Abstract

Abstract

Entrepreneurs hoping for aggressive growth in space markets cite the commercialization of the Internet as a golden age of market dynamism and enlightened regulation. This study investigates the growth of commercial computing, a business-oriented Internet, and spectrum allocation as historical analogs guiding new space policy. These “digital analogs” share common threads of early military backing that developed many of the technological components, policies encouraging the transfer of technology to the private sector, the discovery of new markets, regulatory flexibility, and the power of venture capital financing to develop new technological platforms and stimulate economic growth.

Introduction

Overview

Commercializing the Internet was a signature U.S. policy success of the 1990s. Between 1990 and 1993, the Internet transformed from a controlled research environment to an open marketplace. An investment boom followed. By the end of the 1990s, the Internet was a vital center of economic growth. Despite the unraveling of the “dot com” venture wave in 2000–2001, worldwide growth of Internet users and Internet traffic continued at a rapid pace. Companies such as Amazon and Google are now central to economic activity. Billions of users and millions of organizations rely on the Internet as an essential communication, entertainment, and productivity hub.

The Internet built upon an earlier information technology (IT) and policy success. The computer owes its origins and first decades of prosperity to governmental funding. The transition to commercial markets relied on technology built with public backing. It was not until the late 1960s, nearly 25 years after the first computers, that commercial markets were the prime drivers of both research and demand. Computing progressed at a furious rate, moving to personal computing in the late 1970s. By the time of the Internet, computing was nearly ubiquitous in advanced economies.

Such success invites comparison. As the United States adopts a more commercial space orientation, some space industry participants are calling for a similar Internet regulatory approach. For example, Jeff Bezos commented that 1 “I want to see the kind of explosive growth (in space) that we've seen on the Internet with all of the entrepreneurialism and the dynamism—it's been kind of a golden age that you've seen over the last 20 years.” Steve Jurvetson, a leading Internet and space venture capitalist, has advanced a similar theme. 2

This study investigates the computing and Internet experience for insights applicable to space policy. At first it might appear that the space and information industries are technologically too far apart for meaningful comparison. We believe this is incorrect. There are multiple connections between the IT experience and the move to commercial space, and the future of new space is closely tied to developments in the Internet and computing arena.

Economic historians distinguish between Smithian and Schumpeterian economic growth. 3 In Smithian growth, the same core set of products and applications benefit from efficiencies, higher quality inputs (such as a more educated labor force), and capital accumulation. In Schumpeterian growth, the major benefit arises through new products, new ways of doing business, and innovative applications. Computing and the Internet have been especially rich sources of Schumpeterian growth. Digital technology now pervades all consumer appliances and entertainment media. Online e-commerce reaches into almost all retail categories, with companies such as Amazon.com changing the face of retail. Online advertising has become the largest advertising venue, with companies such as Google displacing traditional advertising mediums such as newspapers and yellow pages. Streaming media has fundamentally changed the music and movie industry, and is threatening to do so for television. Some of the most important policy lessons from the Internet realm are in supporting Schumpeterian growth.

If we are fortunate enough to see dramatic launch cost reductions due to high levels of reuse, Schumpeterian insights from computing and the Internet realm may be especially valuable. With an order of magnitude fall in costs, many new products and services may become viable.

A second reason to look at the history of the Internet is the role of venture capital (VC). Previous historical analog studies did not concentrate on industries relying on VC financing. VC was critical to the growth and success of Internet commercialization and is showing increasing importance in commercial space. Venture-backed firms have different incentives and seek different payoffs than government or private debt-funded firms.

A third reason to consider the history of IT is a shared concern regarding the regulation and use of spectrum. It was clear in the 1990s that the rapid growth in cellular telephony and mobile data would stress available commercial spectrum. Spectrum auctions pushed the creation of new capacity, encouraging the explosion of cell phone networks and usage. Similar actions may be necessary to procure the necessary spectrum for communication to and from space. There is currently a pitched battle over future spectrum usage between new satellite constellation operators and next-generation mobile systems. This is perhaps the most important short-term commercial space policy decision. Lessons from spectrum auctions may also provide guidance for launch rights, with policy makers using auctions as one method of alleviating air space congestion and clarifying conflicts between traditional aviation routes and expanding space activities.

Even without order-of-magnitude cost reductions in launch costs, Internet lessons are relevant to the new space community due to the impact of the Internet on the demand for commercial space services. Many new space ventures are effectively digital spinoffs. Over the past 2 decades, the dominant share of commercial space demand has been digital entertainment and digital communication (primarily direct broadcast television and satellite radio). 4 SpaceX apparently anticipates space-based Internet services as providing a dominant revenue source, substantially exceeding its launch revenue. 5 Although new space may provide important transportation, tourism, and even mining services, to date and in the medium term it is primarily an adjunct to the IT sector.

Previous Analogs for Space Policy

Launius provides a recent look at historical analogs for new space policy. 6 Launius is especially concerned with funding justifications, but also discusses regulatory issues for the transcontinental railroad, early aviation and aerospace, the telephone industry, Antarctic science, large public works such as the Tennessee Valley Authority (TVA), and the National Park Service. As he states: “Each of the six cases covers meaningful lessons in political culture and circumstances, legal precedent, methods of execution, and change over time. Many are considered positive stories of successful public involvement in the private sector; some are cautionary tales of overreach and over-management; and some present lost opportunities that might have been more successful had circumstances been handled differently.”

Launius considers whether a system of resource grants might work for some commercial space ventures. Like the alternating tracts given to the railroads, partial rights to develop the Moon, asteroids, or Mars could provide incentives for construction and valuable spill-over benefits to others. Two immediate problems arise. First, costs must fall dramatically for such ventures to make economic sense. Second, international law must change. The 1967 Outer Space Treaty currently forbids both national sovereignty and private ownership of astronomical bodies. 7 Unless the United States works to alter this treaty, or exits from its rules, no governmental body has the authority to assign property rights in outer space as an incentive. It is unlikely the United States would choose to exit the treaty entirely, as the treaty also has important and stabilizing restrictions on placing of nuclear weapons in space.

Although government demand provided the bulk of early orders, U.S. policy has always relied on private firms to manufacture planes and provide aviation transport services. Militaries around the world spent heavily to transform the airplane from the Wright Flyer to a reliable craft and effective weapon. In World War I, the United States created the Army Air Service, U.S. manufacturers produced 11,950 planes during the war, and 69 military airfields within the United States. After the war, airmail contracts with the U.S. postal service often provided the financial underpinnings of medium- and low-volume air routes and helped establish strong international routes. 8 During the Great Depression, airport construction was a natural project for the Works Progress Administration (WPA). 9 Multiple regional airports provided large projects sharing similar designs and the need for many construction workers. New airports also spurred highway and bridge construction, 2 WPA project favorites. In an ongoing effort to support new engines and airframe designs, the U.S. government created the National Advisory Committee for Aeronautics (NACA). NACA was a very important source of research and development for aviation for decades.

Developing aviation safety regulations provides lessons and context for the beginnings of space tourism. After high-profile collisions, and many near misses, Congress created the Federal Aviation Administration (FAA). The FAA instituted air traffic controls over the most congested regions and enforced a wide variety of safety measures, inspections, and postaccident reviews. Much of this regulatory infrastructure has been brought forward to commercial space.

Telecom provides one of the more cautionary of the Launius policy examples. For almost a century, AT&T dominated the telephone system in the United States. Most economists and regulators viewed telephony as a natural monopoly. This approach became engrained in Bell system practices. AT&T only permitted its own phones, modems, or faxes to connect to the system. Although court and regulatory decisions loosened these restrictions somewhat beginning in the late 1960s, 10 it required the 1980s antitrust breakup of AT&T to set the stage for the telecommunication revolution of the 1990s. 11

Launius's telecom example demonstrates the possible tension between innovation and competition. Competition policy is challenging when a monopoly arises due to patents, market forces that favor a winner-take-most result, or breakthroughs that allow one company to achieve a dominant market share. This may occur in the space market. For example, the first launch company to successfully deploy highly durable and easily reusable boosters may be in a position to dramatically underprice all rivals and deter potential rivals. Wise policy must balance both short-run and long-run efficiency concerns.

Although the digital analogs share some of the Launius themes, there are important factors not present in the railroad, early aviation, or telecom examples. Digital technologies demonstrate the impact of dramatic and continuous declining costs, and also illustrate the role and incentives of VC financing. Digital industries shape the demand for space assets and enable many of the space systems. Policy makers can learn valuable regulatory lessons from these digital analogs and anticipate some of the growth areas of the commercial space business.

Lessons from the Computer's Rise

Transistors, Technology Forecasting, and the Missing Communication Satellite Patent

A satellite orbiting 35,786 km above the equator occupies a technically special and economically valuable position. Such a geosynchronous satellite's speed just matches the Earth's rotation rate. Geo satellites are a fixed spot in the sky for ground-based antennas, with no tracking required. From such a vantage point, satellites also have a large footprint. A communication satellite in geo-orbit can rebroadcast television signals, relay phone calls, and transfer data to nearly one-third of the Earth's surface.

Geo-orbits are sometimes called the Clarke Belt, due to an October 1945 article published by science fiction writer Clarke. 12 In “Extraterrestrial Relays,” Clarke sketched the feasibility of communication satellites, paying attention to the broadcast and receiving power requirements and the appropriateness of the system for television and FM radio. Had Clarke applied for a U.S. patent, he almost certainly would have received the fundamental patent on using geosynchronously located communication satellites.

In later commentary, Clarke explained his lack of patent filing. 13 It was not an early commitment to open source systems, but rather Clarke's belief that a manned space station must accompany any long duration satellite. Satellites require on-board amplifiers to boost and rebroadcast signals. At the time of Clarke's article, amplifiers relied on vacuum tubes. Vacuum tubes are bulky and consume large amounts of power. Even if they survive the voyage to space, vacuum tubes soon burn out with use. Clarke concluded that geosatellites would require frequent maintenance visits, requiring some form of orbiting space station. Clarke was keenly aware of the requirements of a manned space program, and correctly predicted that a manned station was at least 2 decades in the future. Clarke anticipated that his patent would expire long before any such station, and thus licensing revenue would be moot. Publication gave him credit for the insight, even if geosatellites brought him no riches.

What Clarke failed to anticipate was the transistor. Although Sputnik used vacuum tubes for its simple and short-lived radio beacon, 14 communication satellites have all relied on transistors. Transistors are far more durable than tubes, lasting years without repair. Digital innovation made communication satellites much closer to reality than Clarke's forecast, without the need for orbital repair stations. Syncom 3, launched in 1964, was the first geocommunications satellite and transmitted the Tokyo Olympics live to the U.S. market. Many others followed soon after.

Clarke's “missing patent” illustrates 2 important phenomena. The first is the standard uncertainty that accompanies all innovation. Even someone as astute and imaginative as Clarke missed the possibility of an enabling invention just 2 years in the future. 15 Vacuum tubes were the critical barrier for Clarke, and their replacement was well on the way.

The second point shown by the Clarke example is the fundamental enabling role IT plays for the space program. Commercial space is one of many industries, such as the Internet in the 1990s or autonomous vehicles today, that owe their existence to digital technology. The supply of modern semiconductors, integrated circuits, and powerful computers made the space program possible. 16

From Weapons to Word Processing

The military years

The computer was invented with military funding. As Richard Rhodes comments: “The first problem assigned to the first working electronic digital computer in the world was the hydrogen bomb.” 17 Rhodes further states: “The ENIAC ran a first rough version of the thermonuclear calculations for six weeks in December 1945 and January 1946. Los Alamos prepared a half million punched cards of data, enough to keep a hundred people busy for a year at mechanical desktop machines.” For the first decade of computing, the design of atomic weapons provided the major source of computing demand. The U.S. military was the biggest funder of computing, as weapon projects were desperate for more powerful computing tools to analyze the complex design tradeoffs in both fission and fusion devices. 18

As the Soviets acquired a fission bomb (1949), followed by a fusion bomb (1953), early warning systems capable of detecting Soviet bombers became a critical national priority. Such a system demanded far greater computing capabilities than that existed, with sensors stretched over thousands of miles, and led to tens of billions of dollars invested in the SAGE radar and computing complex. The SAGE system drove many computing breakthroughs, fundamental to later timesharing and interactive commercial systems.

Memory was one of the biggest bottlenecks in computer performance and reliability. Early computers used cumbersome and unreliable display tubes as memory storage. Multiple failures per day, triggered by tube failures or even changes in the weather, were common. A real-time, high stakes system such as SAGE needed vastly better performance and much longer mean time between failure. MIT's Jay Forrester made a major breakthrough with the invention of magnetic core memory. SAGE also pioneered interactive displays, advanced methods of time-sharing, fault-tolerant banks of computers, and other speed, usability, and reliability boosting approaches. 19

It was during the computer's military years that programming went from wiring diagrams to software compilers. The early breakthrough general purpose machines—ENIAC, Von Neumann's IAS machine, Turing's Mark I, the IBM 701, and the SAGE Whirlwind, all used machine language. These multimillion dollar mainframes were difficult and expensive to program. It was not until April 1957 that FORTRAN finally was finished, and then only available on the IBM 704. Other machines, and other programming languages, followed soon after. 20 By 1960, most computers used recognizable programming languages, with high-level instructions compiled by the computer into its own required machine language.

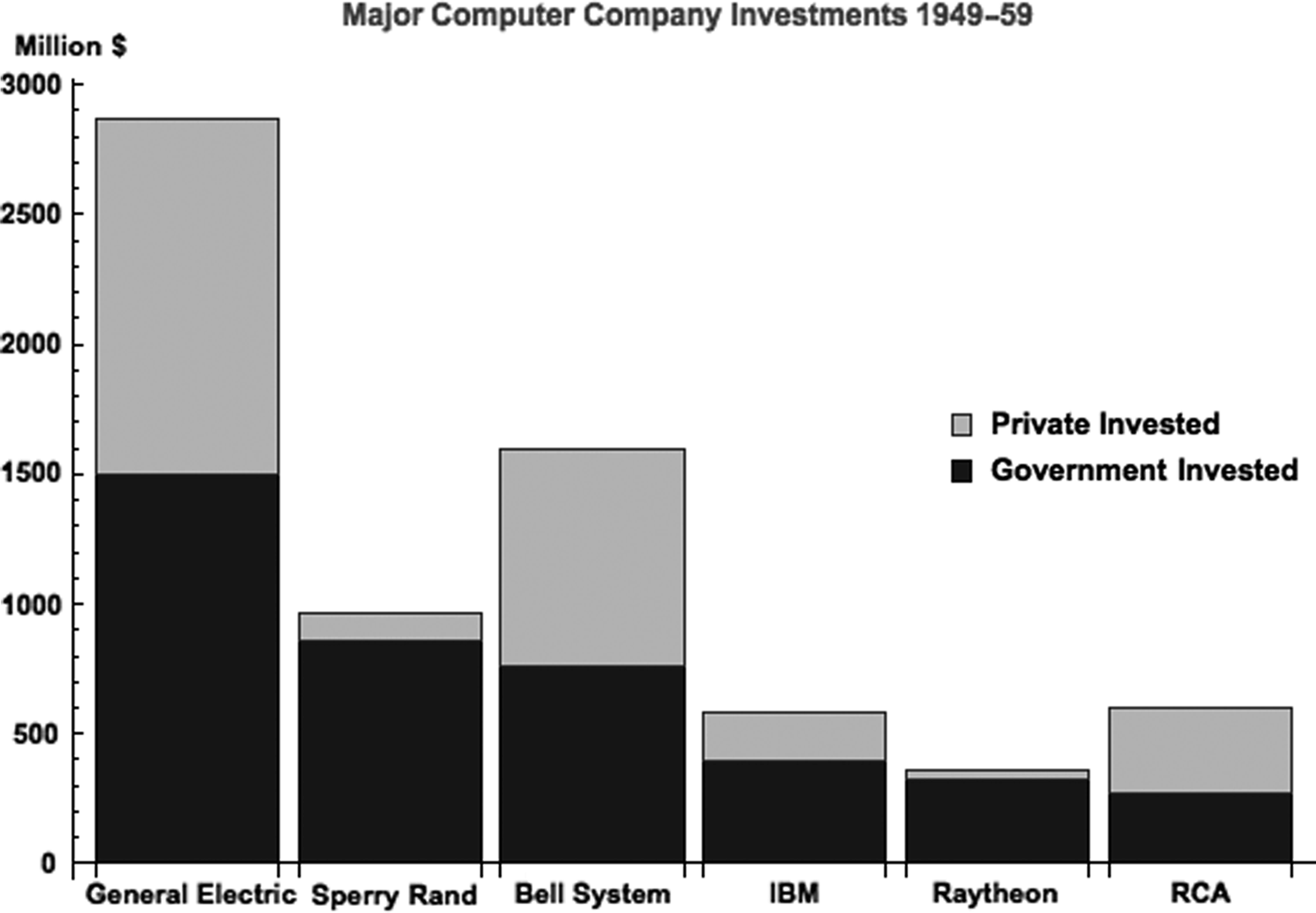

The early wave of computers was almost exclusively government funded. Between 1949 and 1959, the government was the most important funder of research and development. By the end of the period, the balance was shifting toward commercial self-financing, but all the major commercial systems could trace their R&D closely to military systems. Flamm's data, shown in Figure 1, highlight the heavy reliance on government investing in contractor's R&D during the 1950s.

The U.S. Government spent heavily to develop the computer. Data: Flamm. 18

The military was also paramount in funding the development of the transistor. Although computers made great strides between 1945 and 1955, they still relied on bulky, unreliable, and power-hungry vacuum tubes. Were this to continue, computers would remain high-cost specialty devices operated by only the largest of organizations with the highest value needs. What changed this was the introduction of transistors and integrated circuits. With semiconductor logic, computers became vastly more powerful. At the same time, they became much cheaper to build, own, and operate.

Each successive category of transistors, such as the point contact transistor (1948), the junction transistor (1951), and the planar transistor (1958), was developed on government contract: As Riordan and Hoddeson put it: 21

Fortunately, Bell Labs and Western Electric had four wealthy customers—the U.S. Army, Navy, and Air Force, plus AT\&T itself—that were very interested. In the mid-1950s all of them were eager to send, receive, and manipulate electronic signals at the highest frequencies, where the greatest amounts of information could be transferred most rapidly. They were ready to foot the high up-front costs of making diffusion and silicon manufacturing technologies a reality.

Transistors were absolutely vital for the compact advanced avionics used in missiles, satellites, and manned spacecraft. By the end of the 1950s, transistors had replaced tubes in all new computer designs. Integrated circuits would soon follow, where multiple transistors and other circuit elements were combined on a single silicon crystal.

IBM goes commercial and dominates the mainframe market

IBM was not the earliest commercial computing firm. Eckart and Mauchly, inventors of the ENIAC, always aspired to serve the commercial market. As early as 1947, Prudential Insurance was investing in its company and developing a computer for actuarial uses. 22 IBM was the most successful in translating lessons learned on government contracts to the consumer marketplace. IBM's 1950s government contracts implementing SAGE for the Air Force, the Stretch computer for NSA, and the 7090 for the Ballistic Missile Early Warning System all created a technological base and manufacturing capacity that it could turn to creating a consumer computing market. “Well more than half” of IBM's research and development spending in the 1950s was paid for by U.S. government contract. 23 The government attached no royalties or residual payments for this backing, and it helped IBM become the world leader in computing. This is a pattern repeated throughout the decades in computing, where public R&D has been central to new computing capabilities.

Beginning in the 1960s, IBM invested heavily in consumer-oriented computing, leading to the breakthrough System/360. At the time, the System/360 was the largest private investment ever in a new product. IBM invested more than $5 billion in a 4-year period, with $500 million on research and development and $4.5 billion for new plant and equipment. 24

Compatibility was a breakthrough feature of the System/360. The same software could run on the largest or the smallest member of the family. This was a radical improvement in usability, and customer demand was extremely high. The System/360 moved IBM into a leadership position it held for several decades.

Even though integrated circuits were available in the early 1960s, the System/360 was transistor based. IBM moved to integrated circuits in the 1970s, with the successor System/370. Although this was several years after its competitors Control Data and NCR, IBM's combination of compatible software and sales force made it safe for IBM to delay its adoption of integrated circuits.

By the end of the 1970s, the computer had existed for nearly 40 years. IBM was the dominant computing firm, facing a modest challenge from the plug-compatible firms. Minicomputer makers, such as Digital and Data General, had also carved out successful offerings with smaller systems tailored to mid-sized businesses and university departments. Computing appeared to be a stable oligopoly. Industry observers were worried about a lack of innovation and a potential threat from Japanese computer companies. All this would change rapidly with another semiconductor breakthrough.

Personal computing and ubiquity

Computing historian Paul Ceruzzi states that “Second only to the airplane, the microprocessor was the greatest invention of the twentieth century.” 25 This was not Intel's perception when it released the microprocessor. Intel viewed the microprocessor as primarily an industrial control device, and did not envision why anyone would want such an underpowered computer. 26 Intel originally developed its first microprocessor, the Intel 4004, under contract to calculator company Busicom. 27 In the next couple of years it released 2 more powerful versions, the 8008 and the 8080. Intel's 8080 and MOS Technology's 6502 would be the chips to launch the personal computer market.

The personal computer's development fell to hobbyists and startups, rather than established computing firms. The personal computer is a classic example of Clayton Christensen's “entry from the bottom.” 28 Hobbyists and startups create a new, inexpensive product that barely qualifies as a working system. Being cheap, it captures the price-sensitive market willing to live with limitations and partial functionality. Over time, as capabilities grow while retaining a low price, the challenger wins more and more share from the incumbent (and expensive) providers.

The acknowledged first personal computer was the Altair 8800, announced in January 1975, and sold by a small company MITS in Albuquerque. It used the Intel 8080. This is the machine that convinced Paul Allen to join MITS, and Bill Gates to leave Harvard and form Microsoft. A version of BASIC for the Altair was Microsoft's first product.

Microprocessors also stimulated the formation of the Homebrew Computer Club in Silicon Valley, which in turn became a hotbed of personal computing hobbyists. Homebrew's most famous alums, Steve Wozniak and Steve Jobs, launched the Apple I in 1975. By 1977, Apple had become a successful venture-backed startup with the Apple II. Apple went public in December 1980.

The largest selling personal computer in the late 1970s was the TRS-80 from Radio Shack. With a national retail presence, and a willingness to advertise the personal computer, Radio Shack was able to sell several hundred thousand TRS-80s per year from 1977 until the mid-1980s.

IBM was much more proactive when confronting the personal computer market than it had been when confronting the minicomputer. Teaming up with Microsoft, the IBM personal computer quickly became the leading business microcomputer. Over time, personal computers grew to dominate the home market as well. By 1990, IBM personal computers and compatibles had nearly a 90% market share.

Personal computers transformed and expanded the computer industry. In 1974, fewer than 115,000 existed in the world. 29 By 1995, ∼300 million units had been sold worldwide. Computing had become an everyday part of business and society.

The Digital General Purpose Technology

Even after the early computers were developed, businesses continued to underestimate the demand for the new machines. Predicting demand when enormous cost declines have deposited a producer on a distant and entirely unfamiliar region of a demand curve is an uncertain proposition. The lesson, perhaps, is that with a sufficiently new and advanced concept, demand is created by a learning process. Users begin to understand how a radically new piece of technology can fit their needs only through experience with it. Certainly, this theme appears early and prevails throughout the history of information processing technology.—Flamm30

The computer's rise is an example of the broader digital computing general purpose technology (GPT). GPTs are an economic concept highlighting that some innovations are so powerful they serve as the “engines of growth” 31 in the economy. The steam engine, the railroad, electrification, and the internal combustion engine all are acknowledged GPTs. Our era has been dominated by the digital GPT. 32

There are 3 defining features of a GPT. First, a GPT is subject to major cost declines and quality improvements. The early manifestations of the technology are typically expensive and limited in function. Over time, the cost/quality tradeoffs change dramatically. Second, GPTs yield many spinoff industries. Some of these spinoff industries can be sufficiently powerful to be considered GPTs in their own right. Third, GPTs have strong economic and technological complementarities. On the economic side, the fall in the price of the GPT drives up demand for complementary inputs. Systems of production are redesigned to take advantage of the input falling in price and growing in capabilities.

Digital GPT cost reductions

For hundreds of years, computing technology was a backwater. Decades might transpire between improvements. Yale economist William Nordhaus documents the very slow progress from 1850 to 1940 and the exponential improvements thereafter. A key limitation in this early period was the lack of sufficiently precise manufacturing tools. Charles Babbage provides a striking example. In the early and mid-1800s, Babbage created plans for a “Difference Analyzer” and an “Analytical Engine.” His Difference Analyzer blueprints were sufficiently detailed that the British Museum of History used them in 2002 to produce 2 working devices. Babbage's Analytical Engine was much more ambitious, and would have been a full-fledged computer nearly 100 years earlier than actually occurred. Machining capabilities were too crude to build the machine, and mechanical switches too slow, for the computing device to be practical. While Babbage had developed many of the theories and core design principles, as he himself was forced to concede: “another age will have to be the judge.”

By World War II, electronics had developed to the point wherein computers were now feasible. War time needs in cryptography, radar systems, ballistics, and the Manhattan Project 33 provided high priority demands justifying the computer development efforts. The previous 20 years of electronics innovations, especially vacuum tubes, created the necessary components for a digital computer.

Figure 2 demonstrates the astonishing rate of progress of the digital GPT, as measured by the declining cost of computation. 34 Modern computers are over a trillion times more powerful than those early models.

Cost of computing, 1850–2006, with a trillion-fold cost decline after 1945. Data: Nordhaus 34 , Online appendix, 2006 dollars.

Miniaturization is the driving force behind the cost declines reflected in the Nordhaus graph. The underlying physics were sketched out by Richard Feynman in a 1959 after-dinner speech entitled “There's Plenty of Room at the Bottom.” 35 Feynman pointed out the multiple benefits when circuit elements become smaller. Signals travel shorter distances, current requirements drop, material costs fall, and the entire circuit runs faster. This is true regardless of whether the components are tube or transistor, discrete or integrated. As Feynman put it: “There is nothing that I can see in the physical laws that says the computer elements cannot be made enormously smaller than they are now. In fact, there may be certain advantages.” For the past 70 years, computer technology has benefitted from the virtuous cycle of miniaturization. By the time of Feynman's speech, there had already been 15 years of exponential cost decline. This performance improvement has continued for another 55 years.

Although Feynman provided the direction of the computing industry, a short 1965 essay by Gordon Moore of Intel that appeared in Electronics magazine came to be viewed as setting the pace of this miniaturization and cost reduction progress. 36 Asked to consider the evolution of the industry, Moore sketched his thoughts about cost improvements in the rapidly growing semiconductor industry. What is now known as Moore's Law is the steady doubling of computing power and the rapid fall in computing cost. Engineers and business people struggle to maintain pace, and Moore's Law became the focal point for these design objectives.

Innovation in the components underlying digital computing assisted in this race to smaller, faster, and cheaper. The earliest mainframes filled a room, consumed massive amounts of electricity, and failed often. By the late 1950s, transistors replaced vacuum tubes, dramatically improving reliability, speed, and energy efficiency. The 1960s and 1970s saw the rise of integrated circuits, and their incorporation into computer memory and controls. By the 1980s, integrated circuits were powerful enough to support consumer-oriented personal computers. By the end of the 1980s, there were millions of computers capable of communicating and sharing information. At that point, an Internet was both feasible and highly desirable.

The digital GPT has been a central driver lowering the cost of space by reducing the weight needed to perform a task in space. Both the purchase price of satellites and the required mass for a given satellite function have fallen dramatically due to the digital GPT. The biggest difference between space possibilities now and the Apollo era is not in our rockets, but in our computers.

An extreme example of the interaction between space and the digital GPT is a highly ambitious effort by the Breakthrough Initiative to create deep space nanosatellite probes. Funded by Internet-entrepreneur Yuri Milner, the initiative seeks to combine extraordinarily compact electronics, high-efficiency solar sails, and Earth-based laser arrays into a deep space exploration system capable of near-relativistic speeds. 37

Electronic miniaturization is at the heart of the approach. Digital cameras provide a striking example. In precell phone days, digital cameras were bulky and inefficient. Intense market competition, driven by a global cell phone market supply chain, has resulted in vastly smaller, more powerful, and much more energy efficient detector chips and lenses. The same is true of processors, optoelectronics, and other widely used commercial electronic components. The weight of the Breakthrough Initiative satellite components has already fallen by >99% compared with that in 2000. The 2030 improvements needed are modest in comparison. Much more challenging is the propulsion system, utilizing high-power phased-array ground lasers to “push” the nanosatellite toward its target.

Other new space efforts benefit greatly from ongoing digital miniaturization. Companies such as Planet Labs use clusters of small satellites to provide commercial views of Earth for agriculture, mining, forestry, and other uses. Very large constellations of small but powerful Internet communication satellites are being developed for low-earth orbit. As discussed below, for the foreseeable future the new space market is in essence a digital spinoff.

Digital GPT spinoffs and complementarities

Input substitution is one of the most basic and powerful insights of economics. That is, when an input becomes more plentiful, it is efficient to use more of it. This is true for both business and consumer uses. When a technology improves at the rate of the digital GPT, it leads to widespread substitution in an ever-growing number of industries. This is especially the case when new uses and new applications are possible, rather than just more of the same.

Delong and Summers point out that the digital GPT has been able to transform much of the economy by reinventing and expanding its uses. The first 2 decades of computing were dominated by “complicated and lengthy sets of arithmetic operations.” 38 Scientific computing was central to the earliest usage of computing in weapons research and a national radar defense system. Both computing and the space program owe their early successes to the Cold War nuclear rivalry between the United States and the Soviet Union.

In the 1960s, computing moved from primarily governmental to those funded by commercial demand. Corporate databases provided the second broad area of computing applications, with finance and insurance firms using mainframes to track customer accounts and stock market trades. By the mid-1960s, these mainframes were powerful enough to handle real-time databases, such as airline reservation systems and manufacturing inventory control.

Complementary assets are the third defining characteristic of GPTs. Technological complementarities are those “whose full benefit cannot be reaped until many of the other technologies that are linked to it are re-engineered, and the makeup of the capital goods that embody them are altered.” 39 For computing, the most important of these is software.

Although software has always been essential to computing, the software industry was relatively slow to emerge. For the first few decades, computing companies bundled their main packages with the hardware. Software expertise was valuable, and computer services companies emerged as one of the most important adjuncts to hardware. Firms such as CSC and EDS augmented large organizations' computing efforts. 40 IBM announced plans to unbundle its computer systems in late 1968, partially in response to a Justice Department antitrust investigation. Minicomputers and microprocessors always supported third party software.

The personal computer has been especially influential for software innovation. For example, spreadsheets and word processors dramatically altered white collar work. Although it took until 1980 for the U.S. software market to reach $5 billion in sales, by 1990 it exceeded $44 billion and reached $138 billion in 2000. 41

Some of the most widespread and important software is free. There is a long tradition of open source software, partly driven by AT&T's consent decree with the government restricting it from entering computer services. 42 The Unix operating system and the C language emerged from Bell Labs, and became mainstays on university campuses. They would eventually become central to the Internet. The open source movement influenced World Wide Web development, with Tim Berners-Lee and CERN choosing an open source approach to these enabling technologies. 43

Computing and Space: A Symbiotic Relationship

The space program and computing began at roughly the same time and for the same purpose. Both were military in nature, geared to winning World War II and the Cold War. Each was dominated by the specter of the atomic bomb. At the onset, each was impractical for commercial use, requiring major improvements and cost reduction. The U.S. government wisely encouraged commercial adoption of the technologies it funded. By the 1960s, computers were set to become primarily commercial. The IBM System/360 emphasized private sector demand. Military applications continued to drive many of the most advanced integrated circuits, which were then quickly applied in the commercial sector.

Both computing and space are dual use technologies. The balance between military and commercial shifted in computing decades ahead of space efforts. Part of this is technological. Computers are universal devices, and even the most primitive computer can (theoretically) attack almost any problem. Computers were able to evolve gradually from tubes to transistors and integrated circuits. As the digital GPT improved, computing use expanded. Performance improvements meant that the problems that justified computing could move from the existential threat category to more mundane tasks such as tracking insurance policies and scheduling warehouse shipments.

The laws of physics favor low-cost computing more than low-cost spaceflight. Launch thrust, multistage rockets, and required orbital speeds have been well understood since the early days of rocketry. 44 There have been only modest rates of improvement in chemical fuels. Although digital improvements in avionics and communications improved rocket accuracy and control, launch expenses remain high. The dramatic improvements are in the increasing capabilities and shrinking size of the payloads.

Learning from a Commercial Internet

VC and the Netscape Moment

For many investors, the Internet became real on August 9, 1995. 45 This is the day that Netscape went public. The stock launched at $28, tripled during the day and closed at $58. 46 A company that provided mostly free browser software was suddenly valued at more than $2 billion. Netscape was the first big Internet public offering, and it led to money pouring into venture-backed Internet startups.

Microsoft's Bill Gates famously downplayed the early commercial rise of the Internet and Web. Netscape's IPO startled Gates, and even more so the chance that an Internet browser provider might create an alternative operating system to the dominant Windows platform. By December 1995 things had changed, with Gates announcing that Microsoft would become Internet centric. 47 Microsoft had already begun giving away its browser in August 1995, bundling it with Windows. It would aggressively push the use of Internet Explorer (IE), making hardware manufacturers feature IE and creating difficulties for Netscape. Although Microsoft's aggressive attacks on Netscape would eventually be a leading factor cited in its antitrust violations, Microsoft's conviction came after Netscape found it necessary to become part of America Online. Despite Netscape's head start and rapid growth, the power of a dominant incumbent willing to give away the same product as Netscape's main offering was too much.

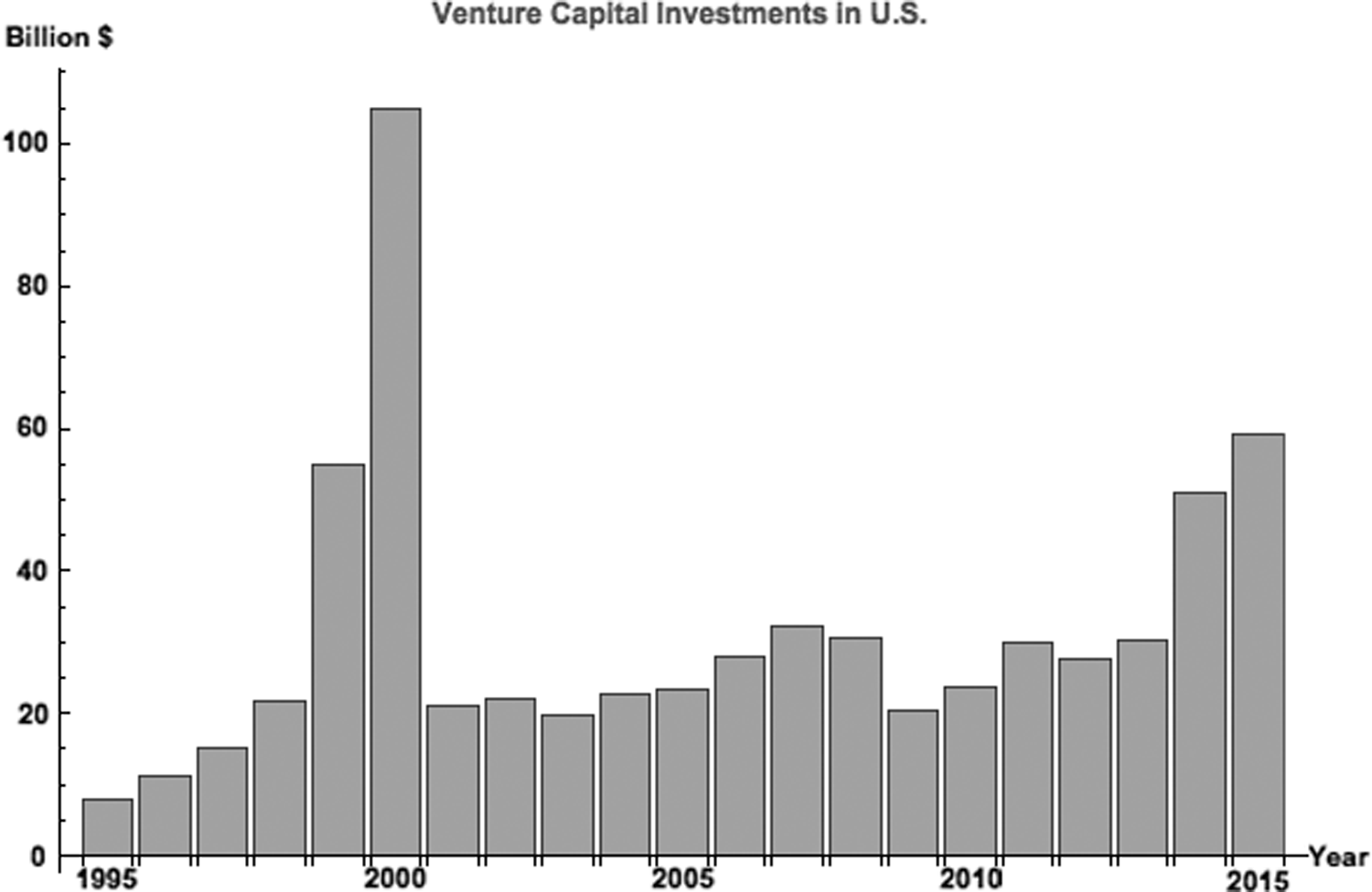

Another feature of the Netscape moment was a flood of resources into a commercial Internet. Figure 3 shows the dramatic rise in U.S venture investing during the late 1990s, driven by the Internet. 48 No subsequent year has come close to the peak level reached in 2000. More than $100 billion of new funding flowed into VC during a single year. The Internet received the lion's share, with $20 billion for Internet software, $14 billion for fiber optics, $20 billion for Internet content, $3 billion for Internet services, and $15 billion for wireless telecommunications. 49 Although many of these VC-funded companies would come to ruin, there were also huge successes.

The Internet spike in the venture capital world. Data: 2016 National Venture Capital Yearbook, nominal dollars.

Founders of some of the largest winners, such as Amazon, PayPal, and Google, are now active in new space ventures. Table 1, adapted from Startup Space, lists 21 billionaires with notable space affiliations. More than two-third of the participants made their fortunes in some version of IT and software. The highest profile examples are Elon Musk and Jeff Bezos. Musk made his fortune as part of PayPal, and risked it all on SpaceX and Tesla. Blue Origin, founded by Jeff Bezos, has had success in landing and reusing its suborbital launcher. Planetary Resources is another space venture attracting investments from Internet veterans. Google is prominent with Larry Page, Eric Schmidt, and Kavitark Ram Shriram. Charles Simonyi, with a Microsoft background, is also a backer. Planetary Resources has asteroid mining as a long-term goal, with Earth observation as part of its shorter term objectives.

The Well-Heeled Space Funders with Internet Backgrounds

Source: Forbes Billionaires, Tauri Group.

These new space leaders bring a mindset and culture nurtured in the Internet world. They have called for an “Internet moment” for the commercial space program. In one sense this is ironic. Space has already had a decade exceeding the 1990s Internet. Between 1960 and 1970, the “Apollo moment” poured money and talent into the race to the moon. Apollo funding came from the government, motivated by Cold War politics. The Internet alums and new space founders hope for something different, a critical private success that crystallizes investor perceptions that space is good business.

VC operates differently than government contracting or debt-based financing. One of the challenges for effective regulation in commercial space is coexisting with the timescales, market needs, and culture common to venture-backed startups.

This section begins with the precursors to a commercial Internet and quickly reviews the movement from propriety systems to an open Net. As with computing, Advanced Research Projects Agency (ARPA) and other agencies funded many of these Internet capabilities. After deregulation, the venture-funded boom sealed the transition.

Setting the Stage

Proprietary networks

Almost as soon as computers appeared in large organizations, researchers began experiments to remotely access these machines. Bourne and Hahn document a wide variety of efforts in the 1960s and early 1970s, highlighting the many “firsts.” 50 Database search was a key theme, tapping into library catalogs and retrieving scientific journal abstracts. By 1975, there were commercial firms such as DIALOG, LEXIS, and Dow Jones News/Retrieval providing online data access. These companies targeted large businesses with support staff, as the data services were both expensive and difficult to use.

Early U.S. consumer online services faced numerous challenges. When CompuServe launched in 1976, the typical modem speed was a glacial 300 baud. Services had to maintain a very “light”page load. Services distributed CD-ROMs with graphics to augment the online textual content. Usage fees were $12.00 per hour during the day and $5.00 an hour off-peak. 51 Despite their limitations, online providers The Source, CompuServe, DELPHI, MCImail, GEnie, The WELL, and AOL pioneered consumer online access during the 1980s. Features included online forums, messaging, online encyclopedias, financial services, e-commerce, e-mail, special interest groups, and games.

There were parallel efforts in Europe, especially England and France. In 1981, travel agents could order online through Thomson Holidays. In 1984, a small e-commerce experiment let residents of Gateshead, England, order groceries, prescriptions, and bakery items. 52 The French Minitel service was much more extensive, and demonstrated the power of rapidly available information, relative ubiquity, and the tendency to create unexpected services. 53 Minitel utilized text-based information and relied on specialized Minitel terminals. Eventually it would become something of a drag on French Internet adoption during the mid-1990s. 54

By the late 1980s, dial-up speeds had increased by an order of magnitude. Costs also fell. The Prodigy online service was able to introduce a relatively low monthly flat rate price ($9.99 at service introduction) for its new service combined with online graphical advertising. The Prodigy Services Corporation was a household shopping and information service that connected home computers with an online network of servers configured to provide a multitude of education, information, and entertainment services. Prodigy was originally developed as part of a joint venture between CBS, IBM, and Sears, Roebuck and Company and launched in certain test markets in 1988 and nationally in 1990. Whereas CompuServe originally started to serve the business community and then branched out to serve home users, Prodigy followed the reverse course. The primary focus of Prodigy was the home user, only later in its history did Prodigy attempt to launch a business services division. 55 These early consumer systems were a marketing revelation. Marketers realized that with the rise of personal computers, fax machines, and value-added online services, they had a new and potentially much cheaper and more powerful method of directly interacting with customers. Computers allowed direct marketers to store individual transaction data cost effectively. The new online services suggested they could utilize this personal information to more effectively target and communicate with individual households. Peppers and Rogers pointed out that this had profound effects on the economics of direct marketing: 56

For what it cost a 1950 marketer to keep track of all the individual purchases and transactions of a single customer, today's marketer can track the individual purchases and transactions of several million individual customers, one at a time.

The proprietary online services demonstrated latent demand for online capabilities. These limited systems needed a more flexible, cheaper, and interconnected technological approach.

Defense Department's Advanced Research Projects Agency creates the Internet

The commercial Internet and World Wide Web grew out of decades of research, heavily sponsored by Defense Department's ARPA and other research agencies. The Internet was already 25 years old when it was deregulated. It was, and continues to be, an especially powerful and expandable set of technologies for general purpose online communication. 57

The governmental origins of the Internet have been well documented, and mirrors early efforts in graphical personal computing. 58 The role of the Defense Department's ARPA, especially the Information Processing Techniques Office (IPTO), is again central. ARPA funded the basic packet switching research of Paul Baran, the initial network deployment in 1969, the original IMP servers, and the operation of the early Internet nodes by the consulting company Bolt Beranek and Newman.

Throughout the noncommercial era, the research network continued to develop capabilities we now view as fundamental. Among the notable are e-mail appearing in 1973, message groups in 1975, and TCP/IP in 1983. At each stage of this development, researchers reached consensus on core features, produced working code, and documented their work. An especially valuable innovation was the “Request For Comments” (RFCs) online database. RFCs began with the earliest stage, with RFC 1 published on April 7, 1969. The full catalog of RFCs continues to grow, 59 and serves as “the principal means of open expression in the computer networking community.” The success of the Internet approach has strongly influenced open source software generally, with many projects mimicking the governance approach.

The Internet becomes friendly

The World Wide Web originated outside of U.S. funding, but in a very similar setting and with active participation in the RFC process. Tim Berners-Lee was working at CERN in Switzerland in 1990 and was struggling with a method of sharing the huge and varied data emerging from particle accelerators. CERN researchers across the globe needed to share and annotate information, much of it including imagery. From these efforts came the concepts of URLs beginning with http, 60 web pages mixing text, images, and links, and many of the specifications so familiar and popular. Other users quickly realized this was a useful tool in many settings, far beyond particle physics. CERN also produced the first web server, with public demonstrations in 1991.

A final critical piece of enabling software was the browser, again emerging from a laboratory setting, this time the National Center for Supercomputing Applications in Urbana-Champaign. Programmers there made a “point and click” interface for the Web, releasing it in 1993, and making Internet use accessible to novices. Many of these NCSA Mosaic programmers relocated to California and formed Netscape. Although there were some disputes regarding naming rights, again a core feature of the Internet began with public funds and was then transferred to the private sector.

By the end of 1993, the main software pieces for a friendly point and click interface to an efficient TCP/IP Internet were in place. What was also needed was access and transmission, which occurred with a modest regulatory change of great consequence.

Freeing the Internet

For much of the 20th century, the telecommunications system on the United States was a regulated monopoly. Had this remained the case, the Internet as we know it would not have happened. “Ma Bell” was very strict with allowable communications. It took a Federal Court decision in 1956 to permit users to attach a snap-on cup to a phone mouthpiece to make a call more private. 61 More devices were possible after the 1968 Carterfone decision, permitting an acoustic client-side link between the phone system and a radio call. AT&T actively worked against competition of any form in long distance, even if transmission occurred over private microwave lines.

These actions and others led the U.S. government to prosecute AT&T on antitrust grounds. 62 The conclusion of the case was a consent decree breaking AT&T into a national carrier and 7 regional Bell operating companies. Although many of these companies have subsequently recombined, with AT&T and Verizon the main surviving companies, 63 during the 1980s and 1990s the U.S. telecommunication network was freer than it had been in a century. In particular, there was no legal presumption against entry or a dominant firm enforcing its choices on the network backbone. This competitive opportunity supported the next critical decision of the government, turning over the Internet backbone to private hands.

For the first 16 years of its existence, ARPA managed the Internet backbone. The first connection occurred in September 1969, linking UCLA and the Stanford Research Institute. By 1971, the network connected a number of the key computer science departments and IT contractors. By 1980, the ARPANET incorporated most of the leading research universities and national laboratories.

In 1985, ARPA transferred control and operation of the nonmilitary nodes of the ARPANET to the National Science Foundation. At first the NSF focused on improving operations of the (now) NSFNET. 64 The backbone speed was increased, although minuscule by modern standards. 65 It entered into a 5-year managing contract with MCI and IBM/MERIT to run operations.

The NSF insisted that the Internet operate for noncommercial research purposes. The guiding document was the NSF Acceptable Use Policy. In particular, users of the NSFNET were not supposed to advertise or place commercial orders. 66

“The purpose of NSFNET is to support research and education in and among academic institutions in the United States by providing access to unique resources and the opportunity for collaborative work.

This statement represents a guide to the acceptable use of the NSFNET backbone. It is only intended to address the issue of use of the backbone. It is expected that the various middle level networks will formulate their own use policies for traffic that will not traverse the backbone.

1. All use must be consistent with the purposes of NSFNET.

2. The intent of the use policy is to make clear certain cases that are consistent with the purposes of NSFNET, not to exhaustively enumerate all such possible uses.

3. The NSF NSFNET Project Office may at any time make determinations that particular uses are or are not consistent with the purposes of NSFNET. Such determinations will be reported to the NSFNET Policy Advisory Committee and to the user community.

4. If a use is consistent with the purposes of NSFNET, then activities in direct support of that use will be considered consistent with the purposes of NSFNET. For example, administrative communications for the support infrastructure needed for research and instruction are acceptable.

5. Use in support of research or instruction at not-for-profit institutions of research or instruction in the United States is acceptable.

6. Use for a project that is part of or supports a research or instruction activity for a not-for-profit institution of research or instruction in the United States is acceptable, even if any or all parties to the use are located or employed elsewhere. For example, communications directly between industrial affiliates engaged in support of a project for such an institution are acceptable.

7. Use for commercial activities by for-profit institutions is generally not acceptable unless it can be justified under (4) already mentioned. These should be reviewed on a case-by-case basis by the NSF Project Office.

8. Use for research or instruction at for-profit institutions may or may not be consistent with the purposes of NSFNET, and will be reviewed by the NSF Project Office on a case-by-case basis.”

Under such a policy, most of the modern Internet would be prohibited. There could be no ad-supported Google or Facebook, no ordering through Amazon, no ticket purchases at Expedia, or countless other activities.

Even with these restrictions, the utility and growth of the Internet continued. By 1990, there were ∼1 million Internet hosts. Capacity growth was needed, and the NSF increasingly felt the demands of network operation would conflict with its support of basic science. At the same time, political leaders were pushing to open up the Internet to additional uses.

Greenstein (2015) details the NSF handoff to private industry. 11 After some initial jockeying by lead contractors for a preferential position, NSF reached a final plan for the handover in May 1993. MCI and IBM continued to operate the backbone, but without a requirement for enforcing the Acceptable Use Policy. Various networks were strongly encouraged to interconnect, and firms developed a method of traffic interchange. Several of the core assets of the Internet, such as the DNS registry, were transferred to private hands in a manner eliciting complaints of cronyism. This aside, the transfers happened quickly and smoothly. By 1994, the Internet was open for business, able to carry both research and commercial traffic. One of the largest investment bursts in innovation was about to occur.

A Commercial Internet

Venture-funded innovation

After privatization, entrepreneurs needed backing for their new ventures. To an unprecedented degree, this was provided by VC. As discussed in Hanson (2000), there was a positive feedback loop involving investors, users, and entrepreneurs. Or, as Mowery and Simcoe put it 67 :

Although antitrust and deregulatory telecommunications policies remained influential, defense R\&D spending was overshadowed by private sector R\&D investment by the 1990s. And one of the most important mechanisms for Internet commercialization was the US VC industry, which assumed a larger role in the commercial exploitation of the Internet than had been true during the formative years of other postwar US high-technology industries.

Large pools of capital, such as pension funds, insurance companies, and other large investors, manage portfolios worth hundreds of billions of dollars. Finance theory shows that efficient and diversified portfolios should devote a (small) portion of their assets to high-risk, high-return investments. Over the past few decades, one preferred method for this risky investment is early stage VC investments in high-technology startups. Some of the largest global corporations, such as Apple, Cisco, Google, and Facebook, trace their origins to this form of risky investing.

Most pension and life insurance companies lack the experience to invest in startups. Instead, they outsource this fraction of their portfolio to VC firms. VC firms gain skill in identifying startup teams with both good ideas and the ability to transform these new approaches into successful companies. The various VC firms organize funds stressing particular areas of emerging technology, such as the Internet, clean tech, or life sciences.

VC firms do not lend money. Rather, they buy an ownership share in a startup. The size of the equity share is in proportion to the funds invested, as well as the current startup valuation. The earliest investments in a new company can be the most lucrative, but they are also the most likely to fail. For example, the earliest investors in Google were able to purchase shares at ∼4 cents a share. These were worth $85 at IPO, or more than $800 per share in 2017. One of these early investors was Jeff Bezos, who invested $250,000 in 1998. If Bezos held on to his Google shares, they would be worth approximately $2.7 billion.

As a startup does not repay a venture investment, which it would with a loan, a VC firm must eventually be able to sell its shares to recoup its original investment and make a profit. Some form of “exit event” is required. For major successes, such as Netscape or Google, this is an initial public offering. More commonly, an acquisition by a more established firm provides the mechanism for selling shares.

Venture investing is a game of averages. In the majority of cases, the venture-backed startup fails to go public and receives only lukewarm acquisition interest. For a venture fund to make money, the few big wins must offset these more numerous failures or modest successes.

The venture capital system is a key reason for the importance and continuing success of Silicon Valley. VC firms and startups have long coexisted in the Bay Area, with veterans of successful companies occasionally starting their own venture operations or joining established firms. Proximity increases the chances of discovering the next big thing, meeting the best entrepreneurs, and bringing in additional investing partners to lower the exposure to any one investment.

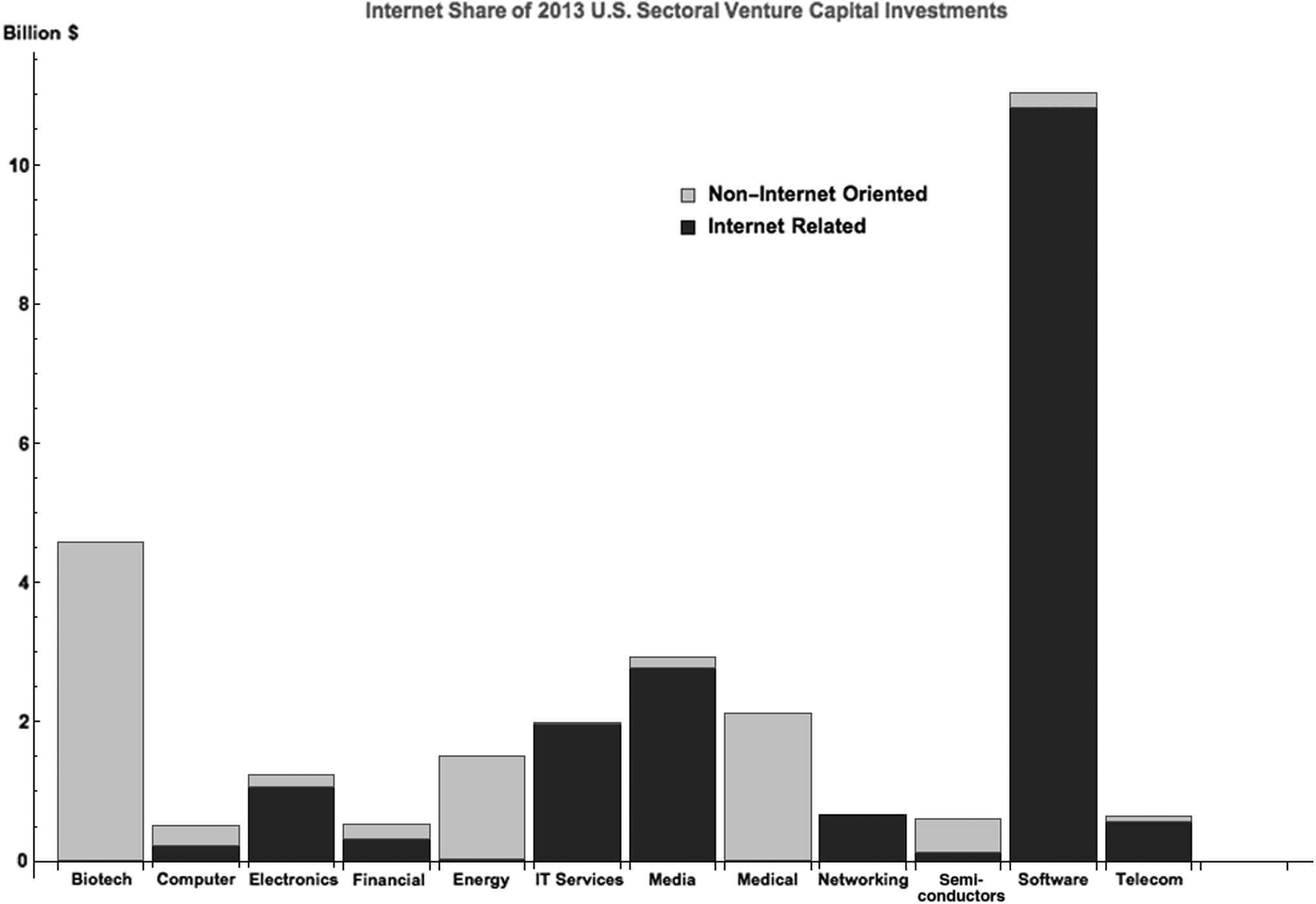

Silicon Valley has had the good fortune of operating with the power of the digital GPT at its back. For more than 6 decades, IT has been central to the Valley's economy. Moore's Law created an ongoing stream of new computing opportunities. Engineers substitute digital technology into more industrial devices, production processes, and final goods. This sequence includes such broad areas as mainframe computing, avionics, minicomputing, personal computing, the rise of the Internet, social media, and mobile computing. Perhaps no other technological area has been so rich in the potential for continual improvements and spinoffs, and the association of IT with VC has been very close. Successful venture capitalists became quite good at extrapolating from current possibilities as new price points emerged. Figure 4 highlights just how widespread the importance of the Internet still is among venture-backed startups.

Internet venture investments occur in many industry sectors. Data: National Venture Capital Association 2014 Report.

Space investments do not appear separately in Figure 4. If they did, the Internet's influence would be large as well. Startup Space reports $1.8 billion in space-related venture investments in 2015. 68 Of this, $500 million went to OneWeb and $900 million from Google to SpaceX. OneWeb is entirely Internet related. Although neither Google nor SpaceX confirms the exact arrangements for their agreement, their agreement appears to be targeting the Internet-related constellation being planned by the firms. This would total $1.4 billion of the $1.8 billion for just those 2 firms alone.

E-commerce pioneered the commercial Internet, but advertising pays the bills

E-commerce was at the core of the first wave of Internet startups. The “dot com” revolution sought to transform both business to business and consumer sales, and attracted a burst of VC funding. Several factors accounted for this emphasis. Facing challenges for Wal-Mart and other “big box” stores and a lack of expertise, existing retailers were slow to adopt online sales. 69 This lack of response created a perceived opportunity for startups, especially in consumer categories such as books, music, consumer electronics, and computers. Business marketplaces hoped to challenge existing supply chains in a wide array of industries. A wave of IPOs seemed to validate these entrants, with investors willing to fund retail startups with very little track record and negative cash flow. Many of these startups came to ruin in the 2000–2001 shakeout, never able to effectively reach profitability. Existing businesses, especially in the B-to-B market, woke up to the power of the Internet and used their existing supply chains and marketing expertise to thwart the startups.

Despite the failure of many speculative ventures, there were notable successes. Amazon.com expanded its product lines from books to almost everything, and has managed to expand its sales substantially every year. It is now a retailing powerhouse. EBay serves as the order-taking interface to tens of thousands of small retailers. Dell and other computer makers pioneered direct sales to consumer and build-to-order systems. Music retail pioneer CDNow expanded the available range of titles dramatically over physical stores, and early digital download sites such as Napster showed the power of purely digital delivery to transform the music business. Thousands of other online retailers, both hybrid and online only, expand their reach to a national (and occasionally international) market using the Internet. Consumer e-commerce is still <10% of retail sales, ∼$500 billion in 2016. The e-commerce retail share has followed a (seasonally adjusted) steady upward trend since the Census Bureau began tracking it in 1999. 70

Although e-commerce has been a notable commercialization success, the Internet's impact on the advertising market has been profound. As seen earlier, the NSF Acceptable Use policy prohibited advertising. The commonly acknowledged first advertisement using the Web, a banner ad paid for by AT&T, appeared on the hotwired.com web site in October 1994. 71 It ran on the top of the page and when clicked led the user to the advertiser's web site. This simple format would remain the dominant method for the first decade of online advertising.

Advertising revenues have long been central to the commercial Internet. During the early years, it funded the rise of online portals Yahoo!, InfoSeek, Excite, and America Online. Much of the money spent by the dot com retail startups went to marketing expenses, especially online advertising, driving the development of many of the online portals, search engines, and access providers. Thus, the early growth of online advertising was closely tied to the dot com wave.

The first wave of Web advertising had few of the current capabilities, lacking even the ability to reliably measure impressions. Early online approaches emphasized sponsorship of particular web site sections, especially on leading Internet portal sites Yahoo! and America Online. In addition to exclusivity, a key feature of sponsorship is duration-based payment. Advertising sites specify pricing by time interval, such as cost per month, rather than by viewership levels or user actions. Sponsorship became less common, and performance-based methods more important, as Internet companies developed appropriate metrics.

Search engines, most notably Google, provided a second wave of advertising growth. Search engine advertising reached beyond online retailers and tapped into thousands of small and medium sized traditional businesses. Advertising format simplicity, combined with strong measurement tools, made it possible for these advertisers to shift their advertising dollars from newspaper and Yellow Pages to search spending. For example, Google AdWords generate billions of dollars of revenue using a few lines of text with links to advertisers' landing pages. More recently, social media and video content have grown to be important advertising venues.

Advertising dollars tend to follow consumer time usage, and the many online applications increasingly attracted viewership. Relevancy, especially for search, has made online advertising very effective. Even primitive ads can be highly effective if they reach the right consumer at the right time.

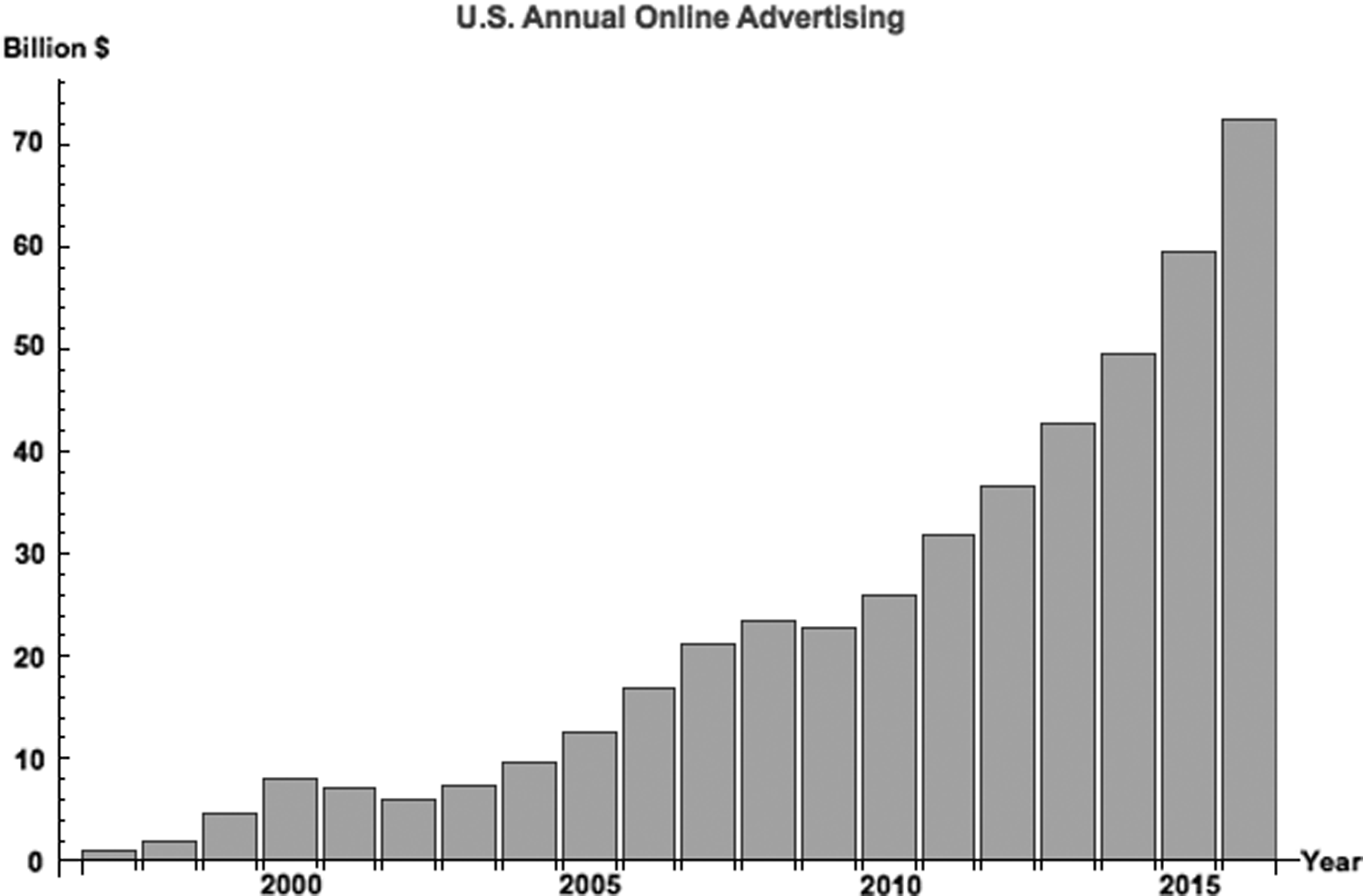

From its humble beginnings in 1994, online advertising revenue is now larger than newspapers, magazines, radio, and even television. In 2016, U.S. online advertising revenues grew >21% and exceeded $72 billion. Some of the most sophisticated technologies in Silicon Valley, such as massive clusters of servers, big data analytics, machine learning algorithms, and artificial intelligence, are devoted to achieving slight improvements in online advertising effectiveness.

Figure 5 shows the rapid growth in U.S. online advertising revenue, with no obvious plateau. 72 This is striking for at least 2 reasons. First, early participants did not view the Internet as a major advertising venue. Deregulators were familiar with some of the most popular services on the Internet, such as e-mail, chat groups, and bulletin boards, and expected them to be popular outside of the research community. Web pages also looked promising for sharing commercial material. There was little discussion during the early 1990s that the Internet would be a major advertising venue and, except for modest success by online services such as Prodigy, little historical basis for optimism. Indeed, a best-selling business and marketing book published in 1993 stressed the interactive potential of faxes rather than the Internet. There was also an antipathy to advertising by many early Internet entrepreneurs, including Brin and Page, who did not initially plan to utilize advertising as part of Google's approach.

U.S. online quarterly advertising revenue. Data: Internet Advertising Bureau, various years, nominal dollars.

The economics of advertising is a second reason why Figure 5 is so surprising. Aggregate advertising spending is primarily a zero-sum game between advertising venues. 73 For decades, U.S. advertising spending has been ∼2% of gross domestic product (GDP). Growth rate of Internet advertising far exceeds the growth in the economy, coming at the expense of other advertising approaches.

As with the computer, there is a strong element of Schumpeterian surprise in the business applications of the Internet. It is highly unlikely that a committee sitting in 1992 could have foreseen the dot com boom or the dramatic rise in Internet advertising. Yet, by permitting these activities, policy makers allowed a creative wave that has altered many aspects of the retail and advertising industries.

Venture-Backed Space Startups and Regulation

Startups are risky and prone to failure. A startup can fail due to technological risk, mismatches with the marketplace, the entry decision of a dominant firm, execution mistakes, and a host of other factors. Successful venture firms learn to distinguish “good failures,” and reinvest in an individual or team with a promising idea, even if they had a previously failed startup. Startups can take big chances, knowing that a failure is not fatal to their entrepreneurial career. One of Silicon Valley's strengths is the recycling of personnel.

Venture funds are structured to allow time for startups to succeed, and to weather any macroeconomic downturns. Venture funds have protections against early withdrawals of funds, as well as provisions that may require additional investments when market conditions are unusually challenging. As long as the long-term expected return is high, this risk fits into the diversification strategy of the ultimate investors. VC's patience and tolerance for failure are much higher than the political or bureaucratic systems. Industries where VC is important reward behaviors that (occasionally) generate unusually high returns. Examples include rapid prototyping, multiple product releases with incremental improvements, and aggressive timetables for new products.

Researchers and industry participants note that changes in the IT ecosystem over the past decade have substantially lowered the entry costs of software-based entrepreneurs. This has lowered the necessary venture funding for many entrepreneurs. When Facebook experienced its extraordinary growth in 2004–2006, it struggled both financially and technically to provide enough server capacity to meet its rapidly expanding usage. Server capacity was much less of a problem for later companies such as SnapChat or WhatsApp. Just a few years later, these startups were able to scale to hundreds of millions of users by relying on cloud providers for both the hardware and the network management skills. Only some aspects of space-based businesses have experienced such entry cost declines. As seen earlier, it is now possible to create small satellites at a fraction of the cost of previous generations. Secondary payload methods can lower the cost of launch. However, many space ventures are still heavily weighted toward large upfront expenditures.

Although venture culture has much to commend as an engine of rapid innovation, there are some common biases and social challenges. As the venture mentality spreads, more broadly into space activities, regulators should anticipate areas where regulatory invention might be required. However, regulatory forbearance may be even more important. A key distinction is between business and physical risks. By and large, business risks should be tolerated. Physical risks are much more the province of regulation, especially for third parties. Current FAA policy allowing higher levels for risk for willing participants during experimental flights reflects this position.

As seen in the late 1990s Internet boom, venture enthusiasm in particular fields can overheat. In retrospect, certain investments will seem wasteful or even foolish. This is inevitable, and is often the cost of achieving breakthroughs and exploring the technological and economic potential of innovations. Although it is easy to find examples of unwise investments and excessive entry, regulators should avoid the temptation to dampen this competitive dynamic. Handling business risk is one of the competitive advantages of the venture industry and one of the biggest weaknesses of the political process.

Policy makers should especially resist the temptation to be an equalizer between incumbent providers and disruptive entrants. A classic setting is price competition. If a new venture is able to undercharge an incumbent service provider, regulators should be very cautious about blunting this competitive pressure. Christensen and others have stressed the power of “entry from the bottom.” Market entrants may get a foothold by providing a low-cost, limited feature service. Over time, the entrant's capabilities grow while still retaining a cost advantage. Faced with a threat to market share and profits, incumbents often resort to lobbying and special political deals rather than a market response. It can be politically tempting to carve out demand segments isolated from competitive forces. This is rarely beneficial to society as a whole.

Venture backing may overemphasize blockbusters and ignore small but necessary improvements. Space projects may require collaborative or public solutions to provide certain necessary but unglamorous innovations. Technological roadmaps and collaborative standards can be valuable aids to an otherwise venture-oriented commercial sector.

Supporting Innovation with Spectrum Auctions

The Internet in Your Pocket

When Steve Jobs introduced the iPhone in 2007, he began with a bit of a tease, claiming to be announcing 3 breakthrough products that day. The first seems quaint today, a multitouch iPod, but at the time the iPod was Apple's biggest moneymaker. The second was a new category for Apple, a smartphone with phone and data capability. The third was a mobile Internet communicator. Of course, these were not 3 separate products, but the first iPhone.

The iPhone would propel Apple to the highest valuation of any company in the world. Google followed with the Android mobile system, utilizing a multivendor approach that helped broaden its reach and lower its price. In 2016 alone, 1.5 billion smartphones were sold globally. 74 This is an amazingly fast diffusion of such an expensive product.

Smartphone data usage has caused congestion of existing networks and high demand for additional radio spectrum. Smartphones use a variety of radio bands. The first iPhone incorporated quad-band GSM, Edge, Wi-Fi, and Bluetooth radios. The second-generation iPhone added 3G for faster data transfer and satellite GPS for location services. By 2011, an iPhone included a world phone with GSM, HSPA, and CDMA radios. High-speed 4G LTE data services appeared in 2012. Apple added short range NFC capabilities for secure payment systems in 2014. Android phones have followed a similar path. Apple and Google now operate platforms with millions of apps available through their online stores, allowing users worldwide to hail a ride, book a room, engage in banking, postmessages to friends, or thousands of other activities. 75

Even before the smartphone, the rapid spread of cellular phones was affecting the commercial space market. A notable example was Iridium, the pioneering commercial low-earth orbit constellation creating a global satellite phone system. 76 The build-out of the terrestrial cellular network and the spread of the Internet were 2 of the most important reasons for Iridium's commercial failure and bankruptcy. By the time Motorola was able to bring Iridium online in 1998, a global traveler could already e-mail back to the home office or use a roaming signal on a cellular network in most major cities in the world. The Internet and cell phones dramatically lowered potential customers' willingness to pay for the Iridium handsets and usage plans.

Neither of these alternatives was significant market forces when Iridium was designed and funded, and supplanted much of Iridium's forecasted demand. After much political wrangling, Iridium was saved from deorbiting by the U.S. military. Iridium remained valuable to Special Forces, Marines, and drones going into distant battlefields. Iridium's global ubiquity could justify its limited data rates and high prices.

5G networks are the next step for high-speed mobile data transfer. These 5G networks hope to rapidly transmit even the highest resolution image and video. There is a serious problem however. Some of the spectrum that is most promising for 5G terrestrial networks is also highly desirable for LEO-based satellite Internet. Current international agreements tilt toward a space usage for this spectrum. Lobbyists on both sides are pushing to secure more spectrum for their respective systems. Spectrum may well be the biggest limiting factor for either 5G or LEO Internet reaching its technical and market potential.

Efficient spectrum allocation was another digital policy success of the 1990s and 2000s, and it helped the Internet make a smooth transition from desktop to pocket devices. This section reviews spectrum policy, its economic logic, and lessons going forward in the coming spectrum battles.

Spectrum Markets

Allocating spectrum

A wide variety of wireless services use spectrum, including broadcast radio, television, point-to-point microwave, satellite, and radar. The U.S. Commerce Department governed the early days of radio broadcast, generally under a “first come, first served” regime and court adjudication of disputes rather than in a regulatory proceeding. With the passage of the 1927 Radio Act, the Federal government asserted more control in assigning licenses to specific operators, designating specific bands for specific uses, and mandating the use of specific technologies.

The 1934 Communications Act assigned to the FCC responsibility for managing non-Federal spectrum “in the public interest.” The National Telecommunications Information Agency is responsible for Federal use of the spectrum. The FCC has historically determined what services and technologies can make use of specific frequencies of the electromagnetic spectrum through an administrative rule making process.

Despite whatever success the FCC might have at determining an optimal combination of service and technology at any point in time, continuing changes in consumer preferences and technology eventually cause that combination to become suboptimal. As the divergence between the value of the current service and potential new uses increases, so do the gains from reallocation. The FCC's increasing reliance on market-based spectrum policies has facilitated such reallocation.

Leo Herzel 77 in 1951 and Ronald Coase 78 in 1959 set forth the intellectual underpinnings that such licenses could (and should) be awarded by markets rather than by a governmental process. The key insight of Herzel and Coase was that the FCC added no value to the allocation/assignment process as licenses would end up in the hands of those who valued them most highly on the secondary market and the FCC process simply hindered such ultimate allocations.