's and the state statute's provisions regarding that category of expenditure are inherently similar in any or all of the following, increasingly specific ways: in their general statutory purposes; in the organizations to which those provisions apply; in their functional impact on outcomes; in the definitions, conditions, numeric thresholds, and other terms the two statutes apply to organizations making the expenditures; or in their actual phrasing.61

We acknowledge that the interpretation we have chosen, which is the broadest possible meaning of “similar,” may be more permissive than any final Regulations will be, if and when they are promulgated. Nonetheless, we conclude that at present, it is the most fitting interpretation, based upon our reading of the Regulations and related authority, for the following reasons:

1. Any interpretation of “similar State statute” that requires the IRS not only to interpret the internal mechanics of a state statute but also to compare that statute to federal election law, is inherently inadministrable. 2. An interpretation that is neither as broad as possible nor as narrow as possible is arguably unconstitutionally vague, because no taxpayer is capable of knowing where along the spectrum of interpretation the IRS's position will fall without more Treasury or IRS guidance than currently exists. 3. A more narrow interpretation puts a burden on the Section 501(c) organization that is inconsistent with the policy rationale behind Section 527(f), as described in Part I above. If following the election laws did not give taxpayers a roadmap for compliance with federal tax laws because the IRS imposed a more narrow interpretation of “similar,” a Section 501(c) organization making a campaign-related expenditure would be compelled to comply with both election law (which makes sense, because election law is designed to regulate political activity) and tax law, even if tax law was inconsistent with election law (which does not make sense). 4. There could be legitimate policy reasons why a state's election law might permit expenditures that under the FECA are not permitted or are not addressed. For example, if a labor union in State X was allowed under State X election law to buy 10 hours per week of air time on state-subsidized radio or television stations to support or oppose candidates in state elections, but under the FECA unions cannot purchase radio or television air time from a federally subsidized radio or television station for use in a federal election, then under a narrow reading of Regulations section 1.527-6(b)(3), a union's purchase of air time for use in a state election would be taxable under Section 527(f)—even though State X clearly wishes to permit (and may have reasons for encouraging) the use of State X-sponsored radio and television stations in state elections. Under our broader reading of “similar State statute,” the purchase of up to 10 hours of state-sponsored radio or television air time for communications about a State X election would be nontaxable (assuming such use were also Allowable, i.e., not subject to a reporting requirement under State X's statute). 5. The fact that the final Regulations under Section 1.527-6(b), when promulgated, will only be applied prospectively, makes it more likely that the broad interpretation of “similar” is the currently appropriate meaning of the term. The Preamble, letter rulings, and IRM acknowledge that final Regulations could adversely affect taxpayers, which suggests that future Regulations might be narrower than the currently applicable rules, which in turn implies that the currently applicable rule is at least no narrower than will be the future Regulations.

C. Applying the Reserved Regulations under the proposed framework

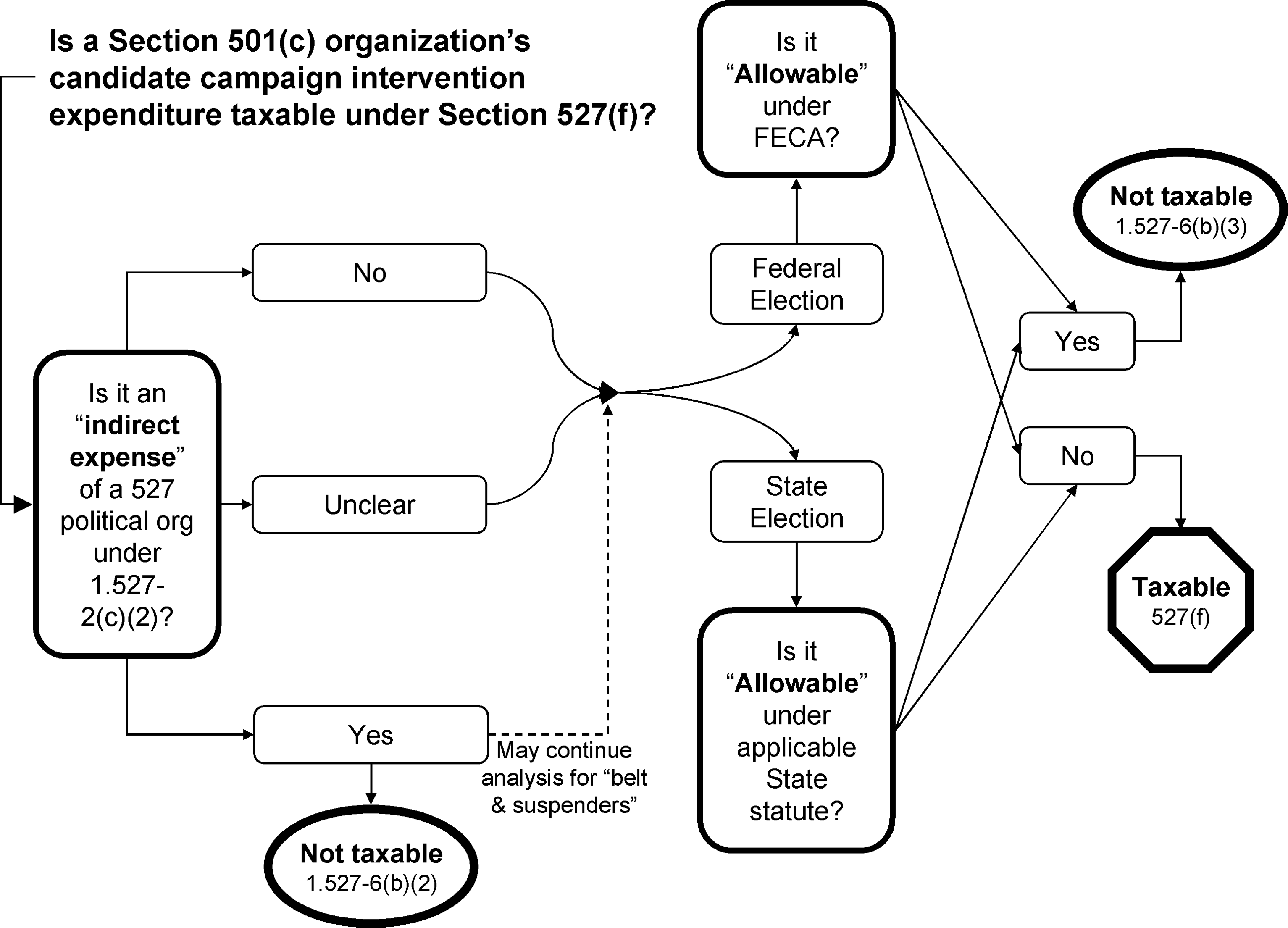

In order to be useful to practitioners and taxpayers, any interpretation of the Reserved Regulations must be capable of being applied to actual organizational expenditures. Our analysis of the Reserved Regulations, and our proposed method of applying this interpretation, is summed up in the decision chart in Figure 1.

Application of the Reserved Regulations under the proposed framework.

The first question is to determine whether the expenditure meets the definition of “indirect expense” in Regulations section 1.527-2(c)(2) (and by extension, Regulations sections 1.527-6(b)(1) and (2)), which we discussed in Part II.B, above. Since we propose reading that definition narrowly, an expenditure will only be an indirect expense if the expenditure is (1) necessary to support the directly related 527-type activities of a Section 527 political organization and (2) is engaged in to allow such political organization to carry out its 527-type activities. For example, expenses related to a political organization's overhead and recordkeeping are indirect expenses because they allow a political organization to be established and to engage in 527-type activities,62 and expenses incurred in soliciting contributions to a political organization are necessary to support the political organization's 527-type activities.63 The 1984 ruling discussed in Part II.B.2 above specifically mentions telephone, postage, and stationery as examples of necessary administrative expenses.64 Only those expenses that are paid by the Section 501(c) organization itself may be deemed indirect expenses and therefore excluded from the Section 527(f) tax (and possibly those expenses paid by the Section 527 using funds earmarked and restricted by the Section 501(c) only for the indirect expense).

If an expense is clearly an indirect expense, one may end the analysis here; the expenditure is not taxable under Section 527(f).65 If it is not clear whether the expense is an indirect expense, or if it is clearly a directly related expense, the analysis continues along one of two tracks, depending upon whether federal election law or state election law applies to the expenditure. The second question, equally applicable to both tracks, is whether the expenditure is Allowable under the relevant federal or state statute.66 If it is Allowable, it is not taxable. If it is not Allowable then (unless it qualified as an indirect expense in answer to the first question above), it is taxable under Section 527(f).

In the remainder of this article, we analyze three categories of possible Section 501(c) expenditures and use the suggested framework to explain whether (and if so, why), such expenditures should be excepted from the Section 527(f) tax if made by a Section 501(c) organization.

IV. Applying the Proposed Framework to Selected Expenditures

In this Part, we walk through the decision process summarized in Figure 1 for three categories of expenditures, to illustrate our proposed process for determining what 527-type expenditures of a Section 501(c) organization may be excluded from the section 527(f) tax. In addition, to compare how the proposed framework would play out if applied to federal versus state expenditures, we have provided parallel analyses of each. We have used California's Political Reform Act (PRA) as the “similar State statute” in these illustrative scenarios, because California's election laws provide a robust reporting framework for election-related activity but prohibit very little. The example of California thus highlights the tensions inherent in the definition of Allowable that we have suggested.67

A. Employee time of the Section 501(c) organization

By “employee time,” we mean (1) compensation paid to an employee while he or she is on the job at the Section 501(c) organization but assigned to work on candidate campaign intervention for a Section 527 organization (Compensation Cost), (2) the opportunity cost to the Section 501(c) organization when an employee uses his or her excess capacity to personally work on activities for a Section 527 organization while on the clock for the Section 501(c) organization (Opportunity Cost), or (3) both. All three possibilities will be considered below.

1. Is the expenditure an “indirect expense” within the meaning of Regulations section 1.527-2(c)(2)?

To answer this question, one must look at the underlying employee activity and the relationship of the Section 501(c) organization to that activity. If the employee is being compensated directly68 by a Section 501(c) organization for the purpose of providing services to or on behalf of a Section 527 organization that (1) are necessary to support the directly related exempt function activities of the political organization and (2) must be engaged in to allow such political organization to carry out its exempt function activities (e.g., completing required disclosure forms for the political organization), then the Compensation Cost expended for such employee by the Section 501(c) organization for such purposes should be an indirect expense. In that case, the outcome—no Section 527(f) tax—is clear, and our analysis is complete. If instead the nature of the employee's services to the political organization are not so clear, we must continue on to the “Allowable” test.

If the Section 501(c) organization does not require its compensated employee to engage in the 527-type activities but rather permits its employee to engage in his or her own volunteer activities while ostensibly “on the clock” for the Section 501(c) organization, without making up such work time, and the Section 501(c) organization does not restrict the employee's on-the-clock volunteer activities to activities described in Regulations section 1.527-2(c)(2) (i.e., services necessary for the administration, establishment, or fundraising activities of the political organization), that Opportunity Cost is arguably (1) an expenditure of the Section 501(c) organization and (2) not an indirect expense. In that case, we would advise continuing the analysis.

2. Is the expenditure Allowable under the applicable election law statute?

Assuming that the employee is not engaged exclusively in necessary administrative activities on behalf of the political organization, we move on to determine whether the expenditure would be Allowable (1) under the FECA and regulations promulgated under the FECA (FEC Regs), if the FECA applies to the expenditure, or (2) under the California PRA and regulations promulgated by the California Fair Political Practices Commission (FPPC; such regulations, “FPPC Regs”), if state law applies.

a. Federal Election Campaign Act

To summarize the relevant provisions of the FECA, a “contribution” is defined in the FECA to include, “(i) any gift, subscription, loan, advance, or deposit of money or anything of value made by any person for the purpose of influencing any election for federal office; or (ii) the payment by any person of compensation for the personal services of another person which are rendered to a political committee without charge for any purpose.”69 The FEC Regs further provide that “[t]he payment by any person of compensation for the personal services of another person if those services are rendered without charge to a political committee for any purpose, except for legal and accounting services…is a contribution.”70 “Expenditure” is defined to include, “(i) any purchase, payment, distribution, loan, advance, deposit, or gift of money or anything of value, made by any person for the purposes of influencing any election for federal office; and (ii) a written, contract, promise, or agreement to make an expenditure.”71

A common theme in the FECA and the FEC Regs is that compensation will not be a contribution as long as the employer is not in any way paying for or subsidizing an employee's personal political activity. The FEC Regs also explicitly state that “the value of services provided without compensation by any individual who volunteers on behalf of a candidate or political committee is not a contribution.”72 More specifically, compensation paid to an employee who provides services to a political organization will not be considered a contribution if any of the following are accurate: (1) the employee is paid on an hourly or salaried basis, is expected to work a certain number of hours per specified period, such employee engages in political activity during a regular work period, and the employee makes up the time spent on political activity within a reasonable period; (2) the employee is paid on a commission or piecework basis, or for work actually performed, engages in political activity during normal working hours, “the employee's time is considered his or her own to use as he or she sees fit,” and he or she is paid only for (non-political intervention) work actually performed; or (3) the employee uses his or her bona fide paid time off (i.e., “vacation or earned leave time”) to engage in political activity, regardless of how the employee is compensated.73

In sum, Compensation Cost paid for anything other than indirect activities are not Allowable under the FECA, and Opportunity Cost for similar purposes are not Allowable unless one of the three rules summarized immediately above are followed (i.e., that the Opportunity Cost must be effectively nil or almost nil).

b. California's Political Reform Act

Turning to our state law example, California's PRA defines “contribution” to include “a payment, a forgiveness of a loan, a payment of a loan by a third party, or an enforceable promise to make a payment except to the extent that full and adequate consideration is received, unless it is clear from the surrounding circumstances that it is not made for political purposes.”74 The statute includes many specific inclusions and exclusions. “Expenditure” is defined in exactly the same way as “contribution,” but with different clarifications and exclusions.75 Under the PRA and the FPPC Regs, contributions and expenditures by corporations and labor unions are not categorically prohibited, but are instead subject to reporting requirements. Under our proposed framework, to the extent an expenditure must be reported, it is not Allowable.

The FPPC Regs permit an employer to exclude from the meaning of “contribution” the compensation (“the payment of salary, reimbursement for personal expenses, or other compensation by an employer”) paid to an employee for the explicit purpose of conducting political activity, as long as the employee spends no more than 10% of his or her paid time on such activity in any month.76 Compensation paid to an employee who spends more than 10% of his or her compensated time in any one month rendering services for political persons is a contribution or expenditure. The amount of the contribution or expenditure reportable under the FPPC Regs is “the pro-rata portion of the gross salary, reimbursement for personal expenses or compensation attributable to the time spent on political activity.”77 Note that this exception to the definitions of contribution and expenditure is reckoned on an employee-by-employee basis, and is not determined by aggregating the time of multiple employees. The 10% rule is a safe harbor, but if compensation is paid to any employee who spends 11% of his or her time on political purpose services, all of that compensation is a contribution or expenditure, not only the compensation paid for time spent in excess of the 10% per month.

As discussed above, if a Section 501(c) organization were engaged in direct political activity relating to a federal election, any Compensation Cost paid to an employee to engage in such political activity would not be Allowable under the FECA, would not fall within the Regulations section 1.527-6(b)(3) exception, and so would be taxable. However, that same Compensation Cost paid to the same employee for similar political activity related to a California state election would not be treated as a contribution if the employee stayed at or below the 10% threshold, would thus be Allowable under a “similar State statute,” and therefore would not be taxable under Section 527(f).

This example illustrates perfectly the significance of defining “similar State statute” to mean a state's campaign finance disclosure code, and not only the narrow provision of that code pertinent to the expenditure. The FECA and the PRA both address use of employee time, but do not treat compensated employee time similarly. Whereas the FPPC Regs explicitly permit an organization to direct a small amount of its employees' time to political activity without treating that compensation as a political contribution, the FECA does not. The FECA focuses additional attention on the treatment of the individual volunteer political activity of employees and when that activity will be treated as a political contribution of the employer, even where the employer did not direct the employee's political activity. The PRA does not.

The contrast may cause some interesting outcomes for Section 501(c) organizations with both federal and (in this example, California) state election activity: Section 501(c) organizations should not expect to be able to direct a compensated employee to engage in federal campaign-related activities governed by the FECA without tax under Section 527(f) (unless another exception applies), but that same employee could do the same type of work on state elections (in California, at least) without causing the organization to incur Section 527(f) tax, as long as that employee's work was under the 10% threshold.

B. Member communications

1. Is the expenditure an “indirect expense” within the meaning of Regulations section 1.527-2(c)(2)?

Expenditures by a Section 501(c) organization for communicating with its members for campaign-related purposes, i.e., to express support of or opposition to a candidate, are not necessary for the establishment or administration of a political organization, and if the communications are engaged in directly, it is difficult to imagine this type of expenditure fitting into the definition of “indirect expense.”78 Therefore, we continue to the Allowable test.

2. Is the expenditure Allowable under the applicable election law statute?

Unlike “employee time,” which can result in out-of-pocket costs or opportunity costs, “communicating with members” is a relatively straightforward concept (as long as one knows what is meant by “communicating with” and “members”). A Section 501(c) organization wants to tell its members about the organization's position on a particular candidate or political party; the question is whether the cost of doing so is permitted under the applicable election law statute and therefore not taxable under Section 527(f), even though it is direct campaign-related activity. Both federal and California election laws have provisions permitting such communication; in fact, the two sets of provisions are fairly similar in scope, key terms, and functional impact. Recall, however, that the Preamble to the Reserved Regulations discussed back in Part II.B.1 also has something to say about member communications—which may turn our proposed framework on its ear where such activities are concerned.

a. Federal Election Campaign Act

The FECA carves out from the definition of “expenditure” amounts spent on communications with members, as follows: “any communication by any membership organization or corporation to its members, stockholders, or executive or administrative personnel, if such membership organization or corporation is not organized primarily for the purpose of influencing the nomination for election or election, of any individual to federal office.”79 The FECA also specifically provides that the term “contribution or expenditure” will not include amounts a labor organization expends to communicate with “its members and their families on any subject.”80

Although the FECA excludes from “expenditure” certain communications with members, such organizations are nonetheless required to report to the FEC if the costs incurred by such organizations (specifically including labor organizations) that are directly attributable to a communication expressly advocating the election or defeat of a clearly identified candidate (other than a communication primarily devoted to subjects other than the express advocacy of the election or defeat of a clearly identified candidate), exceed $2,000 for any election.81 Therefore, to the extent that the communication costs exceed $2,000, they will be reportable and hence not Allowable under our framework, even though they will not be categorized as “expenditures” or “contributions” under the FECA.

This outcome is clearly at odds with the Preamble's apparent acquiescence to commentators' inclusion of “communications with members about candidates for political office” as a category of activities “that are not considered to be political activities under federal or State election laws.”82 The FECA's requirement for reporting when the cost of political communications with members exceeds the $2,000 threshold is difficult to reconcile with the Preamble's rationale that such expenses are not considered political activities under federal law. The Preamble's assessment might make more sense if only expenditures for communications with members about political candidates under $2,000 are considered, but that is neither a practical nor intellectually satisfying conclusion, and there is no evidence that Treasury considered the $2,000 limit significant for purposes of the Section 527(f) tax.83

The FECA's reporting threshold illustrates the significance of our proffered interpretation of “allowable under the [FECA] or similar State statute” compared to a lenient “allowable”-means-“permitted” standard. If we use the dictionary definition of “allowable,” expenditures for member communications are allowable under the FECA, which would appear to be consistent with the Preamble. If instead we use our definition of Allowable, only member communication expenses under $2,000 are Allowable and therefore non-527(f)-taxable. As we have asserted, we believe that our proposed interpretive framework provides a workable synthesis of the principles and authority underlying the Reserved Regulations, but not one consistent with the Preamble where member communications expenditures for federal elections are concerned.

Therefore, despite the conclusion under our interpretation of the Reserved Regulations that such amounts (in excess of $2,000) would not be Allowable, we acknowledge that, because the Preamble explicitly and categorically includes member communications as one of the types of activities carved out from Section 527(f) tax by the Reserved Regulations, an organization could reasonably decide to spend more than $2,000 on federal electioneering communications with members without treating that excess as taxable under Section 527(f). It is difficult to imagine the IRS successfully taxing a Section 501(c) organization for such excess expenditures until a clear Regulation to that effect has been promulgated.84 Accordingly, until such Regulations are promulgated, we recognize that expenditures for member communications concerning federal elections, in excess of $2,000, are an exception to our framework.

b. California's Political Reform Act

The PRA exclusion for member communications is similar to that in the FECA, though the definitions of “member” and “family” are somewhat particular and not altogether intuitive.85 If a Section 501(c) organization expends funds to communicate about California state candidates or political parties with members and their families (as those terms are defined in the PRA), all such amounts should be Allowable; there is no threshold beyond which reporting is required.

C. Administrative expenses

1. Is the expenditure an “indirect expense” within the meaning of Regulations section 1.527-2(c)(2)?

Expenditures by a Section 501(c) organization that are restricted to use for the administrative expenses of a political organization are likely to be within the definition of “indirect expense” under Regulations section 1.527-2(c)(2) and therefore excluded from taxation under Regulations sections 1.527-6(b)(1) and (2). However, as the 1994 ruling86 makes clear, it is not enough for a Section 501(c) organization to transfer funds to a political organization with the hope or intent that the money be used for administrative expenses; the Section 501(c) organization must take reasonable steps to ensure that the funds are used only for such administrative expenses, and not for 527-type activities. The Section 501(c) organization could pay the political organization's administrative expenses directly (e.g., pay its phone bill directly to the telephone company), or it could make a contribution to the political organization that is enforceably restricted to administrative uses. Nonetheless, if there is any doubt regarding whether an administrative expenditure is an “indirect expense,” one should proceed to the Allowable test.

2. Is the expenditure Allowable under the applicable election law statute?

Both federal and California election laws have provisions permitting such expenditures; in this case, the two sets of provisions are similar in scope, key terms, and functional impact. In fact, the wordings of parts of the relevant definitions are actually identical.

a. Federal Election Campaign Act

The federal statute indicates that administrative costs of an SSF are not contributions or expenditures when made by a corporation or labor organization.87 The FEC Regs clarify that a corporation or labor organization “may use general treasury monies, including monies obtained in commercial transactions and dues monies or membership fees, for the establishment, administration, and solicitation of contributions to its separate segregated fund.”88 The FEC Regs provide a great deal more detail regarding the scope of this exception, which we will not attempt to summarize here, except to note that “establishment, administration, and solicitation costs” means “the cost of office space, phones, salaries, utilities, supplies, legal and accounting fees, fund-raising and other expenses incurred in setting up and running a separate segregated fund established by a corporation, labor organization, membership organization, cooperative, or corporation without capital stock.”89 Accordingly, such administrative expenses are also Allowable and therefore not taxable under Section 527(f) (even if they do not fall into the indirect expenses exception).

b. California's Political Reform Act

The PRA's definitions of “contribution” and “expenditure” do not explicitly address administrative expenses of a political organization. However, FPPC Regs section 18215(c)(16) excludes from the definition of “contribution,” “a payment by a sponsoring organization for the establishment and administration of a sponsored committee, provided such payments are reported.”90 “Sponsoring organization” can be any person91 except for a candidate or other individual, and “establishment and administration” means “the cost of office space, phones, salaries, utilities, supplies, legal and accounting fees, and other expenses incurred in setting up and running”92 a sponsored committee. Note that this language is identical to the parallel FEC Regs.

Therefore, it seems clear that any SSF (as that term is understood under federal tax law) of a Section 501(c) organization would fall within the meaning of “sponsored committee” under California's election laws. Accordingly FPPC Reg section 18215(c)(16) permits, without requiring reporting, any establishment or administrative expenses paid by the organization for the benefit of the SSF93; thus making them Allowable, and free from the Section 527(f) tax (again, even if the expenses did not fall into the indirect expenses exception).

Conclusion

Until the Reserved Regulations are clarified, the actual definition of “indirect expenses” for Section 501(c) organizations and the true scope of “allowable under [the FECA] or similar State statute” cannot be known. Over the past several years, exempt organizations practitioners have increased pressure on the Treasury to propose amendments to the Reserved Regulations and to provide definitive guidance about application of the Section 527(f) tax exclusions.92 With the Supreme Court's decision in Citizens United, there is a renewed urgency for this guidance. If and when Treasury does proceed with amendments, it is possible that the analyses we have provided here will prove more prohibitive (or possibly, though improbably, more permissive) than the Treasury's ultimate approach. Until that time, we think that the analyses described above present a sound basis upon which to advise Section 501(c) organizations with respect to Section 527(f) taxation. We hope the IRS and the Treasury may also find this analysis helpful in developing Regulations when the time comes.

Footnotes

1

This result arose from the view that the typical sources of income to political organizations were in the nature of gifts not subject to inclusion in gross income of the donee under general federal tax law. See Communist Party of the U.S.A. v. Comm'r, 373 F.2d 682 (D.C. Cir. 1967).

2

See I. T. 3276, 1939-1 C. B. 108 (superseded).

3

See Ann. 73-84, 1973-2 C.B. 461. See also Rev. Rul. 74-21, 1974-1 C.B. 14 (restating Announcement 73-84), clarified in, Rev. Rul. 74-475, 1974-2 C.B. 22; Rev. Proc. 68-19, 1968-1 C.B. 810 (clarifying that although political contributions to candidates used only for political purposes would continue to be tax-free, IRS considered any funds used for candidate's personal use to be taxable). Announcement 73-84 may be viewed as expanding Revenue Procedure 68-19 principles, which focused on the personal income taxation of candidates, to the investment income of political organizations.

4

All “Section” references in the text are to the Internal Revenue Code of 1986, as amended (Code), unless otherwise indicated.

5

See 93 S. Rep. 1357, 93d Cong., 2d Sess. 27 (1974), 1975-1 C.B. 517. Section 527 was introduced to the Code through the enactment of the Act to Amend the Tariff Schedules to Permit the Importation of Upholstery Regulators, Upholsterer's Regulating Needles, and Upholsterer's Pins Free of Duty (also known as the Pins and Needles Act of 1974), Pub. L. 93-625, 1975-C.B. 510.

6

This article focuses on specific issues in applying Code Section 527(f). The general overview of Section 527 in this Introduction is therefore brief and simplified. For an excellent and comprehensive discussion and analysis of Section 527, well beyond the scope of this article, see Milton Cerny and Frances R. Hill, The Tax Treatment of Political Organizations, 71

7

It is not necessary to incorporate a political organization exempt under Section 527. Many are created as unincorporated associations, and where the political organization is a separate segregated fund of a Section 501(c) organization, it may be created with nothing more than a resolution of the Section 501(c) organization's board of directors. The Section 527 fund must have its own bank account and federal employer identification number, but no application to the IRS for recognition of exemption is required, only notice to the IRS of its creation by filing a simple Form 8871. For further discussion of separate segregated funds, see infra note 38.

8

See I.R.C. § 527(c)(3).

9

Illegal expenditures by a political organization, or expenditures for an illegal activity, are by definition not made for an exempt function. See Treas. Reg. § 1.527-5(a)(2).

10

In 1988, Congress expanded the definition to include expenditures relating to a public office that, if made by the officeholder, would be deductible business expenses of the officeholder under Section 162(a). See I.R.C. § 527(e)(2).

11

All “Regulations” references in the text are to the U.S. Department of the Treasury Income Tax Regulations, unless otherwise indicated.

12

A note on terminology: Although federal campaign finance disclosure law and federal tax law affect one another, their development has not been coordinated. Similarly, federal laws regulating campaign financing have developed separately and without cross-reference to state laws on the same subject. As a result, each type of law, in each jurisdiction, has its own terminology. Even when the same words are used, they often do not share exactly the same meanings. To ease comprehension, this article uses the following terms and definitions based on usage in federal tax law: