Abstract

The green chemistry market is currently valued at around $3 billion according to Pike Research estimates, and our forecasts show a 5-fold increase in value is likely to occur by mid-decade. Substantial durable demand points to significant value potential over the longer term as well. Broad market drivers include a trend towards sustainability in the industrial sector, technological advances, regulations impacting industrial processes and toxic chemicals, shifting consumer sentiment, and improved manufacturing economics.

Competitive Landscape

The green chemistry industry is made up of companies at various stages of commercialization and levels of capitalization. Biobased chemical startups, which seek to commercialize processes that produce petrochemical alternatives derived from biomass resources, and companies pioneering novel chemical production technologies are applying the powerful developmental and analytical biology-based toolkits that have been developed over the last 30 years. Much of the biobased segment is comprised of reformed advanced biofuels companies, which have the greatest long-term potential to revolutionize the chemical industry. Well-established chemical companies are key players in the green chemistry industry as well, often spearheading efforts at reducing waste and pollution in the production process. The value proposition and market opportunities pursued by all of these companies are explored in more detail below.

Definition and Drivers

Green chemistry, which is often used interchangeably with sustainable chemistry, does not lend itself to a narrow, catch-all definition. Without a strict, measurable definition of what makes a particular chemical or compound “green,” Pike Research's analysis distills the green chemistry opportunity into three primary value propositions: 1. Waste minimization in the chemical production process; 2. Replacement of existing products with less toxic alternatives; 3. Shift to renewable (non-petroleum) feedstocks.

Definitions of green chemistry are codified in the “Twelve Principles of Green Chemistry,” articulated by John Warner, then a senior research scientist at Polaroid Corp., in the mid-1990s. Warner's review is based on the pioneering work of Paul Anastas, then chief of the US EPA's Industrial Chemistry Branch. Anastas, and Warner's ideas are elucidated further in their 1998 book, Green Chemistry: Theory and Practice, which has served as a foundation text for the discipline. 1 The “Twelve Principles” speak to the varied nature of green chemistry, but can be narrowed into the above product segments.

Broadly speaking, green chemistry is the manifestation of tightening restrictions around the human health impacts associated with the use of chemicals, economic necessity, and evolving consumer demand fueled by scientific studies and increased media attention exposing the dangers associated with current industrial chemical production processes. As the field develops, consolidation in the industry is likely, with established players partnering or buying up early-stage technology plays that demonstrate feedstock and end-product flexibility. Those companies that can vertically integrate the production process—from feedstock to end-product—are likely to capture significant, early market share as the nascent green chemistry industry scales up.

Waste Minimization

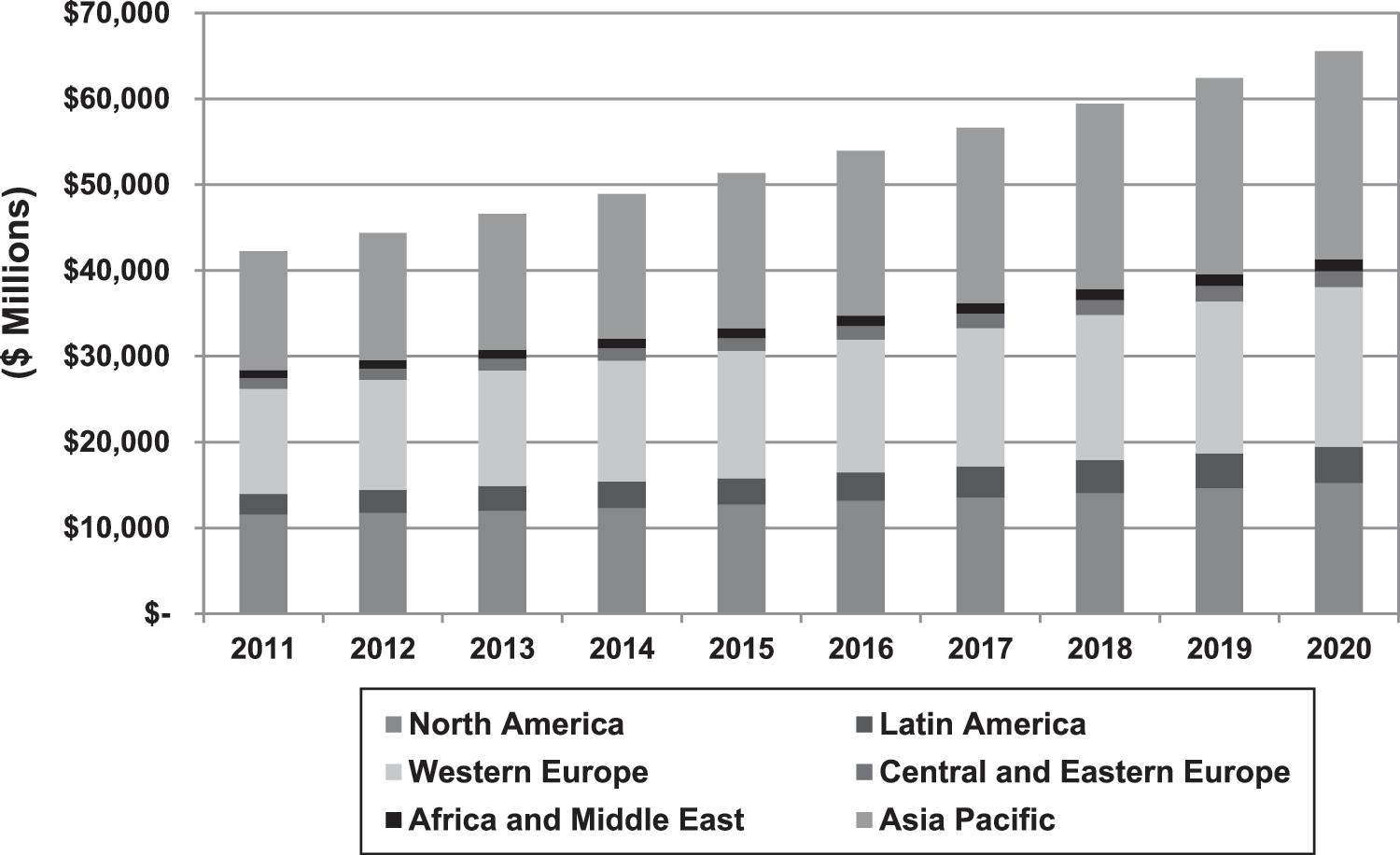

Our analysis shows that the greatest opportunity for near-term positive financial and environmental impact comes from waste minimization improvements to existing, conventional chemical production processes. The global environmental and human health impacts of chemical-related pollution have yet to be quantified in the aggregate as the associated externalities are varied and complex. But with increasing awareness about the pervasive danger, the elimination of waste reduces potential liability for producers and streamlines industrial processes. In both cases, significant cost savings can be achieved and costs avoided. Our forecasts show that a 55% increase over current value can be expected by 2020 (Fig. 1). While this “low-hanging fruit” represents a key near-term value opportunity, it represents a small fraction of the massive global chemicals industry.

Green chemistry savings and liability avoidance by region, world markets: 2011–2020.

Replacement of Existing Products

The replacement of existing products is the green chemistry segment most impacted by changing consumer sentiment, which increasingly seeks cleaner products that match or exceed currently marketed products in performance and price. Although in some cases studies show that consumers are willing to pay a premium for greener products, this has generally proven to be the exception. 2

That said, a number of large public companies have recently introduced green brands into a market formerly dominated by small, closely held companies with positive results. The Clorox Company's Green Works brand, for example, was introduced in December 2007 and is estimated to have grown to approximately $200 million per year in revenue. Meanwhile, one-third of Dow Chemical's 2010 sales were from products introduced within the past five years.

Accordingly, our forecasts project accelerating sales in this segment—reaching a near quadrupling in market value by 2020—assuming green chemistry-derived products can compete on price and performance. This segment primarily applies to chemical formulators, rather than manufacturers—the former companies including those that combine the chemical feedstocks provided by manufacturers into end-use products with desired properties.

Shift to Renewable (Non-petroleum) Feedstocks

A number of macroeconomic and regulatory factors are driving demand for alternative, non-petroleum-based feedstocks used in the production of chemicals. Sustained increases in world crude prices and tightening toxic chemical restrictions are among the most frequently cited of these factors. The scale-up of conversion processes that utilize biomass feedstocks is an opportunity that is gaining widespread attention at present, with a parade of high profile initial public offerings (IPOs) over the past year, due to the potential for supplanting a broad swath of petroleum-based products.

As addressed in Pike Research's reports, “Biofuels Markets and Technologies” and “Algae-Based Biofuels,” this category includes many former advanced biofuels ventures shifting to a “chemicals first” approach. This strategy generates near-term revenue to support longer-term scale-up efforts and provides exit opportunities for weary venture capital (VC) boards. Renewable feedstocks offer three main purported advantages over conventional derivations from petroleum: lower greenhouse gas emissions, reduced toxicity, and lower costs. While these “green black” ventures face many challenges, scale-up has the potential to explode in the latter half of the decade assuming availability of sufficient financing and access to aggregated feedstock sources.

Outlook to 2020

The global chemical market historically has grown at a rate slightly higher than gross domestic product (GDP) growth. The traditional chemical industrial complex is challenged by changes in feedstock availability and price, labor and energy costs, differential rates of economic growth, and environmental pressures. Although primary chemical production has traditionally centered on three geographic regions—Europe, US, and Japan—in recent years, growth has accelerated in emerging markets throughout Latin America, Asia Pacific, Africa, and the Middle East regions.

Although the green chemistry market is still nascent, our projections show that growth will be most pronounced in North America, Western Europe, and Asia Pacific over the forecast period. We expect the market to grow through several clearly defined stages: a profusion of small companies that are able to bring promising technologies to commercialization will gradually coalesce (through failures, acquisitions, and mergers) into a more unified, functioning ecosystem. Our analysis shows that the most robust growth will occur after 2016, as product qualification and infrastructure reach sufficient scale, assuming, of course, that price and performance qualifications are met.