Abstract

Introduction

The GreenPremium is basically understood as the extra-price market actors are willing to pay for a product just for the fact that it is “green” or, in our specific case, “biobased” (derived from biomass). Several questions arise when analyzing the GreenPremium effect and attempting to understand the reasons for market actors to pay a higher price.

How exactly is GreenPremium to be defined and understood? Are GreenPremium prices really paid by the market? In which markets are which GreenPremium prices being paid? What are the relevant motivations and drivers? Do differences concerning the GreenPremium level depend on the position in the value chain? Who pays the extra prices? Will market actors only pay the GreenPremium for a limited time? Do special GreenPremium prices depend on single value-adding factors, such as biobased, biodegradable, non-food and/or GM-free?

This work was funded by two European projects, BIOCORE (“Biocommodity refinery,” a biorefinery concept for the transformation of biomass into 2nd-generation fuels and polymers, n°FP7-241566) and MouldPulp (new biocomposites from bioplastics and pulp fibres, ERA-NET WoodWisdom-Net 2, project number 033R061B) in the framework of two comprehensive techno-economic evaluations including market research on volumes and prices.

Methodology

Our surveys and analysis covers cases of GreenPremium prices for 35 biobased chemicals, polymers, and plastics (drop-in and new biopolymers), and compounds—and additional background information from market insiders for the GreenPremium prices. Information was obtained from expert interviews with representatives of leading companies and market researchers and consultants, online surveys, market observations, and a literature analysis conducted in late 2012 and 2013.

This Industry Report includes excerpts from a report prepared by nova-Institute, March 2014. The full report is available at

Definition of “GreenPremium” Prices

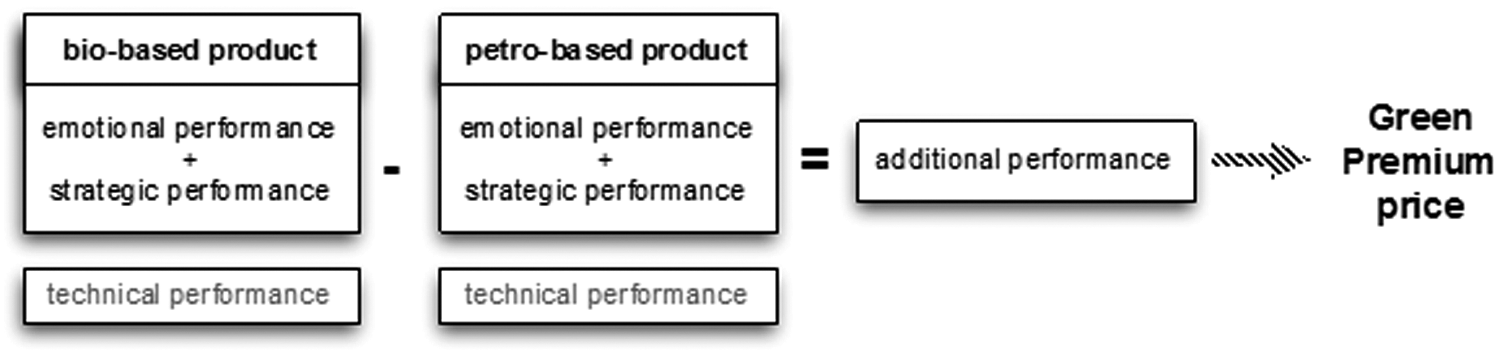

The GreenPremium is commonly understood as the additional price market actors are willing to pay for a product just for the fact that it is “green” or, in our specific case, “biobased” (i.e., derived from biomass). nova-Institute is putting forward the following definition, which will be used in this study: GreenPremium price is the additional price a market actor is willing to pay for the additional emotional performance and/or the strategic performance of the intermediate or end product the buyer expects to get when choosing the biobased alternative compared to the price of the conventional counterpart with the same technical performance ( Fig. 1 ).

The GreenPremium price is defined as an additional price that depends on the additional emotional and strategic performance of the biobased product, independent of its technical performance.

Technical Performance

Technical performance is based on mechanical, rheological, thermal, optical, and chemical properties. The properties are of relevance in regard to processability, waste management (e.g., aspect of biodegradation) and health-related compatibility or application specific characteristics like barrier properties. The properties can be valued differently from one application to the next and depending on the underlying process. In the case of a biobased drop-in solution, the technical performance is precisely the same as its substitute (it can be assumed that the carbon footprint would differ, but that is not part of technical performance). Although specific technical performance could be an important reason for companies to choose or not choose a biobased alternative, this is not part of the GreenPremium price.

Emotional Performance

Emotional performance represents the possibility of assigning a value to the product just because of its nature, e.g., the perception of its nature by the customer. Being seen as green, biobased, sustainable, and/or having a lower carbon and environmental footprint can create a specific emotional performance. The emotional performance can give the customer the feeling that he/she is doing something good by buying the product. The emotional performance increases towards the end of the value chain as end-consumers pay more attention to the “Green Touch” of an application than do companies. 1,2 The increased emotional performance of a product enables the producer and distributor to obtain higher prices for their products and higher selling volumes on the market.

Strategic Performance

This expresses the possibility of positioning the company via the product in the market as a green, sustainable, low-carbon and innovative company, as a forerunner with exclusive access to a new material, or in terms of supply chain diversification, an opportunity to gain a mid-term/long-term market advantage, to hedge the oil price or other price volatilities, and to comply with regulations or expected regulations before the competition does. The strategic performance of a biobased product is strongly dependent on the specific market actor's position in the value chain. An increased strategic performance enables the producer or distributor to get a better position and reception of the company on the market—via the product placement.

The GreenPremium paid for emotional and strategic performance is often associated or mixed with additional technical properties such as biodegradability, waste treatment, or better barrier properties in food packaging. These technical aspects (see technical performance) are not apart from emotional or strategic performance, even though this is not always clearly differentiated by the users.

Results and Discussion

The results of the surveys and analysis of 35 cases of biobased chemicals, polymers, and plastics clearly demonstrate that GreenPremium prices do indeed exist and are paid in the value chains of different biobased chemicals, polymers, and plastics—especially for new biobased value chains and the European market. In line with the definition of GreenPremium, the motivation to pay additional prices is the biobased product's expected increased emotional and strategic performance.

In the absence of any policy incentives, GreenPremium prices are very important for the market introduction of biobased products, and many new biobased polymers and plastics would not even exist without customers willing to pay GreenPremium prices. “The GreenPremium exists, and has enormous impact to get a project financed.” 3

Biobased plastics are usually more expensive than their conventional counterparts at present, and companies also face supply chain challenges when they switch from one raw material solution to another. Nevertheless, the biobased plastics market continues to grow, and multinational brand-owners like Coca-Cola, PepsiCo, Nestlé, Danone, Ford, Toyota, Mazda, Procter & Gamble, and AT&T, as well as many other companies involved in all kinds of branches and applications, already use bioplastics in their products or packaging. 4,5 “Companies that have set goals and objectives to become more sustainable and to leave a more sustainable impression on consumers have an interest in biobased materials.” 6 If materials meet the necessary technical requirements, companies are willing to pay a ‘GreenPremium.’ In regard to their biobased products Braskem generally states: “Regardless of what each customer pays, the important fact is that a GreenPremium is necessary and accepted.” 7

Results of the Linkedin Survey

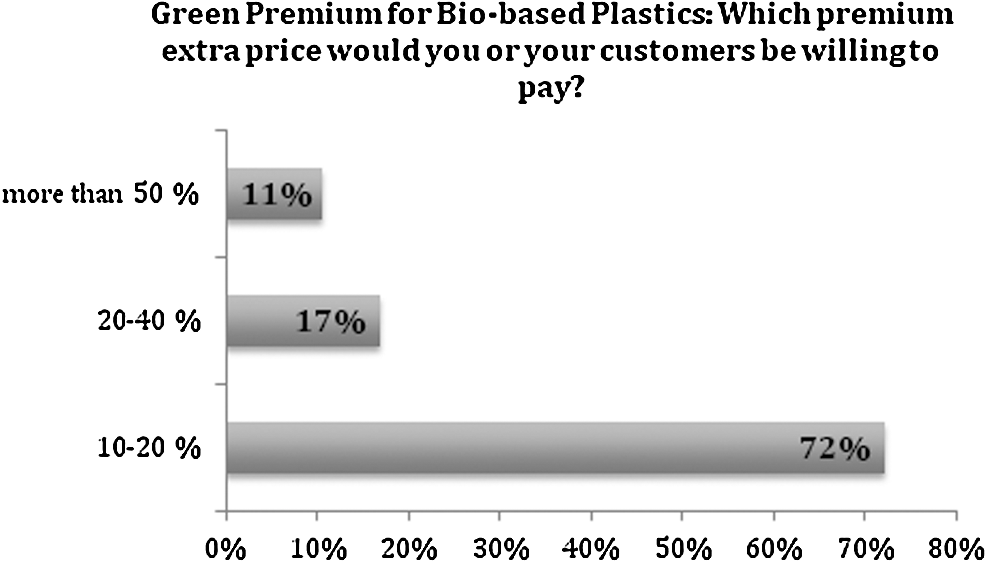

Our survey of the biobased community on “LinkedIn” in 2013 also clearly showed the existence of GreenPremium prices as well as the ranges of GreenPremium and additional background information. The participants voted on the following question: “Green Premium for Biobased Plastics: Which premium extra price would you or your customers be willing to pay?” which nova-Institute addressed to the groups “Bioplastics” and “myBIO Community—Biotechnology Connections,” both of which are involved in the biobased economy. 8 The voting represents participants who were—or whose customers were—in principle willing to pay a GreenPremium. Participants could also make comments, i.e., give reasons and explanations.

Figure 2 shows the level of additional price that market actors would pay for biobased plastics. The values are based on 47 respondents, representing a random sample of biobased plastics producers, traders, and further experts (LinkedIn 2013). 8

Level of GreenPremium (in percentage) that would be paid for biobased plastics, n=47 (Status: August 20, 2013).

The diagram shows that 72% of all respondents estimate that customers (independently of their position in the value chain) would be willing to pay up to 20% more if plastics were biobased instead of fossil-based. Furthermore, 17% would be willing to spend between 20% and 40% more compared to a fossil-based alternative, and 11% of all respondents would even pay a premium of more than 50%.

Greenpremium Price Ranges

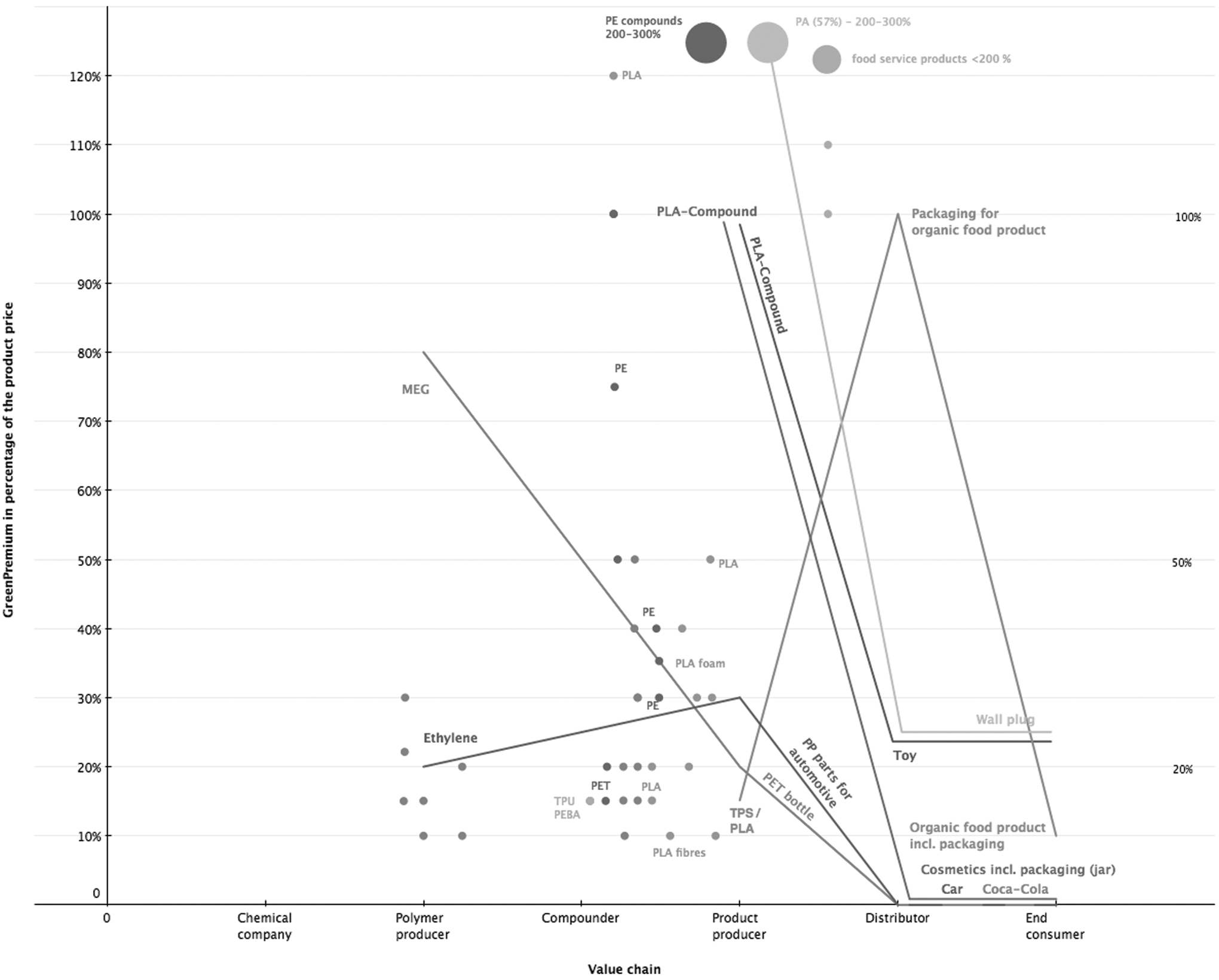

Fig. 3 shows the results of all expert interviews and surveys undertaken and analyzed in the context of this study. Detailed information on analyzed cases of bio-based materials, products, and companies are available from the authors.

Analysis of GreenPremium prices along the value chain of different biobased chemicals, plastics, and end products. Solid lines represent one value chain; single dots represent single findings.

The figure shows the identified GreenPremium levels depending on where they are paid in the value chain; for example, the polymer producer buys a building block from the chemical company and might pay a GreenPremium for it; or the end consumer buys the final product and might pay a GreenPremium to the distributor.

The range of reported GreenPremium prices in the various branches and applications analyzed lies between 10–300% above the conventional petrochemical product with the same technical performance. Most of the GreenPremium price findings are in the range of 10–20% for biobased intermediates, polymers, and compounds, followed by the range 20–40%. Higher GreenPremium prices could only be obtained in specific cases. For the end consumer, the range of GreenPremium prices for biobased products goes from 0% (car, cosmetics, bottle) to 25% (wall plug, toy) with, in the middle, a 10% GreenPremium for organic food with biobased packaging.

These are huge extra prices compared to biofuels. A recent US survey shows that even consumers involved in the biofuel sector only accept 1–3% higher prices for biofuels with the same technical performance as fossil fuels (details below).

Some identified GreenPremium prices are part of the same value chain. The empirical data show that for all lines the GreenPremium price levels (in percentage terms) decrease along the supply chain towards the end consumer, as do the lines for ethylene and TPS/PLA after an intermediate peak. Relatively high GreenPremiums are paid for (early) intermediate products, whereas the end consumer pays a much lower GreenPremium or even no extra price at all.

The reason for this is that intermediate products like building-blocks, polymers, or compounds only account for a minor fraction of overall product costs, with the effect that end-product costs increase only slightly. The material costs share (including the GreenPremium) of the total product price decreases along the value chain. The highest GreenPremium price (in percentage) is paid predominately for the intermediates. And without this enhanced and confirmed willingness to pay high GreenPremium prices for intermediate products, many new biobased value-chains would not have been implemented at all.

Nobody would risk an investment to produce the biobased building-block monoethylene glycol (MEG), for example, if no big business-to-business (B2B) customer guarantees a GreenPremium price for this intermediary to produce biobased polyethylene terephthalate (PET) with an expected increased emotional and strategic performance. This example also shows two additional aspects, often discussed in the context of GreenPremium: • The commitment to pay GreenPremium prices for biobased intermediates or polymers has to last for several years, otherwise the upstream investment is not profitable—and such long-term commitments are indeed being made. • The highest GreenPremium levels are mainly located in the beginning or middle of the value chain, since the end consumer pays the lowest (or even no) GreenPremium price. The main reason behind GreenPremium is an expected increased emotional and strategic performance of the product for the product's producer and/or distributor.

In some cases, the end consumer pays a certain GreenPremium price—they are willing to pay for the “Green Touch” (emotional performance) as the wall plug example shows; in other cases, the product producer is willing to bear the extra costs themselves as there is a strategic benefit to them; e.g., a biobased Coca-Cola bottle contributes to a greening of the company's image (strategic performance).

The green line rises towards the middle of the supply chain, which means that the highest GreenPremium levels are paid by the distributor for the green packaging. This situation can occur when a product is subject to very high emotional performance that would allow producers and distributors to pass on their extra costs to the end consumer. Biobased packaging for organic food can serve as an example, with a small fraction of packaging costs and high emotional performance through “green packaging” making a perfect fit with the consequent “green image” of the organic food product. The distributor can pass his extra costs of the “green packaging” (+100%) on to the end consumer, who only has to pay 10% GreenPremium for the final organic food product. (The high GreenPremium price for the “green packaging” can be explained by a small production volume.)

These unconnected dots represent other empirically proven GreenPremium levels in the market, which could not be allocated to specific supply chains. The distribution indicates above-average GreenPremium levels for compounds and polymers compared to chemicals or end products.

Main Drivers of Emotional Performance

The most commonly mentioned aspects in the context of the emotional performance of a biobased product are as follows: • Benefits in marketing due to ∘ Green or environmental friendly image ∘ Reduced carbon footprint ∘ Access to “eco-labels” • Additional benefits and public attention from exclusive access to scarce, new materials • Cost efficient image effects are possible, if the material costs account for only a small share of overall production costs or the GreenPremium expenses can be fully and directly passed on along the value-added chain • Niche markets can be very sensitive to emotional performance • The emotional performance can give the customer the feeling of doing something good by buying the product.

Additional product properties such as the feedstock used for the polymer production could have an impact on the GreenPremium level. Feedstock from genetically modified (GM) crops or food crops will achieve lower GreenPremium prices compared to non-GM and non-food crops. The level depends mainly on their emotional performance in individual cases. For non-GM-derived biobased plastics the extra premium price can range from 0% to over 100%, mainly depending on specific markets and regions. In regard to the emotional performance behind the mentioned product properties, the respective GreenPremium level is strongly dependent on end-consumer preferences. Non-GM crops or ones “not in competition with food” play a more important role the closer the position in the value chain to the end consumer. 1

The data within the study are largely based on estimations of the European market. It should also be mentioned that the willingness to pay GreenPremium prices is relatively high in Europe, whereas in China it is relatively low, and in North America it is somewhere in between. 9

Additional findings from surveys and literature

Experience shows that consumers tend to pay GreenPremium prices (and hence pass on the difference to other actors in the supply chain) when the environmental or social benefits are explained to them. 10 “The consumers are the driving force. Some consumers already pay a premium for less polluting cars, for organic food and for green plastics, and they are constantly growing in number. ‘Being green’ is the premium, and the consumer shall pay for it. Local regulation can be helpful, but it is definitely the demand that makes the difference. And the current trend is going green, worldwide.” 11

The examples of Coca-Cola and Toyota confirm this assessment, as the image of a product and the emotions customers associate with it become more and more important in certain markets. 9,12 GreenPremium prices can even be achieved for biobased products that can be seen to be controversial from an environmental point of view, as shown by biobased polyvinyl chlorides (PVCs). Prerequisites are, however, exclusive contracts for the customer and that the target markets are susceptible to emotional performance, e.g., flooring and pharmaceutical films. 13

An evaluation of the US market conducted by P&G largely confirms this trend. “Roughly 80% of consumers are either highly engaged with environmental sustainability (they will accept some performance trade-offs for products with better environmental footprints), or are ‘eco-aware’ but will not accept trade-offs. The latter group (70%) are considered the mainstream and are an important target group for biobased products. The remaining 20% are indifferent; in the US, half of this 20% self-classify as ‘never greens’.” 14 Similar results have been revealed by the National Retail Federation, showing that 70% would be willing to pay a premium of at least 5%. 15 Other analyses confirm more generally that “consumers are willing to pay slightly more, but not huge amounts more.” 16

Main Drivers of Strategic Performance

The most-often mentioned aspects in the context of the strategic performance of a biobased product—strategic benefits for the company—are the following: • Creating a positive public awareness and improving corporate identity of the company by: ∘ Meeting sustainability targets ∘ Reducing the product carbon footprint, covering CO2 reduction targets ∘ Strengthening the green company image • Forerunner in technology, public perception as an innovative company, early experiences with potentially long-term cost efficient materials, pathways and products • Meeting public regulations or expected regulations in advance • Increased feedstock diversity and security; supply chain diversification and independency of price volatilities • Benefit from potential subsidies or public incentives • Contributing to a specific corporate identity based on being environmentally friendly, e.g., by reducing the company's carbon footprint, or expressing sustainability and reduced environmental impact.

6,17,18

According to a survey by Genomatica and ICIS, 72% of the chemical producers said their customers are expressing interest in sustainability products. This market-based pull has grown much stronger over the last five years. As a result nearly half of the companies (45%) reported that they have investments in research and development for using renewable feedstocks. 19

Leaving aside public regulations, from a market point of view “gaining market potential” as well as “supply chain diversification” and “a direct/short-term increase of return on investment” are the predominant factors when it comes to strategic intentions. 20

Greenpremium in the Automotive Sector

The study by Hasson and Mestanza 2011 covering OEMs' and Tier X suppliers' willingness to buy biobased materials in the automotive sector identified the following reasons (Table 1), which mainly show strategic aspects. 21 Hasson and Mestanza identified the ranges of willingness to pay an extra price for biobased materials shown in Figure 4. The results show that the GreenPremium prices are lower in the automotive sector than in other branches.

Acceptable price premium for biobased materials in the automotive industry. 21

What Is the Main Reason Why OEMs or Tiers Have or Feel Pressure for Using More Biobased Polymers? 21

Greenpremium for Biofuels?

In early January 2014, Biofuels Digest (

The result shows that over 75% of end consumers in the US involved in the biofuel sector are willing to pay an extra price of between 0–3% for biobased fuels, and only 15% of those end consumers would accept 6–8% more. It is to be expected that the willingness of the average consumer is much lower.

Conclusions

The results of the surveys and analysis of 35 cases of biobased chemicals, polymers, and plastics clearly demonstrate that GreenPremium prices do indeed exist and are paid in the value chains of different biobased chemicals, polymers, and plastics—especially for new biobased value-added chains and on the European market. In line with the definition of GreenPremium, the motivation for paying additional prices is the biobased product's expected increased emotional and strategic performance. In the absence of any policy incentives, GreenPremium prices are very important for the market introduction of biobased products, and many new biobased polymers and plastics would not even exist if there were no customers willing to pay GreenPremium prices.

The range of reported GreenPremium prices in the various branches and applications analyzed ranges from a 10–300% premium over the conventional petrochemical product with the same technical performance. Most of the GreenPremium prices found lie within a range of 10–20% for biobased intermediates, polymers, and compounds, followed by the 20–40% range. Higher GreenPremium prices could only be obtained in specific cases. For the end consumer the range of GreenPremium prices for biobased products goes from 0% (car, cosmetics, bottles) to 25% (wall plug, toy) with, in the middle, a 10% GreenPremium for organic food with biobased packaging.

The empirical data show that in all cases the GreenPremium price levels (in percentage) decrease along the supply chain towards the end consumer, sometimes with an intermediate peak. The two main reasons are: the material costs share of the total product price decreases along the value chain; and the highest GreenPremium price is paid predominately for the intermediates. Without this enhanced and confirmed willingness to pay GreenPremium prices for intermediates, many new biobased value-chains would not have been implemented at all.