Abstract

As a response to the threat of climate change, a growing number of businesses are voluntarily reporting carbon statistics. This article provides a comprehensive understanding of carbon disclosure, organization performance (OP), and cost of capital. This study aims to map the landscape of existing carbon disclosure and firm performance research completed over the past 10 years (2013-2022) utilizing bibliometric analysis. Sparked by the growing political, social, academic, and practical significance of controlling and reporting on climate-related concerns worldwide, this study analyzes the production and acquisition of information about significant regions and territories, institutions, publications, and channels for carbon disclosure and firm performance research using data from 878 publications retrieved from the Scopus database. To identify themes and subthemes in the research on carbon disclosure and firm performance, network analysis was utilized to reveal connections between the topics represented by keywords. Further, critical gaps have been highlighted in the literature, such as: the lack of carbon disclosure research across cross-sector settings, the lack of sectorial comparisons on the carbon disclosure practices, and the dearth of analyses of both pre-carbon disclosure and after-carbon disclosure practices and their impact on various financial and nonfinancial issues (for example, cost of capital and firm performance, sustainability, and climate change). Finally, this study makes specific recommendations for future carbon disclosure and firm performance research.

Introduction

Greenhouse gas (GHG) emissions have emerged as one of the most serious dangers to the survival of life on our planet (Siddique et al., 2021). Excess GHGs in the Earth's atmosphere have negative effects on the environment, resulting in global warming (Liu et al., 2015; United Nations, 1992). The global socioeconomic implications of climate change could be enormous, as a changing climate affects both humans and natural capital (Patel et al., 2021). Organizations such as those that make up the energy sector, transport sector, manufacturing sector, and construction sector have long been primary contributors to the problem of climate change, as they rank high among the leading emitters of greenhouse gases (Heede, 2014; Hoffmann & Busch, 2008; Levin et al., 2012; Wijen, 2014).

Over the last two decades, there has been an increase in deceptive or inaccurate disclosure methods that have had a considerable negative impact on stakeholders' confidence in companies. Due to harmful climate change, environmental disclosures by public entities have attracted a great deal of studied interest in recent years (Dr Bilal et al., 2021; Ramos-Meza et al., 2021). However, according to (Morsing & Schultz, 2006), stakeholders were found to have inadequate information about management strategies and expressed dissatisfaction with the lack of knowledge sharing from the boards of directors.

In the majority of nations, the reporting of environmental disclosures is voluntary; therefore, the discretion of senior management in determining environmental disclosures and expenditures is crucial (Hambrick, 2007). Due to the voluntary nature and managerial discretion, managerial preferences have a crucial impact on carbon disclosure spending (Hemingway & Maclagan, 2004). Most companies aspire to be environmentally responsible even if only to make a favorable social impression on their stakeholders. This has led senior management to implement measures to increase transparency regarding their environmental practices (Kuo & Chen, 2013). Large corporations are also increasingly interested in tracking and reporting carbon emissions.

As climate change becomes one of the most discussed political, societal, and business issues worldwide, along with the introduction of regulations to combat the threat of global warming, such as the Emission Trading Scheme (ETS) in the European Union and carbon taxes (or similar pricing mechanisms) in several other nations (including Australia, Japan, Norway, South Korea, and Switzerland), it is anticipated that the practice of carbon disclosure will continue to rise (Morsing & Schultz, 2006; Qian & Schaltegger, 2017). Specifically, carbon disclosure is becoming a de facto requirement for large companies.

Although there has been an increase in carbon disclosures, it is not yet clear to what extent the reporting of carbon emissions is linked to enhancements in company performance (Dr Bilal et al., 2021; Kuo & Chen, 2013; Siddique et al., 2021; Velte et al., 2020). This issue relates to the classic question of whether rapid changes in carbon reporting have impacted companies' cost of capital and overall performance. However, businesses have recently converged on a more optimistic view of environmental alteration, presenting it as an opportunity as opposed to a burden (Siddique et al., 2021)

In addition, financial markets are now incentivizing companies that are taking proactive measures to tackle climate change, while those that are falling behind are being perceived as riskier. Investors and environmental nongovernmental organizations are pressuring businesses to reveal evidence about their GHG emissions, as carbon revelation is essential for the fair valuation of assets. Several efforts indicate an intent to use the influence of institutional stockholders to generate demand for carbon transparency as an ethical imperative (Qian & Schaltegger, 2017).

Given the significance of the sustainability concept, there have already been studies on carbon disclosure, organizations' performance, and cost of capital; however, they differ substantially from the current analysis. For instance, the analysis by (He et al., 2013) found a correlation between carbon reporting, carbon performance, and capital costs, and their findings reveal a negative association between carbon reporting and the cost of capital. Further, (Díaz Tautiva et al., 2022) give a comprehensive analysis of the literature since the turn of the century that has dealt with the topic of environmental alteration and firms. Further, reviews on carbon performance and disclosure, as well as their financial implications (Paul & Rosado-Serrano, 2019), suggest a positive relation between the variables. More recently, (Borghei, 2021) identifies key research fields and emerging research trends to address carbon disclosure issues.

During this literature review, a limited number of bibliometric analyses concerning carbon disclosure and associated topics were discovered. It should be noted, however, that these findings concentrate on single themes such as carbon disclosure, carbon disclosure management performance, and carbon disclosure and governance; thus they are limited in scope. Therefore, the current work seeks to fill these gaps and inadequacies by conducting a thorough literature evaluation of research related to carbon disclosure, organizations' performance, and cost of capital. Following the analysis of literature reviews that concentrate on bibliometric approaches (Jiang et al., 2023; Khan et al., 2022; Lim et al., 2022; Rasul et al., 2022; Tlili et al., 2022) and organizing paradigms (Hollebeek et al., 2022; Khan et al., 2022; Rojas-Sánchez et al., 2022; Zhang et al., 2022), this study formulates and examines the following research questions (RQs):

RQ1: What is the trend in carbon disclosure, organization performance, and cost of capital publications?

RQ2: Which nations publish the most on carbon disclosure, organization performance, and cost of capital?

RQ3: Which are the most influential journals and media channels for research on carbon disclosure, organization performance, and cost of capital?

RQ4: What is the knowledge structure (themes, subthemes, issues) of carbon disclosure, organization performance, and cost of capital research?

RQ5: What are the possible future directions for research on carbon disclosure, organization performance, and cost of capital?

The subsequent sections are organized as follows: the Overview provides the theoretical context of carbon disclosure, organizational performance, and cost of capital. The Methodology section describes the methodology utilized in the present study and is followed by an analysis of the review's findings and the thematic map analysis. The Discussion section summarizes the review's findings. The last section describes the conclusion, implications, and limitations of the study.

Overview

To predict the association between climate disclosure and environmental/carbon performance, scholars have mostly used two theoretical framework streams (Bewley & Li, 2000; Cho & Patten, 2007; Clarkson et al., 2011). One stream consists of legitimacy and stakeholder theory; the other stream is comprised of signaling theory and voluntary disclosure theory. Stakeholder and legitimacy theory implies an undesirable relationship, whereas voluntary revelation and signaling theory imply a positive one.

The available research on environmental accounting can be categorized into three main clusters (Clarkson et al., 2011). The initial cluster of studies concludes that disclosing environmental information is significant in determining the value of a company. The second cluster analyzes the aspects that influence companies' voluntary disclosure of environmental information. The third cluster of studies shows inconsistent outcomes in the investigation of the association between environmental information revelation and environmental performance.

For example, companies that possess a substantial carbon footprint and do not possess sufficient measures to curtail their carbon emissions are perceived as socially irresponsible (Luo, 2019). These companies could be penalized by society if they fail to adopt effective ways to mitigate climate change (Bansal & Clelland, 2004; Pfeffer & Salancik, 1978). Therefore, these firms employ tactics to counteract publicly available negative news to maintain legitimacy (Bebbington et al., 2008). Voluntary carbon disclosure is one of the methods used to preserve credibility. Firms may employ voluntary carbon disclosure to counter any threats to their legitimacy, which also can assist firms as an image management approach to shape public perceptions (Bansal & Clelland, 2004; Cho & Patten, 2007).

Firms that have higher carbon performance tend to actively pursue low-quality information, characterized by shallowness, partiality, lack of comparability, and ambiguity. This deliberate choice serves the purpose of disguising their unfavorable real situation, enabling them to maintain their legitimacy and cultivate a positive image of sustainability (Hummel & Schlick, 2016).

Carbon performance is the result of carbon emissions-related managerial activities. Companies typically publish their achieved carbon performance voluntarily in anticipation of stakeholders' expectations of such reporting (Deegan, 2002). According to the theory of voluntary disclosure, companies have incentives to disclose favorable information to distinguish themselves from other companies that have negative news (He et al., 2013). However, Bewley & Li (2000) and Clarkson et al. (2008) contend that genuine environmental performance is not directly visible to stockholders; hence, firms with better performance tend to make voluntary direct disclosures that are difficult for companies with poor performance records to match.

Several researchers argue that companies with questionable credibility are more likely to engage in self-interested disclosures, commonly referred to as legitimization (Adams, 2004; Lee & Raschke, 2023). Researchers believe that corporations susceptible to certain sorts of criticism will make voluntary disclosures to deflect or dispel suspicion concerning this type of criticism. Further, Velte et al. (2020) highlight the quantifiable emissions of greenhouse gases that alter the climate, as well as the techniques and processes for reducing air pollution .

As carbon-related operations have gained significance in society (particularly in environmentally sensitive sectors), carbon disclosure has become the communication channel that increases a company's legitimacy in the eyes of society (Deegan, 2002; Velte et al., 2020). On the other hand, the expectation of stakeholders to be informed about carbon observe disclosure may result in increased organizational performance (Qian & Schaltegger, 2017). Therefore, researchers anticipate a favorable correlation between carbon disclosure and the firm's performance.

It was also observed that companies with superior environmental performance tend to present nonfinancial data as a means to substantiate their performance (Clarkson et al., 2008). Environmentally, carbon-efficient businesses are likely to have a lower cost of capital (Dhaliwal et al., 2011), high market worth, and more investors. Carbon performance is a part of how well a company does its job, and it can affect a company's finances by lowering risk or changing its job performance (Guthrie et al., 2009; Wasara & Ganda, 2019). Lueg et al. (2019) contend that transparency has a modest effect on financial performance given variations in permitted cash flows. However, increased openness to high-quality revelation minimizes the information gap between investors and therefore has financial ramifications in the form of reduced risk (Lueg et al., 2019; Velte et al., 2020).

There has been extensive academic study of the connection between carbon disclosure and financial performance (Alsaifi et al., 2020; Barnett & Salomon, 2006; Griffin et al., 2017; Hassan & Romilly, 2018; Velte et al., 2020). Despite contradictory findings, the majority of research has indicated a constructive correlation between environmental disclosure and financial performance. The favorable association has been attributed to innovation offsets exceeding the cost of compliance, strong management competencies, business credibility, and stakeholder aspirations (Alsaifi et al., 2020; Hassan & Romilly, 2018; Lee & Raschke, 2023; Velte et al., 2020; Wasara & Ganda, 2019).

Accounting academics generally would agree that by providing more information, a company might reduce its cost of capital that is at risk of incurring potential loss from the revelation of proprietary information (Consoni et al., 2017; Dye, 2001). The literature predicts that when more information about carbon emissions is released, the cost of capital will decrease since (uninformed) shareholders will confront less uncertainty and hence expect lower returns (Bolton & Kacperczyk, 2021; Bolton et al., 2022). Disclosure of carbon emissions incurs costs due to the need to track, measure, and aggregate emissions. In many small and medium-sized businesses, the fixed expenses of developing the systems that allow the company to consistently monitor and report its emissions may be incredibly expensive (Bolton & Kacperczyk, 2021).

There may also be indirect costs associated with disclosing carbon emissions, such as providing investors with a readily available variable around which to base exclusionary screening criteria and maybe garnering unwanted political attention. Further, (Bolton et al., 2022) mentions that carbon disclosure substantially reduces the cost of capital, as measured by the necessary stock returns of investors. This effect is pretty much completely attributable to unpredictable year-to-year fluctuations in reported emissions.

Increased financial disclosure increases investors' knowledge of a company's presence and expands its investor pool, which promotes risk-sharing and reduces the cost of capital. According to Peters & Romi (2014), carbon disclosure could have unintended repercussions, such as encouraging government agencies to inspect organizations, initiating costly litigation, providing competitors with evidence about firm-specific sustainability policies, and attracting potentially negative exposure from environmental activist groups. Consequently, the empirical aspect of how voluntary carbon disclosure affects a company's cost of capital remains uncertain.

Methodology

A structured systematic review is regarded as an excellent tool for determining the state of knowledge on a particular topic and identifying literature gaps to propose future research avenues (Khan et al., 2022; Niñerola et al., 2019; Nobanee et al., 2021. This article outlines the methodology of framework-based systematic literature reviews (Paul & Rosado-Serrano, 2019) followed in the study. The keyword selection process consists of five distinct phases: screening, collecting, organizing, writing, and lastly, presenting the findings (Dhamija & Bag, 2020). For the analysis of data, bibliometric analysis was used across several fields using VOSviewer and biblioshiny softwares, including organizational behavior, social science, environmental science, and communication, this methodology was used by Dr Bilal et al. (2021), Khan et al. (2022), Niñerola et al. (2019), Nobanee et al. (2021), and Rasul et al. (2022).

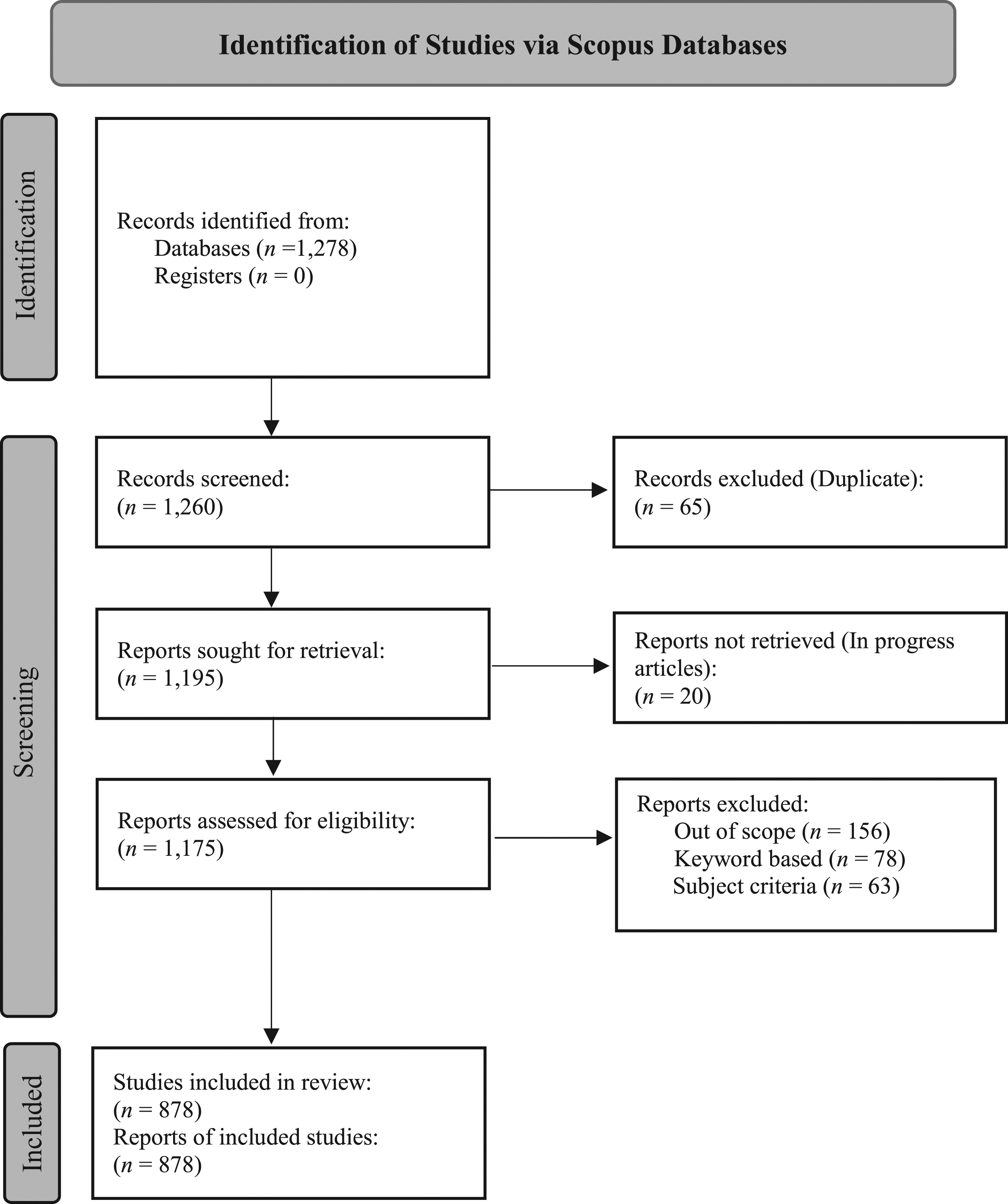

After determining the review technique, a list of relevant keywords was created from previously published research on carbon disclosure, organization performance, and cost of capital. Scopus, the well-known bibliographic database launched by Elsevier in November 2004, is a trustworthy database for academic publications with many effective tools (Lim et al., 2023; Nobanee et al., 2021; Rasul et al., 2022). The data in this study was extracted from the Scopus database, using the relevant keywords in English. The search resulted in the extraction of 1,278 documents, published between 2013 and 2022. (The search ended in January of 2023.) The evaluation was conducted with the PRISMA model (Figure 1) technique for the selection criteria. The abstracts of each document were reviewed to determine if they fell within the scope of the analysis, which was restricted to published articles. In the final retrieval, 878 documents were found to be within the scope of the database.

Database selection criteria using the PRISMA model

Analysis and Findings

RQ1: Research Publication Trend

RQ1 was designed to present insight into the publication frequency in the subject, consistent with prior bibliometric analyses (Nobanee et al., 2021; Rasul et al., 2022) that provide a clear overview of the research growth pattern in a certain research field.

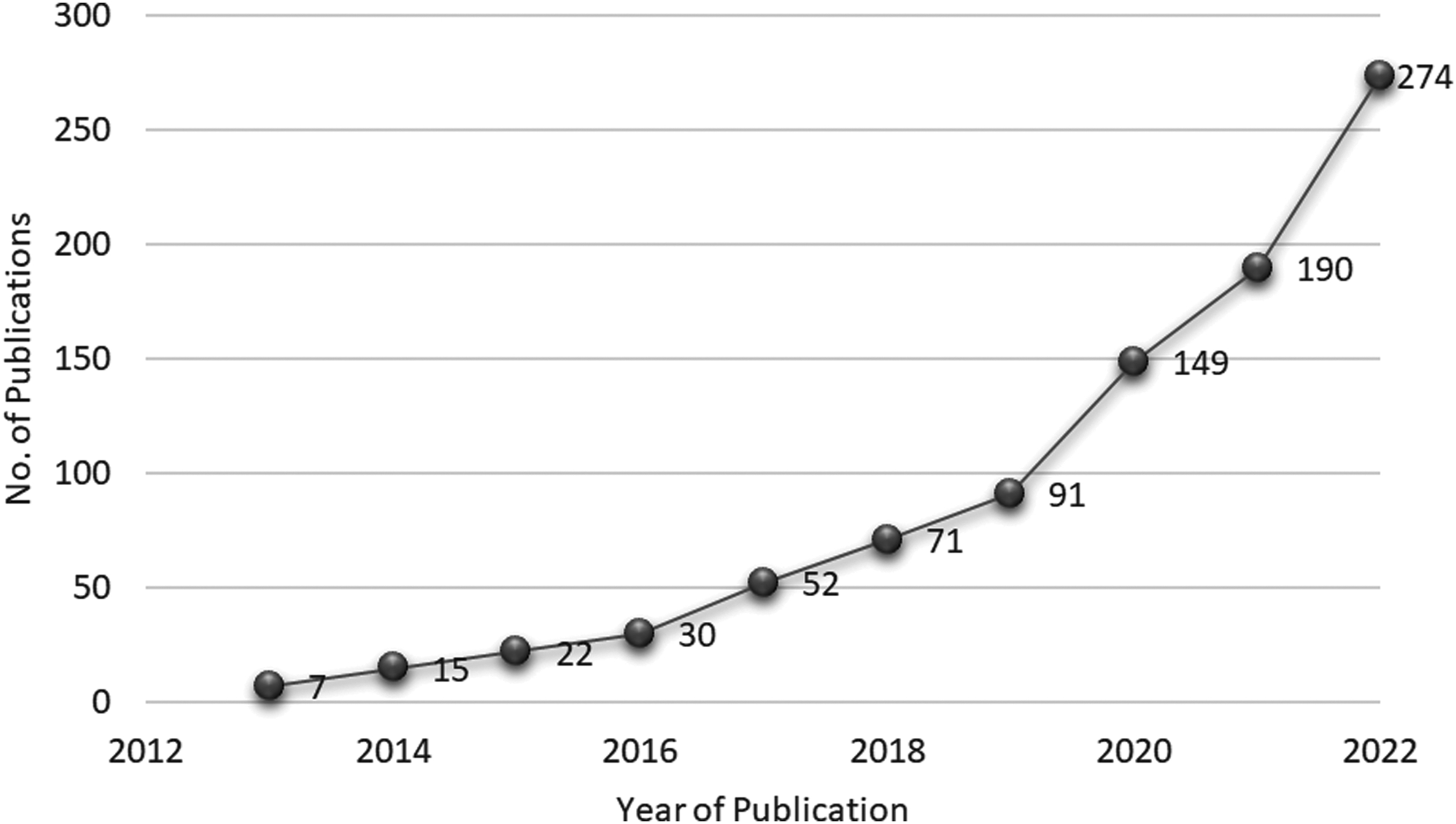

Multiple professions, including energy, engineering, economics, decision science, business management, environmental science, and social sciences, have performed research on carbon disclosure. Figure 2 illustrates the rising trend in the total number of documents published per year. In 2013, the document counts on carbon disclosure, cost of capital, and organization performance was seven, as indicated by the graph. The subsequent 15 articles were published in 2014. Since 2016, studies in this field have been steadily increasing year by year. As can be seen by the pattern depicted in Figure 2, research on carbon disclosure has evolved gradually, with a single-digit number of publications until 2013, followed by an exponential growth to a final total of 274 papers in 2022. Work on carbon disclosure has maintained consistent growth during its formative years.

Publication trend of carbon disclosure, cost of capital, and organization performance (bibliographic data as of December 2022)

RQ2: Countries, and Institutions with the Highest Levels of Productivity

RQ2 aimed to determine the nations that are most productive in their carbon disclosure, cost of capital, and organization performance research. Such analysis is a crucial component of any bibliometric review as it enables readers to identify the countries, or territories, and institutions that have influenced the research agenda. This analysis is standard for the vast majority of bibliometric studies (Dhamija & Bag, 2020; Donthu et al., 2021; Khan et al., 2022; Lim et al., 2022, 2023; Meseguer-Sánchez et al., 2020; Rasul et al., 2022; Tunger & Eulerich, 2018; Zhang et al., 2022).

Table 1 displays the 10 countries that have published the most papers on carbon disclosure, cost of capital, and organization performance. The data reveals that China ranks highest in the number of authors of carbon disclosure, cost of capital, and organization performance publications (215), followed by Australia and the United States with 133 and 120 publications, respectively. The majority of the countries on the list are also among the most economically developed nations. Italy, Spain, France, Canada, Germany, and Malaysia have a significantly lower publication rate than the top four nations. China's dominance in the field of publications can be attributed to several factors: 1.) China is the world's greatest emitter of greenhouse gases, and addressing carbon emissions has become a significant priority for the country (Li et al., 2017); 2.) To reduce carbon emissions and promote sustainable development, the Chinese government has established several laws and regulations (He et al., 2013); and 3.) This increased emphasis on carbon reduction has sparked academic interest in understanding and evaluating the effectiveness of these initiatives, including carbon disclosure.

Top 10 Productive Countries

RQ3: Most Influential Publications and Outlets

RQ3 aimed to conduct a performance analysis of carbon disclosure, cost of capital, and organization performance research utilizing the most significant publications and outlets as measures. This analysis is a crucial aspect of bibliometric studies, as the indicators provide an analytical framework for examining a particular research field and are considered equal to the participant profile in empirical research (Donthu et al., 2021). The 10 most significant works on carbon disclosure, cost of capital, and organization performance based on the number of citations received within the Scopus database are presented in Table 2.

Top Publication for Carbon Disclosures, Cost of Capital, and Organization Performance

The study with the most citations (535) related to gender diversity, board independence, environmental committee, and greenhouse gas disclosure (Liao et al., 2015) introduced the concept of carbon disclosure as a study construct. The authors developed the concept of carbon disclosure and examined the impact of diverse sub-variables, including gender diversity, board independence, and environmental committee. Matsumura et al. (2014) looked into the consequences of carbon emissions and carbon disclosure on firm value. The authors used carbon emissions data from 2006 to 2008 that S&P firms voluntarily reported to the carbon disclosure initiative.

An in-depth examination of the most frequently cited publication on carbon disclosure, cost of capital, and organizational performance reveals comprehensive coverage of multiple perspectives. These include board gender diversity (Ben-Amar et al., 2017), firm performance (Matsumura et al., 2013; Plumlee et al., 2015), supply chain (Ghosh & Shah, 2015), green innovation (Li et al., 2017), and corporate governance (Ben-Amar et al., 2017; Liao et al., 2015).

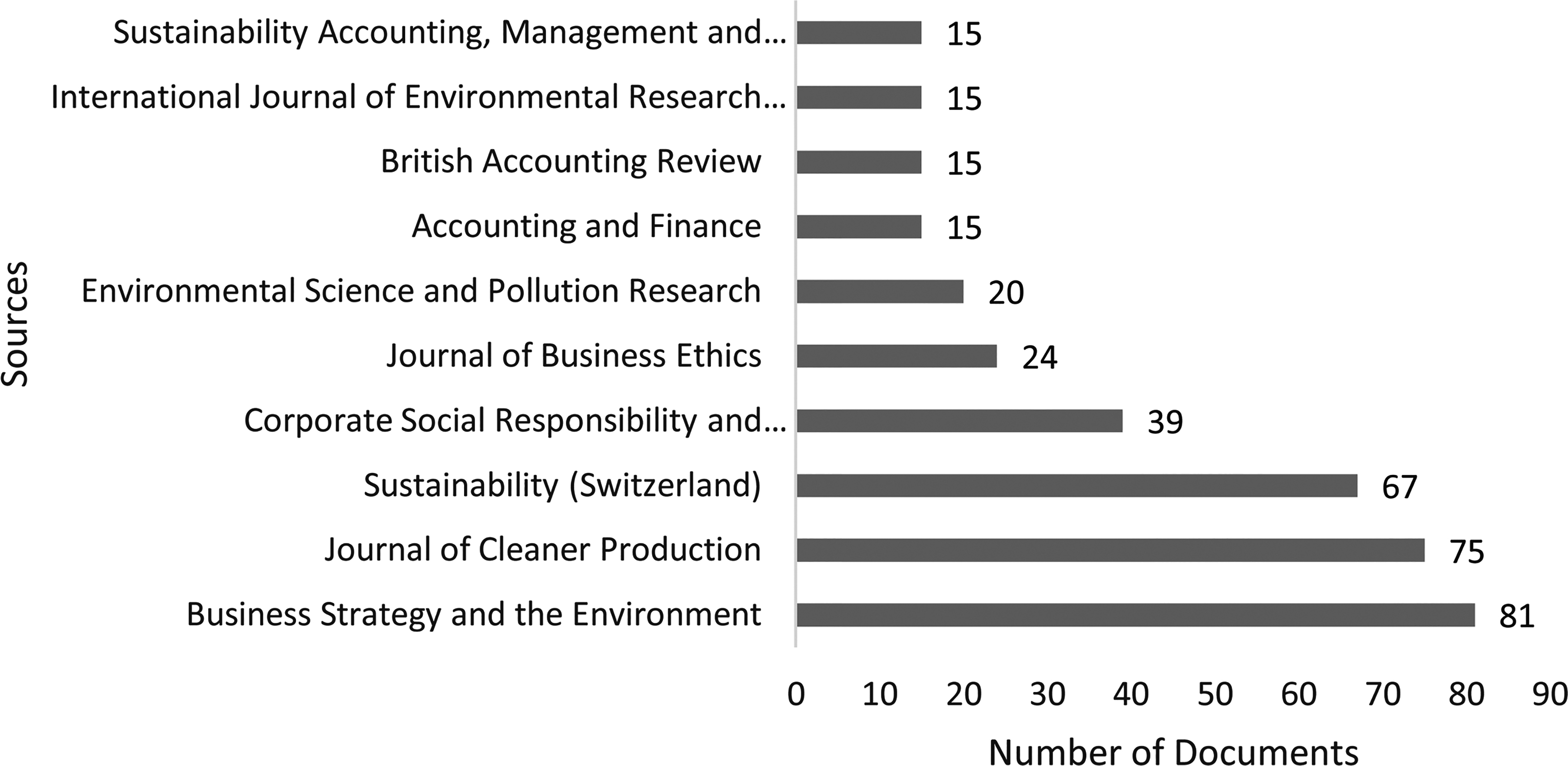

Figure 3 graphs the position of journals based on the number of articles on carbon disclosure, cost of capital, and organization performance. Based on this criteria, the journals named in the figure are the top 10 journals in the field of carbon disclosure-related studies. Business Strategy and the Environment contains the most articles in the field—81—followed by the Journal of Cleaner Production with 75. On the low end, Accounting and Finance, British Accounting Review, International Journal of Environmental Research and Public Health, and Sustainability Accounting, Management, and Policy Journal each have 15 articles. This analysis indicates the journal with the greatest potential for publication on this topic, which can facilitate future scholars in selecting the appropriate journal for their publications in the same domain.

Most influential outlets/journal in the field of carbon disclosures, cost of capital, and organization performance

RQ4: Knowledge Structure of Carbon Disclosure Research: Keyword Co-Occurrence Network

Following the trajectory of prior research (Agarwal et al., 2023; Donthu et al., 2021; Lim et al., 2023; Rasul et al., 2022), RQ4 aims to perform a co-occurrence analysis of keywords and create a network analysis or visualization of keyword co-occurrence. This analysis also attempts to ensure that an article's keywords adequately represent its content. When two keywords appear together in an article, demonstrating a relationship between the two concepts, this is known as keyword co-occurrence. To comprehend the knowledge structure of the field, a co-occurrence analysis begins by using the authors' keywords for the document, as proposed by (Callon et al., 1983), and then is followed by network analysis or visualization of keyword co-occurrences, as co-appearing keywords are believed to indicate a certain level of theme convergence (Callon et al., 1983).

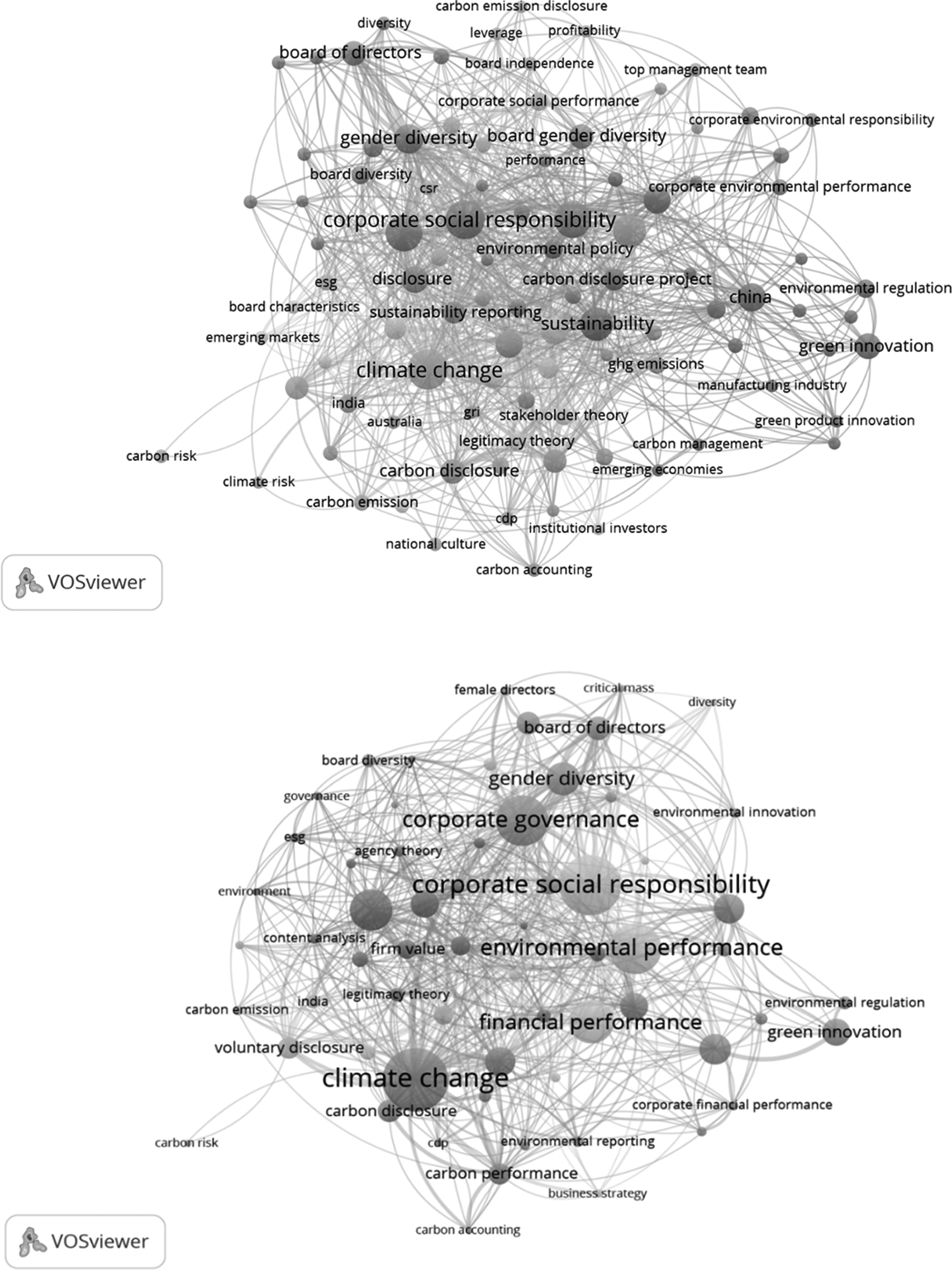

In bibliometric studies, authors typically utilize co-occurrence analysis with keywords to find the subjects and themes that form the foundation of their research field (Assefa & Rorissa, 2013). Networks of co-occurring keywords that are partitioned into clusters could provide insight into the common issues and ideas that underpin the varied aspects of research on a given topic. From the dataset, author keywords with at least five occurrences were selected. There were 126 such keywords, which constituted a co-occurrence network of distinct clusters, each expressing a common subject in the literature.

The keyword co-occurrence network contains 10 clusters that represent themes in the carbon disclosure, cost of capital, and organization performance literature, but only five highly significant clusters were selected for further discussion. Table 3 displays the keywords connected with each cluster (theme). Figure 4 shows the network graphs for the keyword co-occurrence, which has a total of 10 clusters. Each node in these networks symbolizes a key term (the larger the node, the more keyword co-occurrences) (Donthu et al., 2021), and the links between nodes represent the frequency with which keywords co-occur (the thickness of the links denotes the degree of commonality between the keywords they connect).

Keyword co-occurrence

Authors' Keywords Cluster

Table 4 shows that climate change is the most commonly used keyword in carbon disclosure literature. This makes sense given that carbon disclosure is centered on an organization's capacity to mitigate climate change and is part of its corporate social responsibility. Additionally, corporate social responsibility has developed as a prominent topic in the literature. Climate change and environmental performance are the most prominent nodes in the network, indicating their relative importance in the field of climate change and sustainability, as depicted in Figure 4.

Frequency of Keyword Occurrence

Further, Table 4 organizes the keywords from Figure 4 according to their frequency, with each cluster containing interconnected keywords that pertain to the specific node. Table 4 indicates that climate change and corporate social responsibility co-occur most frequently. Another developing concern is environmental performance and firm performance, which is by far the most studied topic in carbon disclosure research. The diverse occurrence of keywords indicates that scholars have demonstrated a great deal of interest in this topic; they have also studied the many facets of carbon disclosure, including corporate governance, environmental performance, company performance, and sustainability. This conclusion shows that academics have paid less attention to other dimensions of sustainability, such as; environmental management systems, greenwashing, stakeholders, climate risk, and innovation. As a result, future researchers have the opportunity to explore these keywords.

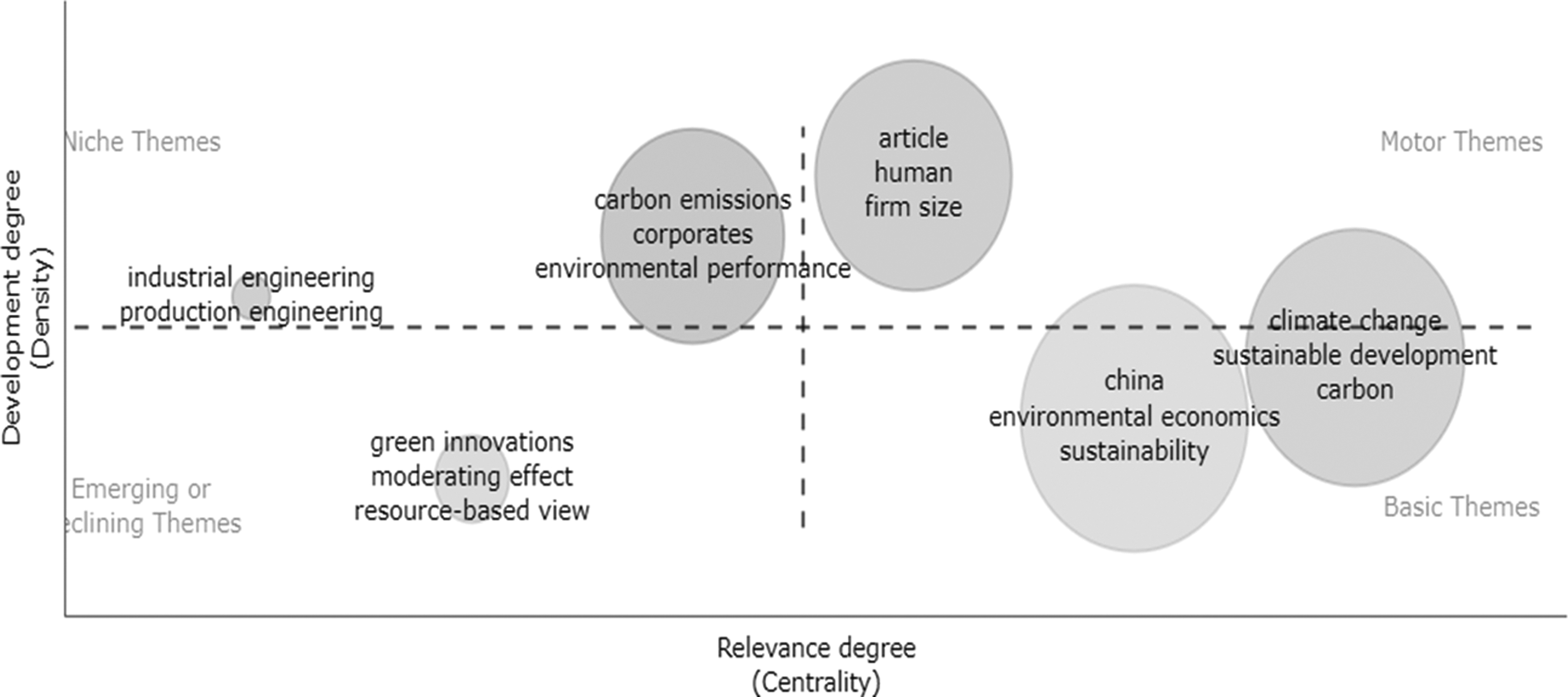

Thematic Map Analysis

The thematic map shown in Figure 5 is provided to help obtain a deeper understanding of the current state of a particular field and to forecast its potential for long-term sustainability. The map was constructed utilizing a technique that includes a review of the keywords of all references analyzed in this study, as well as other applicable key phrases (in addition to the authors' key terms), to identify variants with greater detail. This type of examination can be valuable in imparting knowledge to researchers and stakeholders concerning the possibilities for future research advancements in thematic areas within a field. This analysis can aid all future academics in identifying prospective themes or research domains.

Thematic map of the research illustrating the topic's evolution and significance using biblioshiny software

To derive themes, the thematic analysis examined groups of authors' keywords and their links, which are classified based on characteristics such as density and centrality. Centrality refers to the extent of association between various topics, while density gauges the coherence among the nodes. These two characteristics evaluate the significance and strength of specific topics. Nodes with a greater number of connections in the thematic network possess higher centrality and importance, placing them in critical positions within the network. Similarly, the cohesiveness of a node, indicated by the density of a research field, determines its potential to grow and maintain itself over time.

The upper right quadrant of Figure 5 comprises motor themes or driving themes; these are themes with a high keyword density and significance, firm size, and human effect. As shown in the diagram, the theme of climate change, situated between quadrant 1 and quadrant 4, is significantly developed and possesses the potential to organize and shape the research field. In other words, climate change continues to be the predominant theme in the field. The basic themes (quadrant 4) have the most potential because these issues are highly significant yet are not rigorously investigated. Thus, future academics will be able to focus their research on these terms. This quadrant includes the themes of sustainable development, environmental economics, China, climate change and sustainability. Quadrant 3 (bottom left) contains topics that have been employed but their popularity has dropped, as shown by low centrality and density. This section features items such as green innovation, resource based views, and moderating effects.

Discussion

This bibliometric assessment offers an impartial and retrospective overview of the body of literature concerning carbon disclosure, cost of capital, and organizational performance. The analysis of keyword co-occurrence and the visual representation of networks, as demonstrated in this review, can serve as a valuable tool for understanding the interconnectedness of selected keywords. This study includes a thematic map analysis to help determine the significance and density of keywords for further research. Thus, the study addresses the first four research questions and offers the following significant findings.

Research on carbon disclosure, cost of capital, and organization performance has increased significantly since 2013 when there were just seven articles, followed by a gradual increase to over 274 papers in 2022 (RQ1). In terms of carbon disclosure, cost of capital, and organization performance research, China and Australia were the nations with the most publications (Table 1) Business Strategy and the Environment was the preferred venue for carbon disclosure, cost of capital, and organization performance-related publications, followed by the Journal of Cleaner Production (RQ3) (Figure 3). The groundbreaking research conducted by on carbon disclosure, cost of capital, and organizational performance continues to be the most note-worthy publication in the field, with the article by Ghosh & Shah (2015) following closely behind. The cognitive structure of the research on carbon disclosure, cost of capital, and organization performance, which was reconstructed using keyword co-occurrence analysis, reveals five large clusters (themes) (Figure 4).

To get an understanding of existing research, an in-depth review of the most-cited publications and the leading publications from each cluster of the keyword co-occurrence network was undertaken for this study. Almost every article reviewed on carbon disclosure, cost of capital, and organization performance emphasizes the necessity for sustainable environmental development and the impact of these issues on organization performance and corporate governance. Thus, these issues remain an area of study needs. In addition, the data suggest that the concept has not yet been investigated within a cohesive theoretical framework; thus additional study is recommended.

This study also suggests that scholars in the fields of business, management and accounting, and environmental sciences are more likely to include keywords such as carbon disclosure, cost of capital, and organization performance. In addition, carbon disclosure has frequently been discussed in the context of its causes and consequences, with an emphasis on its intentions. The concept has grown over time, and with it an greater understanding of carbon disclosure practices. A comprehensive review of the literature published in both fields found that management science articles focus on carbon disclosure in the context of the organization's performance, its impact on the cost of capital of the organization, and how the the effects of disclosure unfold for stakeholders.

The review was also found that the majority of authors of articles on carbon disclosure, cost of capital, and organization performance are from China, Australia, and the United States; however, nations such as Italy, Spain, France, and Canada have seen significant growth in recent years. Furthermore, the analysis indicates that research on carbon disclosure and its effect on the cost of capital and organizational performance has increasingly evolved toward empirically explaining it from numerous perspectives, for example, firm-value effects of carbon disclosure (Matsumura et al., 2013); carbon performance, cost of capital, and indicators of carbon performance (He et al., 2013; Hoffmann & Busch, 2008); carbon accounting (Stechemesser & Guenther, 2012); and corporate carbon risk (Lemma et al., 2019).

Conclusion and Implications

The study of carbon disclosure, cost of capital, and organization performance have significantly increased in the last 10 years and has arguably become common practice. Organizations have recently been under increasing pressure from regulators to publish their carbon footprints, which can have a significant impact on their bottom line and reveal the quality of their corporate governance (Kumar, 2022; Peters & Romi, 2014; Sharif & Ming Lai, 2015).

This research has several significant contributions to the furtherance of this area of research: 1.) By evaluating the publication pattern in the fields of carbon disclosure, cost of capital, and organizational performance, this study provides valuable insights into the research trends and developments in these areas. This analysis helps understand the growth and evolution of research topics over the years. 2.) With the help of influential studies in this field, future scholars can gain a better understanding of the foundational research and build upon existing knowledge. 3.) The ranking of the most prominent journals in the subject area provides a guide for researchers to target reputable and impactful journals for publishing their own research. This ranking helps in optimizing the dissemination of research findings to a wider audience and enhances the visibility and credibility of the research. 4.) Cluster analysis (Table 3) and authors' keyword co-occurrence (Figure 4) can help identify trends, themes, and underutilized keywords for further exploration. 5.) Thematic analysis provides potential research avenues for the future to direct research in this field.

This study's findings reveal inconsistent disclosure of carbon footprint among both developing and developed countries. Considering an increased emphasis on curtailing corporate carbon emissions to achieve the goals of carbon neutrality, this is a wake-up call for policy makers to come up with a uniform standard and framework for carbon emission disclosure. Carbon emission disclosure practices need to be implemented across the organization, irrespective of its size. This study can serve as a valuable resource for academics, journal editors, and corporate consultants by providing a comprehensive understanding of various aspects of carbon disclosure research and the potential emerging research area of the field.

Nevertheless, this study has some shortcomings. The bibliometric data utilized to produce the findings and evaluation of this research is limited to the Scopus database, which is subject to modification as new research on carbon reporting emerges. The citation and co-citation numbers of the publications already present in the dataset of this study might be impacted and lead to fluctuation in the ranking of new publications. The search terms employed in this study were carbon disclosure, cost of capital, and organizational performance. Hence, future researchers have the opportunity to incorporate additional relevant keywords to broaden the scope of their research.

Footnotes

Funding Information

No funding was received for this study.

Author Disclosure Statement

No competing financial interests exist.