Abstract

The relationship between legal contents/practices and the development of casino tourism in Macao (or Macau) is deconstructed through an institutional analysis. Specifically, the role and impacts of the Macanese legal system in the advancement of casino tourism, evolution of the industrial organization and business routines in its modern history, and the dramatic expansion of the industry in the first two decades of the twenty-first century, are elucidated. It is found that a lagging legal and regulatory environment actually constitutes as an essential but controversial basis for a series of unorthodox business activities, which is exacerbated by a group of particular gaming agents. Nevertheless, their business practices have clearly diverted Macao from the public vision of the city as a world-class casino tourism destination. Thus, the MSAR government has made profound revisions and promulgated a new version of gaming laws in 2022 for the retendering of new gaming concessions. An investigation into the contents of these new laws and the related documents shows that while the long-established business practices of this industry which have been dominated by gaming agents will come to an end, new business routines will be subsequently instituted for sustained growth. To conclude, positive actions taken by the industry to comply with the new gaming laws and effective enforcement of these laws by the government will revert casino tourism in Macao back to a sustainable trajectory of development.

INTRODUCTION

After years of conducting an in-depth review, and consulting and communicating with the industry, 1 the Macao Special Administrative Region (MSAR) government of China finally approved a new version of its Gaming Law (Law No. 7/2022 Legal Regime for Operations of Casino Games of Fortune, 2 hereinafter “Gaming Law 2022”) in June 2022. Gaming Law 2022 provided a set of new and radical criteria for integrated resort operators to retender six 10-year new casino gaming concessions (i.e., casino gaming licenses) effective January 1, 2023. Furthermore, to further normalize the business scope and activities of the primary stakeholders (namely the casino concessionaries, gaming agents, collaborators and management firms) in related gaming businesses, a new and comprehensive law (Law No. 16/2022 Business Regime for Operations of Casino Games of Fortune, 3 hereinafter “Business Regime 2022”) was promulgated in December 2022.

Under these new laws, some of the major conventional business routines associated with casino gaming in Macao will substantially change; of particular significance is the removal of the third-party operated VIP gambling rooms. Nevertheless, while it is anticipated that the performance of casino gaming in Macao as measured by the reported gross gaming revenue (GGR) will decline, the changes that are outlined in Gaming Law 2022 and Business Regime 2022 may actually lead to a more effective relationship between the gaming and non-gaming tourism segments, hence reinstating the status of Macao as a world-class casino tourism destination. 4 In addition, as a tourism-based mini-economy, the government emphasizes that the reform of the casino gaming sector and its interrelationship with tourism through the new gaming laws will generate positive feedback that sustains the social and economic wellbeing of Macao as a whole.

An institutional paradigm is formulated in this study to investigate the forces that are at play which have not only compelled the need for the MSAR government to revisit and revise its gaming laws, but forced its hand to do so, and most importantly, the impacts of the laws and practices of the legal system in Macao on the modern development of its casino tourism and economy. Overall, the analytical framework of this paradigm is constructed with reference to a few key studies in the literature which offer some common factors to clarify the impacts of the law on the development in general and casino gaming and tourism specifically.

Recently, studies on the impacts of law on social and economic development at the macro level have gained increasing attention in the academia. Lee (2017, 418–419) 5 proposes a general theory of law and development which states that the development of a society and its economy/industries is influenced by the “regulatory impact mechanisms” of law. These “are comprised of three categorical elements: ‘regulatory design,’ ‘regulatory compliance,’ and ‘quality of implementation’, as well as additional sub-elements” which include “anticipated policy outcome; organization of law, legal frameworks, and institutions (LFIs); …general and specific regulatory compliances” and so on and so forth.

At the meso (industrial) and micro (individual) levels, the importance and impact of laws and practices of a legal system on industrial organizations and development, and behavior of market participants have long been common topics explored in socially controversial industries like casino gaming and their interplay with associated industries like tourism. For example, Eadington (1999, 175) 6 explicates that the promulgation of the Corporate Gaming Act in 1969 by the Nevada government generated a new “legal climate for American casinos” to increase their business integrity and efficiency after “permitting publicly traded corporations to hold gambling licenses.” In a recent study on the development of Midwest gaming, Aronovitz (2022, 189) 7 underlines the importance of “(1) determining public policy, (2) defining goals, and (3) implementing legislation” for jurisdictions to incorporate integrity and fairness, and hence the desired path of development of commercial gaming. 8

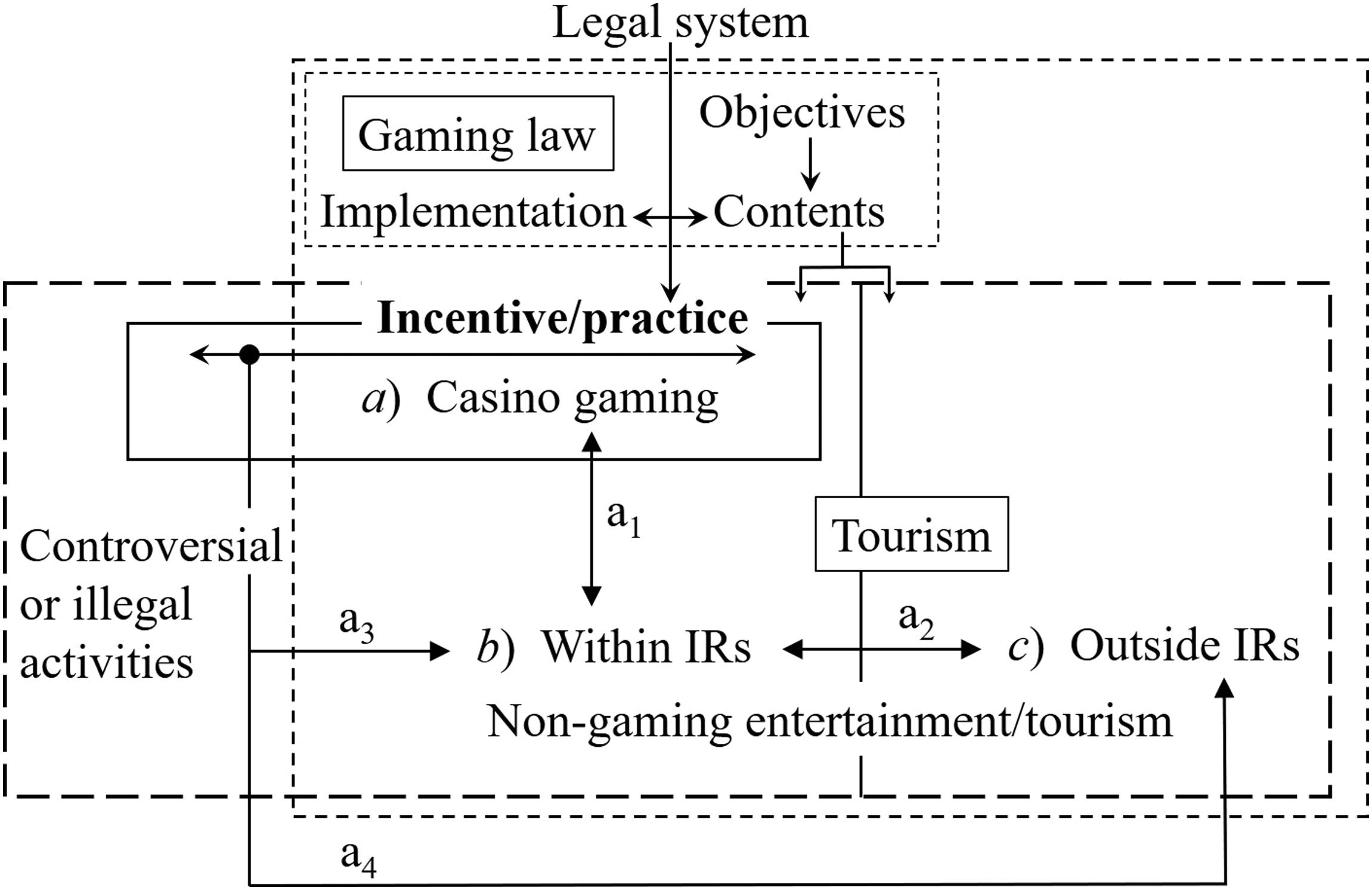

It is evident that the elements and approaches presented by Lee (2017), Eadington (1999) and Aronovitz (2022) share a common ground. Specifically, the impacts from the design/contents of laws and their implementation on the incentive/reactions of the market participants are argued as the crucial (although not the only) factors that bring about the path of development of an industry and its interrelationship with the economy. By referring to these studies in the literature, an institutional paradigm is formulated (as shown in Fig. 1) to reveal the evolution and modern development of casino tourism in different destinations. Based on the analytical framework of this paradigm, the impacts of gaming laws and legal system practices on the modern development of casino tourism in Macao and its dramatic changes in the first two decades of the twenty-first century are explicated in a pragmatic manner, the dynamics of which have led to the critical revisions of the gaming laws and the prospects of the industry afterwards.

Impact of gaming law and legal system on the development of casino tourism

In view of the fact that casino gaming (a in Fig. 1) is a socially controversial business sector, clear objectives and specific (non-ambiguous) contents specified in the gaming law are necessary to minimize its potential downsides and facilitate its interrelationship with tourism development in a destination. These objectives and legal contents will outline public interest towards the contributions expected of gaming firms through non-gaming facilities that are situated within their properties like the integrated resorts (IRs; i.e., the interrelationship between a and b through a1 in Fig. 1), and the requirements to do so, as well as possible joint developments between their properties and the local tourism sectors (i.e., the interrelationship between b and c through a2 in Fig. 1). However, the ultimate impacts of the law on the development of casino tourism as a whole are largely determined by the attributes of the legal system (see top of Fig. 1) through the specific contents of the designed laws and implementation methods.

Actually, the impacts are understood through their influences on the incentive of market participants and hence their businesses practices in compliance with the laws (“incentive/practice” in Fig. 1). Thus, any drawbacks in a legal system (e.g., outdated laws and poor implementation) may drive market participants to resort to controversial or even illegal business activities for greater monetary returns through casino gaming (see left side of Fig. 1), which will have adverse impacts (see a3 and a4 in Fig. 1) and undermine the sustained development of the destination.

Based on the institutional paradigm in Fig. 1, the particular roles of the gaming laws (and regulations) in Macao and its legal system practices which are responsible for the controversial growth and development of its casino tourism from 1960 to 2000, and 2000 to 2020, are explored in the next section.

With reference to the identified facts, the major areas that the MSAR government needs to address to revise its gaming law/regulations in order to realize a desired and sustained path of development for its casino tourism in the years ahead are discussed in the third section. This also includes a detailed analysis of the key contents of the new laws. In the fourth section, the possible impacts of the new laws on the organization and business routines of the industry, including the interplay between the gaming and non-gaming sectors within the IRs, and between the IRs and local tourism in the coming decade will be explored. To conclude, the crucial roles/impacts of the gaming laws and legal system of Macao in the progress of its casino tourism are recapped. The findings and arguments presented in this study emphasize that the prospects of the changes and some ongoing concerns under the particular contextual settings of Macao may still rely on the effective implementation of the new laws.

IMPACTS OF GAMING LAWS AND LEGAL SYSTEM OF MACAO ON PROGRESS OF ITS CASINO TOURISM

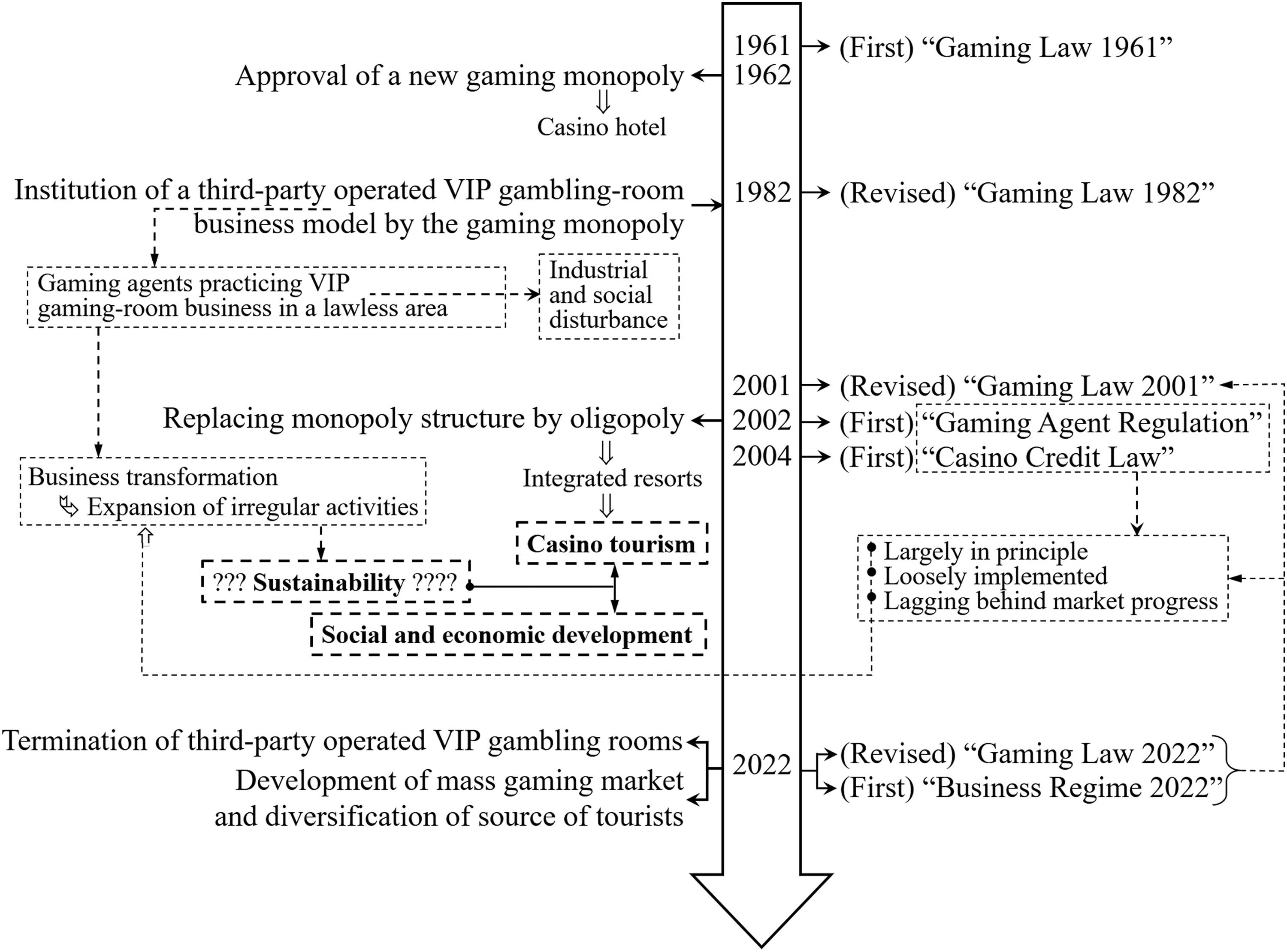

From an evolutionary perspective, the progress of casino tourism in Macao may not simply reflect the automaticity of market forces. Rather, the path of development of the industry (including the business organization of casino gaming and its interrelationship with tourism) is, to a large extent, contingent on the contents of the gaming laws and their revisions following any critical changes in public interest. 9 Moreover, business routines and their changes over time are actually incentivized and embodied by the interplay between the market participants and the practices/implementations of the related laws and regulations in the legal system of Macao (as a particular case to illustrate the “incentive/practice” process in Fig. 1). These impacts and interplays can be recapped as four major periods (see right of Fig. 2).

Law and legal system in Macao and progress of casino gaming/tourism sector

First gaming law (1961) and its revision (1982)

Although the Macao-Portuguese government formally approved gambling as a legal business in Macao in 1847, the first gaming law 10 was only released in 1961 (hereinafter “Gaming Law 1961”). 11 Under Articles 5 and 10 of Gaming Law 1961, the government specified that the criteria to evaluate and approve a tender for gaming concessions included its potential contributions to the development of the city and tourism. The promulgation of this law actually contributed as a key factor from the legislative side to realize the success of the best-known company in the history of the casino gaming industry in Macao, the Sociedade de Turismo e Diversões de Macau (STDM), 12 in obtaining its gaming license in 1962 as a new gaming monopoly and embarking on a new chapter of the modern development of the casino tourism in Macao (i.e., the first period on the top left of Fig. 2). This included the opening of a landmark casino hotel, the Hotel Lisboa 13 in 1970 and the various infrastructure investments to enhance tourism capacity and facilities like a ferry terminal to increase efficiency with tourist arrivals from the neighboring regions, especially Hong Kong. 14

Despite the upsides, the progress of casino tourism in the 1960s and 1970s was indeed limited by the social, political and economic environments both internally and externally. 15 Then, in the 1980s, the industrial organization and business routines underwent critical changes following the promulgation of a revised gaming law in 1982 16 (hereinafter “Gaming Law 1982”). A new article was added in Gaming Law 1982 which conveyed the message that the government may consider replacement of the existing monopoly structure of the industry by approving a maximum of three gaming licenses. 17 Nevertheless, Gaming Law 1982 also stated that the government reserves the right to extend an existing monopoly license if a proposal is submitted by the incumbent. 18

Subsequent to this revision, a crucial and controversial third-party operated VIP gambling-room business model was instituted to promote business turnover (see left of “1982” in Fig. 2) while the STDM took the initiative to maintain its monopoly position by increasing tax payments to the government and subsequently, contributions to the economy and society. However, note that no supplementary regulation was written to update the contents of Gaming Law 1982 to monitor the adverse impacts that explicitly accumulated over time although ambiguous activities (including the participation of triad gangsters as a special group of gambling-room operators and their associated gaming agents, and the flow of questionable funds) largely dominated the practices and expansion of this third-party operated business segment.

Also, the under-supply of casino tourism in the Asian markets in the 1980s and 1990s meant that the expansion of questionable business activities in the lagging regulatory environment, or even the lawless areas, contributed to the snowball effect from the practices of the gaming agents who wrestled for the monetary benefits associated with the VIP gambling rooms. This ultimately led to the spiraling industry and social chaos in the second half of the 1990s (i.e., the adverse impacts (through a3 and a4 in Fig. 1) on both the industry and tourism of Macao spread). 19 Thus, these conflicts actually triggered the MSAR government to review the appropriateness of maintaining a monopoly structure for the industry and revise its gaming law accordingly. To do so, a crucial task awaited the MSAR government in the revision of Gaming Law 1982. The revision was to improve the reputation of the industry and provide new incentives to the industry to reconstruct Macao as a competitive casino tourism destination in the long run.

Gaming Law 2001 and end of gaming monopoly

Following the establishment of the MSAR of China at the end of 1999 and facing the social and economic problems associated with the gaming industry (which also had adverse impacts on tourism development), the MSAR government made the critical decision to end the monopoly structure of its gaming industry upon the expiration of the concession held by the STDM in 2001. To do so, the government amended Gaming Law 1982 and promulgated a new version of the gaming law 20 (hereinafter “Gaming Law 2001”, as indicated in the third period in Fig. 2). In this version, some ambiguous and obsolete articles in Gaming Law 1982 like Articles 5 and 27 were revised or removed, and requirements for new casino gaming concessionaries to contribute to tourism and economic development in Macao were reinforced (note that the expected contributions from a casino concessionary to tourism and economy in Macao as specified in Articles 5 and 10 in Gaming Law 1961 were left out in Gaming Law 1982). In addition, the practice of gaming agents was for the first time, covered in Gaming Law 2001. 21

Gaming Law 2001 formally replaced the monopoly structure of casino gaming with an oligopoly in 2002. Through an international tendering process, world-renowned mega casino resorts like the Wynn Resort and Las Vegas Sands obtained the right to carry out business in Macao. Therefrom, casino tourism in Macao began its evolution through an IR model in which large-scale and different non-gaming attractions, facilities and entertainment were fashioned as primary attractions to encourage tourist arrivals. Nonetheless, the extensive investment of IR operators in non-gaming attractions was indeed largely financed by the considerable income from casino gaming, primarily derived from the spending of Chinese patrons. In the process, the loosely-enforced and lagging legal system under the particular settings in Macao undoubtedly helped to facilitate the transition of third-party operated businesses in their pursuit of larger (but controversial) business turnovers from casino gaming.

Legal system and dramatic industry changes

In congruence with the crucial structural changes of the industry in 2002, new laws and regulations were also promulgated by the MSAR government in their attempts to monitor the new development mode of the industry. Mainly, Administrative Regulation No. 6/2002, 22 hereinafter “Gaming Agent Regulation 2002” was released in 2002 to regulate the qualifications and businesses of gaming agents, and Law No. 5/2004, 23 hereinafter “Casino Credit Law 2004” was issued in 2004 to manage the practices of gaming credits. Judging from the legislative motivation, the introduction of this new law and regulation unarguably represents the intention of the government to address the regulatory gap where gaming-agent business activities (including gaming credits) had been practiced in a lawless area in the 1980s and 1990s.

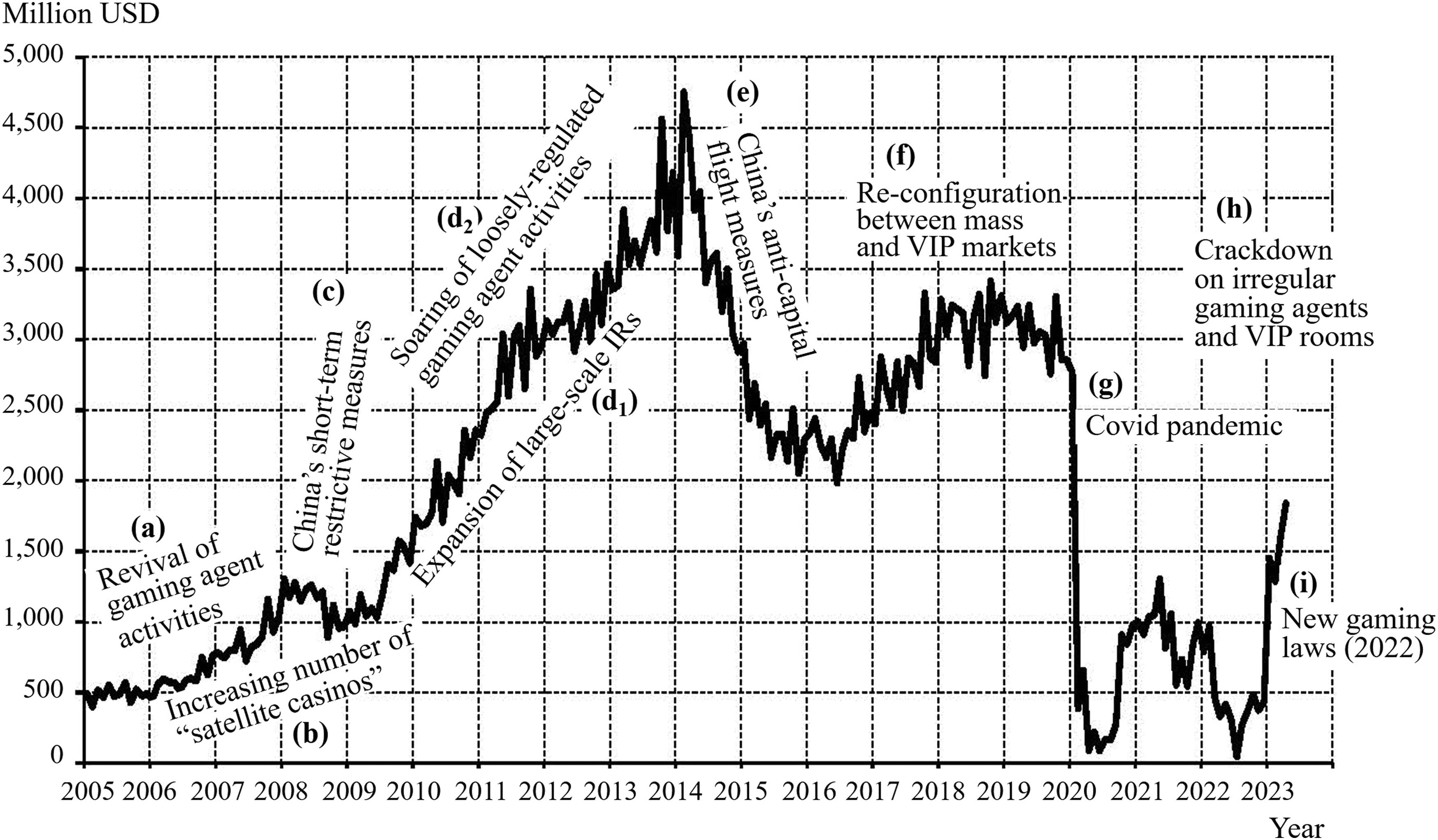

Nevertheless, while the traditions and practices of the legal system in Macao might have largely emphasized on principles, their enforcement was inadequate to counter the possible downsides and rapid transformation of business activities associated with the gaming agents and third-party operated VIP gambling rooms. 24 Thus, opportunities could always be found by the market participants to carry out their businesses in some legal grey areas, which required law/regulations to evolve so that controversial business activities introduced by the gaming agents could be monitored. However, these changes by the government might not be timely enough. Thus, traditional and controversial gaming-agent business activities and VIP gambling rooms were leading the way in the transformation and expansion of the industry since 2006, which contributed to the rising GGR of the industry (as shown in (a) in Fig. 3).

Factors responsible for dramatic changes in monthly GGR (2005.01–2023.04) of Macao

In addition, the MSAR government also exercised its administrative authority shortly after the formal approval of the three gaming licenses in 2002 by granting the right to a major shareholder of each of the three gaming license holders to initiate their IR business respectively. Despite the controversy of this decision (as it was not covered in Gaming Law 2001), this actually led to a dramatic change which saw over a twofold increase in the scale of the casino gaming industry thereafter from doubling the three licenses (under the original approvals given to SJM Holdings, Wynn, and Galaxy JV) to six independent IR operators (i.e., SJM-MGM, Wynn-Melco, and Galaxy-Las Vegas Sands). 25

Following this change, it can also be observed that the number of individually operated casino hotels under the formal gaming licenses of some of the operators expanded in 2006. In Macao, these individually or third-party operated casino hotels (instead of individual VIP gambling rooms within the property of a casino concessionary) are commonly called “satellite casinos” (of a gaming license holder), which were also not directly covered in Gaming Law 2001 or other related laws and regulations. 26 In practice, these “satellite casinos” and their VIP gambling rooms also greatly rely on connections with gaming agents, and their loosely-regulated business contributes to the increasing GGR as reported by the industry (shown in (b) of Fig. 3).

Owing to the revival of gaming agent activities and expansion of “satellite casinos” and VIP gambling rooms between 2006 and 2008, the number of questionable business activities also increased, 27 which prompted the Chinese government to produce counter policies like restricting the number of travel visas of the Mainland Chinese to Macao and limiting gaming agent activities in Mainland China. Thus, the GGR of the industry exhibited a short downturn in the second half of 2008 (shown in (c) of Fig. 3). Yet, the response of the Chinese government to the onset of the global financial crisis in 2007/2008 by stimulating its local economy actually provided opportunities for gaming agents to take advantage of the regulatory loopholes in both Mainland China and Macao to resume and actively expand their business. As the industry benefited at the same time from the opening of attractive IR accommodations and entertainment facilities (exhibited in (d1) in Fig. 3), the lagging legal system and loosely-regulated gaming agent activities pushed the GGR dramatically upwards between mid-2009 and early 2014 (shown in (d2) in Fig. 3).

As for the dramatic increase in the GGR of Macao between 2009 and 2013, it is largely suspected that a significant portion of the gambling funds that flowed from Mainland China to Macao was associated with the capital flight from China following its expansionary economic policies to stimulate the economy in 2008/2009. 28 During this process, the loosely-regulated gaming agents indeed played an essential role in approaching the high income (VIP) group in Mainland China to take advantage of their fondness for gambling and extravagant lifestyle, as well as facilitating questionable/illegal flows of funds. Actually, the particular role of these “loosely-regulated gaming promoters” and the increasing GGR of Macao was for the first time highlighted in the 2011 Money Laundering and Financial Crimes report by the USA government. The report suspected that the gaming agents “profit from sourcing the majority of Macau's VIP players who contribute to over 80 percent of gaming revenues.” 29 Money Laundering and Financial Crimes 2016 further stressed that in Macao, the “gaming industry relies on loosely-regulated gaming promoters …” who actually encourage “Chinese capital flight …”. 30

However, the sustainability of these gaming-agent activities might have indeed depended on the tolerance of both the Chinese central and Macao SAR governments. In a legal system like Macao where the contents of laws/regulations and their enforcement lag behind the requirements to check the unfavorable impacts that stem from legal grey areas, direct administrative interventions have always been the last resort taken by the governments to manage unchecked market behaviors. As shown in (e) in Fig. 3, the gaming industry in Macao slumped in early 2014 right after the Chinese government launched its nationwide anti-corruption and anti-extravagant policies, among which anti-capital flight measures were a major component and strictly implemented. 31 Pressed and incentivized at the same time by the explicit actions of the Chinese central government, it is obvious that the MSAR government was also actively strengthening the enforcement of the related laws/regulations like those in checking the flow of funds which were channeled by the gaming agents and their monetary activities in the community. 32

Following the extensive overhauling of the industry from early 2014 to mid-2016, the market started to re-configurate the proportion of its mass and VIP segments between mid-2016 and 2019 (see (f) in Fig. 3). In this phase, the gaming agents were also seeking for any opportunities to reinvent themselves while the MSAR government continued to increase the efficiency of its legal system (especially enforcing laws and regulations). Thus, the recovery of the GGR of the industry in 2017 and 2018 still needed the resurgence of “VIP” revenue to a certain extent (which accounted for over 55% of the GGR). During this critical tug-of-war between the government and gaming agents, the unexpected global outbreak of the COVID-19 virus in 2020 not only led to a three-year meltdown of the industry (see (g) in Fig. 3), but coincided with the expiration of the existing gaming licenses in 2022.

With the wholehearted support of the Chinese government under the “one-country, two-system” policy and the determination to address public interest concerns by rectifying the internal organization of the industry and strive towards sustaining its growth, the MSAR government took serious action to re-institute the ever-transforming third-party operated VIP gambling rooms and “satellite casino” business model which had long been providing a dynamic but hardly supervised environment to many gaming agents so that they can conduct their questionable/irregular business activities on an ongoing basis. The MSAR government formally cracked down on some of the major gaming agents and their associated VIP gambling rooms at the end of 2021 and beginning of 2022 (see (h) in Fig. 3), 33 and completed the revision and promulgated its new gaming laws in 2022 ((i) in Fig. 3) for the retendering of the new gaming licenses which would be effective in 2023.

NEW GAMING LAWS AND RE-INSTITUTION OF THE INDUSTRY

Despite the complexity of the factors that have led to the dramatic changes in the casino gaming industry of Macao between 2002 and 2022 (for e.g., the Chinese government was lenient in the travel measures of Chinese visitors to Macao under the “one-country, two-system” policy, the economic environment was changing in Mainland China, the new IRs of Macao and the rapid expansion in the variety of services and hospitality capacity had a trademark effect, and so on and so forth), the historical facts that are presented in the previous section show the basis of the public concerns at the time, hence providing an understanding of the motivations and objectives of the MSAR government in formulating the new gaming laws and their potential influences on the development of casino tourism in Macao as a whole. In particular, it is evident that to ensure the sustained growth and real progress of Macao as a world-class casino tourism destination upon the expiration of the gaming licenses in 2022, the legal issues that had to be resolved fell into six major areas as summarized in Table 1.

Legal Issues to be Resolved for Furthering Casino Tourism in Macao

With the need to improve the structure and enforceability of the laws and regulatory system, the changes were evidently accelerated by the national plan of the Chinese government to develop the Guangdong-Hong Kong-Macao Greater Bay Area (hereinafter Greater Bay Area) in 2019, 34 in which Macao was to be developed as a core city. Accordingly, the need for Macao to improve its diversity of industry structure and competitiveness in the long term had to be addressed right away. This implied that the normalization of the gaming industry under a business routine of a loosely-regulated third-party operating model (especially the questionable business activities associated with gaming agents, VIP gambling rooms and “satellite casinos”) might hardly be tolerated under the anticipated new path of development of Macao. To this, legal issues 2 to 5 in Table 1 had to be resolved with extreme measures, which might indeed facilitate the improvement of the last legal issue (in Table 1) for the long-term development of casino tourism in Macao.

Structure and key elements embedded in the new gaming laws

As aforementioned, the key drawbacks associated with the gaming laws and regulations mainly shown by their inability to manage the rapid changes in the organization of businesses in the industry, as well as the poor implementation of various laws/regulations to monitor controversial (or even illegal) business activities, perpetuated over time. Thus, during the revisions, the MSAR government clearly admitted that Gaming Law 2001 “has been implemented for about 20 years since it is put into effect. There are deficiencies and lags in both the practice of the law and monitoring of the gaming industry.

For these reasons, it is necessary to make timely review and revision.” 35 This led to the promulgation of the new laws in 2022 (as shown in the latest period in Fig. 2). Based on the consensus derived from a public consultation process in September and October 2021, the MSAR government increased the maximum number of gaming licenses from three to six. 36 This revision not only removed the ambiguity around the legal status of the overall structure of the industry, but was indeed in line with societal expectations to minimize the possible adverse impacts if the established scale of the industry has to be reverted back (say, by approving less than six operators to continue IR businesses under the new licensing scheme).

As for the core of the legal issues (i.e., legal issues 2 to 5 in Table 1), they were seen largely to have been resolved through the comprehensive revisions of Gaming Law 2001 (see contents of Gaming Law 2022) and further supported with the replacement of Gaming Agent Regulation 2002 with a new law called Business Regime 2022. As compared to the previous versions, it is obvious that while the goals and design of the new laws are more specific, their enforceability is also enhanced with the inclusion of more detailed statements in the contents. To start off, the first objective specified in Gaming Law 2022 to regulate the practice of casino gaming is to ensure that operations will be under the “presupposition of protecting the security of the country and the Macao Special Administrative Region.” 37 Based on this unique standpoint, it is evident that the revised and newly designed articles would be better justified and enforced.

For instance, aside from gaming license holders, others who are regulated like gaming agents and their collaborators are clearly defined in Gaming Law 2022. Then, detailed regulations for monitoring purposes are further specified in Business Regime 2022. In addition, the business model had to be revised so that under the new laws, the “satellite casinos” 38 are categorized under the definition of “management firms” to address the legitimacy and regulatory issues with the gaming license holders. In addition, joint liability between the gaming license holders and their business partners like gaming agents and the management firms are clearly specified. 39 These new articles undoubtedly aim to close the regulatory loopholes for the problematic business activities of the various third parties in the past. Moreover, some of the new articles introduced in various sections of Gaming Law 2022 increase the power of the regulatory authorities (e.g., the Gaming Inspection and Coordination Bureau) to oversee the practices of the gaming industry over time, and provide advice to the government in relation to any particular actions that should be directly taken to investigate suspected or actual shady activities.

Resolving the complexities of third-party operated businesses

With respect to the contents of the new gaming laws, the intricate relationships among the gaming license holders, VIP gambling room and “satellite casino” operators, and gaming agents and their collaborators of different levels have been reasonably resolved. The rights and responsibilities of these entities in casino gaming are clearly defined and not left for interpretation. First, the law clearly identifies that it is the responsibility of the gaming concessionaries to ensure the business integrity of their employed gaming agents to promote their gaming business. 40 To enhance monitoring, the gaming concessionaries are responsible for reporting any potential problems (e.g., financial and credit repayment issues) and illicit activities of their gaming agents to the Gaming Inspection and Coordination Bureau (Direcção de Inspecção e Coordenação de Jogos (DICJ)) within five days. 41 In other words, under Gaming Law 2022, the business practices of the gaming agents are no longer “independent” from those of the gaming license holders.

More critically, gaming agents can only offer their intermediary business services to one licensed gaming firm effective January 1, 2023. 42 Furthermore, gaming agents can only receive an approved scheme of commission with an upper limit from a casino licensed firm to which they provide the services. 43 To this, gaming agents will no longer be permitted to share the GGR with the casinos in any shape or form, and their business activities will be subjected to more scrutiny. In addition, the new regulations also apply to the collaborators of the gaming agents. 44 This change means that not only is the relationship between the gaming license holders and gaming agents clarified, but the decades-long third-party operated gambling room business model has effectively been terminated (see bottom left of Fig. 2).

As for the “satellite casinos”, after taking into consideration of their actual relationships with the local economy (e.g., employment and business networks with the local non-gaming tourism sectors like retail and restaurants), the MSAR government has decided to let them either phase out or transform into management firms of the gaming license holders during a three-year transition period from 2023 to 2025. Consequently, 11 of a total of 20 “satellite casinos” that were still operating in 2022 have received approval to continue operations in 2023 under the new gaming licenses. 45 During the transition period, their business practices (especially those that involve the gaming agents) are subjected to the new gaming laws, 46 although they may still be allowed to retain their GGR sharing model with the gaming license holders. In 2026, those who choose to transition to a business model of a management firm will only be allowed to receive an annual management fee 47 rather than receiving a share of the GGR or commission of any form through the gaming business.

Business Regime 2022 states that the framework of this new law is to stipulate “the specifications for the businesses engaged by the concessionaries, gaming agents, collaborators, and management firms” 48 as provided in Gaming Law 2022. Aside from replacing the Gaming Agent Regulation 2002, the scope and details of this new law are apparently more comprehensive and enforceable. Apart from listing the general requirements for qualification, financial power, licensing, etc., an individual chapter 49 with seven articles specifies the legal responsibilities of the four entities and their joint liabilities when conducting their business.

Though these legal provisions, the transparency of the business activities of the various parties (especially the gaming agents) will not only be enhanced, but a self-monitoring mechanism is also introduced by specifying their joint liability, which clearly reinforces the regulatory power of the government to supervise the practices and integrity of the industry. A major reason is that under this new law, a business entity like the casino license holder or its management firms or gaming agents cannot avoid charges by simply claiming that a suspected or actual illegal business activity (e.g., flight of capital funds or illegal gaming credits) is performed/arranged by an independent third party.

Based on the structure and contents of the new gaming laws, it is reasonable to infer that the adverse impacts brought about from the business routines of loosely-regulated gaming agents under the shelter of third-party operated VIP gambling rooms and “satellite casinos” will be prevented. These pivotal changes will obviously redefine the path of development of the gaming industry from “VIP”-oriented towards the mass market with less dependence on the decades-long controversial third-party operated businesses.

Changing role of the government

As compared to the impact of previous revisions of the gaming laws on the paths of development of the industry (in particular, the three periods of the 1960s–1970s, 1980s–1990s, and 2000s–2010s as indicated in Fig. 2), the role of the government in the new gaming laws in driving the changes in the organization and business routines of the gaming industry and its interrelationship with tourism is clearly different. On top of the aforementioned amendments in the contents of the laws, it is clear that the government has taken a more active role to enforce these new laws in monitoring the practices of the gaming industry, rather than allowing the market participants to circumvent the rules. The government is also preventing the revival of illicit business activities in different forms and shapes. To a large extent, the authority of the government in enforcing these new laws and its discretion to evaluate the eligibility of any newly introduced business activities and proposed changes in the industry are amplified by the provisions in the new gaming laws. 50

For instance, instead of establishing simple targets or providing general criteria for a ten-year development plan of the industry under the new gaming licenses commencing 2023, the scale of the industry in terms of the approved number of gaming devices like gaming tables and machines are to be reviewed by the government periodically. To adjust the scale of the gaming industry, it is under the law that the government will refer to key factors such as: i) the overall economic situation of the SAR, ii) any revisions in the policy for the advancement of the gaming industry, iii) the overall situation of the business operations of the gaming firms (including the business performance of their approved gaming devices within a given period of time); and iv) the investment of gaming license holders in non-gaming activities. 51

In addition, the performance of the licensed firms will be reviewed every three years regardless of whether they meet their contracted commitments for their license even though the new gaming licenses are good for ten years. 52 If a gaming license holder is found to have any significant deviations from its commitments, changes need to be made within a given period of time. Moreover, as a measure to effectively monitor the gaming agent activities, the gaming license holders are also required to submit detailed monthly reports of their transactions and commissions paid to the gaming agents. 53

Furthermore, to implement Business Regime 2022, details of the ongoing involvement and role of the government are outlined at the same time. These include an annual review and the right to determine the maximum number of gaming agents that would be approved to the various gaming license holders, 54 monitoring of the business operations which are performed by different legal entities and so on and so forth. Last but not least, the law that specifies the organization and operations of the DICJ is revised 55 to increase its administrative power in implementing the new gaming laws and monitoring the operations of the gaming industry within a wider scope and depth of authority.

In a nutshell, the dramatic progress of casino gaming and tourism in Macao under the IR model (mainly measured by the reported GGR and the corresponding spending of the industry on the development of its non-gaming facilities) in the first two decades of the twenty-first century has impressed world investors. Nevertheless, the sustainability of its performance under the influence and business routines of a group of market participants who are situated in the grey areas of a lagging legal system might be precarious and subjected to the whims of the government as well as revisions of the related laws. Actually, promulgation of the new gaming laws by the MSAR government will demonstrate the launch of dynamic new business routines in a new era that parallels the emerging new social and economic paths of development as a whole in Macao.

NEW ROUTINES AND SUSTAINED PATH OF DEVELOPMENT

Considering the significant business turnovers from the practices of third-party operated VIP gambling rooms which relied heavily on loosely-regulated gaming agents in the past decades, the end of these business operations and activities through the new gaming laws will undoubtedly reduce a considerable share of the industry's GGR. Nevertheless, the implementation of the new gaming laws will incite radical and progressive changes in the business routines of the industry. Actually, the changes will not simply modify the path of development of casino gaming and operations of the IRs, but also have positive effects through word of mouth which promote their long-term interrelationships with local tourism, hence ensuring the sustainability of Macao as a world-class and internationally competitive casino tourism destination.

Transformation of the gaming business

Under a more transparent and regulated operating system as per the new gaming laws, there is no doubt that the traditional VIP-oriented gambling sector will decline. Although VIP gaming businesses directly operated by casino license holders will continue or even expand, their business scale would hardly be comparable with the business turnovers that could be derived from the loosely-regulated third parties. In contrast, development of the mass gaming market will accelerate. At the same time, the approved gaming agents may still continue to promote and manage gaming businesses, but their real influence on advancing the organization and practices of the businesses in the future will decline. In other words, the gaming business under the new laws most likely will transition from a gaming-agent dominant model 56 to an IR-operator dominant model, in which the business strategies formulated directly by the gaming license holders will have a more important role than largely relying on independent gaming agents to attract and approach the patrons.

Among the potential changes, a unique impact of Gaming Law 2022 on the long-term development of the market that should be emphasized is the incentive provided to the gaming operators to cultivate new customer sources. It is specified in the law that if the GGR is derived from overseas/foreign patrons (i.e., those from outside of Mainland China, Hong Kong and Taiwan), 5% of this share of the GGR which has to be allocated to the government for the development of social and cultural affairs in Macao can be exempted. 57 Even though the potential impact of this provision in the short term might not be evident due to the aftermaths of the COVID-19 pandemic (e.g., in 2023 or 2024) since time is needed to normalize international travel (especially air travel), the IR operators have demonstrated that they are motivated to create effective marketing strategies to take advantage of this benefit. 58

While the actual impact from this provision on the gaming business will require time to gauge the effects, it is reasonable to infer that gaming operators would not only modify their gaming facilities for foreign patrons, but also the associated non-gaming facilities in their IRs. Even if the relative scale (both absolute and proportion) of foreign visitors to Mainland Chinese visitors may be small, the singular composition of the games which is specifically based on baccarat (and for a long time, has accounted for 85% to 90% of the GGR,) may gradually evolve. That is, complementary non-gaming entertainment services may also be enhanced to promote gaming activities to foreign patrons.

Fostering new business routines between gaming and non-gaming activities

Based on the objectives and design of the new gaming laws, the MSAR government has moved forward immediately to specify the criteria to evaluate any tenders submitted for the new ten-year gaming concessions. In a formal call for public tendering in July 2022,

59

seven criteria which parallel those in Gaming Law 2022 were explicitly stipulated. On top of considering the casino operation experience of the bidding firm, its management plans, and the proposed premium payment scheme (e.g., based on a business scale determined by the number of gaming devices being operated) to the government, the other four criteria emphasized are:

plans to cultivate overseas customers; potential contributions of both gaming and non-gaming businesses to the overall benefits of the MSAR; monitoring and preventive schemes to curb any illicit activities within the casinos; and proposed sharing of social responsibility (e.g., the promotion of job opportunities and development of the local workforce),

which are specified in the document as the factors/standards that the government would prioritize when evaluating the eligibility of a tender submitted for the gaming concession.

By setting up these specific policy objectives, the government has thus established a comprehensive and explicit basis to carry out its periodical reviews of the performance of the gaming operators as stated in Gaming Law 2022. 60 Turning to the standpoint of the industry, it is obvious that to meet the regulatory requirements and commitments that are proposed in the tenders, the business activities that the gaming license holders carry out will most likely foster a progressive environment to advance the efficiency of the interplay between the gaming and non-gaming sectors, rather than retaining the conventional business model where the non-gaming business segment had to rely heavily on funds from the gaming sector. 61

To meet the expectations of the government in the new gaming laws and their tender expectations, the six successful IR operators announced that over 90% of their committed investment (MOP 108.7 billion of a total of MOP 118.8 billion 62 ) as stated in their new gaming concessions would be spent on various non-gaming projects and attracting overseas customers. 63 In practice, the six IR operators will need time to realize their various investment commitments in the non-gaming areas; nevertheless, it is reasonable to anticipate that their pace will pick up over time. In addition, the more active role taken by the MSAR government in evaluating the progress of non-gaming activities, 64 together with the potential recovery in tourist spending after the COVID-19 pandemic, may also ensure that the IR operators will be able to meet (or even exceed) their commitments.

Reinforcing the relationship between the IRs and local tourism

The impact of the dynamics generated from the new gaming laws on critical changes in the business routines of casino gaming may not only lead to changes in the interplay between the gaming and non-gaming business components within the IR properties, but also between the IRs and local tourism sectors in Macao. To align with the government objective to promote “moderate economic diversification and sustained development” 65 through casino gaming practices, all gaming license holders explicitly agree in their new concessions 66 that their non-gaming investments would not only be spent on their own properties, but also on projects that are associated with the development of local tourism. These include organizing sporting events, and promoting community and marine tourism, Macao as a gourmet city, etc.

The announcement of the six IR operators right after they obtained their gaming license of their initial plans in December 2022 shows that while their potential investment projects in the non-gaming tourism areas are consistent with the aforementioned directions (broad categories) as outlined in the gaming licenses, 67 their individual focus may not be the same. The differences may largely represent the different market positions of the individual IR operators. For example, while one operator expressed its plans to become more involved in projects that support the revitalization of the historic districts in Macao, another indicated its desire to invest in both community and marine tourism, while a third emphasized on working with local small and medium enterprises, etc.

Unlike its historical role, which was a more passive one, the MSAR government is assuming an active role in this new era to ensure the implementation of these plans. To this, the IR operators are required to submit reports every year to specify the progress of their related investments and detail their plans for development in the coming year. 68 Thus, a long-term and closer relationship between the IRs and the local tourism sectors are actually facilitated at all levels, the likes of which has never been seen previously in Macao. With more comprehensive and real connections between the IRs and local tourism, and by minimizing the adverse impacts of the casino gaming to non-gaming sectors, the positive effects from feedback as indicated by a2 in Fig. 1 will most likely be strengthened in the long run. Thus, the development of Macao as a world-class casino tourism destination (or a world-class tourism and leisure center) has become a real feasible and enforceable goal.

CONCLUSION AND REMARKS

To conclude, this study reveals that the prototype of casino tourism was established when the development of tourism was first specified in Gaming Law 1961 as one of the criteria of the Macao-Portuguese government in approving a casino gaming concession. Nevertheless, despite the positive impacts from this law on the modern development of the industry and its contributions to the economy of Macao, revisions of the gaming law in 1982 and drawbacks in its regulatory design and implementation (for e.g., while Article 5 in Gaming Law 1982 was never being exercised, the contents of the law were also found lagging in addressing the rapid changes in the market activities even though the legitimacy of the majority of these activities might be questionable and undesirable from a social standpoint) actually created controversial incentives and had adverse impacts on the real progress of the industry and economic society. 69

The introduction and expansion of the third-party operated VIP gambling room business model and practices of gaming agents in the lawless and grey areas of the legal system to pursue more GGR (particularly when casino gaming was under-supplied in the Asian markets) largely undermined the real progress of the tourism sector in the 1980s and 1990s. These changes indeed diverted the path of development of Macao so that the city became simply a gambling city instead of a casino tourism destination.

In congruence with the establishment of the MSAR in 1999, the MSAR government revised its gaming laws again (with a clear inclination to sustain the long-term development of Macao) in the attempt to reinvent Macao as a world-class casino tourism destination. To this, the promulgation of Gaming Law 2001 not only concluded the monopoly structure of the gaming industry, but the government also founded a new legal foundation to approve world-renowned IR operators that would introduce a new business model to advance casino tourism. However, the lagging legal system (in terms of insufficient content and inadequate enforcement of the laws, which included Gaming Agent Regulation 2002 and Casino Credit Law 2004) that was in place to monitor the rapid transition of third-party operated VIP gambling rooms and expansion of controversial gaming-agent business activities that strived to gain direct monetary benefits had evidently threatened the sustainability of the growth of the industry again (e.g., as demonstrated by the comprehensive changes in the industry between 2014 and mid-2016; see Fig. 3).

To resolve the fundamental legal drawbacks and create a sustainable trajectory for the development of casino tourism, the MSAR government took the initiative to revise and promulgate new gaming laws in 2022, which were considered most radical at the outset (i.e., to improve the comprehensiveness of the legal system and gaming laws as shown at the top of Fig. 1). Based on the facts and discussions presented in this article, it is evident that the conspicuous gaming turnovers generated from the third-party operated VIP gambling model will be a thing of the past. Yet, under the new normal (new business routines) that is guided and incentivized by the new gaming laws, the sustainability of casino tourism development in Macao has indeed become much more promising in terms of the overall competitiveness of the industry rather than simply measured by its reported GGR.

Indeed, the more effective interplay between the gaming and non-gaming sectors within the IRs, and their closer interrelationships with the local tourism sectors will generate positive effects through feedback, hence strengthening the sustained development of casino tourism through benefits from both internal and external economies of scale. In other words, the positive impacts derived through a1 and a2 in Fig. 1 will be reinforced; and along the same line of thought, the possible adverse impacts through a3 and a4 will be largely inhibited so that a sustainable path of development for the industry will be realized.

Although the reported GGR of the industry will be reduced immediately with the termination of the third-party operated gaming businesses, this is actually an irrelevant concern under the changing public interests which are clearly revealed in the new gaming laws. Besides, the real impact on the IRs is indeed lower than the loss of the third parties as a whole and the immediate reduction in government tax revenue. 70 By cultivating a more sustainable path of development and new business routines, however, it is feasible for IR operators to replenish the loss of their GGR through business growth over time. 71

Nevertheless, it is important to emphasize that despite the upsides from the new gaming laws, their ultimate impacts on the success of Macao in its transformation into a world-class casino tourism destination still largely rely on the continuous and effective implementation of the laws by the government. These definitely require timely and direct actions taken by the government if the market exhibits any significant deviations from the objectives that have been specified in the new gaming laws. Considering that the legal system in Macao evolved from the Portuguese civil law system and historical experiences during the progression of its casino tourism (especially the incentive of some gaming agents to search for any possible opportunities to transform their legally questionable business activities), exercising the executive power of the government effectively and proactively under the new gaming laws is indeed necessary to ensure that casino tourism will develop in a sustainable manner.

Lastly, it is worth emphasizing that the evidence and analyses presented in this article actually constitute as a valuable case to reinforce current understanding of the specific arguments raised by Aronovitz (2022), Eadington (1999) and Lee (2017), 72 as well as similar studies in the literature on the importance of legal design/contents and impact from them, as well as the quality of the implementation of law on development. Their arguments are specifically employed to formulate the analytical framework for this study as depicted in Fig. 1.

For a socially controversial industry like casino tourism, it is evident that its industrial organization, business routines and path of development are largely, although not solely, contingent on the design/contents and quality of implementation of the gaming laws within the legal system like in the case of Macao. During the process, the impacts are largely embodied in the incentives and actual behavior of the market participants in carrying out their business activities and formulating business routines. This simple but pivotal impact of the law on development indeed provides a realistic basis and can be extended to evaluate and explicate the business organization and performance of casino tourism and their changes in different destinations.