Abstract

Financial institutions can make a significant contribution to sustainable economic development. Characterized as “green banking,” banks can foster environmentally friendly practices as well as socially responsible business practices. This study explores the adoption pattern of various green banking activities by different types of banks in Bangladesh between 2014 and 2019, and the extent of banks' contribution to achieving sustainable development in the country. The secondary data used in the study reveals that many commercial banks (private and foreign) have been practicing green banking since 2014 and have instituted green financing policies that are environmentally friendly and sustainable. However, the state-owned commercial and specialized development banks have been more reluctant to adopt green banking practices. The study proposes a framework for adopting green banking practices that will contribute to attaining the Sustainable Development Goals (SDGs), along with policy changes to align banking operations with the SDGs.

Introduction

The banking sector plays a crucial role in the economic development of Bangladesh. Given the challenges of the speed of climate change, banks are more than financial intermediaries but are now also connected with environmental protection and broader eco-system inclusive risk management (Intergovernmental Panel on Climate Change, 2014; Ullah, 2013). To be effective banks need to assume a more direct role in confronting and incorporating climate change (Sarker et al., 2019; Stephens & Skinner, 2013). Given the Sustainable Development Goals (SDGs) and their alignment and dependence, both with sustainability and the prevailing economic system, some have argued that without a vigorous banking system, it will be very difficult to attain the SDGs (Khatun, 2019; Rahman & Barua, 2016; Sahin et al., 2014). Acknowledging the importance of this connection, the Bangladesh Bank, the central bank of Bangladesh, has taken on the role of contributing to sustainable development through implementation of green banking and financing policies. The enlisted commercial banks and financial institutions are bound to follow the guidelines and instructions of Bangladesh Bank. As the central bank, Bangladesh Bank monitors all activities of the commercial banks and imposes penalties if a commercial bank fails to comply with its instructions. So, commercial banks and financial institutions are practicing green banking activities as part of their daily operations.

The term “green” has become ubiquitous in the contemporary world, and green banking has become a buzzword in the banking world. The concept of green was first introduced formally in 2003, and is loosely defined as activities to preserve and protect the environment. Scholars have defined green banking in a variety of ways, but the general focus has been on comprehensive banking approaches that ensure considerable economic growth while also enhancing eco-friendly practices (Lalon, 2015).

According to Bai (2011), green banking is defined to include practices and accountability that establish an environmentally friendly business operation. Green banking is also referred to as moral banking, which broadly encompasses eco-friendly and socially responsible banking practices (Goyal & Joshi, 2011; Sarker et al., 2020b). Amin (2014) referred to green banking as eco-friendly banking practices that make the planet more habitable by preventing environmental degradation. Bihari (2011) found that green banking encourages social obligation by adopting new banking policies in which banks must consider the environmental impacts of a project when determining loan approval. However, the main aim of green banking is to foster accountability in the use of internal or external resources of banks and give priority to supporting sustainable ecological systems (Bahl, 2012).

The core concern of green banking is to encourage financial institutions to support pro-environmental policies and activities such as the use of renewable energy, water and air pollution-free practices in manufacturing, eco-friendly waste management, human and environmental health, and protection of biodiversity (Biswas, 2011). Basically, green banking requires transformation of conventional banking practices into environment-friendly practices that ensure environmental sustainability (Setijawan, 2014; Verma, 2012). However, the approach to green banking varies from bank to bank, with some banks adopting practices such as using an online payment system; optimization of their use of water, gas, and electricity; and adoption of digital technology.

Green banks have also endorsed popular green practices and their slogans such as: “Save paper, save trees”; “Conserve energy, preserve natural resources”; “Use cloth bags”; “Reduce, reuse and recycle”; “Be conscious in the use of everything”; “Adopt a paperless habit” (Bangladesh Bank, 2012). These channels affect operations and perception but do not necessarily constitute operationalized sustainability. In fact, the use of digital technologies may actually result in greater energy and subsequent carbon impact than the use of paper.

For developing countries like Bangladesh, climate change resilience and environmental sustainability are the key components of inclusive socioeconomic development (Alam et al., 2018). Given the concern about environmental protection, in 2011 Bangladesh Bank issued green policies and related guidelines for commercial banks that operate under it (2011). Since commercial banks are working under the guidelines of the Bangladesh Bank, they are asked to incorporate green financing practices into both in-house and external operations. The Bangladesh Bank is committed to providing continuing support and guidelines to all commercial banks to ensure the implementation of environmentally friendly practices (Khan, 2012).

The Bangladesh Institute of Bank Management (BIBM) conducted two studies on the progress of green banking practices in Bangladesh. The first study was conducted in 2011 and selected 25 commercial banks. This study revealed that only 80 to 85 percent of commercial banks were in the planning stage of installing green practices. While 75 percent of the commercial banks adopted plans for instituting green finance, many other banks had not taken any initiative to act (Chowdhury & Habib, 2014).

The second study (2012), which involved 20 commercial banks, found that a large majority (92%) of the banks took the opportunity to use funds targeted for green finance, but they had very low performance in using the climate risk fund (Chowdhury & Habib, 2014). Many commercial banks in Bangladesh had already adopted green banking policies and guidelines but they had a very low rate of executing these practices in their daily business activities—75 percent of commercial banks had implemented only one or two of the guidelines while only 11 percent of commercial banks utilized green marketing funds. Green marketing of a bank focuses on the ethical marketing of banking products, encouraging customers, particularly those in the manufacturing sector, to use the banking funds for pro-environmental compatible products.

To date, there have been very few studies related to the extent of adoption of green banking practices to attain sustainable development in Bangladesh (Islam & Das, 2013; Rahman & Barua, 2016; Rahman et al., 2013; Ullah, 2014). This article explores the nature of green banking practices by different types of banks in Bangladesh and the relationship between environmentally sustainable development and green banking practices.

Methodology

Research Design and Data Sources

Data used in this study were collected from the Bangladesh Bank websites and annual reports for the years 2014 to 2019 (Bangladesh Bank, 2014; Bangladesh Bank, 2015; Bangladesh Bank, 2016; Bangladesh Bank, 2017; Bangladesh Bank, 2018; Bangladesh Bank, 2019); various published sources such as newspapers, magazines, and journal articles; and a variety of working papers and reports. A quantitative approach was adopted to interpret the data; secondary data were extensively used. Fiscal year (FY) data regarding green finance were reviewed to obtain a more realistic overall picture of the green banking practices in Bangladesh. The collected data were analyzed through descriptive statistical methods, and a well-structured data collection observation guide was developed through extensive literature reviews that focused on the key indicators for adoption of green banking and its role in sustainable development.

Measurement of Key Variables

The green banking-related policy of Bangladesh Bank was assessed for its alignment with current practices of green finance in Bangladesh. Data included contributions from various types of banks in the fiscal year (FY). Values are reported in Bangladesh Taka (BDT) in millions, as a percentage of FY contributions to the green product category. Similarly, the role of green banking on sustainable development is measured by assessing the ratio of the rate of adoption of the guidelines to the delivery of associated services that support environmental integrity.

Results and Discussion

Policy Initiatives

The Bangladesh Bank developed a special policy framework outlining three phases of green banking (Table 1). Kicking off the green banking initiative, the first document was published in January 2011 and included guidelines for environmental risk management (ERM) for all banks and non-bank financial institutions (NBFIs) in Bangladesh. The document was comprised of policies and rules for green banking and was undertaken as a measure to help save the environment. In February 2011, the Bangladesh Bank provided a full policy guideline for commercial banks related to regular banking operations. In 2013 a guideline for green banking was given to NBFIs for their operations.

Bangladesh Bank Policy Framework for Green Banking a

Source: Bangladesh Bank (2012)

Green Financing

Green banking is a practical application of traditional banking practices seen through the lens of sustainability and the future of our world. Green banking (GB) is banking that is aligned with environmental improvement (Lalon, 2015). Banks attempt to make industries become green and, in the process, rehabilitate the natural environment (Bhardwaj & Maholtra, 2013). GB also refers to eco-friendly or environment-friendly banking systems that aim to reduce environmental deterioration and make the world a more livable place (Shershneva & Kondyukova, 2020). It entails prioritizing funding for industries that promote various environmental preservation actions. Banks and non-bank financial organizations implement environmentally friendly financing mechanisms and a green transformation of internal operations as part of green banking initiatives (Park & Kim, 2020). The procedure restores the natural environment to maintain environmental safety and long-term ecological balance (Khairunnessa et al., 2021).

Green finance is a broad term that encompasses investment in activities that encourage sustainable economic development. It includes investment in green projects such as: effluent treatment plants (ETPs), solar panel farms, organic fertilizer, biogas plants, manufacturing recyclable products, green security, and safety within a product's industry. Green security indicates the security tools, methods, and practices of an industry or company which reduces the adverse environmental impact. The financing of these green products is also referred to as direct green finance (Shakil et al., 2014). If the manufacturers comply with the environmental ethics guidelines and produce green products, they are eligible to get a loan from the bank, another type of green finance.

Before sanctioning a loan, banks must consider whether or not a proposed project is eco-friendly and if it will have a negative impact on the future people and planet. The amount of investment for underwriting green finance by different types of banks in Bangladesh is presented in Table 2.

Banking Sector Investment in Green Finance, Bangladesh (Tk in million) a

Source: Bangladesh Bank (2014 - 2019)

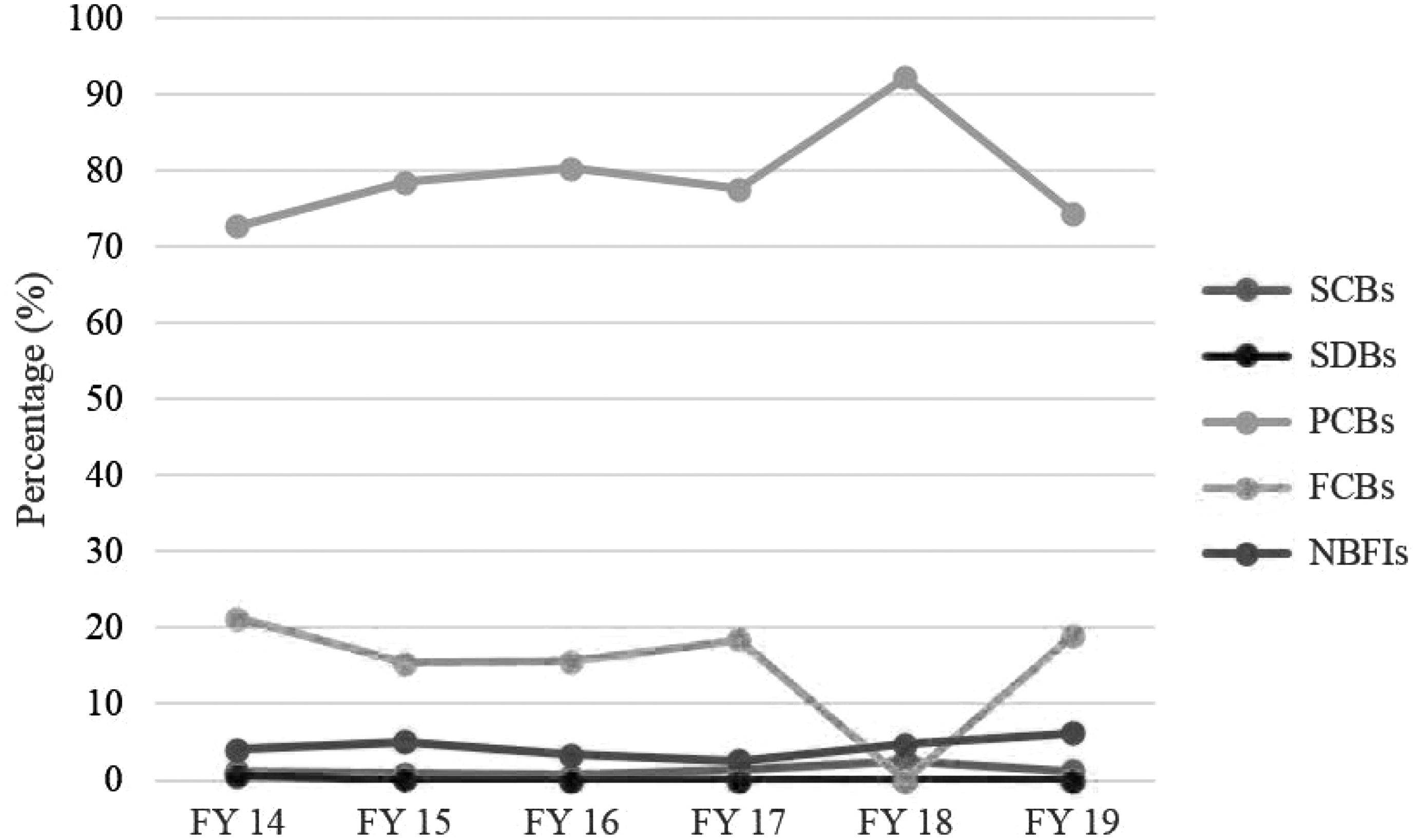

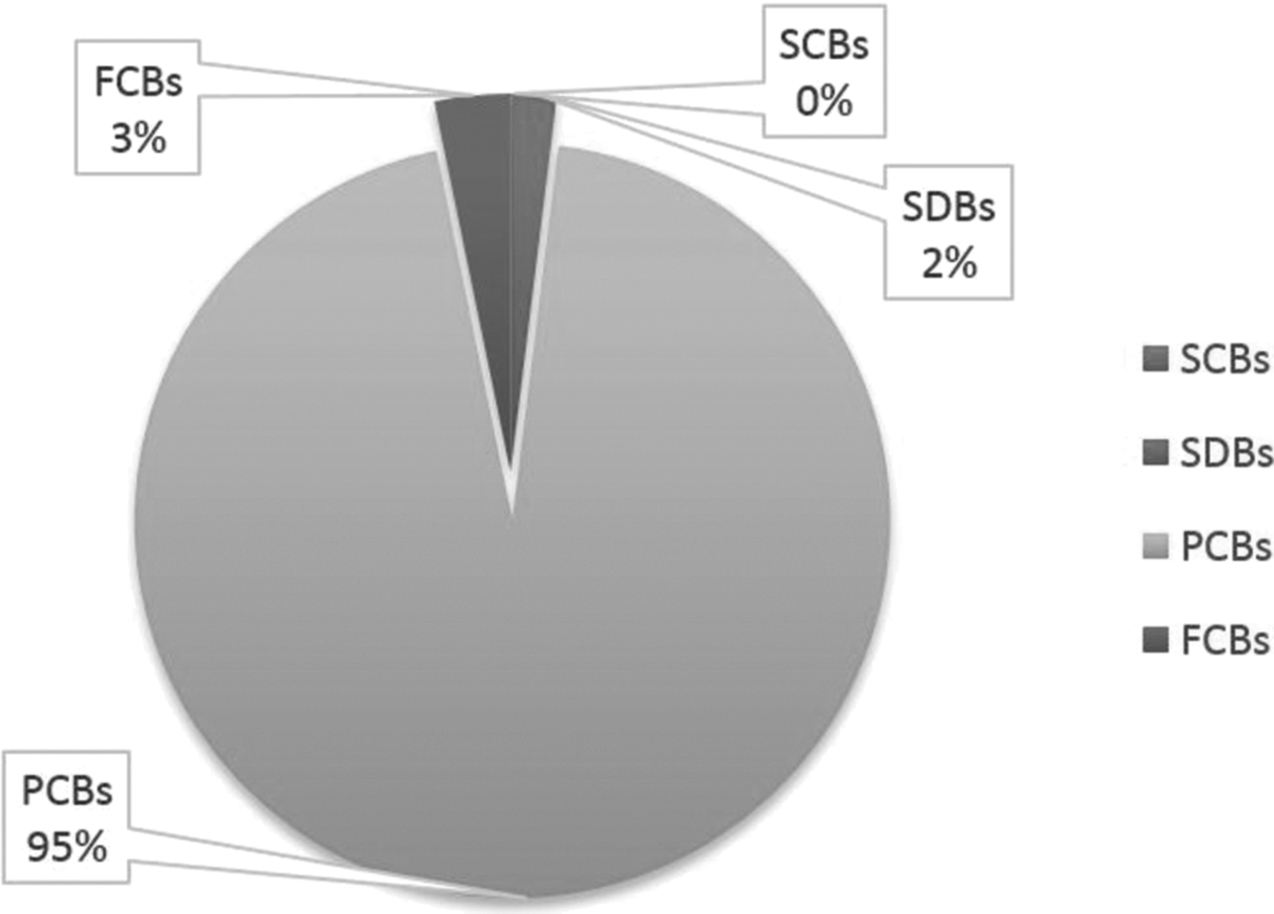

SCBs - state-owned commercial banks; SDBs - state-owned specialized development banks; PCBs - private commercial banks; FCBs - foreign commercial banks; NBFIs - non-bank financial institutions

Generally, private commercial banks (PCBs) have provided more green finance through different products than other types of banks and NBFIs. The PCBs were the only banks whose investment amounts were greater than other types of banks and NBFIs during the 2014 to 2019 period, though they fluctuated. The main reason for the drastic reduction of green finance has been the unwillingness of the PCBs to invest in green products due to their profit-making nature. Actually, the PCBs of Bangladesh are working well under the strict monitoring of the central bank. When the monitoring has been weak, they tended to avoid this kind of finance. The green finance of PCBs declined in FY 2015, and gradually increased to BDT 78,316.88 million in FY 2019. The volatility observed may be due to PCB's unwillingness or limited effort in the management of climate fund use. However, other types of banks and NBFIs similarly revealed a decline up to FY 2018. FCBs and NBFIs showed a higher green finance disbursement in FY 2019 relative to the previous three years. SDBs provided the smallest amount of green finance over the years.

The contribution of the banks and NBFIs to total green finance (i.e., direct and indirect) is displayed in Figure 1. Among all the banks, PCBs showed the highest contribution in total green financing, even factoring in a slightly fluctuating trend that started at a little over 70 percent in FY 2014, reaching about 93 percent in FY 2018, and then decreasing to 74 percent in FY 2019.

Contribution by sector, in total green finance (Bangladesh Bank, 2019)

Bangladesh Bank's Refinance Plans for Green Products

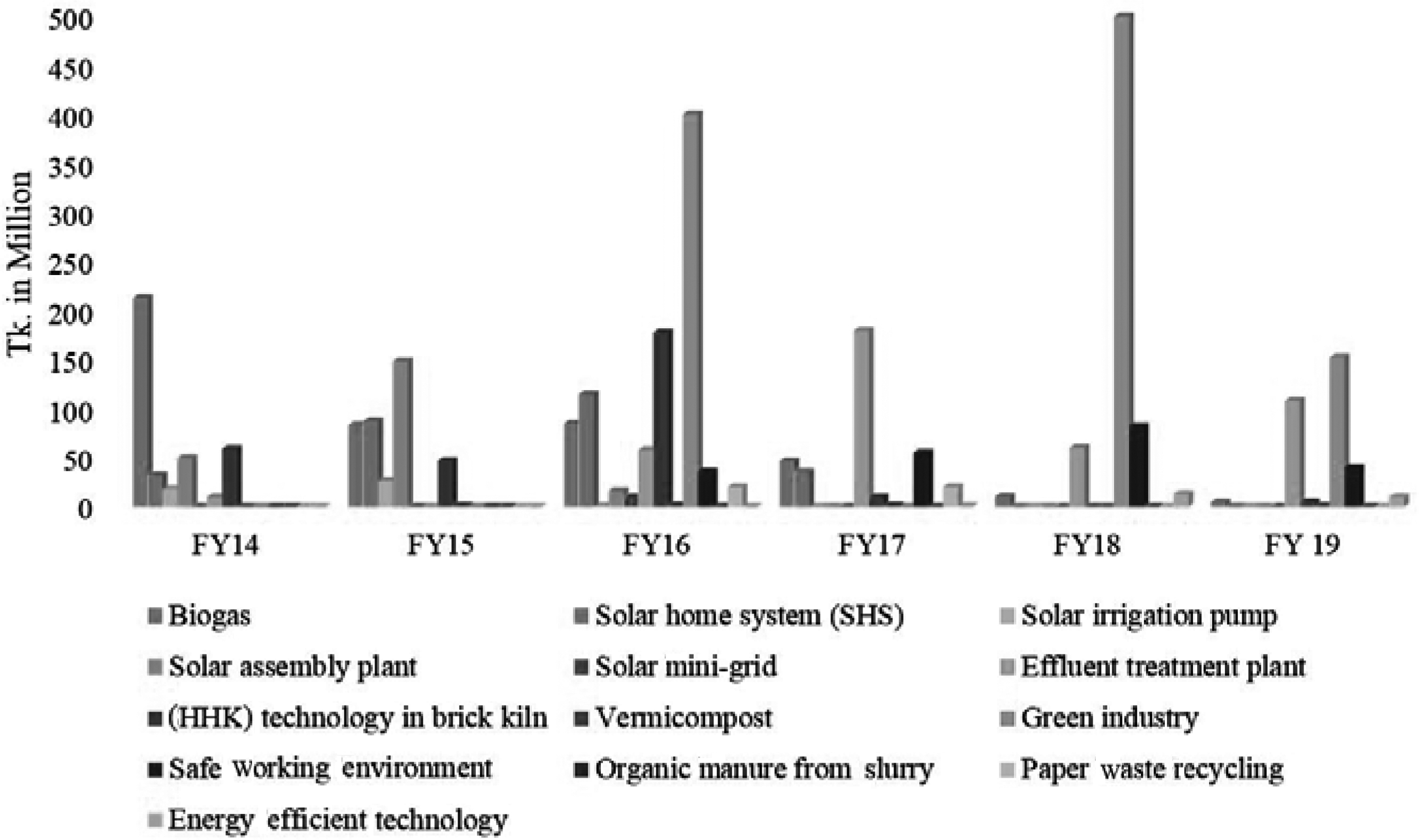

To broaden availability of financing for green products like solar energy, biogas plant and effluent treatment plant, etc., Bangladesh Bank established a revolving refinance scheme amounting to BDT 2.0 billion (≈USD $23 million) from its own fund in 2009. Initially, only six products (ETPs, biogas plants, solar/renewable energy plants, bio-fertilizer plants, Hybrid Hoffman Kiln (HHK), and projects having ETPs) were acknowledged to fall under the refinance funding plans. Since inception to December 31, 2019, the total amount of BDT 4,488.99 million has been disbursed as refinance facility (Bangladesh Bank, 2019). However, given the government's focus on the agriculture sector, the solar irrigation pumping system was given priority over electric pumps for diesel fuel and water (Figure 2).

Disbursement of projects included in refinancing, FY 2014 through 2019 (Bangladesh Bank, 2019)

As shown in Figure 2, the same type of green projects received varied funding in different fiscal years. For example, in FY 2014, biogas received the largest amount of funding, but was reduced over the years, replaced by other other green projects that more directly addressed the need to mitigate climate risks (Islam et al., 2017). Other green projects such as building solar assembly plants and effluent treatment plants received the most funding in FY 2015 and FY 2017, respectively, whereas green industry got priority in FY 2016, FY 2018, and FY 2019.

Green industry means the industry which follows the green banking guidelines and uses green raw materials for production with low emission of GHG. Figure 3 indicates that during FY 2019, green industry received the greatest financing (48%) followed by effluent treatment plants (34%) and safe working environments (13%). The allocation of budget is varied from one sector to another and is based on the priority of the sector. Since green industry received the majority of the financing, followed by effluent treatment plants and safe drinking water, it can help the concerned authority and people for taking effective decision. All told, this data is an indication of government commitment to reducing CO2 emissions from the industrial sectors of Bangladesh.

Finance disbursement by project, FY 2019 (Bangladesh Bank, 2019)

Different Forms of Green Banking That Support Sustainable Development

As an eco-friendly banking system, green banking aspires to promote sustainability. Sustainable development meets the requirements of the present without compromising the capability of future generations (Brundtland, 1987). As per Bangladesh Bank guidelines, commercial banks have undertaken an initiative for greening the environment by offering low interest loans to customers who want to set up solar equipment, ETPs, and biogas plants. Banks are also offering electronic banking in the form of online banking, ATMs, and mobile banking (Kikulwe et al., 2014). These e-banking activities help reduce the use of paper, illustrating one aspect of reducing CO2 emissions (Sarker et al., 2020a). Table 3 shows that FCBs and PCBs have offered online services at almost 100 percent of their branches while SDBs are far behind the others at only 30.89 percent in their best year, FY 2019. SCBs, on the other hand, have showed great progress, increasing their online services from 52 percent to 98 percent in this time period.

Status of Online Branches FY 2014 – FY 2019 a (in percentage)

Bangladesh Bank (2014-2019)

Automated Teller Machines (ATMs) exemplify the individual biggest investment as alternative delivery channel services to the banks' customers. In 2019, there was a total of 7,431 ATMs, the majority (94.82%) of which were established by PCBs while only few (1.87%) were established by FCBs (Figure 4).

Proportion of ATMs setup by different banks in 2019 (Bangladesh Bank, 2019)

In last few years, the convenience of mobile banking, which allows customers to complete banking transaction through mobile devices, has seen rapid expansion in many countries, including Bangladesh (Aker & Mbiti, 2010; Alam et al., 2018; Wesolowski et al., 2012). Mobile banking services allow banking access for people who are out of range of physical banking facilities.

Bangladesh Bank has developed the required infrastructure and is now providing mobile interbank financial services, including private to private (P2P), business to private (B2P), and government to private (G2P) payments (Bhuiyan & Rahman, 2013). The bank has provided green banking related guidelines for this operation to stakeholders. PCBs are providing mobile banking services all over the country while a few SCBs have just begun to build out the necessary infrastructure and SDBs and FCBs have not yet started this service. Rocket, the first mobile banking service, was launched by Dutch Bangla Bank Limited in May 2011 (see Table 4).

Popular Mobile Banking Services in Bangladesh a

Source: website of the respective banks

The Path to Sustainable Development

In emerging economies, banks need to implement green banking policies that include the 3P approach (people, planet, and profit) to sustainability (Gil-Doménech & Berbegal-Mirabent, 2018). The banking sector should also provide a training program for both bankers and their customers to ensure proper implementation of green banking activities (Zadek & Robins, 2015). As the banking sector expands in Bangladesh, banks have started launching a variety of green products and services along with their existing offerings. A growing customer demand for services includes green banking transactions, and a good number of green products and services have already been instituted, with more to follow in the near future.

One such service is green deposits, a rating system for deposits that enable the bank to offer higher interest rates on money market accounts, checking accounts, and savings accounts to customers who bank online. While this service helps make banking activities more convenient and environmentally friendly, the primary function of a bank is to lend money, and green bank lending is specifically targeted toward developing renewable energy projects, climate-resilient infrastructure projects, and installation of more energy-efficient and climate-smart equipment, appliances, houses, and vehicles.

The green banking policy and guidelines issued by Bangladesh Bank underscore the importance of achieving climate resiliency (Shafi et al., 2019). When traditional banking is finally transformed into green banking, internal banking activities will be set up in a way that benefits sustainability through disbursement of loans for greenhouse gas mitigation and climate resilience projects. It is expected that these initiatives will help the banking industry do its part to combat climate change by reducing its carbon footprint from daily banking activities. Underwriting green projects will have a positive effect on the environment by reducing greenhouse gas emissions from increased use of renewable energy as well as changing the pattern of land, forestry, and agriculture practices (Figure 5).

The path to sustainable development

There are many barriers to a green banking transition in Bangladesh, including: lack of a regulatory framework, insufficient financial and economic incentives, limited access to affordable finance, lack of capacity to evaluate and monitor climate projects, high perceived risks of financing climate projects, low awareness about climate technologies and its opportunities, and a lack of climate strategy for environmental and social safeguards. To mitigate these barriers, the banking industry needs to put more effort into identifying and developing climate resilient projects and raising awareness about green underwriting and the impact the banking sector can have on achieving a sustainable environment.

Conclusions and Policy Implications

This study used secondary data to explore the extent of adoption of green banking practices by different banks and financial institutions in Bangladesh with an eye toward achieving sustainable development. The study revealed that most of the PCBs and FCBs made great strides in adopting green banking policy, while SCBs have lagged. In addition to in-house green banking practices, Bangladesh Bank has developed policy for sanctioning loans to environmentally convenient projects where PCBs disbursed the highest amount followed by FCBs and SCBs. However, the contribution of SDBs in green financing has been negligible. It was also observed that different green products received different priorities by the banks in different fiscal years. Biogas, effluent treatment plants, and energy efficiency technology have received less consideration while green industry has been the main concern in the last three years.

Building awareness among bank-related stakeholders is a necessary step in the process of achieving sustainability. The central bank and financial regulators can play a crucial role as they have the power to change and control the landscape of the financial sector. Although the financial sector is highly regulated, the regulatory framework that enables green practices is insufficient and often discourages banks from engaging in green banking activities internally and externally. The banking sector needs to formulate criteria for financing businesses, particularly those in carbon-intensive industries, whose policies will help to mitigate the risks related to an energy transition and thus contribute to making the economy more sustainable.

The Bangladeshi government support of green banking activities through measures such as policy lending, subsidies, and tax benefits along with international grants for technical assistance and long-term concessional loans for bankable climate projects and technologies, will go a long way toward creating a more sustainable environment. To maximize the best outcome, policy-level interventions should provide support for capacity building, sharing of knowledge, and raising awareness about green banking activities. Therefore, monitoring by the central bank should be strengthened so that all financial institutions can be effective in adopting and practicing green banking policies with the goal of creating a low-carbon economy. To achieve this, coordinated efforts of the central bank, government, financial institutions, customers, and environmentalists will be indispensable in paving the way to attaining sustainable development in Bangladesh and contributing to the mitigation of climate change.

Footnotes

Funding Information

No funding was received for this study.

Author Disclosure Statement

No competing financial interests exist.