Abstract

Abstract

Background:

Terminal intensive care unit (ICU) stays represent an important target to increase value of care.

Objective:

To characterize patterns of daily costs of ICU care at the end of life and, based on these patterns, examine the role for palliative care interventions in enhancing value.

Design:

Secondary analysis of an intervention study to improve quality of care for critically ill patients.

Setting/Patients:

572 patients who died in the ICU between 2003 and 2005 at a Level-1 trauma center.

Methods:

Data were linked with hospital financial records. Costs were categorized into direct fixed, direct variable, and indirect costs. Patterns of daily costs were explored using generalized estimating equations stratified by length of stay, cause of death, ICU type, and insurance status. Estimates from the literature of effects of palliative care interventions on ICU utilization were used to simulate potential cost savings under different time horizons and reimbursement models.

Main Results:

Mean cost for a terminal ICU stay was 39.3K ± 45.1K. Direct fixed costs represented 45% of total hospital costs, direct variable costs 20%, and indirect costs 34%. Day of admission was most expensive (mean 9.6K ± 7.6K); average cost for subsequent days was 4.8K ± 3.4K and stable over time and patient characteristics.

Conclusions:

Terminal ICU stays display consistent cost patterns across patient characteristics. Savings can be realized with interventions that align care with patient preferences, helping to prevent unwanted ICU utilization at end of life. Cost modeling suggests that implications vary depending on time horizon and reimbursement models.

Introduction

I

However, the potential ICU cost savings associated with improving palliative care and the incentive to realize these savings may vary depending on the perspective (hospital, payer, society), the reimbursement models (fee-for-service, bundled payment, value-based purchasing, capitated system), and the time horizon (short term with a range from days to months vs. long-term range of years). As our reimbursement models incorporate more value-based purchasing, capitated payment systems, and population-based payment models, and less volume-based fee-for-service, the implications of efforts to reduce costs of end-of-life care in the ICU may shift.

Interventions such as ACP and palliative care consultation that seek to improve decision-making among clinicians, patients, and families may have different economic implications for terminal ICU stays in different reimbursement models. Modeling potential cost savings from these types of interventions requires an understanding of the patterns and distribution of costs for patients who die in the ICU. For example, shortening length of stay (LOS) is often advocated as a target for cost-saving interventions. However, whether or not significant cost savings can be achieved by shortening LOS in the ICU has been debated.6–9 The impact of reducing ICU LOS will vary depending on the proportion of costs that are fixed and the reimbursement model.

The objective of this study was to describe the patterns and breakdown of daily ICU costs in a cohort of patients who died in the ICU to better understand expenditures related to terminal ICU stays and the potential influence of palliative care services or ACP. We describe the variation in total daily costs by ICU day and report the proportion of total costs that were direct variable, direct fixed, and indirect costs. Direct variable costs include supply and drug costs and are responsive to patient characteristics and volume. Direct fixed costs, such as labor (nursing, medical assistants, etc.), are fixed in the short term. Indirect costs are not directly linked to patient care (i.e., information technology and environmental services).

We further explore the pattern of costs by LOS, cause of death, clinical service, type of ICU, and insurance status. In particular, we test two hypotheses for each of these groups: (1) on average, costs are greater the first ICU day than the second day; and (2) on average, costs are stable after the second day. In addition, we examine whether the patterns of costs are similar across different diseases, different types of ICUs, and across different physician disciplines. We demonstrate how these results can be used to simulate what cost savings could look like on both short and long time horizons if interventions that reduce or shorten unwanted ICU utilization were implemented. Our goal is to provide insights for clinicians, healthcare systems, and policy makers on the implications of cost savings regarding end-of-life care in the ICU.

Methods

Design overview

Data were collected as part of an interdisciplinary multifaceted intervention to improve the quality of end-of-life care for critically ill patients and their families.10–12 Eligible patients were adults who had died in an ICU between 2003 and 2005 after a minimum stay of 6 hours. The study setting was a university-affiliated 413-bed Level-1 trauma center. There were 88 ICU beds distributed among five ICUs (medical/cardiac, trauma/surgical, neurology/neurosurgical, burn, and pediatric). The institutional review board approved this study (UW HSC#23503).

Data collection

Trained chart abstractors using a standardized chart abstraction protocol reviewed eligible patients' medical records to obtain demographic (age, gender, type of insurance) and clinical information (diagnoses, ICU, and hospital LOS, code status, life-sustaining treatments). Patient race, education, and cause of death were determined from death certificates. Abstracted data were linked to hospital financial records to obtain detailed cost information.

Predictors/strata

The pattern of costs was stratified by cause of death, clinical service, type of ICU, and insurance status. Cause of death was divided into trauma, cancer, cardiac, respiratory, neurological, and other. Clinical service was grouped into general surgery, medicine, neurology, neurosurgery, and other. Type of ICU included neurology, medicine, pediatric, coronary, burn, trauma, and surgical. Insurance was grouped into private, Medicare, other government funded, and other/none/unknown.

Outcomes

Costs were used instead of charges since charges bear little resemblance to economic cost, and use of charges as a proxy for economic cost may lead to unwarranted conclusions about economic efficiency. 13 These costs were abstracted by hospital financial analysts directly from patient accounts and represent the total costs for all services provided on each hospital day, including overhead costs, labor costs, and supply costs. In the accounting system, cost components are grouped into 3 categories: direct variable, direct fixed, and indirect. These categories allowed us to capture which costs could change in the short term or the long term. Direct costs represent costs that are traceable to a specific cost center providing direct patient care, such as pharmacy, radiology, respiratory care, laboratory, and microbiology. Direct variable costs include supply and drug costs and are the most responsive to individual patient characteristics such as severity of illness and reason for admission. Direct fixed costs include labor, clinical department administration, and overhead fees. These types of costs are fixed in the short term, but responsive to patient volume in the long term. For example, wages and contracts are set for the year, but if bed occupancy decreases over time, new contracts with fewer staff or hours could be written. Indirect costs, which are included in the patient bill, represent services provided by cost centers not directly linked to patient care, such as information technology and environmental services. These types of costs are the least amenable to change based on patient characteristics or bed occupancy.

This institution uses the McKesson Explorer platform for hospital accounting; physician fees are generated from a separate organization and were not included in this analysis because they were not available at the ICU-day level. All costs were adjusted for inflation and compared at the 2013 US dollar value.

Statistical analysis

Patterns of ICU costs

To describe the patterns of total cost over an ICU stay, we examined the average total cost and breakdown by day of stay. The daily pattern and breakdown of costs were then stratified by LOS, cause of death, clinical service, type of ICU, and insurance status. We used generalized estimating equations with independent working correlation matrices to test whether costs were higher on day 1 than day 2 and whether costs were stable thereafter. 14 The first question was addressed by comparing the ratio of average ICU costs between days 1 and 2. The second question was addressed using an equivalence test of the linear trend in average costs after day 2. This test examines the strength of evidence that average ICU costs do not change by more than 25% per week after day 2. This cutoff was chosen to reflect an approximate change in daily costs of about $400 a week; any change in daily costs above this was considered clinically meaningful. We performed this test separately in various patient groups defined by covariate levels to see if the trend was constant across patient groups. Details on the regression model and testing procedures are in Appendix A. All analyses were conducted using R3.1.0 (https://cran.r-project.org/).

Potential cost savings

To estimate cost savings that might be associated with the use of ACP and palliative care consultation, we conducted simulations using the patterns and distribution of costs identified in this sample and current estimates of reductions in ICU utilization associated with ACP (37% fewer ICU admissions) and palliative care consultation (26% shorter LOS).15,16 We estimate savings based on short and long time horizons.

Results

Five hundred and seventy-two patients were included in our sample. The average age was 61 ± 18 years. About 90% of patients were intubated in the last week of life, with 19% dying without any withdrawal of life support. The median ICU LOS was 3 days (interquartile range [IQR]: 1–8). Additional patient characteristics are displayed in Table 1.

Data presented as mean ± SD or n (%), unless otherwise indicated.

Determined by first ICD-9 code listed; this reflects most reimbursable, not necessarily primary, diagnosis.

As reported on death certificate using ICD-10 coding.

Proportion of patients with medical record documentation of a living will (n = 307).

Patients who died after implementation of the intervention to improve palliative care in the ICU (10–12).

BiPAP, bilevel positive airway pressure; ICU, intensive care unit; IQR, interquartile range.

Patterns of cost distributions

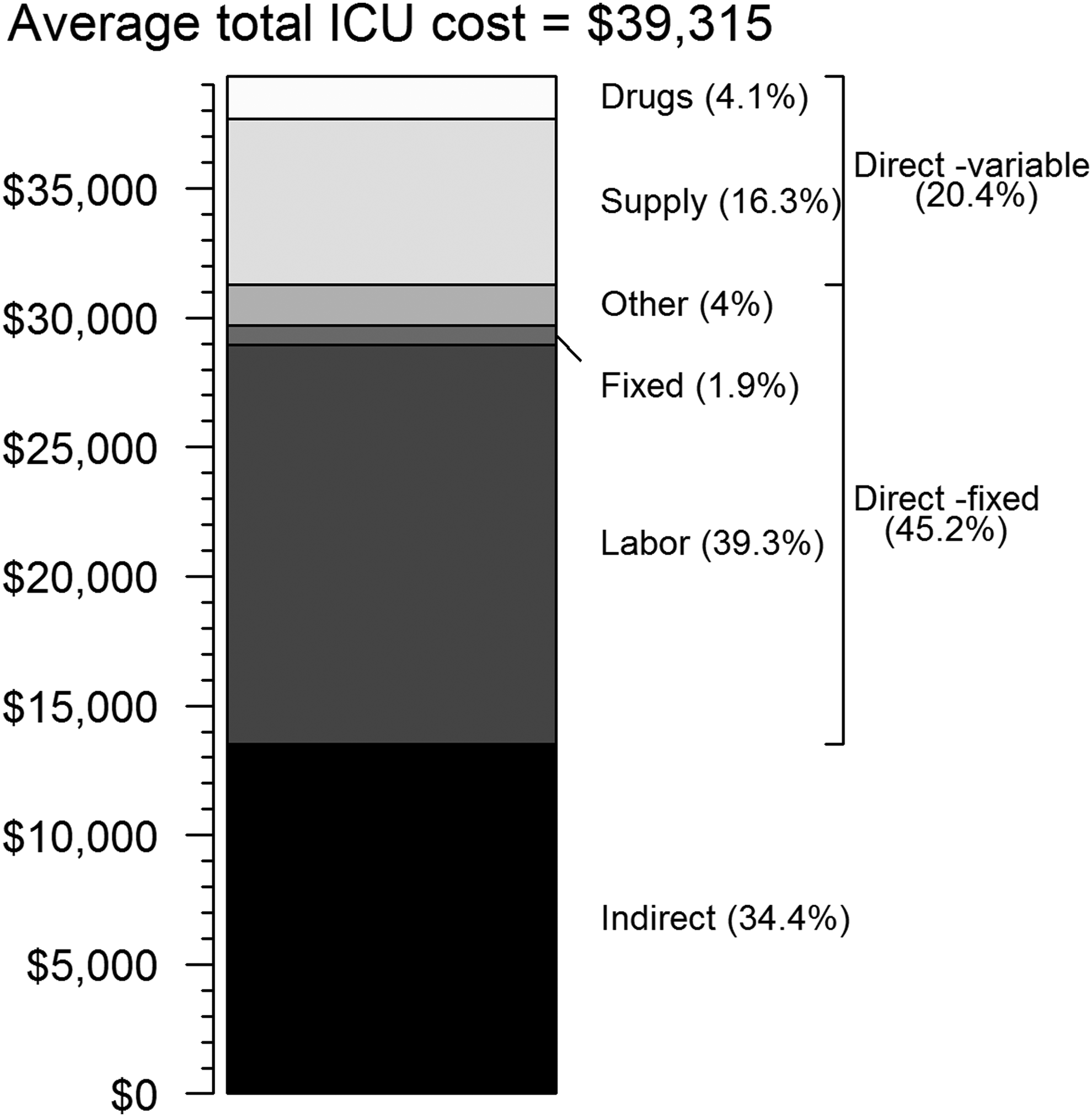

The average total ICU cost per patient was 39.3K ± 45.1K (median 24.1K; IQR 10.4–51.9). Direct fixed costs represented 45% of total hospital costs; direct variable costs were 20%; and indirect costs were 34% of hospital costs. The detailed breakdown of subcategories is displayed in Figure 1. Patients with an ICU LOS of only one day had a higher percentage of supply costs (23.2%) and lower percentage of labor costs (33.3%) than patients with longer ICU stays (15.7% and 39.8% for supply and labor, respectively). High total ICU costs were associated with a higher percentage of costs represented by supplies (correlation = 0.09, p = 0.02) with 17.3% in the upper tertile of total ICU costs compared with 11.8% in the lower tertile.

Average total ICU cost broken down by categories of costs (n = 572). Under direct fixed costs, fixed represents clinical department administrative fees and other represents other overhead fees. ICU, intensive care unit.

Over the length of the ICU stay, the proportion of total costs that were represented by labor increased slightly from 35% to 43% by week 2 and were offset by a decrease in proportion of costs attributable to supplies from 21% to 12%. The remaining categories stayed relatively constant.

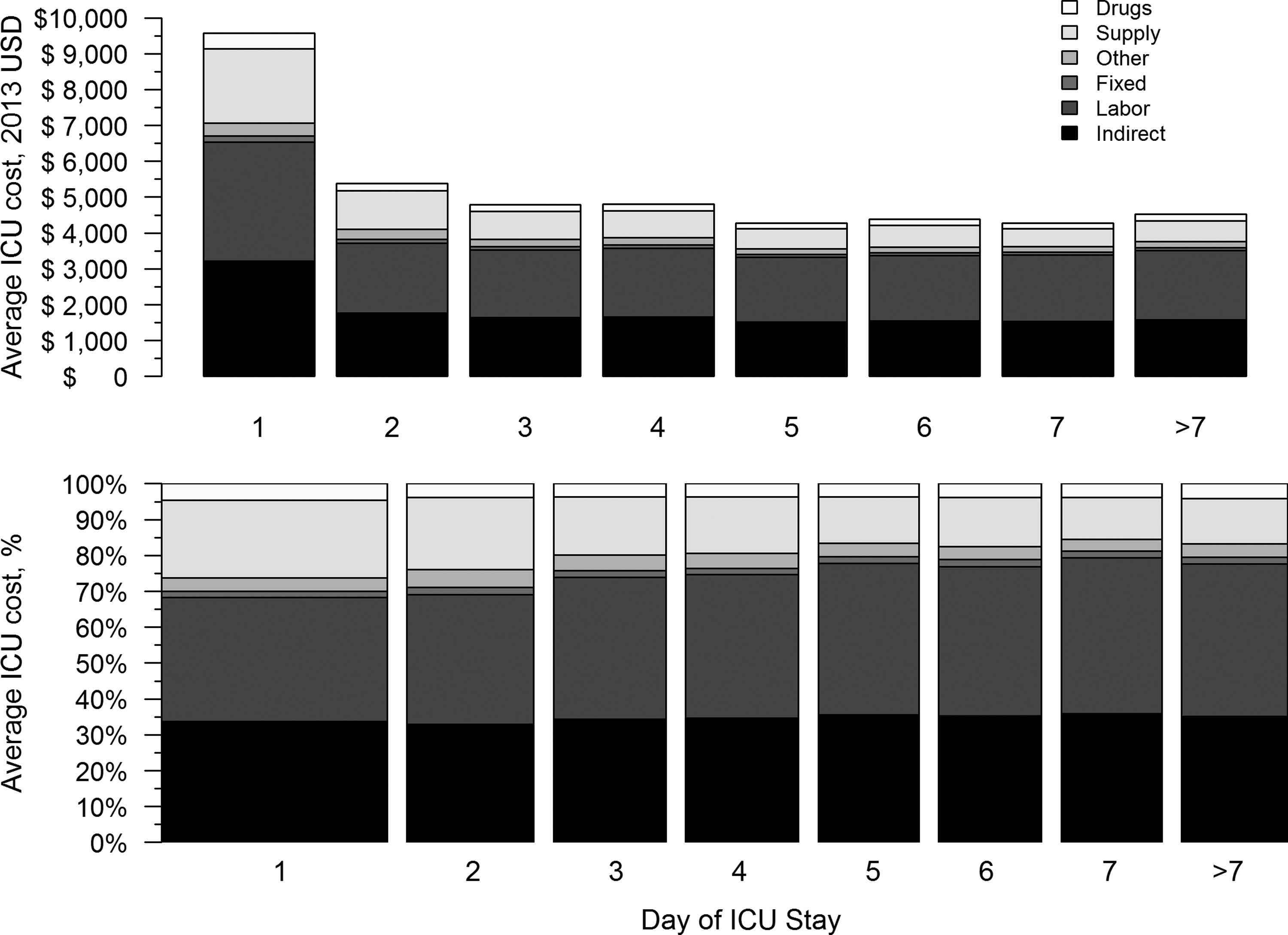

The average cost of an ICU day over the entire LOS was 7.7K ± 6.1K (median 6.1K; IQR 4.9–8.4). Day of admission was the most expensive (mean 9.6K ± 7.6K; median 6.9K [IQR 5.2–11.0]). The average cost per day after admission was 4.8K ± 3.4K (median 4.3K; IQR 3.5–5.5) (Table 2). Mean daily costs beginning with day of admission, broken down by category of cost, are displayed in Figure 2. The day before death was similar in expense to all other days, excluding admission day.

Upper panel: ICU costs broken down by day of stay; Lower panel: Spine plot by day of stay, indicating relative fraction of cost categories (n = 572).

Data presented as mean ± SD, unless otherwise indicated.

Adjusted for inflation and reported in 2013 U.S. dollars.

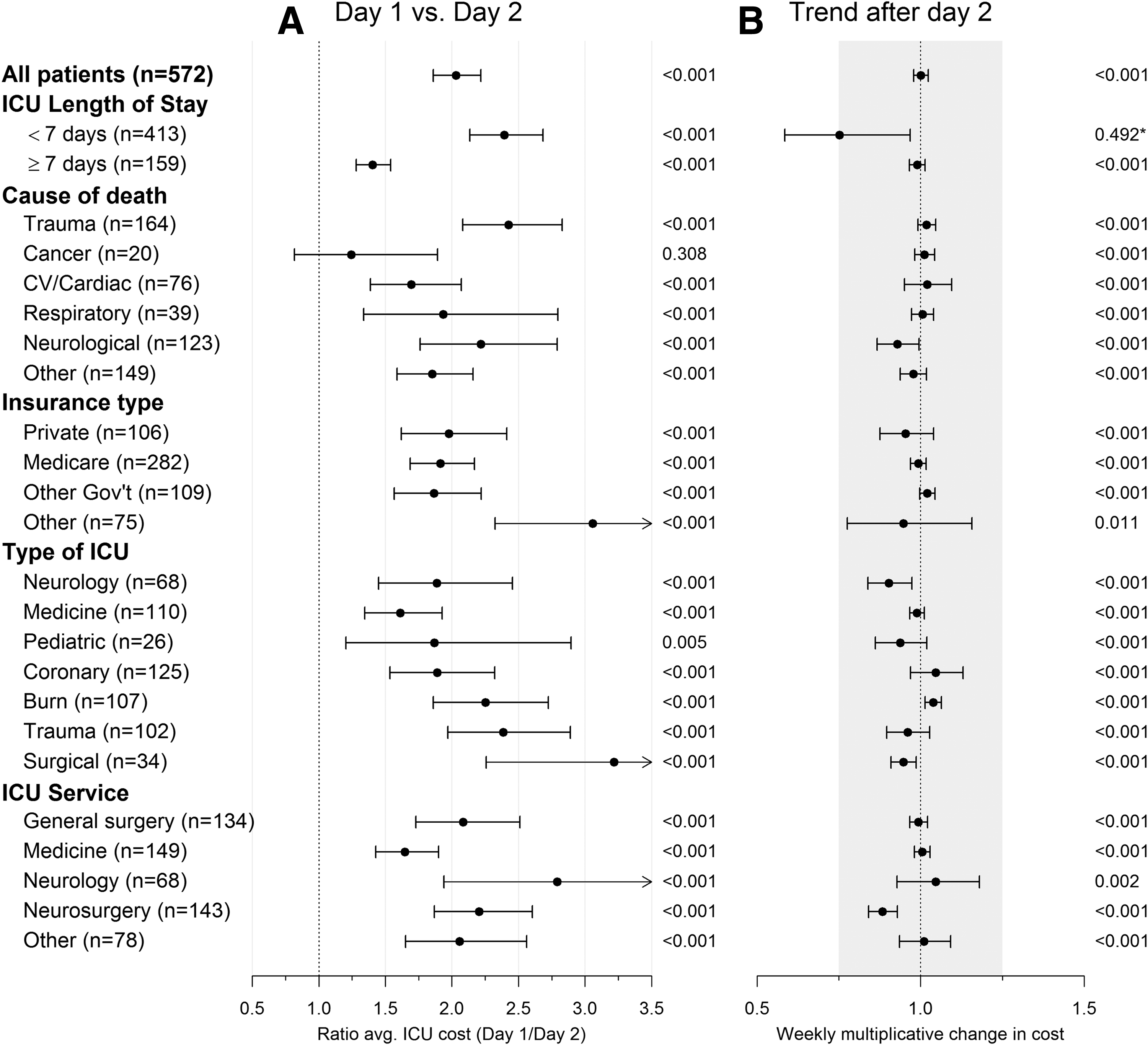

This pattern of admission day being the most expensive and subsequent days having stable costs was consistent across patients and differed by clinical service, type of ICU, and insurance status (Fig. 3). This pattern was consistent across causes of death. It was also consistent across ICU LOS, provided LOS was ≥7 days. For patients with LOS <7 days, admission day was still the most expensive; however, there was a slight trend of decreasing costs from days 2 through 7.

Results of regression analyses stratified by length of stay, underlying cause of death, insurance type, type of ICU, and clinical service.

Projecting cost reductions with palliative care interventions

To illustrate the potential cost savings of these interventions, we applied estimates of ACP and palliative care intervention effects to the costs described above for a representative patient in our cohort who died from complications of chronic obstructive pulmonary disease (COPD) who would have preferred to die at home. Preventing the 6.5-day ICU admission with ACP would immediately save the hospital $6,200 in direct variable costs. Over time, if ICU bed occupancy decreased as a result of ACP and the alignment of patient preferences at the end of life with care received, the direct fixed costs could also be saved, adding on average, an additional $18,400 in savings to the hospital per patient (Table 3).

Direct variable costs include supply and drug costs. Direct fixed costs include labor, administrative, and overhead fees. Indirect costs represent services provided by cost centers not directly linked to patient care, such as information technology, environmental services, and hospital administration.

Based on mean LOS for patients in our cohort whose death was attributed to respiratory causes on death certificate and estimates of effect of advance care planning and palliative care interventions according to current literature. 26

These costs reflect the costs of the last 1.7 days of the ICU stay, taking into account the variation of cost by day of stay. These costs, however, do not reflect the marginal difference between the last days in the ICU and the acute care floor as all patients in this cohort died in the ICU.

LOS, length of stay.

If this representative patient was admitted to the ICU and received ICU-based palliative care intervention of average effectiveness, the LOS could be reduced by an estimated 26%, or 1.7 days. In the short term, this would have led to $1,300 per patient in immediate direct variable cost savings for the hospital. If the palliative care intervention was widespread, in the long term, ceteris paribus, as bed occupancy rates decline, another $2,800 per patient in direct fixed costs may be saved (Table 3). It is important to note that these figures are ICU costs avoided and do not take into account the costs incurred through the alternative care received, whether at home or in the hospital. Thus, these figures represent the upper bound of potential cost saving.

The degree of savings is thus determined by the time horizon—short versus long term. The incentive, however, for hospitals to realize these savings varies depending on the reimbursement model with increasing incentive as we move from fee-for-service toward capitated payment models.

Discussion

Our findings demonstrated that (1) the first ICU day was the most expensive with the days in between admission and death having relatively stable costs; (2) this pattern was consistent across patients regardless of clinical service, insurance status, type of ICU, or cause of death; (3) direct variable costs accounted for ∼20% of ICU costs; this percentage decreased over time; (4) direct fixed and indirect costs constituted ∼45% and 35% of ICU costs, respectively, these percentages increased slightly over time; and (5) high total ICU costs were associated with a higher percentage of direct variable costs (represented primarily by supplies). To our knowledge, this is the first study evaluating the pattern and breakdown of ICU costs by day of stay for patients who died in the ICU, and our findings demonstrate the stability of the pattern across a diverse group of decedents.

Our finding that the first ICU day is the most expensive is consistent with most previous studies.6,17,18 The stability of costs in days between admission and death/discharge is similar to that observed in patients receiving mechanical ventilation in the ICU for >48 hours who survived to ICU discharge. 6 Our study demonstrated that this pattern was consistent and applicable to a broad group of ICU decedents, across different ICUs and different clinical services. By contrast, a recent study did not see higher day 1 costs in patients admitted to medical/nonsurgical ICUs. 19 This difference in findings may be due to severity of illness; ICU mortality was not reported in this study, making it difficult to determine if our cohorts are comparable.

One important implication of the stability of these cost patterns is that the aging population (and accompanying increase in Medicare coverage), and the concomitant increases in chronic comorbidities, will increase ICU costs, but they are unlikely to change the pattern of ICU costs. Instead, policy makers will have to turn to interventions such as ACP and palliative care, which focus on preventing unwanted or nonbeneficial ICU admissions and reducing ICU LOS by matching medical care to individual patient preferences.

Our finding that direct fixed and indirect costs represent the majority of total hospital costs is consistent with previous studies.6,9,20 Our study found that the proportion of ICU costs attributable to labor increased over the ICU stay and that costs attributable to supplies decreased over time. From the hospital's perspective, over a short time horizon, direct fixed and indirect costs are incurred regardless of LOS. However, over a longer time horizon, fixed costs can become variable. 7 Reducing ICU bed days over time may allow fixed expenses attributable to the ICU to be reduced or, alternatively, allow a reduction in the growth rate for ICU bed days. 7 For example, in our study, labor costs represented nearly 40% of total ICU costs and nearly the entire portion of direct fixed costs. Assuming that ICUs do not change ICU admission practices, 21 a reduction in inappropriate or unwanted ICU utilization may prompt reductions in ICU staffing and labor costs.

Our results demonstrate that reducing LOS by preventing an ICU admission versus shortening LOS by reducing days at the end of a stay has very different cost implications. Preventing the ICU admission all together will lead to significantly greater savings; however, our finding that high total ICU costs were associated with a higher percentage of costs represented by supplies suggests that longer stay patients may be an important focus for interventions to improve quality and reduce costs.

Furthermore, the degree of hospital cost savings is largely determined by the time horizon. In the short term, decreases in ICU use are associated with savings in direct variable costs, while in the long term, both direct variable and direct fixed costs are potentially saved. Recent moves away from fee-for-service toward more capitated payment models increase the incentive for hospitals to realize these cost savings and may represent an important opportunity for palliative care.

Under volume-based fee-for-service, in which more ICU stays are profitable (reimbursement > cost), few financial incentives exist from the hospital administrators' perspective to support interventions that reduce ICU admissions and LOS, especially in the short term when the majority of costs are fixed. However, our changing reimbursement systems provide a greater sense of urgency to reduce unwanted ICU utilization. Under bundled payment or episode-based payment systems, hospitals and physicians are reimbursed from the same pool of funds based on the health condition of the patient. 22 This type of reimbursement policy provides stronger financial incentives for both administrators and physicians to decrease ICU usage since both bear some financial risk for costly episodes. However, both the size of the budget and the sharing of financial risk between physicians and hospitals will depend on contract negotiations. Under value-based performance, reimbursement is linked to improving quality and reducing costs. Thus, even in the short term when most ICU costs are fixed, but prevention of unwanted ICU stays is a quality measure, hospital administrators may be incentivized to integrate ACP and palliative care interventions to decrease ICU LOS, prevent unwanted ICU stays, and match care with patient wishes. In fact, ICU LOS has been proposed as a quality measure by the Joint Commission, strengthening the incentive for adoption within quality-based payment systems. 23 Capitated payment systems and fixed global budgets, as recently passed in Maryland, provide a fixed budget per patient regardless of care required, providing even more financial incentives for hospitals to reduce overall costs with hospitals bearing more of the financial burden for costly patients.

Several prior studies have demonstrated reductions in overall hospital costs associated with inpatient palliative care services. 24 One study also found that palliative care consultation was associated with reduced ICU costs 25 ; however, to our knowledge, no study to date has looked at the effect of palliative care and ACP on ICU costs in the short term and long term using direct variable, direct fixed, and indirect ICU costs. This study provides insight into what patterns of ICU cost look like for ICU decedents and potential savings that may be realized in the short and long term.

Our study has several limitations. First, we acknowledge that there is considerable variation in defining direct (variable and fixed) and indirect costs. In addition, this study was conducted in a single hospital and different hospitals may have a different fee structure for direct and indirect costs as well as different patterns of care. Additionally, this hospital was the site of a system-level intervention to improve palliative care in the ICU 11 and thus estimates of cost reductions may be conservative. Second, our analyses do not include physician fees as these are generated from a separate organization and are unable to be broken down by day in the ICU; thus, our cost estimates are conservative. However, this study provides insights into the costs of terminal ICU care that can help guide future studies. Third, our study describes costs for diverse patients dying in the ICU and is not focused only on patients for whom palliative care interventions are appropriate. Nonetheless, these cost findings provide guidance for assessing the economic impact of implementing palliative care interventions on ICU costs. Fourth, we recognize that these findings do not provide information for conducting analyses from the societal perspective. Furthermore, the concept of cost shifting has not been factored in and thus these figures represent the maximum potential cost saving. Finally, data from this study were collected between 2003 and 2005 and should be replicated with more recent data. We did not see changes in quality of palliative care in the ICU between 2003 and 2008, 26 but additional research should be conducted to ascertain if patterns of costs are changing.

Our findings have important implications for palliative and ICU care in the United States as we reduce volume-based fee-for-service reimbursement and shift toward accountable care organizations and value-based purchasing. Value in healthcare is key to controlling costs and improving quality. Most importantly, these estimates provide insight into the range of cost savings that may be realized with interventions such as ACP and palliative care that help to align care with outcomes desired by patients, such as dying outside of the hospital. Future research, identifying cost patterns and implications using additional institutions and more recent data, is needed to inform clinicians as well as healthcare administrators and policy makers.

All the authors attest that they do not have any potential or actual personal or financial involvement with any company or organization with financial interest in the subject matter.

Footnotes

Acknowledgments

This work was supported by the National Institute of Nursing Research (R01NR005226) and the National Institute of General Medical Sciences (5T32GM086270).

Author Disclosure Statement

No competing financial interests exist.

Appendix A

Regression models:

In each group, we used the following regression model:

To test whether costs on the first day are more expensive than the second, we test the null hypothesis

In order to determine an appropriate test for determining whether costs are stable after the second day in the ICU, first note that