Abstract

The continued development of the bioeconomy is expected to transform all segments of the chemical industry, from bulk to fine chemistry. About 10% of the current chemical feedstock base consists of renewable materials such as sugar, starch, cellulose, oils, and fats, but more non-food biomass resources need to be exploited as biobased production becomes more significant in the bulk sectors. Growing demand for feedstocks based on agricultural, silvicultural, and marine sources will increasingly shift global value chains from fossil-rich to biomass-rich countries, but how quickly this will happen depends very much on the cost-competitiveness of the various biomass-based versus fossil-based raw materials. The high costs associated with biomass logistics have been a key limiting factor for biorefinery investments. The best way to integrate mid-sized biorefineries into the established, large-scale chemical infrastructure is also a key challenge. Nonetheless, more and more regions and representative groups such as the Organisation for Economic Co-operation and Development (OECD) and BRIC (Brazil, Russia, India, and China) are recognizing the bioeconomy's economic potential and are developing strategies for growing their biobased industries into global value chains.

Introduction

The bioeconomy has two main drivers: protection of the climate, especially by reducing the emission of greenhouse gases (GHG); and the foreseeable shift from fossil-based to renewable feedstocks. Biomass is widely accepted as the only sustainable alternative to fossil carbon sources and the starting point for developing production processes that can be characterized as having a low, or even zero, carbon footprint.

The development of the bioeconomy faces a number of hurdles. Although processing and transformation of agricultural and silvicultural biomass to chemicals and fuels is established, the feedstock base of these industries is still dominated by fossil carbon sources. However, the transition into the bioeconomy is also an opportunity to build new cross-sectorial value chains linking intercontinental biomass regions and industrial centers. The bioeconomy's technical and product innovation requirements also create market opportunities for research institutes and companies of all sizes. The European chemical industry, which is highly involved in the bioeconomy, divides the bioeconomy's implications into three areas: access to renewable feedstock; innovation; and generation of market-driven demand. 1

The Current Bioeconomy

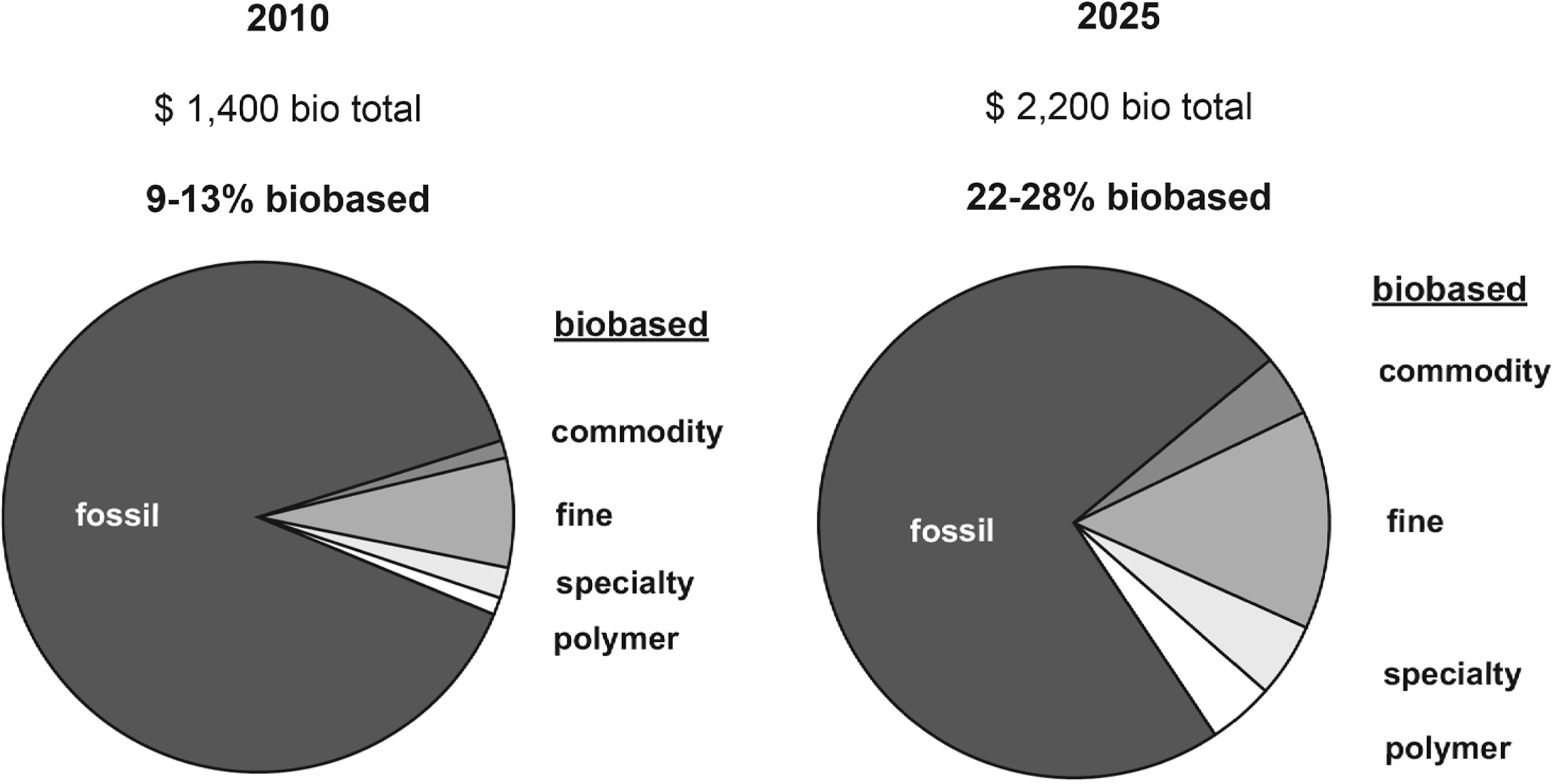

Most commercialized biobased chemicals target the specialty and fine chemicals markets, but applications in bulk chemicals are expected to grow (Fig. 1). 2 Citric acid and ethanol, for example, are considered bulk biochemicals, while enzymes, monoclonal antibodies, and enantiomerically pure compounds such as L-amino acids are considered fine or specialty biochemicals. As in other sectors, product cost and performance and consumer demand are the deciding factors. Consumer preference can be an important factor for some end markets, such as skin care actives, which are currently generally biobased.

Expectation of bioproducts penetrating different markets ($ in billions).

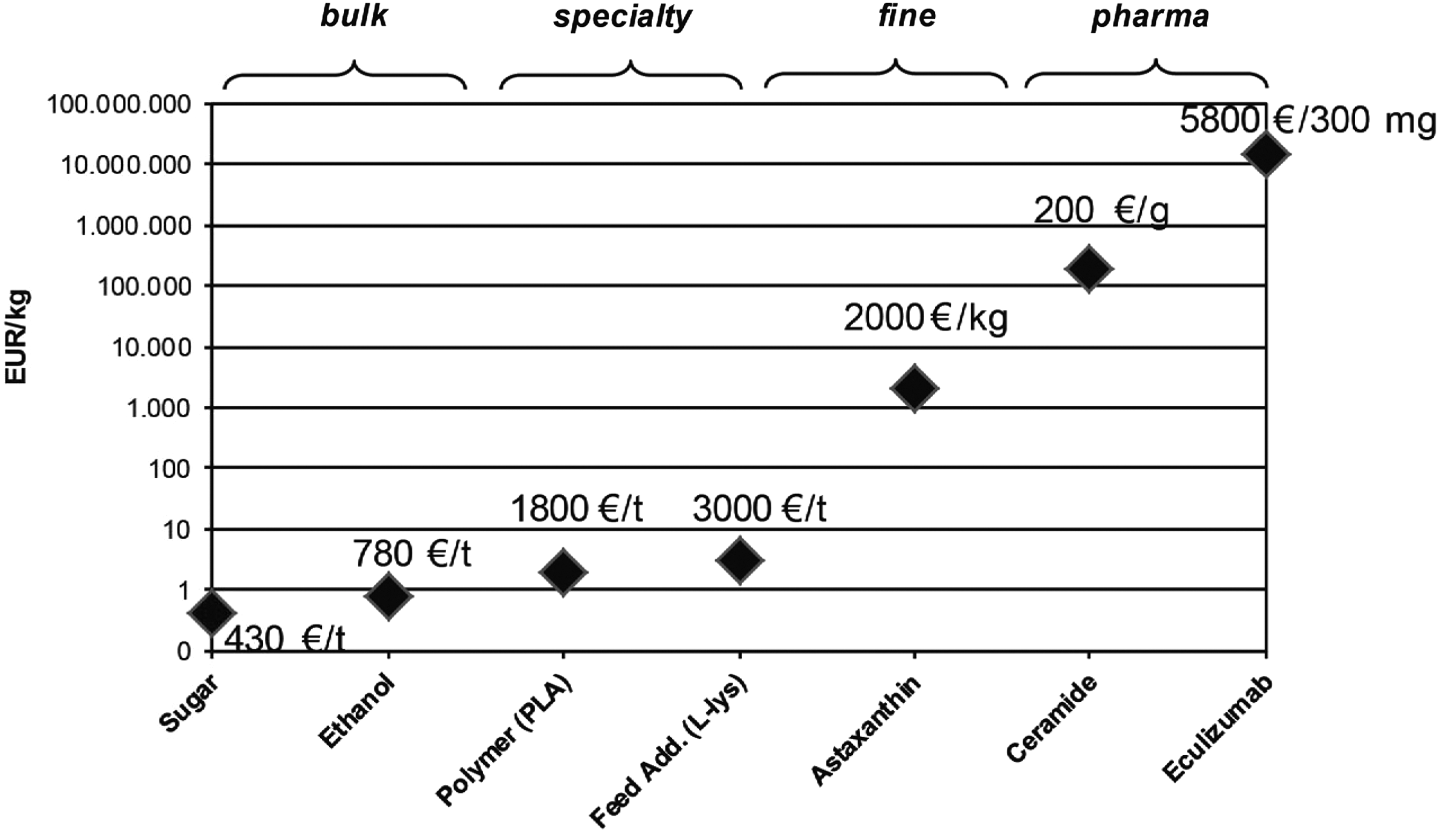

Market diversity is reflected in the wide range of price points for biochemicals. Some bulk biochemicals sell for as little as $1/kg, while high-value products may sell for several million dollars per kg (Fig. 2). At present, global biochemical sales total about $77 billion, but only make up 4% of the total chemical industry. 3 Oil is still the dominant chemical industry feedstock, although biomass is increasingly being used. According to the Organisation for Economic Cooperation and Development (OECD), agricultural and industrial applications will drive the future bioeconomy. 4

Price ranges for biochemicals in different product classes. (1€=USD1.37)

To make a significant impact on GHG emitted by the chemical industry, more bulk chemical products need to shift to biobased production. Such high-volume platform chemicals are the foundation for a broad portfolio of downstream chemicals production and consumer products. For example, fossil-based rubber is a basic material widely used in automotive, construction, and household products: 15 million tonnes are produced annually, mainly by copolymerization of styrene and 1,3 butadiene. Currently, a new plant-based rubber source is being explored by extracting latex from dandelion on a pilot scale. 5 It might stepwise enter the synthetic rubber market (and could account for 54% of total rubber production), thus reducing the carbon footprint of synthetic rubber by establishing an alternative direct agricultural production system besides rubber trees.

This article is derived from a presentation at IBIO 2013, BIT's 6th Annual Congress of Industrial Biotechnology, April 25–27, 2013, Nanjing, China. Industrial Biotechnology Editorial Board member Pabulo Henrique Rampelotto, PhD, coordinated the acquisition and review of this article.

Other chemicals depend on transforming a biological carbon source to achieve the biobased alternative. An example is bioethylene, which could be derived from sugar and would compete with fossil-based ethylene, which has a global production volume of approximately 140 million tonnes, making it the largest bulk chemical. From a technical standpoint, switching to biobased ethylene is easily achieved by dehydrating biobased ethanol—thus providing a so-called drop-in compound that can be introduced into existing processes without any adaptation. Producing biobased ethylene from sugarcane uses an estimated 60% less energy compared to the fossil-based method because of the integrated heat- and power-generation in burning bagasse. GHG emissions would also be cut by 40%. 6

Such compounds initially compete on the basis of cost with their fossil analogs if the ability to achieve a more sustainable carbon footprint is not valued. A recent agreement in which the packaging firm TetraPak (Lund, Sweden) agreed to buy low density polyethylene (LDPE) based on biobased ethylene from Braskem (São Paulo, Brazil) for use in 13 billion packages for liquids produced in Brazil demonstrates the viability of biobased PE in packaging applications. 7 However, the viability of such processes is determined primarily by cost compared to their fossil analog, not by the environmental benefit. A recent cost assessment of producing bioethylene from sugar beets in Europe indicated that currrently it is not commercially viable. 8 Therefore, on the one hand global biobased ethylene capacity has increased to 1 million tonnes since Braskem launched the first biobased ethylene plant in Brazil in 2010, but on the other hand, these investments still cover less than 1% of total ethylene capacity. 9

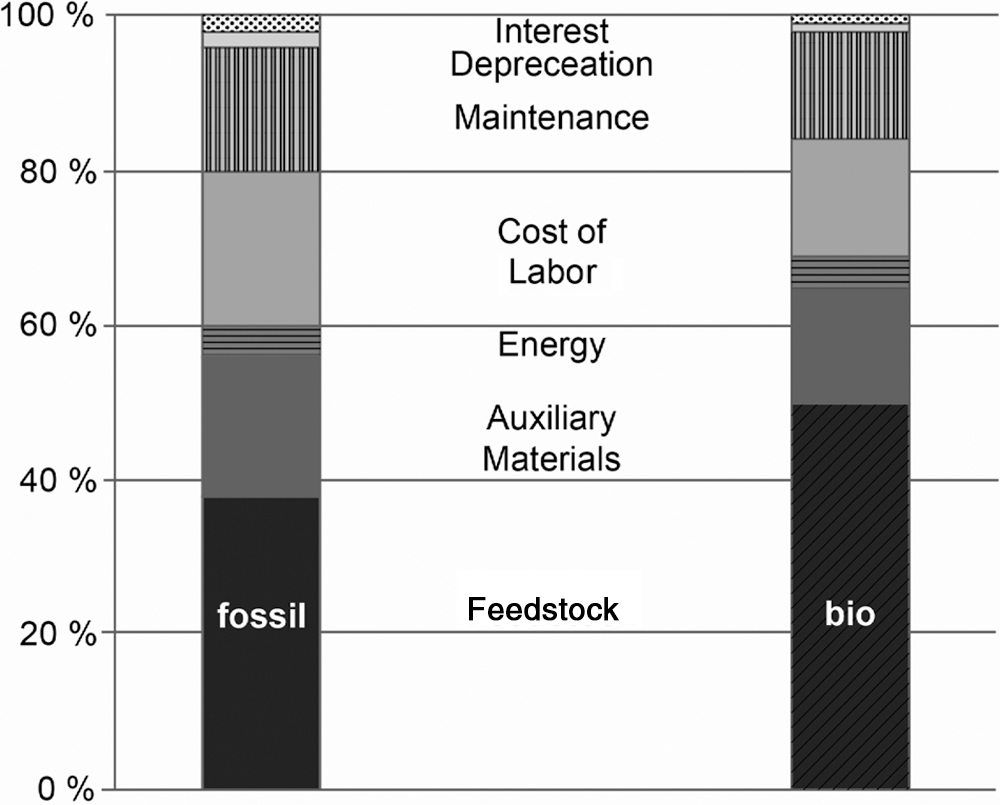

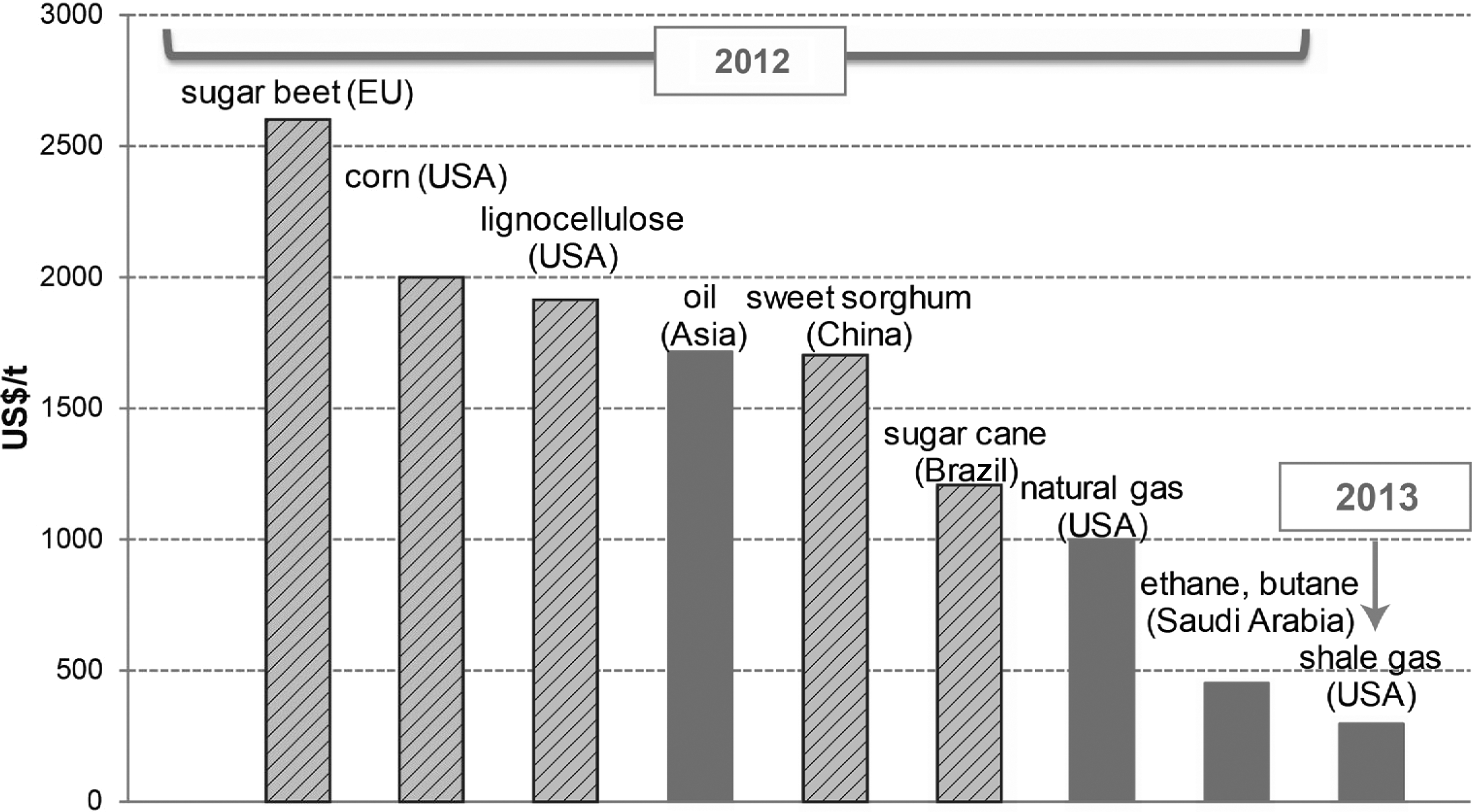

Capturing a bigger market share requires an improvement in the cost competitiveness of biobased processes. Feedstock cost on average accounts for 30–40% of chemical production costs (Fig. 3). Consequently, the production region and feedstock source dictate total production costs (Fig. 4). 10 Biobased ethylene based on Brazilian sugar appears to be the most competitive, but it is still more costly than fossil-based ethylene, particularly in light of the cheap feedstock opportunities presented by shale gas development in the United States. Reducing the cost of biobased carbon sources is a challenge not only for biobased ethylene but for biobased chemicals in general.

Cost factors in chemicals production.

Cost of ethylene production depends on regional feedstock.

Succinic acid is a platform biochemical that is about to enter the bulk sector. In the chemical industry, succinic acid is a precursor to several bulk chemicals, including polyester polyols, butanediol follow-on compounds, coatings, plasticizers, and biodegradable polymers, but does not directly substitute for a fossil-based analog. Biobased succinic acid producers include Reverdia, a joint venture between DSM (Heerlen,The Netherlands) and Roquette Freres (Lestrem, France); Myriant (Cambridge, MA); and BioAmber (Minneapolis, MN). The companies have announced projects to build a combined 35,000 tonnes of biobased succinic acid, which they expect to be a fast-growing market. In 2012, BASF (Ludwigshafen, Germany) and Corbion (Diemen, The Netherlands) also founded a biobased succinic acid joint venture in Germany, called Succinity.

Natural compounds might replace fossil analogs such as ethylene or initiate new precursor markets like succinic acid, but to enter the bulk field with a broader product portfolio non-natural compounds should be available from biobased feedstock as well. In fact, 1,3 propandiol (PDO) has been since 2002, when DuPont (Wilmington, DE) and Tate & Lyle (London, UK) formed the joint venture DuPont Tate & Lyle BioProducts (Loudon, TN), the first example of a synthetic compound produced by a biological system. It is an Escherichia coli transformed by biosynthetic pathways from Saccharomyces and Klebsiella. 11 Another breakthrough in the field of non-natural bioproducts was reported this past summer, when Evonik (Essen, Germany) launched its pilot plant for ω-amino lauric acid (LL) from palm kernel oil at Fermas (Slovakia). This bio-LL may replace fossil butadiene as the central precursor to the high-performance polymer polyamide 12 (PA12) 12 with ecological and economical implications: 1) green PA12 comes into reach; and 2) an alternative molecule might help to balance the rising cost of butadiene when, due to increasing fracking and production of shale gas instead of naphta, the supply of crude C4 compounds becomes difficult.

Synthetic biology is expected to revolutionize biobased synthesis in the chemicals industry, with the development of artificial genes for defined synthetic steps in the form of gene cassettes for a specific reaction chain. Several such cassettes would be used to transform a host cell to produce the intended molecule, whether known to nature or not. To avoid unwanted side reactions, so-called “minimal cells” would serve as hosts. The genome of such cells is scaled-down to the physiological functions essential for viability and synthesis under production conditions. The expectation is that synthetic biology will expand the portfolio of biobased products in the chemical industry, lead to new procursors for high-performance products, and improve the efficiency of bioprocesses both for natural and non-natural bioproducts.

Food vs. Fuel

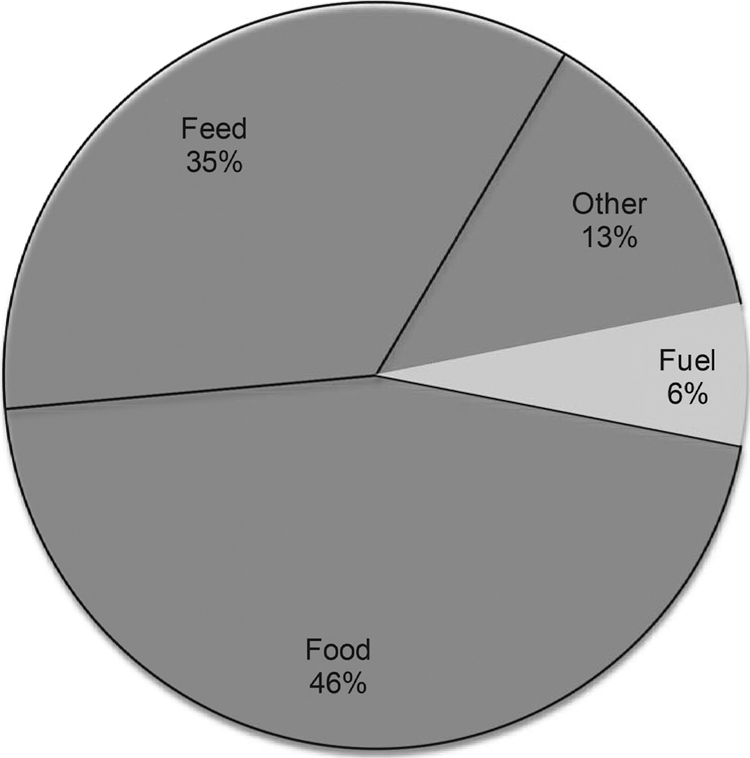

The example of biobased ethylene illustrates another hurdle to overcome as the market share of biobased chemicals grows to a significant scale. Only 25% of today's ethylene demand could be met by the 61 million tonnes of biobased ethanol produced at present. 6 Substituting all fossil-based ethylene would require more than 2 times the annual world sugar yield of 165 million tonnes. Given the fact that the current production of ethanol and sugar is already used for other purposes, it is obvious that state-of-the-art agriculture becomes a limiting factor in producing fuels and chemical feedstocks in addition to food, feed, and fibers. 13 According to the Food and Agriculture Organization (FAO) and the International Grains Council, 6% (149 million tonnes) of global cereals were expected to be used for fuel in 2013 (Fig. 5). 14

Use of global cereals (2.415 billion tonnes).

When it comes to the industrial use of food and feed crops, the public debate in general prioritizes food and feed production despite evidence that the competition is not about food or fuel but about land. 15 Nonetheless, the debate will further incentivize non-food biomass and drive its gain in relevance (Table 1). Volumes are currently limited, which demonstrates the relevance of resource-efficient use when considering the 11.8 billion tonnes of fossil carbon currently consumed. 16

Estimated Volumes of Non-Food Biomass

The European chemical industry declared early on that it would prefer to use non-food biomass as feedstock. Accessible resources such as residual agricultural, silvicultural, and marine biomass plus industrial and municipal organic waste meet this guideline. Broad industrial application depends, however, on cost-efficient processing and transformation.

Feedstock Sources

Current biotechnological processes for fuels and chemicals production primarily use C6-sugar, which is readily consumed by established microbial biocatalysts such as eukaryotic yeast and prokaryotic E. coli as a carbon source. C6-sugar is extracted directly from conventional crops such as sugar beets and sugar cane or derived through enzymatic digestion (amylase) of corn or wheat starch. Oil plants like soy, rapeseed, or oil palm are sources of vegetable oils used for food, feed, and industrial purposes. Biomass from sugarcane (bagasse) can be used to generate power, but most agricultural residues find only niche applications and are thus left on the ground. Residual biomass from sugar, starch, and oil plants mainly consists of lignocellulose, which is comprised on average of 70–80% C6-sugar and 20–30% C5 -sugar. These sugars are integrated into the complex and rigid lignocellulosic structure and are not as easily available as sugars from fruiting bodies or tubers. Mechanical and chemical pretreatment is necessary before the sugar can be released by enzymatic catalysis. The C6-fraction of lignocellulosic sugar can be fed into bioprocesses, but most established microbial biocatalysts are not prepared by nature to use the C5-fraction. It is necessary to introduce the suitable physiological tools into these cells to prepare them for lignocellulosic processes.

A number of large projects are underway to produce biofuels from residual biomass. Clariant (Basel, Switzerland) has launched a pilot plant in Germany for second-generation biobased ethanol production from wheat straw. POET-DSM Advanced Biofuels (Sioux Falls, SD) is preparing a plant in the United States using corn cobs, husks, leaves, and stalks. Whereas the POET-DSM unit uses a lignocellulosic enzyme cocktail produced by separate cultivation of the enzyme-expressing microbes, Clariant grows the lignocellose-degrading microbes directly on the feedstock.

In addition to feedstock from agricultural residues, lignocellulose from municipal solid waste (MSW) can also be used as feedstock. On July 1, 2013, Abengoa (Seville, Spain) launched a pilot plant in Spain that transforms 25,000 tonnes of MSW into 1.5 million liters of ethanol. And while lignocellulosic ethanol is set to reach production scale, biochemicals production based on second-generation feedstock sources is also being achieved. In March 2013, Direvo (Cologne, Germany) announced the first process to derive lignocellulosic lactic acid.

Another relevant component of lignocellose (comprising 20–30%) is lignin, However, it has only a few applications at present–in construction materials and ceramics, dyes, pesticides, and binding agents in animal feeds and briquettes. The vast majority (98%) of lignin is burned for heat generation because methods to tranform it into useful products are lacking.

Only 70–80% of the lignocellulosic biomass carbon is currently entering the chemical value chain through fractionation into C6- or C5-sugar and lignin. Breaking down whole biomass into C1-compounds might result in a higher carbon transformation yield. Conversion of biomass into synthesis gas (syngas; CO, CO2, H2) is one such option. The Karlsruhe Institute of Technology (Karlsruhe, Germany) uses fast pyrolysis close to the field to convert biomass into bio-oils that are then shipped to central gasification plants. 17 Fischer-Tropsch heterogenous catalysis enables the generation of syngas as a source for hydrocarbons, but without sufficient control of the molecular weight. In contrast, biological transformation of syngas by anaerobic Clostridia delivers defined hydrocarbons because of the microbes' specific biosynthesis. Suitable species that not only excrete the natural intermediates ethanol and butanol but can also be genetically engineered to produce additional target chemicals are also being widely explored. 18 For example syngas-based fermentation of a precursor to acrylic glass (2-hydroxyisobutyric acid) was reported for the first time in December 2013. 19

Gas fermentation has gained attention not only because of the prospect of biomass-derived syngas, but also because any organic material such as MSW can be used. Carbon monoxide and carbon dioxide (CO2) are present in large amounts in industrial flue gases, such as those generated at steel mills (∼33% CO2) and power generation plants (∼14% CO2). The technical viability of feeding flue gas as the only carbon source into gas fermentation has been demonstrated by Oakbio (Cupertino, CA), which transformed CO2 from cement plant flue gas into building blocks for bioplastic, and by Lanzatech (Auckland, New Zealand), which demonstrated its process at a 300 tonnes biobased ethanol pilot plant at a Bao Steel mill in Shanghai. 20, 21 Lanzatech and Siemens Technologies (Erlangen, Germany) signed a partnership agreement on June 19, 2013 for the conversion of steel mill off-gases into bioethanol, and on December 9, 2013, Evonik added another step to the future gas fermentation value chain by partnering with Lanzatech on polymer building blocks. 22,23 Both deals indicate the potential of gaseous carbon sources and, the fact that gas fermentation is suitable for fossil-based flue gas as well as biobased syngas, might also attract early investors.

Another C1-compound gaining relevance is methane in the form of biogas. In principle, any aqueous solution or suspension containing carbon and nitrogen sources complemented by growth factors delivers biogas. In Germany, 7,500 biogas plants generated 3.1 gigawatts of electrical power—equivalent to one nuclear power station—in 2012, proving that biogas can contribute significantly to power generation. In Brazil, the residual broth in ethanol fermentation, dubbed vinasse, offers another biogas option. The Brazilian state of Gojas produces 37 million tonnes of vinasse annually. This volume contains only 1.4% organic material, but the resulting biogas is theoretically an energy resource in the gigawatt range. These two examples are both based on agricultural residues, but biogas may also be sourced from liquid municipal waste, particularly in heavily populated regions like Tokyo (35 million people) and Seoul (25 million people). Such cities might be advantageous sites for biogas on-site power generation and, after purification, on-site gas fuel production. Biogas can also be fed into the grid as a substitute for natural gas, thus leveraging established infrastructure.

Converting sugar, biomass, and industrial and municipal waste are promising options for establishing biobased value chains. However, when comparing biorefineries and conventional, fossil-based refineries, there is a fundamental difference from the perspective of economies of scale, and an obvious disadvantage for biorefineries. Whereas fossil-based refineries are integrated into the global feedstock grid of on-shore pipelines, off-shore sea communication, and harbors, biorefineries in general have to depend on regional feedstock supply. The logistics of oil transport are easy and cost-efficient over long distances, and readily serve global markets. Oil is produced year-round, at near-homogenous consistency; is chemically stable; and has a high energy and carbon content (∼85%). In contrast, biomass is a seasonal product, collected from large areas, transported batch-wise, on-shore by truck and railway, is heterogenous in composition, is biologically unstable, and has relatively low energy content and carbon density (roughly 50% carbon derived from 40–55% cellulose, 10–35% hemicellulose, and 18–41% lignin). The logistics of utilizing bulky biomass is therefore expensive and has limited current biorefinery infrastructure to a hinterland region of about 100-km radius and processing capacity of about 130,000 tonnes of carbon. Braskem's 200,000 tonnes/year biobased ethylene plant in Brazil consumes about 280,000 tonnes of sugar (118,000 tonnes of carbon), which is the yield of 65,000 hectares (160,618 acres) of sugarcane (equivalent to a 100-km radius area). In contrast, the average capacity of a conventional ethylene plant is larger by a factor of 7 (∼1.5 million tonnes of ethylene). Europe's largest biobased ethanol plant (360,000 tonnes/year; CropEnergies, Mannheim, Germany) converts about 180,000 tonnes of sugar (76,000 tonnes of carbon) annually. Developing more efficient logistics and increasing the capacity of biorefineries is one of the urgent challenges for improving their competitiveness.

Biorefinery Integration

Another unsolved challenge is how best to integrate biorefineries into the existing large-scale infrastructure of oil refineries and chemical plants. Germany's chemical industry—the fourth largest in the world—depends on importing 86% of its oil needs, 90% of gas, and 65% of bio-feedstock. Central production sites, which are home to various individual companies, are linked to global feedstock markets via oil and gas pipelines from Russia and the harbors of Antwerp, Belgium; Rotterdam, The Netherlands; and Triest, Italy. Processing intermediates such as ethylene are transported between production sites via pipelines (Table 2), thus allowing cost-efficient distribution of large-scale platform chemicals to companies executing the next step of transformation in the value chain.

Olefin Pipelines Linking European Chemical Production Sites

1€=USD1.37

ARG(formerly Aethylen-Rohrleitungs-Gesellschaft)operates a pipeline grid linking Antwerp to Cologne and the Ruhr industrial area.

Biorefineries need to find a way to integrate into this existing infrastructure to be able to combine their advantegeous carbon footprint with the large-scale benefit of conventional chemical processing. The Ghent Bioeconomy Valley (Ghent, Belgium) and its Bio Base Europe Pilot Plant are an excellent example of how this can be accomplished. Connected to the Port of Ghent's logistics infrastructure, the pilot facility uses local and imported biobased feedstock for the production of high-value and bulk chemicals, as well as fuel and power. The pilot plant is prepared to develop and test biorefining methods as well as their integration into chemical industry infrastructure. Technically easy options include feeding biogas into natural gas pipelines or biobased ethylene into the downstream chemical processing infrastructure. More platform chemicals upstream in the fossil-based and biobased value chains might fit into the existing infrastructure as well. Cost of feedstock will be a key factor, however.

Linking biorefineries to the global feedstock infrastructure not only helps to take advantage of large-scale, downstream processing facilities but is also a prerequisite for biobased production to become a relevant partner to the chemical and fuel industries. Using the chemical infrastructure for distribution of biobased intermediates is a promising option for biomass-rich regions looking to integrate into global energy and chemical value chains. This can only be the first step in building an infrastructure specifically adapted to the evolving global bioeconomy, however. At some point the global dimension of the bioeconomy will have to come into play. The German chemical industry delivers 30,000 different chemicals, but its feedstock base is primarily fossil-based—13.5 million tonnes of oil (71%), natural gas (14%), coal (2%), and 2.7 million tonnes of bio-feedstock (13%). 24 The oil volume contains 11.5 million tonnes of carbon (85%). Replacing this with biomass theoretically requires at least 23 million tonnes of biomass that is comprised of 50% carbon on average. Local straw, of which 11.3 million tonnes providing 5.6 million tonnes of carbon are available annually, might meet half of this chemical demand, but only if other sectors, like energy (ethanol) or livestock breeding do not claim access. 25 Even when considering additional domestic biomass resources such as wood, future imports of biobased carbon to serve all biomass-consuming industries seem realistic.

Global demand and competition must be considered when determining the availability of international resources. Chemical industries use 310 million tonnes, or 8% of the world's oil consumption. This is equivalent to 265 million tonnes of carbon, which would require at least 530 million tonnes of lignocellulosic biomass to displace. Sugarcane biomass (globally 530 million tonnes) nearly half of which originates in Brazil—could meet this demand if the chemical industry were its only consumer.

In fact, the chemical industry is a rather minor consumer of carbon compared to other industries. About 93% of global oil consumption serves the energy sector. The 3.3 billion tonnes of fossil oil carbon (85% of the total 3.9 billion tonnes of oil produced in total) consumed by the energy sector corresponds to roughly half the current biobased carbon provided by agriculture (7 billion tonnes of carbon in 14 billion tonnes of biomass). 26 This underscores the future challenges faced by the biobased industries. To avoid competing with the food and feed sector, the industrial bioeconomy must explore any available carbon source and focus energy generation on sustainable non-carbon technologies (e.g., hydro, wind, solar, ocean, geothermal power).

Conclusions

OECD and states like those that comprise the BRIC nations recognized this carbon challenge and put together bioeconomy roadmaps. 27 The European Union, which since 2005 has committed to the bioeconomy as a model to slow climate change and ensure jobs and economic competitiveness, has since increased the budget dedicated to “food security, sustainable agriculture, marine and maritime research and the bioeconomy” within its Horizon 2020 program (2014–2020; €70 billion (USD95.76 billion) in total) to €4.2 billion (USD5.76 billion) in addition to the €2.3 billion (USD3.16 billion) invested as part of the Seventh Framework Programme (2007–2013). Germany initiated the National Research Strategy BioEconomy 2030 in 2010 with a budget of €2.4 billion (USD3.29 billion). In 2011, the United States adopted the National Bioeconomy Blueprint, while Malaysia presented its National Biomass Strategy, Russia approved its National Technology Platform Bio-Industry and Bio-Resources (Biotech 2030), and China runs a three-step bioeconomy program (2007–2020).

Translating these strategies into a profitable bioeconomy is not only a technological issue, but it is also a question of cost-competition with the fossil-based economy and integration into new value chains. Producing biobased carbon is still more expensive than fossil carbon production. Fossil carbon also has an advantage in the profit margin when comparing production costs and market price. Cutting the cost of biobased carbon starts with breeding crops for industrial purposes. Input traits such as growth on marginal land and output traits like higher biomass/fruit ratio, reduced biomass-lignin, or adaptation to processing parameters should be targeted. Collection of biomass and wood residues requires machinery with integrated densification and early processing steps. Another important cost-cutting target is the transport of biomass from the field to intermediaries and central biorefineries. Additionally, specific infrastructure needs to be developed to exploit industrial and municipal waste. Finally, the interface of small- to medium-size biobased carbon processing with large-scale chemical production facilities remains an open question—one that Germany has since 2011 attempted to address by integrating a lignocellulosic pilot plant into a chemical site at Leuna. 28

Solving these issues requires that significant public and private investment be made in parallel with unfolding bioeconomy value chains. Because of the global dimension of the future biobased carbon trade, the formation of new value chains goes beyond individual companies and national programs. It needs active participation by industries, investors, and academia and the development of value chains according to a coordinated approach. Domestic and international cooperation across sectors is key and will be particularly promising if the partnering regions have a strong position in renewable resources, science, or forward-thinking industrial sectors.

One such model, founded in 2008 to pursue such a bioeconomy-focused strategy, is Germany's Open Innovation Cluster on Bioeconomy, CLIB2021. This cluster has a strong foundation in the chemical industry and academia and works with stakeholders in Europe, Russia, North and South America, China, and Southeast Asia. Part of CLIB2021's strategy is to join feedstock-rich regions with technology champions and industry leaders. CLIB2021 has partnered with Brazil, Canada, Malaysia, and Russia in exploring biobased feedstocks, while pushing academic R&D and working to accelerate industrial cooperation. In Europe, the ARRR-Region, which covers the harbors of Antwerp and Rotterdam along the Rhine river down to the Ruhr region in the German state of Northrhine-Westfalia, has been identified as an excellent candidate to integrate the modern bioeconomy in a highly developed cross-national industrial region that spreads out down the Rhine river to Ludwigshafen—home to the world's biggest chemical company, BASF— to Greater Basel where the Swiss chemical industry is located. 29

This activity is discussed in the context of the EU's framework programme Horizon 2020 (2014–2020), in which two public-private partnerships (PPPs) are under preparation: BIC (Biobased Industries Consortium), which is focused on biorefinery value chains, and SPIRE (Sustainable Process Industry through Resource and Energy Efficieny), Both PPPs intend to invest several billion euros of private and public money, thus validating the competitive value of the bioeconomy. The time is right to take an active part in the bioeconomy and realize its commercial potential.