Abstract

Introduction

The boom of shale gas in the United States first impacted the primary market of natural gas, followed by the market for power generation. Now, the huge production of shale gas will impact the chemical industry in a very significant way with secondary impacts on world markets. This ongoing process could be an impediment to the competitiveness of the industrial bioeconomy. Even if the externalities of shale gas are less negative than in the case of oil or coal, in terms of the environment it is still a fossil fuel.

A Huge Pack of Investments by a Chemical Industry Relying on Shale Gas

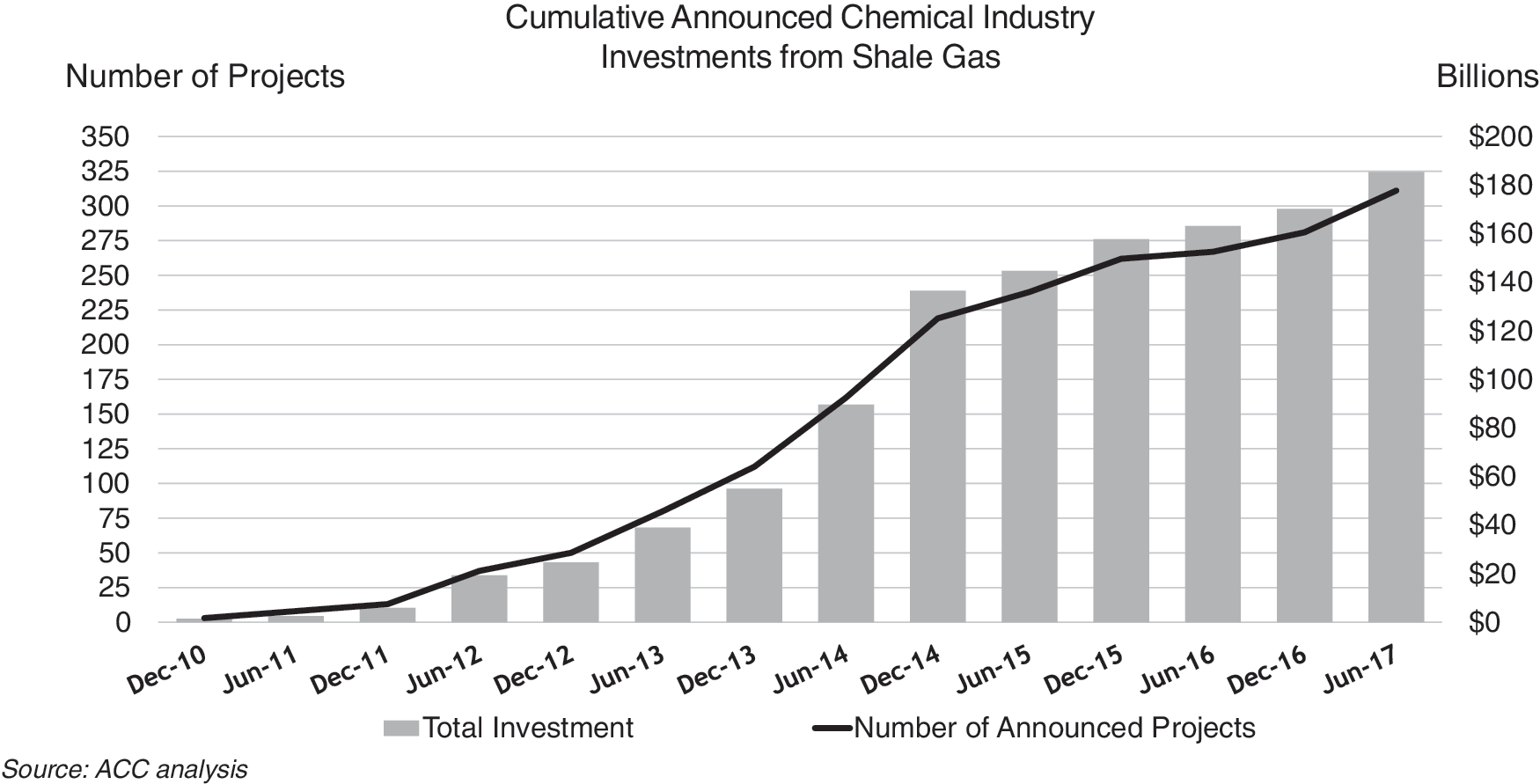

The increase of the level of investments by the US chemical industry over the last four years is tremendous, reaching $185 billion for 310 projects (Fig. 1). The average investment size is therefore around $600 million, but the biggest projects are reaching $4–9 billion. These projects are either under construction or have been announced as forthcoming. In 2016, the share of actual investments by the chemical industry was 50% of all US industrial investments; the share of the chemical industry in the US GDP is 26%.

Cumulative announced chemical industry investments from shale gas. Source: American Chemistry Council (2017).

As a first wave of investment is already committed (it takes four years to build such mega-refineries and their associated infrastructure), the impact on chemicals markets will be seen in the near future (2017–2021).

According to the American Chemistry Council (Washington, DC), this investment wave should contribute an additional $295 billion sales revenues by 2025 and create 462,000 direct and indirect jobs. Sales revenues of the whole US chemical industry is forecast to jump from $790–$1,085 billion. US exports should grow from $17 billion to $110 billion, mostly targeting Latin America and Asia.

Heavy Weights are Investing to Produce Ethylene, a Key Building Block

The most significant investments include:

Dow Chemical

Under construction at Freeport, Texas, Dow is building an $8 billion facility to produce ethylene. The project, which will generate 200 jobs, will produce 1.5 million metric tons of ethylene, starting December 2017. Dow is considering a second, $4-billion project.

Exxon

Under construction near Corpus Christi, Texas, within a joint venture with Saudi Arabia Basic Industries, Exxon is building a $9.3 billion facility. It is expected to begin production in 2021, producing 1.8 metric tons of ethylene and generating 600 permanent jobs. Overall, Exxon is considering investing up to $20 billion.

Chevron Philips

The company is building a plant to produce 1.5 million metric tons of ethylene in Baytown, Texas. Expected to cost $6 billion and generate 200 jobs, construction began in 2017.

Since oil—and not just shale gas—are relatively cheap fuels, the European chemical industry, which is based on oil (naphta), was also well off in 2016. As a result, the commodities from the chemical industries (ethylene, butadiene) have already suffered a price decline of 30–50% per ton. This pressure on prices could be less stringent in the future if the expected demand growth is materializing (from 147 million tons in 2016 to 186 million tons in 2023, according to PCI Wood Mackenzie, a consultancy).

On top of this US surge in investments, operators in the Middle East also have projects well underway, also in the range of a $4–$8 billion per facility. Asia will soon follow suit.

Low prices in bulk commodities from the chemical industry are good news for downstream industries (plastic, fibers, cleaning products for households, car bodies, cosmetics and all kind of additives, etc.) and also for the end consumers.

What About Climate Change Adaptation?

This trend is perhaps less favorable for a transition towards a bioeconomy or for new economic models that would promote a climate change adaptation and renewable fuels.

As these refineries are built for at least 40 years of operation, a lasting footprint on markets and the environment can be expected.

Will this surge in investment intensity from the United States and the Middle East create a supply shock on markets in the near future?

Will Europe be outspaced by the United States for a very long period of time? This issue can be discussed in the context of another question: What if Europe would also start producing shale gas?

What If the Production of Shale Gas in Europe Were Again Seriously Considered?

While this section aims to highlight the prospects of production of shale gas in Europe vis à vis other options for consumption and production of energy, the authors do not take any stance for or against shale gas. As a matter of fact, producing shale gas in Europe or importing shale gas in large quantities from the United States or other countries could have the same kinds of impacts on markets.

In the case of France for instance, this question could not even be raised under Hollande's Presidency (2012–May 2017) since the government labelled shale gas taboo. No civil servant was authorized to mention shale gas and no research project could be funded by the state. It remains to be seen whether the new French administration will or will not be as adamant regarding a ban on shale gas.

A scenario whereby shale gas would start to be produced by 2020 in Europe has been introduced in a modelization process targeting the potential competitiveness of a bioeconomy in 2050 with different hypotheses regarding the relative prices of energy fuels, including biomass. As this scenario was deemed inappropriate under the former French administration, it was reasonable to figure out a production by 2020 only. This is what has been introduced within the Global Change Assessment Model (GCAM). 1 In the next three figures, the above scenario is labeled S3. Another scenario S1, also labelled the reference scenario, features an oil barrel at $45. The last scenario, S2, is dubbed the business as usual scenario (BAU) and is based on an oil barrel at $80.

The GCAM model has been developed in US for the last 30 years by one of the laboratories of the Department of Energy (the Pacific Northwest National Laboratory). It has been chosen because it conveniently combines different modules—one on energy, one on agricultural commodities, one on greenhouse gas and polluters' emissions, as well as one on international trade.

A Significant Impact on Energy Consumption in Europe

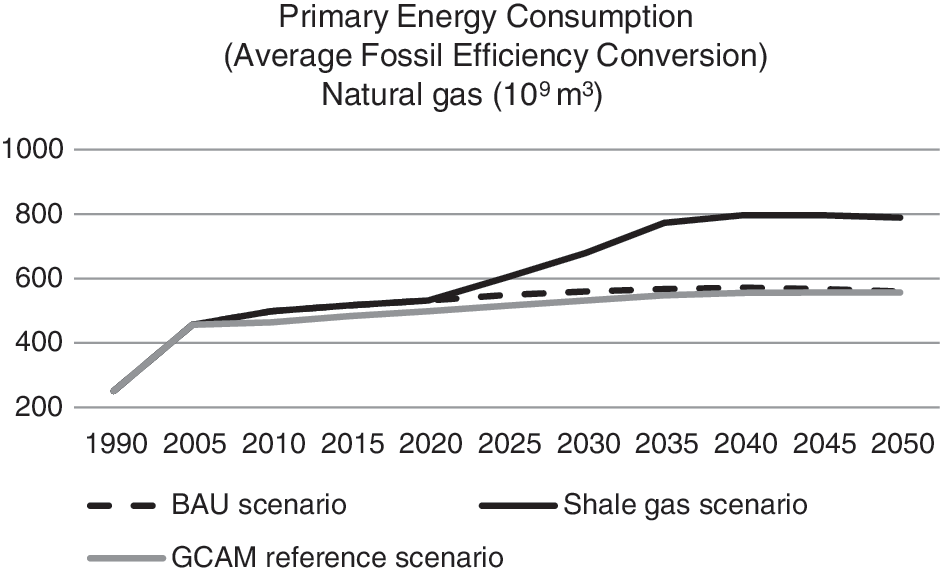

A 40% decrease in the price of gas in Europe could be triggered by local production of shale gas under scenario 3. By the same token, the consumption of natural gas in Europe could increase by 41%, almost in sync with the price decrease. The overall natural gas consumption could rise from 560 billion to 790 billion cubic meters ( Fig. 2). 1

Evolution of the consumption of natural gas in Western Europe, 1990–2050.

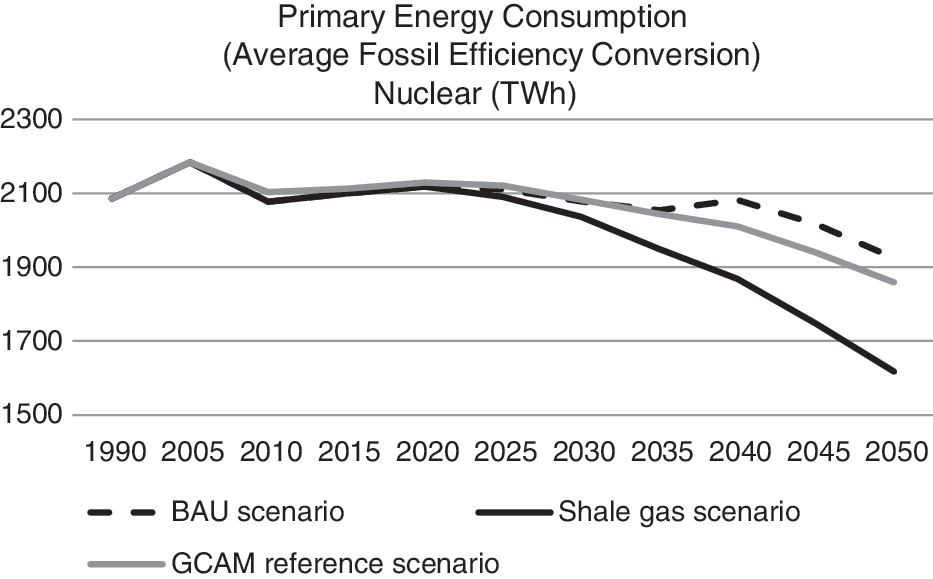

This increase could entail a 15–20% decrease in the share of other sources of energy. The consumption of biomass could decrease by 120−110 million tons oil equivalent (Mtoe) during the period, nuclear energy could drop from 1930 to 1600 terawatts (Fig. 3), and coal use could decrease from 677 Mtoe to 580 Mtoe. 1 From 2035, the consumption of wind and solar energy would also drop by 20%.

Evolution of the consumption of nuclear power in Western Europe, 1990–2050.

In the field of applications, the production of shale gas could also create a decrease of −8% in the production of cellulosic bioethanol by 2050. The decline of the consumption of liquefied coal could reach 120 Mtoe. Eventually, biogas would see its production divided by 2 or 3—the worst case of all impacts of shale gas.

A Relatively Small Impact on the Greenhouse Gas Emissions

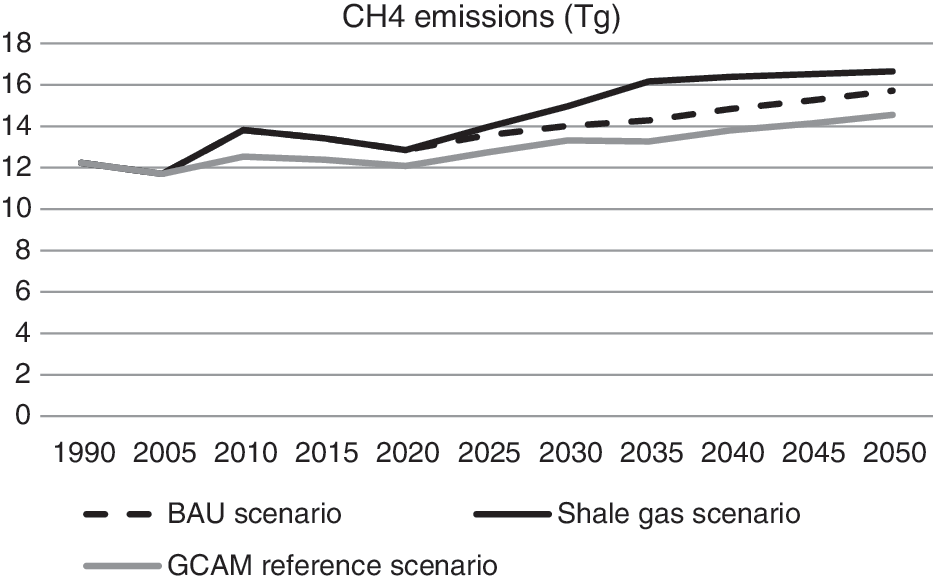

Should the consumption and production of natural gas stay relatively modest compared to the other energy fuels, the impact on something like 30 different greenhouse gas and pollutant emissions is also relatively weak. However, methane and HFC 245fe emissions would grow by 17% (Fig. 4). 1 Conversely, non-methanic volatile compounds and nitrogen oxide could decrease.

Evolution of methane emissions in Western Europe, 1990–2050.

The Production of Shale Gas in Europe, a Dilemma to Be Revisited ?

The consumption of shale gas in Europe could have significant negative, impacts on the other options, whether they originate from fossil fuels, such as coal, or from renewable sources, such as biomass, wind, or solar energy (which is not so favorable for a sustainable development).

Among applications, shale gas could be a business killer for biogas. Regarding greenhouse gas and polluters' emissions, it could translate into a mixed bag of impacts: a relative increase in methane emissions and a decrease in non-methanic volatile compounds and nitrogen oxide.

What About a Supply Shock Due to Imports?

One of the key questions for the future is the potential flow of import of shale gas from the United States. This process started in 2017 with the first deliveries to the United Kingdom. It could well be that if large volumes of shale gas are one day imported to Europe, the impacts could be quite equivalent to a potential production in Europe.

One cannot exclude either that shale gas could be imported in Europe from other countries or that the overall amount of shale gas produced globally would translate into a long period of low price whatever the countries of origin.

Conclusion

To conclude, the issue of the potential impacts of shale gas should stay present in any discussion on energy policies and the transition to a bioeconomy. Even if the energy mix is sensitive to public policies on a national/regional basis, the volume of imports is heavily dependent on global market conditions, such as price.

The European chemical industry could continue to be challenged in the near and medium future since many refineries have been closed because of a lack of demand growth, high costs, low profits, and, as a result, very low investments.

A transition to a bioeconomy will be equally challenged in Europe because it cannot compete on the basis of price with such medium/long term prospects of low prices of fossil fuels. Only small-volume, high-value molecules could be succesfully produced in Europe—but then where are the environmental benefits?

This trend could still be reversible. If Europe or any other major countries would like to counter these scenarios and build a transition to a bioeconomy, then they would have to be pro-active by • implementing a significant carbon tax, • creating a level playing field by removing the direct and indirect subsidies to fossil fuels, • de-risking the “death valley” that investors have to overcome if they wish to move to biobased production, • maintaining consistent support policies over at least 20 years to help investors justify the investment, and • promoting a multi-stakeholders dialogue to begin.