Abstract

Abstract

The U.S. federal government has acknowledged the importance of having a robust domestic space launch industry since the 1980s for national military, civil, and commercial purposes. Since then, many policies have been structured to promote the growth of the industry. Due to these efforts, as well as other macroeconomic and external market factors, the U.S. launch industry is in a period of expansion. In 2006, one company existed in the market to serve the government's launch needs. In 2012, the number of companies grew to 3. The industry is looking to have 12 independent companies with the capability to launch payloads to low-Earth orbit by year 2020. In the midst of the growth in supplies, this research article aims to alert the readers that such an expansion closely resembles a speculative economic bubble and the government should be concerned. This is first achieved by examining a set of unique characteristics of the commercial launch industry that create uncertainty and risks. Second, the current commercial launch market is applied to Robert Schiller's model of a speculative economic bubble. Third, a comparative analysis between the Telecom bubble, the Dot-com bubble, and the U.S. launch industry is conducted to explain the similarities between the 3. Finally, the research article concludes with what the bubble means to the United States and why the government should intervene with recommendations to support the stability of the launch industry. The scope of this thesis is solely in regard to the U.S. launch market and launch vehicles.

Introduction

The commercial launch industry began to see a significant inflow of new companies in the 21st century. Previously, only 3 companies, Orbital Sciences Corporation, Lockheed Corporation, and The Boeing Company existed in the market. In the 2000s, numerous new companies, such as Space Exploration Technologies Corporation (SpaceX), Virgin Galactic, Blue Origin, XCOR, and Rocket Lab, entered the industry with the goal of providing low-cost access to space. The Federal Aviation Administration (FAA) now projects 12 companies with the capability to provide orbital launch services in the United States by 2020.1,*

The industry is experiencing an expansion in every dimension. Government policies are supporting the growth of the industry, financial investments are coming in to the industry from new sources and in unprecedented amounts, and new technologies are being developed to create better and cost-efficient vehicles. However, of the 12 projected companies, only 3 have proven their technological capability and are currently operating. The other 9 have not yet been successful at producing an operable launch vehicle. Some of these companies have been around for a decade.

The major concern explored throughout this article is that such an expedited expansion of the industry is not the best direction toward sustainability and stability. Based on macroeconomics law of supply and demand, a sudden increase in the supply of launch vehicles without the suitable demand can be detrimental to the industry. If the industry is not able to achieve a sustainable growth and become a stable market operating under healthy competition, it is likely to run in to a contraction. In such a case, the industry will again collapse and be left with 1 or 2 companies, as was the case in the early 2000s. As further explained in the History section, several companies went through a series of mergers and acquisitions to become one company at the end. A small number of companies mean limited industrial capacity, which is the opposite of what the U.S. government is trying to achieve based on the series of national space policies since the 1990s.

The government has decided to rely on the private sector for access to space. Manufacturing and operation of launch vehicles for low-Earth orbit have been directed away from the government based on the belief that a robust commercial launch industry can lead to a significant decrease in the cost of access to space through market competition. However, the launch industry is not a business that should be left to a pure market supply and demand system, because the government heavily depends on it for access to space and the market itself is not self-sustainable. For this industry to achieve sustainable long-term growth, proper government support through subsidies and stable demand have to be coupled with prudent investment decisions based on objective market analysis, not based on optimism and hope. However, the current market environment does not reflect these characteristics.

This article explains how the commercial launch industry is currently unstable and how it exhibits the characteristics of a speculative bubble by exploring the following areas:

History of the commercial launch industry. Characteristics of the commercial launch industry that contribute to the unique risks and uncertainties. Speculative bubble and the commercial launch industry. Comparative analysis of previous speculative bubbles and the commercial launch industry.

After exploring these areas, it aims to provide a set of policy recommendations to adequately support the growing industry that is vital to the federal government. This article should not be considered as an opposition to the growth of the commercial launch industry as the robust industry must exist for the commercial, civil, and military development of space for the United States. The purpose of this article is to provide a conservative warning about the outlook of the industry and advocate for an incremental approach to lead the industry to long-term sustainability, so that the nation can continue to lead the world in space endeavors.

History

The U.S. commercial launch industry has been a part of the United States access to space since the 1950s, at the burgeoning height of the Cold War. The 3 prominent launch vehicles of the early days, Atlas, Delta, and Titan, were expendable launch vehicles (ELVs) manufactured by private corporations under the contracts of the U.S. federal government (henceforth, the government). Derivations of these rockets are still currently being used. The commercial industry also contributed significantly in the making of the national vehicles, as well. The Saturn V, famously known for the Apollo missions, had 3 stages that were manufactured by 3 different companies. The 3 major parts of the Space Shuttle, which are the solid rocket boosters, the external tanks, and the orbiters, were all manufactured by different companies as well.

With the completion of the Apollo program in 1975, the U.S. government directed its efforts to develop a reusable launch vehicle, namely the Space Shuttle. With this program, the government was to expand its portfolio of space launch vehicles: the ELVs from the commercial industry and the reusable launch vehicles from the fleet of the Space Shuttle program. 2 However, the Reagan administration in 1982, through the National Security Decision Directive Number 42, decided to only use the Shuttles for all future U.S. launches, whether civil or military. This decision ended the manufacturing of the ELVs in the commercial industry as the U.S. government constituted most of the demand for the industry. With the Commercial Space Launch Act of 1984, which officially recognized the private sector's capability to operate its own space launch vehicles, and the Challenger accident in 1986, after which the government refused to carry commercial payloads on the shuttles, the commercial launch industry was back in production.

General Dynamics (Atlas), McDonnell Douglas (Delta), and Martin Marietta (Titan) were the 3 companies that provided commercial launch services to the government and the satellite operators during the 1980s. In the 1990s, a series of mergers and acquisitions occurred. In 1993, Martin Marietta acquired General Dynamic's launch business, and the company itself merged with Lockheed Corporation in 1995 to form Lockheed Martin. In 1997, McDonnell Douglas went through its own merger with The Boeing Company. In 2006, Lockheed Martin and Boeing merged their launch business to create the United Launch Alliance (ULA), which essentially ran a monopoly of providing launch services to the government, until the recent emergence of the new launch service providers.

2000s—Surge in Supply

As explained above, the U.S. launch industry was a market with very few companies providing the sources of supply and, essentially, the government as the sole source of demand. In the period of mid-1990s through the 2000s, government policies were enacted to stimulate entrepreneurs to enter the market. At the same time, significant growth in other technology sectors fueled the growth of the commercial launch industry. Such a series of events changed the landscape of the industry.

After the Commercial Space Launch Act of 1984, both the Legislative and the Executive Branch put out a series of acts and policies that specifically focused on the importance of a stable U.S. commercial launch industry. First of the series is the Commercial Space Act of 1998. This act gave several mandates that promoted the growth of the launch industry. First, the act added reentry vehicles and operations within the activities of the commercial launch industry. Second, the act made it a requirement for the government to acquire access to space through the domestic commercial launch service providers, to the extent possible. Third, the act required government agencies to purchase scientific data from commercial sectors, to the extent possible. The first and the second factors expanded the scope and the role of the commercial launch industry. The third factor provided the potential for the growth in the demand of the commercial launch vehicles, as the commercial sectors that provide data to the government would need the commercial launch industry to launch their satellites.

A year later, in 1999, Congress passed H.R. 2684. Section 434 of this law called for the National Aeronautics and Space Administration (NASA) to focus on the feasibility of utilizing commercial launch activities for the International Space Station (ISS). In 2000, Congress passed the Commercial Space Transportation Competitive Act, to further support the growth of the commercial launch industry. Through this act, the space launch liability indemnification program was extended for 5 years. The indemnification program was put into place in the 1988 amendment of the Commercial Space Launch Act, to share the liability of any catastrophic event that inflicts damage to a third party between the commercial industry and the government. The purpose of the program was to encourage the commercial launch industry to develop launch technology, which may cause damage to unexpected parties in case of failure.

Consistent with these laws and other national policies, in 2005, NASA issued Policy Directive 8610.12G, which laid out the plan to utilize commercial launch vehicles made in the United States for the agency's launch needs. The Shuttle program was to be used only under limited circumstances, for such missions as human exploration and those unique to the shuttle's capabilities. This was the beginning of the NASA programs, such as the Commercial Orbital Transportation Services (COTS) and Commercial Resupply Services (CRS), which provided the seed investment for new commercial companies to research and develop launch service technology.

More policy actions from the government followed. The Obama administration supported the importance of developing a robust commercial launch sector through the National Space Policy of 2010. The U.S. Air Force (USAF), the National Reconnaissance Office, and the NASA signed a memorandum of agreement in 2011 to promote efficient launch certification process and the stabilization of the ELV industry. Last but not least, in 2015, Congress passed the U.S. Commercial Space Launch Competitiveness Act “to facilitate a pro-growth environment for the developing commercial space industry.” 3 This act allowed the commercial ownership of assets acquired in space, which spurred the development of the asteroid mining industry, and extended the liability indemnification period to 2025 to further protect the emerging launch industry from the inherent risks of developing the launch vehicles.

Many of these policy measures encouraged entrepreneurship in the commercial space sector in the period of the U.S. history when a surge of new billionaires was being made due to the combination of nontraditional entrepreneurial activities and new technology. Jeff Bezos of Amazon, Inc., Elon Musk of PayPal, Inc., and Paul Allen of Microsoft Corporation are the prominent examples. Each of these entrepreneurs founded their own space launch company, Blue Origin, SpaceX, and Stratolaunch, respectively, using their own wealth made during the time when technology industries were experiencing an exponential expansion. These executives had been successful in commercializing a new technology to a new market with the Silicon Valley business and management style. Their goal is to repeat the same in the space launch industry, which comes with the glorified “next frontier of humankind” epiphany.

Along with the series of policies that encouraged the growth of the commercial launch industry and the new entrepreneurs, technologies in the sectors that create demand for the launch industry have developed. The decreased cost of satellite manufacturing and the advancement in data communication technology have created business opportunities where they did not previously exist. Examples of these industries include satellite imaging, small- and nanosatellite manufacturing, geospatial data, and weather data. Ultimately, these industries are in the business of providing data collection and transfer. The idea is that such data from different types of satellites can provide a better understanding about corporate activities such as marketing and supply chain, 4 and even create new service markets, when coupled with other technologies such as mobile phones, GPS-enhanced location services, and real-time-augmented reality. Furthermore, new companies, such as Deep Space Industries, Planetary Resources, and Moon Express, with plans to mine mineral from extraterrestrial bodies, have evolved due to the general advancement of technology and changes in the government policy. The products and services of these companies all need launch vehicles to become operable. Therefore, the general increase in the investment and development of these commercial space industries led to the belief that the demand for the launch services would increase.

The relative magnitude in the recent increase in the investment in the commercial space sector, including the launch industry, is staggering. The Tauri Group's 2016 Start-Up Space reports the following about the recent growth in the sector:

Looking at the investment only…nearly two thirds of investment in space ventures since 2000 has been in the last five years.

More venture capital was invested in space in 2015 than in the prior 15 years, combined.

This research has identified over 250 investors in start-up space companies; all investors are not always disclosed, so the total number of investors is higher. 5

These findings strongly support the existence of the surge in the investment. However, many of the companies do not currently have a finished product or service to sell to generate revenue. Much of the economic growth in the commercial space sector is based solely on potentials. Venture capitalists (VCs) have enjoyed a significant financial gain during the late 1980s to the early 2000s by investing in risky, high-tech industries. The same investment appetite moved over to the commercial space sector, and, specifically, the commercial space launch industry.

The combination of the favorable government policies, the participation of the high-tech billionaires and VCs, and the development in the space industries that would potentially generate demand has stimulated the attention and the investment to the commercial launch industry in the 2000s. However, the expansion of the commercial launch industry in the current era should be examined more closely. Many government and industry officials are concerned about this rapid expansion as the stability and robustness of the industry depend on multiple factors beyond financial investment. The next section explains these factors that add to the uncertainties of the commercial launch industry.

Risks and Uncertainties in the Commercial Launch Vehicle Industry

Risks are often overlooked in favor of the futuristic optimism and the enthusiasm that spring from the “space cadets” in the minds of the investors. The nature of space exploration has the emotional theme of “exploring the unknowns” that is similar to the Manifest Destiny. Furthermore, beginning with the Moon landing in 1969, countless appearances and references to human spaceflights in the media for the last 5 decades have built an epiphany for space exploration. Prominent examples of these media appearances, as many readers of this article would recognize, are the following: Hollywood blockbuster movies such as 2001: A Space Odyssey, the Star Wars series, and Interstellar; MTV's iconic Moonman; celebrity status of NASA astronauts in the 1960s to the 1990s; and the famous “Earthrise” picture from Apollo 8. The adventure to the final frontier and the consistent media coverage spanning across multiple generations, coupled with the popular American ideology of retaining the “number 1 in the world community,” 6 have placed space exploration in many people's hearts. These naturally lead to a general optimism toward space-related subjects.

Such cognitive bias has been an important factor in some of the most significant decisions in the history of the U.S. spaceflight. For example, the Shuttle program was approved in 1972 based on the belief that “a reusable spacecraft would cut the cost of space access by a factor of 10.” 7 Heiss and Morgenstern conducted a study for NASA and advised that a shuttle program can bring the cost per kilogram to $220 with 60 launches per year.8,† However, according to NASA, the Shuttle program's average cost per mission came out to be $450 million 9 and the published maximum payload was 25,000 kg. The actual cost per kilogram of the Shuttle flights was $8,000. Also, the shuttles were launched for 135 missions for 30 years, averaging about 4.5 flights per year.

The same optimistic approach is driving the development of the commercial launch industry. Such an approach may negatively impact the fair and appropriate valuation of the space launch companies. The commercial space launch industry has a number of characteristics that are unique. Some parts of the industry resemble the tech companies of Silicon Valley, but other parts resemble traditional industries such as the airline and the railroad industry. This part of the article will explain the characteristics of the space launch industry that lead to the question of whether the investors in the industry are making sound business decisions, based on logic and not emotion. Most of these characteristics are risks and uncertainties that cannot be quantitatively measured and pose significant difficulty when trying to appropriately value the space launch companies. These characteristics are (1) the industries' heavy dependence on the government, (2) the uncertainty in the demand outlook, (3) the nature of the sources of capital, (4) the unclear profit model, and (5) the cost of failure and schedule delays.

Heavy Dependence on the U.S. Government

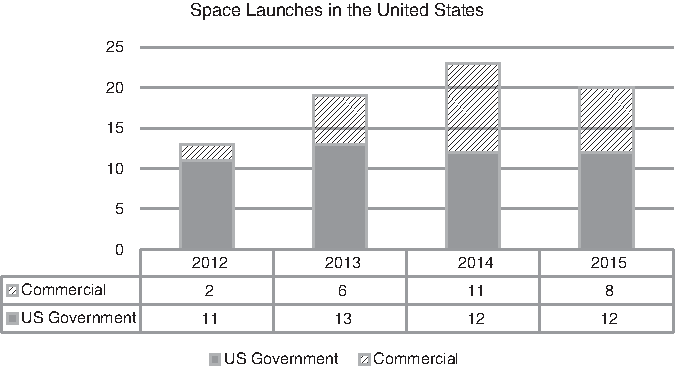

Since the beginning of the commercial launch industry, one single customer dominated the demand side: the U.S. government. As shown in Figure 1, the government constituted as much as 85% of the overall launch activities in 2012, 68% in 2013, 52% in 2014, and 60% in 2015. Furthermore, all 3 launch companies that are currently active in the market ‡ have survived on the contracts from NASA and the Air Force. As such, the consequence of a terminating contract can be detrimental to the companies in the industry. For example, Rocketplane Kistler, once a COTS awardee, filed for bankruptcy after NASA terminated its contract due to the inability to meet several milestones. 10

Number of space launches in the United States from 2012 to 2015. Source: FAA 2012–2016 Annual Compendium of Commercial Space. Transportation. FAA, Federal Aviation Administration.

Beginning in 2006, through various Space Act agreements, NASA contracted out the development of cargo and crew deliveries to the commercial entities. A series of contracts, including the COTS, CRS, and Commercial Crew Development (CCDev), were signed to encourage and support the commercial launch industry and develop its capabilities. Many of the current key companies in the industry are able to stay in business and develop their technologies because of these and other government contracts. For example, in 2014, Orbital ATK reports that 84% of its sales came from the government. 11 This ratio may be higher if only the firm's launch vehicle business is considered by itself.

However, the heavy dependence on a sole source of demand is incredibly risky for the industry. The risk is even higher when that sole source of demand is the government. The riskiness of the dependence does not lie in the credit worthiness of the government, but in the nature of the government's spending on space. The federal government's annual budget process begins from the Executive Branch and gets approved by the Legislative Branch. This process is completely external to the commercial launch industry, but due to the heavy dependence, it can have a significant impact.

First, the White House has been inconsistent with its priorities for space. The national space policy has experienced major changes for the last 2 decades, when every new president comes into power. President George H.W. Bush announced the plan to go to Mars with the Space Exploration Initiatives. However, President Clinton mentioned nothing about going beyond low-Earth orbit in his space policy. President George W. Bush, through his Vision for Space Exploration, put the agenda back into the national policy, and called to go back to the Moon first and then onto Mars. President Obama, in the 2010 National Space Policy, altered the plan by skipping the Moon and directly going to Mars by the 2030s. Finally, the Trump administration, although no formal plan or policy has been announced, has indicated its desire to go back to the Moon in the near future, 12 changing the direction of the previous administration's plan, again. Each of the changes created significant disruptions in the development of launch vehicles for the United States. This trend of new presidents changing the national space policy of the previous president presents significant uncertainties for the commercial launch industry.

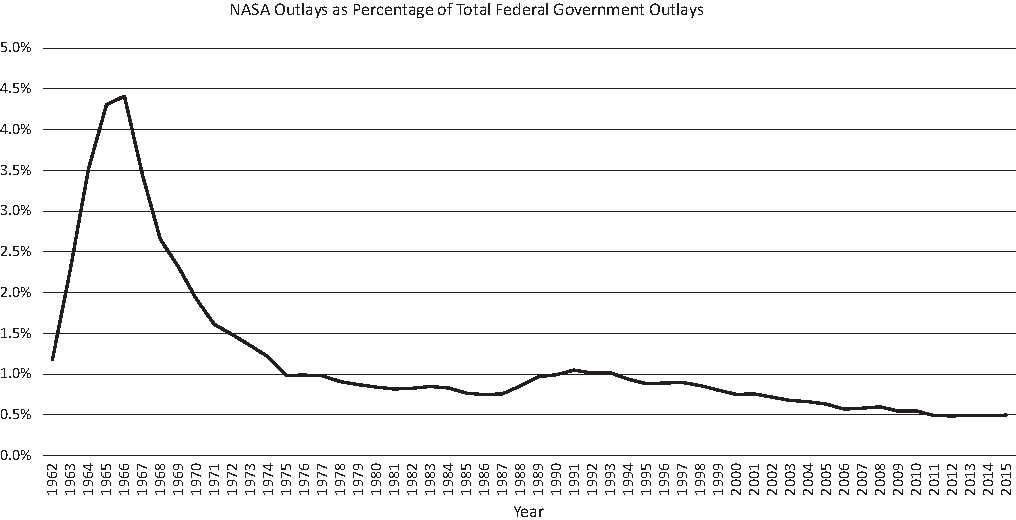

Expenditures on the nonmilitary part of the budget are considered as “discretionary spending,” and decided as less of a priority. Such type of spending is considered as an option for the government and is not required by the law. Unfortunately, the White House does not consider space as the more important agenda for the federal government's discretionary spending. As exhibited in Figure 2, the NASA annual outlay in percentage of the total federal government outlay has been in a downward trend since the middle of the 1960s. Spending on space on the military side faces a similar issue. Space spending is consistently being considered as a second priority when competing for budget allocation against other Department of Defense projects. 13

NASA outlays as percentage of total federal government budget. Source: Office of Management and Budget. NASA, National Aeronautics and Space Administration.

Once the White House decides on how much it wants to spend on space, it has to go through the annual Congressional appropriation process. Consequently, the decision on how much money is to be spent for space can be inherently political, instead of the actual merits of each individual space program. For example, the NASA current Space Launch System (SLS) development is forced to use solid rocket boosters built by ATK in northern Utah, because of a Utah senator's pork-barrel politics. 14 Such political influence can bring certain advantages to the launch industry, but also creates uncertainties. If the demand for a certain launch vehicle is driven not only by the traditional economic factors, such as price and reliability, but also by a political process, significant uncertainties would threaten the accuracy of a company's outlook.

The low priority of space in the federal government budget process, changing national priorities within the realm of space, and the inherent politics of the budget appropriation process, all create uncertainties, therefore increasing risk for the commercial launch industry as a whole. Many cases in which such risk materialized to impact the commercial sector exist. For example, when the Constellation program was canceled in 2010, many of the contractors involved with the program became financially deprived as the future commercial revenues to be realized from the completion of the program were lost. Commercial launch service providers that are wagering to launch future government missions, which are the results of current programs such as CCDev and CRS, all face the possibilities of major disruptions. The risks should be considered significant as the U.S. government is a major source of launch demands for the industry.

Uncertainty in the Demand Outlook

The first decade of the 21st century has seen a surge of commercial launch providers. Previously, Lockheed Martin, Boeing, and Orbital Sciences Corporation were the only companies in the launch industry. However, from the middle of the 2000s, a handful of companies emerged to provide space launch services. The launch vehicle divisions of Lockheed Martin and Boeing merged to create ULA. Orbital merged with ATK and created Orbital ATK. SpaceX and Blue Origin were founded to develop new families of launch vehicles, including reusable first-stage boosters. Virgin Galactic, Firefly, Vector, Rocket Lab, and numerous other companies were created to offer affordable launch vehicles for small satellites. According to the FAA, the Projected Number of Orbital Launch Vehicles That May Be Available for Commercial Uses in the United States by 2020 is 17, operated by 12 different companies. 1 In other words, the number of companies that can supply orbital launch vehicles will increase by 400% in just a little over a period of a decade.

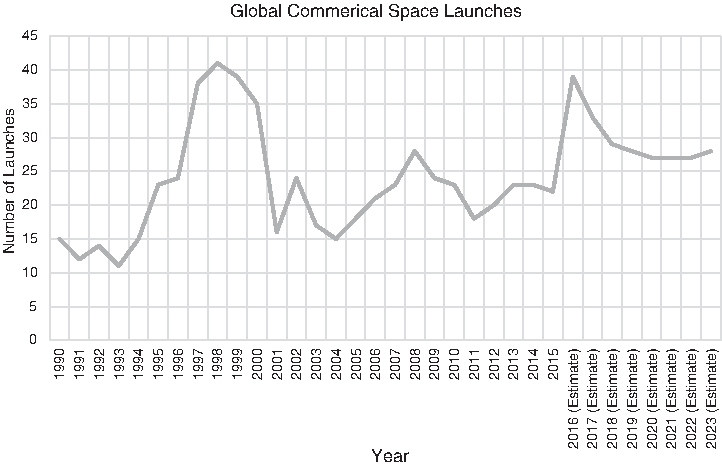

Unfortunately, despite the surge in the supply of launch vehicles, the demand for the launch service does not seem to be growing as fast. Figure 3 shows the historical counts of global commercial launches from 1990, as well as the estimates into 2023. The estimates come from the FAA 2014 Commercial Space Transportation Forecasts report. According to this report, the estimates consider the following factors among the many:

Projections of satellites to be launched over the next 10 years from global satellite operators, satellite manufacturers, and launch service providers.

Publicly announced satellite and launch contracts.

Availability of financing and insurance.

Potential consolidation among operators.

New launch vehicle capabilities.

Hosted payload opportunities.

Global commercial space launches. Sources: From 1990 to 2014—The U.S. Department of Transportation. From 2015 to 2023—The U.S. Federal Aviation Administration.

The report also states the following:

Launch vehicles and satellite programs are complex, and susceptible to delays, which generally makes the forecast demand for launches the upper limit of actual launches in the near-term forecast. 15

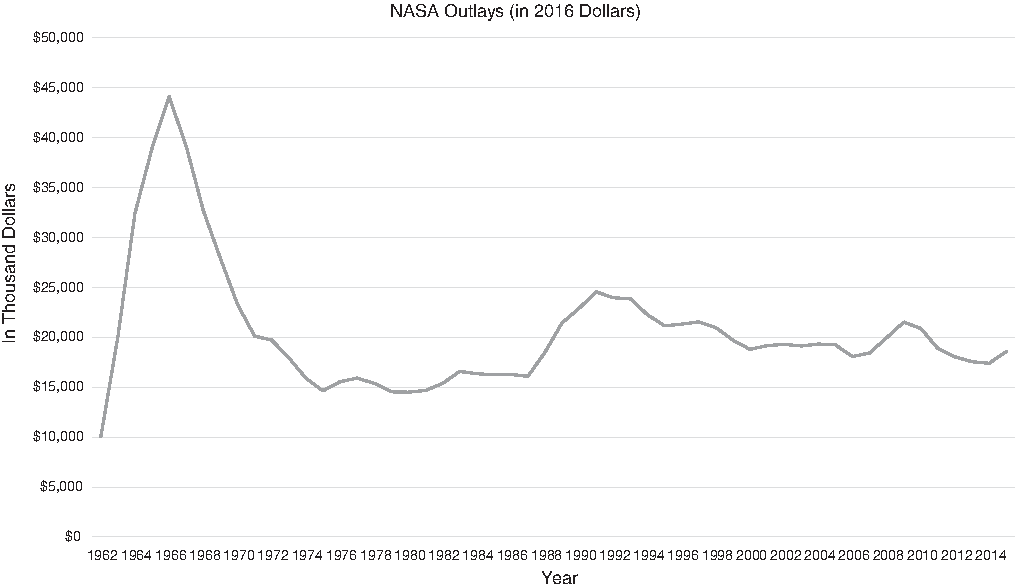

For almost the last 20 years, the global launch demand has not exceeded 40 launches per year, and mostly stayed below 30. Furthermore, the estimated number of launches from 2018 to 2023 is below 30 per year. Adding to the bleak outlook is that NASA, one of the largest sources of demand, is not likely to substantially increase its demand. Figure 4 shows the historical NASA outlays since 1962 in 2016 dollars. Since the days of Apollo, NASA spending has been in a steady state, without much surprises. This trend is expected to continue as NASA competes for budget, as with any other nondiscretionary budget in the federal government. The budget process is only going to be more competitive in the future.

NASA outlays in 2016 dollars. Source: Office of Management and Budget and Bureau of Labor Statistics.

The Department of Defense, the other large source of demand, also projected a decrease in their launch needs. The U.S. Government Accountability Office (GAO) reports that “the Air Force estimates that the demand for national security launches will decline from approximately 8 in 2015 to about 4 per year beginning in 2020.” 16 This 50% reduction in future demand by one of the most prominent customers significantly adds to the uncertainty of the industry.

The launch industry's demand is also heavily depended on the outlook of the satellite industry, as the growth in this industry would be followed by an increase in the demand for launches. The global satellite industry, which includes businesses such as satellite services, ground equipment and satellite manufacturing, represents the vast majority of the global commercial space sector. As shown in Table 1, the growth rate of this industry for the last 10 years has been in a downward trend to a rate close to the inflation rate. Although the size of the total revenue increased, the growth rate of the revenue is decreasing. This is an indication that the future launch demand from this industry may not be strong.

Global Satellite Industry Revenue

Sources: The Satellite Industry Association 2011 and 2016 State of the Satellite Industry Report.

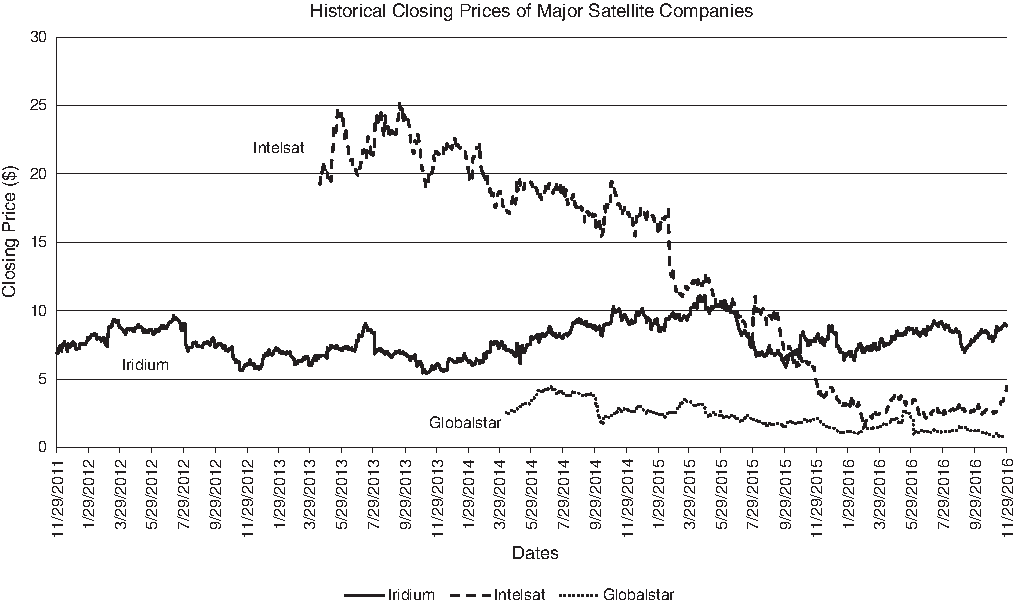

Another factor to examine in the satellite industry is the stability of the satellite companies themselves. The performance of a company's public stock is a standard indication of a company's robustness and its future outlook. Unfortunately, the investors' response to the major satellite companies is not bright. For example, when Intelsat, the world's largest provider of satellite services, offered its shares to the public through an initial public offering (IPO) in 2013, the offering price was set to $18 per share, which was below the anticipated range of $21 to $25 per share. 17 Even at this price, the company sold 2.4 million shares less than the total shares offered. § Furthermore, as shown in Figure 5, the historical stock prices of the 3 major satellite companies are either fairly constant or at a downward trend. These are all indications that a significant expansion in the satellite industry is not likely to happen in the near term; therefore, the commercial portion of the launch industry's demand is not likely to increase.

Historical closing prices of major satellite companies. Source: Yahoo! Finance.

Considering these factors, the global demand for commercial launches will most likely stay between 25 and 30 launches per year for the foreseeable future. In the most optimistic outlook, if the 30 launches were spread equally among the 12 launch providers of 2020, each will perform 2.5 launches. This is a discouraging number of launches per year. At this rate, not many companies will be able to make the necessary profit to stay in operation. Unfortunately, even this number is a highly optimistic exaggeration as the 30 launches per year is a global figure. As there will be other launch providers in the global market, the likelihood of the American companies capturing 100% of the market share is minimal.

The uncertainty of the growth in demand increases when forecasting beyond 2023. In 2014, the United States announced the plan to fund the ISS until 2024. The ISS is currently the only destination for commercial cargo and crew missions and makes up a sizeable portion of the launch forecast up to 2023. The U.S. government does not have a plan to construct another space station, as of yet, and NASA hopes that the private sector will create a commercial space station. 18 However, the private sector is only in the research and planning stage. Essentially, for now, the commercial cargo and crew launch service providers do not have demand beyond 2024. **

Many argue that a decrease in launch cost will increase the demand of launch services. The issue with this argument is that launch cost itself is a function of launch frequency. The National Academies' calculation of launch cost per kilogram is as follows

19

:

where

fixed cost = annual cost of the fixed infrastructure and critical skill base

variable cost = cost to build and launch one unit

N = number of launches per year

kg/launch = payload mass delivered by one launch

This equation explains that to decrease the launch cost, either fixed cost or variable cost has to decrease, or N (number of launches per year) has to increase. Furthermore, because N is a significant contributor to the denominator, an increase in N will have the most significant contribution, per unit basis, in decreasing the launch cost.

Moreover, the overall production cost can significantly decrease with the increase in number of launches. Microeconomics theory of economies of scale explains that cost advantage can increase with increase in output. This is because total cost per unit is the sum of fixed cost per unit and variable cost per unit. Fixed cost stays constant regardless of the number of output. This total fixed cost gets spread out among the total output produced. Therefore, per unit fixed cost decreases with increase in output. Total variable cost will increase with the increase in number of output, but often production efficiency is gained with increase in output, therefore decreasing the variable cost per unit. If no such efficiency is gained, per unit average cost will stay constant. Launch vehicles are not ready-made products. The production begins after a contract is signed. Therefore, in the launch vehicle industry, demand equals output. When the economies of scale are applied to launch vehicle production, cost again becomes a function of demand.

Considering these factors that contribute to the uncertainties of the future demand, the commercial launch industry is operating under the “engineering first, customers second,” mind-set. However, such mind-set creates a critical risk to the viability of the industry as a whole. Unfortunately, the supply and demand law of microeconomics explains that if supply is greater than demand, price of a launch will decrease (explained more in detail in the Demand and Supply Inequality section). With the current demand forecast, and the uncertainties going into the future, price might decrease to the point below the cost of production, in which case the industry is not profitable.

Source of Capital

In the current U.S. commercial launch industry, 2 groups make up the majority of the investment pool: the government and VCs. Both groups pose risk to the industry's long-term sustainability due to their unique characteristics.

The Columbia Accident in 2003 was the beginning of the end of the Shuttle program 20 and NASA did not have any plan to build a replacement of the shuttles. Instead, with President George W. Bush's Vision for Space Exploration in 2004, NASA shifted its reliance on the access to low-Earth orbit to the commercial launch industry.21,†† Since then, NASA has injected about $12.4 billion worth of contracts to the industry through the Commercial Crew and Cargo Program Office (C3PO), as shown in Table 2. Other than CRS and COTS, which were service acquisitions, these contracts were used to stimulate the development of the industry's technology for the government to purchase in the future. ‡‡

NASA Commercial Launch Service Contracts

Sources: NASA–“Commercial Crew Program-The Essentials” and “Commercial Crew and Cargo–Space Act Agreements.”

NASA, National Aeronautics and Space Administration.

The C3PO contracts are contracts to develop technologies for spacecraft. Therefore, they are not to be mistaken for contracts specifically for the launch industry. However, the companies that have been selected for the programs include the companies that are in the launch vehicle industry, including Blue Origin, Boeing, Orbital ATK, and SpaceX. Providing source of capital for these companies to research and develop spacecraft inherently supports launch vehicle development. Furthermore, the development of these spacecrafts will certainly support the launch vehicle industry, as launch vehicles would be required to place the spacecraft into Earth's orbits. NASA states that these contracts “support an end-to-end transportation solution that will encourage the development of a range of launch vehicle and spacecraft combinations,” 22 recognizing the relationship between spacecraft and launch vehicle development.

The issue with the government being the major investor is that the federal agencies are susceptible to changes in budgets and plans, especially for nondiscretionary spending. As previously explained in the Heavy Dependence on the U.S. Government section, the annual budgets for federal agencies, such as NASA, are products of volatile politics, therefore, not always based on prudent economic decisions. Contracts always carry the high risk of being disrupted, or canceled altogether, and the guarantees of future contracts do not exist. Therefore, heavily relying on the government capital assistance can add to the uncertainties of the future capital inflow when compared to the traditional equity and debt financial markets as sources.

The second major source of investment is the VCs. As shown in Table 3, venture capital is a significant portion of commercial investments made in the commercial space sector, including the launch industry, in recent years. In essence, venture capitals are investments in the early stage of a company in exchange for a share of the company. The role of VCs is to provide the financial resources needed to carry a start-up company from the initial development stage, where the heavy research and development happen, to the expansion stage, where sales of the company's product generate sustainable profit. If the venture capital investment is successful, in the expansion stage, the VCs share of the company is sold to another company, usually private equity firms, or to the public equity market through an IPO. VCs have become an integral part of the American start-up companies as 50% of venture capital-backed start-ups are acquired or go public, whereas only 1.06% of nonventure capital-backed start-ups go public. 23

Magnitude of Investment in Commercial Space Sector by Different Investment Types for the Period of 2011 to 2015

Source: The Tauri Group—Start-Up Space.

The risks that VCs present to the commercial launch industry are in the nature of the duration of venture capital funds and the current financial environment. First, venture capital funds are short-term investment vehicles. The nature of VC is high risk because they invest heavily at the very early stage of a company's life cycle. Also, VCs invest in several companies. If a VC does not realize return on investment (ROI) in a company within a short time period, it will likely exit and take a loss and move on to a new start-up. They have the investment appetite to invest in many start-up companies, dispose quickly, and move to the next to decrease the risk. This life span is typically from 6 to 10 years. 24

Except for ULA and Orbital ATK, which are publicly owned companies, most space launch companies have received some form of venture capital investments. Nevertheless, most of these VC-backed companies have not yet generated any ROI. The VCs' willingness to keep the investment in the industry for the next few years will significantly impact the viability of the launch providers. However, based on the demand forecast, the ability of these companies to generate ROI in the upcoming years is questionable, which increases the possibility of the VCs exiting the industry.

One factor that has delayed the exit of the VCs is the current low interest rate environment. Due to the global financial crisis in 2007, the U.S. Federal Reserve's federal funds interest (risk-free) §§ rate has been historically low, ranging from 0.25% to 1%. This means that the opportunity cost of making investment is low for the VCs. For a simplified example, if the federal funds rate is 5.25%, which it was in June of 2006, a VCs foregone cost of investing in a company would be 5.25%. For every $1 million the VC invests, the opportunity cost of the investment would be $52,500 per year. This is because they could have made this much amount of money by simply investing in the risk-free federal government bond. In comparison, the federal funds rate is at 0.5% at the time of this writing. The same investment would only have the opportunity cost of $5,000 per year. The difference is significant when the investment is hundreds of millions of dollars, making the cost of capital an important factor when deciding on the continuation of investment.

Furthermore, the investors are staying in the launch industry for a longer period of time, because, in general, investors look to invest in riskier businesses in low interest rate environment. In the financial market, interest rate is based on the federal risk-free rate and the amount of risk (risk premium) the investor takes. In other words, if an investor is looking to generate a 5% return on an investment, the 5% would be based on the federal funds rate plus the risk premium. If the risk-free rate is 3%, the investor would invest in a business with risk premium of 2%, therefore making a 5% return. If the risk-free rate is 0.5%, the investor would have to invest in a business with a risk premium of 4.5% to generate the same 5% return. The commercial launch industry is one of the riskier sectors the investors can invest in. This factor only serves their investment appetite in the current low interest environment.

However, the overall U.S. economy is recovering and the federal funds rate is expected to increase for the foreseeable future. Since the rate was set at the historic low of 0.25% in December of 2008, it increased 3 times: to 0.5% in December 2015, 0.75% in December of 2016, and 1.0% in March of 2017. As the U.S. economy stabilizes and the growth rate increases steadily, the rate is bound to increase to a point around 4.0% to 5.0%. The opportunity cost of investing in the commercial launch industry will increase. The investors will not have to take as much risk to generate the same rate of return. These factors will be critical for the investors when deciding to take their investment out of the launch industry. As the venture capitals make up a major source of investment for the industry, the increase in the interest rate therefore increases the risk to the overall sustainability of the industry.

Questionable Profit Model

Generating revenue by providing access to space is a reasonable profit model. For example, Orbital ATK financial statement shows that its Flight Systems Group, which the launch service is a part of, generated about $110 and $145 million, in fiscal year 2014 and 2015, respectively, in income from continuing operations, before interest, income taxes, and noncontrolling interest. 11 Also, ULA has generated average annual earnings of $150 million for Lockheed Martin and Boeing, the 2 parent companies of ULA, combined. 25 These incumbent companies' profit models have proved themselves to be sound. The new entrants, however, have profit models that are questionable, thereby creating uncertainty.

The prominent example is SpaceX. SpaceX has built a cost-effective launch service for satellites to the commercial orbits and cargos to the ISS. The company is also in the development of its crewed flight system, to be launched in the end of 2017. 26 SpaceX is a private firm that is not publicly traded, and therefore, its financial statements are not available. However, many experts believe that the company is likely to generate profit from its launch services. 27 What is questionable, however, is the company's plan to colonize Mars. Elon Musk, the CEO of SpaceX, stated in September of 2016 that the company is developing a launch system to send humans to Mars by the mid-2020s, and colonize Mars with 1 million people by the 2060s.

Considering that SpaceX is a private corporation, the profitability of the plan to Mars should be questioned. First, for a company to be able to profit from a different planetary body in any way, it has to have a marketable product to be sold on Earth. Other than data that can be transferred from Mars through satellite communication, such marketable products do not exist without the physical return back to Earth. Even if returning any materials from Mars would be possible in the next decade, the commercial value of such materials is uncertain, and would most likely only yield scientific value. Therefore, the cost of going to and returning from Mars would be difficult to be justified based on these materials. This is why space exploration has historically been primarily for government entities, as they do not need to generate profit from their activities.

Providing transportation to Mars can only be profitable if a self-sustaining civilization existed in Mars. Without a plan on how such a civilization would be developed, SpaceX's profit model for providing transportation services to Mars becomes highly questionable. Unfortunately, such a business plan does not exist in detail. *** Also, civilizing Mars is not an endeavor that can be carried out by one company. Creating a civilization in a different planet has a vast range of implications other than just getting there, including politics. Even if SpaceX did end up developing the cost-effective technology to transport humans to Mars, governments from across the globe will have to be involved to resolve issues such as how sovereignty and property rights will be recognized. This is just the beginning of the series of questions and decisions that would have be resolved before any civilization begins to form on a different planet. Most importantly, however, the survivability of humans on Mars has not even been answered. We have not yet figured out how humans will even live on Mars as we have not understood all of the effects of long-term radiation exposure to human body.

Again, SpaceX is a private corporation with the primary objective to generate financial return for its shareholders. Developing a technology that is ahead of its time should be carefully considered as a business decision. Too many uncertainties exist in the firm's plan to develop the Interplanetary Transportation System. This development is going to cost billions of dollars, even only in the research and development stage, but the return on the investment will be difficult to be realized, if ever. Scott Pace, a professor at the Space Policy Institute of the George Washington University, and a former NASA associate administrator, stated, in an interview about SpaceX's plan to Mars, “I don't see how a Mars program is really going to be sustainable. I don't see a commercial rationale for it.” 28 The unexplainable profit model creates significant uncertainty as to if such ambitious developments foster sustainable businesses.

Another example of a questionable business model is the launch service providers for space tourism. XCOR and Virgin Galactic plan on providing suborbital flights to its customers at the prices of $150,000 and $250,000, respectively. During the flights, the customers will be able to experience weightlessness and see the Earth and space at suborbital altitudes. The price of these flights is not something an average wage earning person in a developed country can afford. Only the high net worth millionaires can afford these flights, and therefore, the potential customer pool is small to begin with. Furthermore, according to a survey of 1,008 Americans, only 28% replied that they would take a free trip to space and 69% replied they would not. 29 Such a lack of inclination for space travel would further reduce the customer pool. Finally, suborbital tourism companies currently do not offer any destination flights. Currently, they offer the experience of being in a suborbital flight to the customers. This experience is a one-time adventure for most people so the customer retention rate will be very low. Consequently, as more customers experience the flights, the potential customer pool shrinks. Therefore, in order for these companies to survive for a long period, they would have to devise a different profit model.

Some investors have expressed their concern about the viability of the new commercial space sector companies, including the launch companies. The Tauri Group interviewed potential investors, whose investment portfolios include technology-oriented firms and are interested in the developments in the space sector, on the reason why they are not currently investing in the space sector. They responded that many of the companies in the sector do not seem to have the ability to generate revenue quickly, within the next 3 to 5 years, and some even do not have the capabilities to close the business case. 5 These responses concur with the idea that some of the new companies in the space launch industry do not have clear profit models.

The 2 examples above provide how the companies in the commercial launch business are directing their resources in developing technologies that have questionable profitability. A similar concern is evident in other companies. For example, both ULA and Blue Origin are developing launch vehicles with capabilities to go beyond the commercial orbits. ††† However, beyond these orbits, minimal commercial opportunities exist, especially when NASA, the most significant client in the industry, is developing its own heavy rocket system, called the SLS, for transportation beyond the Earth's orbits.

The idea of affordable space transportation and commercial deep space exploration is all very emotionally captivating. However, whether these ideas are sound business models are questionable and unconvincing considering their profitability. They may have extravagant and interesting ideas that draw the attention of the public, but these ideas do not necessarily equate to commercial viability. This uncertainty in the profitability of the companies in the launch industry greatly adds to the questionable sustainability of the current market.

Cost of Failure and Schedule Delays

Since the launch of the first manmade object to space 60 years ago, launch technologies have evolved astoundingly. Both commercial and government entities, collectively, have developed new launch technologies such as the super heavy-lift launch vehicles, such as the Saturn V, that can place payloads of 140,000 kg to low-Earth orbit, reusable launch vehicles such as the Shuttle Orbiters, and reusable first-stage boosters such as those of SpaceX and Blue Origin. Nevertheless, space launch is still a difficult endeavor. Even after 60 years of development and technological advancement, rockets unexpectedly explode, causing launch failures. The nature of high-tech companies is the constant research and development required to reduce failure and achieve stability in the operation. However, the launch industry is different. Even at the operational stage, many uncertainties exist and success is never guaranteed before the rocket is launched. In the midst of high uncertainties, launch failures have been frequent in recent years. These launch failures have increased the risk to the industry's sustainability due to the high cost of failure and schedule delays.

Schedule delays due to launch failures have been very common for the launch industry. Virgin Galactic's original promise to operate its commercial suborbital flights in 2011 had been delayed every year until 2014. After the 2014 accident of the SpaceShipTwo test flight, which killed 1 of the 2 pilots, the schedule has been pushed indefinitely. Orbital ATK launch vehicle, Antares, did not fly for nearly 2 years after it exploded 15 s after the launch in October 27, 2014. SpaceX also experienced a launch explosion in June 28, 2014, which halted the company's operations by 6 months. Falcon 9 returned to flight in December of the same year. However, on September 1, 2016, the launch vehicle exploded again during a test, 2 days before the launch. SpaceX announced the plan to launch 18 times in 2016. 30 Eight launches were made and the vehicle that exploded in September was the ninth scheduled launch of the year. SpaceX did not return to flight until January of 2017, and it was not able to meet its promised flight schedule in 2016. Even if the September flight was successful, given the rate of one launch per month, completing 18 launches in 2016 would have been difficult.

The implications of schedule delays are significant to the industry because of the direct cost associated with the delay. Many of the launch industry's commercial clients are in the satellite communications business and delayed launch of their satellites means delayed return on their investment in the satellites. If a satellite was to replace an existing satellite, delay in the operation of the new satellite may cause a halt in the satellite operator's business altogether. For example, Iridium was scheduled to have its satellite launched in September 2016. This satellite is a part of the firm's new NEXT constellation of satellites and is to replace the current constellation. However, the launch of the satellite has been delayed due to Falcon 9's explosion in September. If Iridium cannot place its new constellation before the current one is decommissioned, then the company will lose its operability. 31

Furthermore, a delay in 1 flight can result in delays in many subsequent flights for the launch provider. Considering that when a launch failure occurs, the length of the delay in the schedule is undefined, the uncertainty in the timing of the ROI increases for all of the satellite operators that were slated for launches by the launch service provider. Due to this increased uncertainty, customers may choose a different launch provider. Therefore, the direct cost of failure can be exponential.

The indirect cost of failure has even greater implications. The Falcon 9 rocket that exploded in September 2016 was to launch Space Communication's (Spacecom) Amos-6 satellite. Because of the explosion, SpaceX is expected to either pay the satellite operator $50 million or provide a free ride. 32 This is either a $50 million increase in cost or up to $62 million loss in revenue, considering that the publically announced price of Falcon 9 is $62 million per launch. For Spacecom, the cost is greater. The day before the explosion, the company's stock price listed on the Tel Aviv Stock Exchange was around $1,117. However, on the day of the explosion, the stock price fell 8.88%, and on the second day, the stock price fell an additional 32.73% to around $683. 33 Furthermore, the successful launch of Amos-6 was a condition to the Spacecom's acquisition by the Beijing Xinwei Group. However, due to the launch failure, the deal is to be amended, or canceled altogether. 34 How much SpaceX is financially liable for the loss is yet to be determined; but, depending on the terms of the deal between Spacecom and SpaceX, compensation litigation may be inevitable.

The above examples demonstrate the difficulties of achieving successful space launches at an affordable cost and the direct and indirect costs of failed launches. In extreme cases, launch failures can lead a company to file for bankruptcy. Sea Launch filed Chapter 11 of the U.S. Bankruptcy code in 2009 after a launch failure in 2007, which was the result of issues such as launch delays and customer defections. 35 The frequent explosions of the past few years are not coincidence. Before the influx of the new launch providers, the few launch providers that existed had near-perfect launch records. For example, ULA boasts 111 consecutive successful launches. The industry is now focused on making the launch vehicles more affordable. However, as the record shows, affordability comes with less reliability and more launch failures. Unfortunately, launch failures result in a significant cost to the launch provider and external stakeholders, thereby increasing the total risk of the industry.

Speculative Bubble and the Commercial Launch Industry

“Speculative bubble” is not a definitive term. Many speculative bubbles have burst over the period of modern economy. Each one of them has different aspects that are distinctive, hence, making it difficult to define the term in a specific way. In the basic sense, a speculative bubble is when a company, an industry, or a collection of industries are priced at a higher value than what it is actually worth, based on a speculation of the future. 36

A speculative bubble is designated as one with absolute certainty only ex-post. 37 An industry would have to experience a significant contraction to be proven for it to have been in a bubble. Fama, a Nobel laureate in Economics, states that “Statistically, people have not come up with ways of identifying bubble.” 38 Market conditions can depend on countless factors, so, an argument that a specific industry is experiencing a bubble can always be criticized by a counter argument.

Although one cannot confirm that an industry is in a speculative bubble until the bubble bursts, a set of common characteristics has existed in the past major bubbles. Robert Shiller, a professor of economics at Yale University and a Nobel laureate in Economics, explains a series of events that happen before a speculative bubble bursts. According to Shiller, speculative bubble is defined as follows:

…a situation in which news of price increases spurs investor enthusiasm, which spreads by psychological contagion from person to person, and, in the process, amplifies stories that might justify the price increase and brings in a larger and larger class of investors, who, despite doubts about the real value of the investment, are drawn to it partly through envy of others' successes and partly through a gambler's excitement. 39

Shiller explains that such “irrational exuberance” consists of 3 distinctive factors. First, precipitating factors, usually politics or technology, cause a market to steer to a new direction. This is followed by cultural factors, such as the media, that catch the attention of the mass, including investors. Meanwhile, psychological factors, such as overconfidence and the tendency to tell stories, intensify the market.

These 3 factors are visible in the commercial launch industry. First, the federal government provided the support to encourage the commercial space launch industry through policies such as the Commercial Space Act of 1998 and the 2010 National Space Policy. The policies were followed by technological advancements in the other commercial space industries that created the potential demand for the launch industry. Furthermore, the ultrahigh net worth individuals who became billionaires in the 21st century from other industries entered the commercial launch industry. They brought in massive amounts of capital into the industry and each of them promised “the new age of space.” With their arrival, changes were introduced that enhanced the rocket technology and the production process.

Second, stories of the commercial launch companies have been inundating various types of media coverage with captivating headlines such as “The Battle of the Billionaires,” “Amazon vs. Tesla,” and “The New Space Race” since the middle of the 2000s. Furthermore, some of the new companies in the industries are headed by the executives who are not shy of press coverage. Richard Branson, whose group owns Virgin Galactic, is known for performing bizarre marketing stunts, such as driving a tank down the Fifth Avenue of New York City to advertise his soft drink business. For Virgin Galactic, he held a press conference wearing a spacesuit. Elon Musk, the chief executive of SpaceX, is known for his Steve Jobs-like showcases of his products. Historically, such showmanship and the abundance of media coverage were not common in the launch industry.

The last factor that completes Shiller's model of speculative bubble is the psychological factor, which includes overconfidence and people's tendency to tell stories. Shiller states, “Overconfidence…appears to be a fundamental factor promoting the high volume of trade we observe in speculative markets.” 39 In the launch industry, this fundamental factor is evidenced by numerous cases of delays in promised breakthrough technologies and missed milestones. These are explained in detail in the Cost of Failure and Schedule Delays section, but one example is Virgin Galactic's repeated delays of its first operational flight.

Shiller also explains that in a speculative bubble, people tend to sell products by telling stories instead of quantitative evidence. Instead of providing concrete evidences of “whether the price is at the right level in terms of quantitative evidences about future dividends or earnings,” 39 stories describing qualitative factors such as the history of a company and the nature of a product are often told to the public and the investors. Unfortunately, this also is true of the commercial launch industry. Many of the companies in the industry sell their products to the potential clients and investors by selling the “space theme” that touches many hearts. Furthermore, the story sold in the launch industry is supported by the overly optimistic characteristic of the people of the industry.

Are these enough evidences to conclude that the commercial launch industry is in a state of a speculative bubble? As explained earlier, bubbles are confirmed only after they burst. The idea here is that the industry's current environment clearly resembles the characteristics of a speculative bubble. The next section of this article will focus on the comparative analysis of the launch industry with 2 other industries that were in speculative bubbles that burst.

Comparative Analysis

So far, this article has explained the history of the commercial launch industry, the key companies of the industry, and the uncertainties unique to the industry that increase the riskiness of the business. The article then explained what speculative bubble is and how the commercial launch industry resembles a speculative bubble. In this section, the article takes a close look at 2 of the most significant economic events of the 21st century and compares them to the commercial launch industry. These 2 examples were chosen, in part, because of the significant impact they had in the U.S. economy, but more importantly, they were the technology-centric industries' bubbles created from overconfidence, optimism, and incorrect industry valuations. These characteristics are similar to those of the commercial launch industry.

The Dot-com Bubble of 2000

The wide spread of the Internet in the 1990s, which was the precipitating factor, led to the creation of numerous companies providing services through e-commerce. Investors, mostly VCs, were overly optimistic about the potentials of the Internet and supported these new companies that were trying to become the next Amazon or Yahoo, both of which went through successful IPOs. These e-commerce companies with the “next big idea” were receiving investments from the VCs without sound business models.

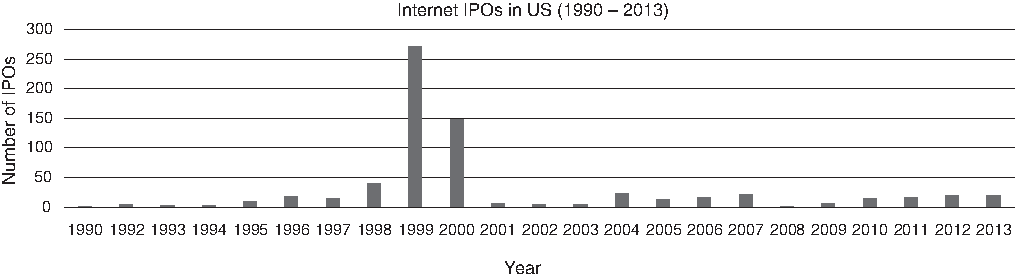

The excitement of the Internet companies grew throughout the late 1990s and were highly overvalued, not based on the actual merits of the company nor the ability to actually generate cash flows. As previously explained in the Source of Capital section, a successful venture capital exit strategy is an IPO. These overvalued companies were pushed through the investors' exit strategy to the public market at an unprecedented rate. Figure 6 shows that the number of IPOs of Internet companies increased to 272 in 1999.

Internet IPOs in the United States (1993–2013). Source: Jay R. Ritter, the University of Florida—“A List of Internet IPOs.” IPOs, initial public offerings.

McKinsey & Company reports that in early 2000, at the peak of the bubble, tech companies were valued 165% higher than the general market. 40 Ben Geier of Time Magazine recalls the time period as the following:

With the investment and excitement, stock values grew. The value of the NASDAQ, home to many of the biggest tech stocks, grew from around 1,000 points in 1995 to more than 5,000 in 2000. Companies were going to market with IPOs and fetching huge prices, with stocks sometimes doubling on the first day. It was a seeming wonderland where anyone with an idea could start making money. 41

The second and third factor of Shiller's speculative bubble model, the cultural and the psychological factors, exacerbated the problem. Financial measures, such as the profit-to-equity ratio, that were traditionally used for valuation of a company were largely ignored. Even logical investment strategies were disregarded. The investors felt the requisite to include such stocks in their portfolios because of the popularity of the industry, 42 not based on their business models. The dot-com companies were the new phenomenon in the media and the financial market. More people bought stocks of these companies, which further drove up the already overvalued share prices. Benchmarking from the successes of these companies, more companies went public. In early 2000, the truth of these companies' profitability unfolded and the dot-com bubble burst. Many reported losses and collapsed within the first year of being a public company. As a consequence of the bubble, about $2 trillion asset was wiped out and thousands of jobs were lost. 43

The Telecom Crash

The wide spread of the Internet did not just create a bubble in the dot-com industry. The telecommunications (henceforth, telecom) industry also experienced a sudden expansion due to the expected growth in the Internet usage across the globe. In 1996, President Bill Clinton signed the Telecommunications Act, which opened up the telecom industry, which includes the Internet providers, to the market for competition. Previously, only a few companies were licensed by the Federal Communication Commission to operate in the industry. The objective of this act was “to accelerate private sector deployment of advanced telecommunications and information technologies and services to all Americans by opening all telecommunications markets to competition.” 44 With the act enacted, numerous new players flooded the industry that traditionally had only a few companies.

With the optimistic belief that the wide spread of the Internet would result in a significant increase in the demand for the Internet, the new and the old companies began to build telecom networks, spending more than $500 billion. However, the demand did not exist at the anticipated level. By 2000, the industry was experiencing a significant excess in supply and lack of demand. Litan explains that the American companies overbuilt the network by so much, that by 2002, no more than 2% of the network was being used. 43 The telecom companies expected to all take a share of a large pie, but the size of the pie turned out to be much smaller and each firm had to fight to increase its market share. This led to drastic cuts in the consumer prices. 45 As a result, the ROI decreased significantly.

To hide the instability of their businesses and financial statements, many companies engaged in fraudulent accounting practices. The profits that have been reported by the industry since the deregulation in 1996 were found to be losses. The industry's mishaps unfolded one by one; numerous companies filed for bankruptcy, were forced to close down, and multibillion dollars of investments evaporated.

Much of the investment for the telecom industry came from the debt issued by bankers and financial institutions. These investments were followed by a surge in the market value of the telecom companies. The investment banks that invested in the telecom industry were the same ones that analyzed the value of the stocks of the telecom companies. To serve their own institution's short-term interest, the research reports and stock valuations were overconfident, overly optimistic, and biased. 46

Furthermore, before the bubble, the telecom industry itself was a much matured industry with slow growth. The rapid change in technology completely changed the environment, but the financial professionals did not have the correct performance indicators to properly value the companies. 46 This second factor, when coupled with the conflict of interest, allowed the analysts to manipulate the financial valuations to a direction that they thought would benefit the banks, investors, the telecom industry, and anyone in between.

After the telecom industry collapsed, the financial industry was criticized for being overly optimistic about the telecom market, ignoring the traditional quantitative financial valuation methods, and using unproven, new indicators to value the companies. As a result of the bubble, about $2 trillion of market capitalization were wiped out of the telecom industry, 45 leading the overall economy to a significant contraction, together with the dot-com bubble.

Comparison: The Commercial Launch Industry

Risks and Uncertainties in the Commercial Launch Vehicle Industry section described several factors that create uncertainty in the commercial launch industry, thereby increasing the risks involved in the business of providing space launch services. The above parts of the Comparative Analysis section provided overview of the causes of the boom and the bust of the 2 most significant speculative bubbles of recent history. A number of similarities between the commercial launch industry and the dot-com and telecom industries exist, with significant indicators to believe that the commercial launch industry strongly resembles a speculative bubble. These similarities are explained in the rest of this section.

Precipitating factors

Shiller's model for speculative bubbles begins with a precipitating factor that forms the foundation of the bubble. For the 3 industries, the precipitating factors are both technology and politics. The technological precipitating factors for the previous 2 bubbles were the spread of the Internet to the mass and the technological enhancement of transferring data. For the launch industry, as explained in the History section, the precipitating factors are the demand growth due to the technological advancements made in the other commercial space sectors and the production enhancements that were the results of the inflow of investments made by the ultrahigh net worth individuals.

Politics were also the precipitating factors for all of these industries. For the telecom industry, the Telecommunications Act of 1996 initiated the deregulation and allowed market competition. For the launch industry, the political precipitating factor is the series of policy events, including the decision to retire the Shuttle program and to support the growth of the commercial launch industry. The political factors in these industries focus on growth through free market competition and encouraging more companies to participate.

Old industries and nontraditional performance indicators

Both the telecom industry and the space launch industry are not new industries. The telecom industry has been in existence since the early 1900s and the launch industry since the 1960s. However, both industries have been significantly disrupted by the advancement of technology and increase in the number of suppliers. As explained previously, the Telecommunications Act of 1996 allowed many new companies to enter the market and create competition. In a similar progression, a series of policies and noncorrelated events, including technological advancements, drew companies into the launch industry, which is now expecting up to 12 companies to provide orbital launch service by 2020.

Kam explains that the dynamics of the telecom industry was rapidly changing due to technology, but the financial institutions did not have the performance indicators to correctly value the companies. 46 Therefore, they invented new ones such as “subscriber penetration for the mobile operators, average activation costs, cities connected with fiber, or miles of fiber laid.” 46 Whether these new performance indicators were accurate measurements of the success of the telecom companies is highly questionable. The companies' share prices continually increased using these new measurements, but the industry turned out to be a bubble.

Similar to the telecom industry, the launch industry is experiencing technological changes. The most significant change is the reusability of the rockets. So far, SpaceX and Blue Origin have successfully demonstrated the technology to certain degrees. SpaceX has successfully returned, landed its orbital launch boosters, and reused a returned booster once so far. On the contrary, Blue Origin has returned, landed, and reused its booster, but this booster was only for suborbital launches, which requires significantly less thrust than orbital launches. Although more progress needs to be made, the technology is being successfully developed. Also, other companies, such as XCOR and Virgin Galactic, are developing reusable vehicles. Because reusability is associated with cost reduction, it will be a key factor in the competitiveness of the launch providers.

The concern is that because of the novelty of the technology, the method of financially quantifying the effects of reusability on the value of a company does not exist. Not to mention that the effectiveness of the cost reduction from reusability has not been fully understood. In regard to the cost-effectiveness of this technology, Dan Dumbacher, former NASA deputy associate administrator of the Human Exploration and Operations Mission Directorate, cautioned that, “We are not as smart as we think we are and we don't understand the environment as well as we think we do.” 47 The shuttle orbiters were reusable, but the refurbish cost was incredibly high and did not contribute to significant cost reduction. In the midst of the uncertainty, financial analytical models using this key factor, and many other new technological factors of the industry should be carefully examined as to whether they lead to correct valuation of the launch providers.

Furthermore, traditionally, the U.S. launch industry only consisted of a few companies; and launch service was only a part of a list of operations these companies were engaged in. For example, Lockheed, Boeing, and Orbital ATK all have substantial businesses in aerospace manufacturing, defense, and IT services. For most of the new launch companies, however, their sole source of revenue is providing launch services. The method of valuation of a company that operates a wide variety of businesses, of which launch service is a part, should be considerably different from the method of valuation of a company that offers only launch services.

New methods of financial analysis and new performance should be carefully reviewed and proven to accurately evaluate the subject's value. Many financial models have the tendency to be utilized based on the face value of the models, regardless of whether they are accurate or true. If the model becomes commonly used, people tend to believe that the “commonness” of the model validates the “correctness” of the model. In other words, if the majority of the analysts use model A, instead of model B, regardless of the true merits and correctness of the models, model A would be considered more correct. This happened with the new performance indicators of the telecom industry. If the same happens in the launch industry, the consequence may also mirror that of the telecom industry.

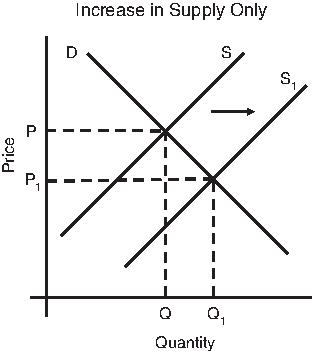

Demand and supply inequality

Based on the classic economic theory, excess supply creates a new pricing point. As shown in Figure 7, when supply increases, the supply curve moves from S to S1. Considering that the demand stays the same, quantity supplied increases from Q to Q1, and as a consequence, the market price, also called the equilibrium price, decreases from P to P1. This means that the product has to be sold at a lower price. If the price is set above P1, the market would not be interested.

Increase in supply and constant demand.

Furthermore, consider the below equations:

Given these equations, if price decreases, revenue decreases, and profit decreases. An industry as a whole, would experience a decrease in profit. When this is applied to the individual company level, the companies in the industry would have to fight for market share to keep the same profit level. In the process of doing this, some companies will disappear from the market, as they cannot make the profit to sustain their operation. As a result, the supply curve will move back to S.

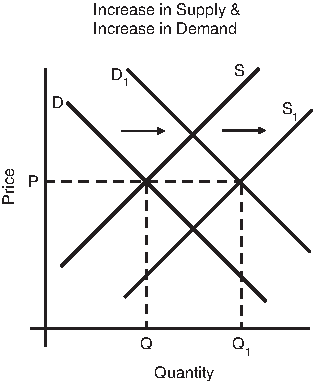

On the contrary, if the market size increases, meaning an increase in demand, the increase in supply will not cause the market price to decrease. In Figure 8, the supply curve moves from S to S1, and the demand curve moves by the same amount from D to D1. In this case, the quantity supplied increases from Q to Q1 and the market price stays at P. When looking at the industry level, profit increases and the industry experiences an expansion. If the growth rate of demand is greater than the growth rate of supply, then the rate of expansion would be greater. If the growth rate of demand is less than the growth rate of supply, the industry will experience a contraction; and this would end at the same result as the constant demand example above.

Increase in supply and increase in demand.

Unfortunately, for both the dot-com industry and the telecom industry, the growth rate of demand was much slower than the growth rate of supply. The industries and the investors believed that the spread of the Internet would be extremely significant and fast paced. Essentially, they pushed out the supply curve as much and as fast as they believed the demand would be spread. This speculation was incorrect for both industries. Profits decreased and the overvalued companies disappeared and with them extensive amounts of capital disappeared as well.