Abstract

As of March 23, 2012, the Internal Revenue Service (IRS) requires tax-exempt hospitals to conduct a Community Health Needs Assessment (CHNA) every 3 years. This study assessed whether the IRS CHNA mandate incentivized North Carolina's tax-exempt hospitals to increase investments in community health programs. The authors gathered the 2012–2016 community benefit reports of 53 North Carolina private, nonprofit hospitals from the North Carolina Hospital Association. Community benefit spending data from the year of the first CHNA were compared to that 2 years later using paired t tests among matched subjects. No significant increases were found in hospitals' community health programs spending (P = 0.6920) or in providing patient care financial assistance (charity or discounted care) (P = 0.0934). In fact, aggregate community health programs spending effectively decreased by 4%, from $393.3 million to $377.5 million. Among all community benefit items, only the unreimbursed cost for treating Medicare patients increased significantly (P = 0.0297). The proportion of spending on community health programs relative to patient care financial assistance decreased significantly (P = 0.0338). Performing CHNAs did not incentivize North Carolina's tax-exempt hospitals to progressively invest in community health programs. The hospitals continue to spend heavily on patient care financial assistance and little on disease prevention and community health improvement activities. These findings suggest that tax-exempt hospitals continue to function as a safety net for the poor and the uninsured rather than as active partners in population health management initiatives. At present, performing CHNAs may be more a demonstration of compliance than a tool to improve population health.

Introduction

Nearly two thirds of hospitals in the United States are nonprofit hospitals that are exempt from paying taxes under Internal Revenue Service (IRS) Code Section 501(c)(3). 1 –8 The Congressional Joint Committee on Taxation reported that the US government gave up $12.6 billion of tax revenues in 2002, equivalent to $25 billion in 2011 dollars, by granting tax-exempt status to nonprofit hospitals. 3,9 –11 For their part, tax-exempt hospitals provide community benefit in various forms of charitable activities to legally justify their privileged tax status. 8,12 US tax-exempt hospitals provide community benefit that is approximately equivalent to 8% of their operating expenses. 9,10 However, a considerable proportion of their community benefit expenditures was in the form of patient care financial assistance (charity or discounted care), with little allocated to community health programs. 1 –3,10

Historically, tax-exempt hospitals spend approximately 85% of community benefit on patient care financial assistance, with only 5% invested in community health improvement programs. 1,10,13 The remaining 10% is spent on education, research, and contributions to community groups. 10 In North Carolina, the community benefit spending of tax-exempt hospitals follows a similar pattern. 14

The United States spent less than 4% of its total health care expenditures on prevention and public health programs even though more than 80% of its health care spending was related to preventable chronic health conditions. 15 –19 Concurrently, the US government cut the funding reserved for state and local public health programs by $580 million because of a weak economy and its plan to increase defense spending. 18 Consequently, many US communities lack financial resources to support community health programs while the nation's health care costs continue to increase. 18 In this context, tax-exempt hospitals potentially could augment the supply of much-needed disease prevention and community health improvement services if they were to shift even a tiny portion of their community benefit expenditures away from traditional patient care financial assistance and toward population health initiatives through implementation of the IRS Community Health Needs Assessment (CHNA) policy. 2,7,8,13

However, determining the extent of the shift is controversial, especially in North Carolina – a state that has not expanded Medicaid. That inaction perpetuates poor residents' reliance on hospital charity care. 20 Thus, shifting community benefit away from charity care and toward community health programs may have unintended negative consequences for vulnerable patients. Nevertheless, despite the tax incentives that North Carolina nonprofit hospitals enjoy, some spent modest amounts on charity care and some denied care to the poor, while others reported considerable profits. 21 Further compounding this ambiguity, North Carolina does not require hospitals to expend any resources in the form of charity care to maintain their not-for-profit status. 22,23 Similarly, the IRS expansion of community benefit classifications to include expenditures that promote community health did not specify minimum spending on charity care or community health promotion. 21,24

The IRS policy has nudged tax-exempt hospitals to invest and engage more in activities that promote community health by requiring them to conduct a CHNA every 3 years. 1,2,7,8,13 The IRS also instructs tax-exempt hospitals to prepare responsive implementation strategy plans and report yearly their community benefit spendings and activities on IRS Form 990 Schedule H. The requirements became valid for tax years after March 23, 2012, per IRS Code Section 501(r) following Section 9007 of the Affordable Care Act (ACA). 2,8,25 –27 Tax-exempt hospitals must comply with the IRS requirements to maintain their tax-exempt status and avoid a $50,000 excise tax penalty per hospital unit per year for noncompliance. 11

State laws regarding providing community benefit as an obligation for maintaining tax-exempt status vary widely. 4,5,24 In North Carolina, no state laws explicitly require tax-exempt hospitals to provide community benefit, conduct CHNAs, or submit implementation strategies. However, North Carolina State Law 2015-241 House Bill 97 does require nonprofit hospitals to submit annually the community benefit information contained on IRS Form 990 to the state's health department. 21,23

Five years have passed since the IRS Code Section 501(r) took effect, yet little is published in the literature about whether the tax policy has altered the community benefit spending pattern of tax-exempt hospitals. Studies in the peer-reviewed literature were completed years before or just around the time that IRS Code Section 501(r) became effective. This study assessed whether performing IRS-mandated CHNAs incentivized North Carolina's tax-exempt hospitals to increase investments in community health programs.

Methods

This longitudinal study focused on tax-exempt hospitals that operate in North Carolina. Study hospitals were selected using a purposive sampling method. The study team identified 132 North Carolina member hospitals from the 2016 North Carolina Hospital Association (NCHA) Membership Directory. The team excluded 22 for-profit and 40 government-owned hospitals not covered by the IRS Code Section 501(r) rule. Seventeen of the remaining 70 private, nonprofit hospitals were excluded because of incomplete or missing community benefit reports. The remaining 53 hospitals constituted the samples – 76% of all identified private, nonprofit hospitals listed in the 2016 NCHA Membership Directory. Table 1 compares the hospital characteristics of the study hospitals with all North Carolina private, nonprofit hospitals with tax-exempt status.

Characteristics of Private, Non-Profit Hospitals in North Carolina

NC, North Carolina.

Design and analysis

The study team determined the year the study hospitals first completed their CHNA after IRS Code Section 501(r) went into effect. The majority (87%; 46 out of 53) of the study hospitals completed a CHNA in 2013. The team tabulated the community benefit spending data in an electronic spreadsheet and imported the spreadsheet into statistical software for analysis. Community benefit expenditures of the study hospitals during the period they first completed the CHNA requirement (CHNA-Year) were compared against their community benefit expenditures 2 years later (2-Yrs-Later). CHNA-Year community benefit expenditures were adjusted to account for the effect of inflation using Consumer Price Index data. 28 The study team analyzed the inflation-adjusted dollar changes in spending between CHNA-Year and 2-Yrs-Later using paired t tests among matched subjects, applying the upper-tail test with .05 confidence level, and used descriptive statistics to describe the differences in community benefit spending data.

Study variables

In comparing CHNA-Year versus 2-Yrs-Later CHNA spending levels, the analysis used the following dependent variables: (a) the dollar differences of community benefit expenditures for the items listed in Table 2 and (b) the difference in proportion of community health programs category in relation to financial assistance category. Table 2 lists and describes community benefit spending by category and type based on NCHA community benefit reporting guidelines. 29 The study team selected the 10 items that the NCHA defines as a community benefit. Similarly, the team categorized the 10 items into 2 groups in the same way NCHA did. 29

Community Benefit Categories and Items According to the North Carolina Hospital Association

CB, community benefit; CHIP, Children's Health Insurance Program; NCHA, North Carolina Hospital Association.

The Institutional Review Board (IRB) of the University of North Carolina at Charlotte determined this to be an IRB-exempt study.

Results

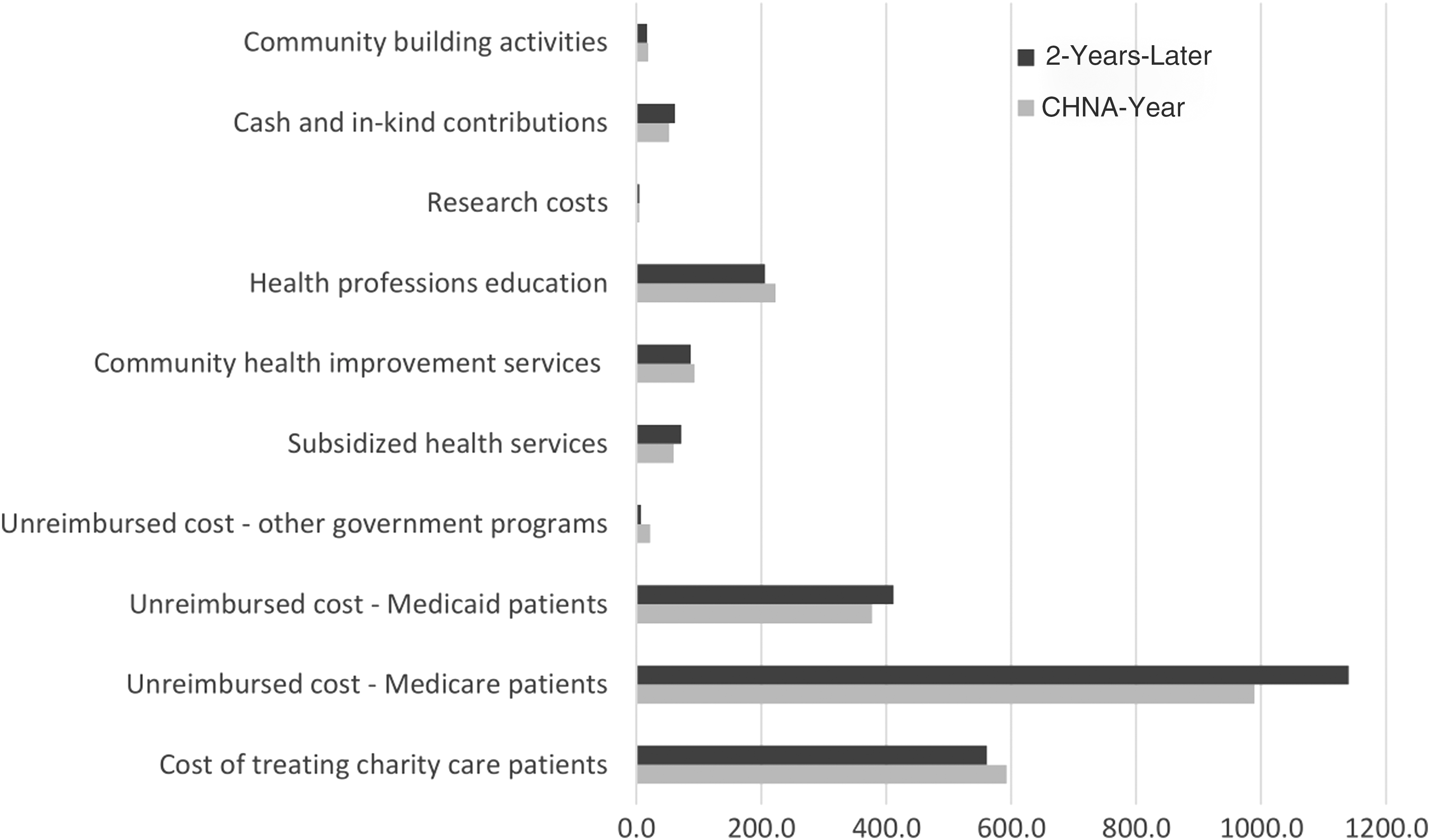

The majority (87%; 46 out of 53) of the study hospitals completed CHNAs in 2013. Three study hospitals completed CHNAs in 2012, and the remaining 4 study hospitals completed CHNAs in 2014. The study team gathered 2012–2016 community benefit spending data of study hospitals from the NCHA website. Table 3 presents the dollar differences in community benefit spending between CHNA-Year and 2-Yrs-Later among the 53 study hospitals. Figure 1 displays the dollar differences. Overall, the total community benefit spending increased by 5.6%, or by $135.2 million. The 15.2% increase in unreimbursed cost for treating Medicare patients ($150.7 million) accounted for much of the increase in total community benefit spending, along with patient care financial assistance. In contrast, community health programs expenditures decreased by 4%, or by $15.8 million, mainly because of reduced spending on health professions education by $16.4 million, or a decline of 7.4%. Among the items under the community health programs category, only spending in cash and in-kind contributions increased, by 17.2% or $9.1 million.

Community benefit spending by type in millions of US dollars, CHNA-Year vs. 2-Years-Later. CHNA, community health needs assessment.

Dollar Differences in Community Benefit Spending by Category

In million US dollars.

Inflation adjusted.

CHNA, community health needs assessment.

The paired t test (Table 4) reveals no significant increase in community benefit expenditures among matched study hospitals between CHNA-Year and 2-Yrs-Later (M = 2.551, SD = 15.129); t(52) = 1.23, P = 0.1126. Community health programs spending did not increase significantly between CHNA-Year and 2-Yrs-Later (P = 0.6920). Moreover, patient care financial assistance did not increase significantly between CHNA-Year and 2-Yrs-Later (P = 0.0934). Among all community benefit items, only spending for the unreimbursed cost for treating Medicare patients increased significantly between CHNA-Year and the 2-Yrs-Later (P = 0.0297) (Table 4). The proportion of community health programs spending relative to financial assistance did not increase (M = -0.04, SD = 0.12); t(52) = -2.17, P = 0.9825). Instead, the proportion of spending on community health programs relative to financial assistance decreased from 0.15 during CHNA-Year to 0.12 during 2-Yrs-Later.

Mean Differences in Community Benefit Spending Between CHNA-Year and 2-Years-Later

In million US dollars.

Upper-tail paired t test.

CHNA, community health needs assessment; CL, confidence limit; LL, lower limit; SD, standard deviation; UL, upper limit.

Limitations

This study is bounded within the context of tax-exempt hospitals that operate in North Carolina. It is limited to analyzing self-reported quantitative data before and after specific time periods. It includes only the differences in spending 2 years after the study hospitals completed their first-ever IRS-mandated CHNA and does not investigate variations in community benefit spending between groups. Factors not addressed in this study may have affected the relationship between IRS CHNA policy and the community benefit spending observed. For instance, North Carolina's non-expansion of Medicaid might have increased spending on charity care and unreimbursed care for Medicaid patients. 20 Also, pay-for-performance schemes instituted by the Centers for Medicare & Medicaid Services (CMS) and reductions in Medicare and Medicaid disproportionate-share hospital payments may have negatively impacted hospital operating margins and influenced choices to favor patient care financial assistance over community health programs. 30 –32

Discussion

This study assessed the pattern and growth of community benefit spending made by North Carolina's tax-exempt hospitals after IRS Code Section 501(r) took effect. It provides insights on whether implementation of the IRS-mandated CHNA is an effective tool in incentivizing tax-exempt hospitals to address a broad set of identified health needs in their communities. This analysis of community benefit expenditures data of matched study hospitals reveals that not only did investment in community health programs not increase from the year they completed the CHNA to 2 years later, but aggregate expenditures in community health programs effectively decreased by 4%, from $393.3 million to $377.5 million (Table 3).

The decrease in community health programs spending was related primarily to decreased spending on health professions education, which may be related to the shortage of physicians, medical residents, or interns in the United States. 33 Spending on community health improvement services and community-building activities declined while expenditures on research remained virtually constant. Only cash and in-kind contributions increased. The decrease in spending for community health improvement services by 6.8% and community-building activities by 10.8% is a troubling development. Community health improvement services are outreach programs to improve community health (eg, health education, free health screenings) while community-building activities pertain to interventions that will enhance the health of the community or provide a safe, healthy environment; for example, shelter for the homeless, job opportunities for impoverished residents, environmental improvements, and public health improvement advocacy. 29

In contrast, the study hospitals' overall patient care financial assistance expenditures rose by 7.4%, from $2.04 billion to $2.19 billion. A substantial portion of the increase came from the unreimbursed cost for treating Medicare patients, which increased by 15.2%, from $989.5 million to $1.14 billion, and from the unreimbursed cost for providing care to Medicaid patients, which also increased by 9%, from $377.4 million to $411.5 million (Table 3).

This study did not examine the causes underlying the upsurge in unreimbursed cost for providing care to Medicare and Medicaid patients. The study team presumes that payment cuts from Medicaid disproportionate share payments (mandated by the ACA when the law assumed that states would expand Medicaid coverage) and payment reductions from the pay-for-performance structures instituted by CMS – namely, the Hospital Value-Based Payment Program, Hospital-Acquired Infection Reduction Program, and Hospital Readmissions Reduction Program – all negatively impacted North Carolina's tax-exempt hospitals.

Nevertheless, it is discouraging to see the glaring difference between the high costs of providing patient care financial assistance that increased over time as opposed to the little investments in community health programs that declined over time despite performing CHNAs (Table 3). Had North Carolina expanded its Medicaid coverage, perhaps its tax-exempt hospitals would have been in a better position to invest more in community health programs because Medicaid expansion would have reduced or eliminated the need for poorer residents to rely on charity care. 20

The disparity in the amount and growth of spending between the 2 categories of community benefit in favor of patient care financial assistance over community health programs suggests 6 things. First, North Carolina's tax-exempt hospitals continue to function as a safety net for the poor and the uninsured rather than increasingly as active partners in population health management initiatives.

1,7

Second, tax-exempt hospitals are more inclined to provide free or discounted medical care to patients with financial difficulties than to improve the health of their communities because providing medical care has been their core competency.

1

Third, their experience of incurring high unreimbursed costs for providing patient care financial assistance to the indigent and Medicaid/Medicare patients may have given the study hospitals a sense of sufficient legal justification for their tax-exempt status, which makes performing CHNAs to spur investments in community health programs as a legal requirement moot. A quote from NCHA community benefit reporting guidelines succinctly summarizes the perceived justification: “No hospital or health system could survive financially if its only patients were ones with government payers. Governments recognize this and expect hospitals to subsidize the cost difference. The financing of this unpaid government debt is a large part of community benefits.”

29

Fourth, the tax-exempt hospitals' community benefit choices are incongruent with the health needs of their communities. Although patient care financial assistance, a large part of which is allocated to “unpaid government debt,” provides a crucial safety net for the poor, it does not contribute to promoting preventive care and improving population health, which were critical priorities of the tax policy and the ACA. 1,10,13 Fifth, performing the IRS-mandated CHNA failed to bring about the desired shift in community benefit spending away from traditional patient care financial assistance and toward population health-focused programs. Sixth, in total, these observations suggest that conducting IRS-mandated CHNAs may have devolved into a mere exercise of compliance to preserve privileged tax-exempt status rather than becoming a tool to improve population health. 8

Controversy in measuring and reporting community benefit

The addition of unreimbursed cost for providing care to Medicare patients as a community benefit has been controversial because excluding this item as a community benefit will cause a significant reduction in reported total community benefit costs. 4,5,26 This controversy can be traced back to the lack of a standard definition of what community benefit is and what items should legally be considered to fall under it. 6,26 The IRS does not include unreimbursed Medicare costs as a community benefit on Part I of IRS Form 990 Schedule H, indicating that the agency does not consider that mentioned item to be a type of patient care financial assistance, or a community benefit for that matter.

However, that item is reported separately on Part III of IRS Form 990 Schedule H together with bad debt expenses. This manner of reporting gives the impression that the agency has given tax-exempt hospitals some latitude with regard to what activities count as community benefit. 26 Consequently, North Carolina's tax-exempt hospitals measure the cost of community benefit based on NCHA community benefit reporting guidelines, which includes the unreimbursed cost of providing care to Medicare patients as a community benefit under patient care financial assistance. 29 Therefore, their published total community benefit expenditures are significantly higher compared to the total community benefit costs found in Part I of IRS Form 990 Schedule H.

Implications for policy and practice

Because the provision of community benefit is the legal standard from which non-profit hospitals are granted tax-exempt status, the IRS should articulate an explicit stance regarding what items should rightfully and legally count toward community benefit. The IRS should issue clear pronouncements on how the items should be measured and reported to the public to avoid confusion in determining the true cost of community benefit. In the same manner that for-profit hospitals are held accountable by the IRS for measuring, reporting, and paying the correct amount of taxes, so private, non-profit hospitals with privileged tax status also should be held accountable by the IRS for measuring and reporting the true cost of community benefit. The public deserves to be supplied with valid and reliable community benefit reports. It also would be helpful if the accountancy profession develops a set of generally accepted accounting principles regarding the measurement, reporting, and auditing of community benefit.

Organizational change takes time and the desired results of policy interventions are usually incremental. Thus, conducting CHNAs must remain a legal obligation by nonprofit hospitals for maintaining their privileged tax status in order to facilitate organizational paradigm shifts in community benefit programming toward population health management programs and away from individual welfare. Policy makers, health care systems organizations, and the community need to work together and bring the word “community” back into the concept of community benefit. 34

The study team recommends that the current CMS prospective payment algorithm for paying inpatient hospitalizations be modified by the addition of a premium factor for Costs of Providing Population Health Programs. It will function like the Indirect Costs of Graduate Medical Education factor. The addition of Costs of Providing Population Health Programs to the algorithm will afford additional payment to hospitals that invest more in preventive care and population health programs. The addition of this payment premium factor will motivate hospitals to spend and engage more in disease prevention programs that hopefully will translate into better community health outcomes.

Future studies may offer more insights into the study of community benefit after implementation of IRS Code Section 501(r). The study team proposes program evaluation studies to assess delivery of community benefit programs and their impact on the health outcomes of the communities around the immediate service areas of tax-exempt hospitals. Analyzing qualitative data on how hospitals provide programs, services, and activities to cater to the identified health needs of their communities may offer other insights into the study of community benefit. Additionally, the team recommends studies that examine the magnitude of differences in how community benefit items are categorized, measured, and published based on hospital associations' guidelines vis-à-vis the items measured and reported on IRS Form 990 Schedule H.

Conclusions

Performing CHNAs did not incentivize North Carolina's tax-exempt hospitals to progressively invest in community health programs, at least in the 2 years after implementation of the requirement. Aggregate community benefit spending increased primarily because of the upsurge in patient care financial assistance. In contrast, except for cash and in-kind contributions, community health program spending declined despite the conduct of CHNAs, which is a troubling development. The community benefit spending pattern of North Carolina's tax-exempt hospitals has continued to be directed primarily toward providing patient care financial assistance, with little investment in disease prevention and community health improvement activities. These findings suggest that North Carolina's tax-exempt hospitals continue to function as a safety net for the poor and the uninsured rather than as active partners in population health management initiatives. At present, performing IRS-mandated CHNAs may be more a demonstration of compliance than a tool to improve population health.

Footnotes

Author Disclosure Statement

The authors declare that there are no conflicts of interest. The authors received no financial support for this article.