Abstract

Alternative Proteins in Context

In just the past few years, alternative proteins have morphed from a niche product to a mainstream phenomenon. Plant-based meats are now a fixture at fast-food restaurants around the world, plant-based milk is a household staple, and you can taste meat grown from animal cells in restaurants in Singapore and Israel. What we see today is only the beginning of the protein transformation.

Based on our analysis, by 2035, every tenth portion of meat, eggs, and dairy eaten around the globe is very likely to be alternative. That's a lot. If the alternative-protein market were a country, by then it would be a top-50 economy, larger than Finland's 2020 GDP. Is this unrealistic? Not at all. And it could be much more, if all four of the dominoes now lined up were to tip over.

The first domino is already falling: public concern for the climate—and, more broadly, sustainability—is rife. Many consumers want to reduce the amount of animal protein in their diets, especially if they can do it without sacrificing taste or paying more. In addition, fully 85% of investors now incorporate environmental, social, and corporate governance (ESG) criteria into their investment strategies.

We predict that, taken together, these concerns will generate enough consumer demand and investor interest to tip over the second domino: refinement and scaling of existing technologies to unlock parity, when the taste, texture, and price of alternative proteins closely match those of animal proteins. The first two dominoes are all that's needed to allow alternative proteins to capture 11% of the global protein market by 2035, our base-case growth estimate.

What if the industry can generate even more momentum? Step changes in alternative-protein technology, whether at incumbent food companies or startups and supported by public or private investment, could lead to rapid gains in production efficiency, better taste and texture, and lower cost. The result: the third domino falls, leading to earlier parity and a 16% market share by 2035.

The final domino could fall if regulators give it a push. Higher carbon prices and support for farmers transitioning from animal agriculture to alternative-protein inputs could boost consumption to 22% by 2035. At that rate, Europe and North America would reach “peak meat” by 2025, and then the consumption of animal protein in those markets would actually begin to decline.

The rise of alternative proteins is a transformation, not a revolution. Several major incumbent meat companies are already redefining themselves as “protein” companies, making and marketing their own alternatives. This makes sense, given the size of the prize. We estimate that alternative-protein revenues will reach $290 billion in 2035, with the profits distributed throughout the value chain: to the startups and incumbent food companies producing alternatives, the upstream players providing the industry with the inputs and tools needed to unlock these revenues, and the investors willing to support their efforts.

Profits aside, the protein transformation can make an enormous contribution to the efforts to combat climate change. In our base case, by 2035, the shift to plant-based meat and eggs alone will have saved more than 1 gigaton of CO2-e. 1 That's the equivalent of Japan going completely carbon neutral for an entire year. 2 Eating that much plant-based protein would save enough water to supply the city of London for 40 years 3 and make a major contribution to food security and our planet's biodiversity.

Alternative proteins also open up an opportunity for individuals to contribute to the fight against climate change. For instance, every portion of spaghetti Bolognese made with plant-based meat avoids as much greenhouse gas as a new car emits when driven 10 kilometers.

So what does the protein transformation taste and feel like, and how much will it cost the consumer? Good news: it will require few material sacrifices. As alternative proteins reach parity with animal proteins in taste, texture, and price, they can replace animal protein in 90% of the world's ten favorite dishes, from burritos to dim sum.

These alternatives won't require new recipes, change the taste of what people love to eat, or cost a lot. Making that Bolognese sauce with alternative meat will be just as easy and taste just as good. It also won't burn a hole in consumers' wallets.

In this first-of-its-kind report, we crystallize the expertise of the alternative-protein field, on the basis of a recently conducted survey and more than 40 interviews with industry veterans, researchers, and startup entrepreneurs. We provide detailed forecasts of the growth potential of the market for alternative plant-, microorganism-, and animal-cell-based proteins that can directly replace conventional animal protein, excluding traditionally plant-based foods such as pulses, tofu, and tempeh. We support our model with deep dives into the relevant protein production technology.

From this body of knowledge, we then identify the most exciting investment themes along the value chain. We also aim to answer key questions posed by all stakeholders, including farmers, incumbent food companies, startups, investors, and consumers: How will parity determine the future growth of the market? What will be required to bring each type of alternative protein to parity, and when will that happen? How can investors both support and benefit from its growth?

The Promise of Parity: Alternative Proteins Could Soon Match Animal Protein in Taste, Texture, and Price, Fueling Widespread Adoption

Consumers' appetite for alternative proteins is growing, as animal-free protein emerges as a healthy choice. A recent Stanford study, for example, showed that eating plant-based alternatives instead of conventional animal proteins reduces cardiovascular-disease risk factors. 4 The health of the planet stands to benefit, too, thanks to the potential of these proteins to decrease greenhouse gas emissions as well as water and land use.

Issues surrounding animal suffering and biodiversity loss are also playing an important role in the shift away from animal protein. Concerns about the ethics of intensive animal farming have already increased demand for grass-fed meat and free-range chicken and eggs. In addition, the risk of animal-borne illnesses such as mad-cow disease has come into sharp focus in light of the COVID-19 pandemic.

The market for alternative proteins is still nascent—13 million metric tons were consumed globally in 2020, just 2% of the animal protein market. Large numbers of consumers, however, say they are willing to try to change that. A recent study found that about 11% of consumers in the US, UK, and Germany are very interested in alternative proteins; 66% are somewhat interested, indifferent, or somewhat not interested; and only 23% are not interested at all. For consumers who aren't very interested, the key changes that would increase their interest are improved taste and a lower price. 5

In short, alternative proteins must reach parity with animal proteins in three key areas: Taste. Alternative proteins must effectively imitate the well-known flavor—and smell—of meat, seafood, dairy, and eggs. Texture. Alternatives must also look and feel the same as animal proteins. The experience of eating meat depends largely on its fibrous structure. Fish appears flaky, cheese feels hard or stretchy. Alternative eggs and dairy must also behave like real eggs and dairy when being cooked; eggs alone have up to 70 different uses, from scrambled to merengue to mayonnaise to cakes, and alternatives must be able to be used in all these cases. Price. At present, alternative proteins are usually not the bargain option, compared with animal proteins. If large groups of consumers are to repeatedly purchase alternative proteins, the cost must match or undercut that of protein from animals farmed under nonorganic conditions.

Nick Halla, the senior vice president for international at Impossible Foods, summarizes the issue of parity as follows: “You'll buy the product once based on novelty, you'll come back if the taste was good and if there are benefits such as nutrition and sustainability, and you'll buy it in the long run if the value is right.”

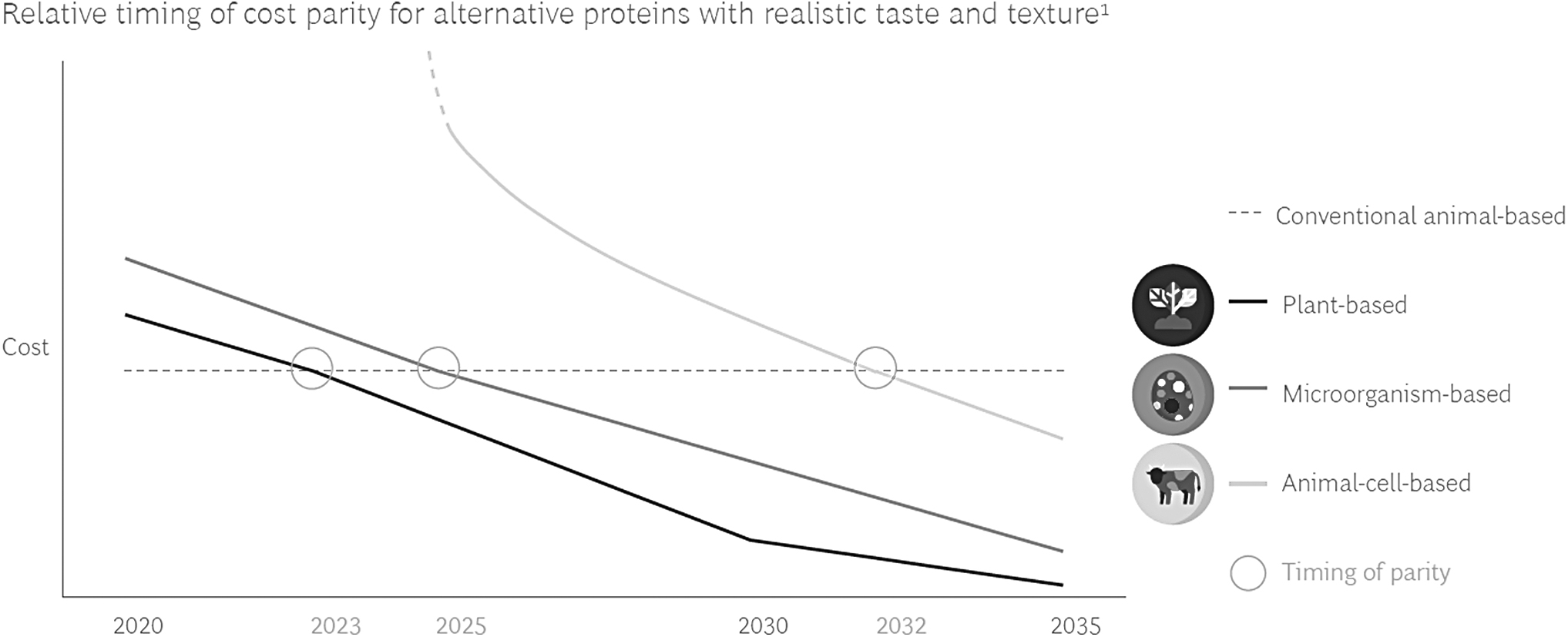

Each of the three types of alternative protein is currently at a different stage of parity with conventional proteins. We expect that plant-based alternative proteins will achieve parity by 2023, those based on microorganisms by 2025, and those based on animal cells by 2032 (Fig. 1).

Alternative proteins can reach parity between the early 2020s and the early 2030s. Sources: Expert interviews, industry reports, Blue Horizon and BCG analysis. Illustrative data for US and EU; variations by product group and geographic area are omitted for clarity.

These dates will vary to some degree, depending on the type of animal protein being replaced. Plant-based burgers, for example, are very close to parity today and may reach it within the next two years. Plant-based chicken pieces, however, will likely only reach full parity after 2023. They are already close in taste and texture but need to get less expensive in order to compete with conventional mass-produced chicken.

Microorganism- and animal-cell-based products will first reach parity with more expensive animal products such as meat; achieving parity with eggs and dairy will take more time.

A Fast-Growing Market: By 2035, Every Tenth Portion of Protein is Very Likely to be Alternative

How large will the alternative-protein market grow, and how quickly will it get there? In our base-case scenario, we expect the alternative-protein market will increase to more than seven times its current size over the next decade and a half, from 13 million metric tons a year now to 97 million metric tons by 2035, when it will make up 11% of the overall protein market. (Fig. 2) Assuming average revenues of $3 per kilogram, this amounts to a market of approximately $290 billion. Real revenues are likely closer to $10 per kilogram for high-quality meat alternatives but significantly less for high-volume products like milk.

Alternative proteins will very likely account for 11% of the protein market in 2035. Sources: US Department of Agriculture, Euromonitor, UBS, ING, Good Food Institute, expert interviews, Blue Horizon and BCG analysis. Note: Addressable proteins include ground meat, fillet, milk, eggs, and other forms of animal protein for which like-for-like alternatives can be created by building on current technology. Nonaddressable proteins include highly structured meat such as large cuts with bones.

We predict that adoption of alternative proteins—the proportion of total protein consumption made up of alternatives—will grow in three phases. Until each product type reaches parity, uptake will continue to increase at the current rates. Once the products reach parity, interest in them will soar, and the rate of adoption will double. This level of high interest will then remain steady for five years, after which use will continue to expand at a base rate of about 5%.

Once plant-based alternatives reach parity, in 2023, a five-year period of soaring interest and steeply increasing adoption will ensue. Proteins based on microorganisms will likely reach parity by 2025 and then grow the fastest until 2032, when animal-cell-based protein will reach parity. After that, this protein's growth rate will top that of the other two, although total consumption of animal-cell-based protein will remain relatively small compared with the others until companies can scale up production.

Milk and other dairy alternatives, already the most widely used alternative-protein products, will likely remain the largest portion of the market through 2035. Egg substitutes will grow more quickly, however; the first realistic alternatives are available today. The market for alternatives to meat, especially chicken, and seafood will increase especially fast, rising from 21% of total alternative-protein consumption in 2020 to almost 37% in 2035. We anticipate that alternative cheese will remain a relatively small market, as producing realistic substitutes has proved to be especially challenging.

Note that none of our estimates of market size takes into account the possibility of using alternative proteins as a basis for animal feed. Replacing the fishmeal and bone meal used as feed in aquaculture and other types of animal farming could grow into a sizable market even more quickly than alternatives for human consumption.

On a regional basis, North America (defined as the US and Canada) and Europe are the most mature markets for alternative proteins, with a number of such products on grocery shelves for several years. Adoption in both markets is likely to grow quickly, thanks in part to their climate- and health-conscious populations.

The largest opportunity lies in Asia-Pacific, however. Growth in that region is being driven by a large and growing population that is consuming more proteins as it becomes wealthier; the market will account for two-thirds of global consumption by 2035. Latin America and the rest of the world will grow rapidly but remain considerably smaller.

Building the Protein Value Chain: Parity can be Reached by Developing and Scaling up Existing Technologies at Key Steps of the Value Chain

The growth of the alternative-protein market depends largely on consumers' willingness to use these substitutes in their chosen diets. Acceptance depends on parity, and parity depends on boosting the technological expertise and manufacturing efficiency to produce these alternatives at scale.

Each of the three types of alternative proteins must pass through similar steps in the production process, from sourcing and growing the required plants, microorganisms, and animal cells and extracting their protein to formulating the right taste and creating the proper texture. The analysis below shows which improvements in each step will contribute to the effort to reach parity and unlock the alternative-protein market's growth. To confirm our analysis, we also conducted a survey of industry players to determine where, in their view, the most promising value creation opportunities lie.

Plant-Based Alternatives

Plant-based alternative proteins, typically derived from soybeans and yellow peas, are already approaching parity with conventional protein. Products like Beyond Meat's various meat alternatives and Impossible Foods' ground beef closely resemble conventional proteins in taste and texture. Beyond Meat's plant-based products are already sold in grocery stores, restaurants, and fast-food outlets such as McDonald's and Pizza Hut; when the company went public in May 2019, its shares soared 163% on its first day of trading. Other segments are close behind; the Just Egg scrambled-egg substitute and multiple soy- or pea-based chicken alternatives are proving very popular.

Today, the cost of goods sold for realistic plant-based alternative proteins is still about two times the cost of conventional animal proteins. To improve this ratio, the industry must optimize and scale up every step of the way. Improving sourcing and growth are prerequisites for production at scale, while perfecting extraction, formulation, and texturizing will significantly reduce costs. The results of our survey confirm this: the majority of respondents pointed to sourcing, formulation, and texturizing as the biggest challenges, with the greatest value creation opportunities.

Optimizing protein crops

Neither soy nor pea has been optimized for use in alternative-protein products. Most of the soy grown today has been bred for animal feed. New varieties, more suitable for human consumption, must be developed and grown with fewer off-colors and off-flavors so that fewer additives are needed to make tasty products. The protein content of soy and peas must also be increased to reduce the amount of input crops needed per kilogram of finished product and lower the cost of extracting the protein.

Improving protein extraction

The process of extracting the protein from crops is growing in technical sophistication and scale but still has to be improved and scaled up. Today, if the pH of the water used in extraction isn't properly balanced, the entire process can be disrupted. Improving the extraction process can lower the cost and increase the quality of the final product by removing more of the off-flavors, reducing the need for expensive and unappealing chemical additives.

We expect optimized extraction to decrease production costs, driven by savings in the capital-intensive separation and drying steps. Additionally, while the cost of soybean extraction can be offset by the production and sale of byproducts such as soybean cooking oil, viable uses for the byproducts of pea extraction have yet to be found.

Reducing the cost and complexity of additives

Making tasty alternative proteins from plants is largely a matter of choosing the right ingredients to mix with the extracted protein. To reach parity, new taste and texturizing ingredients will be needed. Consumers want foods that are completely free of animal products, and thus substitutes for commonly used binding agents like gelatin and egg whites need to be found. Foods must also be “natural,” however, so ingredients such as methylcellulose, a chemical used as a binding agent in many industries, are becoming less popular. In addition, ingredients must be familiar; many companies are looking to replace artificial flavors with suitable plant extracts. Atze Jan van der Goot, a professor at Wageningen University, notes, “If you find something that works the same way methylcellulose does, is cheap, and has a name that people can pronounce, it could become the industry standard very quickly.”

Scaling of texturizing capacity

The final step in the process of producing plant-based alternative proteins is to create the proper texture. This is accomplished primarily by extruding the formulated product through an opening in a perforated plate or die designed to give the required texture and shape. High-moisture extrusion can create structured products like chicken pieces, while low-moisture extrusion can produce smaller granules that, once rehydrated, can be made into burgers and other products.

Properly texturizing alternative proteins remains a significant economic bottleneck for the industry. Experimentation is expensive: highly skilled extruder operators must be able to experiment with large batches of product and adjust many parameters in order to perfect the final texture. In addition, the machinery is highly capital intensive. Production of the final product therefore must increase from the current hundreds of kilograms per hour to thousands in order to bring unit costs down to a reasonable level.

New technologies may soon complement extrusion. For instance, a team led by Professor van der Goot has developed shear cells, which shred (or shear) protein mixtures at high temperature to create fibrous structures; they can generate very realistic fibers and are well suited for small- to medium-scale manufacturing of specialized products. This offers the potential for radical decentralization—gourmet restaurants might even be able to make bespoke alternative-protein dishes right in the kitchen.

Unlike plant-based meat, plant-based dairy, egg, and cheese products do not need to be texturized. Achieving parity for these products will thus depend on the adoption of optimized protein crops and improvements in extraction and formulation. For cheese, the Swiss company New Roots has identified cashew nuts as an efficient input, requiring just one kilogram of input for every two kilograms of finished cheese; the remainder is mostly added water. In contrast, it takes 10 to 15 liters of milk to make one kilogram of animal cheese.

Microorganism-Based Alternatives

In second place in the race to reach parity are microorganism-based alternatives. These include proteins produced using bacteria, yeasts, single-celled algae, or fungi that are flavored and texturized into edible products. The process begins with a specific strain of microorganism that is then grown in a carbohydrate-rich solution to produce protein through fermentation.

Two technologies are currently being used to make microorganism-based alternative proteins. In the first, filamentous fungi are grown in a solid-state culture, a technique used primarily to produce meat alternatives, and all of the resulting biomass is included in the final product. In the second, microorganisms such as fungi, bacteria, or algae are grown in liquid suspension culture, from which a specific protein is extracted, rather than the complete biomass. This process is called precision fermentation because it targets a single protein.

Microorganism-based alternatives are not new. The UK's Marlow Foods, founded in 1985, was the first company to develop a process for creating microorganism-based alternatives for human consumption and has been selling its meat replacement product, called Quorn, since 1993. More recently, several companies, including US-based Meati Foods, have been experimenting with filamentous fungi that can generate realistic meat-like fibrous structures. Microorganisms also hold the promise of making realistic substitutes for eggs and cheese by enabling the production of proteins directly responsible for specific physical properties; Clara Foods, for example, produces foamy egg white protein substitutes that can be used in applications like merengue.

Microorganisms can also play a role in improving the taste and texture of plant-based protein. Impossible Foods' meat substitute burgers, for example, contain a molecule called heme, synthesized from genetically modified yeast, that gives them their realistic “bloody” color and meat-like taste.

Microorganism-based proteins, however, have a way to go before they fully reach taste, texture, and cost parity with conventional animal proteins. At present, for example, the cost is still two to three times greater than that of conventional proteins, especially for precision fermentation. The greatest potential for cost reductions will come through progress made in the first two steps—sourcing and growing the right organisms—a view confirmed by our survey participants.

Increasing metabolic efficiency

Improving the efficiency with which microorganisms convert their feedstock into protein is key to reducing costs. It can be optimized by choosing the right strains and adjusting the conditions under which they are grown. Depending on how the mixture is stirred and aerated and on the combination of nutrients that support the process, microorganisms can be induced to make much more protein from fewer inputs in less time. Increasing metabolic efficiency can also have a big impact on taste and nutritional value by speeding up the production of protein while slowing the creation of unwanted outputs such as off-flavors. Kevin Brennan, Quorn's ex-CEO, summarizes the challenge as follows: “It took us six weeks to find the right microorganism and 20 years to get the process to work reliably at scale.”

Adopting low-cost feedstocks

A major factor in bringing down the cost of microorganisms involves finding a carbon feedstock that is less expensive than the glycerol and glucose commonly used today. Scotland's 3F Bio, for example, is experimenting with growing microorganisms on byproducts from other processes, such as ethanol production. Using a byproduct as feedstock for fermentation not only lowers cost but also opens up the possibility of even greater sustainability than plant-based proteins. “If sustainability is your long-term game,” says Brennan, “then fermentation is the future.”

Optimizing the harvesting and protein extraction processes

For precision fermentation, multiple steps are required to get from a suspension to a protein extract, including centrifugation, filtration, and drying. Improving and scaling up these processes—using efficient filtration membranes requiring less maintenance and less water, for example—can substantially reduce production costs. As Alex Berlin, the founder and CEO of SolarBiotech, explains, “Decreasing the cost of these liquid-solid separation steps is a major lever for alternative- protein companies, and there is room for startup technology disruption here because this is an oligopolistic industry segment with technologies that have not evolved in decades.”

Reducing the cost and complexity of additives

As with plant-based alternative proteins, low-cost so-called “clean label” functional additives must be developed to reach taste and texture parity. Experts agree that such additives are scientifically possible but need to become more practical and much less expensive. “Take making cheese that is similarly stretchy on pizza, with protein and fat and all,” says Dayal Saran, the former head of R&D at Motif FoodWorks. “We are analyzing fat replacements and proteins from all sorts of animals to identify the ones that are both easy to produce in microorganisms and shelf-stable—from sturgeon eggs to camel milk and everything in between.” While improvements in additives will have only a minor effect on cost, they are essential for microorganism proteins to gain parity in taste and texture.

Animal-Cell-Based Alternatives

Animal-cell-based alternatives need more efficient growth in much less costly media and better ways to replicate key non-muscle elements of the meat experience. Products grown directly from animal cells, including “cultivated” meat and seafood, are already beginning to appear on the market, although it will take years before they reach parity with conventional animal proteins. The first test restaurant for SuperMeat's cultured chicken recently opened in Israel, and Eat Just has received approval to sell its cultured chicken in Singapore. Other companies around the world are hot on their heels, currently testing a variety of products. The cost of making cultured meat is still at least an order of magnitude above that of conventional meat, however.

The technology for making animal-cell-based alternative proteins is transformative. A few cells are taken from a living animal—for instance, a cow or a certain species of fish—and then grown in a nutrient-rich medium in a tank, producing thousands of kilograms of that species' flesh. Animal-cell-based alternative proteins are the next logical step in how agriculture has changed over the centuries, from having a single cow in your backyard to farming animals at factory scale to a factory farm without the animals.

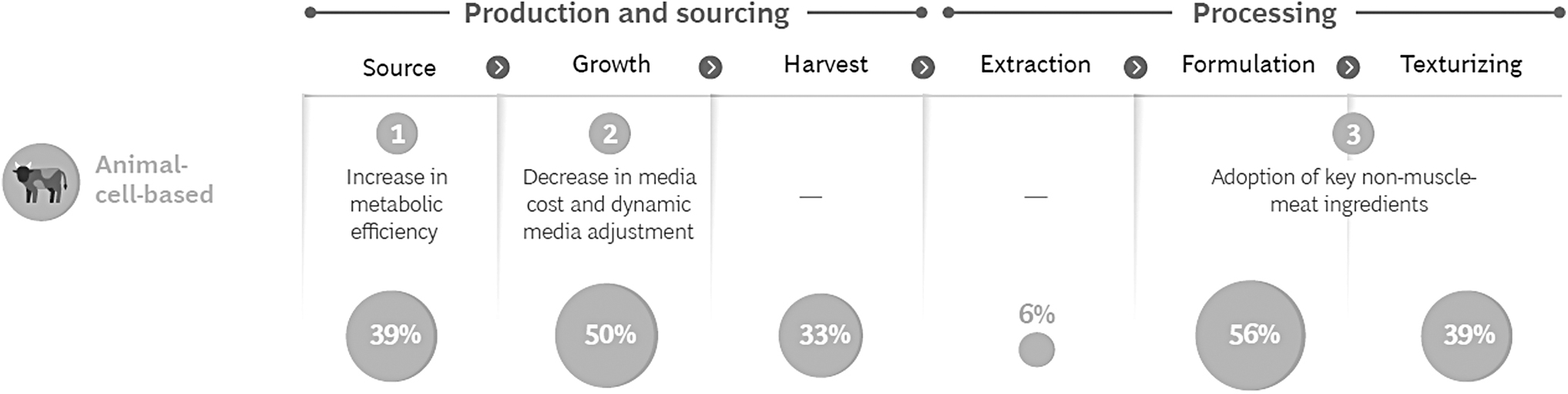

Indeed, some companies are planning to produce animal-cell-based meat in what is essentially a large farm, with multiple bioreactors next to one another, like cows in a barn. We expect animal-cell-based meats and seafood to approach parity in the early 2030s. To get there, growing cells efficiently and getting the taste right through formulation will prove the greatest challenges—and provide the most value, according to experts (Fig. 3).

Experts see the greatest potential for value creation in optimizing animal-cell growth and formulation. Sources: Industry survey of 59 experts, conducted by Blue Horizon and BCG, November–December 2020; Blue Horizon and BCG analysis. Note: The list of measures is not exhaustive, focusing only on the measures with the greatest impact.

Increasing metabolic efficiency

As with microorganism-based alternative proteins, the speed and output of the culturing process must be improved. Selecting the right cells and optimizing the growth conditions will enable companies to reduce the cost of facilities, labor, utilities, and input material per kilogram of finished product. “There is a lot you can do with metabolic-efficiency optimization,” says Dr. Steve Oh, the chief scientific advisor at SingCell, a Singapore-based contract development and manufacturing company for culturing meat cells. “We are looking at taking cells from young versus older animals, different tissues, and so on, to produce meat on microcarriers in suspension bioreactors. Then we can also think about modifying the cells so they produce fewer byproducts like lactate, which can become toxic to the cells if too much of it accumulates in the very high density cultures that we achieve.”

Decreasing media cost and dynamically adjusting composition

To reach cost parity, the media in which animal-cell-based proteins are cultured must become less expensive and more efficient. Accomplishing this will be the main lever to achieve cost parity. To get there, companies must first switch from expensive pharmaceutical-grade media ingredients, including growth factors, to less expensive food-grade ingredients; and these must also drop further in price through economies of scale in their production. The next step will be to use the media more efficiently, continually recycling it for reuse by removing waste products and adding nutrients. This will require delicate sensors and instruments that can adjust the media dynamically, depending on each cell type's specific needs. Many industry veterans are actively conducting research in the area.

Lavanya Anandan, the head of partnerships and external innovation at Merck KGaA, in Darmstadt, Germany, explains: “We are now developing customized bioprocessing solutions such as food-grade cell culture media to achieve the cost and scale ambitions of the cultivated-meat industry.”

The last step is more speculative but especially promising. Mosa Meat recently partnered with feed producer Nutreco to create low-cost media using plant material that has been pretreated with enzymes to feed the growing animal cells. The technology is still nascent but offers the potential to reduce cost even further. As Peter Verstrate, cofounder and chief operating officer at Mosa Meat, notes, “We are essentially trying to mimic cow digestion, giving the cells what they would get from the cow in nature.”

Adopting key non-muscle-meat ingredients

To reach parity with whole cuts of meat, animal-cell-based proteins must replicate the fibrous quality of conventional meats. This requires adding nonmeat ingredients to induce the growing cells to form fibers and meat-like fat. Overcoming this challenge will not significantly affect the cost of the protein but will help considerably in encouraging consumers to accept it. Fiber formation can be induced by seeding cells on so-called scaffolds: edible structures made from polymers produced in plants, microorganisms, or even texturized soy protein. Companies differ considerably in the type of scaffold they use. Aleph Farms, for example, grows its thin steak slices on a scaffold of a material it claims is “something natural and recognizable.” Some companies use no solid scaffolding at all. SuperMeat grows its chicken cells in suspension without scaffolds—the cells mature into meat tissues while excreting their own natural scaffolding. Mosa Meat creates a viscous environment in which its cells should eventually be able to differentiate into the various types of muscle and fat needed to make structured meat. No matter what kind of scaffolding material proves to be the most effective, it seems likely that it will not be expensive.

“I would be surprised if the scaffold ends up costing more than 10% to 20% of the total cost of goods sold for the finished product at the point of parity,” says Liz Specht, associate director science and technology at the Good Food Institute (GFI). The GFI is an international nonprofit providing ample resources for players across the food system. Adding fat to animal-cell-based meat is a challenge, but some companies are actively working to address this issue. For instance, Aleph Farms in Israel recently created a rib-eye steak, a cut with no bone but plenty of fat, using different types of animal cells grown in culture. The cells were “bioprinted” into the shape of the steak with a technology similar to 3D printing.

Animal-cell-based meat holds the promise of providing meat that is equivalent to animal flesh in every aspect but without slaughtering any animals. Further developments could even exceed the standards set by animal protein, by removing unhealthy saturated fat, for instance. As Paul Shapiro, the author of the best-selling book Clean Meat: How Growing Meat Without Animals Will Revolutionize Dinner and the World, points out: “If people ask whether I have concerns around the health effects of eating cultivated meat, my answer is the same as for conventional meat—there is too much saturated fat. But with cultivated meat, the difference is we can change that. We should strive to make something better than meat.”

Expanding the Protein Market: With Step Changes in Technology and Support from Regulators, Every Fifth Portion of Protein Could be Alternative by 2035

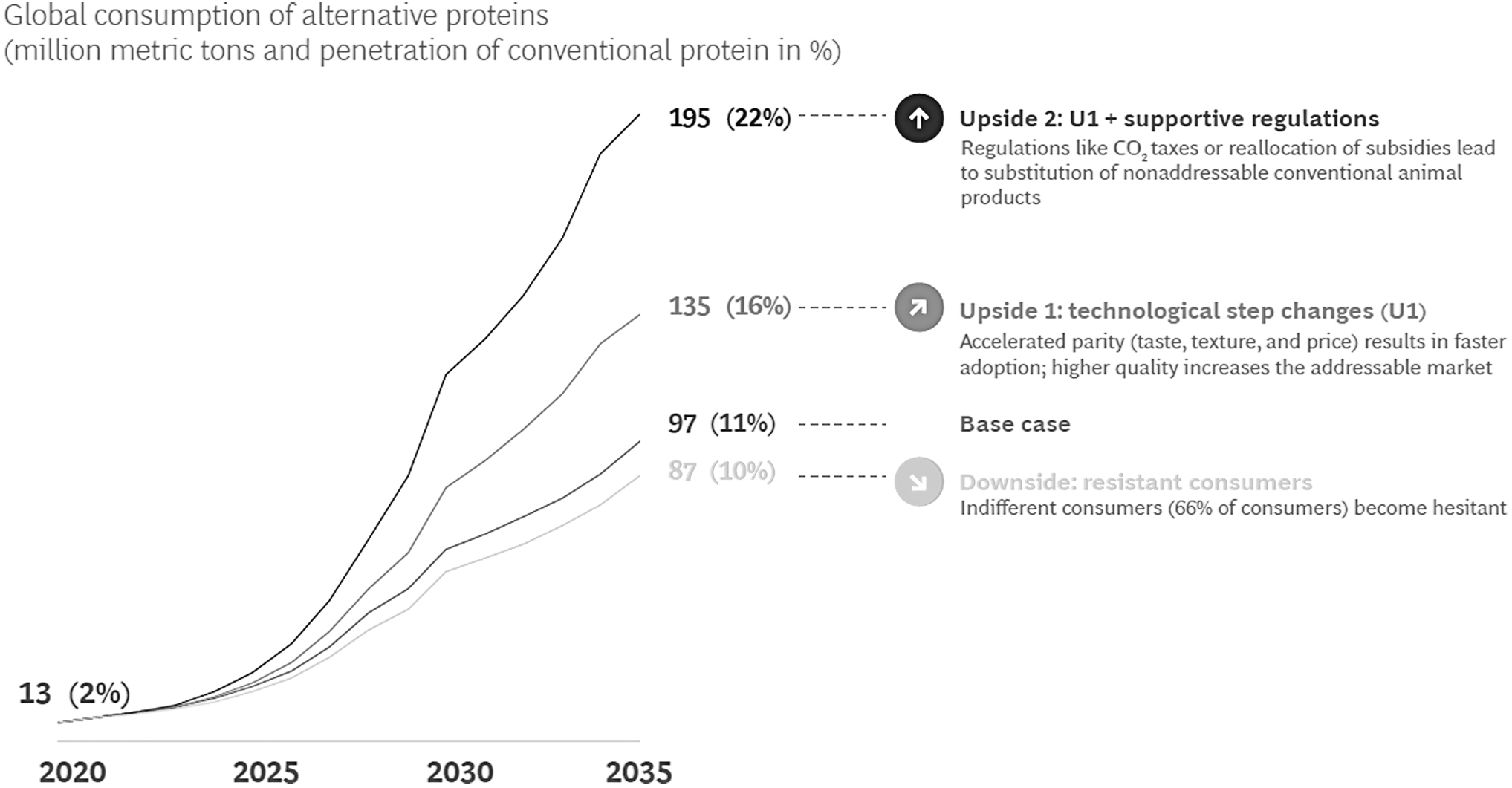

Our base case for the growth of the alternative-protein market needs only two dominoes to fall. The first, in motion already, is public concern for sustainability, which unites consumers, businesses, and investors in a push toward higher ESG standards and is driving the initial demand for alternatives. ESG-driven capital and consumer demand will likely tip the second domino—technological progress toward parity, as outlined in the previous chapters. The base case conservatively assumes a consistent pattern of consumer acceptance, regulatory support, and technological change, but we explored other possibilities as well. How would changes in these assumptions affect the market's growth? Significantly, and mostly on the upside, according to the alternative scenarios we developed. (Fig. 4)

Alternative proteins could claim as much as 22% of the overall protein market by 2035. Sources: Blue Horizon and BCG analysis.

In the first upside scenario, further efforts on the part of scientists, startups, incumbents, and investors tip the third domino: technological step changes, such as rapid, large improvements in metabolic efficiency thanks to better conditions for microorganism fermentation or animal-cell cultures. These efforts accelerate the time to parity of microorganism-based alternatives by a year, to 2024, and the parity of animal-cell-based alternatives by three years, to 2029. Improving fermentation can also unlock better taste, as fermentation-based “superstar” ingredients such as heme become easier and less expensive to make. As a result, alternative proteins grow more quickly, to 16% of the market in 2035.

The second upside scenario requires an additional push from regulators, causing the fourth domino to fall: more supportive policies and regulations, such as widespread taxation of greenhouse gas emissions or reallocation of agricultural subsidies to support the transition to alternative proteins. Such interventions could make alternative proteins substantially less expensive than conventional animal foods. A wider price gap, in turn, would encourage consumers to choose alternative proteins over highly structured products like steak, pushing penetration to 22% of the market in 2035.

On the flip side, what happens if technological step changes and regulatory support cannot be unlocked, and consumers turn out to be less willing to switch to alternatives than the base case assumes? Even if consumers who currently say they are ambivalent about protein substitutes end up behaving like those who currently say they are unwilling to try them, alternatives would still make up 10% of the 2035 protein market.

Both upside scenarios offer the possibility of reaching “peak meat”—the point at which the consumption of conventional animal proteins begins to decrease, at least in North America and Europe. All the scenarios assume that the consumption of protein in all its forms will grow at the same rates, depending on region, from 2020 to 2035. In the upside scenarios, however, alternative proteins will make up an increasing proportion of the total protein. If all four dominoes fall, the consumption of conventional animal protein will drop in Europe and North America from 2025 onward. While the growth rate of conventional-protein consumption in Latin America, Asia-Pacific, and the rest of the world will slow, total consumption will not yet decline. We suspect that the most optimistic upside scenario could be constrained by production and distribution capacity. For instance, the scenario assumes that about 120 million tons of alternative proteins will be consumed throughout Asia- Pacific, where many people, including more than 50% of India's population, still live in rural areas and are unlikely to find alternative proteins in their local markets.

Investing in Alternative Proteins: The Status Quo: The Industry Offers Sustainable Opportunities and has Begun to Attract Significant Capital

Regardless of whether either upside scenario comes to pass, the alternative-protein arena is wide open to investors. What does the investment landscape look like? The expected base-case penetration of 11% by 2035 already implies a market that's the size of a top-50 economy—our high-level estimate of $290 billion is close to Finland's 2020 GDP. The scenario analysis shows that the base case is conservative; penetration could double to 22% if the industry has the capital and vision to make technological step changes and regulators support the transition. Alternative proteins are penetrating a market— food—with very low exposure to recession and cyclicality, making them strongly resilient against any “unknown unknowns” that might influence the overall economy.

The demand for alternative proteins is fueled by several powerful megatrends, from health concerns to climate action and the increasing awareness of ethical issues in factory farming. It's not just about the consumer, however. Evidence is mounting that investors who take ESG issues into account can reap better financial returns. Most institutional investors already consider ESG factors when making investment decisions. In a 2020 survey of investment professionals, 85% said such issues influence their decision making, up from 73% in 2017. 6 Sustainable investing, in combination with the industry's already promising growth rates, ensures that capital will continue to flow to alternative proteins.

Substantial capital will be needed to support the growth of the alternative-protein market. Almost 30 million tons of bioreactor capacity for microorganisms and animal cells will be needed to reach the baseline case of 11% adoption by 2035. Building all these bioreactors will require up to $30 billion in investment capital—and $100 billion if all the dominoes fall, leading to a 22% share for alternatives. That's because far more bioreactor capacity will be needed if microorganism- and animal-cell-based proteins reach parity more quickly and demand for these alternatives rises rapidly. On the plant-based side, the extrusion capacity needed in the base case will require up to $11 billion, and as much as $28 billion if the greatest upside scenario comes to pass.

These high-level initial estimates do not include the necessary R&D spending or materials and operating costs of all these bioreactors and extruders. The total capital needed to unlock alternative proteins' growth will likely be much higher.

The investment community is instrumental to the success of the alternative-protein industry. Investor interest in the field is already strong, and investors are spreading their funding bets across the industry. This can create a snowball effect: as investment fuels technological progress, the demand for alternative proteins and the production facilities required to make them will increase, boosting the need for yet more investment capital. Venture capital funding alone totaled more than $4 billion from 2015 to 2020, according to Pitchbook. Most of that—about $3 billion—went into companies pursuing plant-based alternatives, followed by $733 million in microorganisms and $416 million in animal-cell-based proteins. Development efforts directed at adjacencies such as byproducts attracted less, just $120 million through 2020.

Regulating Alternative Proteins

If alternative proteins are to reach their full potential, consumers must trust them, knowing that these foods are safe to eat and that their ingredients are clearly and accurately labeled. To that end, proper regulation of how alternative proteins are made, approved for marketing, and labeled is essential. At present, the global regulatory environment is still vague and fragmented but is developing rapidly. In general, alternative proteins made from commonly used ingredients such as soy and peas do not require regulatory approval in the form of authorization to market and sell a specific product in a specific country. Alternatives made from novel substances such as microorganisms, or that contain an unusually high concentration of specific proteins such as mung bean protein isolate, do require approval. Paths to approval exist for many novel foods and ingredients and genetically modified foods. In Europe, the approval process for novel foods differs from that of genetically modified foods, which are strictly limited. In the US, the Food and Drug Administration and Department of Agriculture are working on a separate process for cultured meat, but it remains unclear how other governments will act. In this context, Singapore's approval of Eat Just's cultured chicken is an important milestone. Debates continue about proper labeling of alternative proteins across regions. On one hand, the names of conventional products, like “ham,” may be protected by national or state governments, prohibiting companies from using them to describe alternative proteins. On the other hand, growing interest in requiring companies to include products' climate impact on labels could make the benefits of alternatives more transparent to consumers. Given the current state of regulation, alternative-protein companies and their investors should closely monitor ongoing regulatory developments.

Editor's Note

The text presented here is excerpted from a report prepared by Blue Horizon, a Zurich-based impact investor shaping the alternative protein sector, and Boston Consulting Group. The information and views expressed here do not necessarily those of Industrial Biotechnology or Mary Ann Liebert, Inc., publishers, or their affiliates. The full report can be found at: