Abstract

Sports wagering in the United States attained mainstream status in 2022, aided by New York's entry into the mobile marketplace and the widespread popularity of parlay offerings, led by FanDuel. Handle and revenue rose substantially compared to 2021 and has positioned the industry for further growth with more states already online in 2023.

Last year will be remembered as the year sports wagering came of age and entered the United States mainstream to stay. It is no longer a destination to-do solely restricted to Las Vegas as the smartphone has replaced the brick-and-mortar sportsbook as the primary means of placing a wager.

Additionally, the dynamics of sports wagering have changed. The single-event wager remains popular, and it is still where most of the handle is derived. But the rise of the same-game parlay has tilted the playing field towards the operator. It has made FanDuel, the first mover for this specific type of wager, into the premier operator in the United States and the first sportsbook to turn a profit in the country ahead of the industry's fifth birthday of being available on a state-by-state basis.

As one looks back to 2022, it is readily apparent 2023 has gotten off to a roaring start thanks to another large-market launch in Ohio. Massachusetts also offers promise with mobile wagering having just started ahead of the National Collegiate Athletic Association (NCAA) Tournament. Those two states will eventually be addressed going forward, but the focus will be on last year following the Arizona Department of Gaming's recent publishing of its December revenue report that allowed for a final tally of plenty of dollars.

MOBILE EXPANSION FUELS HANDLE INCREASE MORE THAN ADDITIONAL STATES

As Figure 1 shows, handle increased by a whopping 62.4% from 2021 to just shy of $93.8 billion despite Kansas being the only state to launch sports wagering in 2022.

Yearly U.S. Sports Wagering Handle. 2018–2022.

Prior to operators in the Sunflower State accepting their first wagers in September, there were mobile launches in states that already had retail wagering in place for varying lengths of time that made a much larger impact.

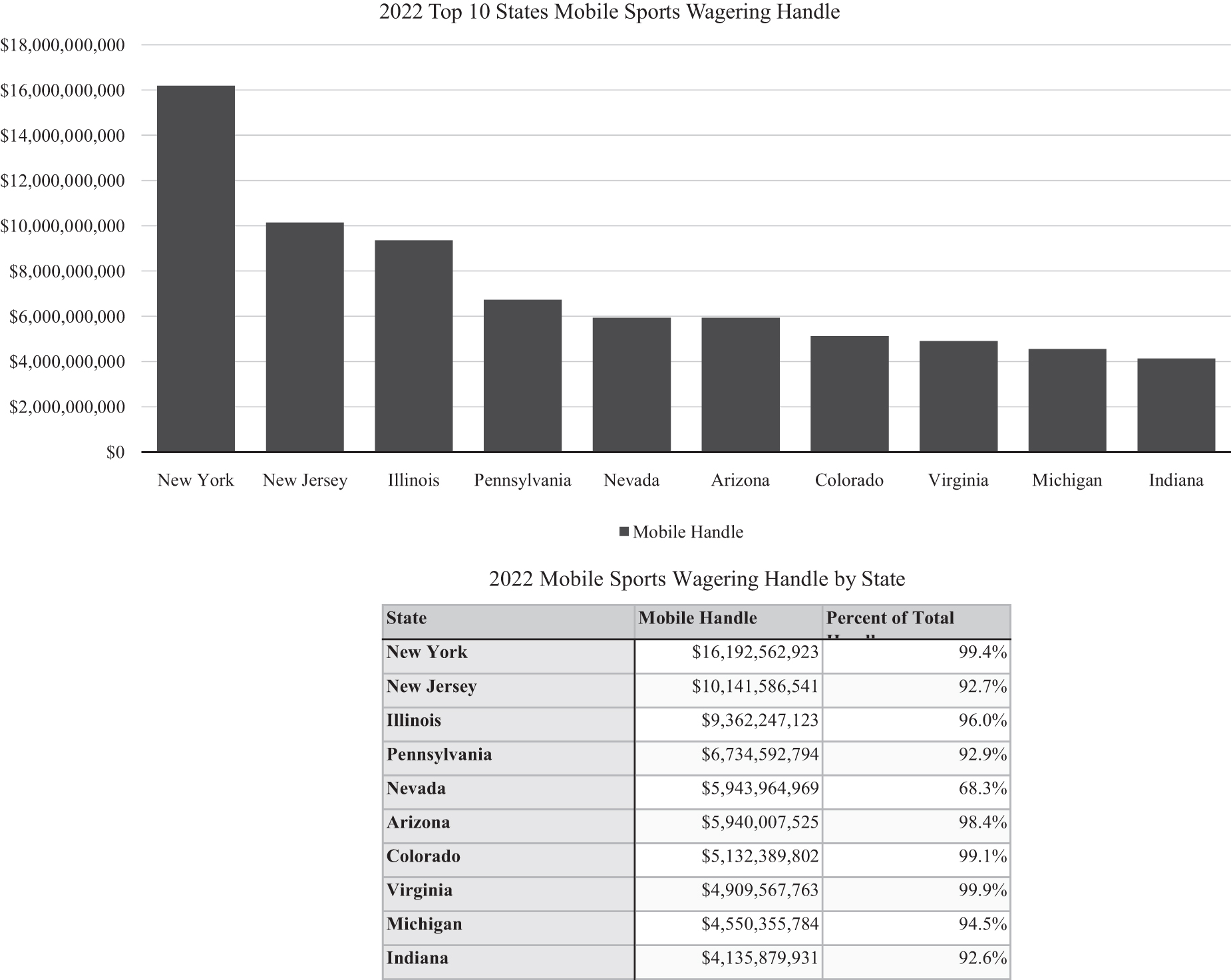

None were bigger and more anticipated than New York's, with its mobile launch timed perfectly for the final weekend of the 2021 National Football League (NFL) regular season. As Figure 2 illustrates, New York's entrance into the mobile sports wagering arena proved worth the wait as one of only two states to surpass $10 billion in online handle. Bettors were counting down the days they no longer had to deal with the inconvenience of driving to one of the state's four commercial casinos or make the trek across the Hudson River into New Jersey to make a mobile bet via phone or laptop before resuming their everyday activities.

Top 10 states for mobile handle, 2022.

Operators fed into that frenzied anticipation, with introductory sign-up offers akin to an arms race. Caesars blew everyone out of the water with its $300 free bet sign-up and $3,000 matching deposit, which served the short-term purpose of making a huge splash and the long-term purpose of cementing itself as the No. 3 operator among the nine mobile options.

New York's mobile handle of close to $16.2 billion accounted for nearly 45% of the $36 billion in overall dollar handle increase from 2021 to 2022.

Louisiana, which opened its mobile market in the final week of January, generated close to $2 billion in online wagers while Maryland mobile operators accepted nearly $665 million worth of bets placed in the final five-plus weeks of the year.

Arizona's first full year of sports wagering saw mobile handle eclipse $5.9 billion, coming within shouting distance of Nevada. The Silver State still requires in-person registration for access to mobile wagering, a key reason mobile handle accounted for only 68.3% of total handle compared to the 92% and higher for all the other states that had top 10 mobile handle figures in 2022.

PARLAYS PROVE WILDLY POPULAR NO MATTER THE STATE

That influx of $36 billion in additional handle for 2022 had to be wagered somewhere, and the belief is that a notable portion of it was on parlays. FanDuel had a large hand in this as the first mover of single-game parlay offerings, but the NFL now fully entrenched with official sportsbook partners and approved sportsbook operators also played a huge role in that increased amount.

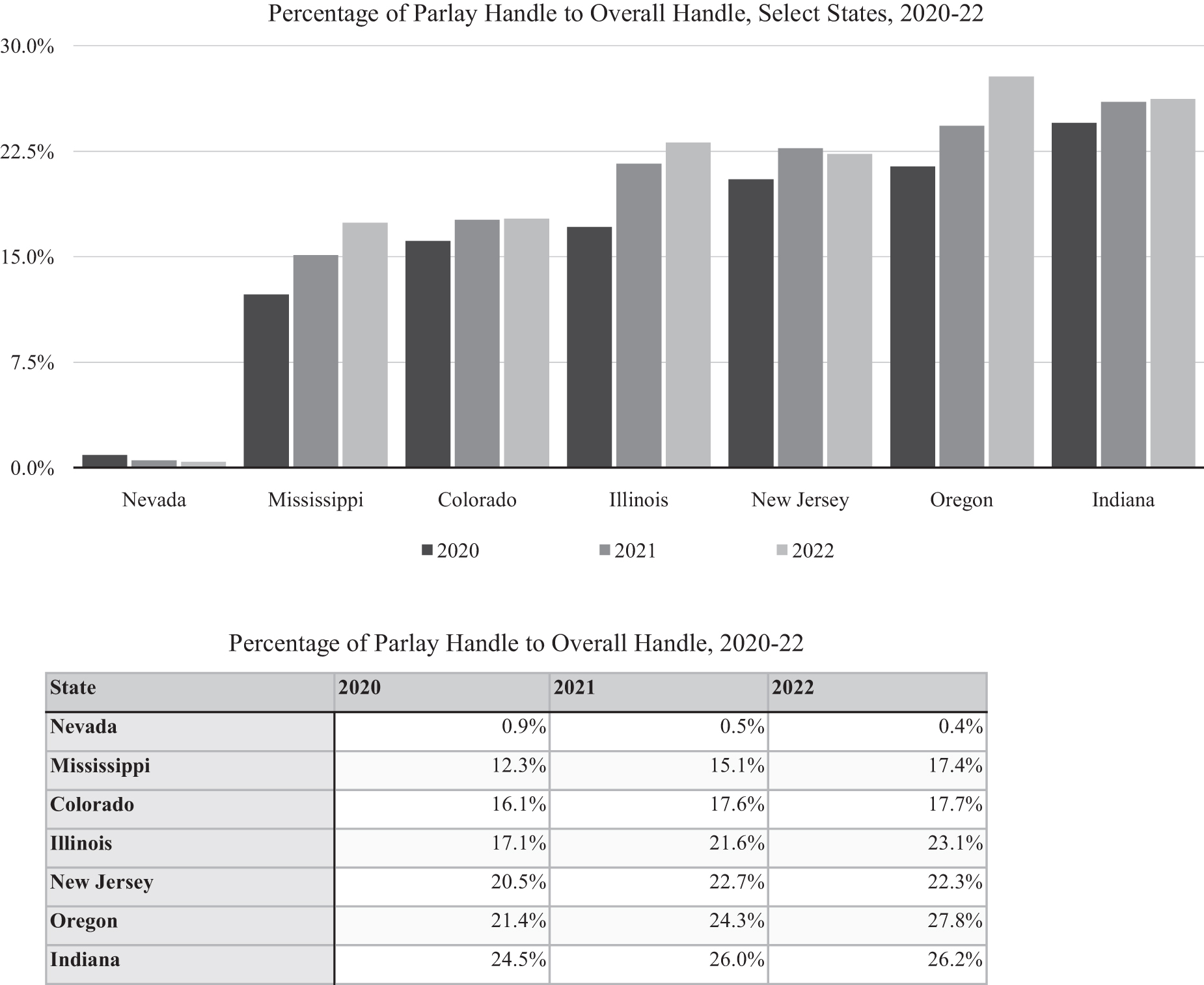

Only seven states provide a full accounting of parlay handle and revenue, and except for Nevada—an outlier in this wagering discipline—nearly every state showed year-over-year increase in the percentage of handle from parlay wagers to overall handle from 2020 to 2022, as shown in Figure 3.

Percentage of parlay wagering handle versus overall handle for select states, 2020–2022.

That time frame is being used since all seven states that furnish parlay handle and revenue information were live markets at the time.

In the case of New Jersey and Illinois, parlay handle in 2022 surpassed $2 billion, while it cleared $1 billion in Indiana and $900 million in Colorado. While Oregon had a modest parlay handle of $138.4 million, it should be noted that the percentage of parlay handle jumped from 24.3% to 27.8% in the first year DraftKings—which also has same-game parlay options available—ran sports wagering on behalf of the Oregon Lottery. Those seven states combined for more than $15.2 billion in parlay handle in 2022, just over 16% of all U.S. commercial handle.

Gross sports wagering operator revenue outpaced the explosive handle growth, increasing 74% from 2021 to close to $7.6 billion. Again, parlays were a key component of revenue growth as the win rate from such wagers skewers far greater to the house than single-event wagering.

As seen in Figure 4, the win rates for the house are substantially higher than the industry standard of 7%.

Percentage of parlay revenue to overall revenue for select states, 2022.

In the case of Mississippi, the operator hold is more than triple that amount. Though a small sample size as an outlier, Nevada's hold is more than four times above the standard. Outsized win rates led to outsized revenue totals, creating almost a dependency for operator profit via parlays, and that dependency gets passed onto the state as a means of generating tax revenue that can be plugged into a budget forecast.

The total gross revenue from parlays from these six states is more than $1.07 billion. Though the New York State Gaming Commission does not disclose handle and revenue by category, there were seven instances during the 18-week NFL season when the combined win rate among the state's nine mobile operators was 10% or higher, highlighted by a 13.5% hold for the week ending October 9.

Given FanDuel's dominant market share for both handle and revenue in the Empire State—its $6.5 billion handle accounted for more than 40% of the marketplace while its $650 million-plus revenue was nearly 48% of all mobile revenue generated, makes it reasonable to believe parlay wagering proved very beneficial for both operators and state government—especially with New York's 51% tax rate.

In the case of New Jersey and Illinois, two large-market states, the majority of operator revenue is derived from parlays. In the case of Illinois, the universal 15% tax rate means the state received close to $63.5 million in receipts from parlays in 2022 while single-event wagering generated just shy of $55 million.

Though economic conditions will help dictate just how much is wagered—in a perfect world, sports wagering is done with discretionary income and in proper moderation—it appears clear reliance on parlay wagering is the revenue model operators will utilize as a faster path to profitability. Ohio may have provided a hint of that as operator revenue in the launch month of January set a national post-Professional and Amateur Sports Protection Act (PASPA) record of nearly $209 million while the $1.1 billion handle ranked 16th at the time it was published, though the state's Casino Control Commission does not publish figures by category.

To put Ohio's revenue in perspective, consider New York has reached a peak handle of just shy of $1.8 billion but has yet to clear $150 million in operator revenue. Parlays were a reason the win rate for gross revenue in 2022 cleared 8% for the first time in the post-PASPA era, landing at 8.06% and continuing the trend of inching higher for a third consecutive year.

The second half of 2022 was an unparalleled success for operators, who were able to lift the all-time win rate of the post-PASPA era nearly six-tenths of a percentage point to above 7.7% while generating nearly 59% of their 2022 revenue. To borrow from Charles Dickens, it truly was the best of times in the last six months as the nationwide hold was above 9.4% compared to the worst of times in the opening six months of last year when it was just under 6.7%.

How operators fare in 2023 remains to be seen, though the additions of Ohio and Massachusetts will likely overwhelm any potential dips in handle from existing markets. Whether the betting public can find a winning formula for parlays to knock the house down a peg likely will determine if the good times will continue for operators.