Abstract

Introduction

The emerging biofuels industry currently relies primarily on the yeast strain Saccharomyces cerevisiae for the production of fuel alcohol from food sources such as corn, wheat, sugar cane sucrose and molasses. S. cerevisiae is also the fermentation microorganism of choice for the production of fuel alcohol from non-food sources in the initial second-generation, or lignocellulosic biorefineries. Not all lignocellulosic ethanol facilities utilize S. cerevisiae, but this yeast is currently the leading microorganism due to its superior industrial characteristics and ease of use.

In this article, we provide insights on the lignocellulosic biofuels industry, its current state of development, and how it may evolve as it expands and begins to replace significant quantities of nonrenewable fossil-based transport fuels with ethanol derived from non-food renewable biomass. We offer predictions on how the evolving lignocellulosic biofuels industry is likely to impact sugar cane production from an Australian perspective.

The information and conclusions come from the perspective of Microbiogen, an Australian-based industrial biotechnology research and development group that specializes in S. cerevisiae yeast. The company has developed unique and proprietary breeding technologies that can lead to the optimization of yeast strains for industrial purposes, and in particular the production of ethanol from a variety of sugars and the upgrading of low-value waste streams into high-value feed products.

S. cerevisiae yeast is the world's most utilized microorganism, with millions of metric tons produced on an annual basis. This particular strain of yeast is utilized more than all other microorganisms combined for industrial purposes and underpins in excess of $300 billion in products per year. Industries in which S. cerevisiae dominates include baking, brewing, fuel ethanol, spirits, wine making and speciality alcohols.

Lignocellulosic Ethanol: Once a Dream, Now a Reality

Looking back 5 years, the lignocellulosic fuel ethanol industry was non-existent. Extensive work had been conducted on various aspects of technology development, but no company or consortium had actually built a commercial-scale facility. Technology was still under development and many of the smaller start-ups had failed to bridge the “valley of death.” In the past, Microbiogen has collaborated with more than 20 companies to develop fermentation solutions that could be incorporated into biochemical lignocellulosic facilities. Despite all the good work and best intentions, very few first-wave technology developers are still operating today. It is important to understand that producing lignocellulosic fuel ethanol is not in itself a new technology–it has been done for nearly 100 years. The key challenge with lignocellulosic fuel ethanol biorefineries is to make them produce the fuel efficiently and economically.

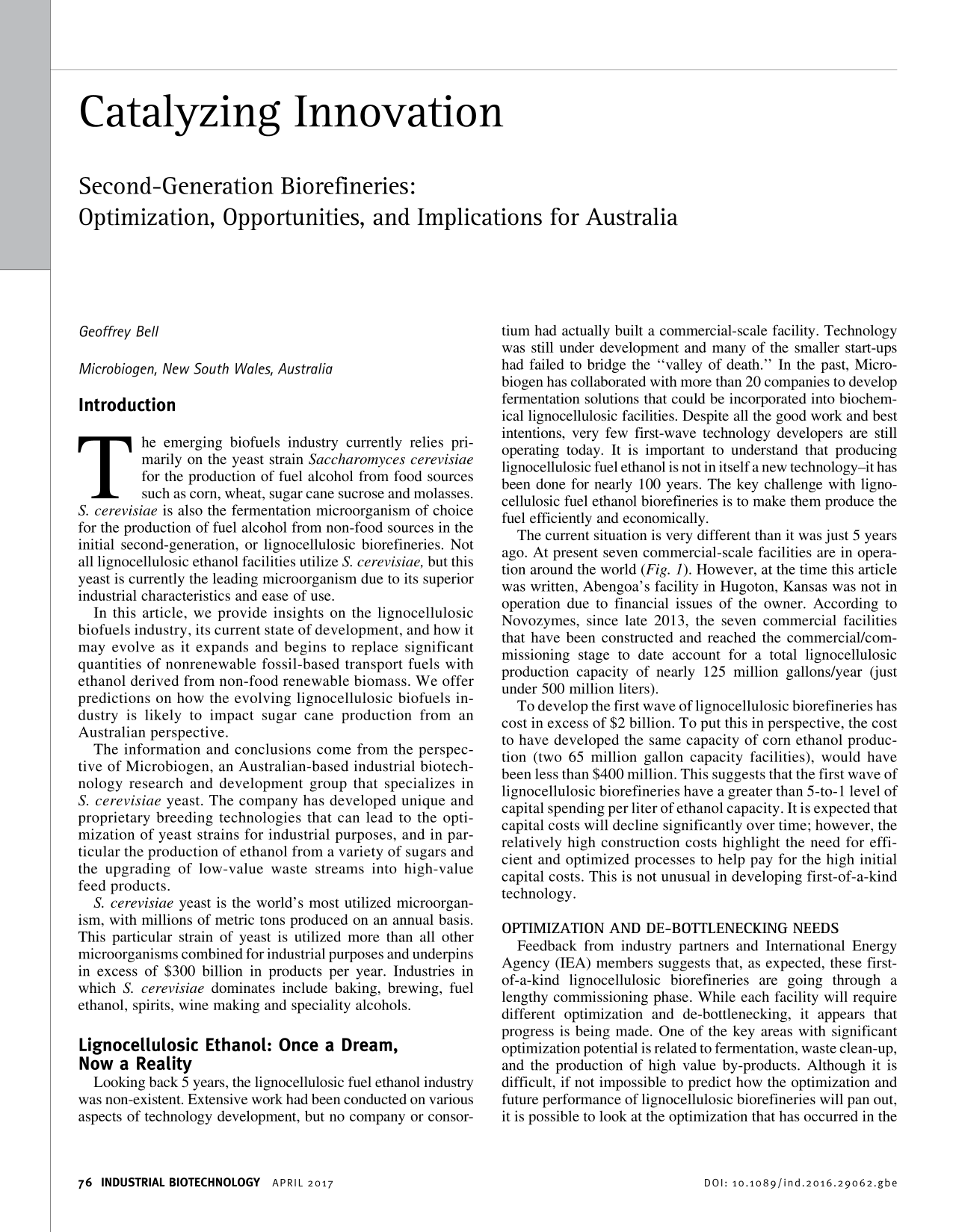

The current situation is very different than it was just 5 years ago. At present seven commercial-scale facilities are in operation around the world (Fig. 1). However, at the time this article was written, Abengoa's facility in Hugoton, Kansas was not in operation due to financial issues of the owner. According to Novozymes, since late 2013, the seven commercial facilities that have been constructed and reached the commercial/commissioning stage to date account for a total lignocellulosic production capacity of nearly 125 million gallons/year (just under 500 million liters).

Development time line of lignocellulosic biofuel commercial facilities (Source: Novozymes, presentation at BIO World Congress on Industrial Biotechnology, May 2016).

To develop the first wave of lignocellulosic biorefineries has cost in excess of $2 billion. To put this in perspective, the cost to have developed the same capacity of corn ethanol production (two 65 million gallon capacity facilities), would have been less than $400 million. This suggests that the first wave of lignocellulosic biorefineries have a greater than 5-to-1 level of capital spending per liter of ethanol capacity. It is expected that capital costs will decline significantly over time; however, the relatively high construction costs highlight the need for efficient and optimized processes to help pay for the high initial capital costs. This is not unusual in developing first-of-a-kind technology.

Optimization and De-Bottlenecking Needs

Feedback from industry partners and International Energy Agency (IEA) members suggests that, as expected, these first-of-a-kind lignocellulosic biorefineries are going through a lengthy commissioning phase. While each facility will require different optimization and de-bottlenecking, it appears that progress is being made. One of the key areas with significant optimization potential is related to fermentation, waste clean-up, and the production of high value by-products. Although it is difficult, if not impossible to predict how the optimization and future performance of lignocellulosic biorefineries will pan out, it is possible to look at the optimization that has occurred in the corn-to-ethanol industry over the last 20 years to better understand the opportunities that are available.

Lessons Learned from the US Corn Ethanol Industry

The US corn ethanol industry is highly optimized and de-bottlenecked. In 1996, the US produced 1.088 billion gallons of ethanol. This level increased to 4.884 billion gallons in 2006 and 14.81 billion gallons in 2015. Over a period of 20 years, the US increased production by a factor of 14 and, in the last 10 years, by a factor of more than 3. Not only has the rate of growth been impressive, but the industry has become significantly more efficient.

Increased Revenues

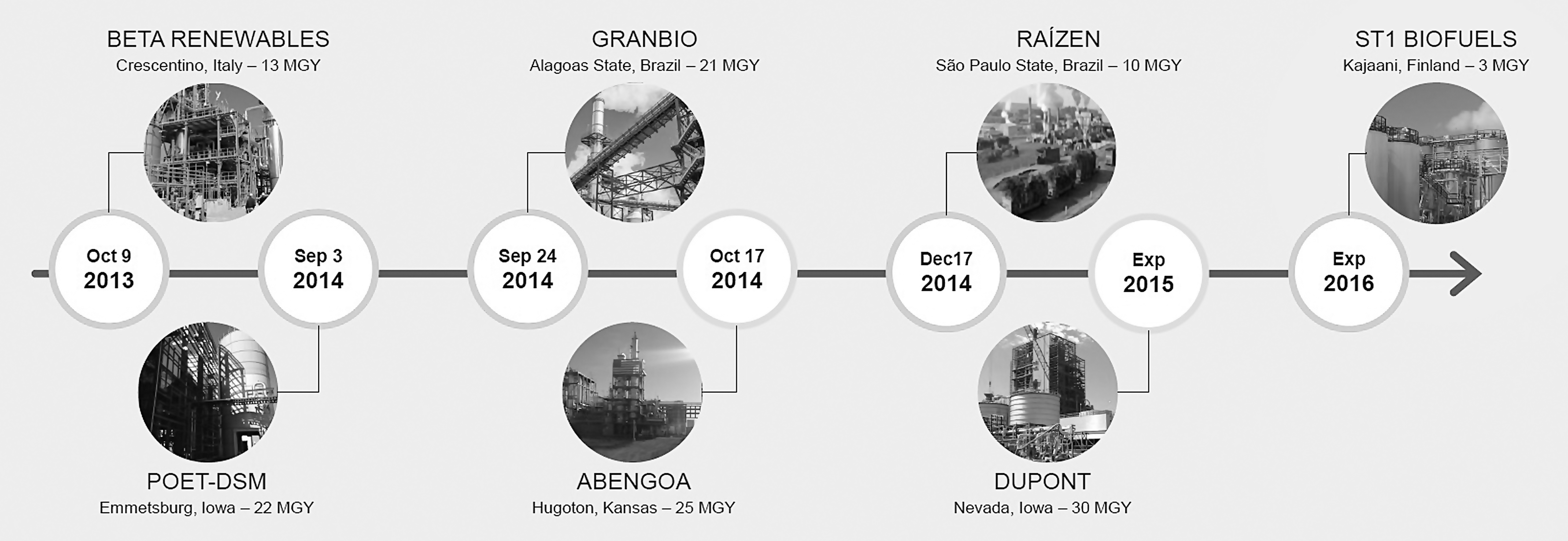

In considering the optimization of the corn ethanol industry, performance can be measured in a number of ways. One approach focuses on revenue enhancement, which is critical to ensure that the industry is cost effective. Over the past 20 years, various improvements have been made: • Conversion efficiency of starch to ethanol • Extraction of corn oil • Conversion of some cellulosic elements into ethanol

Converting more corn to ethanol and oil does lead to a partial offset loss with respect to value and volume of dry distillers' grains and solubles (DDGS). However, even after taking this into account, it is estimated that utilizing the same corn today as 20 years ago, a modern corn-to-ethanol facility will generate an additional 17% in revenue (Fig. 2).

Value of products from a corn ethanol facility, 1990–2016 (Source: Microbiogen estimates). Assumptions: corn = $3.50/lb; ethanol = $1.52/gal; DDGS = corn price; corn oil = S$0.35/lb; capacity = 35M/gal/y.

Decreased Energy Consumption

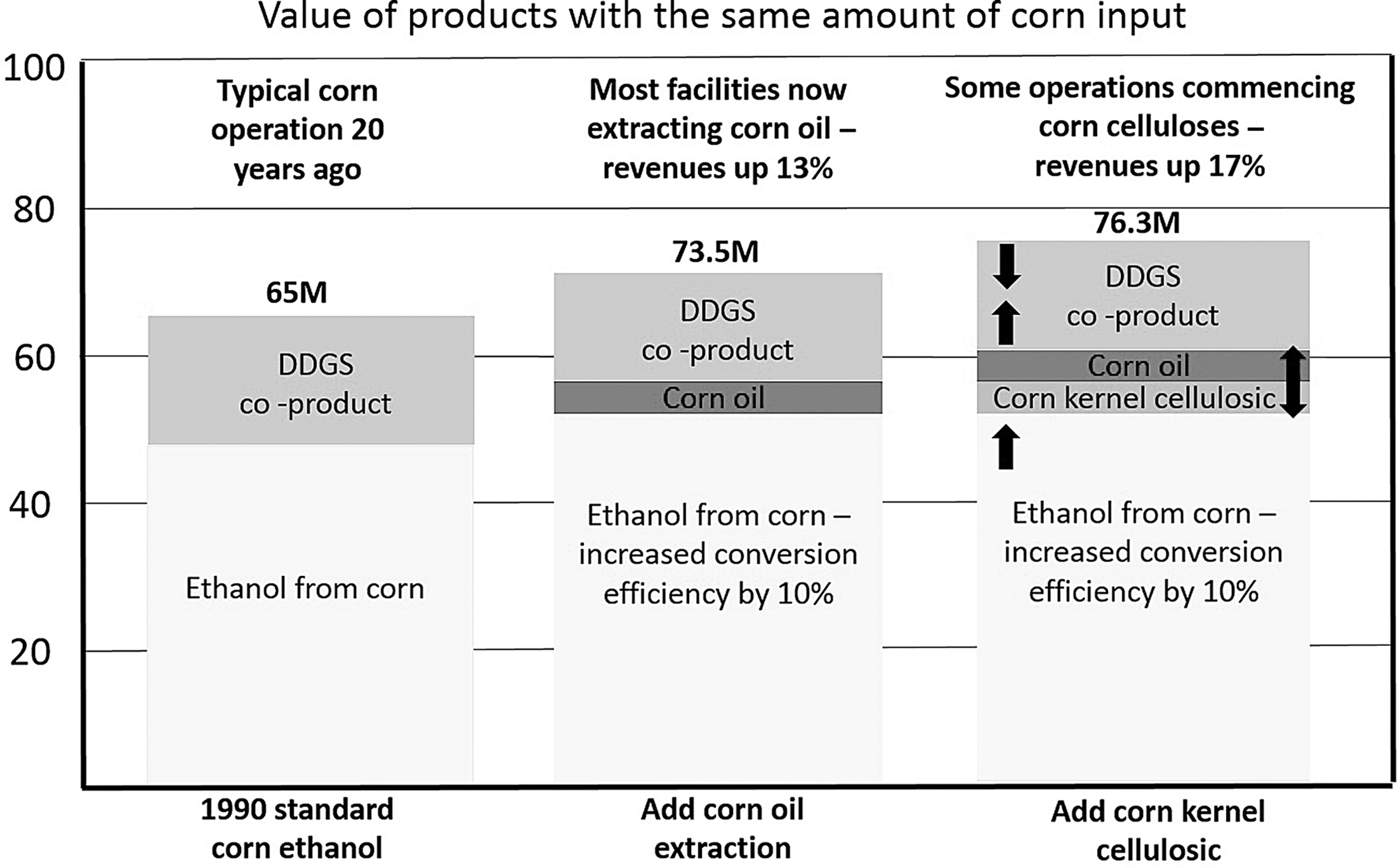

Over roughly the same period in which revenues have increased 17%, energy consumption to produce ethanol has declined substantially. Data from the US Department of Agriculture (USDA) via ICM (Colwich, KS), the leading engineering group that designs ethanol facilities, show that since 1991, energy consumption to produce one gallon of ethanol has declined by about 40% (Fig. 3).

Energy balance for corn ethanol facilities, 1991 to 2010 (Source: USDA 2015 Energy Balance for the Corn Ethanol Industry).

Additional Cost Savings

In addition to increased revenues and lower energy costs, other efficiency improvements have been deployed over the past 20 years, including a decrease in water usage throughout the production process. According to POET-DSM Advanced Biofuels (Sioux Falls, SD), one of the largest ethanol producers in the US, water usage to process corn into ethanol has declined by approximately 15% since just 2009. Over the next decade, a range of further improvements are expected: • Higher conversion rates of corn sugars to ethanol (improved yeast strains) • More efficient and greater conversion of starch to monomeric sugars (better enzymes) • Higher levels of corn oil extraction (enzymes and process) • Conversion of cellulose contained in corn to ethanol (cellulosic technology) • Conversion of C5 sugars in corn into ethanol (enzymes and yeast) • Further reductions in energy use (process) • Further reductions in water use (process and yeast—higher titers)

Convergence of Gen I and Gen II Biorefineries

A convergence trend has already commenced between Gen I and Gen II biorefineries. This trend is marked by several notable examples in the industry: • Corn ethanol facilities are not only recovering the inedible corn oil, but in some cases they are adding a biodiesel facility at the back end of the plant to generate even higher revenues. • Processes are being deployed that break down cellulosic fibers contained in the corn kernel into glucose, which is then converted into additional ethanol; companies such as Edeniq (Visalia, CA) specialize in this area. • Companies are adding a lignocellulosic facility to a corn ethanol plant; POET has already done this at its Emmetsburg, Iowa facility. • Renewable Developments Australia is planning to develop a biofuels facility at its Greenfield 340 million L/y Pentland project at a cost of A$800 million (USD612 million); with expected production of equal quantities from the food portion (sucrose) and biomass portion (bagasse, trash, and tops) representing an integrated Gen I and Gen II biofuels facility. This project is expected to be developed in stages with the first stage converting sugar juices to ethanol and the second stage converting the sugars contained in bagasse, trash, and tops into ethanol.

Opportunities to Optimize Lignocellulosic Biorefineries

Microbiogen specializes in the development of optimized industrial yeast strains for a range of industrial activities. As part of its optimization program the company has identified significant opportunities by which costs can be reduced, processes sped up, efficiencies increased, and the value of products increased through the use of S. cerevisiae in lignocellulosic biorefineries. Many opportunities also exist to improve the efficiency of lignocellulosic biorefineries outside of microorganisms. In this article we focus on what Microbiogen expects to be able to achieve, which is lower costs and facilities with a higher internal rate of return that produces a range of value-added products in addition to low-cost, renewable biofuels.

Increasing Biomass Conversion

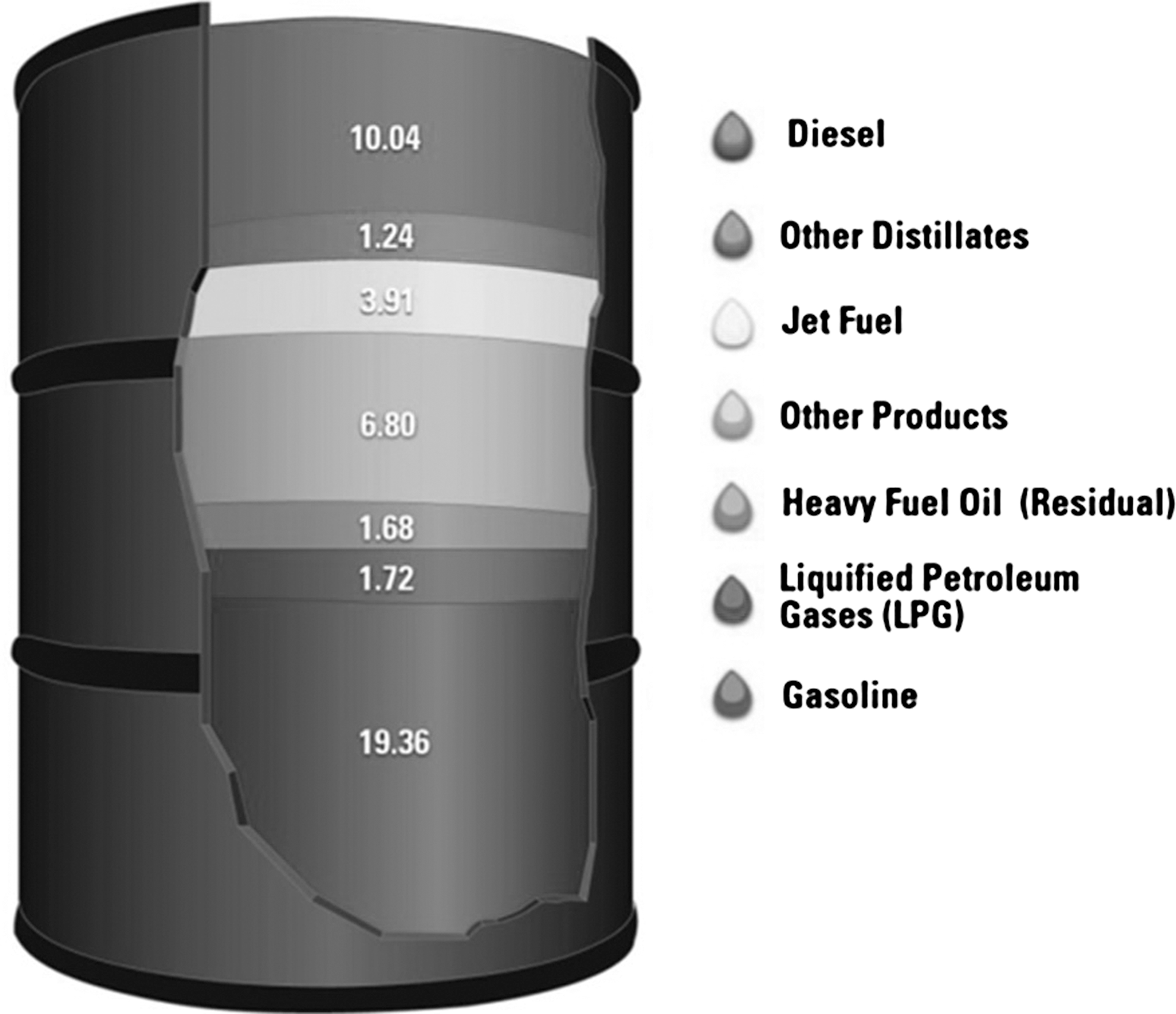

The current group of biochemical lignocellulosic biofuel facilities represent the first iteration of a new industry that will mature over time. Just as oil refineries have been optimized and upgraded over time to produce a wide range of value-added products from a low-cost commoditized material, namely crude oil (Fig. 4), lignocellulosic biofuels facilities will likely transition over time in much the same way. However, with an important exception—the input will not be non-renewable crude oil, but renewable biomass.

Products generated from a barrel of crude oil (Source: Kite International).

Whereas almost all crude oil is converted into higher value products, the first of the lignocellulosic biorefineries have two major issues that will be resolved over time: • Only a small proportion of biomass is upgraded into a high-value product • Only one higher-value product is produced: fuel ethanol

By way of example, Clariant is expected to produce high-value fuel ethanol from lignocellulosic biomass from its proposed commercial facility, but ethanol will only represent 25% of the total output (Fig. 5). The remaining 75% will be relatively low-value vinasse and lignin. Note that ethanol currently sells at approximately $500/t, whereas lignin is likely to sell closer to thermal coal ($60/t), and vinasse for even less.

Products from proposed Clariant commercial lignocellulosic biofuel facility (Source: Clariant, presentation at BIO World Congress on Industrial Biotechnology, April 2016).

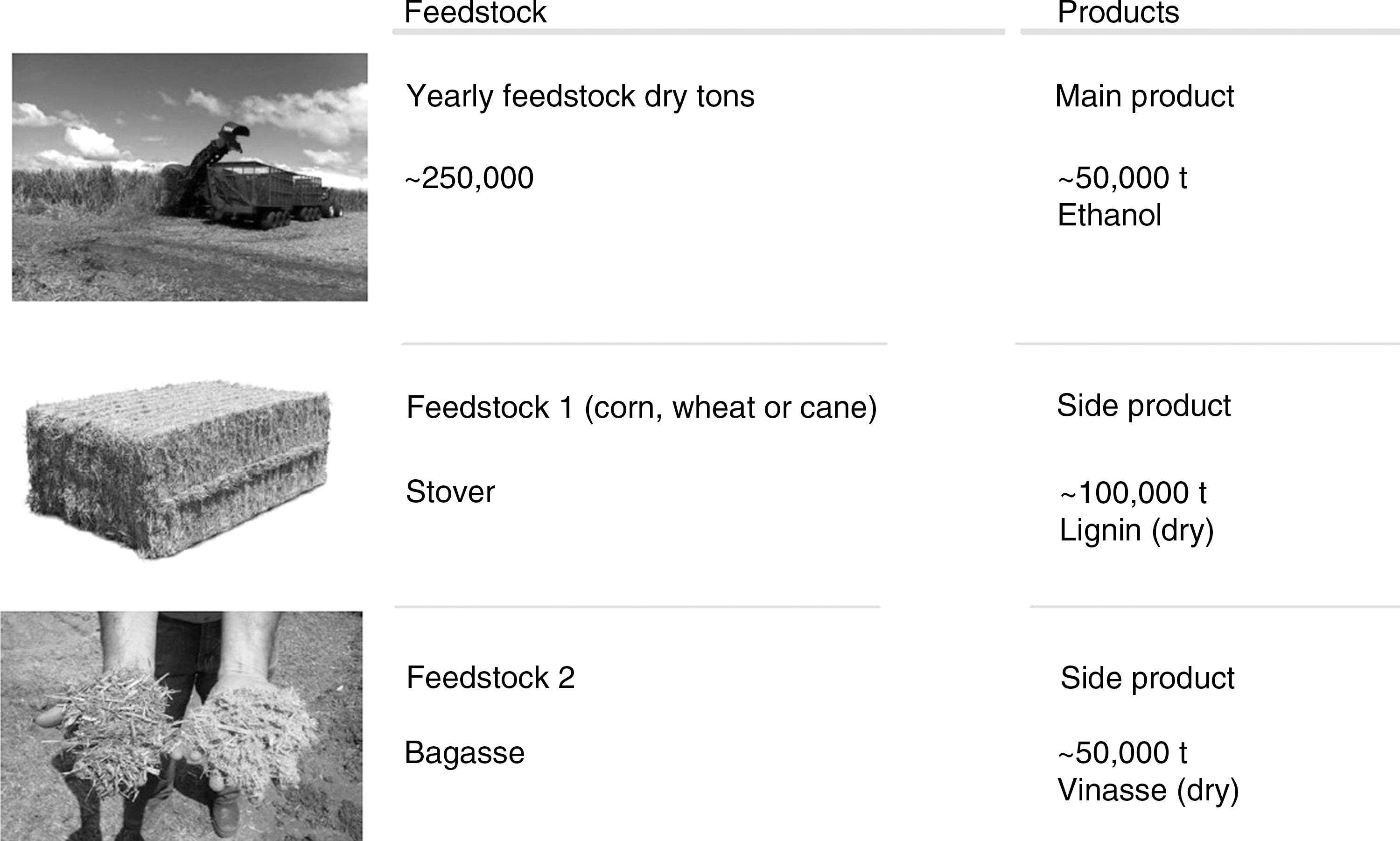

Research carried out by Microbiogen in its laboratories and through its industrial partners over the last decade shows that the first generation of lignocellulosic biorefineries will have a reasonably low conversion rate of sugars to ethanol. The estimated losses described below are generalizations, and those of each commercial facility will differ. For example, one facility may utilize very heavy loadings of microorganisms to ensure close to complete fermentation, whereas another may reduce the yeast loading, save on propagation costs, and accept a slower and/or less complete fermentation.

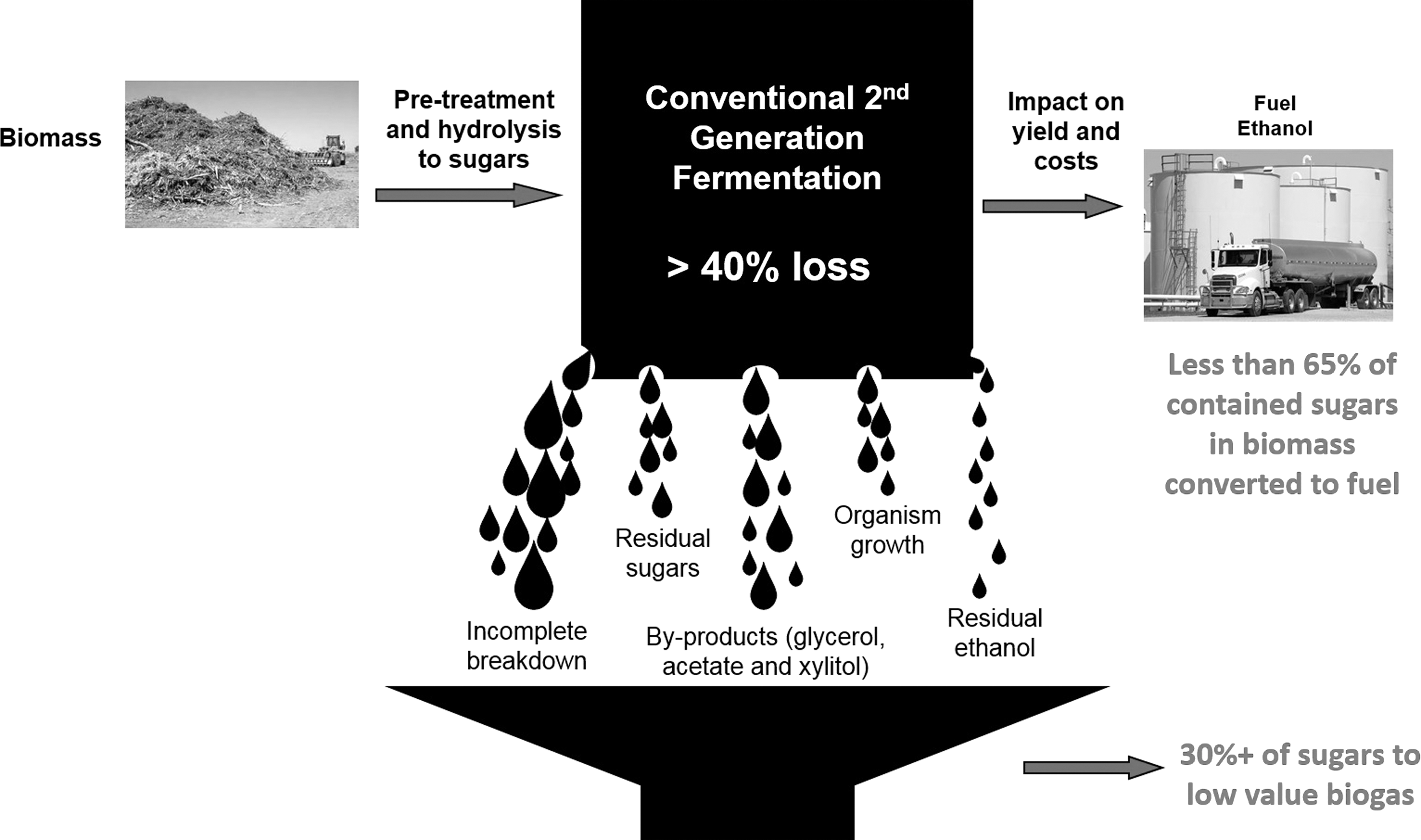

Incomplete breakdown

Pre-treatment and enzymatic breakdown technologies are not yet optimized. Depending on the process, anecdotal evidence and industry feedback would suggest that at least 10–15% of the sugar polymers are either not broken down, are lost through the process, or are broken down into low-value or unusable carbon molecules. While it is possible to reduce losses, at this time it is not economical to do so.

Residual sugars

No fermentation is ever fully complete. Even in the mature corn ethanol industry, low levels of sugars and carbohydrate are left behind. In lignocellulosic bio-refineries, the additional issues with respect to C5 sugars and increased levels of inhibitors means that a higher percentage of sugar is expected to remain unfermented. Depending on fermentation time (the longer the fermentation the more complete the fermentation), up to several percentage points of sugars can be left unconverted into ethanol. Higher yields are achievable, but extending the fermentation time or inoculating much higher levels of yeast has limitations due to economics.

Unwanted by-products

During a typical corn ethanol fermentation, for every 100 g of ethanol produced, approximately 10–12 g of glycerol and organic acids are produced. In the current generation of lignocellulosic biorefineries, these unwanted streams of by-products generally go to the vinasse, with very little value.

Fermentation organism growth

In corn ethanol fermentations, the yeast that ferment the sugars to ethanol are utilized only once for fermentation. That is, they are used once and then killed when processed through the distillation columns. The yeast then becomes part of the DDGS and adds to the DDGS nutritional profile. In a lignocellulosic biorefinery, the dead yeast is lost to the vinasse or lignin, depending on where the lignin comes out of the system. Due to the inhibitory nature of the hydrolysate streams and some loss of robustness of the yeast as a consequence of required genetic modification to central metabolism, several percentage points of sugars can be lost to the system. The loss is driven by a requirement to grow significant quantities of yeast on sugars that would otherwise be available for conversion to ethanol.

Residual ethanol

In a typical corn ethanol fermentation, the final ethanol titer reaches close to 14% (w/v). In a lignocellulosic biorefinery, the first facilities are likely only to reach 5–6% (w/v) ethanol. This means that there will be some losses of ethanol through the distillation process–more than in a corn ethanol facility on the basis of % of total ethanol. This is not a major amount, but is in addition to all the other losses.

Overall, it is estimated that less than 65% of the original sugars contained in the biomass will be converted into ethanol (Fig. 6). Even at 65%, this may be seen as an optimistic estimate–some plants may only be able to convert as little as 50% sugar to ethanol. This compares with approximately 85% conversion of the original starch contained in corn converted into ethanol, because of secondary metabolites such as glycerol and organic acids as well as residual sugars and starch polymers, such as maltodextrin.

Losses incurred in the current generation of biochemical lignocellulosic biorefineries (Source: Microbiogen).

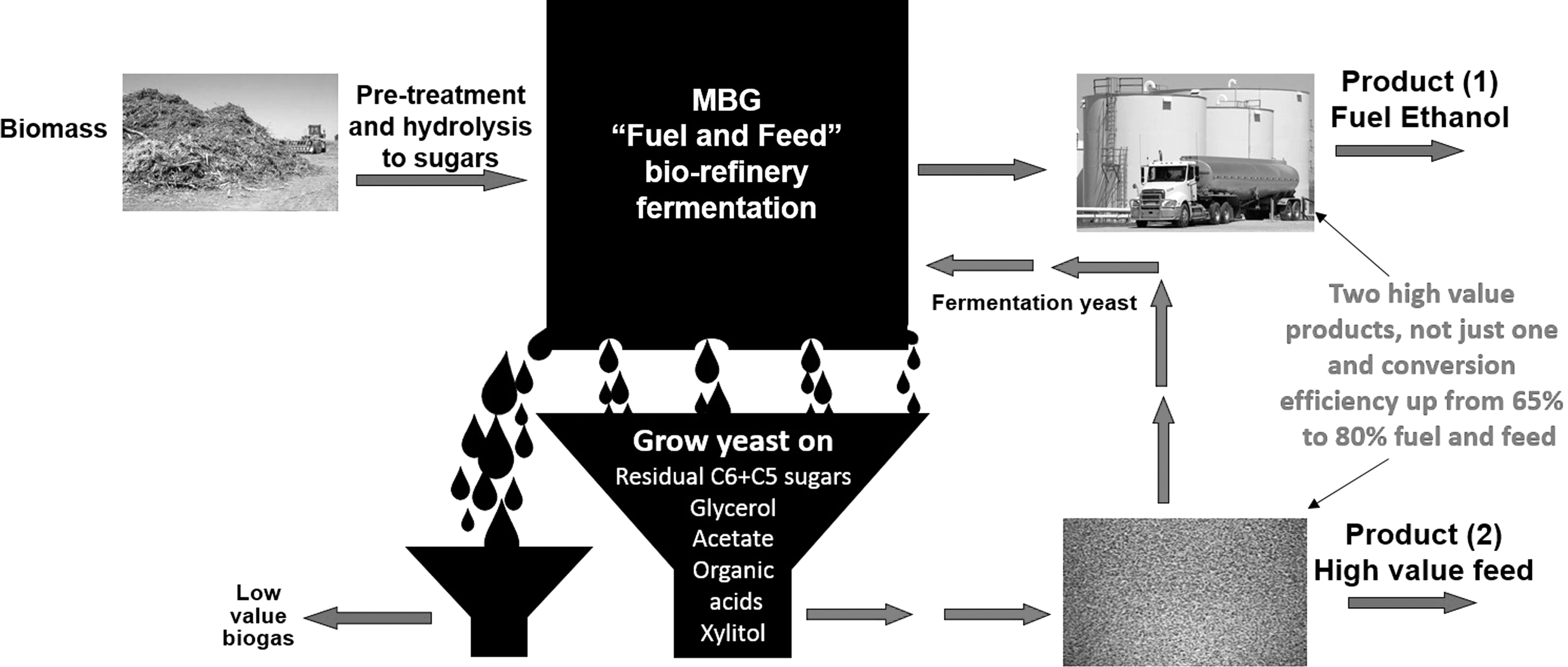

Increasing Conversion Efficiency

Over the past decade, Microbiogen has identified opportunities to improve efficiencies in an “average” lignocellulosic biorefinery. Some of the key areas identified for improvement include the following: • More robust and hydrolysate resistant yeast • Higher temperature tolerant yeast • More efficient conversion of sugars to ethanol under anaerobic conditions • Low inoculation yeast • Organic acid resistant yeast • Yeast that can grow aerobically on glycerol and organic acids (fermentation waste streams)

If the above industrial characteristics were to be developed and incorporated into a single strain and then utilized in a lignocellulosic biorefinery, with process adjustments to take advantage of the optimized organism, then the impact on yield, product value, and returns are expected to be significant (Fig. 7).

Impact of utilizing an optimized yeast on process efficiencies (Source: Microbiogen).

Key Assumptions of an “Average” Lignocellulosic Ethanol Biorefinery

The assumptions made here have certain limitations due to the lack of publicly available information and differences between commercial facilities that are already operating. However, calculations can be made in a generic form and the impact measured in a broad sense or, to put it another way, the impact on an “average” lignocellulosic biorefinery (Table 1).

Assumptions for Average Lignocellulosic Ethanol Biorefinery

Identified Organism and Process Targets

The development of a superior yeast strain with greater hydrolysate resistance, more efficient conversion of sugars to ethanol, lower required inoculation rates, and the ability to grow on its own waste streams, would target improved efficiency outcomes (Table 2).

Identified Performance Targets

Impact if Targets were Met

If one assumes that the above targets are met, then the impact on the process economics would be significant (Table 3).

Predicted Performance Outcomes

Potential Benefit to Australia's Sugar Cane Industry

Australia is one of the world's major sugar producers. Although Australian sugar production is not as large or on the same scale as that of Brazil or India, sugar is a major export product: • 380,000 hectares of sugar cane grown and harvested annually • 24 sugar mills in operation • 4,400 cane farming entities • 95% of sugar cane grown in Queensland • Up to 4.5 million t of raw sugar produced annually • Approximately 1 million t of molasses produced annually • About 10 million t of bagasse produced per year • Up to about A$2 billion (USD1.5 billion) exported each year • Approximately 85% of Australian sugar exported

The industry generally has been under pressure over the last decade with the closure of several mills, as well as a reduction in the number of sugar cane growers. Sugar cane farmers and processors essentially sell only one high-value product, namely sugar. This exposes the growers and processors to a commoditized product that has a high level of price volatility. The sugar price over the last decade has traded as high as $0.30/lb for a short period of time to as low as $0.10/lb at other times (Fig. 8).

Commodity futures prices for sugar #11, last 10 years, in $ (Adapted from: Nasdaq).

Australia's First Lignocellulosic Biorefinery

Following the deployment of the first commercial-scale lignocellulosic biorefineries around the world, the risk associated with the recently developed technology has declined. Consequently, the first full-scale facility in Australia is nearing the completion of the planning and finance stage and could be ready for Stage I construction as early as 2017 or 2018.

Renewable Developments Australia (RDA) is in the process of finalizing financing to develop the world's largest integrated Gen I and Gen II biofuels project based on sugar cane (Fig. 9). The project is based in the Burdekin region of North Queensland, and Stage I and Stage II are expected to produce approximately 340 million L/y of ethanol. Stage III could see the expansion of the project to over 1 billion liters of ethanol per year.

Location of the proposed Pentland Project (Source: Renewable Developments Australia).

The lignocellulosic portion of the project is expected to be based on PROESA® lignocellulosic ethanol technology developed by M&G Group (Tortona, Italy). M&G was the first company to construct and commission an 80 million L/y facility, located in Cresentino, Italy. This facility has been operating since the first quarter of 2013.

RDA has forecast the operating costs to be among the lowest in the world due to a number of factors: • Economies of scale: Stage I and II expected to be 340 million L/y • Low-cost sugar and biomass substrates: The project is expected to be able to achieve approximately 19,000 L of biofuel per hectare of sugar cane, which compares favorably with the US corn ethanol industry, for which the yield of ethanol per hectare is approximately 3,500 L. • With a combined area available for cropping of over 70,000 hectares, and an initial cropping on over 15,000 hectares, the size of the project means that there will be economies of scale.

Estimated operating costs for the Pentland Project are shown in Figure 10.

Estimated operating costs of the Pentland Project (Source: Renewable Developments Australia).

Optimization Over Time

The Pentland project is being developed based on the initial optimization of the first iteration of lignocellulosic biorefineries. As described earlier, the progress made by the corn ethanol industry can be used as a guide as to where the lignocellulosic biorefinery industry will be heading. Corn ethanol revenues are up 17% in 20 years, energy costs are down 40%, and water usage is down 15% in just 6 years–with more cost cutting and efficiency increases expected.

Projections for the Pentland project are based on the performance of yeast strains developed to date. However, if the previously presented targets are applied to an integrated Gen I and Gen II biorefinery, then one can see that overall project revenues could increase by 11–13% depending on whether the liberated xylose sugars are converted to biofuel or to high-value feed yeast. Either is possible by changing and optimizing the process design.

Using the xylose as a substrate for growing yeast to sell as a high quality animal feed product would generate the greatest increase in revenues on a per unit basis. However, there would be extra costs associated with the aerobic growth of yeast due to the energy required to concentrate the stillage through multiple effect evaporators and to aerate the concentrated stillage. The sale price of the yeast is the key determinant of whether the economics are superior for a lignocellulosic biorefinery optimized towards ethanol or one optimized towards feed and ethanol.

An Opportunity for Lower Risk and Higher Returns

Figure 11 demonstrates the opportunity for the Australian sugar cane industry if the industry starts to adopt new technology and move towards integrated and diversified biorefineries instead of single product sugar operations. These opportunities can be summarized as follows:

Impact of optimized yeast on revenue streams of an integrated sugar cane biorefinery (Source Microbiogen estimates). Key assumptions: sugar = $0.15/lb; ethanol = $0.60/L; high protein yeast feed = $1/kg; met coal = $80/t. Note: the lignocellulosic component includes trash and tops over and above the 1 t of cane. Exported power is considered insignificant for this analysis.

• Almost double the value generated per hectare of land based on the assumed deployment of Gen II technology

• Optimized yeast strains expected to add another 11–13% in revenues over and above those generated from the first of the lignocellulosic biorefineries

• Sugar is expected to remain an important product, but biorefineries could be expected to diversify and produce two or even three major products (sugar, ethanol, feed), thus lowering single commodity price risk

• Only optimization of the yeast has been considered. Other opportunities include more efficient pre-treatment and hydrolysis (higher yield), conversion of sugars to even higher value biochemicals and upgrading the value of the lignin into alternative products

• Greater sustainability credentials through the production of high quality, high-value animal feeds from what is currently low-value waste

Importance of Scale in Transition to Lignocellulosics

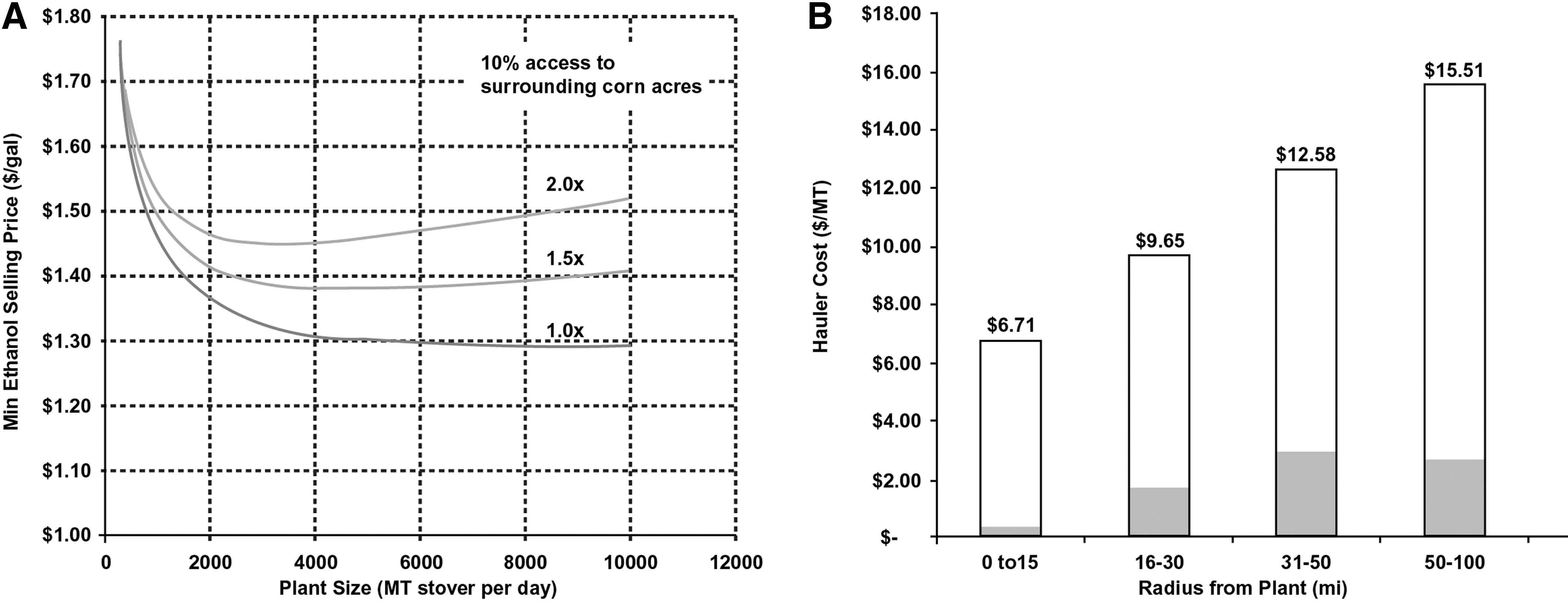

As with all industries, size is important and there is typically an ideal size to maximize returns while balancing a number of competing factors. In the US, the optimal capacity of a corn processing facility is approximately 400 million L/y of ethanol. At this scale, the process efficiencies balance against increased hauling costs to deliver corn to the facility, among other factors that must be balanced (Fig 12).

Maximizing returns based on plant size and other factors.

In the case of lignocellulosics, work carried out by various third parties shows that in a bagasse process facility, a throughput capacity of 2,000 dry t/day or more of biomass is required to achieve minimum economies of scale. This equates to about 200,000 L/y of ethanol. Given that the Pentland project is targeting Stage I production of 340,000 L/y, it would appear to be in the “sweet spot” with respect to scale.

Potential for Further Consolidation of Australian Sugar Cane Industry

Stage I and II of the Pentland project is expected to utilize close to 17,000 hectares of high yielding, irrigated sugar cane to produce 340 million L of ethanol. Stage III projects an expansion to 1 billion L. The average Queensland sugar mill currently draws cane from approximately 15,000 hectares of sugar cane crop. This suggests that, at least in the short term, the sugar industry is reasonably well placed should the conditions become favorable to look at upgrading and expanding into lignocellulosic biorefineries. Not only can the current industry consider upgrading the value of the current 380,000 hectares of sugar cane, but the Pentland Project shows that an expansion of the sugar cane industry into other suitable areas may also be possible.

If the Pentland project is successfully financed and developed, then one major barrier will have been overcome for a transition of the Australian sugar industry towards high-value renewable energy. While there will still be many hurdles to overcome for industry-wide deployment, such as market development, successful large-scale development and deployment, and access to risk capital among others, a glimpse of a potential industry transition can be seen.

Just as the US corn ethanol industry was transformed over the last 15 years, the same potential applies to the Australian sugar cane industry. The difference is that sugar cane is an inherently more productive crop with higher biomass densities and thus greater return potential and renewable credentials. Over the next 15 years, the technology and efficiency of lignocellulosic biorefineries will be optimized. Australia has the potential to be a world leader in renewable liquid biofuels, not only supplying its own liquid fuel requirements, but also becoming a major exporter.