Abstract

As Congress tackles the 2023 Farm Bill reauthorization, one important topic that requires attention is the emerging demand for a federal label to effectively track the carbon intensity of agricultural feedstocks and products throughout the value chain. This need is being driven in large part by biobased industries, brands and financial institutions that have publicly committed to a net-zero carbon transition. This paper presents five important insights for Congressional members and industry to consider.

Introduction

Congress has begun hearings and debates regarding the 2023 Farm Bill, with sights set to improve upon the previous 2018 Farm Bill. The timing of this round of reauthorization comes at a unique period when America's agriculture and industrial sectors are realizing greater interdependency as well as domestic economic job growth opportunities. Specifically, we refer to one of the most significant developments within global business in the last decade—the commitment by companies to transition to a net-zero carbon economy, which is in part based on the expansion of low carbon biobased feedstocks in lieu of legacy non-renewable sources. Over the last few years, the researchers in our lab have been actively working with leading companies and industry associations spanning agriculture, chemical, energy, consumer products and retail sectors as they seek pathways to meet low carbon feedstocks and products as a result of global demand from manufacturers, brands, the finance sectors, shareholders and consumers.

In light of these opportunities and the upcoming Farm Bill reauthorization deliberations, we provide five insights for Congress to consider as part of their work on the 2023 Farm Bill. The insights are based on our work on both the net-zero carbon transition and years of work by the first author in supporting American agriculture, manufacturing and rural America in regard to the U.S. Biobased Economy and the Biobased Products Industry.

1

-6

We have also gained significant perspective from our collaboration with the Alternative Fuels and Chemicals Coalition (

These five insights are presented with the goal of maintaining America's leadership role in supplying the world with growing demands for food as well as low carbon climate smart feedstocks and manufactured products. However, to achieve this goal, Congress will need to support industry and farmers as they innovate and transition to a new generation of low carbon climate smart solutions for domestic and global consumers.

Insight #1: Industry and Governments are Rapidly Transitioning to a Net-Zero Carbon Economy

As of November 2022, around 140 countries had announced or are considering net zero targets, covering close to 90% of global emissions, a stark contrast compared to 130 countries, covering about 70% emissions in May 2021. 7

Additionally, state and local governments are also committing to a net-zero carbon economy. New York State's Climate Leadership and Community Protection Act (Climate Act), which is considered one of the nation's most ambitious climate laws in the United States, seeks to reduce economy-wide greenhouse gas emissions 40% by 2030 and a minimum of 85% by 2050 from 1990 levels. 8

Governments may in fact take a back seat to the broader impacts and pace of corporations. Currently, 826 of the largest publicly traded companies have made net-zero commitments including Walmart, Apple, BP, Procter and Gamble, Amazon and many more. 9 Additionally, as of 2022, over 75% of the 166 focus companies in Climate Action 100+ that have been selected because they account for up to 80% of global corporate industrial greenhouse gas emissions have committed to achieve net-zero emissions by 2050 or sooner across all or some of their emissions footprint (up from 69% in March 2022). In addition, over a third of focus companies have set long-term targets that align limiting temperature increases below with a 1.5°C pathway (an increase of 9% from March 2022). 10

These commitments are backed by corporate strategies addressing (1) emissions reductions through technology including carbon capture and sequestration; (2) the electrification of transportation, modes of production, and buildings; (3) sourcing materials to create cleaner supply chains; and (4) purchasing carbon offsets from voluntary carbon markets. And, to further structure and ensure transparency the U.S. Securities Exchange Commission (SEC) has proposed requiring disclosure of climate related risk to investors in addition to scopes 1, 2, and 3 GHG emissions if emissions targets are included in a company's climate commitments. 11

Numerous brands, non-governmental organizations and governments have begun placing some form of carbon intensity labels on specific products. In fact, a recent study by the Dynamic Sustainability Lab done in collaboration with the AFCC accounted for over 250 such non-standardized labeling schemes across the globe which signals a need for oversight and coordination to minimize greenwashing and to increase both the utility and the trustworthiness of carbon labeling schemes. 12

Insight #2: Recent Government Incentives are also Driving the Net-Zero Carbon Economy

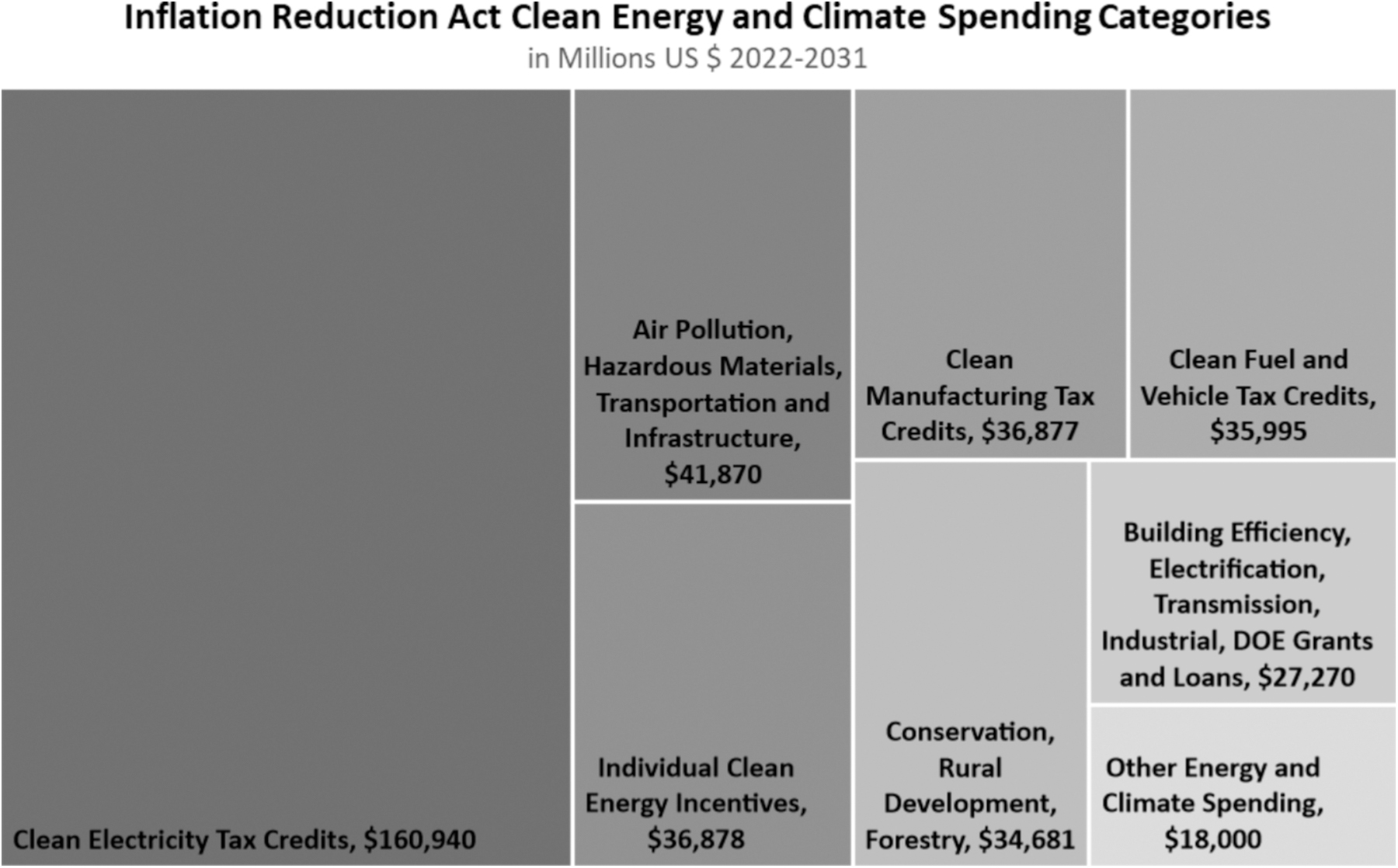

Further accelerating the net-zero carbon transition is the very recent and unprecedented infusion of large amounts of financial capital into the economy to drive the net-zero carbon transition especially in the United States. In 2022, the Biden Administration and Congress passed the Inflation Reduction Act (IRA) which will make available over $370 billion over 10 years for climate and renewable energy initiatives. The IRA provides over two dozen tax provisions that will accelerate the deployment of clean energy, clean vehicles, clean buildings, and clean manufacturing. It also provides billions of dollars in grant and loan programs and other investments for clean energy and climate action (Fig. 1). 13,14

Distribution of the Inflation Reduction Acts expected clean energy and climate spending 2022–2031. Source: Congressional Budget Office. 14

Additionally, in late 2022 the U.S. Department of Agriculture (USDA) launched the newly crafted Climate Smart Commodities program by investing more than $3.1 billion in 141 projects across the country. This is expected to expand hundreds of markets and revenue streams for more than 60,000 farmers and ranchers with commodities across agriculture and forestry ranging from traditional corn to specialty crops. The goal is to sequester more than 60 million metric tons of carbon dioxide equivalent sequestered over the lives of the projects. 15

Insight #3: The Important Role of American Agriculture in the Transition

Increasingly the biobased economy has given rise to new and emerging opportunities for American agriculture providing economic growth and jobs especially in rural communities across the United States. If we reflect and explore biofuels as a starting point, we see that as recently as 1986 just 3.9% or 290M bushels of domestically produced corn was used for biofuels in the U.S. Jump forward to 2021 and 5.326 billion bushels of corn were used for ethanol equaling 35.6% of the domestically grown corn used for biofuels. While records of soybean oil used for biofuels only date back to 2001, the share used for biofuels was less than 1%, compared to 38.9% in 2021 or 10.35 billion pounds of soybean oil. 16

While the USDA is currently updating their report on the Economic Impact Analysis of the U.S. Biobased Products Industry, the most recent release that examined 2017 showed that the biobased products industry supported 4.6 million American jobs through direct, indirect and induced contributions, contributed $470 billion to the U.S. economy and generated 2.79 jobs in other sectors of the economy for every biobased job. Further, this jobs calculation does not include biobased energy and fuels nor biobased food additives. 6

Insight #4: Federal Government Coordination is Needed Now

To achieve governmental and industry led net-zero carbon commitments and annual reporting of carbon in operations and the supply chain, businesses across the country and globe are seeking a trusted way to communicate carbon intensity of feedstocks and products.

Yet, due to a lack of federal oversight and coordination many domestic and international businesses, non-governmental organizations and even some U.S. states are filling the void of the federal government to create pathways to track, validate and communicate carbon in the value chain and to consumers.

Many times, these approaches lack any transparent and scientifically grounded standards. Even if they have some vetted standards, the lack of federal oversight and coordination across various forms of a carbon intensity label can be contradictory with one another. At best, this causes confusion in the marketplace and at worst, promotes greenwashing. Now is the time for Congress and the federal government to address this rapidly evolving challenge and exert its role.

Insight #5: The 2023 Farm Bill Reauthorization Provides a Clear Opportunity

The 118th Congress is currently deliberating and holding hearings for the reauthorization of the Farm Bill which takes place by statute every five years since 1930. This provides members a unique opportunity to support not only rural agriculture and farming families, but it also has direct implications for U.S. green tech manufacturing, economic growth and trade by supporting the development of a national carbon labeling scheme.

We believe that the U.S. Department of Agriculture and the Office of Rural Development in consultation with other federal agencies provides the most appropriate federal lead to develop a national strategy as well as the implementation of a carbon label over the next few years.

In part this is due to their experience and market confidence in managing the USDA BioPreferred program. The BioPreferred Program and labeling scheme was developed under the 2002 Farm Bill to increase the utilization and consumption of biobased products. 6 This program introduced a federal purchasing program for biobased products and launched a national voluntary product labeling program for biobased products in 2011. 6 Twelve years later, the USDA boasts over 20,000 biobased products in its BioPreferred registry with 3,000 companies and 15,000 products utilizing the USDA BioPreferred label (Fig. 2). 6

The USDA BioPreferred Label. Source: Daystar et al. 6

However, it is time for a next generation label which aligns with USDA's recent efforts to grow Climate Smart Commodities in the marketplace. It is our recommendation that Congress in the new Farm Bill authorize and appropriate funding to USDA to immediately convene appropriate stakeholders from agriculture, manufacturing, retail, finance, insurance and logistics as well as relevant state and federal agencies, academia and non-governmental organizations to evaluate and develop pathways for a national carbon label. The immediate goals should be to signal to the marketplace the federal government's intended leadership in developing and coordinating a carbon label and importantly, to make recommendations on a logical pathway to develop the technical approaches to produce and maintain a national label.

Without the leadership of Congress and the Administration, we risk confusion and distrust in what will no doubt be the emergence of a plethora of unvalidated and confusing carbon labels on products.