Abstract

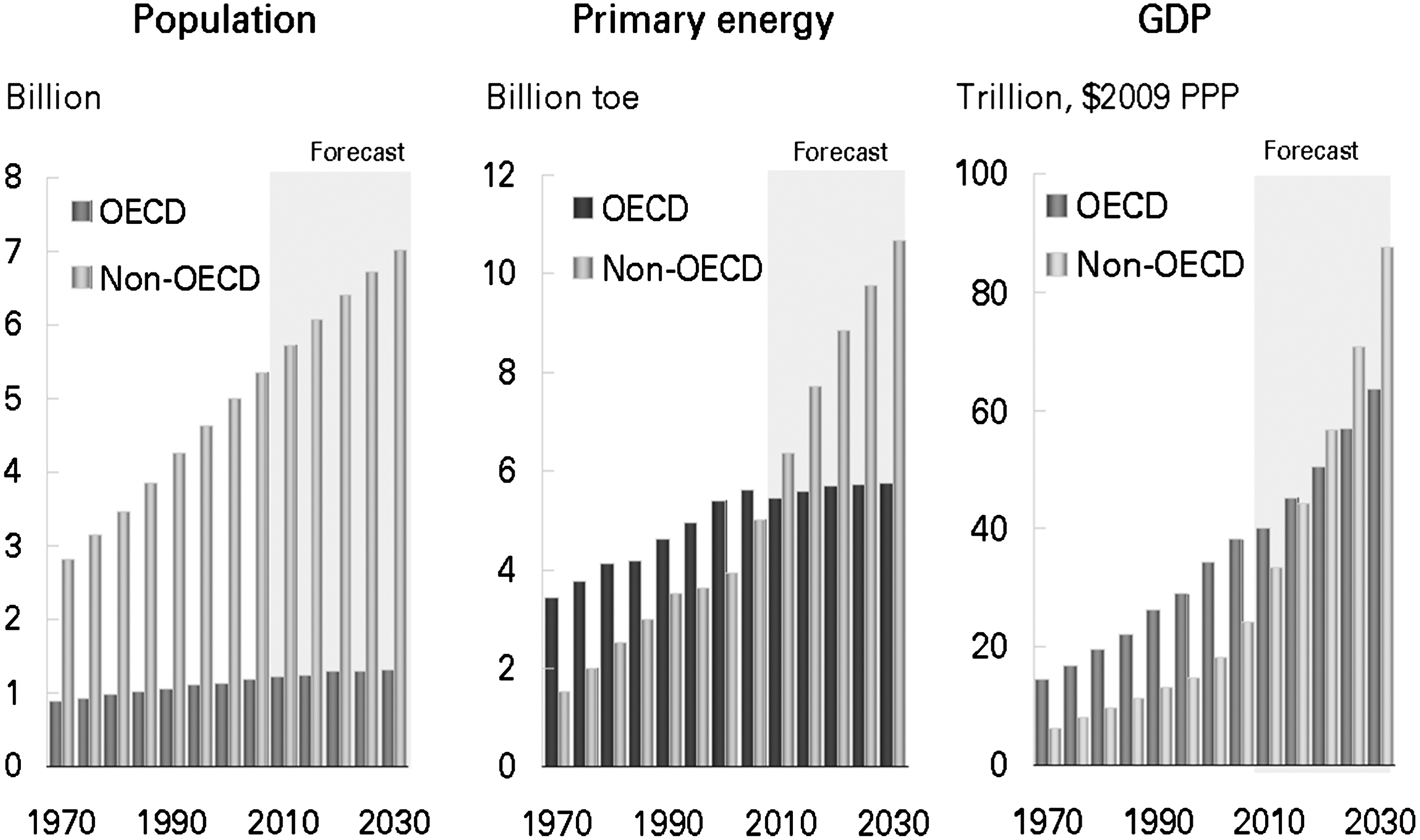

The timing for initiating a national bioeconomy strategy could not be better. With a rapidly growing world population that recently passed 7 billion and is headed to 10 billion, it is a time when we need to think about how we can accommodate that growth, particularly in emerging economies where not only the population is growing but so is the demand for energy. The emerging middle class in these economies has expectations for diet and lifestyle that will necessitate increased energy consumption. Despite greater efficiencies, energy consumption is going to rise dramatically. The International Energy Agency estimates global energy demand will increase one-third by 2035, with China and India representing 50% of the growth (Figure 1).

Emerging economies – high growth rates, high expectations. OECD=Organisation for Economic Co-operation and Development; toe=tonne of oil equivalent; PPP=purchasing power parity. (Source: BP)

How do we address the challenges of this growing population and its demand for energy? We do it primarily by focusing on two main factors: maintaining energy security and providing a nutritious diet. Energy security and food security are the two main drivers of the emerging bioeconomy. The additional challenges that arise as we address energy and food security are the need to do so with low-carbon-emitting technologies, so we can mitigate the effect on global climate change, and the need to do so in a sustainable manner that allows us to preserve the planet for future generations.

As we move toward biorenewables, we are putting extreme pressure on the existing land; we will need to increase productivity in a sustainable manner, using limited land and water resources to meet the demand. So the real pinch point where technology is going to be important is in meeting this challenge.

It is almost as if we were going back to the future. In the past, we had a renewable energy source. We then had what I would call the “oil interlude,” and during the oil interlude–over the last 50 to 75 years–there has been explosive growth in the global population. As I indicated, it comes with an expectation for higher energy use as individuals improve their diets—in some cases moving from vegetables to meat, for example–and also increasing their energy consumption. Looking to the future, we are again going to depend on the land to provide us not only with food and feed, but with renewable energy sources and feedstocks to replace all the components in a barrel of oil. So the challenge that we face is how to meet those future energy and lifestyle expectations with renewable sources of energy.

Thus, moving to a bioeconomy is not an option, it is an imperative.

What do we need to have in place if we are going to achieve this? We are going to have to use all of the tools and technology at our disposal to increase productivity, with an emphasis on improving efficiency. We are going to have to invest in innovation. We cannot address these challenges without having the best basic science and the efficient application of that science to develop solutions.

Once these are in place, we will need capital to fund the commercial deployment of these technologies, and we will need supportive policies. Policy traditionally lags behind the opportunity that technology gives us, and so it will be important to develop conducive policies that allow us to deploy these technologies effectively to identify and implement solutions to the challenges before us, and to make them available to the ready-and-waiting markets.

Benchmarks for Success

Certainly, the retail market pull is there. The US Navy, for example, has set a goal of moving its fleets to 50% biorenewable fuels by 2020, with plans to sail a naval fleet around the world on 50% biorenewables by the end of 2012. Another example is Procter & Gamble committing to the replacement of 25% of its petroleum-based materials with sustainably sourced renewable materials by 2020.

So there are some real drivers, or market pull if you will, coming from the military, the airline industry, and a number of major retail chains and consumer products companies that are responding to consumer demand for greater access to biodegradable products and materials from renewable sources.

The market pull is there, and the companies are responding, led by some of the largest international corporations. Just recently, for example, Coca-Cola and Pepsi were talking about polyethylene terephthalate (PET) bottles coming from renewable sources, a $30 billion market opportunity. The chemical companies are responding as well. A number of renewable products are already on the market and generating billions of dollars in revenues. This is no longer just science in the laboratory; this is science that is actually being commercialized by some of the largest corporations in the world. One estimate of the global size of the renewables market is USD 8.3 trillion. It may or may not be that large, but regardless of the exact number, it is huge. So we have a ready and large market, which is what is needed to justify investment in a new area.

Global policies are also enabling, and in fact have a critical role in creating the markets. Almost every country has some kind of policy around biorenewables and a green economy, and those policies, if they remain stable and predictable, will be important drivers for fostering and stimulating private sector investment.

The other important factor is the status of the enabling science. One of the most important areas of technology to evolve over the past several years is synthetic biology. Scientists can now go out into the environment, find relevant genes, assemble them into pathways, insert them into organisms such as yeast, and convert sugar feedstock into a broad range of chemicals that will contribute to the bioeconomy by supplying a source of biorenewable chemicals.

Some of the early products derived from these emerging technologies are already in the marketplace. They have been commercialized, so these are not laboratory-based technologies anymore. Some of the companies that have new second-generation products and applications of these technologies are in scale-up mode, whether scaling up to demonstration scale or to commercial scale (Table 1). These include companies that are part of the Malaysia Life Science Capital Fund; for example, Gevo, which expects to begin commercial isobutanol production during the first half of 2012 in a retrofitted ethanol plant, and Segetis, which has developed a process for converting biomass into ketals. Some of its products are already in the marketplace in detergents and plastics. And there are many other examples of the commercial development of renewable chemicals. So the technology is ready for commercialization.

Status of the technology (many more in scale-up)

Source: Burrill & Company

Finding the Capital

Now that we have ready markets, a base of technology, and companies ready to go commercial, where do we find the capital they need and where do we find the renewable feedstocks? Those are the two main limiting factors in this industry today: access to capital and access to biomass-derived feedstocks at a competitive price.

From the financing side, the traditional sources of funding for innovation have been angel investors, seed funds, and venture capital. In recent months, the market for initial public offerings (IPOs) has been open, and a number of companies have accessed the public markets to gain access to the capital they need to move forward with scale-up. Corporate partnerships have been and continue to be critically important across the life sciences, and certainly in agriculture and health care this has been one of the major sources of funding for developing companies. It is emerging to be equally as important in industrial biotechnology. One of the most critical challenges for companies going commercial today is the need to access 100 million, 200 million, or 300 million dollars to cover their capital expenditures.

Venture capital investments have been on the decline during the last couple of years. From the perspective of a venture capital investor that is actually good in some ways, as it means there is less money chasing a small number of deals. Therefore, valuations are more realistic and reflect the risk to commercialization. Having too much venture capital can cause a valuation bubble.

I mentioned the importance of partnerships as a source of capital, and many are in place. Large chemical and energy companies are investing in the renewables space, partnering with technology-rich startup companies to gain access to the technologies that will help both achieve future growth.

The recent IPOs in the industrial biotechnology space, namely Codexis, Amyris, Gevo, Solazyme, and KiOR, have been quite successful. They have raised, on average, about $140 million (Table 2). Most of these companies filed IPOs early, pre-revenue, and many of them were only in the demonstration stage of development. They went out early because they needed access to capital and the markets were open; overall, they were successful in raising the needed capital, but post-IPO performance has been disappointing.

Recent IPO financings in greentech

Source: Burrill & Company

Following that, nine more companies in the sector have lined up to go public and filed their S-1s (Table 3). The big question now is whether they will get out, and the reason for the uncertainty lies in the significant challenges facing the US and European economies. Whether or not the IPO window remains open is anyone's guess.

Biogreentech companies in the IPO queue

Source: Burrill & Company

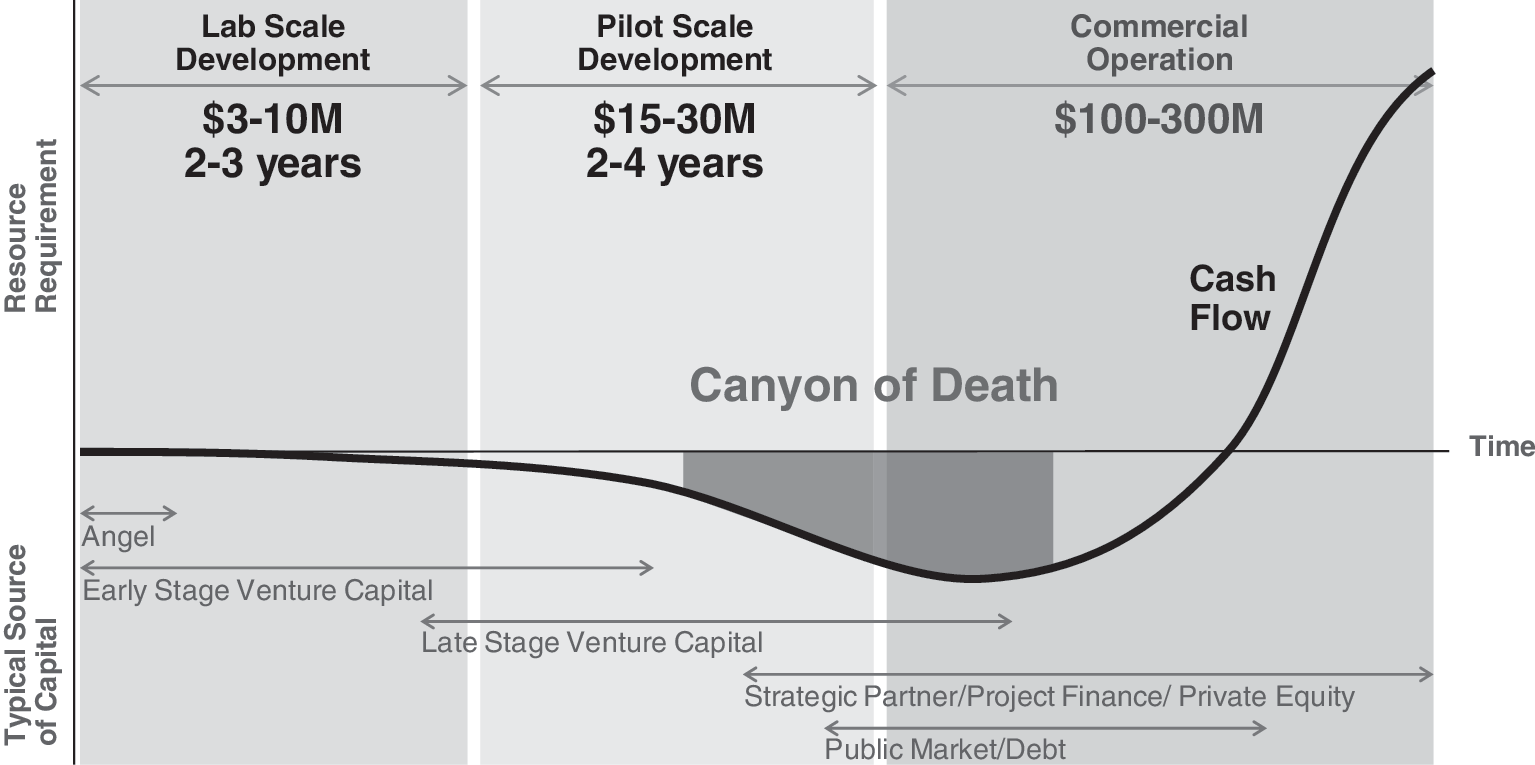

This industry has a massive need for capital. We talk about the ‘valley of death’ for small companies, but now we are talking about the ‘canyon of death,’ because we are looking at several multiples of the amount of money that needs to be raised (Figure 2). The companies need that capital at the stage when they have to go from demonstration scale to commercial scale. The question is, especially in the US and Europe, whether that capital will be available given the financial situations in those countries.

Development and financing of bio-based startups

The US in particular has invested heavily in the scale-up of technologies, roughly $3 billion in investments. Those technologies are now in scale-up, and we will have validation of most of those technologies around 2014. At that point we will hit a financial wall, and successfully making it over that wall will depend on whether the companies can continue to access the capital they need.

The numbers are huge. If you consider the amount of capital needed to support the renewable fuel standard (RFS) in the US, we will need to build more than 300 biorefineries, and that will require an investment of about $95 billion. If you multiply that out across several countries, you can see the amount of total capital that will be necessary. Access to that capital is coming from a number of sources, including countries and even individual states, such as Mississippi, which recently established a relationship valued at $100 million with one of the companies in which we invested. In addition to countries and state governments, we are beginning to see the US military put up money, and this is all going to be critically important if the industry is going to continue to grow.

Accessing the Biomass

Biomass will be a very important part of supplying the renewable feedstock needed to grow this industry, to produce the renewable chemicals and materials that are part of a bioeconomy. Ready access to biomass at a price point that would allow companies to produce higher-value chemicals will be crucial. The most important question is which feedstock to use. Certainly, the easiest choices for fermentation early on were the feedstocks that were readily available, mainly sugar and starch. The corn ethanol industry developed incredibly rapidly primarily because it relied on proven technology, and the infrastructure to collect the feedstock, corn grain, was in place. The technology was old, we knew how to do it, and it was simply a matter of scale-up.

The really important breakthrough will be access to lignocellulosics. This will allow the industry to move away from the food-versus-fuel issue. It will require technologies for conversion that will yield sugar at a cost–around 20 to 30 cents per kilogram–that allows companies to supply the large commodity chemical markets.

The most interesting aspect of this for Malaysia and for the ASEAN is the large number of companies that are looking for access to low-cost, or at least competitively priced sustainable feedstock supplies, and these companies will move from where the technology is to where the biomass is. The low energy density of biomass makes it necessary to move the technology to the biomass, in contrast to what we do now, which is to move the more energy-dense petroleum to the technology and to the market.

If one looks at where the technologies are being developed, they are in the US and Europe. But the long-term sustainable supplies of biomass and large emerging markets are in Southeast Asia, particularly in the ASEAN. We are seeing companies rapidly moving to the sources of these biomass supplies. Brazil certainly is a magnet because it has a ready supply of sugar. A number of companies have recently moved to Thailand and to Indonesia. Companies are moving globally to gain access to the biomass.

Two opportunities are available: waste conversion, or the development of dedicated energy crops. For waste conversion, the infrastructure is already in place, apropos to the palm industry in Malaysia. However, the pathways for converting biomass represent a significant challenge. Nature's goal for millions and millions of years has been to make biomass recalcitrant to breakdown, and we are now trying to reverse that in just a few years.

Several different approaches are being pursued. Enzymes and enzymatic hydrolysis, for example, are already in commercial use. Other methods in development for breaking down cellulosic biomass include acid hydrolysis, gasification, and supercritical fluid hydrolysis. Obviously, one can ferment glycerol directly in some cases. Pyrolysis is another option, essentially making biocrude oil, which can then go into a standard petroleum refinery. Pyrolysis is being scaled up at present, but most of the other technologies are in demonstration scale and are still several years away from commercialization. But we can certainly see a path to commercialization of lignocellulosic feedstocks in the next three, four, or five years.

If we assume that we have the capital and the biomass conversion technology, the ASEAN is in an incredibly strong position. It is close to some of the major markets, including India and China. China is spending massive amounts on developing renewables and is investing in this region. Relative to the rest of the world, these are the only growing economies at present. These countries are trying to make the transition from developing/emerging to developed economies, and they are seeking innovation to drive that transition.

Furthermore, there is already an existing plantation industry in the ASEAN. There is an infrastructure in place, ready for the integration of this innovation and these new technologies. One of the reasons corn ethanol works well is that the US has a very efficient system for moving that corn biomass around. So infrastructure is an important component for success.

In addition to proximity to large markets, the ASEAN has the advantage of economic growth. The International Monetary Fund (IMF) is predicting growth in the ASEAN in the 6% to 7% range, compared to the US and Europe, where it is almost zero or even negative (Table 4). There is an opportunity here to bring in technologies and to assist in the economic growth of these countries, increasing their gross domestic product (GDP) per capita. Malaysia has set a goal of doubling its GDP by 2020–an audacious goal. But the only way they can achieve this is to bring in innovation and technology.

Strong economic growth projections for ASEAN

Source: IMF

There are some challenges across the region in terms of accessing the technology and integrating it rapidly into these economies. Despite the impressive infrastructure in Malaysia, the same is not evident in places like Indonesia. But with the available access to biomass, there are global investors looking to move money and capital into this region. I think the timing is right for the ASEAN to take advantage of this opportunity.

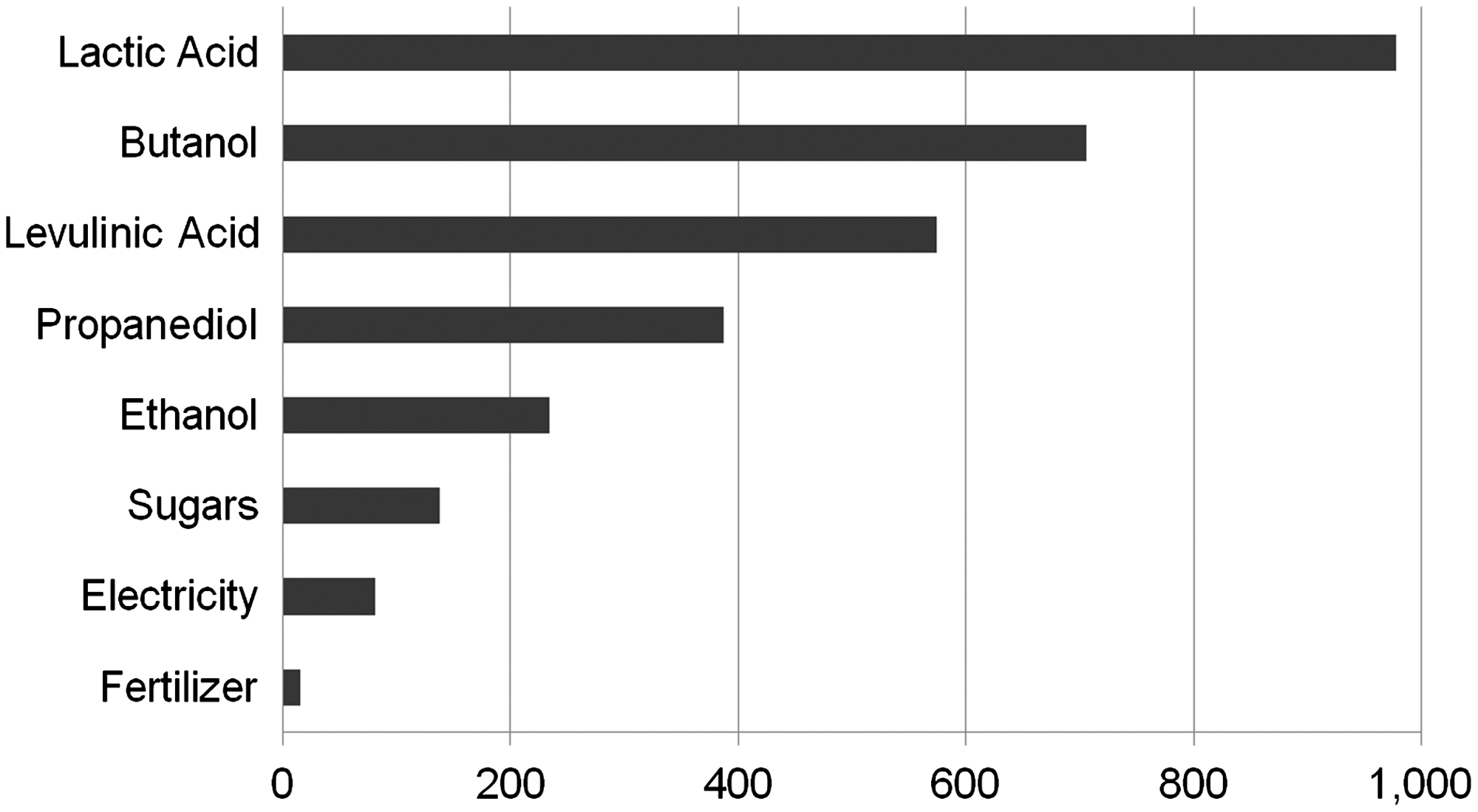

We and some of our colleagues conducted a survey recently to assess what biomass is available in the ASEAN region, and we came up with a figure in excess of 300 million dry tons of biomass, some portion of which could be made available for supporting a biorenewable chemicals industry (Figure 3). There is also the opportunity to bring dedicated crops into the region, so although we talk a lot about palm waste, we really should think about the broader opportunities.

Value generated per dry ton of biomass (USD) (Source: Malaysian Life Science Capital Fund)

Focusing on palm waste, there are 175 million tons available in Malaysia, Indonesia, and Thailand combined. Currently it is used primarily for power generation, as well as for fertilization on plantations, a relatively low-value use if you think about the eventual economic opportunity. If that palm waste were to be converted to sugar, and subsequently into some of the foundation chemicals, the increase in value would be significant. The conversion of even 30% of the biomass that is available in these three countries into foundation chemicals would represent a significant amount of annual revenue. Conversion of those foundation chemicals into downstream, higher-value products would respresent a significant economic stimulus for the economies in the ASEAN. We estimate USD 60 billion of potential annual revenue. The point is, this represents a significant opportunity to inject economic growth in this region.

In summary, we have a convergence of factors that make for a very exciting opportunity for the industry. We need to move technologies to regions that have capital and biomass. I would argue that the ASEAN is well poised to be a recipient of that opportunity. The financing is available and there is global interest in investing in this region. The technology is ready to be integrated and applied, and the potential economic impact on emerging economies is huge. The challenges are certainly not trivial, but as an industry we have an exciting opportunity to feed a growing world population with a nutritious food supply and to use the principles of biotechnology to convert some of that feedstock into fuels and chemicals that will contribute to a more sustainable society, with a lifestyle and a quality of life that all of us would be proud to have our future generations inherit from us.