Abstract

The first month of sports wagering in 2023 picks up where the final month of 2022 left off: A record national handle and an all-time high of operator gross revenue in the post-Professional and Amateur Sports Protection Act (PASPA) era.

There was a time coming out of the COVID-19 pandemic, in the summer and fall of 2020, when 18 states and jurisdictions had legal commercial sports wagering. There was starry-eyed talk about the nationwide monthly handle potentially reaching $3 billion, which would then be a springboard to bigger, though not necessarily always better, things.

Sure enough, that $3 billion handle came in October of that year. Then $4 billion followed in January 2021, a tailwind started with the additions of Tennessee and Virginia. The talk then centered around $5 billion—would it happen in March with the NCAA Tournament? Alas, no, but that would come in September with the first real impact of the NFL's deals making FanDuel, DraftKings, and Caesars official league partners in various avenues of wagering.

Fast forward another 15 months: More states have “seen the light” when it comes to the potential tax revenue sports wagering can provide, including higher amounts if regulated correctly. Twenty-nine states were now offering legal commercial betting by the end of January 2023, with Massachusetts sneaking in via retail launch on January 31, and Ohio having the mother of all launches to ring in the New Year.

The NFL is now the unquestioned leader among market movers for sports in U.S. wagering. The meteoric rise of parlay wagering in general and single game parlay wagering specifically has somewhat bucked the challenging overall economic trends of a country grappling with high inflation and increased costs of living. Bettors are willing to wager $1, $5, or even $10 to make a wager that is akin to playing a lottery ticket given how every leg of a parlay must hit to be a winner.

Add all these things together, and the result is a still-expanding national market. As of the writing of this article, Kentucky had recently legalized sports wagering and North Carolina was on the cusp of doing likewise for commercial betting.

The history-making closeout to 2022 in which nationwide handle surpassed $10 billion for the first time in December was quickly shoved out of the way with the number topping $11 billion in January. But the start of 2023 will also be remembered for the first $1 billion gross revenue total in the post-PASPA era, in large part thanks to Ohio's debut.

The Buckeye State's eagerly awaited entrance not only brought a $1 billon handle, but also a jaw-dropping gross revenue total north of $200 million. It was a figure unfathomable considering New York had failed to touch $150 million in any month during 2022 despite becoming the unquestioned leader in handle during its first year of having mobile wagering available.

THE BUCKEYE BOUNCE

There was considerable anticipation for Ohio to launch given Kansas was the only state to have a full launch in 2022. New York's mobile launch, however, whet the appetite for what could happen in the Buckeye State. Those hopes were heightened when it was announced there would be a simultaneous mobile and retail launch on New Year's Day offering the tantalizing possibility the clock would strike “12” and a flood of wagers would hit sportsbooks after Ohio State defeated Georgia on New Year's Eve to advance to the College Football Playoff Championship.

That never materialized as the Buckeyes squandered a two-touchdown lead in the fourth quarter and offered few live bets when the game continued to the other side of midnight, but there were plenty of places where handle would originate. One came from the NFL, where bettors had the opportunity to wager on the final two weeks of the regular season and ride the Cincinnati Bengals in the playoffs.

Another was the NBA, with the Cleveland Cavaliers blowing past expectations to be a playoff-viable team. College basketball offered plenty of options with 13 Division I teams, but also a soft landing place for Kentucky bettors, who could now wager on their beloved Wildcats in neighboring Ohio and Indiana. Lastly, there would be lots of “risk-free” wagers in the forms of promotional offers from operators that come with a launch in a new state as they seek an early foothold in a pristine market.

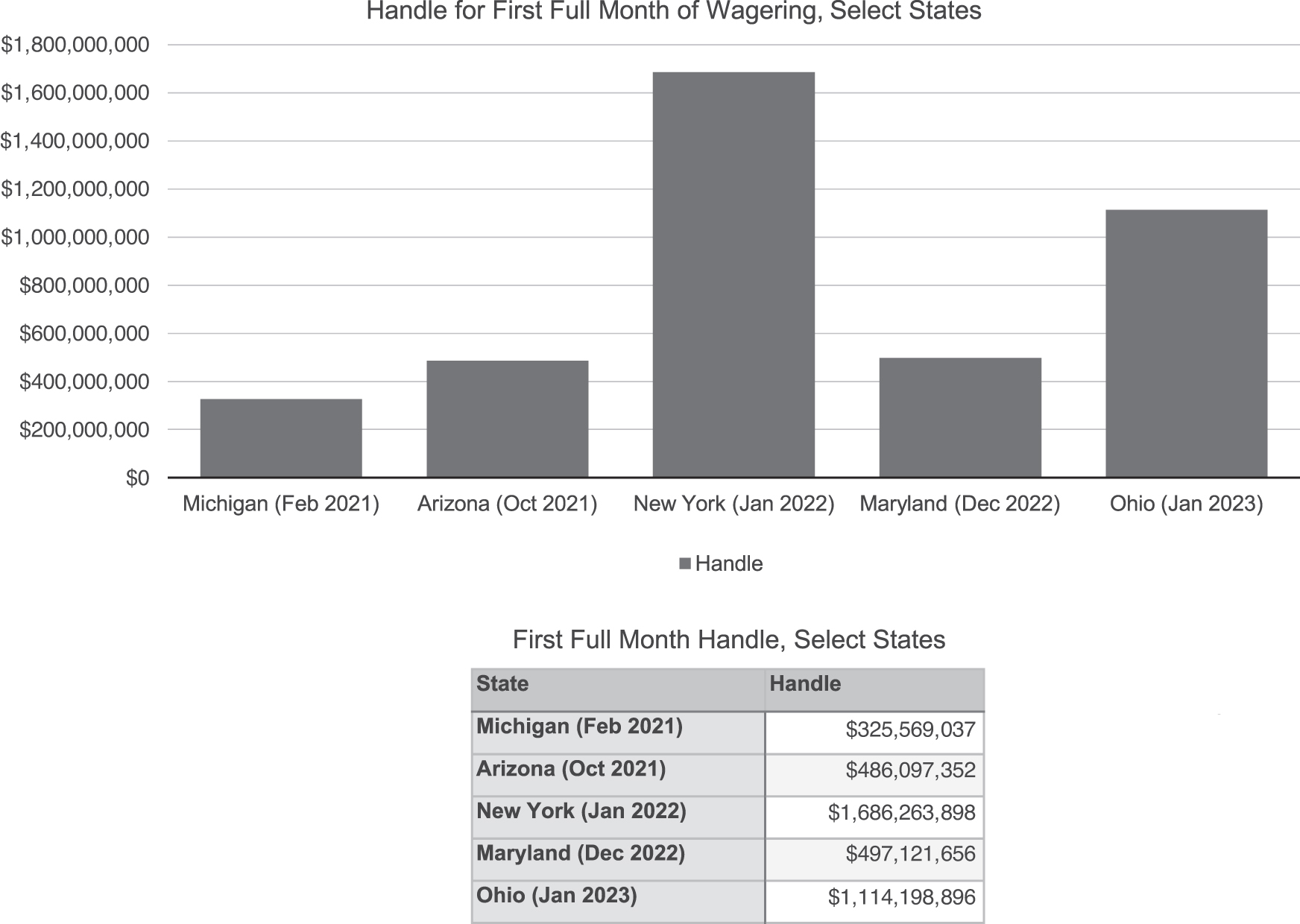

Thus, it was no surprise that Ohio surpassed $1 billion handle in January (please see Figure 1) for the first reports published by the state's Casino Control Commission and Lottery since both have jurisdictional standing for sports wagering. Also unsurprising was the amount of promotional outlay by operators to gain market share.

Handle for First Full Month of Wagering, Select States

Of the more than $1.1 billion in accepted wagers, nearly 30% of that amount—close to $320 million—came from operators' promotions (please see Figure 2). The top two operators in the United States—FanDuel and DraftKings—ranked 1–2 in promotional spend, and FanDuel accounted for more than 50% of the overall total at nearly $168.7 million. To put that figure in perspective, it would have ranked 17th nationally for January handle on its own.

Promotional Spend by Mobile Operators in Ohio, January 2023

While no one was surprised FanDuel and DraftKings accounted for more than one-quarter billion dollars in promotional spend between them, there were some unusual suspects who attempted to make a splash. BetMGM, which may be the only other operator who has the bottomless pockets to spend at a relatively comparable level to FanDuel and DraftKings, was third with more than $27.3 million.

Very few people, though, would have pegged bet365 as the only other operator to have an eight-figure promotional outlay at close to $16 million. Ohio is just the fourth state bet365 has entered in the U.S., with New Jersey, Virginia, and Colorado the others.

Barstool Sportsbook rounded out the top five with nearly $5.5 million in promotional credits, but that spend is lower in scale to its overall marketing budget considering the PENN Entertainment-owned sportsbook relies heavily on promotion through its social media presence via Barstool founder Dave Portnoy.

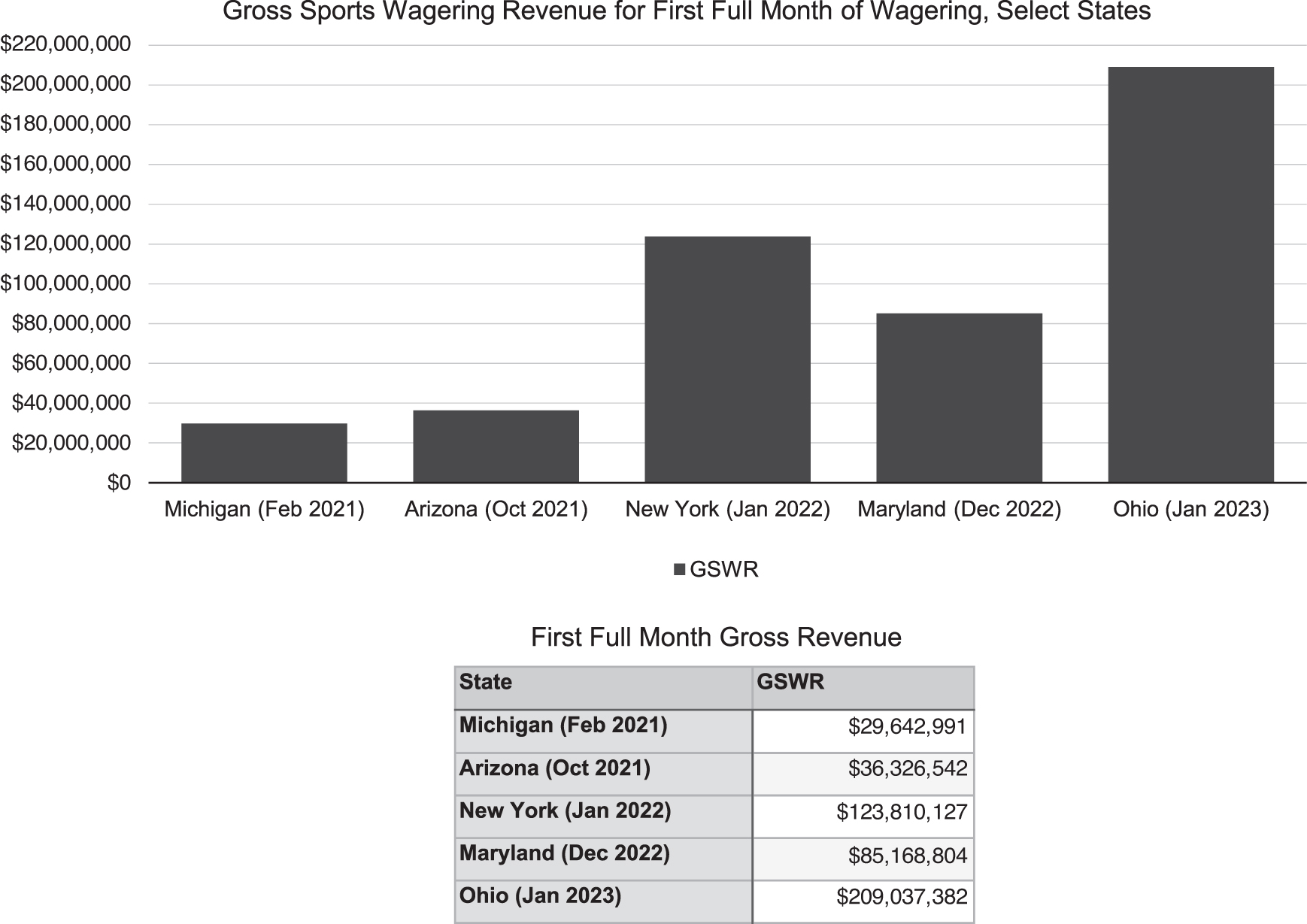

No Ohio state regulatory agency provides wagering statistics by sport or category, but what was overwhelmingly evident was operators were the early winners (please see Figure 3). Of the 16 mobile operators who took bets in January, only one—Betly—finished with negative gross revenue. Of the remaining 15, all but two—BetRivers and Ohio-specific betJACK—posted holds on gross revenue of 10% or higher.

Gross Sports Wagering Revenue for First Full Month of Wagering, Select States

In the five states selected for comparison purposes from recent launches, be it full mobile and retail wagering (Arizona, Ohio) or exclusively mobile wagering (Michigan, New York, Maryland), three states allow for promotional deductions while two do not. Ohio will not allow operators to deduct promotional credits through 2026, one of the savvier decisions learned by observing launches from other states.

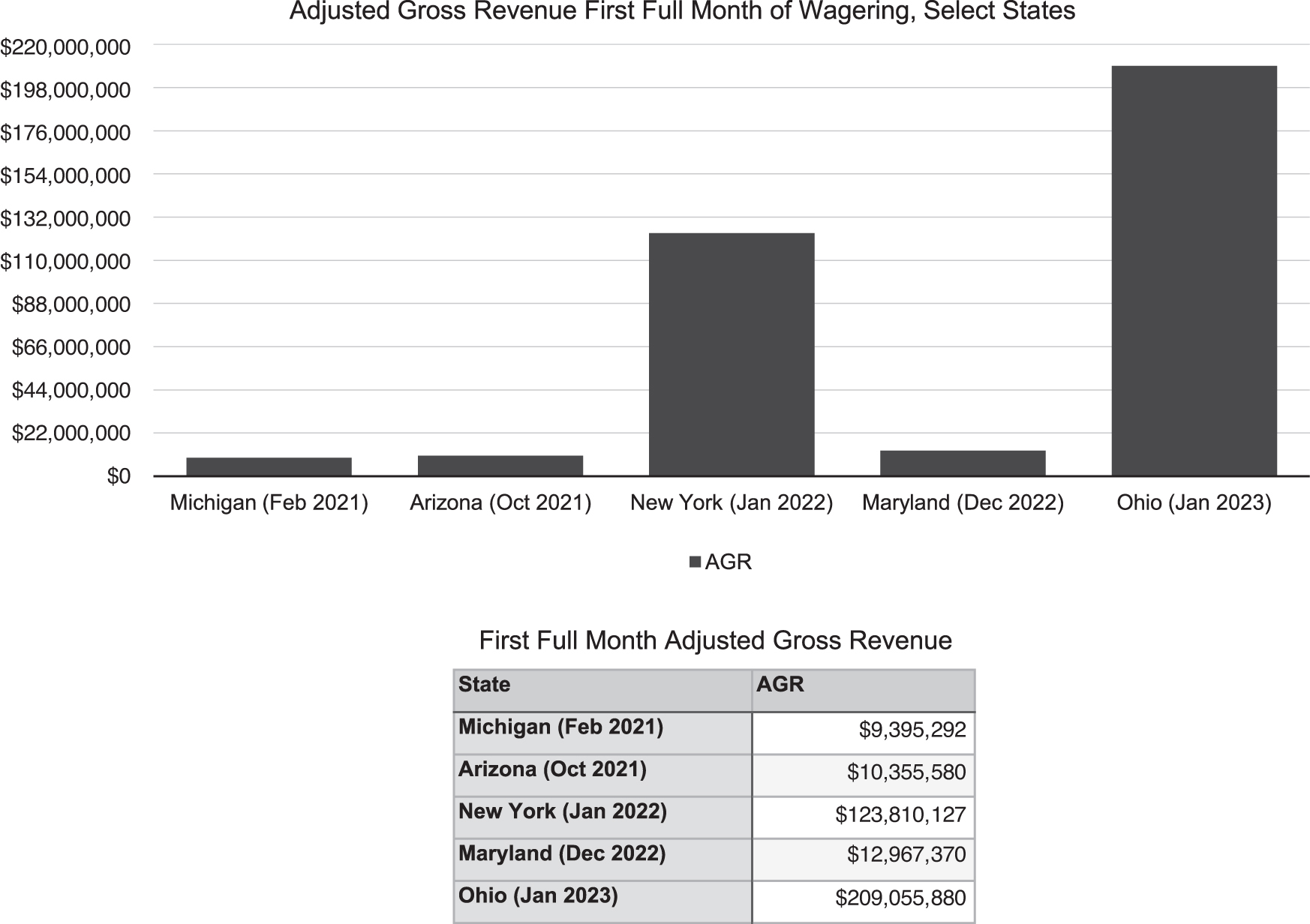

Maryland's first full month of mobile wagering last December (please see Figure 4) illustrates the potential chasm that can occur in the opening few months of wagering when credits are allowed to be deducted. The spread between operator gross revenue and adjusted gross revenue in the Terrapin State was more than $72.2 million; based on the state's 15% tax rate, the state missed out on over $10.8 million in tax revenue.

Adjusted Gross Sports Wagering Revenue for First Full Month of Wagering, Select States

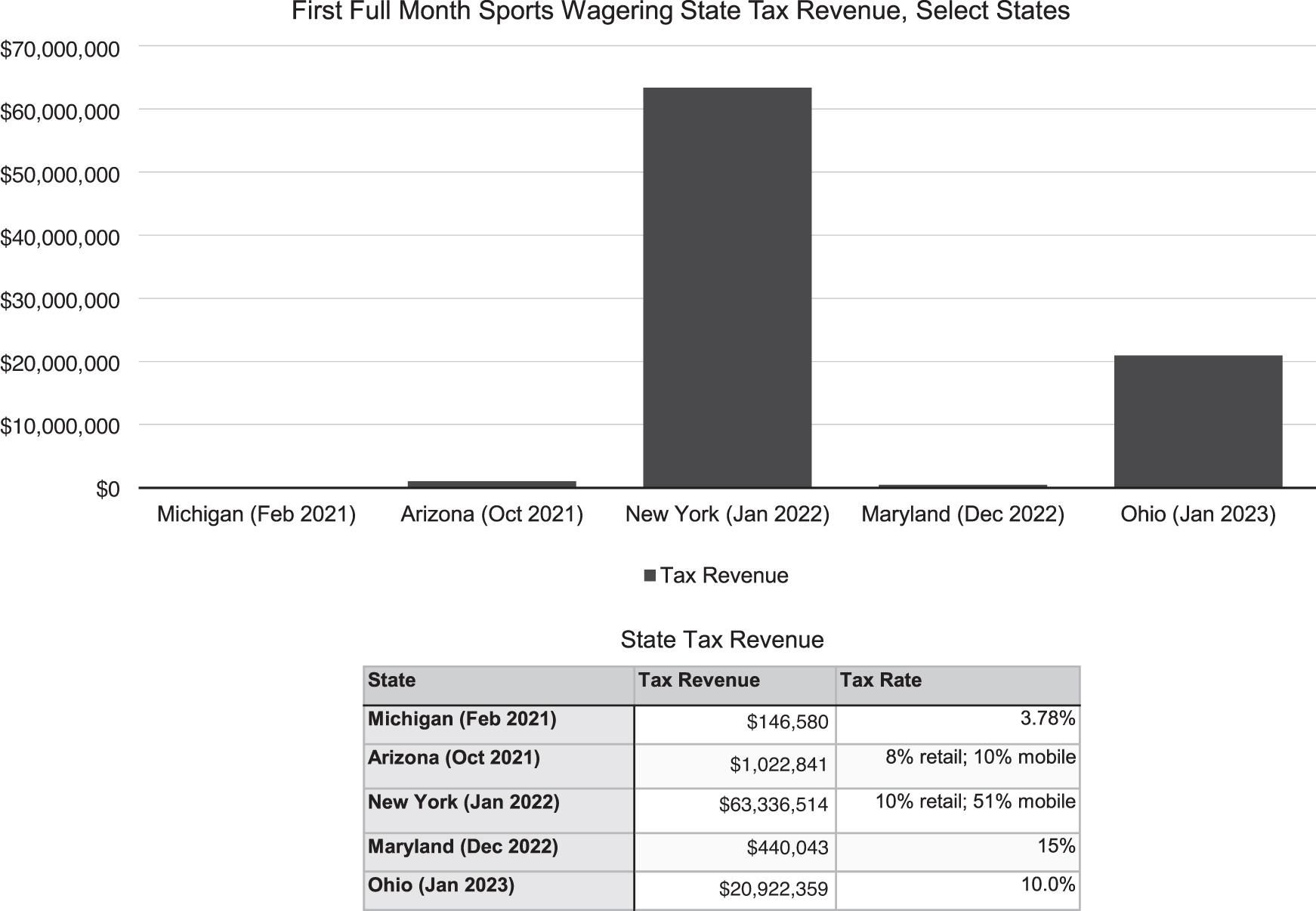

Only two operators generated more revenue than promotional spend in Ohio in January, Caesars and micro-betting platform Betr. Had operators been allowed to deduct their full promotional spend, the Buckeye State would have received less than $66,000 in tax receipts from those two operators compared to the $20.9 million-plus it did receive (please see Figure 5) while using a business-friendly 10% tax rate compared to the 51% on mobile revenue New York utilizes.

First Full Month Sports Wagering State Tax Revenue, Select States

ONE BILLION DOLLARS OF OPERATOR REVENUE

Ohio is a primary reason the nationwide gross revenue for January cleared $1 billion for the first time, but as mentioned in previous abstracts, the rise of single game parlay popularity and the NFL playoffs are not far behind.

This space previously called for revisiting the “industry standard” of 7% when it came to sportsbook performance. Put simply, it is believed operators can sustain their business when they keep at least $7 out of every $100 wagered for revenue, though that does not count deductions including the federal excise tax and state taxes. January marked the sixth time in the last seven months the hold on gross revenue topped 9%, but all seven cleared the 7% benchmark. Additionally, those six months when the hold was above 9% all rank in the top 14 of the post-PASPA era, which spans 56 months dating to June 2018.

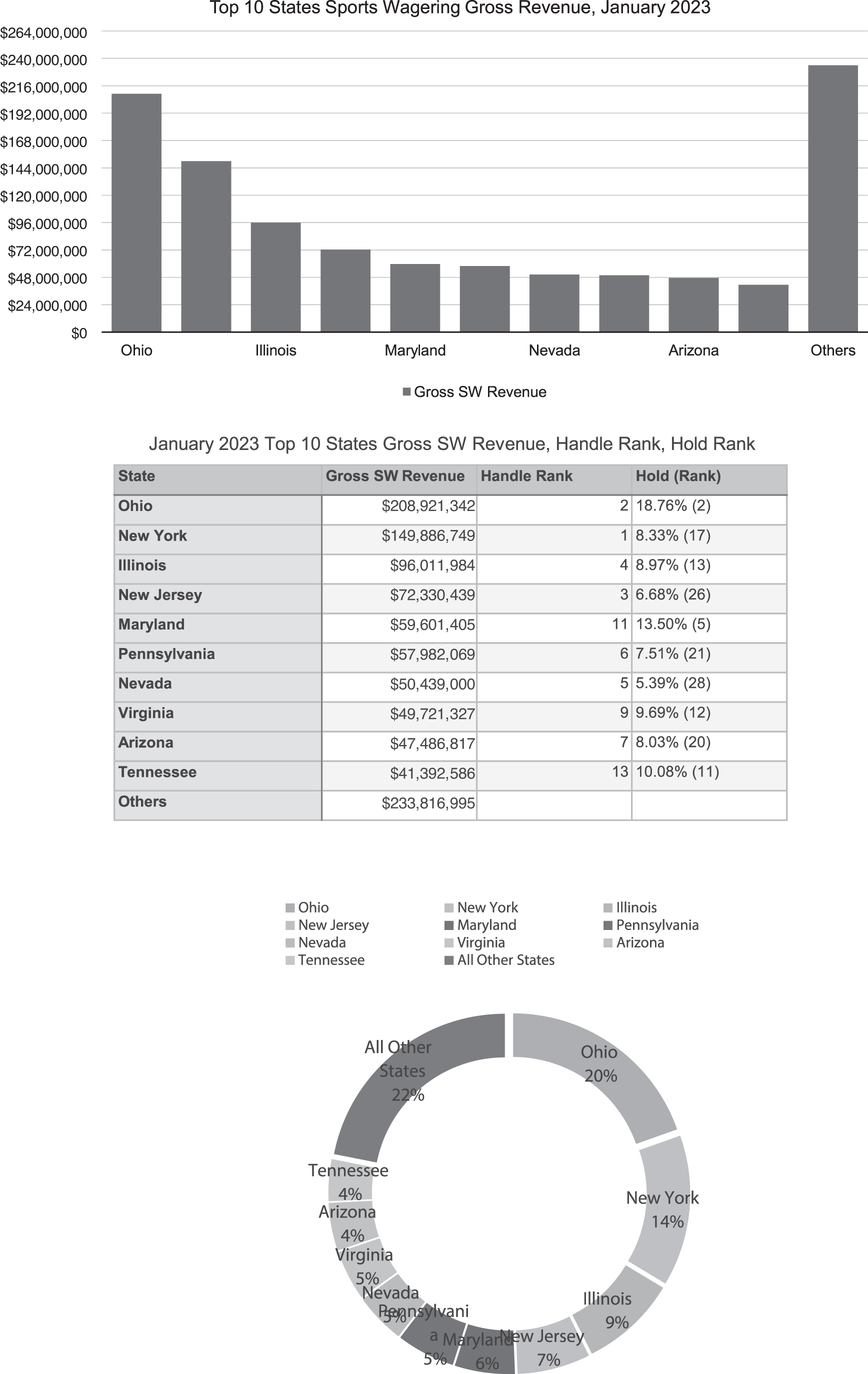

The hold for January was close to 9.3%, slightly below the 9.5% reported for December, with 21 of the 29 jurisdictions having a hold above 7.5%. Removing Massachusetts and its one day of retail betting that resulted in a negative hold, three of the top 10 gross revenue-producing states had holds in the bottom quarter (please see Figure 6), and the four lowest holds all came from states that ranked in the top 10 for handle.

Top 10 States Sports Wagering Gross Revenue, January 2023

Ohio's January figure was to be a very large outlier—February's figure was less than half that amount while also producing a robust hold as promotional spend was substantially less as operators began their pivot from customer acquisition to customer retention. But if the first month is any indication of how sports wagering in 2023 will go in the U.S., the smart money may be on the house to continue its roll.