Abstract

Introduction

Since the U.S. Food and Drug Administration (FDA) approved the first biosynthetic drug, insulin, four decades ago, the market for products created through precision fermentation and biomanufacturing has grown to $100 billion. The sector’s success led to predictions that precision-fermented bioproducts would disrupt industries from pharmaceuticals to food to chemicals.

But in areas other than pharma—whose business models are built on high-margin, low-volume products with low sensitivity to costs—innovations have created only niche markets in enzymes, fragrances, and food and feed supplements.

This may be about to change. Demand is solidifying for products that use biological processes and genetically modified microorganisms in place of traditional production methods, driven by the need to achieve sustainability in manufacturing while reducing carbon emissions. At COP28, nearly 200 nations signed on to moving away from fossil fuels and, therefore, petrochemicals. More than 4,100 of the world’s largest companies have established emissions–reduction targets, according to the Science-Based Targets initiative, with more than 2,600 of them including net zero emissions commitments. In its March 2023 report, Bold Goals for US Biotechnology and Biomanufacturing, the White House set a target of producing “at least 30% of the US chemical demand via sustainable and cost-effective biomanufacturing pathways” within 20 years.

But for change to happen, costs must come down. Meeting the sustainability and emissions—reduction needs of global industry depends on achieving economically viable precision—fermentation biomanufacturing at commercial scale and bringing production costs into parity with existing methods. These in turn require construction and optimization of biofoundries—large-scale, standardized biomanufacturing facilities that can meet industrial-level demand—and continued improvements in strain engineering.

Participants all along the value chain have important roles to play. Most immediately, corporate customers—the same companies that need to meet sustainability and net zero pledges—must demonstrate that the demand is real by committing to offtake agreements for future delivery of new ingredients and by adapting their supply chains and product formulations accordingly. Policy makers and regulators can smooth the way by offering incentives and loan guarantees and removing red tape. As demand for new facilities gains traction and financial risks recede, project finance investors can step in with necessary capital.

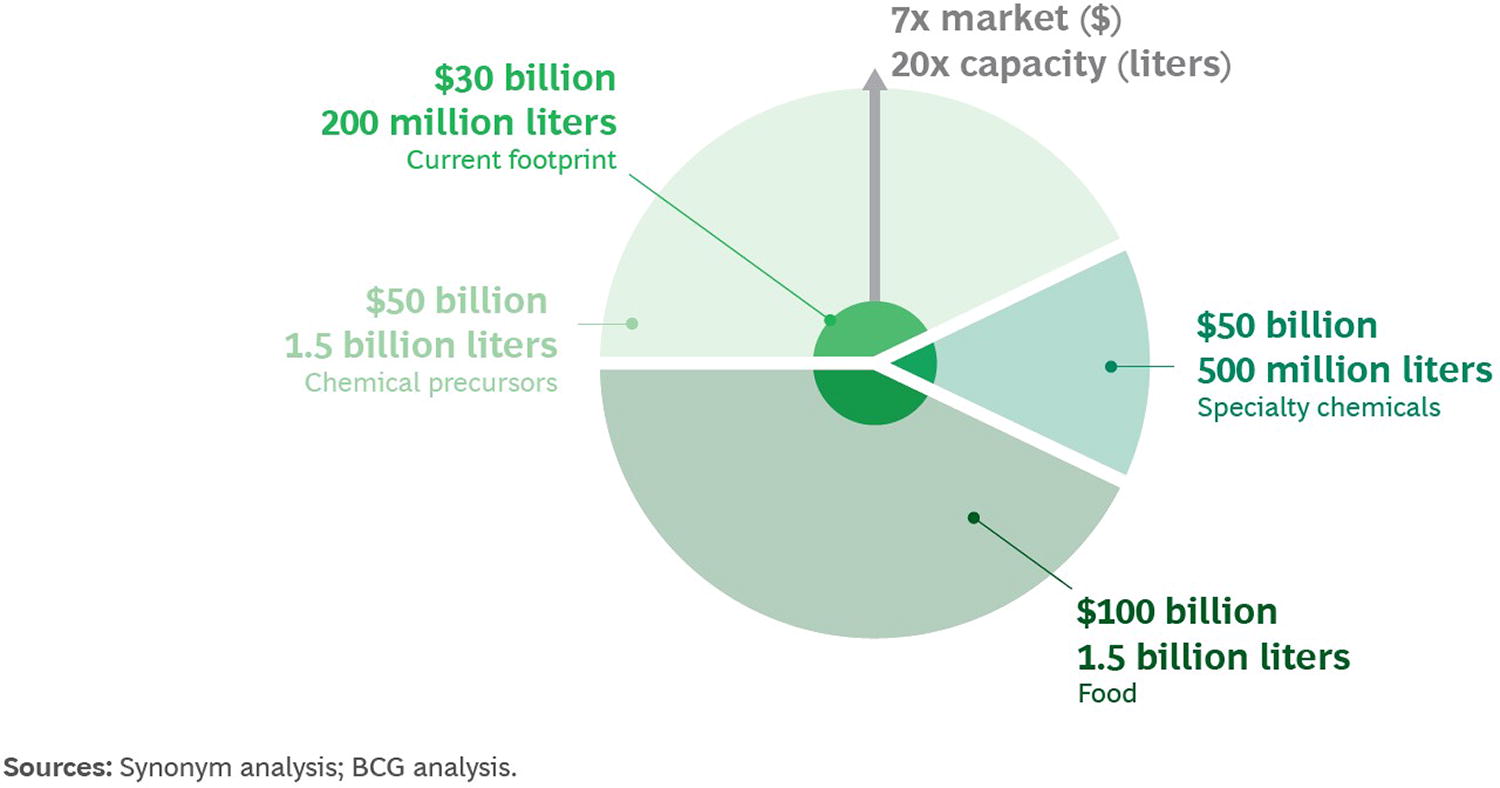

As we have seen with other advanced technologies, the result can be a virtuous circle. The first optimized largescale facilities can lower production costs by as much as 50% on existing strains, enabling some cost parity with incumbent technologies. More and larger facilities, as well as improved strains, could reduce production costs by up to 90%, achieving or surpassing price parity with current incumbent methods for most products (Figure 1). In fact, we estimate that the market for biomanufactured ingredients in three industries—specialty chemicals, food, and chemical precursors—could reach $200 billion by 2040—if the manufacturing capacity is there.

BCG has been researching and advising clients for years on developments in advanced technologies. Synonym is developing the physical, digital, and financial infrastructure to catalyze a biomanufacturing revolution. Here is our view on how biomanufacturing can finally fulfill its promise of achieving commercial scale.

Boosting Biomanufacturing Supply by Driving Down Costs

Two truths: the range and performance of precision fermented products are relevant for almost all manufacturing companies, and biomanufacturing is a tried and tested technology. The big problem—and the reason that precision fermentation remains an underused technology despite continuing advances in genome engineering and strain development—is the high cost of production, which stems from adherence to rigorous standards to ensure high quality (Figure 2).

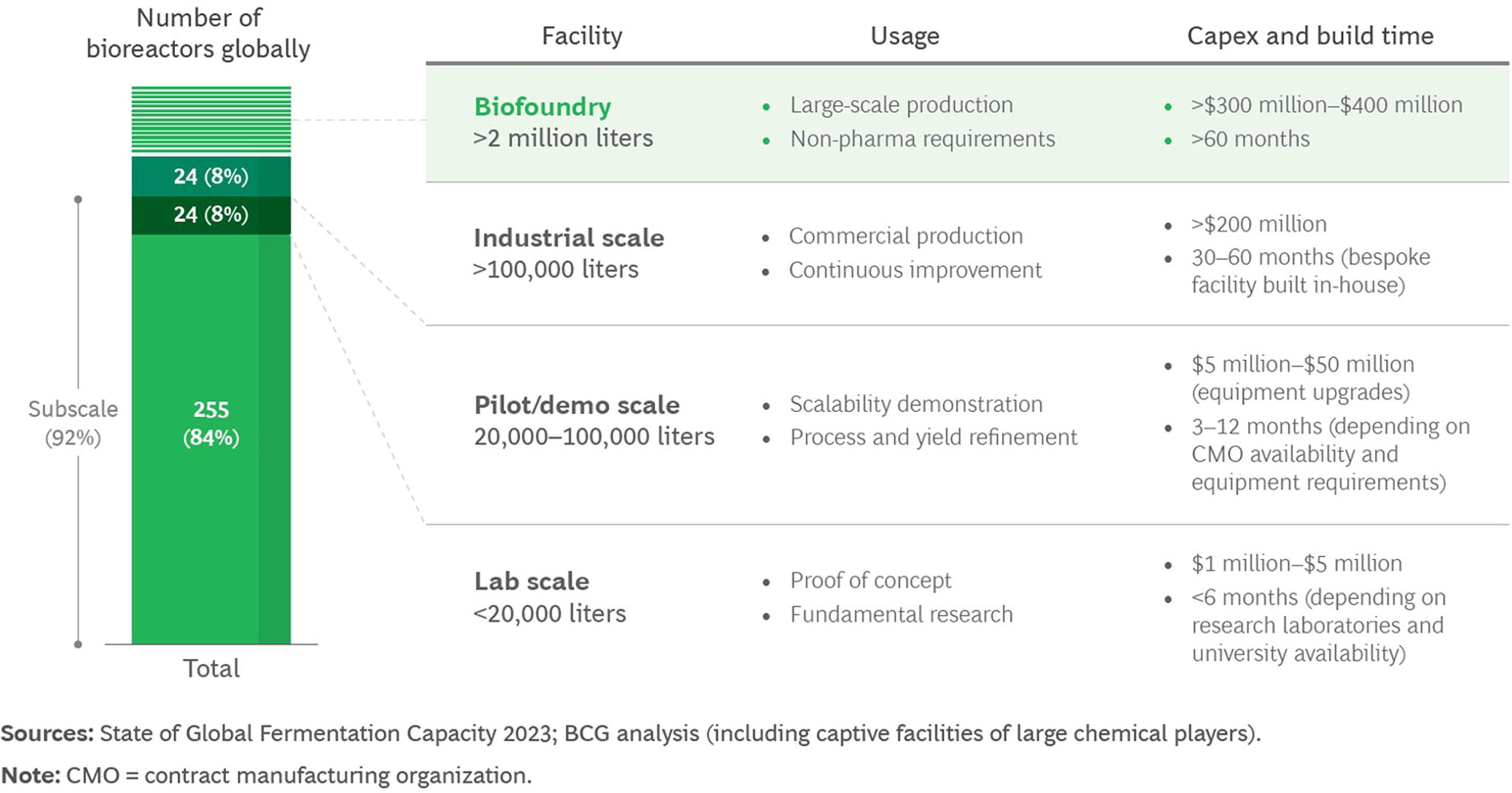

Biomanufacturing involves fermentation under optimal conditions (pressure, temperature, pH, and concentration of oxygen and nutrients) in a fermentor purpose-built for aerobic fermentation followed by downstream processing (DSP) to isolate the end product via separation and purification steps such as filtration and spray drying. Advances to date have been driven primarily by pharmaceutical standards. Contract manufacturing organizations (CMOs), which serve the pharmaceuticals industry, have small-scale, high production costs, and unprofitable unit economics for most nonpharma bioproduct companies. In addition, customers must invest a significant amount of up-front capital to fund DSP, making the economics even more unfavorable. Only a handful of CMOs have the available capacity of more than 100,000 L.

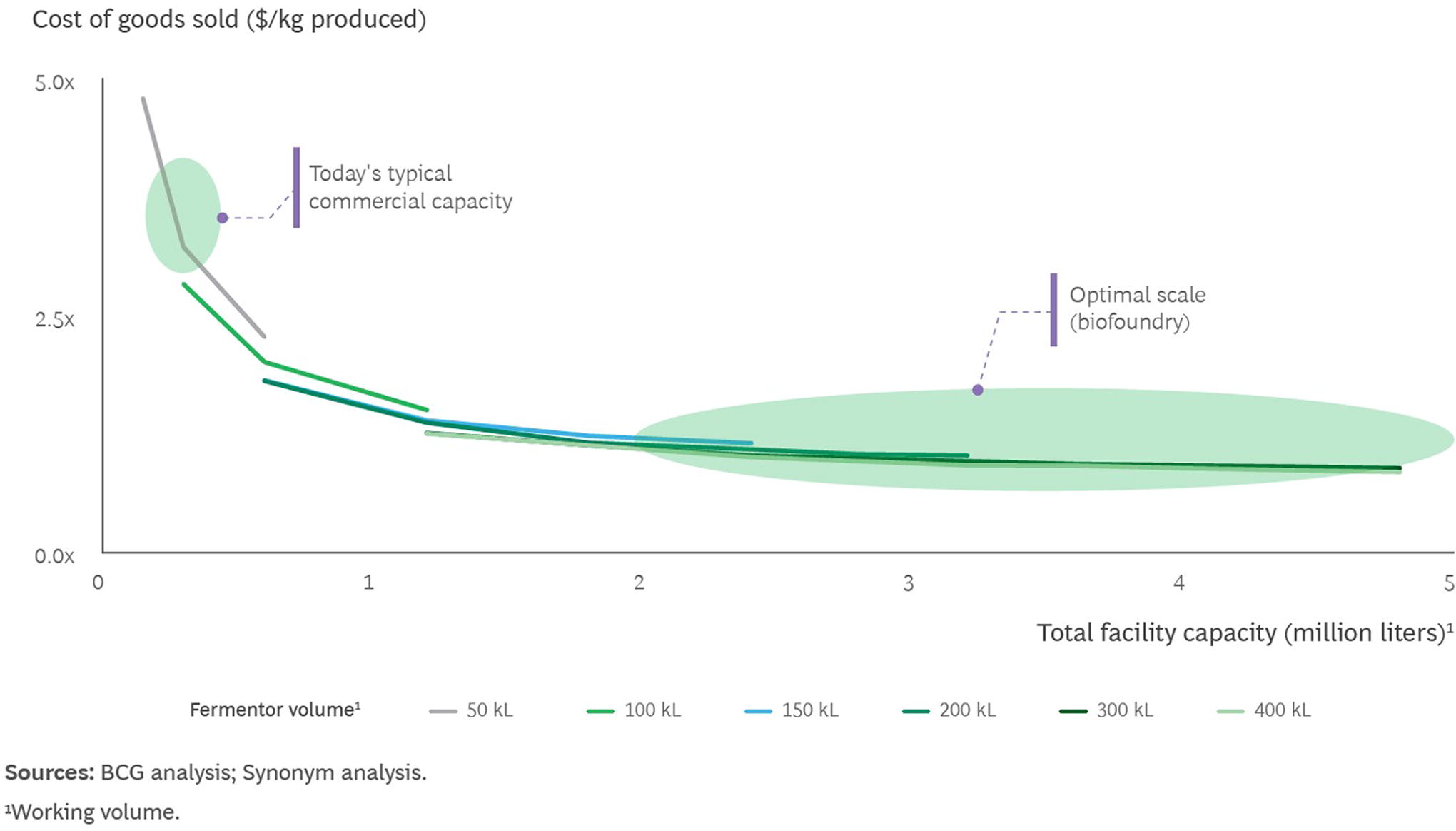

Enter biofoundries—facilities that are designed, built, standardized, and optimized for efficient production of nonpharma bioproducts. Each such facility can provide at least 2 million liters of capacity, achieving commercial economics and bridging the cost gap for large production categories such as foods and biomaterials by reducing unit costs by about 50% (Figure 3).

Some innovations that make biofoundries possible (such as the use of AI and high-precision sensors) require advances in technology, but many other improvements involve only cost optimization related to process engineering. These levers focus on such high-cost items as energy demand and labor and maintenance. For example, three pieces of equipment—agitators, chillers, and air compressors—account for approximately 70% of an entire facility’s electrical demand. For some strains, companies can reduce these requirements by optimizing mass transfer design to lower the combined agitation and air compressor electrical loads and by improving the cooling system design to lessen the chiller system electrical loads. Modular design reduces construction timelines and costs and augments utilization rates by accommodating varying customer needs.

Companies can improve costs in at least ten specific areas in categories ranging from variable costs to factory utilization (Figure 4).

Standardization and optimization provide biofoundries with significant advantages over existing large-scale biomanufacturing facilities, particularly with respect to cost, timeline, and adaptability. The bespoke nature of traditional facilities results in elevated costs and prolonged timelines. These facilities demand substantial up-front capital investments, ranging from $300–$400 million each, and the time required for design and construction is typically 3–5 years.

In contrast, standardized biofoundries have the potential to reduce costs and construction times. Initial facilities are expensive, but they offer multipurpose functionality and adaptability. Standardization can reduce the capital investment for later biofoundries by up to 30%. This approach not only mitigates risks but also helps make biofoundries a versatile solution that can meet evolving needs and advances in future strains.

A Potential $200 Billion Market

There are strong financial reasons to press forward. We estimate that scaling up industrial precision fermentation can create a $200 billion market by 2040, seven times the current size, if companies build enough production capacity to lower costs (Figure 5). Indeed, the primary constraint on ultimate market size is biomanufacturing capacity. There are practical limits to how much and how fast such capacity can be built.

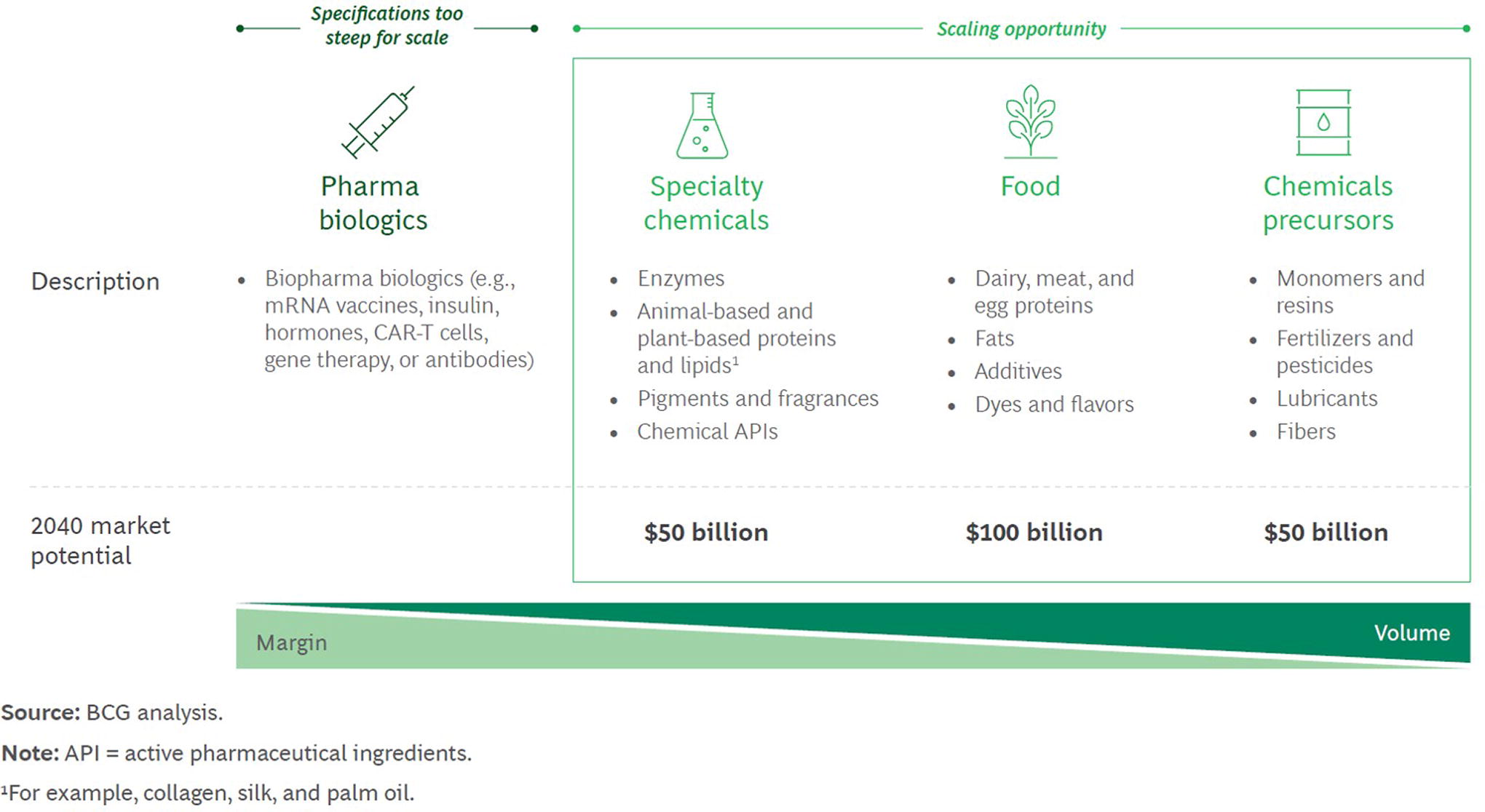

Market sizing estimates by others have run into the trillions of dollars. We, however, focus exclusively on the market for the bioproducts produced by the new biofoundries, which are most often used as ingredient inputs, and not the market for formulated finished products, which (as noted) include most of the products made today. Three of the biggest near-term opportunities involve specialty chemicals, food, and chemical precursors (Figure 6). Standardized biofoundries can serve all of these markets, with construction focusing on higher-margin, lower-volume molecules first.

SPECIALTY CHEMICALS

Molecules include enzymes, nonedible proteins (such as collagen and silks) from animal sources, pigments, fragrances, and chemical active pharmaceutical ingredients such as certain antibiotics and statins. In this segment, biomanufacturing currently commands an average cost premium of 30% to 50%, depending on the molecules involved. The segment also encompasses cosmetics and active ingredients that are regulated and therefore require large and lengthy R&D investments (e.g., 5–10 years for cosmetics). We estimate the segment’s 2040 market potential at $50 billion.

FOOD

The potential bioproduct market for foods includes dairy, meat and egg proteins, fats, additives, and food dyes and flavors. Companies already produce several molecules (including some vitamins, amino acids, and flavors) at scale, proving the demand for such products. Current biomanufacturing costs for some products are two to three times as high as for the same products manufactured by incumbent methods, but biofoundries could lower those costs to parity or below. Animal agriculture is responsible for 15% of greenhouse gas emissions and significant water and land usage. It provokes ethical concerns related to animal cruelty. Biomanufacturing offers a competitive, sustainable, cruelty-free alternative (see “Precision Fermented Foods: The Next Wave?”).

The task of building demand still faces plenty of challenges, including the need for widespread customer education and for new rules and regulations (including for food labeling and manufacturing facilities inspections). Regulatory authorities such as the FDA in the United States and the European Food Safety Authority must also develop validation and inspection rules and procedures to facilitate the development of new, sustainable, and safe products without increasing time-to-market. By achieving both price parity and decreased emissions, the overall fermentation food market should grow to $100 billion by 2040.

CHEMICAL PRECURSORS

Currently, chemical precursors consist of petrochemical compounds such as ethylene (which after polymerization becomes PET plastic). They are a $600 billion market that is growing at 3% a year along with fossil fuel production. The products are cheap to make, since they use compounds found as byproducts of the fuel refining process. They are found in an array of end products, including polymers (such as plastic), resins, fertilizers, pesticides, lubricants, cloth fibers (such as polyester), and even drugs (aspirin, for example) and food additives (think truffle flavor). In the past 70 years, they have displaced preexisting methods and products that sometimes used fermentation (such as ammunition produced during the two world wars).

Because chemical precursors are so inexpensive to produce, early biofoundries may struggle to compete. Nonetheless, we expect a market of $50 billion to develop over time. Specific products for which cost parity or increased performance is achievable will emerge. We also expect further regulation or even restriction of petrochemical use, increasing customer interest in bioalternatives such as bioplastics. Ultimately, as the recent COP28 agreement suggests, petrochemical use will decline along with oil production, which will open further opportunities for alternatives.

CARBON BENEFITS

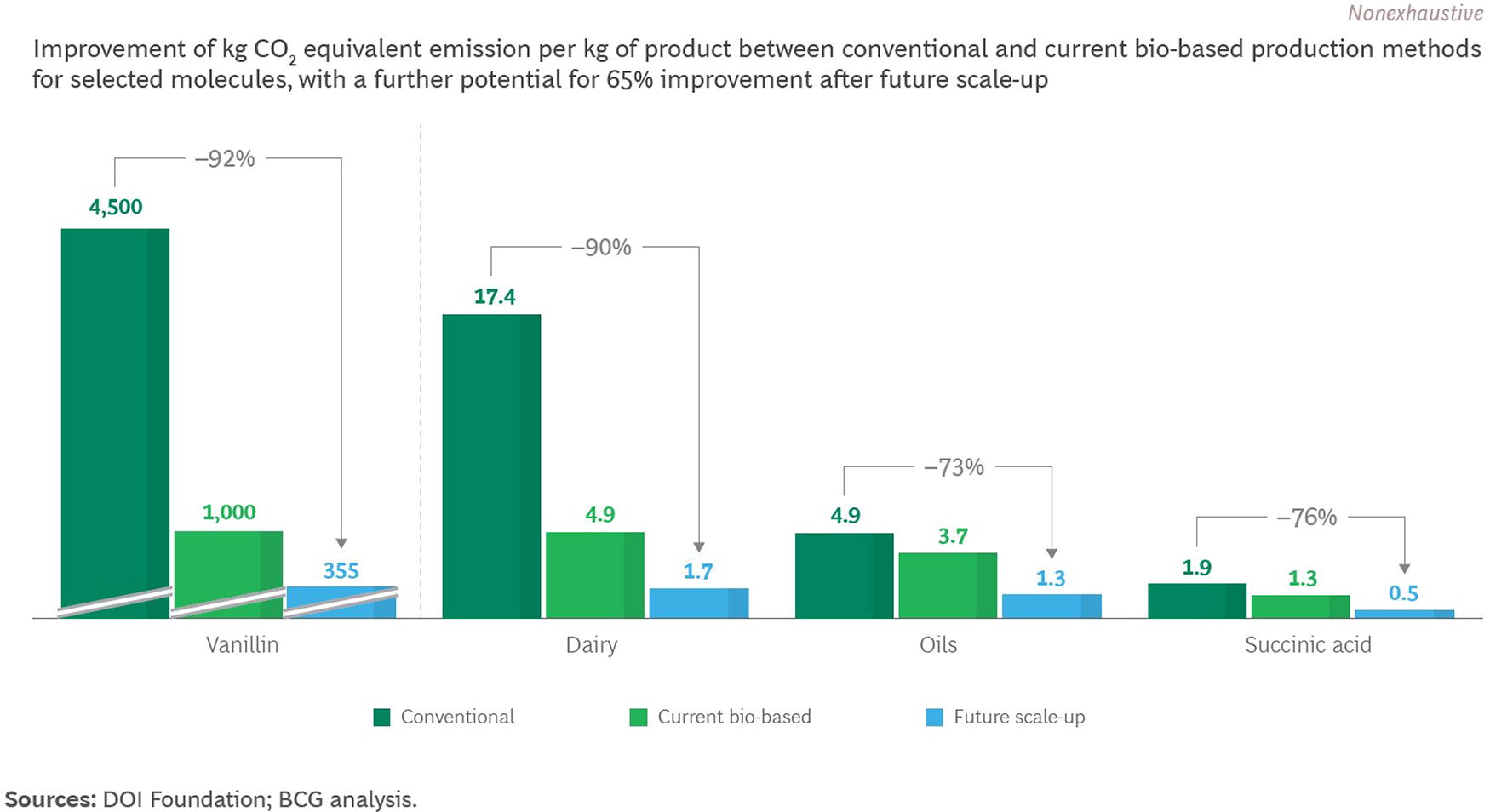

In addition to reducing greenhouse gas emissions, by using biogenic rather than fossil-derived inputs, biofoundries improve yield and energy efficiencies, making biomanufacturing at scale a more appealing alternative for producing most molecules, from the standpoint of CO2 emissions (Figure 7).

Precision Fermented Foods: The Next Wave?

Companies are already using precision fermentation at scale to produce some additives. Products include flavor enhancers (glutamic acid), acidifiers (citric acid, fumaric acid, and malic acid), low-calorie sweeteners (aspartic acid), and thickening agents (xanthan gum). Decreasing costs could enable companies to target new markets.

Several dyes and flavor molecules are currently being supplanted by bioproduced equivalents. These include flavors such vanillin, santalol, menthol, Nootkatone, lactones, alpha-ionene, and valencene, and dyes such as carminic acid (used in products ranging from candy to yogurt to sausage), anthocyanin, and carotenoids.

We expect precision fermentation to unlock the next wave of growth in alternative foods. As the growth of plant-based foods plateaus, precision fermentation is on the cusp of offering new alternatives for meat, eggs, dairy, additives, dyes, and flavors.

For example, multiple companies are now fermenting various types of proteins to formulate such dairy end products as milk (including infant milk), cheese, butter, and cream.

Fermentation is also well suited to the production of animal protein replacements, such as egg protein for making cakes, and heme (a precursor to hemoglobin) to give more meat-like flavor to plant-based alternatives.

Thanks to the latest developments in strain engineering, the cost of developing a strain for a specific molecule has fallen drastically. This opens the way for precision fermentation to produce more molecules than before, without being restricted to addressing only very large markets. In the future, we expect precision fermentation to enter many midsize and smaller markets.

Investing in the Infrastructure of the Future

Breaking through the cost conundrum that has bedeviled biomanufacturing will depend on investment coalescing behind standardized designs for biofoundries. Lead times are long, so corporate customers and governments are key players in these early stages of kicking investment and construction into gear.

Our estimates show that serving a $200 billion market requires a 20-fold expansion of current production capacity (Figure 8). By 2040, the world will need 6,000 new fermentors spread across 1,000 biofoundries that have 2.4 billion liters of total capacity (see “Fermentation Economics”). Supplying the primary feedstock, sugar, would take 65,000 square kilometers (40,000 square miles) or roughly equivalent to the land mass of Bavaria or West Virginia.

Although this is a massive challenge, it is not out of reach. Bioethanol, which represents 10% to 15% of US gasoline consumption, has almost reached price parity with fossil fuels in a single decade (thanks in part governments mandates) and has built the infrastructure to sustain a $100 billion market. Although bioethanol facilities are simpler and cheaper to construct, they are close enough to precision fermentation facilities to demonstrate feasibility (see “The Corn Ethanol Growth Wave”). The eventual phase-out of gasoline cars also will free up a large quantity of corn and sugar for precision fermentation.

The shift to large-scale, standardized biomanufacturing sites represents an enormous opportunity for infrastructure investment (Figure 9). Some pilot facilities and a few commercial-scale facilities now exist, but standardizing the asset class in line with offtake demand will unlock capital from later-stage investors. There is already an infrastructure construction opportunity stemming from higher demand than supply (see “An Emerging Infrastructure Asset Class”).

Fermentation Economics

Both the standardization of biomanufacturing facilities and the development of new strains that make further innovation possible will reduce the costs of production for the bioeconomy. As the cost of production for an individual product falls, demand for it will increase.

Realizing economies of scale is a matter not just of the facility’s total capacity but also of the size of its fermentors.

For example, a 2.4 million liter facility that operates six 400,000 L fermentors has lower capex and opex than a facility that runs sixteen 150,000 L fermentors. Furthermore, the facility with the sixteen 150,000 L fermentors will have lower capex and opex per liter of capacity than a 600,000 L facility with only four 150,000 L fermentors.

There are other variables to consider as well. In biofoundries, costs fall as tank size increases—up to a point of diminishing returns. Facilities incur baseline production costs no matter how large the fermentation tank is: baseline quantities of energy and materials are needed to sterilize the tank, formulate and sterilize the medium, and maintain cooling water. There are tradeoffs with larger fermentor sizes. Tanks larger than 150,000 L require fabrication in the field rather than in the shop, which means less quality control. Larger fermentors have a higher volume-to-surface-area ratio, making heat and mass transfer design more challenging. And with larger fermentors, each batch is very expensive. Currently, a single 400,000 L fermentation batch requires about $100,000 in raw materials alone—so a single failure is costly. Startup costs are high, too, as companies must spend several million dollars before a facility can generate revenue.

Companies must take all of these factors and others—including the robustness of the microbe strain, the product demand (for the current tenant as well as for potential future facility users), product pricing (margin), and available financing—into account when selecting the size of the facility and of the fermentors. For this reason, we are likely to see a mix of size and makeup, which will increase the importance of standardizing plant design and features to limit construction and operating costs.

Ethanol, which in the United States is made primarily from corn and blended up to 10% with gasoline, has been used as a gasoline blend-in ingredient or alternative since the earliest days of the automotive industry. Henry Ford designed the 1908 Model T to run on ethanol as well as gas. Demand for ethanol in the United States took off in the 1990s, spurred by government policy and regulation in the form of the Clean Air Act of 1992, and sustained later by the Energy Policy Act of 2005 and the Energy Independence and Security Act of 2007. In just six years, demand more than tripled—from 4 billion gallons in 2005 to 13 billion gallons in 2010. In 2021, US production of ethanol neared 21 billion gallons.

Currently, some 200 ethanol plants operate in the United States. The engineering firm ICM designed about 100 of them, the construction company Fagen Inc. built about 75, and POET about 34. By standardizing facility designs, including offering two size options (50 million gallons per year and 100 million gallons per year), these companies lowered the cost of the facilities and shortened their construction times. At the peak of construction demand, the companies were building more than 30 plants a year in the United States. Early facilities (built in the early 2000s) were much smaller, but the average size increased over time, from about 35 million gallons per year in 1999 to about 75 million gallons per year in 2011. During the same period, capital costs dropped by 30%, from $2.07 per annual gallon to $1.25 to $1.50 per annual gallon.

An Emerging Infrastructure Asset Class

The ability to produce bioproducts at projected demand levels depends on constructing sufficient new purpose-built capacity, which in turn requires substantial capital investment. Large, nonpharmaceutical-grade facilities permit economies of scale that make microbial fermentation and biomanufacturing competitive with many legacy production methods. Companies can build facilities today to produce the strains of tomorrow, and standardization and replicable designs can reduce capex and construction timelines.

Biomanufacturing is an emerging asset class that will provide critical infrastructure for the overall energy transition.

As a standalone asset class, it will rely on project finance to build assets. This will separate the credit quality of a durable asset from the credit quality of its sponsor and will facilitate involvement by investors who accept lower returns as the price for removal of the risk associated with the company itself. These investors give up potential business upside in return for downside protection in the form of contracted revenues and low customer churn that the facility provides.

A high-level snapshot of a well-structured investment from an infrastructure investor at present might look like this: with capex of $350 million and a long-term tenant product margin of more than 10%, a project finance equity investor can expect to see an internal rate of return in excess of 20% and to achieve breakeven after four to five years of facility operation.

Capitalizing on advances in biomanufacturing and a focus on nonpharma bioproducts, synonym has designed a highly standardized facility for which 80% to 90% of the capex goes to facility elements that are applicable across many precision-fermented products. Only 10% to 20% is for molecule-specific equipment. As a result, investors and funds that specialize in infrastructure investments can approach biofoundries as a single asset class in which each project has similar specifications and requirements:

Given that we are still in the early days of the industry, the biomanufacturing asset class presents a near-term opportunity for investors to capture higher returns. Over time, as facilities become cheaper to finance and build, risk will recede and returns will fall accordingly. One key risk in securing financing today is product offtake: we can project large and diverse demand, but long-term contracts are not yet common.

As more biofoundries are built and more long-term contracts with customers are executed, the asset class will become commoditized, depressing yields. Standardization and replicable design will progressively reduce capex by about 30% and construction timelines to two to three years for subsequent facilities. Other once-new infrastructure asset classes—such as solar, cell towers, and data centers—evidenced this pattern as they proceeded down the risk-return spectrum.

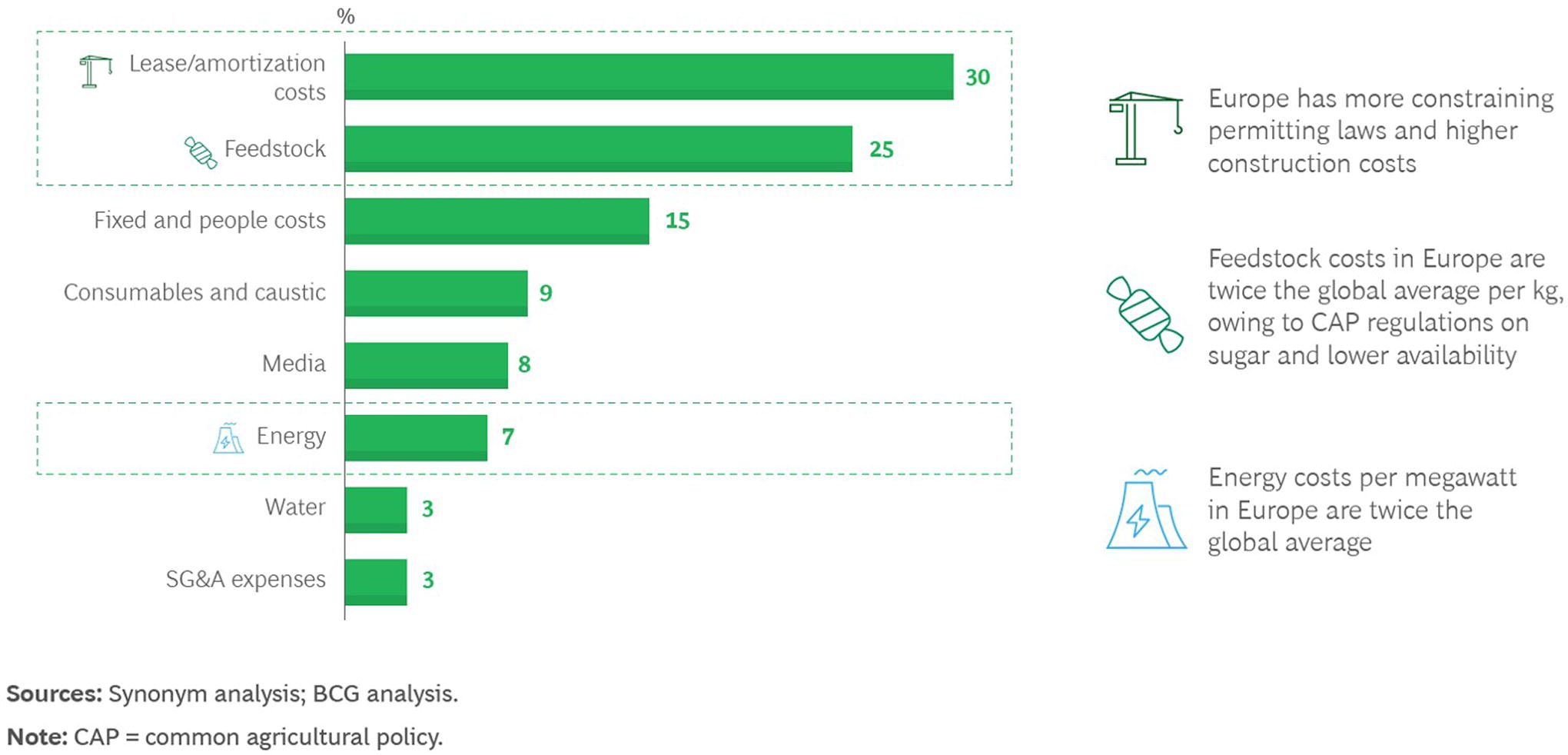

In some respects, Europe is currently better positioned than other regions for this kind of infrastructure scale-up. Europe has approximately twice the precision fermentation capacity of the United States, for example. On the other hand, several roadblocks could limit future development (Figure 10). On paper at least, the United States enjoys a number of advantages that make it attractive: plentiful feedstock in the form of corn, cheap energy (relative to much of the world), and a pool of some of the largest potential offtake buyers. Investment has been slow, but we expect this to change as US companies realize that bioproducts represent their most expeditious path to meeting their climate commitments.

Improvements in Strain Engineering and Other Technologies

To reach their full potential, biofoundries need to work with new strains engineered with large-scale manufacturing and other technologies in mind to sustain the scale curve.

Strain engineering has been well financed to date, and its track record of advances in terms of new molecules has been impressive. Recent technological breakthroughs have improved facilities’ ability to manipulate biological systems at scale. These include: DNA synthesis Development of new genetic engineering tools Adaptive laboratory evolution Development and analysis of data from various “-omics” technologies (genomics, transcriptomics, metagenomics, proteomics, and metabolomics) High-throughput enzyme screening Protein design Use of industrial or wild strains in place of conventional strains (with scale in mind)

Companies can now combine these technologies with data-driven and AI methodologies to discern which strains, metabolic pathways, and enzymes are most likely to excel in large-scale manufacturing conditions—a capability that could reduce cost and time-to-market.

Moreover, these technologies can use mastered metabolic pathways to reduce R&D effort (time and money) for other molecules of the same family. For instance, Amyris has achieved scientific success in improving a strain to produce a molecule from the terpenoid class of organic chemical compounds (which are used to prevent and treat multiple diseases, including malaria and cancer). Because it builds on previous work, the improved strain requires much less R&D time and money to optimize, potentially for production of up to 80,000 known terpenoids. Other synthetic biology companies are adopting this approach as well, using previous work for one molecule to accelerate the development of molecules of the same family. This strategy could quickly unlock numerous other molecules at industrial scale in the coming years.

Efforts of this kind can yield multiple benefits: high-performance strains that maximize production rates, robust strains that minimize failed batches, and selective strains that reduce DSP complexity, all of which can significantly reduce the overall cost of production.

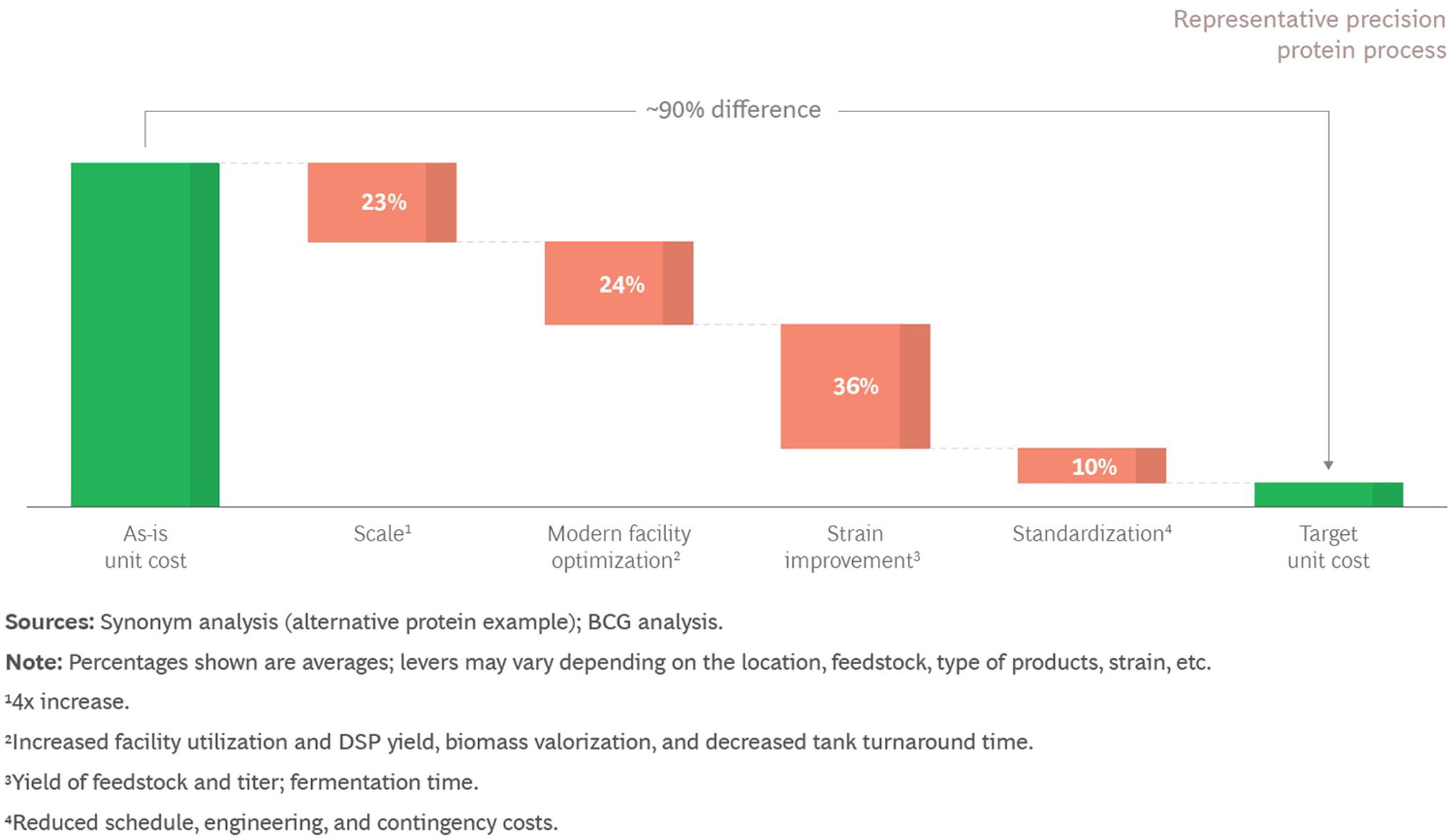

Improvement should be continuous: customers of early biofoundries will reap the benefits of subsequent developments that emerge from the same facilities. We estimate that producing strains optimized for large-scale manufacturing in optimized large-scale biofoundries can bring costs down by 90% (Figure 11).

In addition to being suitable for genetically modified strains, versatile biomanufacturing facilities will accommodate newly discovered wild-type (or natural) strains or microbial communities with new properties, thanks to the latest-omics technologies.

Other fundamental feedstock developments can reduce manufacturing costs, too. Sugar, known in the industry as a Gen 1 feedstock, is the primary precision fermentation feedstock today. Two future generations of feedstocks are expected to reduce costs and facilitate increasing scale, although they may take at least a decade to mature. Gen 2 feedstocks consist of nonedible materials such as wood and recycled biowaste. Gen 3 feedstocks use CO2 and photosynthesis, and they require far less land for the initial production stage. Using these upcycled waste streams—such as food waste, gas fermentation (CO2 or CH4), cellulosic materials, and glycerol (waste steam from biodiesel)—as carbon sources has the potential to reduce production costs and shrink the facility’s carbon footprint.

Another anticipated technological advance, continuous fermentation, can significantly increase biomanufacturing production rates. The process entails spending less time growing the cells and cleaning and sterilizing the fermentors, so the same infrastructure can produce more product. However, continuous fermentation is not yet viable at commercial scale other than for biofuels. Major challenges include reducing contamination and constraining genetic drift. Advancing on both of these fronts will require developing or optimizing strains adapted for new bioprocesses, building new continuous fermentor systems with adapted upstream equipment, and installing larger DSP equipment that can handle higher volumes of material.

One additional promising technology on the horizon is cell-free production, which uses enzymes from precision fermentation to perform biocatalysis or green chemistry. This technology is complementary to precision fermentation; in combination, they can unlock lower production costs.

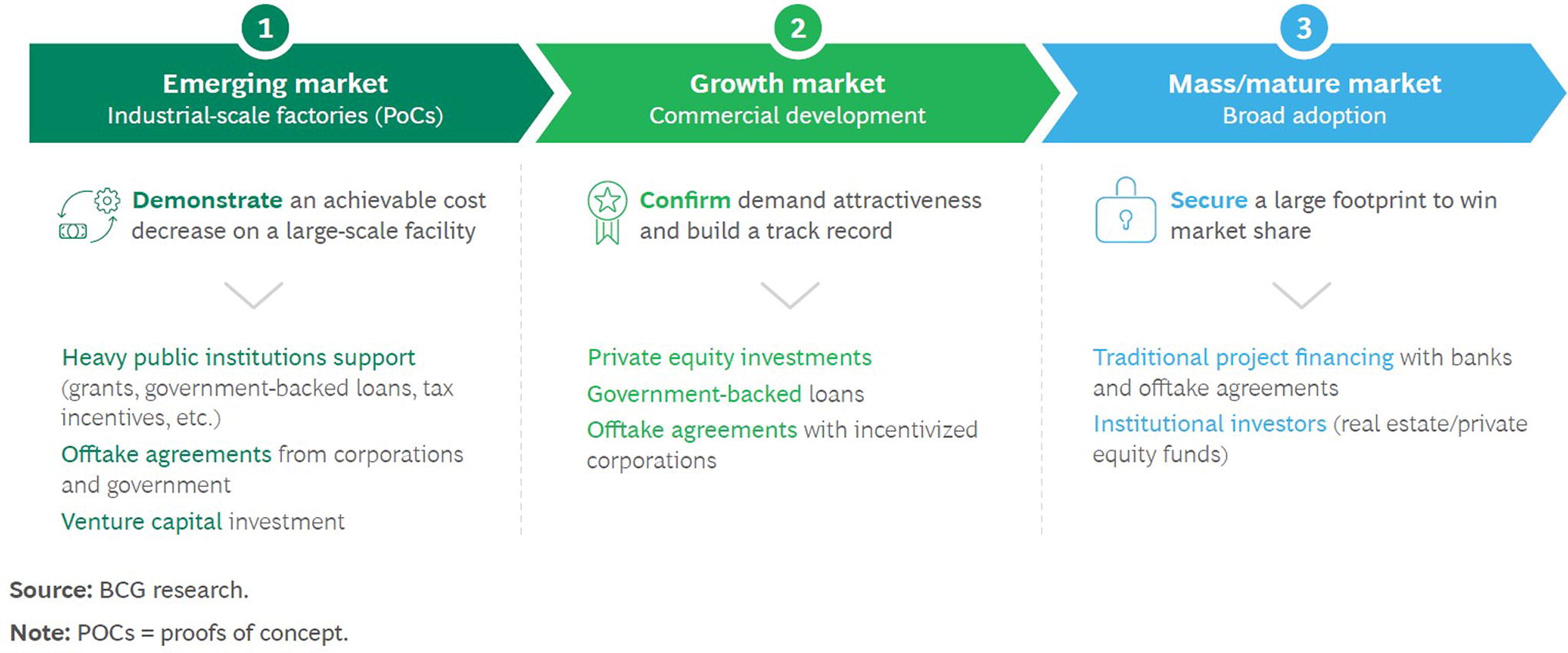

Corporations and Governments Must Step Up

In large capital-intensive projects, demand typically anticipates supply through contracted offtake agreements. These agreements, which are common practice in chemicals and specialty chemicals, are likely a prerequisite for investors to finance facilities and production line setups.

We expect the bioproducts market to develop in three phases, and we see support from corporate–customer and governments are critical for the first two (Figure 12). The phases are as follows:

Precision fermentation has demonstrated its potential time and again. The key question now is whether biomanufacturing can overcome the cost-scale conundrum and support a broad-based shift to more sustainable alternative processes to unlock new products and markets.

With proven technology and a vast range of potential bioproduct applications, biomanufacturing is at a commercialization tipping point. Infrastructure can be built today for the strains of tomorrow. Large companies looking to meet their sustainability goals should act now to transform their supply chains by committing to purchase from biomanufacturing companies. Far-sighted investors with a focus on infrastructure should evaluate the emerging asset class and be ready to commit capital to attractive projects.

Synonym

Synonym enables the commercialization and manufacture of bioproducts, accelerating the world’s transition to better, more sustainable materials. We believe that bioproducts—created using biology—represent a key part of our future industrial base and will transform crucial elements of supply chains across multiple sectors while helping to catalyze a decarbonized future. Synonym works with companies building these next-generation bioproducts to expand and scale seamlessly becoming their strategic biomanufacturing partner. We have also launched two, free online tools to help companies on their paths toward commercialization: Capacitor, the world’s most comprehensive directory of available biomanufacturing infrastructure Scaler, a techno-economic analysis (TEA) and life-cycle assessment (LCA) calculator that generates insights designed to help companies optimize their paths to market.

Learn more about us at www.synonym.bio or follow us on LinkedIn for the latest on the biomanufacturing revolution.

Boston Consulting Group

Boston Consulting Group partners with leaders in business and society to tackle their most important challenges and capture their greatest opportunities. BCG was the pioneer in business strategy when it was founded in 1963. Today, we work closely with clients to embrace a transformational approach aimed at benefiting all stakeholders—empowering organizations to grow, build sustainable competitive advantage, and drive positive societal impact.

Our diverse, global teams bring deep industry and functional expertise and a range of perspectives that question the status quo and spark change. BCG delivers solutions through leading-edge management consulting, technology and design, and corporate and digital ventures. We work in a uniquely collaborative model across the firm and throughout all levels of the client organization, fueled by the goal of helping our clients thrive and enabling them to make the world a better place.

For Further Contact

If you would like to discuss this report, please contact the authors.

The three keys to achieving biomanufacturing’s potential.

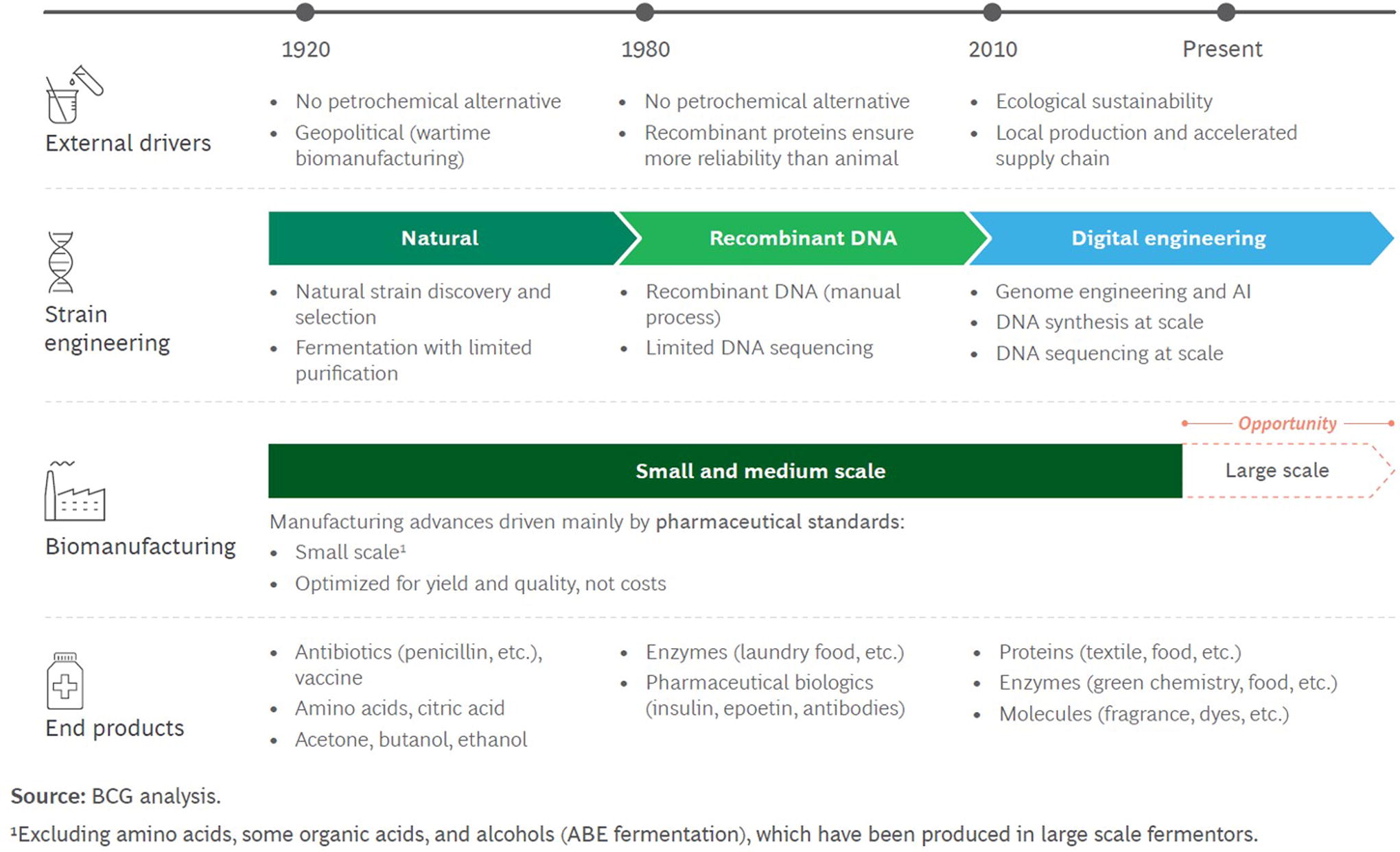

Unlike strain engineering, biomanufacturing has improved only incrementally in the past century.

Optimized biofoundries with a minimum working capacity of 2 million liters can cut costs by about 50%.

Facility optimization can drastically reduce biomanufacturing costs.

Reducing costs can unlock $200 billion in demand.

Potential biomanufacturing development toward 2040.

Biofoundries reduce greenhouse gas emissions in the production of most molecules.

A $200 billion market requires a 20-fold expansion of current capacity.

Biomanufacturing facilities can be a new asset class.

Feedstock, energy, and leasing costs jeopardize Europe’s ability to compete.

Combining strains engineered for scale with biofoundry manufacturing could reduce costs by 90%.

The three phases of market development.

Footnotes

Acknowledgments

The authors thank Nicolas Goeldel and Max Richly of BCG, Joshua Lachter of Synonym, and Per Falholt of 21st.BIO for their contributions to this article.