Abstract

Executive Summary

As investors and manufacturers seek new market opportunities for growth in the chemical sector, one of the portfolios attracting attention is the expanding portfolio of green chemicals. The US EPA defines green chemistry as chemical products and processes that reduce or eliminate the use or generation of hazardous substances. Green chemistry applies across the life cycle of a chemical product, including its design, manufacture, use, and ultimate disposal. 1 While green chemistry has traditionally represented a very small segment of the broader chemistry industry, there is emerging evidence that this segment is poised to grow rapidly.

In this report, we examine the business case for investment in green chemistry on the part of manufacturers, retailers, brands, and R&D teams. We present compelling evidence through a multi-method approach, relying on case studies, consumer product sales trends, economic value-added analysis, and prior research that suggests the green chemicals and products sector is growing rapidly and will likely become a dominant element of major investment portfolios in the near future. The findings presented here build on earlier reports over the last ten years, including by Pike Research (2011), Heintz and Pollin (2011), the Center for International Environmental Law (2013) and the Green Chemistry & Commerce Council (GC3), American Sustainable Business Council and Trucost (2015).

One of the primary drivers of the growth of green chemistry products is growing consumer and retail demands for products that are less impactful and healthier for people and the planet. As an increasing number of Fortune 500 companies commit to carbon neutrality and zero emissions targets by 2030, rational investors are naturally gravitating to the benefits of chemistries that can contribute significantly to these goals, whilst also appealing to a much more aware consumer base that is paying attention to the ingredients list in the products they buy. Our analysis suggests that significant growth in the last five years has occurred, but also projects that this growth is likely to increase significantly in the next five. Given the urgency to achieve multiple sustainable objectives such as addressing climate change, meeting UN Sustainable Development Goals, reducing the volume of non-degradable plastics in our oceans, and responding to increasing government requirements, we make a compelling case for expanding investments in this sector.

The $4 trillion conventional chemicals segment represents 7.1% of global GDP, making it the fifth largest global manufacturing sector in terms of annual contribution to GDP. The US chemical sector is the second largest in the world after China and produces 15% of the world's chemicals, produces more than 70,000 diverse products and is responsible for more than a quarter of US

GDP. More than 96% of US goods manufactured in 2016 and used in our everyday lives contained chemical sector products. Today, many of these products are produced using chemicals derived from finite and non-renewable fossil and mineral feedstocks. Given the massive footprint of chemicals across multiple product sectors, the replacement of fossil fuel petrochemicals with green chemicals represents a significant opportunity to make an impact on sustainability goals for many industries.

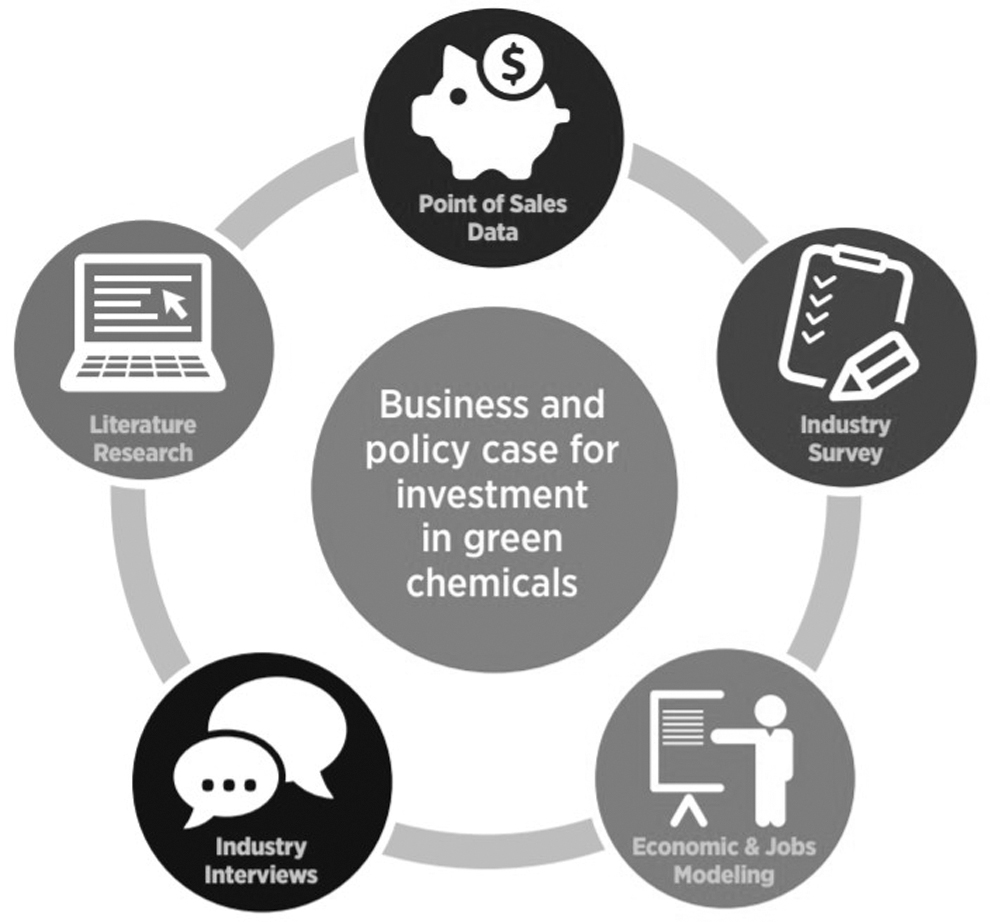

As shown in Fig. 1, the research team developed a multi-method analysis of the recent and projected growth of green chemistry products. First, researchers at NYU Stern School of Business conducted an analysis of IRI point of sales data in the United States. This analysis revealed a remarkable fact: there was more than a 40% market sector sales growth over conventional chemistries in the consumer products segment. Second, we conducted an industry survey that confirmed that the significant projected growth forecast holds not just for consumer products, but across a multitude of segments. Third, we developed an economic analysis using IMPLAN© economic modeling, that suggests that green chemistry will be a major source of job growth in the coming decade.

A multi-method analysis of the recent and projected growth of green chemistry products.

Finally, we reviewed extant literature and conducted numerous case studies, which suggest that green chemistry is being adopted and has become a critical component of corporate product innovation strategy across multiple sectors. The case studies we assembled in agricultural products, apparel, sporting goods, consumer electronics, retail, and beauty products all point to the same fact: enterprises are gravitating towards green chemistry for sound business reasons. Together, these multiple sets of analyses all point to the same conclusion: The green chemistry sector is set to become a major investment growth sector, which was confirmed by a major ESG investor that we interviewed as well.

The Five Key Findings

Our analysis provides a clear picture that an increased focus on protecting human health and the environment has become a priority for consumers, policy makers, upstream supply chain investments, and ESG-focused investors alike. The on-going goals for reduced carbon footprints by Fortune 500 companies makes this an important component of a sustainable corporate strategy, given the widespread use of chemistries across multiple industry portfolios.

There are five clear insights that emerge from our study: Green chemistry-marketed products significantly outperform their conventional counterparts in consumer markets. Consumers and institutional buyers are driving demand for green chemistry products. Emerging government policies and investor expectations are fueling growth of the green chemistry sector. The green chemistry sector will become a strong driver for job and economic growth. In response to increasing demands for more sustainable product portfolios, sales, sourcing, and R&D are working hand in hand to drive green chemistry solutions into the future product mix.

FINDING #1: GREEN CHEMISTRY-MARKETED PRODUCTS SIGNIFICANTLY OUTPERFORM THEIR CONVENTIONAL COUNTERPARTS IN CONSUMER MARKETS

Researchers at the NYU Stern Center for Sustainable Business conducted an analysis using IRI data which reflects all scanned package goods purchased in measured US outlets including food, drug, mass merchandisers, dollar, and convenience stores between 2015 to 2020. Ten categories were analyzed that included products with green chemistry formulations. As shown in Fig. 2, from 2015–2019 (prepandemic) green chemistry marketed products grew at a much faster rate than their conventional counterparts by 12.6x and faster than the overall market by 5.4x.

Growth of green chemistry marketed-products from 2015–2019. From 2015–2019, green chemistry-marketed products (10 categories examined) grew 12.6 times faster than their conventional counterparts, and 5.4 times faster than the market.

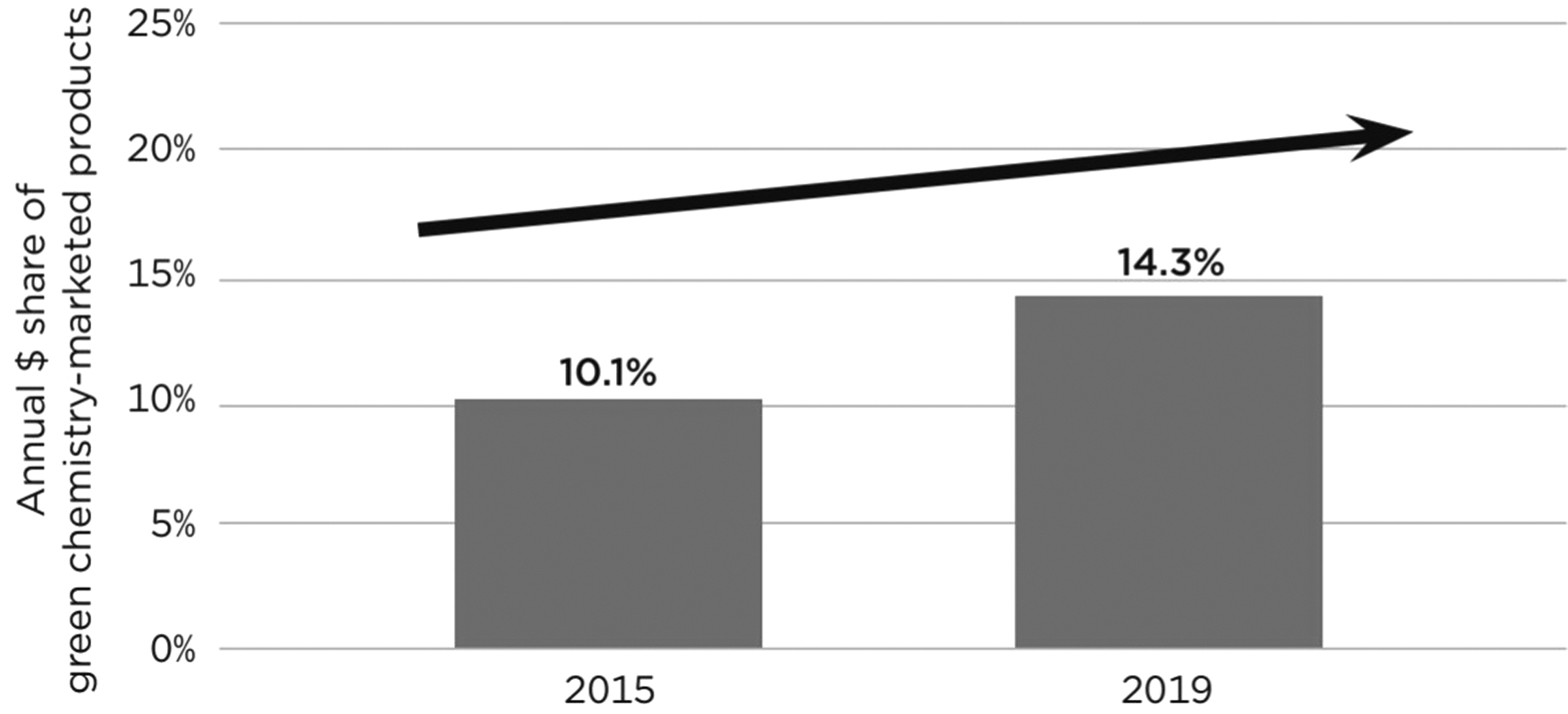

The data tell the story. Between 2015 and 2019, green chemistry-marketed products represented almost 62% of overall market growth for the 10 categories evaluated (Fig. 3). During the same time, green chemistry products rose to over 14% of the total market share in 2019 using US dollars. Even the pandemic did not slow down the growth of the green chemistry sector and the longer-term outlook of analysis of the sector indicates a 6.6%–11.5% compound annual growth rate (CAGR) between 2020–2025 (Fig. 4).

Market growth of green chemistry products. Green chemistry marketed products (10 categories examined) are 14.3% of the market and delivered 62% of the categories market growth (2015–2019).

Green chemistry-marketed products continue to climb in 2020, despite the pandemic. Across 10 categories studied, green chemistry-marketed products account for 14.3% share of market ($) in 2019, up from 10.1% in 2015.

FINDING #2: CONSUMERS AND INSTITUTIONAL BUYERS ARE DRIVING DEMAND FOR GREEN CHEMISTRY PRODUCTS

During winter 2021, the research team undertook a survey of companies across sectors and the value chain. The findings, based on 54 respondents representing 15 sectors and the full value chain, reinforced what we heard from our one-on-one interviews with industry leaders. Although the greatest growth of green chemicals is occurring in consumer-facing industries, such as consumer cleaning products, health and beauty, footwear and apparel, and children's products, we are seeing growth in the B2B sector as well, including paints and coatings, construction materials, packaging, electronics, and other areas. This suggests that both consumers and institutional buyers are responsible for the growth of the green chemistry sector. Other factors driving growth identified in our survey included:

C-Suite priorities

Regulations

Shareholders and investors

Advocacy campaigns

The consumer demographics driving the largest growth in demand for products of green chemistry include Millennials (1981–1996); Gen Z (1997–2012); and Higher Income Consumers.

Our case studies also suggest that large brands are leading the way and using their purchasing power as leverage to shape the industry. Companies such as Apple, Unilever, Lowe's, and Nike are all establishing aggressive goals to reduce their chemicals and carbon footprints. For example, in January of 2021, multinational consumer products powerhouse Unilever, announced that it is committed to making all its cleaning products carbon neutral by 2030. They will devote more than $1.2 billion to switch to renewable or recycled carbon in its cleaning products.

Finding #3: EMERGING GOVERNMENT POLICIES AND INVESTOR EXPECTATIONS ARE FUELING GROWTH OF THE GREEN CHEMISTRY SECTOR

Our analysis of key trends suggests that strong government policies do indeed make a difference and are driving growth of innovation in green chemistry across multiple sectors. New policies such as the European Commission's Chemicals Strategy for Sustainability, state policies in the United States, and implementation of the Lautenburg Chemical Safety for the 21st Century Act in the US have created strong regulatory signals to the marketplace that are influencing investors. A greater number of investment houses outside of the traditional ESG sector are making significant inroads into the green chemical space, such as Carlyle's acquisition of Beautycounter (discussed in our case studies). Policies that foster increased investments in research and development, preferred acquisition status on government contracts, preferred product placement in retail establishments, and private and public labeling and certification programs that assist consumer and institutional purchasers in identifying safer and more sustainable products are attracting more and more companies to pursue green chemistry objectives.

Our previous research indicated that between 2017 to 2019 the growth in the number of products certified by the USDA's BioPreferred Program increased by 93%. More than 2,000 products currently carry the US EPA Safer Choice Label.

Due to investor and consumer pressures multinational corporations are working on efforts to market more sustainable and green chemistry products including the world's largest retailers Amazon and Walmart. Many brands are driving the green chemistry sector. More than 32 global brands, along with suppliers and others have come together to form the ZDHC, which enables companies in the textile, apparel, and footwear industries to implement chemical management best practice across the value chain to advance a zero discharge of hazardous chemicals.

FINDING #4: THE GREEN CHEMISTRY SECTOR WILL BECOME A STRONG DRIVER FOR JOB AND ECONOMIC GROWTH

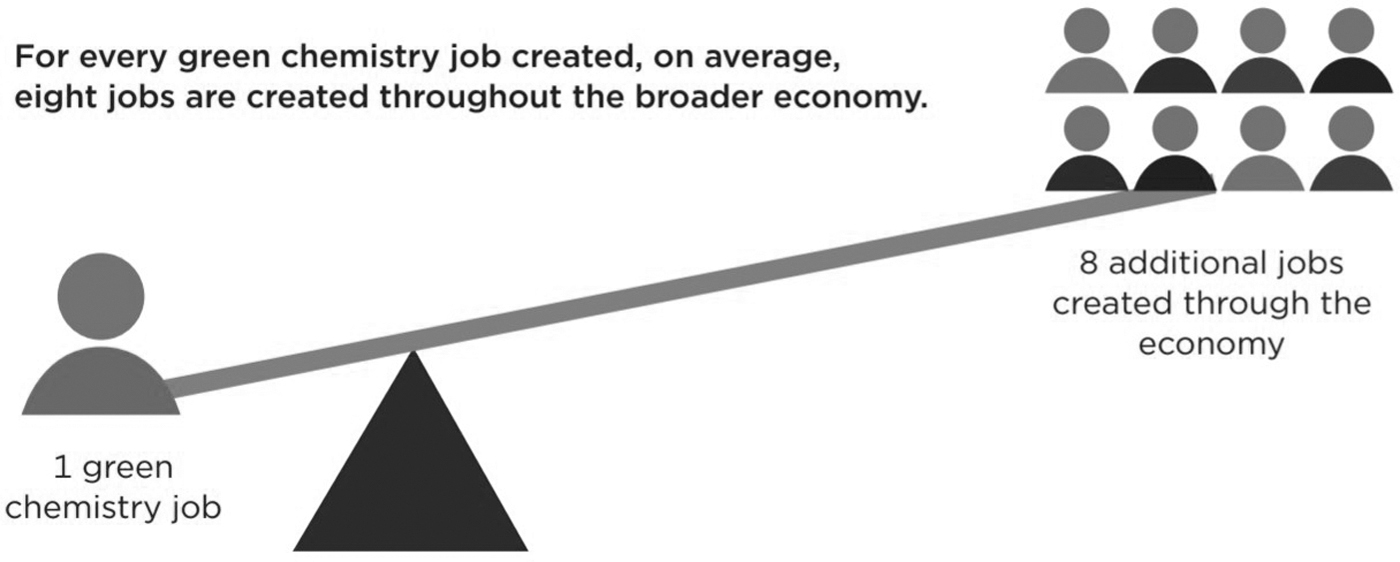

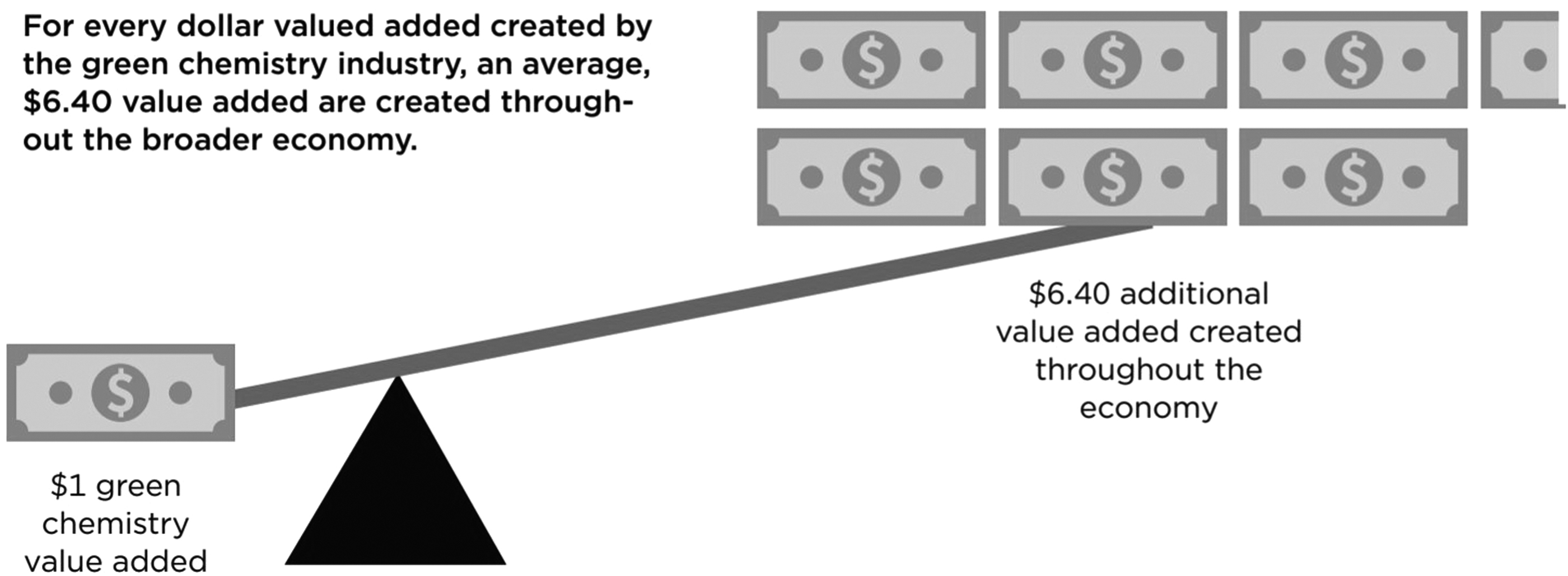

When sales of products of green chemistry increase, jobs in the industry increase accordingly (Fig. 5). While such jobs may only be a small part of the industry, our data indicate that growth in this segment is faster than traditional chemistry. While the direct jobs in the green chemistry industry are important to quantify, the indirect (green chemistry supply chain) and induced (restaurants and lifestyle supporting industries) jobs are also a major contributor to employment. The employment multiplier is another metric used to understand the economic impacts of an industry. In this case, for every job created in the green chemistry industry, on average, 8 additional jobs are created throughout the broader US economy. this case, for every job created in the green chemistry industry, on average, 8 additional jobs are created throughout the broader US economy (Fig. 6).

Green chemistry jobs and economic growth.

Green chemistry value added multiplier.

Example: Biobased Products

A subset of green chemistry industry is the biobased products industry which is a sector with increasing demand and corresponding production of goods. Biobased products are based on plant materials in lieu of petroleum-based and other synthetic raw materials. In 2017, the biobased industry in the US supported over 4.6 million people and created $470 billion in value added. This industry as a whole had an economic multiplier of 2.79 (Fig. 7).

Biobased products economic impact.

FINDING #5: IN RESPONSE TO INCREASING DEMANDS FOR MORE SUSTAINABLE PRODUCT PORTFOLIOS, SALES, SOURCING, AND R&D ARE WORKING HAND IN HAND TO DRIVE GREEN CHEMISTRY SOLUTIONS INTO THE FUTURE PRODUCT MIX

Almost 58% of the respondents from our survey of business leaders across the value chain indicated that during the period of 2016 to 2020 sales of green chemistry products showed either greater growth (40%) or much greater growth (17.78%) as compared to traditional products. The survey also shows that 84% of industry respondents have increased investment in R&D of green chemistry products during the last five years and 98% anticipate continued R&D investments in green chemistry products over the next five years. More than 58% of respondents believe that sales growth will be significantly greater in the same period. Specifically, most respondents reported moderate to very strong growth both in the United States (68.43%) and outside of the US (83.93%) during the past five years. Growth is particularly high in packaging, health and beauty, household CPG products, along with toys and footwear/apparel.

Interviews with business leaders demonstrates a strong commitment across sectors, the entire value chain, and companies of various sizes to investment in green chemistry solutions. The following quotes provide a number of key insights into how different organizations are making big shifts in their product portfolios in response to demands for a new generation of emerging green chemistries.

Footnotes

Acknowledgments

This report was commissioned by the Green Chemistry & Commerce Council (GC3), a multi-stakeholder business collaborative. whose members include major brands, retailers, chemical suppliers and innovative startups, across sectors. The GC3 drives large scale commercial adoption of safer, sustainable, high-performing chemical solutions by fostering value chain collaboration, cultivating first-movers, convening industry decision-makers to secure major commitments, and creating a supportive policy environment.

The Passport Foundation provided funding to support the research and writing of this report. Information Resources, Inc. generously provided NYU Stern School of Business academic access to its data. Our thanks to the many individuals who provided insights, connections, and support for the research conducted as part of this report, including Jim Jones, Michele Jalbert, Molly Jacobs, Tensie Whelan, and Alexandra Walstad.

DISCLAIMERS

The information and opinions expressed in this report are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. It is only intended to provide education about the green chemistry sector.

All estimates and analysis in this paper based on Information Resources Inc., data are by the authors and not by Infor-mation Resources, Inc.

Editor's Note

This report was excerpted with permission from the Green Chemistry & Commerce Council (GC3). The full report can be found at