Abstract

Despite all the twists and turns on the path to mobile sports wagering launching in the state of New York in early 2022—which included the unexpected resignation of Governor Andrew Cuomo, a licensing process that made powerful sportsbooks “frenemies,” and an eye-watering tax rate of 51% on operator revenue—the sense was that it was always going to be big.

That, of course, is fitting. Most everything about New York screams “big,” from brash attitude to the Manhattan skyline and many places in between. It is also big in the sense of population. New York is one of the four “Holy Grail” states when it comes to sports betting operators, a market so large operators would do practically anything to enter—hence the 51% tax rate with no deductions for promotional revenue that the nine licensees accepted while swallowing hard.

One of the first clues about how big it would be came from the New York State Gaming Commission, which oversees sports wagering and also publishes revenue reports for the gaming industry. Originally, it published revenue reports from the four retail sportsbooks monthly as part of the overall casino revenue snapshot—it did not even publish sports betting handle for those locations until last fall.

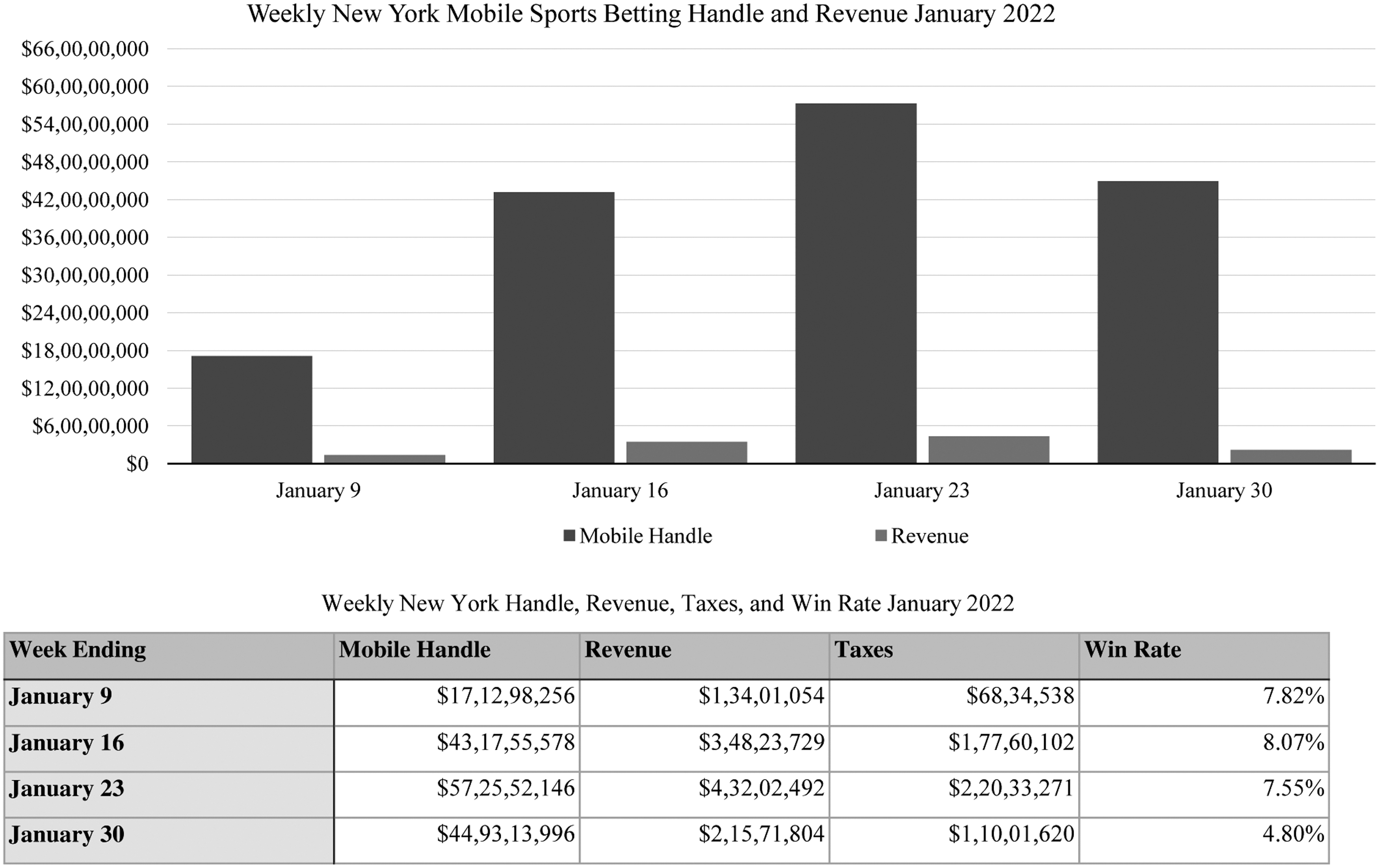

Rather than keep industry media in suspense for what would have been approximately six weeks from when the first online bets were placed to the January monthly report, it changed formats to publish revenue reports on a weekly basis. This allowed for the sizzle during a launch that accomplished the rarest of things in this age of instant gratification—exceeded the hype created during the buildup (Fig. 1).

Weekly New York Mobile Sports Betting Handle and Revenue January 2022. Weekly New York Handle, Revenue, Taxes, and Win Rate January 2022.

The first bets were placed January 8, a wise launch date considering it preceded the final Sunday of the NFL regular season. It has been established previously how much the NFL has contributed to the spiral-like rise in overall sports betting handle in the U.S. last fall and winter by embracing the legal market with official partners and approved operators. Of the four operators poised to launch the first weekend—FanDuel, DraftKings, Caesars, and BetRivers, three fit one of those two categories.

The quartet hit the ground running, generating more than $170 million handle in the first 39 hours. The first full week of betting, aided by the six NFL playoff games that included one involving the Buffalo Bills, sent handle surging to more than $430 million. The next week, the always-anticipated divisional round of the NFL postseason and another Bills game sent handle spiraling higher to nearly $575 million.

Though the final full week of January saw handle retreat to just shy of $450 million, the excitement to participate was clearly evident, as was the desire for operators to attract new customers with promotional offers that were simply jaw-dropping.

No large operator arguably had as much at stake as Caesars, which like other operators, also had been preparing to launch mobile wagering in Louisiana at the end of January. But New York called for something bold, befitting the largest market in the country now with legal wagering.

Prior to New York launching operations, Caesars had not made a large footprint in other large-market states. It had less than one-half of one percent market share in Pennsylvania, with its $26.4 million handle in 2021 looking like an accountant's rounding error compared to FanDuel's nearly $2.3 billion in the Keystone State that equated to almost 38% of the mobile wagering amount.

In Illinois, its failure to gain traction was exacerbated by the state's in-person registration policy to gain access to mobile wagering. Though that was suspended for most of the pandemic via executive order by Governor JB Pritzker, many sports bettors were not making their way to Grand Victoria Casino in the Chicago suburb of Elgin, and Caesars also did not make its migration from William Hill as part of its makeover with any urgency in the Prairie State.

The numbers again spell this out in stark fashion. Caesars did generate nearly $120 million handle in Illinois in 2021, but it represented less than 2% of the more than $6.7 billion wagered among the six mobile operators accepting wagers. Caesars again was looking up at both FanDuel and DraftKings as the duo claimed close to 70% of the market share.

Caesars went all-in for the New York launch, matching initial bettors' deposits up to $3,000—well above any other operator in the space and believed to be the largest of any legal sportsbook in any state in the U.S. post-PASPA (Professional and Amateur Sports Protection Act) era going back to May 2018. The butterfly effect was immediate as it accepted close to $630 million in wagers for the month, which came to slightly more than three dollars out of every eight bets in New York in January.

It was, therefore, no surprise that New York set the all-time national monthly handle record with nearly $1.7 billion, and it completed the “Triple Crown” in also setting national monthly records for operator revenue and state tax receipts. With high handle comes high revenue, though that number fluctuates to a degree. But seeing the 51% tax levied on operators after months of it being an abstract that sounded and/or looked high was the other big story from the launch.

The $63.3 million collected overall for the month nearly tripled the previous record of $21.6 million established by Pennsylvania last November. The Keystone State taxes adjusted revenue at 34%, a rate that is 50% lower than New York. Caesars alone paid $30.1 million in taxes to the state of New York in January, the only number higher nationwide was the $33.2 million paid by the other six operators in the state.

Even its highest weekly tax bill of $9.7 million for the week ending January 23 would have ranked third nationally among states outside New York. In some respects, it was a win-win-win all the way around as New York bettors no longer have to cross state lines to place bets, operators can conduct business in the largest market available to them, and the state of New York is on pace to exceed the $500 million it expected in annual tax revenue from sports wagering.

New York, though, was not alone in setting records for handle. That phenomenon was again a nationwide occurrence similar to what took place in the month of October when $7.5 billion was wagered. Like October, January had 10 weekend days for people to spend more time watching sports and gambling on them.

In addition to the NFL playoffs as a handle driver, January also had the meat of the college basketball season. More than 350 schools playing one to three times a week, often in matchups against long-time conference rivals that stoke fan passion and betting interest.

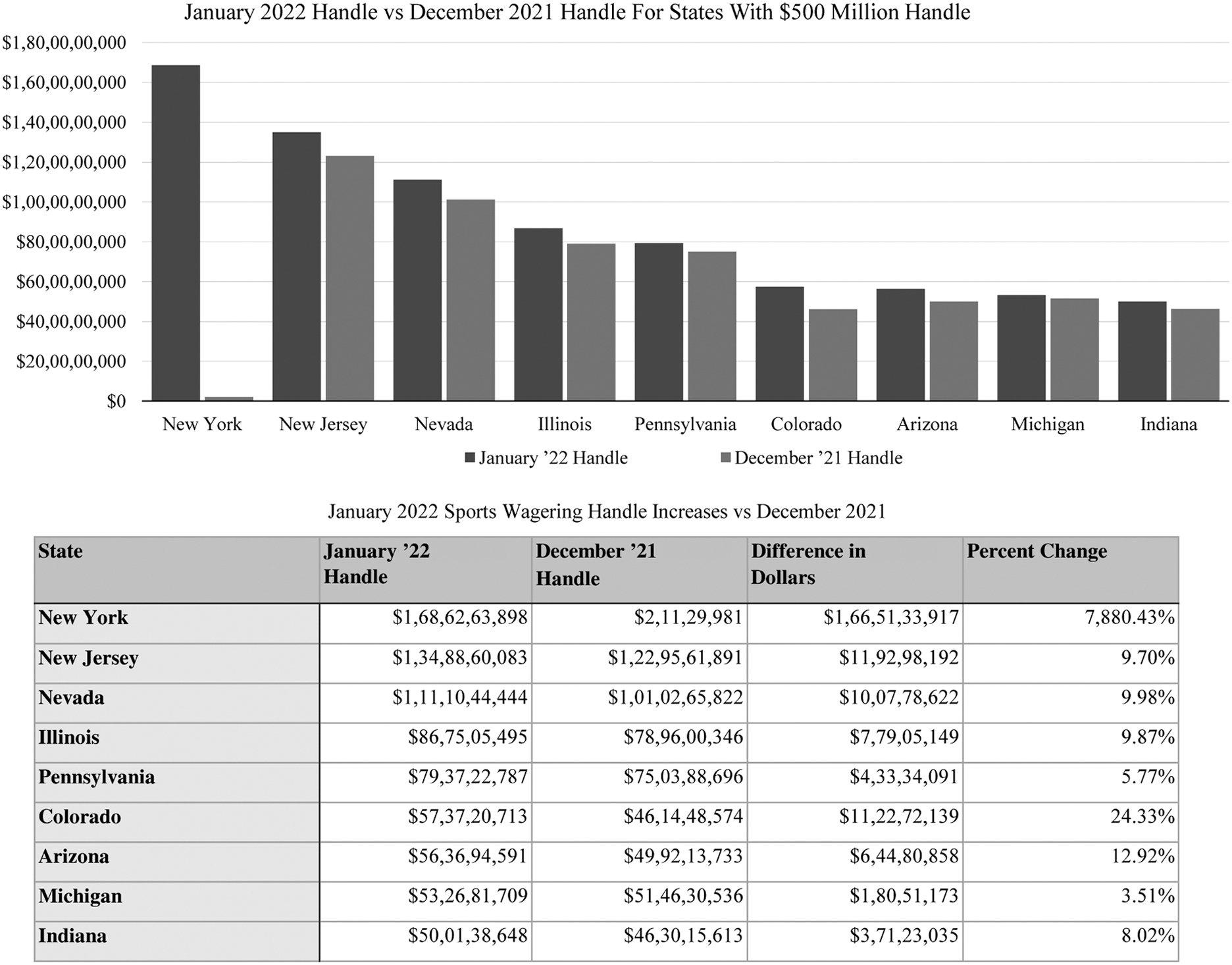

The ripple effect was evident seemingly everywhere (Fig. 2) as a record nine states cleared $500 million handle in the month of January. The eight states outside New York with pre-existing mobile wagering available that cleared one-half billion dollars in wagers had a combined handle increase of 10% versus December, with three of them having a month-over-month increase of more than $100 million.

January 2022 Handle vs December 2021 Handle For States With $500 Million Handle. January 2022 Sports Wagering Handle Increases vs December 2021.

The eight states set new all-time monthly handle records, helping contribute to a record national monthly handle of more than $9.8 billion. Given February does not lend itself to month-over-month growth with three fewer days of wagering available and no true marquee events after the Super Bowl, January can be used as the end point of an unprecedented four-month frenzy of sports wagering in the United States largely fueled by football in general and the NFL specifically.

The period from October 1st through January 31st saw $31.6 billion worth of bets placed, equal to 91% of the $34.6 billion wagered nationwide in all of 2019 and 2020 combined. That is not a like-for-like comparison given more states currently have sports wagering available and the COVID-19 pandemic shuttered the industry for three-plus months in 2020. Still, the next-highest handle of any four-month window that does not overlap with October 2021 through January 2022 is the $16.8 billion wagered from December 2020 through March 2021.

Another way to put the four-month surge in perspective is to consider the amount of the 10th-highest handle among states before and at the end. In September 2021, Tennessee ranked 10th with a handle of $257.4 million. Virginia claimed that spot in January but needed $485.5 million worth of wagers to do so, an increase of 88.7%.

The NFL helped in both ends of January with its first 18-week season in history that led to two full weekends of regular-season games that led into a postseason with unmatched excitement and drama from wild-card round to divisional playoffs to conference championships.

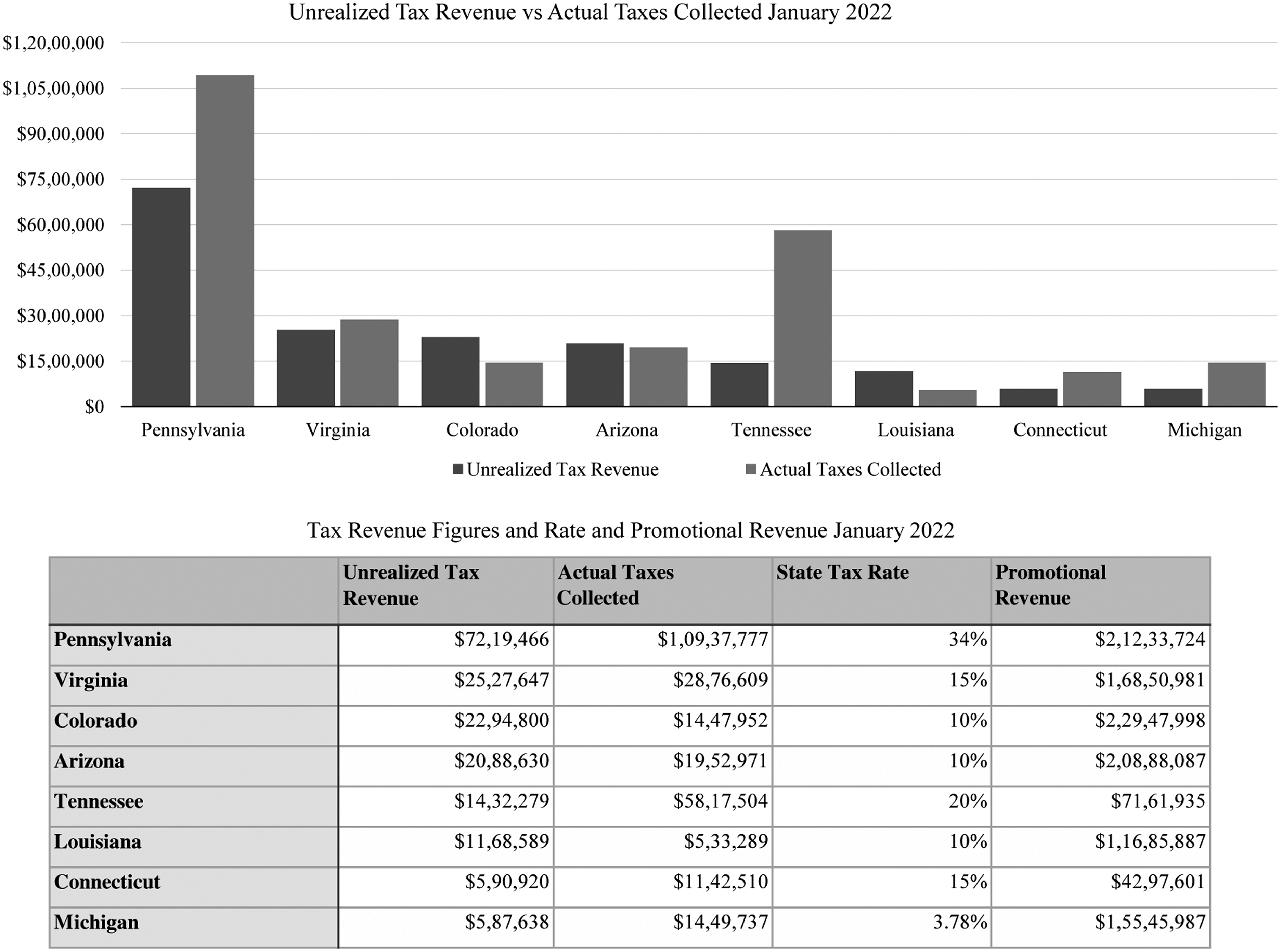

The last by-product of a record-setting January for handle and tax receipts again revolves around New York. Its 51% tax rate coupled with the inability of operators there to deduct promotional revenue may be creating an outlier when it comes to national monthly tax figures. The Empire State accounted for 49.3% of the record $128.6 million in tax receipts from sports wagering, but that figure also hides a notable amount of promotional revenue that goes untaxed from select states.

There are nine states that allow operators to make a portion of their promotional revenue tax-free (Fig. 3). Of the nine, five ranked in the top 10 for handle in January, and Tennessee was 11th. Operators in those states were able to claim a combined $121.2 million as untaxed promotional revenue, an amount close to the actual amount of taxes collected and also 18.7% of gross sportsbook operator revenue totaling $648 million in the first month of 2022.

Unrealized Tax Revenue vs Actual Taxes Collected January 2022. Tax Revenue Figures and Rate and Promotional Revenue January 2022.

Because states tax revenue at varying rates, different definitions of promotional revenue and varying levels of limits on promotional revenue, the range of the actual dollar amounts of unrealized taxes among states will be wide. The size of the market is another variable. For example, the amount of unrealized tax revenue in Michigan, which levies a 3.78% tax on adjusted sports betting revenue, will be far less than that of Tennessee, which does so at 20%.

Not including Wyoming, the other eight states had an estimated $17.9 million in unrealized tax receipts in January. Three states—Colorado, Arizona, and Louisiana—had higher unrealized tax revenue totals than actual tax receipts, while Pennsylvania's 34% tax rate meant it easily had the highest unrealized tax amount despite collecting the most taxes among the eight states shown.

Eighteen million dollars per month may not seem like a notable amount when pooled together, but $216 million in “lost” tax revenues annually nationwide is bound to generate some attention—especially when you consider states still on the path to legalization.

It is important to remember that sports betting does not operate in a vacuum for state legislators. It is sometimes the vehicle that creates the path for casino-style iGaming, which states can tax at a higher rate given the profit margins are less prone to the monthly fluctuations sports wagering has. Additionally, many sportsbook operators offer their wares as part of iGaming platforms, so the game of give and take with legislators is part of the game within the game of the gaming industry.

Some statehouses have become savvy about promotional revenue, with newcomers Connecticut and Louisiana prime examples. Connecticut currently allows operators to deduct up to 25% of their gross revenue for promotional play, but that percentage will drop by five points each following year until it zeroes out. Louisiana limits promotional play to $5 million per operator, which fosters business strategy that includes keeping powder dry for big events, including the Super Bowl and NCAA Tournament.

The state that may be paying the most attention currently is Ohio, which is on a deliberate path to launch that looks to be on or near Jan. 1, 2023—the latest date allowed by state law. Rules packages are being submitted constantly, and the eventual end product will undoubtedly affect the extent to which the Buckeye State can add to its own coffers.