Abstract

Abstract

Disruptive trends in mobile wireless computing can be useful for anticipating and forecasting future directions and behaviors in the small satellite marketplace by examining historical measures and corollaries between these marketplaces in an effort to develop more accurate forecasting and assist regulators, policy experts, and stakeholders in planning and strategy.

Anticipating the Future of the Smallsat Market Can Help Avoid Missteps

Smallsats are entering a new historical period of not only augmenting functions previously performed by larger satellites but also entering into a realm of their own in creating new networks, products, and service offerings. Their importance to the future of space communications, augmentation of terrestrial broadband, sensing, monitoring, and communicating is rapidly escalating. Success is bringing with it substantial investment capital, but also the potential burdens of regulatory impacts, stabilization in manufacturing costs, and other factors that can weigh heavily as market pressures set in.

To better understand how the smallsat market might develop within the context of commercial space, it is relevant to look at disruptions in similar markets, such as commercial mobile wireless computing. By exploring the relationship between the commercial mobile wireless computing market and the commercial smallsat market, we may be better able to anticipate possible future paths for the small satellite market in viewing it through the lens of disruptive trends. 1 These disruptive trends include (1) disruption through network behavior, (2) disruption through product evolution, (3) disruption through human behavior, and (4) disruption through price.

Long before small satellites emerged as a viable business model, telecommunications and computing went through similar market evolutions. Understanding disruptive tendencies in other markets can be helpful to anticipate future events in the small satellite industry and broader satellite marketplace. However, it requires an appreciation for disruptions, how they occur, and how markets are moved and shaped. By understanding these trends and their pace of development, stakeholders may be better able to contribute to a healthy small satellite market.

Disruptions Can Happen Through Network Behavior

Disruptions occur across the technology spectrum and can emanate from network behavior. 2 Terrestrial networks have segmented, become meshed, and now extend into space, creating a new reordering of the networked and mobile computing universe that is continually morphing to meet consumer demands. Small satellites can be thought of as “nodes on a network” in the context of past and future network development. In this sense, they are simply another part of extending the network in a data-centric world as terrestrial telecom networks extend into LEO, MEO, and GEO.

Today we have many of the problems in network capacity that we had 2 decades ago. In the late 1990s, terrestrial telecom networks were a coagulated mix of heavy duty switching equipment, servers, and hardware connected to expensive computers. In many ways, global network infrastructure today, both terrestrial and in space, has many of the same challenges it had in the late 1990s, including limitations on data throughput and the resultant bandwidth bottlenecks. 3 In 1997, David Isenberg, a researcher at AT&T wrote an essay entitled “Rise of the Stupid Network.” 4 In Isenberg's essay, he postulated that a telecommunications network that is made up of bits and bytes is not only unintelligent but also nothing more than a conduit made redundant by the Internet protocol technology planners, over the years, to move data traffic, have had to load balance between end-user devices and network capacity.

The question over how to allocate data between the network and devices touched off a debate. This debate is noteworthy and relevant to small satellites because their lower cost structure now makes them a candidate for mobile wireless backhaul. A network can tell a story. It is about us, how we communicate and interact with each other. It can also telegraph how we might interact with each other in the future. Moore's Law has continued to play out in smarter computing devices, such as mobile phones, cloud computing, and network-based storage. 5 What we learned from Isenberg's passionate essay is to question the function and purpose of networking as we look into the future by looking for disruptions and nonlinear paths for technological adaptation and progression. Understanding how terrestrial telecommunication networks have evolved and anticipating future evolution can help us better anticipate how the small satellite market may mature. Although networks did undergo a “dumb” phase, the past 20 years have presented slightly different scenarios as data packets, packed with voice, were delivered to smart computing devices at the other end of the network, leading to segmentation between networking and computing providers in the early 2000s.

As terabyte size computing, massive data storage requirements, and hosting applications in the cloud have become in vogue, the cloud-based network has become the “brain” where everything resides, and less smart devices can park data. As data growth has supersized and moved through terabyte, petabyte, and is rapidly approaching zetabyte growth, as we move toward 2025, the interaction between network and end-user devices has become a load-balancing act while staging an encore performance for cloud computing.

Disruptions Can Happen Through Product Evolution

Watching for disruptions in product evolution can be a guideline for anticipatory paths, in particular market segments, including mobile wireless computing and satellites. The futurist Graham Molitor spent more than 40 years analyzing trends and characterizing technological and social change. Molitor pointed out that time lines between discovery, lag time, and acceptance of technology appear to create S-curves, and these S-curves continue in cycles repeating throughout industries. 6 Some aspects of Molitor's work included anticipating when disruptions might occur and analyzing their relationship with past and future events in an effort to forecast future implications and impact. Table 1 depicts the life cycles across mobile wireless computing and how product differentiation and market segmentation occur as product evolution takes place.

Market Segmentation in Mobile Wireless Computing—M.K.R., 2016

Small satellites like cell phones and computers appear to be evolving.

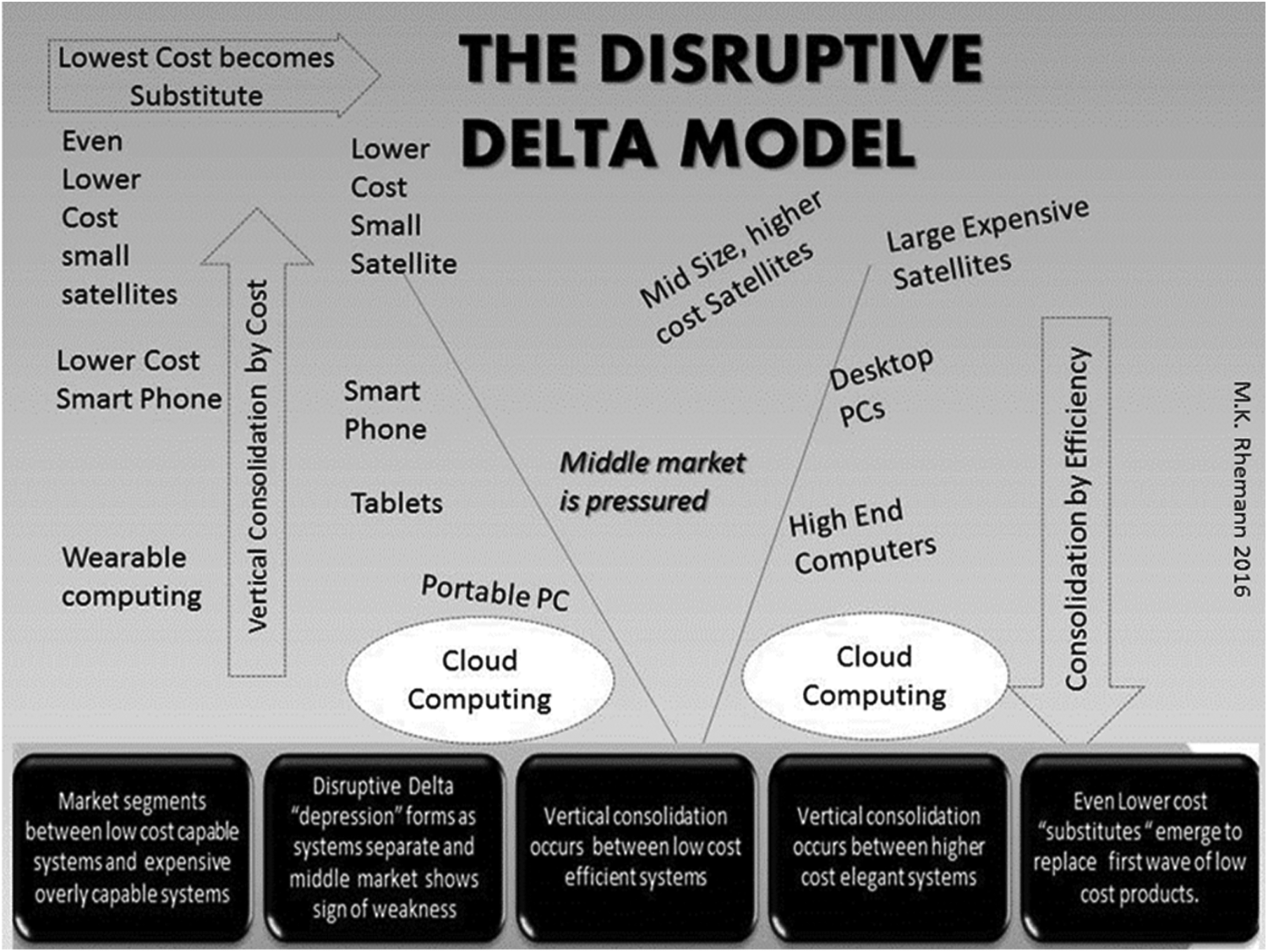

The small satellite market, having gained momentum in the past decade, is relatively new, and its market trajectory is still a work in progress. Satellites appear to be following a path similar to other technology products, in which they were developed as highly specialized, costly, and unique solutions. “The Disruptive Delta Model” shown in Figure 1 is named for points in the market where subtle differences are detected. 7

Rhemann: Disruptive delta model, 2016.

(1) The market begins to segment between low-cost, capable systems and expensive overly capable systems. This has been observable through portable PCs breaking away from desktops and higher end computers in the computing market. In the satellite market, it is evident between smaller imaging satellites and larger previous generation imaging satellites, with the same to be true in communications and broadband.

(2) Disruptive Delta depression forms as systems separate, and the middle market shows signs of weakness.

(3) Vertical consolidation occurs between low-cost efficient systems. This has been evident in mobile computing, in which, with increased computing power, longer battery life, and better LCD displays, device consolidation is taking place between notebooks, tablets, and mobile phones, as consumers try to choose their preferred device.

(4) Vertical consolidation also takes place between high-cost elegant systems. Larger computing systems have morphed into cloud computing environments to drive efficiencies. This is evidenced by manufacturers of high-end computers and servers, such as IBM, HP, and EMC, moving into the cloud computing space.

(5) Even lower cost “substitutes” emerge to replace the first wave of low-cost products. In the mobile computing environment, this is evidenced by lower price manufacturers such as Lenovo, a PC manufacturer, moving into the mobile phone segment to compete with Samsung, and mobile computing manufacturers moving into the cloud space.

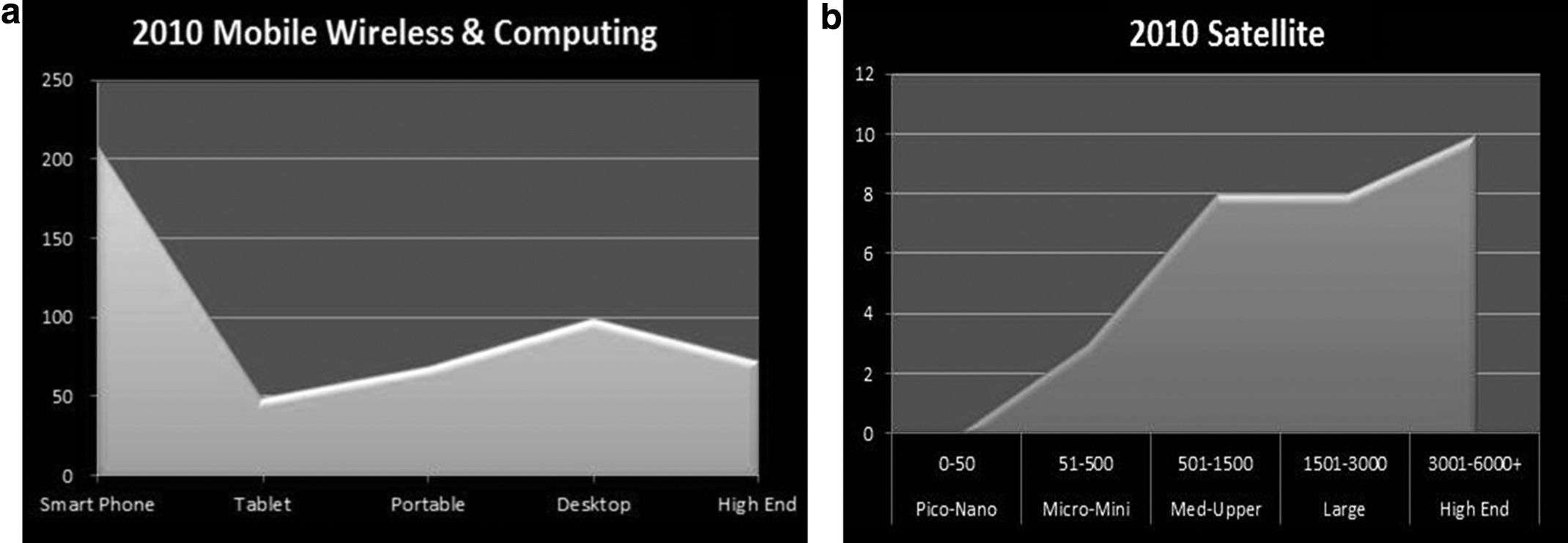

In Figure 2a, we can see the Delta curves form in the mobile wireless and computing sector trends from 2010. 8 In Figure 2b, we can see the beginning of the commercial satellite market shifting between smaller more utility systems and larger more elegant systems. 9 Satellites seem to be following a path similar to the mobile wireless computing market. Whereas 20 years ago, roughly 88% of satellites were more than 1,800 kg, the end of the 1990s ended with the bankruptcy of Iridium, the demise of funding for Teledesic and cancellation of more than 10 other small satellite programs slated to be less than 500 kg that were on the drawing board at the time. 10 In version “2.0” of the small satellite market, we can see more solid trends emerge that seem to bode well for market longevity.

However, by looking at other similar markets and focusing on disruptive trends that can anticipate how markets move, we may also anticipate potential future outcomes for the small satellite market. Small satellites and mobile phones continue to have more in common with one another. In 2013, NASA launched a CubeSat as part of its PhoneSat mission using a Samsung Nexus smart phone for processing and utilizing an Android operating system. 11 These markets have continued to follow similar paths, as those paved by the server and PC market that preceded them.

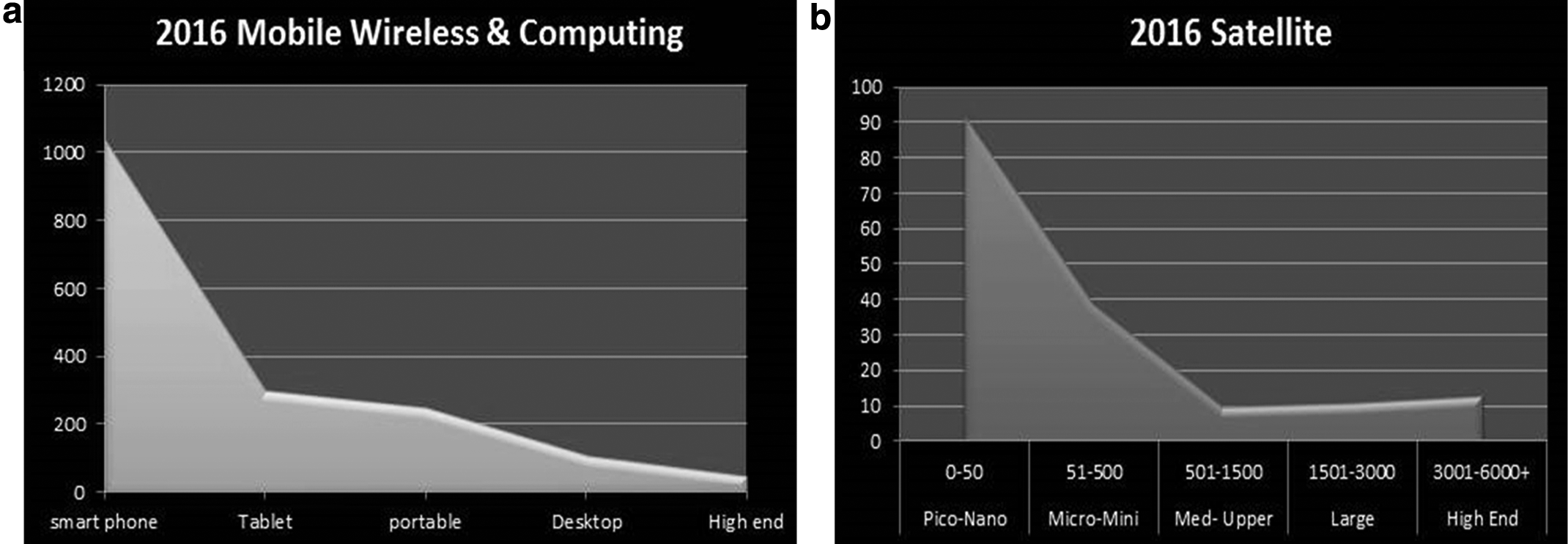

In Figure 3a, we can see the continued shift in the mobile wireless market, where smart phone use continues to outpace other products. 12 In Figure 3b, we can see the smaller end of the commercial small satellite market developing in a similar manner and infer that the small satellite market seems to be following the path of the mobile wireless and computing market in many ways. 13 The similarities between markets cut across size, features, and market adoption. A natural growth path continues to emerge between systems in which the market separates between more robust and featureful systems and lower end systems. In 2005, there were only 83 million smartphones engaged globally. As of 2016, that number will be closer to 1.4 billion. 14 In the mobile phone market, the past decade saw a pronounced separation in systems from featureful systems that were highly priced to less featureful commoditized versions. Slowly, over the past decade, more featureful, higher priced systems, such as Samsung, the global market leader, are rapidly being challenged by lower cost producers such as Lenovo, which has moved from low-cost computers to the smart phone space. As price pressures have increased, technology life cycles have quickened, and lower priced competition has been able to replicate more features for a lower cost.

The miniaturization of chips, radio transmitter, receivers, coupled with advanced processing power, has enabled the evolution of smaller electronic devices, resulting in market segmentation as specialization emerges. 15 This trend has matured across every aspect of computing and electronic devices, including computers, servers, mobile phones, and satellites, bringing with it progressively advanced capabilities. It has also become a theatric stage for observers to view Michael Porter's theory of substitutes play out. 16

The evolution of small satellites has not been so different than the evolution of any other electronics product or supply chain, such as computers, servers, or mobile phones, and small satellites are afforded no special dispensation simply because they have evolved from elegant systems to lower cost, less complex systems comprising “off the shelf” parts. Technology evolution in electronic and technology products tends to follow common patterns. 17 In fact the market is moving, in many ways, much like the computing and telecommunications markets have.

Disruption Can Happen Through Human Behavior

In trying to anticipate disruptions, human behavior may not only be the most important but also the most unpredictable. Networks are built based on how humans communicate, and markets are built based on how masses of humans manage to channel their preferences. My firm was involved in research in the late 1990s that showed 80% of people only utilized 20% of the features across mobile wireless and ground-based networks. This research was a disruptive realization in that telecom infrastructure companies were spending billions in upgrading fiber and cable while not paying attention to end-user adoption rates. Although the discovery of better software methods to organize packetized data for delivering video was ground breaking at the time, widespread adoption of fixed and mobile videos has been staggered in terms of technological progress and human adoption. It was evident early on that the fiber buildouts of the late 1990s would end badly, as they did, with mass bankruptcies in the telecom fiber business. More than 2 decades later, not only are consumers making maximum use of telecommunications features, but they are also becoming demanding and creative in their preferences. 18

By 2025, Microsoft estimates 4.7 billion people on our planet will become globally connected citizens. 19 That has changed how we think about technology and how we use and deploy it.

In 2020, more than 58% of wireless bandwidth will be devoted to mobile video, and roughly 12% devoted to social networking, and by 2025 mobile video utilization is likely to climb to 70% and social networking 16%. 20 The forecasted increase is primarily because of mobile conferencing, enabling automotive apps, and growth in mobile advertising, which has been gaining increasing market share. These increases in data growth are anticipated to have an order of magnitude increase every 5 years, resulting in zetabyte data growth in the upcoming decade. 21 The acceleration of efforts to connect more humans to the Internet through mobile devices is likely to increase because a 10% growth in broadband translates to a 1% increase in GDP. 22

Disruption Can Happen Through Pricing

Both mobile computing and small satellites have seen costs come down by more than an order of magnitude and capabilities rise disproportionately with cost. Business models can often be more disruptive than technology. For example, in 1998, AT&T introduced its “One Rate Plan” in the United States, offering a single monthly rate for set groupings of services and replacing the “per minute” charges that mobile phone companies had traditionally offered. 23 Almost overnight, airport phone booths were vacated, forever changing the industry business model and change in pricing strategy. Like mobile phones and computing, small satellites have now reached a price point that makes them accessible for replacing existing services at a lower cost. These services continue to increase and include but are not limited to imaging, broadband, messaging, tracking, navigation, and future services that remain on drawing boards. In the case of broadband small satellites in which pricing may be less than $1.5 million for a <150 kg satellite and launch, the order of magnitude reduction in price versus previous decades is indicative of market disruption, in which a given price point opens the floodgates for substitute products and market consolidation.

As small satellites have become affordable, they offer a newer solution for providing broadband and wireless backhaul services. As mobile wireless networks morph into meshed networks that rapidly become mobile wireless 4G/5G/6G networks, future networks are likely to become ubiquitous mobile networks that connect mobile users to LEO, MEO, and GEO constellations. This trend is rapidly being witnessed in observing investments between satellite operators, such as the acquisition of O3B by SES, and mobile operator Bharti Airtel's investment in the satellite broadband startup OneWeb. 24

Conclusion

The small satellite market has tendencies similar to the computing market and specifically the mobile wireless computing market, including portable computers, tablets, and mobile phones. As products progress across their life cycle, product differentiation and pricing reductions occur. Products often segment between high and low capabilities and high and low pricing, developing a “Disruptive Delta-Curve” as less essential products slide toward the middle and slide into a chasm.

The movement of the mobile computing market is a useful barometer of potential future disruptions in the small satellite market. As products become commodities, they are more vulnerable to substitutes or are more likely to be integrated into a larger supply chain or integrated product offering. As this happens, these products may become more sensitive to market conditions and pricing. It is not immediately clear how low-cost small satellites might become or how far down the path of miniaturization smallsats may go. What is becoming clearer (if business models hold) is that smallsats may soon enter a phase of global price sensitivity as a direct proportion to their future services, such as broadband and imaging, as they move toward a commoditized service delivery model. Next generation business models beyond 2025, when services become more competitive, may require tightening of the value chain to relieve cost pressures on labor and production.

In creating a healthy small satellite environment where satellites less than 500 kg can thrive, stakeholders, including policy makers and regulators, must bear in mind the sensitivity of this market to cost, policy, and price pressures. “Substitute” products, such as lower cost satellites, may be replaced with “even lower cost” satellites, leading to an environment where even slight regulatory activities can have massive implications for such a fragile and sensitive market.

Footnotes

Author Disclosure Statement

No competing financial interests exist.