Abstract

Summary

This study looked at every kind of bio-based polymer produced by 247 companies at 363 locations around the world and it examines in detail 114 companies in 135 locations. Considerably higher production capacity was found than in previous studies. The 3.5 million tonnes represent a share of 1.5% of an overall construction polymer production of 235 million tonnes in 2011. Current producers of bio-based polymers estimate that production capacity will reach nearly 12 million tonnes by 2020. With an expected total polymer production of about 400 million tonnes in 2020, the bio-based share should increase from 1.5% in 2011 to 3% in 2020, meaning that bio-based production capacity will grow faster than overall production.

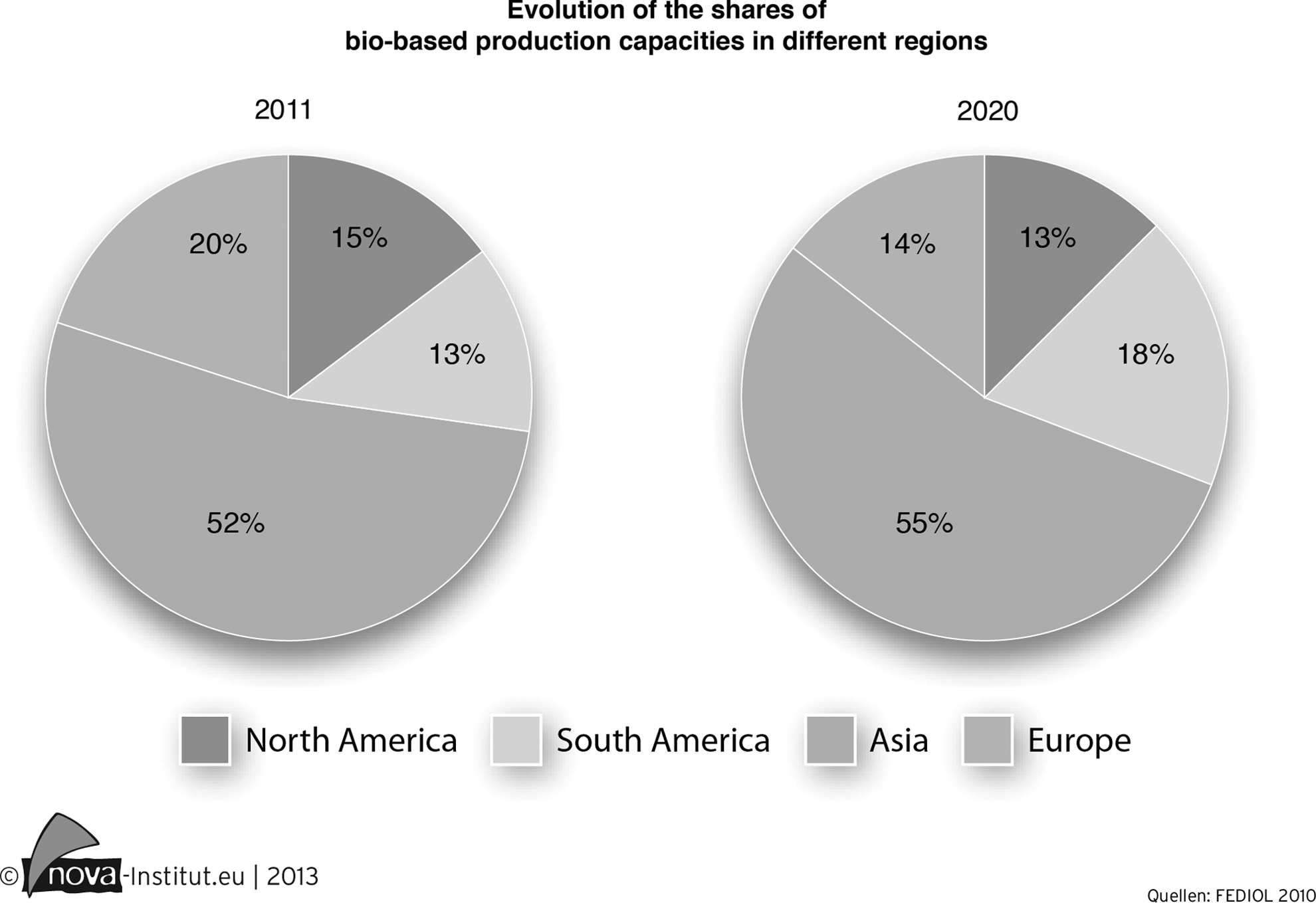

The most dynamic development is foreseen for drop-in biopolymers, which are chemically identical to their petrochemical counterparts but at least partially derived from biomass. This group is spearheaded by partly bio-based PET (Bio-PET) whose production capacity will reach about 5 million tonnes by the year 2020, using bioethanol from sugar cane. The second in this group are bio-based polyolefins like PE and PP, also based on bioethanol. But “new in the market” bio-based polymers PLA and PHA are also expected to at least quadruple the capacity between 2011 and 2020. Most investment in new bio-based polymer capacities will take place in Asia and South America because of better access to feedstock and a favorable political framework. Europe's share will decrease from 20% to 14% and North America's share from 15% to 13%, whereas Asia's will increase from 52% to 55% and South America's from 13% to 18%. So world market shares are not expected to shift dramatically, which means that every region of the world will experience development in the field of bio-based polymer production.

Michael Carus, managing director of nova-Institute, reacted to the survey results thus: “For the very first time we have robust market data about worldwide production capacity of all bio-based polymers. This is considerably higher than in previous studies, which did not cover all polymers and producers. The forecast of a total capacity of 12 million tonnes by 2020—a tripling of 2011 levels—suggests that bio-based polymers are definitely polymers for the future. It is also shown that the development of bio-based polymers is still very dynamic. Only five years ago, nobody would have expected bio-PET to grow to the biggest group among the bio-based polymers due to an initiative by one big brand-owner. This could happen again with any other bio-based polymer. PLA and PHA also have a remarkable growth ahead of them, even without the existence of such a ‘supply chain captain’.”

Editor's Note:

This Industry Report presents excerpts from a market study on bio-based polymers prepared by Germany-based nova-Institute. The full 360-page report can be ordered at

Study Background

The bio-based polymers branch is a dynamic, versatile field, in which bio-based polymers have reached development stages that range from research level, via initial market adoption to long-term established performance plastics like cellulosics or nylon—all of them revealing significant market growth.

A number of factors affect the growth rate of the bio-based polymer branch. These factors include state policy, technology, feedstock cost, competition (biomass versus fossil fuels), crude oil prices, consumer acceptance, and, last but not least, access to clear and reliable market data.

There was in fact broad agreement—not only from the major industrial players but also from the user side—about the need for solid, transparent, and worldwide market data about the bio-based polymer branch.

Methodology

The field of bio-based polymers is broad and the available information very diverse and sometimes inconsistent. This can lead to confusion and misinterpreted results. It therefore seems crucial to explain the methodology that we used for this survey. This study focuses exclusively on bio-based polymer producers, and the market data therefore do not cover the bio-based plastics branch. We must clearly differentiate between these two terms. A polymer is a chemical compound consisting of repeating structural units (monomers) synthesized through a polymerization or fermentation process, whereas a plastic material constitutes a blend of one or more polymers and additives.

Market data cover only the first polymer producers, excluding plastic and compound processing in an attempt to avoid double counting over the various steps in the value chain. Starch blends are the single exception among plastics to have been included in the market research. They are always used in complex blends of many components such as aliphatic polyesters (e.g., PCL, PLA, PBAT, PBS). In order to also avoid double counting here, it was attempted to leave out the capacities of bio-based polymers used in starch blends.

The focus of the study is on construction polymers, i.e., the polymers that will later constitute the structural mass of the finished plastic part. Functional polymers used in inks, coatings, adhesives or simply as a performance enhancer in other materials were only covered selectively and are not included in the totals given in this summary. Regenerated cellulose (e.g., cellophane and viscose), natural rubber, and linoleum are beyond the scope of this study.

This market survey covers current market trends on bio-based polymers, i.e., derived from biomass (which may be biodegradable or not). However, we decided to include market data on some polymers that are currently still fossil-based, namely polybutylene succinate (PBS) and polybutyleneadipat-terephthalate (PBAT). It may seem paradoxical, but the reasons for covering their production capacities are as follows. Their development is highly linked to the development of other bio-based polymers, as they are often used to enhance their properties in bio-based compounds. In the case of PBS, which is currently produced from fossil resources in relatively small quantities, the capacity development is spurred by the development of its bio-based precursors, as bio-based succinic acid can be produced at lower cost than its fossil-based alternative. They are both drop-in processable, i.e., every fossil-based PBS or PBAT producer can switch to bio-based PBS or PBAT if the bio-based diacids and diols become available, with no need to change equipment. From announcements and seeing the capacity development in their bio-based precursor chemicals, the polymers of the companies covered here are expected to be increasingly bio-based, reaching shares of 50% (PBAT) and 80% (PBS) by 2020. Table 1 gives an overview of the covered bio-based polymers and the producer companies with their locations.

Bio-based Polymers, Short Names, Average Biomass Content, Producer Companies, and Locations

Currently still mostly fossil-based with existing drop-in solutions and a steady upward trend of the average bio-based share up to given percentage in 2020.

Including joint venture of two companies sharing one location, counting as two.

Upcoming capacities of bio-pTA (purified terephthalic acid) are calculated to increase the average bio-based share, not the total bio-PET capacity.

Starch in plastic compound.

Main Results

Building Blocks and Monomers as a Precursor of Polymers

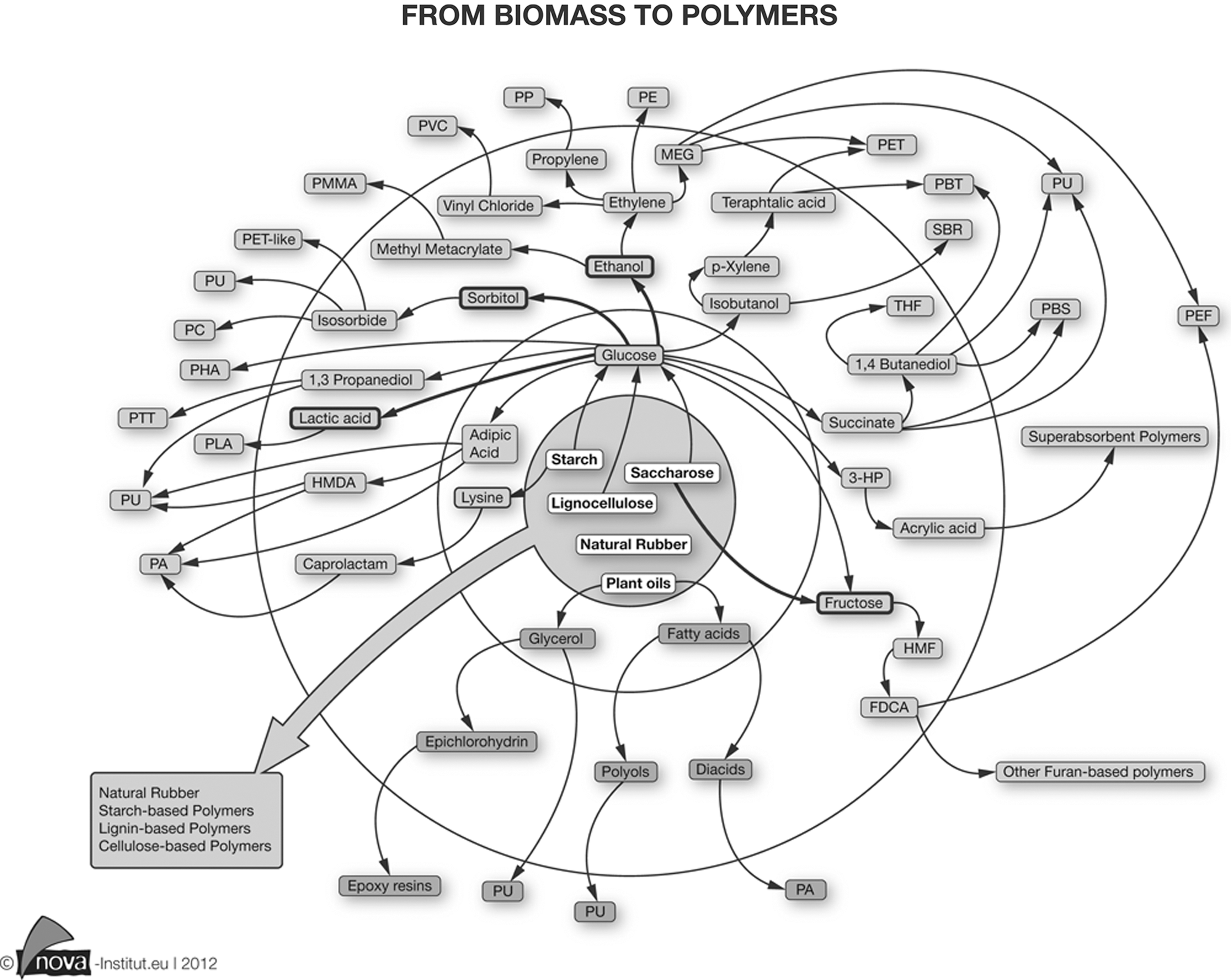

Figure 1 shows the most important pathways from biomass to building blocks to polymers. The thickness of the arrows is related to the current market relevance of the corresponding building blocks. Only existing routes currently engaged in industrial production have been taken into consideration. There are many more pathways under research or at pilot stage. However, one can clearly see that bio-based chemical producers currently have the potential to build extensive alternative supply chains for a variety of chemicals and polymers (e.g., PU, PA).

From biomass to polymers.

There is a strong growth in the market for bio-based precursors for drop-in solutions, which are also partially covered by the report and database. Often there are not yet any announced capacities at the polymer producer stage, so the study could not reflect the volumes of polymers derived from these precursors.

There is also a strong upward potential for bio-based PA precursors for example, as well as plans to make commodity PA like nylon 6.6 and nylon 6 (partly) bio-based. For different building blocks like adipic acid (2,800 kt market in total), HMDA, caprolactam, etc,. the bio-based market share is purely a matter of price compared to petrochemical routes, which is already lower in some cases.

The ongoing increase in bio-based MEG and pTA capacity has a considerable impact on the production capacities of partly bio-based PET. Our forecast for the total Bio-PET production capacity is based on the forecast of bio-based MEG production capacity in particular—supported by announcements of future market demand.

Bio-Based Polymers

The report shows that the production capacity of bio-based polymers will triple from 3.5 million tonnes in 2011 to nearly 12 million tonnes by 2020. Bio-based drop-in PET and PE/PP polymers and the new polymers PLA and PHA show the highest growth rates on the market. Most capital investment is expected to take place in Asia and South America.

Considerably higher production capacity was found than in previous studies. The 3.5 million tonnes represent a share of 1.5% of an overall construction polymer production of 235 million tonnes in 2011. Current producers of bio-based polymers estimate that production capacity will reach nearly 12 million tonnes by 2020. With an expected total polymer production of about 400 million tonnes in 2020, the bio-based share will increase from 1.5% in 2011 to 3% in 2020, meaning that bio-based production capacity will grow faster than overall production.

The most dynamic development is foreseen for bio-based PET (Bio-PET) with production capacity of about 5 million tonnes by the year 2020, based on bioethanol from sugar cane. The second are also drop-in biopolymers, which are chemically identical to their petrochemical counterparts but derived from biomass. Bio-based polyolefins like PE and PP, are polymerized from components, based on bioethanol. But also the “new” PLA and PHA bio-based polymers will more than quadruple their capacity between 2011 and 2020.

Bio-based PET

The Coca-Cola Company, Ford Motor Company, H.J. Heinz Company, NIKE Inc. and Procter & Gamble announced in 2012 the formation of the Plant PET Technology Collaborative (PTC), a strategic working group focused on accelerating the development and use of 100% plant-based PET materials and fiber in their products. In just a few short years, The Coca-Cola Company has expanded from producing PlantBottle™ plastic in a single location to now having facilities in most of their major markets, with further expansion to come.

When such brand corporations join forces and build alliances, their impact on the supply chain becomes inevitably visible. Mono-ethylene glycol (MEG), a key component of PET resins, is already going to be produced in high volumes as bio-based diol in India (Indian Glycols LTD., 175,000 t/a) and Taiwan (Greencol Taiwan, 100,000 t/a). The Indian company JBF Industries plans for additional MEG capacities of 500,000 t/a in Brazil to come on-stream after 2015. Also developments in the production of bio-based purified terephtalic acid, the other monomer of bio-PET, have been announced.

As these precursors can be used to produce partly bio-based PET in any existing PET facility at relatively short notice, only very little of the bio-MEG capacity to come already matches announcements about the production of bio-PET. Companies already dedicating part of their PET capacities to the production of bio-PET are, for example, Teijin and Indorama Venture, both located in Asia, with 100,000 t/a and 300,000 t/a, respectively.

In the year 2011 about 620,000 tonnes bio-based PET were produced from bio-MEG, expected to grow to a production capacity of nearly 5 million tonnes in 2020.

PLA –polylactic acid

At 30 sites worldwide 25 companies have developed a production capacity of (presently) more than 180,000 tonnes per annum (t/a) of polylactic acid (PLA), which is one of the leading bio-based polymers. The largest producer, NatureWorks, had a capacity of 140,000 t/a in 2011. The other producers have current capacity of between 1,500 and 10,000 t/a.

According to their own forecasts, existing PLA producers are planning to considerably expand their capacity to reach around 800,000 t/a by 2020. There should be at least seven sites with a capacity of over 50,000 t/a by that time. A survey of lactic acid producers (the precursor of PLA) revealed that production capacity could even rise to roughly 950,000 t/a to meet concrete requests.

Investment by region

Most of the investment in new bio-based polymer capacities will take place in Asia and South America because of better access to feedstock and favorable political frameworks.

Asia has become a key region for bio-based polymers and their precursors. Some examples are current developments in Thailand (Purac, PTT), India (India Glycol Ltd.), Taiwan (Greencol Taiwan), China (Henan Jindan, Shenzhen Ecomann, Tianan Biologic Materials, Tianjin Green Biomaterials) or Japan (Kaneka, Teijin Limited, Toyota), which include future or existing production of lactic acid, lactide, succinic acid, 1,4-BDO, MEG, PET and PHA.

The expanding global utilization of bio-ethanol for chemical building blocks has led to the establishment of large-scale production facilities for bio-based MEG in India and Taiwan and for bio-ethylene, precursor for, e.g., PE, MEG, but also EPDM, in Brazil. Furthermore, the bio-based drop-in market is developing fast in Asia, where many converters are SMEs and cannot afford important alterations to their existing processing equipment.

Europe's share will decrease from 20% to 14% and North America's share from 15% to 13%, whereas Asia's will increase from 52% to 55% and South America's from 13% to 18% ( Figure 2 ).

Evolution of the shares of bio-based production capacities in different regions.

Share of bio-based polymers in the total polymer market

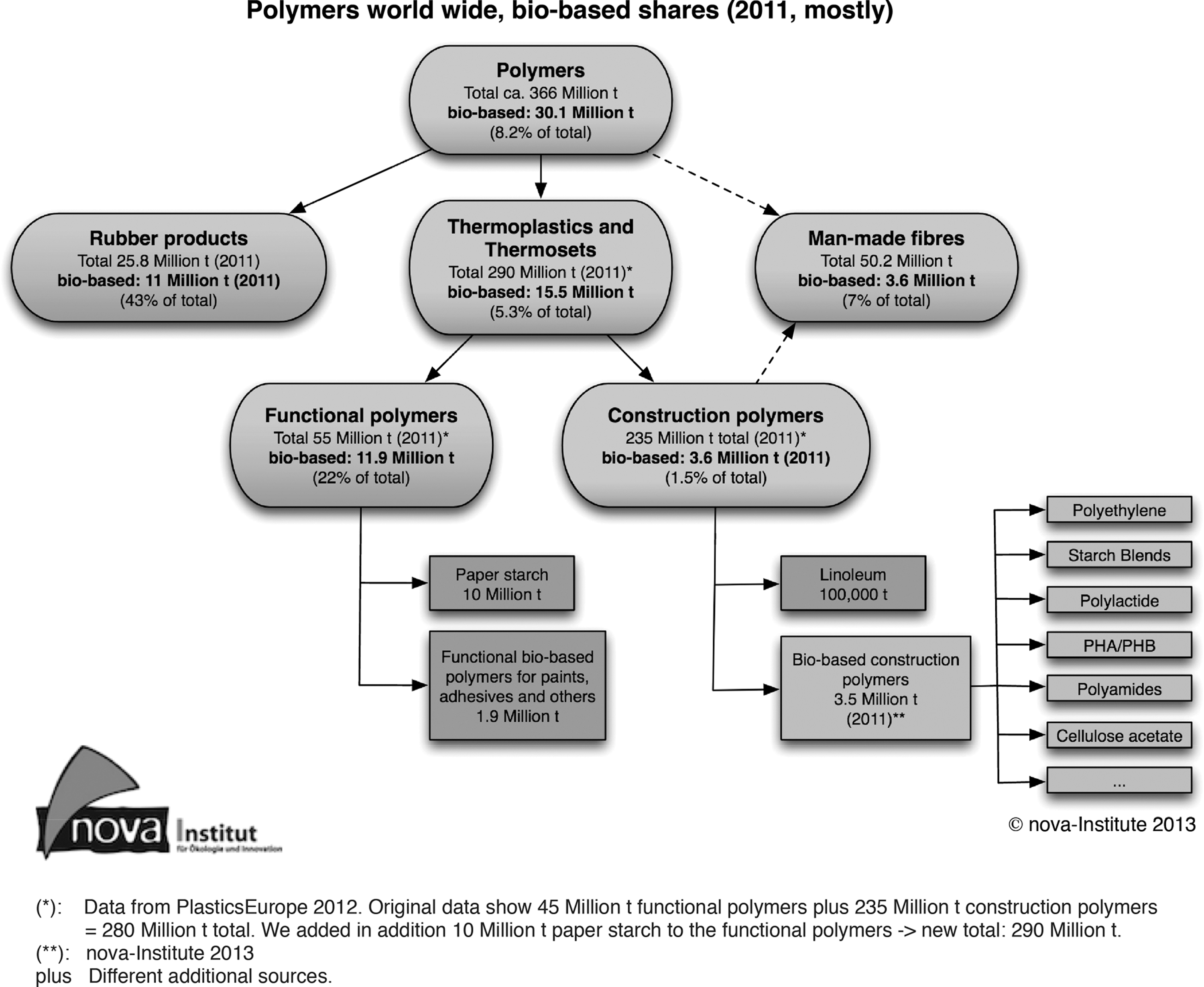

Figure 3 gives an overview of all kinds of polymers including rubber products, man-made fibers and functional polymers–and not simply construction polymers as usual. This figure includes bio-based shares at different levels.

Polymers worldwide, bio-based shares (mostly 2011).

The share for construction polymers, which are the focus of the study, is 1.5%, but for polymers overall the bio-based share is even higher (8.2%) because of the higher bio-based shares in rubber (natural rubber) and man-made fibers (cellulosic fibers).