Abstract

Introduction

In the United States, climate action at the national level has to go one of two ways, both of them challenging. One way is to unite the left: have Democrats take control of Congress and the presidency and then pass climate legislation. As this commentary goes to press, in August 2022, Democrats are on the verge of doing exactly that, with the Inflation Reduction Action supported by Democrats but no Republicans.

But climate change is a long-term challenge, so even if the Inflation Reduction Act passes, it is worth considering the other approach to climate action: bipartisan climate action that can gain support from climate-concerned Republicans. Senators Mitt Romney of Utah and Susan Collins of Maine are among the unfortunately small number of such Republicans now at the national level. There are not many conservative climate champions at the state level, either, but opportunities do exist in the so-called “laboratories of democracy” to produce both legislation and leaders, with the twin goals of acting on climate at the state level and setting the stage for future action at the federal level.

This commentary describes one such opportunity: the Climate Action Tax Cut, a policy that can work in many US states, some municipalities, and at the national level in countries that levy Value Added Tax (VAT) on residential electricity consumption. After describing this policy, the discussion ends with a cautionary note from Washington State about how there are only two obstacles to bipartisan climate action: the left and the right. On the right, the obstacle is finding climate policies that conservatives can say Yes to. On the left, the obstacle is that the compromises required for a bipartisan approach to climate action might be less attractive than betting the planet's future on a unite-the-left approach.

Background: The Political Economy of Carbon Pricing

Economists agree that putting a price on carbon is an effective and economically efficient way to reduce the CO2 emissions that contribute to global climate change. Politically, however, carbon pricing is challenging because it explicitly raises consumer prices for things like gasoline and electricity. Every $10 per metric ton carbon tax increment raises the price of motor gasoline by about 10 cents per gallon, the price of natural gas by about 5 cents per therm, and the price of coal-fired electricity by about 1 cent per kilowatt-hour (Hafstead & Picciano, 2017).

This poses a political challenge because voters and their elected representatives are sensitive to these prices. This is especially true in conservative states, where voters are more sensitive to tax hikes and where many elected officials have signed the Taxpayer Protection Pledge (Americans for Tax Reform, n.d.-a), a pledge that requires politicians to vote against or veto any net tax increase.

A related political challenge, one that is a policy challenge as well, is about regressivity. The Consumer Expenditure Survey shows that annual household expenditures on electricity, the focus of the Climate Action Tax Cut, average about $1,500, or almost 2 percent of household income (US Bureau of Labor Statistics, 2019). This expenditure share is greater for lower-income households than for higher-income households, meaning that taxes on residential electricity are regressive.

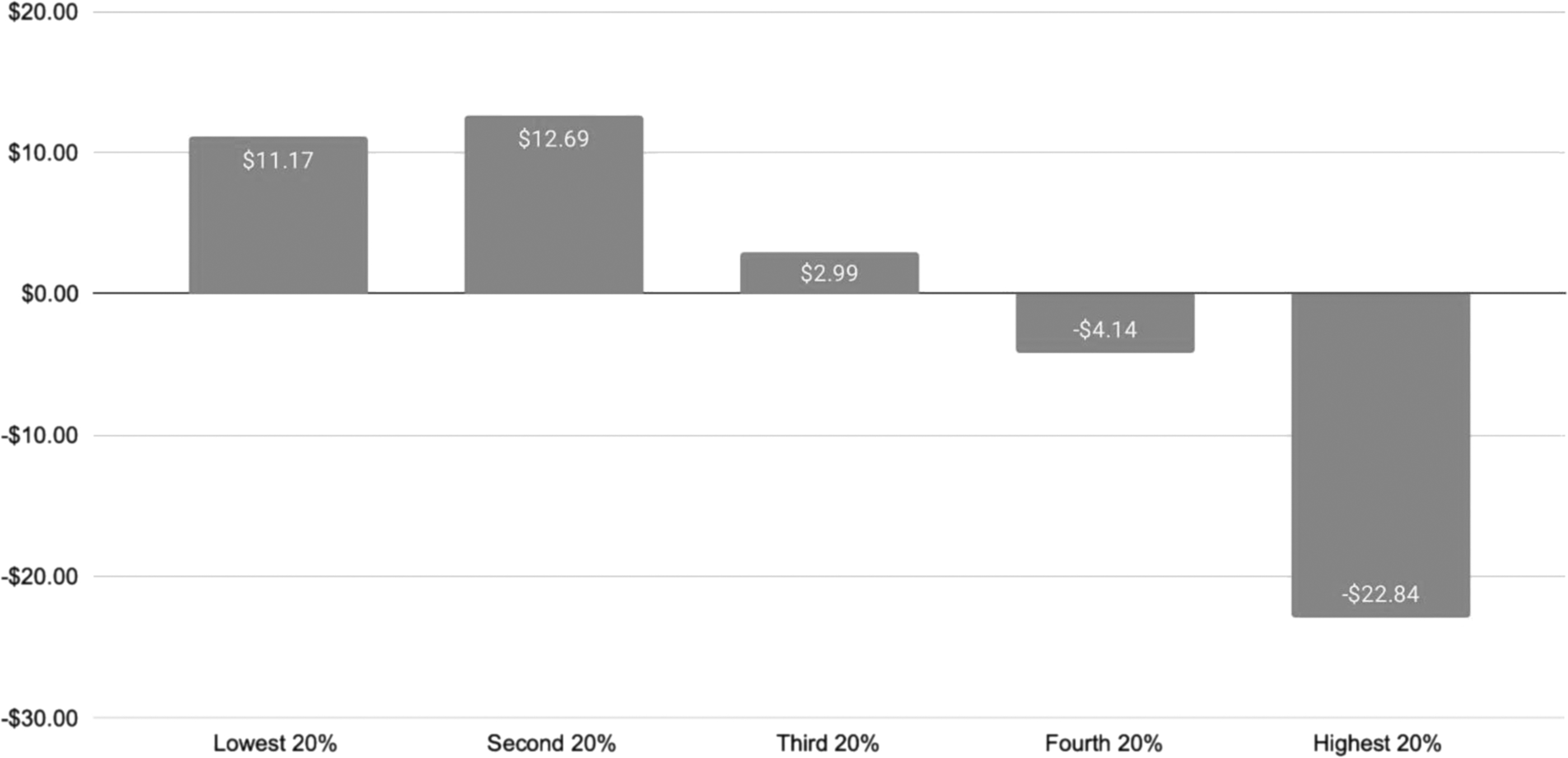

Figure 1 shows that taxes on residential electricity are even more regressive per dollar than taxes on grocery-store food. It illustrates the impact by income quintile of a hypothetical revenue-neutral tax shift that—for an average household—replaces $100 in taxes on electricity with $100 in taxes on grocery-store food. Because the shift is revenue-neutral, the columns sum to zero. The comparison is instructive because of the political treatment of groceries: most US states have sales tax exemptions for groceries (Figueroa & Legendre, 2020), and a recent effort in Utah to raise the sales tax rate on groceries was repealed after encountering bipartisan opposition (Wood, 2019, 2020). Similar opposition is likely to await climate proposals that raise the price of gasoline or electricity.

Savings by income quintile for a revenue-neutral sales tax shift that decreases electricity taxes and increases grocery-store food taxes, each by $100 for an average household

It should be noted that economists and carbon tax advocates have a reasonable response to these concerns, namely, that consumers can be made whole by using the revenue from carbon pricing to reduce existing taxes or fund a per-capita dividend (Climate Leadership Council, 2019). Indeed, this is an option for officials who have pledged not to raise taxes: The website of Americans for Tax Reform, as well as statements by Grover Norquist, the creator of the Taxpayer Protection Pledge, make it clear that revenue-neutral or revenue-negative tax swaps do not violate the pledge (Americans for Tax Reform, n.d.-b; National Journal, 2022). Reasonable though it may be, however, this response has not been convincing in practice. Hesitancy—if not outright opposition—on the part of voters and elected officials remains a significant hurdle for carbon pricing.

A third political challenge for carbon pricing is the attitude of businesses, notably electric utilities. Although many utilities—including investor-owned utilities such as Georgia Power (Southern Company, n.d.) as well as publicly owned utilities such as Nebraska Public Power District (2021)—are pledging to reduce their carbon emissions, they also remain focused on keeping rates low, and so they are unlikely to be advocates for carbon pricing. These utilities are politically powerful, in part because they are so closely connected to customer utility bills.

The Climate Action Tax Cut

The Climate Action Tax Cut is a modest but not insignificant opportunity to put a price on carbon without increasing consumer prices. As such, it may be particularly appealing in conservative states. This opportunity arises in one key sector of the economy, the electricity sector, both in these states and in other jurisdictions that currently impose sales taxes or other taxes on electricity. The presence of these existing taxes—in 18 US states as well as municipally and internationally—opens the door for a policy that gives utilities an incentive to reduce carbon emissions while eliminating or reversing the price impact on consumers. A Climate Action Tax Cut reduces the existing tax on electricity in line with reductions in the carbon intensity of that electricity.

In the short run, this policy is close to revenue-neutral, both in aggregate and for individual consumers. In the long run, it helps to sunset regressive taxes on electricity and, simultaneously, electric-sector carbon emissions. The long-run revenue impact is modest in comparison to both the impact of tax exemptions for other necessities such as grocery-store food and the likely increase in tax revenues over time resulting from natural economic growth.

Table 1 provides existing tax rates on electricity in 20 US jurisdictions and the carbon tax equivalents of those taxes, i.e., the carbon tax rate that would generate the same revenue in the electricity sector as the existing tax.

Jurisdiction Tax on Residential Electricity (Percentage per Dollar or per kWh), and Carbon Tax Replacement Rate (Dollar Value)

A Climate Action Tax Cut reduces the rate of the existing tax on electricity based on the carbon intensity of that electricity. In Georgia, for example, the state sales tax rate could remain at 4 percent for utilities with a carbon intensity at or above the statewide average (about 0.4 MTCO2/MWh) but go down to 3 percent for utilities with a carbon intensity of 0.3, to 2 percent for utilities with a carbon intensity of 0.2, and so on, leading ultimately to zero state sales tax for utilities with zero carbon emissions.

The resulting incentives are generally similar to those from a carbon tax. To see this, consider a Georgia utility with an average before-tax retail price of $100/MWh that is considering an investment in renewables that would lower its carbon intensity from 0.4 to 0.3 MTCO2/MWh. Implementing a carbon tax of $10/MTCO2 would boost the financial attractiveness of this investment by $1/MWh. This is identical to the boost that would accrue under the Climate Action Tax Cut described: a 1 percentage point reduction in the state sales tax would amount to $1/MWh. (This example uses round numbers for simplicity; using exact numbers raises the carbon tax replacement rate from $10/MTCO2 to the $12 shown in Table 1.)

Will a Climate Action Tax Cut Motivate Utilities?

The assumption throughout this discussion is that all taxes—carbon taxes as well as sales taxes—are fully passed through to customers. Given this assumption, it is worth asking whether utilities will be incentivized to act in a way that saves money for their customers. The answer is Yes—or at least the answer should be Yes—but the logic depends on which of three categories the utility is in.

First, there are publicly owned utilities: electric co-ops or municipal utilities such as Nebraska Public Power District or Dalton (GA) Utilities. These utilities are controlled by their customers (e.g., through board elections) so the utility should act in the public interest. All else being equal, if moving from (say) coal to renewables can reduce customer bills, then the board should pursue those moves, and if they don't, then voters have an incentive to replace the board.

Then there are utilities in deregulated markets, where customers can choose their electric supplier. In this case each supplier generates or contracts for the power it sells, so each supplier can be associated with a carbon intensity for the power it delivers. That carbon intensity will affect customer bills, so the incentives should work smoothly in accordance with Adam Smith's invisible hand: If the tax-inclusive price from supplier A is higher than the tax-inclusive price from supplier B, consumers have an incentive to switch from A to B. The power of competition consequently leads electricity suppliers to minimize costs for their customers by reducing their carbon emissions when possible.

Finally, there are regulated-monopoly investor-owned utilities such as Georgia Power. For these entities, regulation is determined by a public utilities commission (PUC) or similar public board (Georgia Public Service Commission, 2021). The regulatory environment here can be a bit opaque, but there are at least two paths by which the policies could create incentives for utilities to reduce emissions. First, many utilities have carbon-reduction goals, but these utilities also often target the goal of low-cost power, so a Climate Action Tax Cut could help utilities make the case that low-carbon investments will also lower costs for customers. Second, the PUC could push utilities to reduce carbon emissions in ways that will lower the tax-inclusive price for customers.

A Free Lunch?

Economists generally believe that there's no such thing as a free lunch, so it's worth pointing out two of the costs associated with a successful implementation of a Climate Action Tax Cut.

One such cost comes from utility investments as a utility may choose to, for example, invest in renewables plus batteries to replace fossil generation because that would result in lower tax-inclusive prices for consumers. Despite these price reductions, it is still true that the investment in renewables comes at a cost. This can be easily seen by comparing the Climate Action Tax Cut to an alternative that simply exempts electric utilities from sales taxes, no strings attached. Of course, this alternative approach wouldn't provide any incentives for emissions reductions.

Another cost is a loss of state tax revenue if utilities reduce carbon emissions. Of course, the lost tax revenue accrues to the state's residents. There are four other considerations as well. First, the revenue impact phases in over time; as described, the policy is close to revenue-neutral in the short run. Second, and related, is that long-run economic growth likely means that there will not be a reduction in state tax revenue in absolute terms. (There will be a reduction in relative terms, i.e., compared to the status quo.) Third, the regressive nature of taxes on electricity is a strong argument for eliminating these taxes, in the same way that most states don't impose taxes on grocery-store food. Fourth, state tax data show that the amount of revenue generated by taxes on electricity (about 2 percent of total state revenue) is equal to or less than the revenue that would be generated from imposing sales taxes on groceries, so budget-based opposition to a Climate Action Tax Cut should logically lead to opposition to sales tax exemptions for groceries. Finally, there are climate considerations that bolster the case for taking action on climate.

Applications in Other Jurisdictions

It might be possible to implement this sort of tax swap at the municipal level—for example, many local jurisdictions in Utah impose a 6 percent municipal energy tax (Utah State Tax Commission, n.d.)—but municipalities might be highly dependent on this sort of revenue. If the revenue could be made up elsewhere, however, some municipalities have high enough sales taxes that a tax swap could make a big difference. For instance, as seen in Table 1, New York City's electricity taxes are the revenue equivalent of a hefty $47 carbon tax.

It might also be possible to implement this sort of tax swap internationally. Table 2 highlights value added tax rates on residential electricity as listed in the International Energy Agency's (IEA) World Energy Prices (n.d.). Some of these international jurisdictions could be especially promising opportunities for emission reductions because their value added tax rates are much higher than state sales tax rates in the United States, meaning that the revenue-equivalent carbon tax rate would likely be higher.

Value Added Taxes on Electricity

Source: International Energy Agency, n.d.

A Cautionary Note from Washington State

In 2016, a grassroots group founded in Washington State put a carbon tax on the ballot in the United States for the first time ever. Initiative 732 (I-732) was revenue-neutral, meaning that money from the carbon tax was offset by tax reductions elsewhere, principally a reduction in the regressive state sales tax, but also an Earned Income Tax Credit match for low-income working families, plus business tax cuts for manufacturers to help them stay competitive.

I-732 was smart, small-government climate action. It got endorsements from three sitting Republican state senators and from Republican leaders like Rob McKenna, who had narrowly lost the governor's race in 2012. Other would-be opponents took a neutral position, including the powerful Western States Petroleum Association. Sightline Institute, a Seattle-based sustainability think tank, said I-732 would be the state's most progressive tax measure in 40 years (Eberhard & Durning, 2016). The Audubon Society endorsed it as strong climate policy (Audubon Washington, 2016).

But making progress wasn't enough for some in the progressive environmental community (Geiling, 2016). Washington Conservation Voters (2016) recommended a No vote. So did the Sierra Club and Democratic Governor Jay Inslee. They wanted the Green New Deal or bust.

So, they fought I-732. It ended up with 41 percent of the vote, opposed by right-wingers who were afraid that it was socialism and left-wingers who were mad that it wasn't.

Two years later, in 2018, progressives in Washington State spent $15 million on a Green New Deal ballot measure, Initiative 1631 (I-1631). The petroleum association spent $30 million on No ads, many of them starring Rob McKenna. I-1631 got 43 percent of the vote.

For the environmental left, these losses carried a clear message (Roberts, 2020): Blame economists, ignore Republicans, and double down on unite-the-left approaches.

This strategy may or may not work in Washington, DC, but [it has] succeeded in Washington State—to a point. In 2020 the Democrats gained control of the state legislature. Without any Republican votes, they passed a “cap-and-invest” bill that starts in January, funding $500 million annually in clean energy investments (Turner, 2022). It will be paid for primarily at the pump: The state's economic models predict a gas price increase of between 35 and 60 cents per gallon (Washington State Department of Ecology, 2022). Proponents call this “significant benefits at minimal costs” (Woodward, 2022). Time will tell if it inspires the nation, but it's worth exploring other options, too, including the Climate Action Tax Cut. There are other pocketbook-friendly approaches, too: An effort in Utah called Clean The Darn Air aims to eliminate Utah's unpopular sales tax on grocery-store food—and improve the state's terrible local air quality (Kennington, 2022)—with revenue from a carbon tax.

Conclusion

The Climate Action Tax Cut described in this commentary is a modest but not insignificant effort toward pocketbook-friendly, economically sensible climate action. This policy is close to revenue-neutral in the short run and holds the promise of sunsetting regressive electricity taxes in the long run. And it shares one of the key advantages that come with all market-based policies: creating a menu of choices rather than restricting choices in the manner of a command-and-control-style regulatory approach. Reducing the sales tax rate in line with carbon intensity doesn't force utilities to cut emissions. If there are concerns about the reliability or cost of low-carbon power sources, utilities can simply continue their current operations: no harm, no foul. But if a lower-carbon alternative does make sense, a Climate Action Tax Cut creates a financial incentive to pursue it.