Abstract

Executive Summary

Introduction

The field of green chemistry emerged from the interaction of industry, government, and academia in the early 1990s. One key milestone was the passage in the United States of the Pollution Prevention Act of 1990, which sought to broaden the focus of regulation from cleaning up pollution that had already been emitted to changing industrial practices and processes to prevent or minimize the creation of pollution. In 1991, the U.S. Environmental Protection Agency (EPA) declared the elimination of pollution at its source as one of its objectives.

Editors Note:

The above text is a reprint of the Executive Summary of a report prepared by Pike Research (2Q2011;

Perhaps the most challenging aspect of assessing the green chemistry industry is that green chemistry is less a description of a discrete industrial segment than it is a way of carrying out industrial activity, from design to manufacturing. As an end-to-end process, green chemistry includes the following elements: • Modifications to chemistry and chemical engineering educational curricula • Choices of chemical feedstocks and process design • Awareness and use of the information and tools that are available • Integration and firm anchoring in existing and proposed regulatory regimes

For the purposes of this report, Pike Research has narrowed the major themes of green chemistry to the following: • Waste minimization in the chemical production process • Replacement of existing products with less toxic alternatives • A shift to renewable (non-petroleum) feedstocks

These themes are reflected in three major market segments: • A segment centered on process improvements in conventional chemical synthesis • A segment featuring chemical formulators • A particularly dynamic (but still nascent) segment focused on chemical manufacturing

The Value of Green Chemistry

The worldwide chemical industry is valued at approximately $3 trillion. Thus, even small improvements in efficiency can have a very large absolute impact. The greatest opportunity for near-term positive financial and environmental impact comes from waste minimizing improvements to existing, conventional chemical production processes. Pike Research estimates that it is possible to capture over $40 billion in process cost savings and avoided environmental and social liabilities just by bringing laggard companies up to the baseline standard of the chemical industry as a whole.

One of the core tenets of green chemistry is the minimization of waste. In this sense, the opportunity for process improvements through the application of green chemistry is reminiscent of the lean production imperative to drive waste out of discrete manufacturing processes that has helped to transform the automobile (and other) industries. Certainly, green chemistry typically represents a significant source of cost savings. In contrast to the consumer market, where we are trained to pay a premium for green products, greener is cheaper in industry.

On the consumer (e.g., household cleaning chemicals) side, a number of large public companies have recently introduced overtly green brands into a market formerly dominated by small, closely held companies. For example, The Clorox Company's Green Works brand, introduced in December 2007, has grown rapidly and is estimated to now generate approximately $200 million per year in revenue for the company. Moreover, this growth appears to be the result of taking share from conventional chemical preparations, rather than existing boutique green product lines such as Seventh Generation.

Evolution of the Green Chemical Market

There has been a great deal of activity in the development of renewable feedstocks for a wide range of chemical processes, both replacements for commonly used “merchant molecules” and new compounds with interesting and commercially valuable properties. Claimed advantages for renewable feedstocks over conventional derivations from petroleum include lower greenhouse gas emissions, reduced toxicity, and lower costs. Most renewable feedstocks are produced through biological processes (primarily fermentation of plant sugars into the desired compounds or their intermediates) or thermal and chemical processes applied to cellulosic materials such as wood, agricultural waste, or non-food plants like switchgrass.

The evolution of the green chemical market is being driven by a combination of technical, regulatory, consumer preference, and economic factors. Improved chemical screening technology and advances in the science of mechanistic toxicology have improved our understanding of the effects of manmade chemicals on humans, animals, and the environment. The rapid advances in biotechnology achieved over the last several decades have created powerful, new toolkits for the manipulation of organisms (bacteria, yeasts, and algae) such that they produce industrially useful compounds with great efficiency and minimal waste.

While regulatory regimes at the federal level in the United States do not appear likely to become increasingly stringent soon, several states have imposed strict new regulations on hazardous chemicals, as has the European Union. Consumers are becoming increasingly aware of the potential effects of the chemicals used to produce common materials (recall the BPA controversy of recent years) and are demanding green alternatives. Companies are being forced to meet not only end-user demand, but also the demands of powerful retailers, which can dictate product specifications to their suppliers by virtue of their vast sales. Finally, the rising (and highly volatile) price of petroleum – crucial both as a source of process energy and as a feedstock for many chemical processes – is driving interest (and investment) in finding alternative, renewable feedstocks for key chemical products and intermediates.

Competitive Landscape

Green chemical industry players run the gamut from vast multinationals that have been in operation for over a century to tiny startups. Much of the biobased segment, which perhaps has the greatest long-term potential to revolutionize the chemical industry, is nascent. Technologies are just a few steps beyond the laboratory and production facilities are a few years from reaching their modest full production levels. The biobased segment of the market excluding biofuels is liable to grow slowly over the next few years. Issues of scale are never simple. Also, in the chemicals and materials business, the adoption cycle often requires long lags for extensive customer testing before new products are introduced.

As is the case with many nascent markets, the green chemical market will grow through several clearly defined stages: a profusion of small companies based on exciting technologies will gradually coalesce (through failures, acquisitions, and mergers) into a functioning ecosystem. Many of these small companies will choose to follow a model that is common in the biotechnology industry, whereby small, innovative companies partner with industry incumbents to obtain capital and distribution channels. Established companies have the luxury of choice. They can either establish their own green operations, or watch the startups as they develop and acquire those that are the best fit for their own businesses once some of the technology and market risk has been wrung out.

Market Forecast

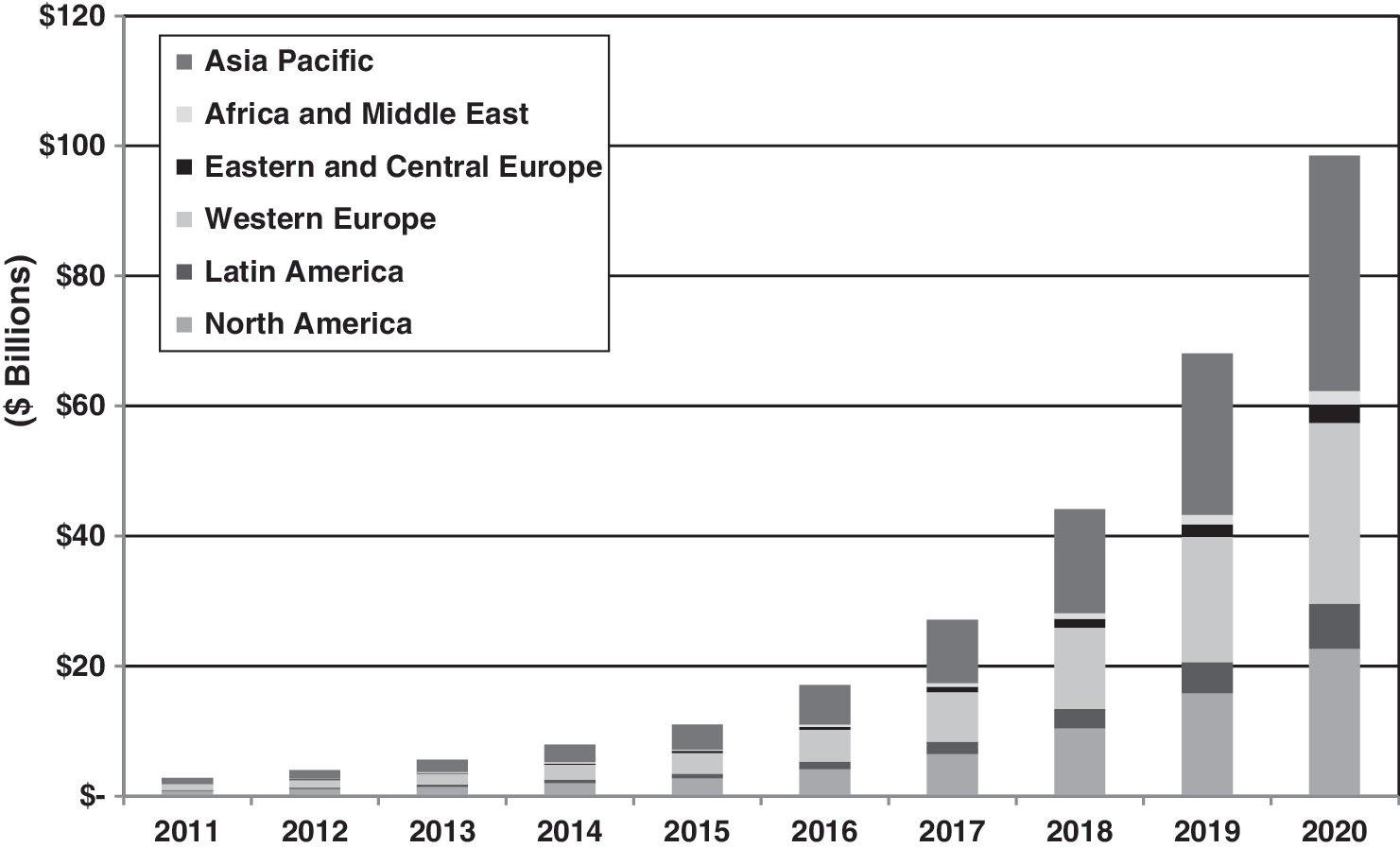

Pike Research estimates the current size of the green chemical industry at approximately $2.8 billion worldwide. It will likely grow to about $11.0 billion in 2015 and nearly $100 billion in 2020. These estimates could be dramatically affected to the downside by another significant reversal in the world economy, or to the upside by prolonged, dramatic increases in the price of petroleum. Figure 1 graphically illustrates the size and growth of this market by geographic region.

Green chemical market by region, World Markets: 2011–2020.