Abstract

The global Space Industry's transition to New Space—that is, smaller and cheaper hardware and more easily accessible space data—is expanding space-related economic activity into new, peripheral geographical areas. This paradigm shift has been particularly successful in establishing a budding ecosystem of small-to-medium-sized enterprises in Scotland, which is sometimes referred to as the “Space Glen.” These developments are linked to the U.K. and Scottish policymakers addressing the growth of the Space Sector within the innovation policy, rather than a separate Space policy/program. In this review article, I argue that the resulting small-scale and dispersed investment in R&D and business development put forward by the various governmental actors led to the creation of dispersed and divergent clusters of firms, strongly linked to research expertise at local universities, as well as other sectors with more mature markets, such as oil and gas and forestry. Recently, these have been joined together in a common regional sectoral identity, through industry-led grouping initiatives, mainly through promotion at events. Deploying mixed-method data collection and document analysis, this scoping study examines the interplay between innovation policy and emerging sectoral structures in the space sector and poses further questions for a more detailed understanding of the “Space Glen” phenomenon.

Introduction

The Space Sector is currently undergoing a major industry transition, often described by players as the emergence of “New Space,” 1 which is defined on one hand by promises of radical technological innovation, especially through hardware cheapening and miniaturization 2 and on the other hand wider access to open satellite data. 3 In particular, these developments have expanded toward new user groups (local government, educational sector, small-to-medium-sized enterprises [SMEs]) with the introduction of New Space developers in previously peripheral geographies. 4 One of such key locales is Scotland in the United Kingdom, where a dynamic ecosystem of New Space firms, mainly SMEs was established, something referred to as the emergence of the “Space Glen.” 5

One of the underpinning factors for the transition and expansion of the Space sector is the emergence of new markets based on the commercialization of space activities away from Space Industry's traditional alliance of government public procurement and multinational corporations.6–8 This alliance was linked to the military origin of the majority of governmental space programs, something referred to in the past as being part of the military–industrial complex. 9 As such, public sector procurement of civil and military space technology has been the pivotal part of space policy since the Space Race. 10

However, with the “digital revolution” in the 1990s and 2000s, small (nano-) satellites and data analytics platforms are now within reach of private customers and the New Space development is, in fact, a feature of more broad innovation policy, rather than a purely space one.11–14 Hence, the focus is moving away from the traditional government role in the sector and from multinational corporations toward SMEs as centers of economic activity. However, government policy and positions of a variety of actors still crucially shape the development of the “New Space” sector through innovation policy and related interventions. This collective “buzz” is particularly felt in geographical contexts where the past involvement with the Space Sector was at best peripheral, such as the space industry in Scotland. Although many such ambitions arose in many locales around the world, in particular how did the now well-known Scottish “Space Glen” develop?

To try to answer this question and understand the emerging trends it examines, I carried out a scoping 4-stage enquiry in the development of the Space Sector in Scotland presented in this article. The rest of this article is structured as follows. In the next 2 sections, I outline the overall framing of the Space Sector value chain and its transition to New Space, exposing the need for a better understanding of SME innovation dynamics. I then propose a set of 4 scoping research question and a mixed-method approach to answering them. As a result, in the subsequent 4 (combined results and discussion) sections, I develop economic, policy, geography, and community angles on the sector. Specifically, I first analyze the economical significance and historical context of the policy development of the wider U.K. Space Industry and its Scottish subset, which is examined through the U.K.-wide innovation agenda and the Scottish regional economic development one, leading to dispersed investment. Second, I survey the clusters that make up the Scottish New Space Sector. Third, I examine how Scotland's Space Sector has become “unified” and known as one of the growing places for the New Space industry by developing a regional sectoral identity through a series of shared events. Fourth, I explore a series of actors' views on these political aims and economic configurations of the sector. In conclusion, I discuss some limitations of the current study and propose a further research agenda.

Background Review: The Structure of the Space Sector

Globally, the increasingly varied and interconnected economic activities concerning Outer Space* are routinely collectively labeled “The Space Sector,” which is defined by the Organization for Economic Co-operation and Development (OECD) as including:

[…] all actors involved in the systematic application of engineering and scientific disciplines to the exploration and utilisation of outer space, an area which extends beyond the earth's atmosphere.

15

Sometimes, this is also referred to as the Space Industry or indeed included in bigger terms such as Aerospace, which incorporates Aviation as well. It is important to note that for the purpose of the analysis presented here, which is mainly based on secondary sources, 2 areas of the Space Sector activities are excluded. The first of these are Military/Defense Applications, which is by and large classified data, but rumored to be up to 10 times the worth of government's civil space exploration programs. The second is direct public investment in Space Science and Space Exploration for scientific purposes, which is delivered through research grants and multinational agencies subscriptions. Although this is often not accounted for directly, its impact on the economy is captured in the overall econometric data.

The different technology-based subdivisions of the value chain are at different development stages, for historical and commercial reasons.1,16,17 The Space Sector analysts distinguish between 3 key types of technology applications and consequently products/services involved: Earth Observation (EO), which is predominantly based on multispectral imaging; Geo-Positioning and Navigation, most commonly associated with geo-positioning systems (GPSs); and Telecommunications and Broadcasting, with satellite television being the dominant part of this arena.16,18,19 All 3 of these applications are enabled by the work of many scientific disciplines and crucially by civil, mechanical, electronics, and aerospace engineering. The most mature and profitable of these areas is the telecommunications one 20 since the signal transmission was the first and easiest product/service to develop, requiring only 3 types of technologies: launch capability, in-orbit power generation, and signal reception/transmission. These technologies were developed early in the commercialization of the space exploration, whereas more complex components, such as digital signal processing (key for EO) and high precision atomic clocks (key for Satellite Navigation), were slower developed and adopted and are by and large still too expensive for private commercial deployment, although this is now changing.

Analysts ordinarily split the Space Sector into 3 main areas according to the overall value chain: upstream—consisting of hardware development and launch infrastructure, mid-stream—satellite launch/deployment, operation, and data downlink, and downstream—made up of data processing and applications.1,19,20 In the next 3 subsections, I examine the 3 main parts of the value chain in greater detail, in particular, exposing the historical makeup of the value chain, before moving on to address its expansion in the New Space Arena in the next section.

Upstream

The high-tech R&D and technology development demands a large-scale engineering-based business-to-business market. Due to the consequent need for significant upfront capital investment and resources, the upstream segment of the global Space Sector value chain is dominated by “big global players,” such as multinational corporations Airbus, Boeing, Lockheed Martin, and others.20,21 Investments in projects delivered by these upstream players are often very expensive and only within reach of governments (in particular, the United States and Russia), international agencies (such as European Space Agency [ESA]), or a small number of corporations who specifically operate in space-related business (e.g., satellite TV broadcaster BSkyB and satellite telecommunication provider SES). 21 Importantly, due to the complexity of products and the technology-requirements-dominated design, the innovation model in this segment is closed, with a very large amount of IP protection, commercial secrecy, and often issues related to national security.21–23 As will be discussed in the later section “Policy Angle: Space and Innovation Policy in the UK,” this is also one of the reasons that a slower rate of development and growth is predicted in this area in the United Kingdom and globally.16,19,24

Traditionally, in the upstream arena, the smaller players, SMEs, and entrepreneurs only provided a limited range of specialized (niche) products; however, several smaller companies have managed to scale up, quite often only to be bought up by one of the “big players.” 25 As a U.K. example, the large multinationals Finmeccanica (in 2008) and Telespazio (in 2011) acquired systems engineering firm Vega, 26 and the conglomerate Airbus took over the small satellite manufacturer Surrey Satellite Technologies. 27 Across Europe, the 4 large industrial holdings represent ∼70% of the Space Sector's workforce and win 70% of the ESA contract spending. 21 However, as the satellite technology is becoming smaller, cheaper, and more standardized, an opportunity is emerging for entrepreneurs to capture the “New Space” markets through Mini-, Micro-, Nano-, and Pico-Satellites. These roughly correspond to satellite sizes of less than 500, 100, 10, and 1 kg, respectively. 28

Midstream

The midstream enterprises in satellite launch, on-board systems management and operations, and data acquisition are often attached to either downstream or upstream segments. However, there is a growing interest in the development of this diverse segment of the value chain, as technological miniaturization seems to be expanding the demand for its services. In particular, new opportunities are arising in the area of small launch capabilities, in particular expanding the capacity and geographical distribution, as well as the proliferation of technological systems.29,30 Hence, “spaceports” are being conceptualized as a significant way forward, 31 moving toward horizontal capability, that is, airborne launch, and into new locales,32,33 including Scotland.

In terms of the downlink, as all the data are transmitted from locations in space, “open access” was initially a default position and there was no specific data downlink element to the value chain. However, with the increased volumes of data traffic, particularly in the most advanced EO activities, the industry moved to “packaged” high-bandwidth downloads between specifically tasked satellites and selected ground stations. This is not only a technical challenge, but it is also limiting data receiving to satellite's “handlers.” In many cases, this restrictiveness is counteracted by “open data” policies,3,34 that is, protocols for “open access” sharing after the high-resolution data download, which is a key component of the ESA mandate and hence incorporated in all ESA EO projects,35–37 although more concerted effort in archiving and developing data pipelines is being called for.38,39

Downstream

In contrast to the upstream segment, in particular, the downstream part of the sector has for a long time been a more open and competitive environment as issues of national security aside, broadcasting and telecommunications—and lately EO and positioning navigation as well—are built on the principle of a wide access to data and 2-way interaction between the data producer or enabler (i.e., the space company) and the user or consumer. 40 A good anecdotal example is Sputnik, the first artificial satellite ever to be launched in 1957. This USSR built device transmitted a series of “beeps” while in orbit around the Earth, which every citizen in every country could hear as long as they had a radio receiver. 41 With the advancement of encryption technologies in 1970s–1980s, these data became commercially useful, that is, satellite TV works only with a decoder 42 ; however, the distributed nature of data receiving and low requirements for processing remain dominant in broadcasting/telecommunications and navigation part of the sector, making it the largest and most established part of the downstream space industry—and the most profitable, too.

In addition, even at the height of the Space Race, the science done in space and from space was publicly discussed and many modern research satellites transmit information in such a way that anyone with appropriate receiving technology can collect it (e.g., Meteosat, SeaStar, and the NOAA series). 43 However, both through the previously mentioned wider availability of high-resolution data as well as increasing access to computing power, the need for (advanced) data processing and analysis gave rise to the new commercial opportunities. These opportunities are further enhanced by significant political commitment and investment into global sustainability and development programs based on space-powered geoscience intelligence, 44 which is largely delivered through science-driven spin-off and entrepreneurship.

The entry of these new players in different segments of the value chain (nano-satellites in upstream, small-scale launch providers in midstream, and open access data applications in downstream) marks what the industry analysts describe as the transition toward the “New Space” era. 1 In particular, a significant expanse of the space applications arena and refocusing of infrastructure toward larger distributed systems of individually smaller, cheaper, and more dynamic units mark a departure from past innovation practices in the Space Industry, toward a more open, cooperative, systemic configuration of players. In the next section, I analyze the history behind this transition and outline aspects of theories of innovation, which may help to develop a better understanding of the changes it brings to the value chain.

Industry Transition and Emergence of “New Space”

In the past few decades, the global Space Industry Sector's historic development moved into its third phase. After the initial state monopoly in the 1960s and 1970s (first phase), the technology was commercialized in 1980s and 1990s by large multinational corporations (second phase) and is now (since 2000s) being democratized through innovation and entrepreneurship (third phase).1,16 The latest development trend (from second to third phase), possibly setting the future of the sector, is commonly described within the Space Industry as “New Space.” This term is describing a set of key changes to the makeup of the Space Sector's products and the introduction of new markets and liberalization of established ones, which used to be dominated by government-backed or large corporate monopolies. 16 This is particularly visible in 3 trends: first, an increase in commercial tendering for government programs, in particular with regard to “services” such as launch capability and operations management. Although the corporate monopolies are still dominant in the “classical market,” disruptive technologies are making this area much more competitive, for instance, through entrants such as SpaceX (working on reusable launch rockets) and Virgin Galactic (space tourism). 45 Second, the Smaller Satellites (<500 kg) market has been established, operating outside the traditional paradigms, with relatively cheap, “not-(as)-complex,” mass-produced products. Third, there is a significant expansion of space data market, driven by the high-tech tail end of the development of data science and global connectivity creating data storage, analysis, and access to information on an unprecedented scale. For instance, there is increasing investment into open-access space data by global players, most notably the European Union (EU). 46

Electronic devices, which are a key component of space technology, were made more versatile, compact, and also cheaper with the IT advancement over the past 20 years. 2 This not only made more complex missions possible, previously burdened by the weight of the equipment since the cost of spaceflight is still measured in the number of kilograms one needs to launch into orbit, but are also cheap enough for them to be treated as expendable. 47 For instance, CubeSats, the most popular form of Nano-sats, are of a size of 10 × 10 × 10 cm (>10 kg) and can be built for as little as £30,000–50,000. 48 However, due to the (small) size of these devices, the power generated by the solar panels mounted on them is insufficient for some applications, although solutions such as launching a constellation or network of several smaller satellites are being explored.

However, an additional driver for this development was the re-definition of the Space Sector actors, with both new countries 4 as well as new communities emerging.1,49 Although the latter will not be examined in too much detail in this article, it is particularly interesting that these new communities are being actively developed. On one hand, (super-) angel investors with interest in space, for instance, Elon Musk (SpaceX), Richard Branson (Virgin), and Jeff Bezos (Blue Origin), 1 are attracting significant international expertise into their (new) entrant firms' R&D processes. On the other hand, through the establishment of a “Global Space Community,” composed of space enthusiasts now globally connected via the Internet, actual public/citizen science and crowdfunding operations (e.g., Mars One, Lunar Mission One, Planetary Society) are being enabled. 49 While there always was a large community of space enthusiasts, they were previously unable to participate in most of the actual developments due to key barriers to entry, such as the need for amassed expertise and significant capital investment.

However, New Space-related changes are taking hold in all aspects of the Space Sector. 1 Particularly noted in the (popular) media is the commercial launch capability in the upstream segment of the industry, which is delivered by emergent large corporations bankrolled by the previously mentioned angel investors.45,50,51 However, due to the persistently high development costs and reliance on public procurement contracts,52,53 the more economically and societally interesting New Space development is in satellite miniaturization and proliferation of space data application solutions. 54 In particular, SMEs are key for the (smaller end) of the Small Satellites market and emerging data applications, where the transition to New Space is being most clearly demonstrated. With the cheaper core technologies and easier access to space data, companies are being set up on the basis of a new generation of products and services (e.g., nano-satellites and data analytics platforms), which are being developed more closely with the end users 55 (e.g., local government, multinational corporation, and community groups), and are based on “productization” of R&D solutions into mass production. 56 In essence, this approach, new to the Space Industry, is transforming the SMEs involved into end product manufacturers, rather than business-to-business subcontractors and suppliers. 57

With these changes in market access strategy and investor profiles, the innovation dynamics are also changing. In particular, the new product development is moving away from focusing on single-mission complex products and services and toward mass manufacturing. Hence, if innovation is split along what core management literature describes as 4 categories (or “4Ps”) of innovation: “product,” “process,” “position,” and “paradigm,” 58 my summative analysis of the trends outlined above shows that all 4 of the “4P” innovation categories in the New Space Sector are changing substantially, as outlined in Table 1. Such significant changes also align well with the famous Schumpeterian definitions for radical innovation, 59 modified to take note of the specific technological/sectoral focus, 60 as new products, processes, value chains, markets, and business models are all emerging within the sector.

4Ps of Innovation Analysis of the Transitions Observed in the New Space Industry

SMEs, small-to-medium-sized enterprises.

Although some analysts challenge the notion of a natural state monopoly over the Space Sector as relics of historical involvement, 12 that perception is prevalent in particular in the context of the main space powers such as the United States.61,62 Furthermore, space policy has always been seen as a critical domain for states and individuals attempting to project political leadership, 63 which was also recently evidenced in the U.K. parliamentary context, with Members of Parliament attempting to frame their role in championing their constituencies, while referencing “national aspirations.” 64 However, in the post-Cold-War era, these policies predominantly revolve around the power of innovation.13,14 In particular, on one hand, the discourse is built on the expectations of technology transfer from publicly funded basic and applied science,65–67 and on the other hand, the creation of new markets for the Space Sector applications68–71 as part of economic (development) policy. Hence, the Space Sector's growth is being supported by deliberate top-down policy interventions, often delivered dispersedly by publicly backed innovation intermediaries, while it also relies upon a pre-existing environment and bottom-up entrepreneurial action, that is, the Open Innovation approach.72–74 The latter has been extensively studied in particular in Europe22,23; however, there is a gap in in-depth studies of links between the policy frameworks and emerging specific innovation ecosystems. 11

Developing critical understanding how SMEs interact with each other to frame an emergent New Space cluster is of particular interest, as it underpins the belief that technology transfer and bottom-up industrial entrepreneurship are sufficient conditions for the success of current space innovation policies. One of the most significant examples is the emergent Space industry in Scotland, United Kingdom.5,75–78 Hence, to fill this gap and understand the interplay of the innovation policy and New Space entrepreneurship better, in particular in the context of a smaller regional unit, I propose a further analysis of the historic and contemporary development of the Space Sector within Scotland—the “Space Glen”—with particular reference to innovation policy and industry perspectives, collective and individual.

Methodology: Unpacking the “Space Glen”

Investigating the interaction between space/innovation policy and industrial/entrepreneurial activity requires a multilayered approach, to unpick each element separately and then contextualize them with each other. The scoping study presented here is based on both comparative analysis of secondary sources (major policy and econometric trends) 79 and primary data collection by mapping out the emergence of the specific interplay between policy and industrial/entrepreneurial activity. It is structured around 4-partite enquiry of the framing of overall economic and policy development (from document analysis), the geographical configuration of industrial/entrepreneurial activities (participation in over 45 industry event and site visits) and the practitioners' views of all these (with 5 scoping interviews).

In the following sections, I begin with an analysis of the U.K. and Scottish Space Sector and the plans for its expansion, which represent a distinctly institutionalized view of this dynamic and challenging economic area. In doing so, I have formed questions about the experience of actors as my research philosophy being build on abductivist critical realism80–82

—that is, following the questions emerging from analysis and interaction with the field of study. In particular, having examined the historical and political context, as well as informally engaging with key stakeholders, I distilled 4 interrelated strands of enquiry:

What is the economic significance and policy landscape of the United Kingdom and more specifically Scottish Space Sector? How is the Scottish Space Sector configured/structured? How and where has the “Space Glen” framing come about? What is the actor's view on these developments?

To answer these questions, I have first conducted a detailed survey and analysis of secondary sources,79, † cross-referenced with informal discussions with the gatekeeper organization and the Scottish Space Sector players, ‡ to map out the economic profile, trends in policy agenda, and sector's geographical structure. This was summarized and structured using thematic narrative analysis to address the main questions relating to formal economics (in particular turnover and its segmentation, employment statistics, and companies' structure), policy (history of space policy, formation of innovation policy, and Space Sector targets), and geographical positioning (the number and location of firms and their clustering).

Second, I have addressed the conceptualization of a joined-up vision of the “Scottish Space Sector,” that is, the “Space Glen” as it emerged through a variety of institutional players and in particular through conferences and events, 83 which I examined ethnographically through participatory observation84–88 (please see a list of sites in Appendix A1). This was based on unstructured information gathering through taking part in activities within the sector through one central gatekeeper, a team delivering one of the flagship business development projects in the sector.

Finally, to have a more complete understanding of how the economic, policy, and geographical contexts are perceived by the actors in the sector and hence provide a descriptive critique of the “Space Glen” conceptualization, I have carried out a set of 5 scoping semi-structured interviews89–92 with carefully selected key stakeholders. § As noted by several economics and social science scholars, investigations of professionals' views on a set of topics are best carried out through a technique based on a clear framework of themes, but allowing for enough flexibility to digress if addressing important points, that is, the “semi-structured” approach.93–96 The questions in the Interview Guide ware deliberately broad and open-ended, to encourage interviewees to address issues without too much influence of the interviewer. 90 In addition to answering any single specific question, my participatory observation of, and interaction with, these different groups of practitioners over several years of my research provided me with a comprehensive overview of how representative the conclusions reached through document analysis and interviews are, as well as framed the identification of the lead themes presented in the next 4 empirical sections.

Economics Angle: Space as an Emerging High-Tech Powerhouse

The economic performance of the overall U.K. Space Sector is measured with the biannual The Size and Health of U.K. Space Industry survey97–101 and by the evolving impact assessment of the Space Sector contribution to the U.K. economy, put forward in the regularly updated Case for Space reports.102,103 In particular, as presented below, the analyses explore turnover, employment, and market/firm structures. Some of the elements of these analyses contain regional breakdown, so can be further examined in terms of the Scottish Space Sector.

The latest results in the 2018 survey, 100 which contain the figures for up to 2016/2017 financial year, show that the long-term growth trends are slowing down overall, although picking up from a slump in 2014/2015. For instance, the average growth rates for 2016/2017 stand at 3.3%, up from the 1.7% low point in 2014/2015, but still well behind the earlier highs of 7.3% in 2012/2013 and 7.5% in 2008/2009.98–102 This is also in contrast to previous long-term trends, for instance, the 2014 report estimates the average year on year growth in turnover since 2008/2009 at 8.6%, in comparison to 8.8% for the period since 1999/2000. 98 However, this is perhaps not inconsistent with the overall upward trends, due to the change in the economic climate in recent times; also, the Space Sector growth was at this point still well ahead of U.K. GDP (1.5% average since 2008/2009, 1.6% since 1990/2000).

Perhaps unsurprisingly, the key reason given for the overall stagnating growth emerging from the econometric data presented above is “economic uncertainty,” initially in the aftermath of the financial crisis (pre-2016) and uncertainty surrounding the United Kingdom exiting from the EU (post-2016).99,100 This is clearly related to the importance of trade with European partners, as Europe is the destination for 54% of exports (49% in 2014/2015) and the source of 69% of imports (inputs). 100 In addition, EU-funded programs, such as the global navigation system Galileo, account for 4.8% of total nondirect-to-home-television industry income. 100 Hence, the U.K. Space Sectors' trade association, which is behind the Space Innovation and Growth Strategy (IGS) group, has released a leaflet outlining the critical need for continued close cooperation with EU. 104 Although access to EU and overseas markets might continue after implementation of new (free) trade deals,** the disruption to R&D investment could be a significant setback, as well emerging geostrategic challenges. 105

The U.K. Space Sector turnover in 2016/2017 was estimated at £14.8bn, of which less than 1% (£140m) was generated in Scotland. 100 There was also only very modest growth in this period, only £6m increase from 2012/2013 (which was in line with overall U.K. trend).98,100 However, the U.K. Space Sector was estimated to include 41,929 jobs directly in 2016/2017, of which 7,555 (18%) are based in Scotland, within only 132 firms (9% of total 948). 100 This is a significant increase in employment since 2012/2013 (by 32% indirect terms and 2.5% over national growth) when Scottish companies accounted for only 5,709 jobs of 36,696 total (i.e., 15.5%). 102 There is also a significant increase in company formation, as it grew from 67 in 2012/2013 to 104 in 2014/2015 to 132 in 2016/2017 (or 35% and 22% increase, respectively).98–100 The combined figures of relatively low turnover but high employment and firm number growth show the significance of (New Space) start-up firms in the Scottish Space Sector, with capital investment (still) being the predominant factor in its current growth; in line with the overarching R&D intensity of the whole sector. 102

Overall, 70% of all the analyzed companies in the United Kingdom were found to be SMEs, with a highly skilled workforce (75% have higher education qualification). 99 The Space Sector is found to be very export-oriented with 37.4% of turnover is from exports (growing from 36.4% in 2014/2015 and 31% in 2012/2013) or even 65.4% if discounting the effect of the predominantly domestic broadcasters, which make up a significant part of the sector.99,100 Foreign investment in the U.K. Space Sector was also on the rise, with a 40% increase in 2006–2015 in comparison to the previous decade. 102 However, the industry is very concentrated with four organizations accounting for 67% of total income, and 7 for 76%. 100 This shows in terms of growth rates as well since very large enterprises account for 56% of overall growth, although the larger SMEs (28% of total growth) are growing particularly fast (31% per annum, compared with very large enterprises at 2%). 100

The key industry dominating the sector is Satellite Broadcasting, most of it concentrated in 1 company, BSkyB. This segment of the sector accounts for 51% of the total turnover. 100 Due to the dominance of space applications (including broadcasting), with a 71% turnover share of the entire sector, it is not surprising that 51% of the Space Sector customers are private individuals (although that is dropping, as it was 78% and 65%, respectively, in the 2012/2013).99,100 However, as shown in Figure 1, Scottish firms are much more equally distributed along the value chain, with 2012/2013 turnover split on 23% in upstream (manufacturing), 33% in midstream (operations), and 44% in downstream (applications). 106 This is in contrast with the United Kingdom as a whole, where the same split is much more downstream dominated (8%, 12%, and 78%, respectively), even if the dominating Satellite Broadcasting is excluded (which brings it to 17%, 27%, and 52%, respectively). †† ,106

Breakdown of the Space Sector's turnover by value chain segments for Scotland and the United Kingdom as a whole. Data from 2012/2013, as reported in The Case for Space 2015 and Development of the Scottish Space Industry.

In summary, the analysis of the U.K. and Scottish Space Sector economic position points to a specifically fertile ground for Government-backed bottom-up expansion. In the next 3 sections, I will unwrap the origins of the translation of economic activity into innovation policy and then into practical interventions, then proceed to try to map how the Scottish New Space industry is structured and what are the views of the practitioners involved in it on space innovation policy, which supposedly got them there.

Policy Angle: Space and Innovation Policy in the United Kingdom

The United Kingdom was one of the first countries to invest in space exploration program, having space presence in 1962. Crucially for the development of commercial Space Sector, it was the only one to fully commercialize its launch capabilities 17 —now part of a European concern Ariane—putting the development of (upstream) space technology out of government's reach. Moreover, U.K. investment mechanisms in this area are peculiar as they joined several (European or American) space-related projects, which were evaluated separately on “value for money” basis, 107 without reference to any national framework or program. In fact, setting up the U.K. Space Agency, an independent coordination body with its own funding portfolio and a comprehensive development strategy, was completed only in 2010. 108 Moreover, many other funding agencies are involved in space-related research programs, with STFC, EPSRC, and NERC being the prime examples, which make the funding landscape complex and somewhat uncoordinated. Consequently, I argue that the overarching policy direction is one of a “free-market-led” development, working to support science and industry, rather than actively steering it through large investment and specific industrial procurement programs, which is seen by many analysist as a U.K.-specific success. 109

The commercial U.K. Space Sector has shown exponential expansion in 1980–1990s, although this was predominantly on the back of one area—satellite broadcasting—which has limited potential for further growth due to established dominance and market saturation. Since the early 2000s, the sector's growth slowed in terms of turnover, but growth in the number of companies and the variety of products on offer continued. A particular trend was a significant increase in spin-out from U.K. universities as well as new opportunities within the ESA. The latter grew significantly over this period (2000–2015) with the backing of the EU, currently providing 25% of ESA budget through a direct contribution on top of that of the member states. 110

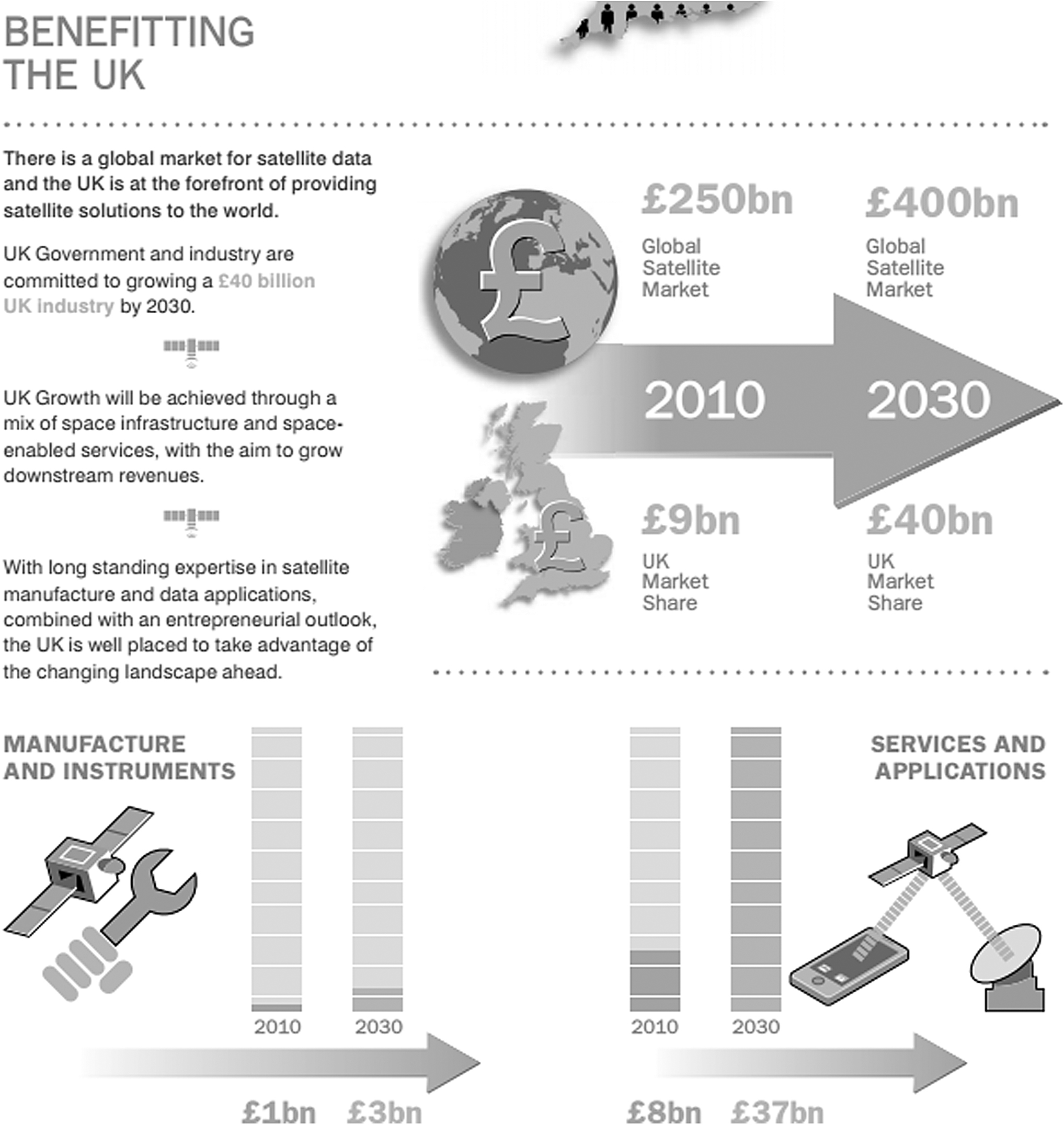

To make further significant gains in terms of growth of the U.K. Space Sector, a new industry-developed and government-backed strategy was formed in 2010 in the move to “New Space.” 16 Central to this policy is a government-backed target of increasing the U.K. share of the global space market from 7% to 10% by 2030,16,17,111 estimated to be worth £40bn of the £400bn total. Similarly, Scottish Enterprise (SE) acting on behalf of the Scottish Government (under U.K. devolution) has the ambition to see 10% of that economic activity based in Scotland. 106 These targets are seen as somewhat unreliable today, as they are prone to severe impact from currency exchange rates fluctuations, although current analysis shows that starting from the original base point, the ambitions are being met so far. 99 It is important to note that as shown in Figure 2, most of this growth is expected in the downstream part of the sector (with £37bn of the £40bn total), which is based on products and services in applications of space technology, rather than the more investment intensive upstream developments.

Projected growth infographic from “Satellites: The Big Picture” (2014). 19

Critically, these targets are to be achieved mainly through a set of flagship interventions to shape the overall sector, in particular through R&D grants and investment in commercial space activities, 108 but not through a full-scale government-led program. 109 As proposed at the time of its establishment, the U.K. Space Agency here assumed the role of a funder and regulator, but not actual developer, leaving the R&D to the industry–science collaborations. 16 This is in line with general U.K. innovation policy since 2010,112–115 in part built on a pivotal “8 Great Technologies” policy white paper, 17 which proposed a mix of governmental steer in supporting the existing industries through new opportunity areas. Satellite applications were included, and this framing, which also supported the Space Sector, has extended into the current U.K. Industrial Strategy's attention for space. 116 These complementary, yet also diverging approaches are pointing to different perceived niche opportunities in the sector, as well as the complex and dispersed nature of the sector.

For instance, the U.K. Space Sector's development since 2010 is framed by the Civil Space Strategy 2012–2016, 108 which is built upon the U.K. Government/U.K. Space Agency backed, but industry-designed Space Innovation Growth Strategy.16,117 On the basis of this strategy, Space IGS produced Space Growth Action Plan, 111 which highlights 5 areas of required actions:

Develop the high-value priority markets identified to deliver £30 billion per annum of new space applications by promoting the benefits of Space to business and Government and engaging service providers.

Make the United Kingdom the best place to grow existing and new space businesses and attract inward investment by providing a regulatory environment that promotes enterprise and investment in the United Kingdom.

Increase the U.K. returns from Europe by continuing to grow the U.K. contributions to ESA programs and securing greater influence in large European-funded programs.

Support the growth of U.K. Space exports from £2 billion to £25 billion per annum by 2030 by launching a National Space Growth Programme and defining an international policy that will improve collaboration with nations across the world, enhance the U.K. competitive edge in export markets, and enable targeted and market-led investments in leading edge technology.

Stimulate a vibrant regional space SME sector by improving the supply of finance, business support, information, skills, and industry support.

However, although these objectives are concise and clear, their implementation is more patchy. The main recommendations and the associated action points were adopted by the U.K. Government/U.K. Space Agency through its Government Response to the U.K. Space Innovation and Growth Strategy 2014–2030 118 and National Space Policy. 119 In particular, the implementation is by and large delivered “through coordination across departments and in partnership with the wider U.K. Space Sector” 119 and particularly focus on regulation 120 and wider economic development. 121 Although there have been some investments in specific “nation-wide” projects, such as the establishment of spaceport capability, 31 the vast majority of the funding available is distributed through R&D grants and business development support.121–123 Although the Space IGS strategy has recently been superseded by the new Prosperity from Space Partnership 124 and the U.K. Government's Industrial Strategy: Aerospace Sector Deal, 125 I argue that the main drivers going forward remain. First, these “space innovation policies” are driven by the industry, and second, they are born out from the evidenced and projected significant economic impact for the sector and wider U.K. economy—which leads to a dispersed investment being implemented.

From Policy to Action: The Scottish Dimension

Given the very high ambitions for capitalizing on this growth in an economic sector that is primarily outside institutional control, and which has experienced exponential growth mainly on the back of one key subarea (satellite TV), policymakers and sector leaders are focusing their attention mostly into finding new niche opportunities and consequently to the early stages of business development (U.K. Space Agency, 2014). These are mainly either specialized hardware products (upstream) or integrated applications based on space data (downstream). Primarily, public agencies are investing in a series of initiatives to ensure that such knowledge “spill-overs” from (academic) research126,127 reach the market via “knowledge intermediaries,” which is currently the subject of a broad consensus in the field of science and innovation policy internationally128,129 and in the Space Sector in particular.65,66,130 These ideas have been adopted at both the U.K.-wide level as well as within the specific regional (Scottish) context, with divergent implementation.

The 2 main U.K.-wide flagship programs linking the innovation policy and the Space Sector growth agenda are the Satellite Applications Catapult and the U.K. Space Agency, both working in tandem with national R&D and innovation agency, Innovate UK. Through a combination of these organizations, several projects were funded in Scotland, in particular, the first U.K. built cube sat, UKube-1, 131 and the investment in developing Spaceport capabilities. 132 In addition, the U.K. Space Agency as well as the Satellite Applications Catapult are investing in business incubation facilities123,133 and R&D/technology transfer support. 121 Additionally, U.K. research councils are expanding their space-related technology transfer programs in this arena, too. Hence, in 2011, the STFC have opened an ESA backed Business Incubation Centre (BIC) at their Harwell (Oxfordshire) site, which is now part of the flagship U.K. Space Gateway, a cluster of space-related R&D based in Harwell. 134 More recently, ESA BIC in the United Kingdom took on the structure of a national program with several centers. 135 As such, this program is now extending to Royal Observatory Edinburgh in Scotland, with the establishment of the Higgs Centre for Innovation 136 and its combined ESA, U.K. Space Agency and STFC incubation programs.

These U.K.-wide initiatives are supplemented with regional programs, in particular, work coordinated by the 2 largest Scottish Government's devolved economic development agencies, the SE and the Highlands and Islands Enterprise. The flagship programs here include high-tech R&D grants and commercialization support through the SMART Awards program, 137 and wider coordination of sectoral development, in particular through past investment into innovation network integration through Scottish Space Network initiative 138 and by currently convening Aerospace, Defense, Marine and Security Industry Leadership Group (ADMS-ILG). This work is largely underpinned by 3 main policy documents, Scotland Can Do economic development manifesto, 139 which is effectively Scottish Government's industrial strategy, the SE-commissioned Development of the Scottish Space Industry report, 76 and the industry-driven Aerospace, Defense, Marine and Security Industrial Strategy for Scotland. 78 The ADMS-ILGs Space subgroup has also very recently evolved into a standalone Scottish Space Leadership Council. 140 Overall, I argue that these documents spell a similar mix of coordination and small-scale direct investment as the U.K. Government's ones, although with a specific focus on making Scotland distinctly advantageous for businesses working in the sector. This chimes with both the regionalization of innovation and economic policy in Europe/EU through “smart specialization”141,142 as well as Scotland's leading political party's ambition for Scottish independence. 143

Overall, I have shown how the space innovation policy interventions on one hand benefit from the U.K.-wide interest in high-tech innovation for economic growth, as well as on the other hand play out well with the devolved Scottish government agenda of promoting a stronger sense of regional identity. However, the question is emerging as to how has this overall development translated into the emergence of a distinct ecosystem in a traditionally peripheral U.K. region with respect to the Space Sector? In particular, how did this group constitute its distinct identity and what are its features? Hence, the analytical amalgamation of the actual on the ground development is required, analyzing not only the projected visions but the constitution of this ecosystem across firms and other organizations operating in the Scottish New Space Sector. The next section analyses the sectoral configuration and exposes some of the trends emerging from its structural features.

Geographic Angle: SMEs Clustering And The Present Makeup of the “Space Glen”

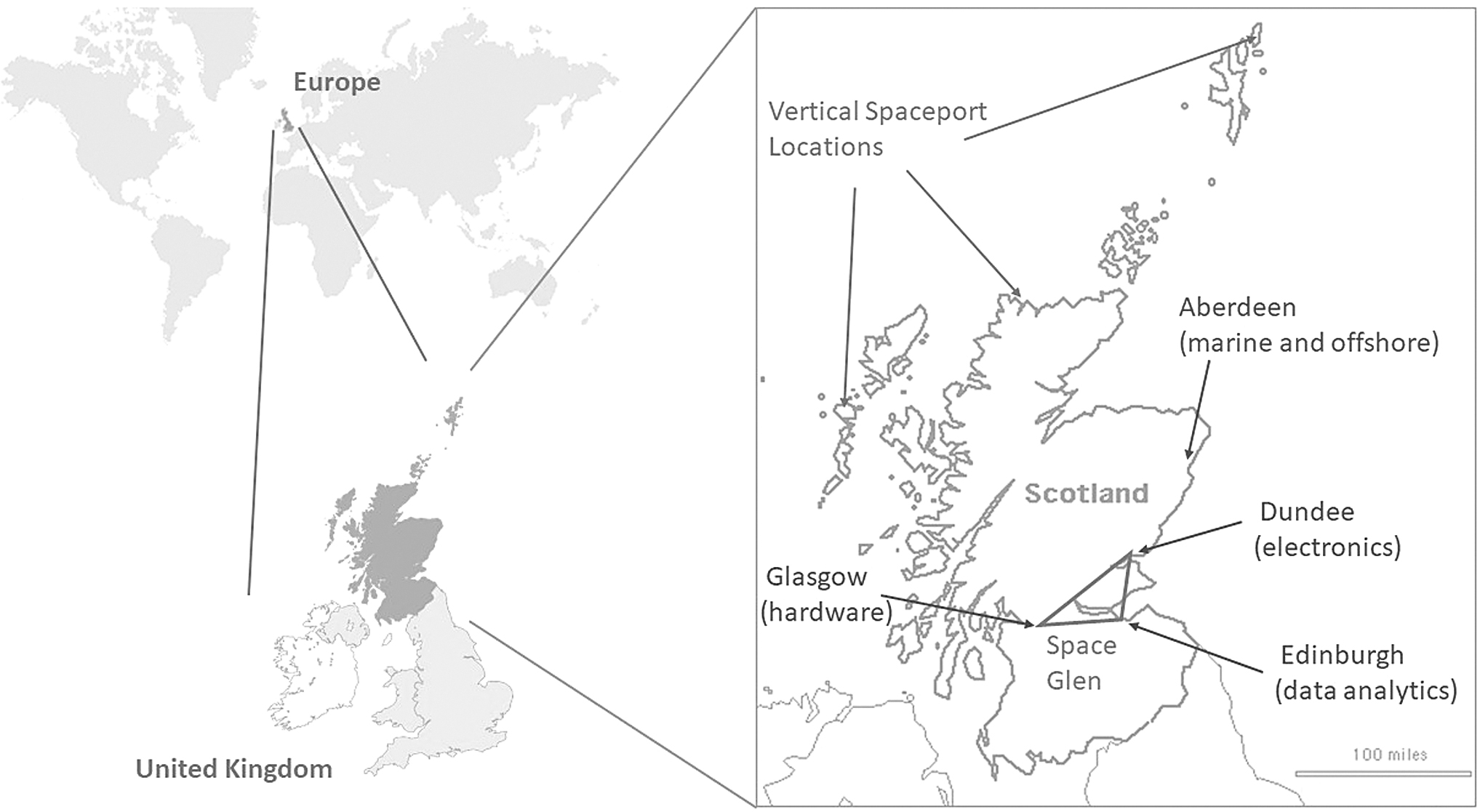

The empirical data collected with the extended participatory ethnography and document (news) analysis show that Scotland is indeed building up an active ecosystem of SMEs and partner organizations, which developed from about 2005. This ecosystem seems well placed to exploit the opportunities of the emergence of the New Space opportunities due to U.K. track record in commercializing space technology combined with a strong interdisciplinary tradition embodied by “city campuses” of Scottish Universities. However, the dispersed investment outlined above has led to niche specialization and fragmentation. This resulted in 3 somewhat distinct emerging clusters of activity in Scotland: the Communication Electronics cluster in Dundee, (nano-satellite) hardware engineering and manufacturing in Glasgow, and EO/Geoscience data analytics applications in Edinburgh, creating a “Space Glen” triangle as shown in Figure 3. (Additional significant geographic locations are the proposed sites of Scottish spaceports and the space-based marine services supporting off-shore industries in Aberdeen.)

The geographical location of Scotland's Space Glen and the distribution of its clusters in the corners of the “Space Glen” triangle.

The cluster in Edinburgh, based on software data analytics technologies, is certainly the most economically active and has the largest number of companies (∼10), ‡‡ although not the largest number of employees. The Edinburgh location is not coincidental, as it relies heavily on academic research in geoscience and informatics, both very strong areas of research at the University of Edinburgh. There is also extensive business support provision for the digital economy, with the added appeal of the availability of finance. 144 Although pan-Scottish and U.K.-wide general financial support are available regardless of the business location, 145 more risky start-up investments are often tied to tried and tested ecosystems. 146 With data unicorns such as Fanduel and Skyscanner, Edinburgh data start-up scene is far more encouraging than most other locations in the United Kingdom,147,148 with extensive ecosystem support. 149

Similar to the Edinburgh trying to lead globally on downstream space data applications, the Glasgow nano-satellites manufacturing cluster is looking to take on the global space industry by becoming one of a handful and of world-leading centers in small space hardware. Due to the nature of manufacturing R&D as well as production, these are the largest firms with most employees. In particular, Glasgow is home to a small group of companies (∼5), §§ most of who produce cube-sats and pocket-cubes and as they are highly modular and smaller in size, they can be produced more rapidly. In fact, in 2016, 60 nano-satellites were produced in Glasgow, making the city the largest satellite producer outside Silicon Valley.75,150 Interestingly, due to Glasgow's investment in support for developing digital companies and the lower cost of infrastructure (and living) in comparison to Edinburgh, some of the data firms previously associated with Edinburgh are now also being either set up or relocated to Glasgow. Closely related to the hardware manufacturing segment of the sector is also the Dundee cluster, specializing in space electronics (sub)systems. Although this is the smallest of the 3 clusters (fewer than five firms),*** it is also the oldest, as space data acquisition was part of the research and service provision here for more than 30 years. This is also the most research-driven of the groupings, with a particular unit of Dundee University and its spin-outs being responsible for most of the development.

In addition to these clusters, there are a few SME-size consultancies in and around Aberdeen, which are not really integrated into a wider ecosystem and not very visible to the rest of the sector in Scotland. They are primarily part of a subcontracting service industry, supporting shipping and oil extraction in the North Sea. As such, their primary concern and motivation is user-driven demand for technology capabilities, many of which are developed internationally and imported to United Kingdom/Scotland as end products. A notable exception to this modus operandi is a company called Veripos, providing high-precision GPS equipment for the oil and gas industry. Although they do feature in-house R&D activities, they focus almost exclusively on providing products and services to energy and maritime industries and are far more integrated into those sectors than in the Space Sector. Furthermore, their acquisition in 2014 by a global multinational group Hexagon 151 led to a different innovation model within the company, collaborating more with international units of the corporation than external partners in Scotland. A similar acquisition of an emerging space tech company also happened in the case of 2016 takeover of Optocap, a Livingston-based company, by Alter Technology, a division of TUV Nord 152 and they, too, are not very visible within the Scottish Space community.

The low level of interaction with the local innovation ecosystem can also be observed in the case of bigger multinational corporations, although they engage with aspects of policy development. Of particular note here are Leonardo (Edinburgh), BAE Systems and Lockheed Martin (West Coast), BSkyB (Central Belt), and Axon Cables (Fife). Like with Veripos and Optocap, most of these operations are “branches” of very large enterprises, with dispersed innovation and business development processes. Furthermore, as some of these firms are intensely defense oriented in their operations, their innovation processes are very closed and restrictive. As such, they are less rooted in the regional ecosystem and have a less intense interest in the emergence of the “New Space” part of the sector, as well as a more cautious approach to the global sectoral transformation, described earlier.

There are a few more companies scattered across Scotland (about 5), who do not clearly belong to any of these clusters. There are several data transition developers and re-sellers in Ayrshire (SW Scotland) and Moray (NE Scotland), although little of that development is carried out in Scotland. There are also emerging interests in linking geospatial and EO information with agriculture, with several developers and retailers of such products emerging, although again, their development projects and consortia are mainly outside the regional context. These developments are in particular very interesting since they indicate that the region is also benefiting from a global value chain development.

Finally, between 2015 and 2018 horizontal launch and spaceport developers based at Prestwick Airport, as well as other spaceport consortia have been emerging, although they are more akin to local government groups than industry players. These consortia have received a significant boost lately through recent Industrial strategy funding, as the U.K. Space Agency has now provided £31.5m for the establishment of vertical launch capability in Sutherland (NW Scotland). 153 However, it is not clear if the £2.5m dedicated to ground infrastructure will be sufficient to get the project off the ground, and contenders such as the island of Unst in Shetland archipelago as well as North Uist in the Western Isles are proposing to develop their own independent capabilities.154,155

To characterize the economic effect of these clusters as well as the overall level of economic maturity across the sector, I have also analyzed business formation and capitalization. In particular, looking at the spread of current business interests across the sector, one can clearly see that there has been a significant amount of proliferation and institutionalization, typical of sectors in conclusion of their emergence phase. 156 Looking at the development of SMEs segment of the sector, which is the object of this research and where most of this growth is happening, our research shows that the number of core firms has jumped from about 5 in 2002 to ∼10 in 2007, 15 in 2012, and 20 in 2017. Recently, we have also seen the first investors exit the start-ups, with a £26 million merger of Clyde Space, one of the sector's primes, with a Swiss partner AAC Microtec. 157 In comparison to the Veripos and Optocap acquisitions, which took place in the more traditional and mature Space Sector markets, this merger was on a more equal footing as far as relative size and history of the 2 players and might be a precursor to the formation of a new multinational corporation, independent of long-standing space industry primes.

There has also recently been a series of inward investments, for instance, the establishment of an office and manufacturing facility for a fast-growing U.S.-originating SME Spire, which worked closely with Clyde Space to carry out their first batch of R&D, before moving on to in-house R&D and production. This level of international recognition and economic maturity likely marks the endpoint of the early (development) stage of the sector. Furthermore, many firms are now at the stage to end serial R&D projects and move to productization, manufacturing standardization, and shifting focus from radical innovation to a more incremental one. In many ways, due to the structure of the global market as well as the nature of products and their customers, the key monetization of the past investment is through exports, although the latter is so far limited to government-backed programs in the United Kingdom and abroad, such as the downstream International Partnership Programme.158,159

Overall, the described dispersed and divergent nature of the “Space Glen” SMEs does little to explain Scotland's ability to project the joined-up view of a distinct emergent sector, although it underpins the critical importance of research–business partnering in innovation, as one of the main reasons for clustering. However, how has this been mobilized to create a globally recognized regionally based sector?

Community Angle: Creating a Joint Vision of a “Space Glen”

I propose that the crucial development within the sector is its consolidation based on a creation of a shared sensemaking, which is performed through establishing a joint vision for a “brand” identity, such as the “Space Glen,” 5 building on previous well-known “Silicon Glen” framing of Scottish electronics industry, 160 itself modeled on Silicon Valley. 161 Although different names are also used near synonymously, for instance, the more abstract and generic “Agile Space” discussed later, it is the parallel with the past ambitions for a global high-tech value chain powerhouse that make “Space Glen” a particularly evocative label for the emerging Scottish New Space Sector. In particular, I argue that this regional sectoral identity development is coordinated through shared spaces, especially through conferences and events—by having joint Scottish representation, announcing major ideas and/or policies and by hosting them in Scotland to showcase local capabilities as in presented in this section.

Scotland has in recent years (2000–2017) attracted some of the largest international space conferences, with focus on space science, engineering, and business. Most notably, in 2008, Glasgow hosted the International Astronautical Congress, the largest and most prestigious conference in the sector. It occurs annually and is often marked by landmark national and regional developments, for instance, the establishment of U.K. Space Agency was announced as well as U.K. joining ESA manned space exploration programs (completed in 2010). Similarly, Edinburgh hosted the European Space Agency's Living Planet Symposium in 2013, focused on the development of Planetary Science and Earth Observation. Attracting about 1700 delegates from around the world it “[brought] together scientists and users from across the globe to present their latest findings on Earth's environment and climate derived from satellite data.” 162 These conferences gave a substantial boost to the relevant scientific communities and brought attention to the local Scottish dimensions of the global Space Sector. In the years since these major events were hosted in Scotland, the SE in partnership with other key agencies, U.K. Space Agency in particular, also secured joint Scottish representation at their subsequent international locations.

Scotland also recently hosted a series of specialist conferences about the use of optical systems in Astronomy and Satellite/Space Data Applications, organized by the International Society for Optics and Photonics (SPIE). There were SPIE Astronomical Telescopes+Instrumentation as well as SPIE Security+Defence and Remote Sensing (the latter 2 are always taking place at the same location at the same time), all hosted in Edinburgh in 2016. These conferences are quite focused and it is important to note the significance of the topics coalescing around themes of astronomy and space science and engineering, predominantly focused on optics. Scotland being a recent host and local organizing committees including leading scientists and engineers from the region helped establish it in a position of global leadership within the scientific and engineering community. In the latter category, more targeted and less international events provide development opportunities and much more accurately demonstrate the innovation potential within the region and showcase its activities. For instance, the hosting of the 2013 U.K. Space Conference in Glasgow marked the beginning of the end of the first, constitutive phase of the sector's emergence. At the subsequent 2015 and 2017 conferences, the Scottish New Space Sector was jointly showcased under the SE coordination and sponsorship. Furthermore, Glasgow was host to a series of other leading events, such as the British Interplanetary Society's Reinventing Space conference in October 2017. Although smaller in size than the U.K. Space Conference, it has a specific focus on New Space development both in the upstream as well as in the downstream part of the sector, including site tour of a leading Glasgow-based New Space upstream firm, Spire. It also featured the re-launch of the British Interplanetary Society's Scotland regional branch. 163

The Scottish Space sector is also establishing its own events, primarily through the leadership of Scottish Centre of Excellence in Satellite Applications (SoXA), who run a very successful series of Scottish Space Symposia, in partnership with several other actors in the sector.

164

2017 saw the inauguration of Data.SPACE conference hosted annually in Glasgow, which aims at establishing Scotland as a leading player in Space Data applications globally. Such capability is underpinned by a critical mass of past activity as well as an ecosystem of players interested in developing a common vision for the sector in the region. For instance, at the inaugural Data.SPACE conference in 2017, 2 leading Scottish New Space Sector SMEs, announced the creation of a conceptual integration of the Scottish New Space value chain, in a grouping called “Agile Space.” The vision behind this proposal, put forward by the lead upstream satellite manufacturers Clyde Space and largest downstream data analytics company Ecometrica, was to exploit the fragmented nature of the sector and from an “informal grouping open to companies and research organizations operating in Scotland” to collaborate on “specific market opportunities,” “develop funding and support models,” and to “ensure seamless operation and communication of key messages.”

165

In particular, it seems that the key message of the Agile Space Group was that:

Scotland's space industries and research institutions could benefit by promoting Scotland as Home of Agile Space. By emphasising this strength we can attract inward investment and talent, and promote the creation of a vibrant technology and service ecosystem leading to high value technology and service exports.

165

These events and the initiatives developed through them also get sporadically picked up in the media, although primarily for either a U.K. audience (such as the BBC and the U.K. and Scottish broadsheets) or within very specialized outfits (such as business magazines). Although these reports clearly reinforce the narrative of a collective Scottish New Space brand, whether it being “Space Glen,” “Agile Space,” or specifically the city of Glasgow's satellite manufacturing records, they by and large repeat the messages produced by leaflets and press releases at these events and do not in themselves constitute new perspectives or analysis. Hence, to further advance the understanding of the consolidation of the Scottish New Space economy, the practitioners' views of the political drivers and on the ground configuration is needed. In the next section, these are analyzed using primary data from interviewing a select small group of informants from across the sector.

Critique: Stakeholder's Perspectives and the Future of “Space Glen”

The dominance of the 2 main conflicting perspectives outlined above, that is, the unified innovation policy targets and interventions and the dispersed, fragmented nature of the sector, meant that the main thrust of my interest in understanding the stakeholders perspective of the “Space Glen” development was in comparing and contrasting these 2 conflicting framings.

The Politics of Numbers and Targets

To begin with, the interviewees' observations confirmed this “common wisdom” about the industry being fragmented, commercialized and, at least in terms of the turnover dominated by satellite TV provider(s). Explicitly, a business development manager at one of the universities commented:

The problem with the Space sector is that a lot of it is smoke and mirrors. […] When you talk about a £10bn-a-year Space sector, £5bn of that is Sky [satellite TV provider]. […] (Interview B)

This consequently raises a concern about the implications for the current policy setting ambitious growth targets. The same interviewee immediately commented “where are you going to find another 2 or 3 ‘Sky-s’?” Similarly, another interviewee, also a business development manager, but based at a national research laboratory, remarked that the current updated data showing the targets at the moment are being met is potentially misleading as

they are not looking at linear growth up to 2030, the growth rockets at some point, and you go: “Oh, ah well!” [shrugs and rolls his eyes] (Interview C)

This latter comment clearly shows that the interviewee is unconvinced that the methods employed to project future growth are realistic; rather that there is some potential of “massaging the numbers” being deployed. However, this is not to say they consider targets as unimportant: all interviewees argued that there is strong evidence on the ground, specifically mentioning conferences as the venues where that can be noticed, that the policy framework and a sense of optimism regarding the growth trajectory are electrifying the sector, both within the academia, as well as with the entrepreneurs. On this topic, the same interviewee specifically commented:

It is not whether you hit the target that counts; what counts is how much of an impact you make, how much growth you actually get and if you turn that into viable industries. If it turns out that we end up with 9.5% or 9% of the World market in Space by 2030, that is still bloody good! […] The target is just something to aim for. (Interview C)

Interestingly, they also believe that the targets, or something close to that outcome, is achievable, in particular in the case of Scotland, as the conditions here are more favorable in their view:

I think it will [work] […] because [emphasised by the interviewee] of these differences [with the rest of UK]. Scotland, as far as I understand, has a larger relative manufacturing sector than the UK as a whole, and also there is still a lot of memory of a proud engineering heritage in Scotland […]. There are also […] industries that currently exist in Scotland like the Oil and Gas, for example, who are potentially very good markets for downstream [Space] applications […] (Interview C)

Although they recognize the Scottish New Space Sector's dispersed and divergent configuration, they by and large believe that such dispersed clustering is an advantage, as the SMEs are embedded less in a “Space Sector” grouping context and more in research/industrial groupings with existing commercial applications, which have shorter paths to market. The scoping here clearly pointed at a specific structural feature, which merits further investigation. How do such views marry with the overarching loose value chain integration, as we have seen in the case of the emergent “Agile Space” group? And how is such integration actually playing out in support of innovation within SMEs? Answering these questions will illuminate the structural configuration of innovation systems and processes within an emergent sector.

In contrast with the positive view of the targets, most interviewees were very critical of the overall U.K. policy with respect to not providing systemic growth-oriented funding schemes. The key problem they foresee for future growth is access to finance for firms just outgrowing the SME size—they commented on the lack of venture capital investment for “scaling-up” and noted that:

[…] the UK wants to grow SMEs and then sell; USA wants to build multinationals! (Interview C)

This was also mentioned by the interviewees in relation to establishing new firms requiring significant capital investment to begin with, in particular, for example, related to launch capabilities. This has been somewhat rectified very recently with the investment in spaceports in Scotland, 132 although the location and small size of the infrastructural investment have been criticized. 166 Overall, the dispersed small-scale investment through R&D and commercialization grants, which is recognized as key U.K./Scottish policy intervention in the sector was described in several comments having relied upon the “low hanging fruit,” which has now been collected and from now on it will get harder to grow and develop the sector to meet the targets.

Bringing It All Together?

What are the informants' views on how to reconcile the unifying policy ambition and the dispersed state of the ecosystem? Informants suggested business strategies in the Space Sector are similar to those used in other areas of high-tech industries, with the primary focus being on securing financial resources and business expertise. As expressed by one of the early-stage business development managers, coordinating U.K.-wide programs, this is based on their belief that the

… premise of technology transfer from Space is not about necessarily having a Space Industry to base it on, [rather it] is having entrepreneurs looking for technology, and Space has always been a driver for innovation. (Interview A)

This is an important lead for future research to build a deeper understanding of the “Space Glen's” evolution as well as in the sector moving toward the next stage(s) through a new set of policy interventions. For instance, very recently dedicated space-specific incubation and business development/support programs have emerged, such as the STFCs Higgs Centre for Innovation 136 and SoXAs Space Incubator at Tontine, 167 although there are already many other (non-Space focused) technology incubators in Scotland, in particular in Edinburgh. With respect to implementing the innovation policy on the ground, one interviewee touched upon the importance of educating the SMEs in business development while still in the early stages, and another mention the need to provide a (more) tailored support depending on each of their circumstances.

However, interviewees broadly agree that the sector's long-term challenges are related to access to further capital investment, appropriate recruitment, and the establishment of business networks leading to markets. In many ways, all 3 of the above depend on the primary network the company has in terms of finding support for its creation and development, which bring about the need to understand these networks and how they influence the process of innovation. This is a key point to understand how the innovation ecosystem works and indeed how to support it going forward, as one of the business development executives within an SME specifically commented:

Key for success [in the early-stage enterprise] is having some key contacts, who can help you open the doors to the industry […] (Interview D)

In line with the strong feeling about the importance of the networking, they also commented that it is often felt that the Space Sector is a bit of “an old boys club” of (large, international) established firms, hence connections are crucial to break into the market or open up a niche, although to do so SMEs need “to gain credibility in the market.” Here, the establishment of new branding, be it “Space Glen” or the “Agile Space” may be helpful, as well as direct certification or approval by association from established “traditional” Space Sector players, in particular, the ESA and NASA, although the latter requires firms to have the United States presence (subsidiary), before directly engaging with them. †††

Overall, the qualitative data support my earlier analysis that the space innovation policy pursued in the United Kingdom and Scotland is being accepted by the stakeholders as an opportunity for further sectoral development, although they are critical of the targets themselves and methods employed to achieve them. In particular, the current policy delivery method of small-scale dispersed R&D investment is seen as insufficient for growing the SMEs into larger corporations and innovation in more difficult and complex technology areas requiring significant upfront capital. This is seen as a critical way forward, in combination with the development of a united sectoral identity through networking, although keeping the SMEs in current clusters close to target non-Space applications markets, to ensure easy access to those. These ideas spell a new approach for innovation, which seems to derive from a looser ecosystemic view of value chain integration, as advocated in the “Agile Space” approach. However, the questions emerge how this leads to new product development and growth of economic activity, and what the role is for innovation policy interventions, most often through intermediaries.

Conclusions and Further Research

This article outlined the Scottish perspective on the global trends of the emergence of the New Space Sector and in particular, its integration in industry-led innovation policy and the economic trends on which developmental targets are made. In particular, it traced the main reasons behind the hands-off free-market approach to the Space Sector, which has a long-standing history in the United Kingdom. It combines small-scale dispersed governmental R&D investment with support for sector building through business development delivered through a series of innovation intermediaries. I have argued/shown how this is reinforced in Scotland with an additional regional impetus by the Scottish Government to diversify the Scottish economy and build a distinctive Scottish industrial base.

Furthermore, by analyzing the structural configuration of the New Space Sector in Scotland, I identified 3 distinct research-linked clusters. To integrate them in a joint vision of a Scottish “Space Glen” I propose that the idea of a unified Scottish Space Sector was put forward through a series of international and national conferences and events. At those events, Scottish SMEs were jointly represented and new ideas about their collaboration and loose value chain integration were presented. In particular, a critical moment was the “Agile Space” framing proposed at Data.SPACE 2017 by the leading upstream and downstream players. However, when contrasting these policy and structural observations with views from practitioners, several (upcoming) challenges were addressed, although there was overall agreement on the significance of the opportunities presented in the sector as well as approval for policy ambition as a vehicle to energize the stakeholders. The distinct clustering of SMEs within the sector was noted as a strength since their embeddedness in other local sectoral ecosystems shortens the path to market for applications derived from the space sector, which is an asset for a nascent value chain.

However, the analysis presented here is incomplete and new questions are emerging regarding the relationship between the political and economic developments and the actual processes of innovation. Being a scoping study, it only covers the preliminary insights and is limited to secondary data and broad ethnographic observation, with a small number of semi-structured interviews. In terms of new research questions, 2 are standing out in particular—what is the fundamental link between these new narratives and modes of innovation, that is, the “Agile Space,” and development of new products and services in the emergent Scottish Space Sector? And how is innovation actually realized through the “Space Glen's” Agile Space framing? To understand the “Space Glen's” emerging New Space economy, and how developments in Scotland can be understood in the global context, these questions need a more detailed answering.

Footnotes

Acknowledgments

This article greatly benefited from constructive feedback and suggestions from many colleagues. Specific thanks go to my mentors, Niki Vermeulen, Alessandro Rosiello, and Robin Williams, all from the University of Edinburgh, Julian Dines from the U.K. Astronomy Technology Centre (STFC); and many others with whom I discussed this work. I am also very grateful to all participants in the study who have assisted me with my enquiries, the amazing New Space editorial team, especially Ken Davidian, as well as the 2 patient and thorough anonymous reviewers.

Author Disclosure Statement

No competing financial interests exist.

Funding Information

This research was funded through a (1 + 3) Pathway Studentship, bestowed by the Scottish Graduate School of Social Science (SGSSS) on behalf of the Economic and Social Research Council (ESRC) (grant no. ES/J500136/1) and was conducted in collaboration with the Innovations Team at the U.K. Astronomy Technology Centre (ATC), part of Science and Technology Facilities Council (STFC).