Abstract

A study conducted by Bryce Space and Technology on the quantification and cause-mapping of launch delays of small satellites revealed that all 1,078 small satellites launched commercially in the past five years had suffered launch delays. The study attributed the primary reasons for this delay to schedule slippages of launches and the primary satellite. Such delays are a huge financial drain for the small satellite manufacturers. As a critical step toward addressing such problems by streamlining the supply chain and imparting the elements of interoperability and cross-compatibility, there are renewed calls for extending the scope of standardization of satellites—sizes, interface, and other aspects—from the currently existing CubeSat standards (CDS) to cover larger small satellites up to 500 kg. There are several initiatives such as Launch U by Aerospace Corporation, for example, aiming at addressing this area. In this context, the article tries to assess standardization through several strategic frameworks such as the Transaction asset model, Kraljic matrix, and Project planning model to identify the positive effects of standardization and also the negatives to impress on the need to define a proper extent until which standardization can be allowed to happen.

Introduction

The global space industry is on the verge of a paradigm shift in value creation in the coming decade. With the emergence of newer application areas such as non-geostationary communications, high-frequency change detection, and other commercial business opportunities, a more significant share of the market would be taken over by the private industries from the traditional model of government owning the assets and controlling the operations. Although satellites of yore were always bulky and stand-alone, the un-tapping of commercial opportunities in recent times and the consequential emergence and resounding success of newer firms such as Planet labs have brought forth the idea that satellites at the lower end of the mass spectrum could be excellent value propositions in the total business canvas. As complementary computing powers evolved, the focus on higher temporal resolution received increased prominence in various space application areas, leading to satellites becoming lighter and smaller and the emergence of CubeSat standards. However, for smaller satellites beyond the range of CubeSats, standardization has still not reached its prominence, creating significant launch hurdles and also increased financial troubles for the owners.

A study conducted by Bryce space and technology on the quantification and cause-mapping of launch delays of small satellites revealed that all 1,078 small satellites (weighing <600 kg) launched commercially in the past five years had suffered launch delays. 1 The study reports that although the median delay is about 128 days, the main reason for the same is the readiness of the primary satellite (40%). It may be noted that small satellites are generally launched on a ride-sharing basis wherein they fly as secondary payloads on a mission for a bulkier primary satellite. Such a model makes it less costly for the small satellite owners, who are typically start-ups and universities whose primary motivations are reduced launch costs. However, because such contracts are tilted more toward the financially heavy primary satellites, the primary satellite delivery delays affect the overall launch schedules. The study also revealed that 34% of the delays in the launches of small satellites are related to launch vehicle (LV)—earlier LV anomaly, LV development and manufacturing—which is again a technically, infrastructurally, and financially involved activity.

Such delays create substantial financial strains on the small satellite makers and significantly hamper their monetary and resource utilization plans. Besides, the current Covid crisis may affect the investor interests in the sector, primarily because of the more prolonged pre-revenue phase and increased capital investments in space compared with other easy-milk industries.

Grant Bonin, Vice President, Business Development in Spaceflight, Inc., which commissioned the study by Bryce, argues that the scenario throws more light on the importance of having more standardized approaches toward accommodating small satellites (such approaches already exist for CubeSats) to be able to switch among launchers at will in case of schedule slippages. He says, “locking in the electrical interfaces, standardizing the mechanical interfaces, and standardizing how a spacecraft needs to be processed is really key.” 2

Not just Bonin, the big question of standardization in space is getting more vocal, perhaps now more than ever before, courtesy of the testing times the world is passing through. Driving standardization further down the lines from the current industry state to include aspects such as the sizing of the satellites, launcher—satellite interface and the satellite pre-processing before assembling to the launcher could potentially lead to significant cost savings, a better market balance, and overall better prospects for commercial space, notwithstanding some associated pitfalls. Although we currently have standards such as the CubeSat Design Specification (CDS) developed by California Polytechnic and endorsed by NASA globally, the question of standardization remains elusive for bigger sizes that cannot be quantified as a primary satellite, but not as nanosatellites either.

This article is a theoretical assessment of the advantages and disadvantages of standardization in the satellite sector. There are two critical assumptions around which the study is carried out.

Value from the space sector in the coming times is expected to be hinged on customer centricity and not on the technical prowess of building and positioning space assets. Identifying and solving business problems on earth would be the drivers, and satellites are among the enablers in the end-to-end chain, including other assets such as software capabilities, analytics, ground systems, strategic partnerships, etc. Owning/leasing/controlling a space asset depends entirely on the respective business model.

There is a clear demarcation between commercial space and strategic space, and that governments adopt a more global and less protective outlook for the commercial space so that a conducive business environment is enabled.

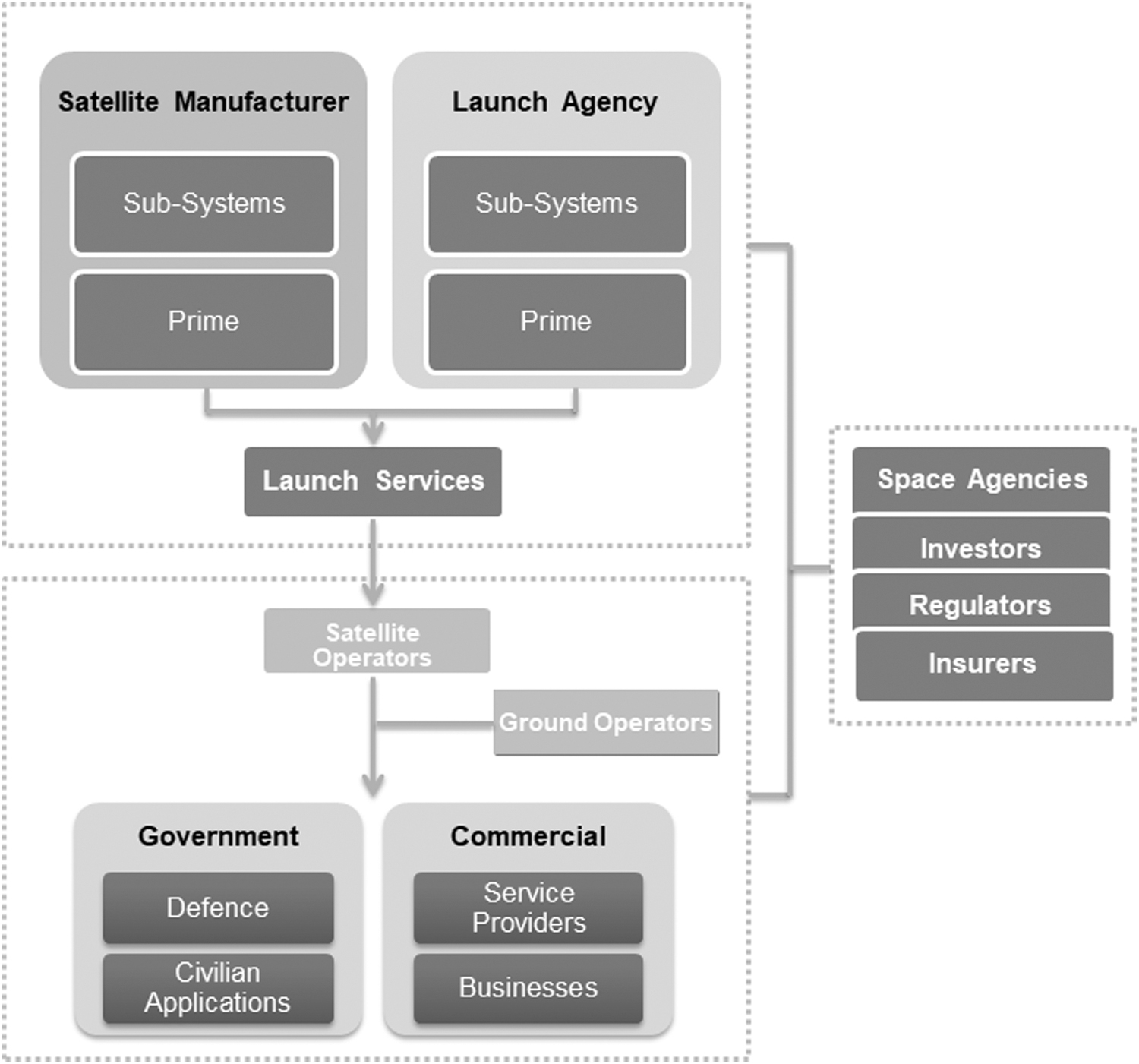

The focus of the study is on the upstream of the value chain that is, steps until the satellite is positioned in orbit. From Figure 1 that depicts the overall space value chain, the boxes representing satellite manufacturers and launch services are only covered in the scope of this study.

A schematic of the space value chain | Courtesy: Euroconsult, Satellite value chain: Snapshot 2017.

Small Satellite Market

Euroconsult 3 predicts that about 8,600 small satellites will be launched in the decade 2019–2028. This is a 22% increase over their estimation of 2018 and augments the hypothesis that the market is only looking bullish. The current uncertainties associated with Covid may be considered a short-term phenomenon—a couple of years out of the decade. It is only safe to assume that subsequent governmental interferences, increased market dynamism, rise in telecom applications through constellations, and new and innovative applications derived for small satellites are set to increase the overall numbers in the coming years.

It may also be noted from Figure 2 that about 95% of the small satellites (<500 kg) by mass predicted to be launched in the 2019–2028 decade are >50 kg. Even by numbers, about 60% of the satellites to be launched in the next decade are expected to be 50 kg and above. Although it may be noted that the portion of this heavier mass of satellites are predominantly due to the Mega constellations such as OneWeb, Starlink, and Kuiper that are already falling under the realm of standardization among themselves (proprietary de-facto standards that are mutually exclusive), the co-operative scheme of a consensus-driven global standard and cross-fitting are missing in terms of interfacing with the launcher, sub-systems, electrical connections, separation systems, and manufacturability of the suppliers. The constellations are also exorbitantly expensive, and only those firms with deep pockets can afford to get those through to completion. Starlink constellation, for instance, is expected to cost a whopping $4.2 billion and Kuiper over $4.6 billion. However, Space X, which is vertically integrated, can take away all benefits of launch costs, whereas OneWeb having had to rely on several launchers—Soyuz, Virgin Orbit, and Ariane—is expected to face significant programmatic difficulties, which finally translate to considerable launch costs. CEO OneWeb, Adrian Steckel, has publicly acknowledged this cost advantage for Space X and highlighted the importance of launch costs being a major determinant in the total costs of getting its satellite in orbit. 4 On extrapolating, it can be concluded that with the emergence of newer business models and the consequent increase in demand for satellites, the upstream cost pressures will drive the industry toward better consolidation and operational streamlining. Such a situation makes it beneficial for the industry to drive the evolution of consensus-driven global interfacing standards that can be key co-operation enablers—both technical and business.

Small satellites to be launched 2019–2028 | Courtesy: Euroconsult, Prospects for small satellite market, 2019.

Standardization—Current Status

During the early times, space crafts were unique and exclusive to the builder and were usually launched on a one per mission mode. The primary uses of these satellites were communication and earth observation, with the control rights predominantly resting with the government. Later with the emergence of innovative business models, the value spectrum derived from space applications tilted, and commercial players galloped into the sector. In 1999, Calpoly introduced a specification, which later became the globally accepted CDS for CubeSats. As technical modifications in the likes of electronic miniaturization and use of Commercial-Off-the-Shelf components proved their durability, the commercial potential of CubeSats also improved over time.

The evolution of standards in the CubeSat sector facilitates cross-compatibility and interoperability among the launchers. Standard form factors in multiples of U led to the development of a whole suite of associated sub-systems such as satellite dispensers, standard buses, electrical interfacing, etc. They became a vital growth factor for the CubeSat market, enabling rapid development, better technology, and low costs.

However, with the widening of scope for business models, the average weights of the satellites are also increasing, and more and more number of smaller satellites that are beyond the classification of CubeSats are evolving. In the same study, Euroconsult 3 predicts that there is going to be a 21% increase in the single satellite average mass that is going to get launched in the next decade (<500 kg class). This is a clear indication of the rise in average satellite mass and, consequentially, the need to think beyond the aspects of only mission diversity. The introduction of standardized sizes becomes a natural follower. Replicating the CubeSat model for heavier satellites is a difficult proposition primarily because of the reasons listed next.

Mission diversity is high, making the sizes and the associated packaging on the satellite different.

The electrical interfacing varies from that of a CubeSat, which traditionally can be managed with standard 9 PIN connector sets or otherwise. For heavier satellites, other sub-systems such as Propulsion, features for trickle charging of the battery on the launch pad, extensive health monitoring, etc., need to be accommodated.

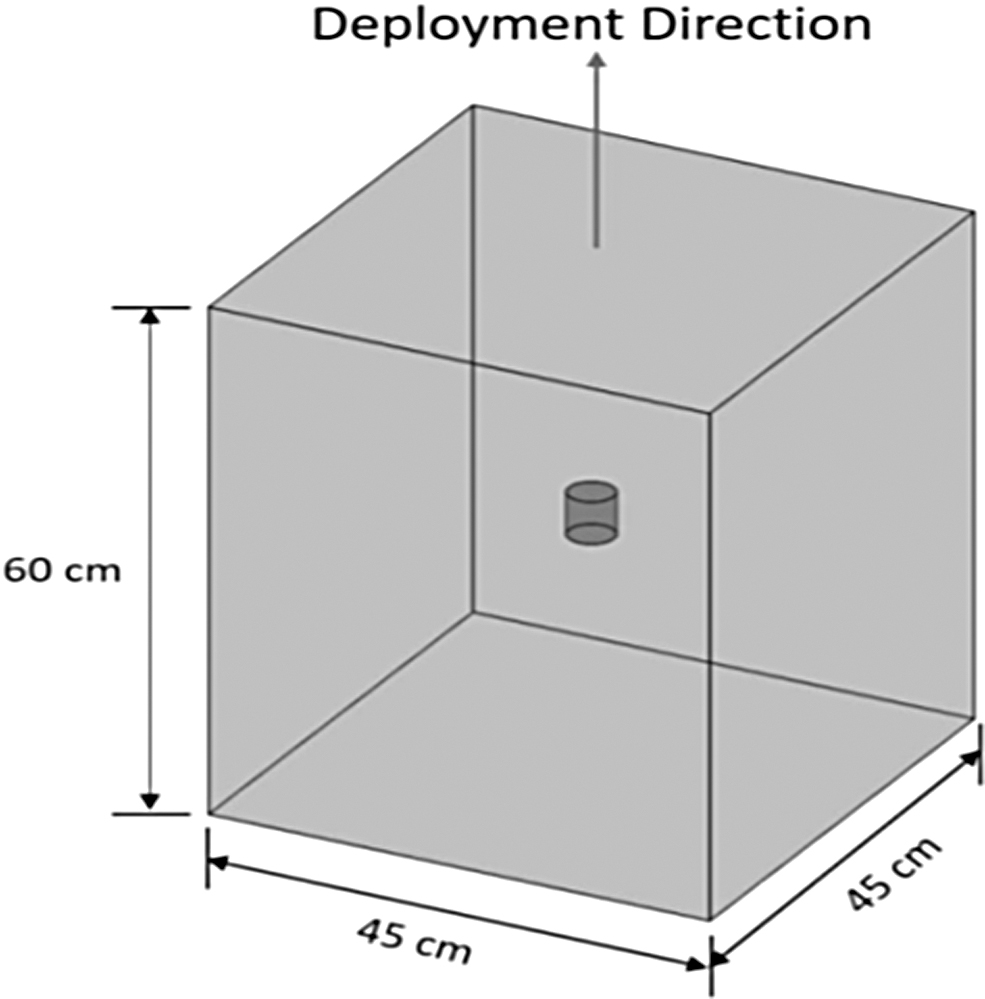

However, there are theoretical initiatives such as the launch unit (Launch U, as shown in Figure 3) by the Aerospace Corporation for satellites between the size of 12U and an evolved expendable launch vehicle secondary payload adaptor. After careful studies of loads, vibrations, and various payload sizes, the Aerospace Corporation recommends a size of 45 × 45 × 60 cm, with a range of mass between 60 and 80 kg. 5 The primary aim behind such an approach is to increase the launch availability and flexibility so that the satellites can swap the launchers if there is a delay in the schedule. Such an initiative would also result in reduced launch costs. This general cost effect can ripple backward through the value chain, resulting in reduced manufacturing costs. Another initiative worth mentioning is the The Consortium for Execution of Rendezvous and Servicing Operations (CONFERS), an industry-led program backed by The Defence Advanced Research Program Agency to evolve consensus-driven technical and operations standards for on-orbit servicing and rendezvous and proximity operations.

Launch U volume | Courtesy: Aerospace Corporation.

The subsequent analysis of standardization is broadly split into two classes—(1) forward chain, which covers the launch, and (2) backward chain, which covers the design and manufacturing of the satellites and associated sub-systems such as adaptors, interfaces, and testing procedures.

Why Do We Need Standardization?

Forward Chain—Establishing Sustained Relationships with Launch Providers

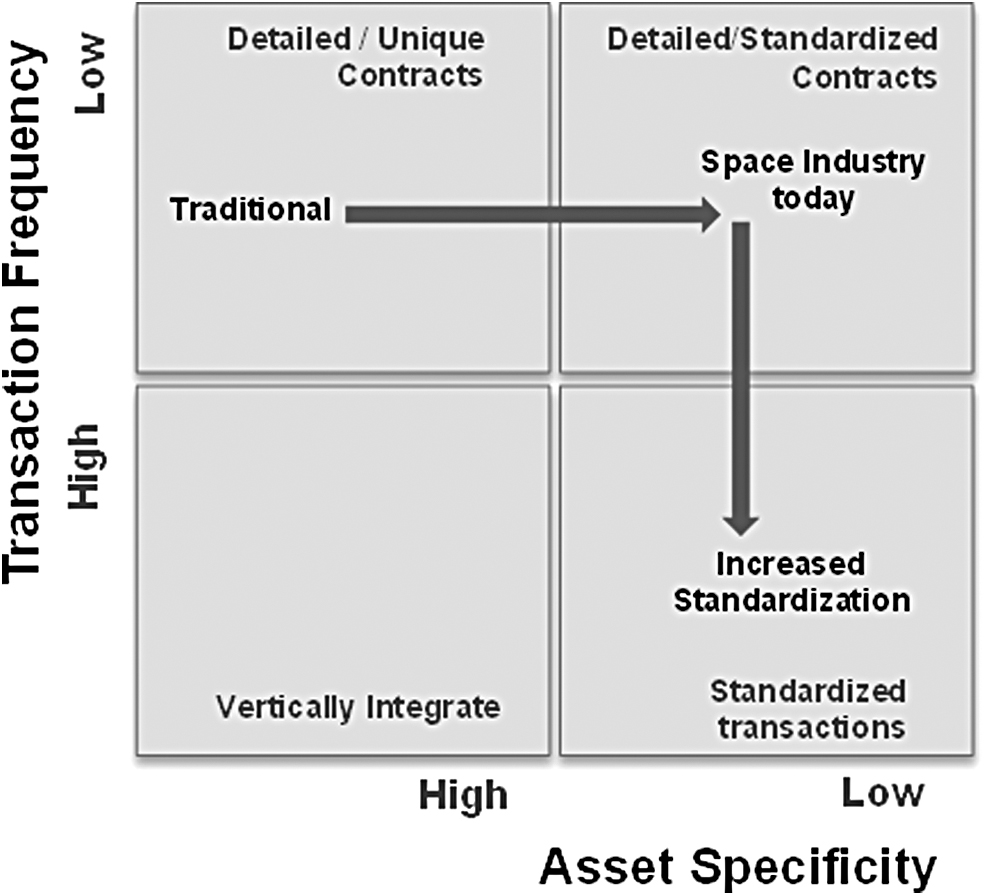

Analyzing the scenario primarily based on Mckinsey's Transaction Asset framework 6 and focusing on the forward part of the value chain, that is, the interaction with the launch service providers, there are some interesting theoretical revelations.

Traditional satellite—launcher transactions have more or less remained in the top left quadrant (Figure 4) until recent times when it started shifting to the top right (led by CubeSats and constellations). The shift in business models from a traditional asset-in-space specificity to customer centricity drove this positioning to the zone of Detailed/Standardized contracts. In other words, the higher focus on independently owning the satellite as an asset and unavoidably suffering exorbitant launch costs piqued over to better value-add models such as shared ownership/M & A's (such as Maxar—Digital Globe—Space Systems Loral, Planet—Terrabella, etc.), data platforms aiding aggregation, and better delivery of customer desirable business insights that create better prospects for the firms—both upstream and downstream. And the outcomes were—(1) rise in standardization (2) attention to interface management that consequently opened up paramount importance for aggregators in the full value chain, and (3) an observable shift in the industry from a traditional zero-sum game tilted in favor of the seller (Launch owner) to a balanced field with the buyer also acquiring better bargaining powers. This is of course good, though limited to CubeSats/smaller sized satellites. A typical 3U cubesat is shown in Figure 5, so as to give the reader a better appreciation on the size and consequently, the procedural easiness in supporting the outcomes described above. When bigger sized satellites are treading the path of standardization, transactional efficiencies will increase accordingly.

Transaction—asset matrix | Courtesy: McKinsey and Company.

A typical 3U CubeSat | Courtesy: Morpheus Space.

Standardized transactions can probably be claimed the closest to being a fair scenario—a net zero balance of power system. This situation can drive the launch market toward a tending-to-perfect-competition market where the launch providers would also have to vie for shares aggressively. The indications of industry shifting toward this are already out there, even with the current level of standardization.

SpaceX has announced highly competitive launch prices heralding a price war, and to no surprise, the response from competing companies in the small satellite market such as Rocket labs, for example, has been in the lines of further segmenting the market than reducing the prices to the same levels.

Small launch vehicle development is at a never-seen-before pace, and there is increased investor interest in this segment. More than a hundred companies globally exist for small satellite launcher development. Though the possible conversion ratio in this ecosystem is debatable, the trend is a testimony to the direction that the market wants the industry to take.

Aggregators, supplemented with exclusive export rights/preferred partner agreements and separation systems/dispensers, are becoming a more prominent force in the launch market.

There is an emerging trend toward territorial consolidation, driven mainly by the aggregators in the small satellite segment. So, there are a couple of big names (such as Spaceflight, ISL, Exolaunch) who hold business volumes from their surrounding geographies and can leverage this to define their terms and enter into long-term launch agreements with a slew of other factors such as time to launch, early book the capacity, etc. to further enhance their revenues in the backend deals with their customers (satellite makers). Some of the recent launch agreements 7 look to be silent manifestations of this shift.

However, although the share of standardization with respect to the total market value is minuscule at present, the trend observed is noteworthy and can serve as a strong driver for further decision making in this direction. The current stage of standardized contract transactions is not free of the usual negotiations and haggling. When the industry further matures to the stage of standardized transactions, an open-market scenario primarily driven by a rational demand–supply economics rather than a balance of power system that is unpredictable and unstable would result. Considering that the current launch costs for medium/bigger-sized satellites are significantly high, a market dynamic projected here would bring tremendous relief to a commercial entity.

Backward Chain—Design and Manufacturing

Standard platforms and associated ancillaries will tremendously aid in cost reduction and help firms exert better control on the time-to-market lever. Besides, standardization leads to laid-out operations procedures and drives process orientation among the manufacturers that will ultimately translate to a reduction in marginal cost to realize each additional product. Another possible outcome is the evolution of a modular approach for sub-system delivery that will enable the owner to adopt a plug and play mechanism for product building best suiting his business requirements and development schedules. Irrespective of the mission parameters or purpose, all components (mechanical systems, fueling, Telemetry, Tracking and Command Network, etc.) except the strategic/critical ones—such as mineral mappers, high-res spectral cameras, particle counters, etc.—will be available off-the-shelf.

Standardization will also help commoditize the associated complementary products and drive the costs of sub-systems further down. Clubbing these aspects into an Expenditure—Supply matrix (A variant of the basic Kraljic Matrix)8,9 as shown in Figure 6, it can be seen that those components that are at lesser supply risk may be moved into the Routine-Products space. Satellite makers can obtain such components at lower prices by forming suitable long-term alliances with the production houses and exert better controls over the specifications. On their side, the production houses can put economies of scale to play, reducing the input unit costs.

Expenditure—supply matrix | Courtesy: Kirsten Ejlskov Jensen, PublicProcurementDK, March 28, 2012.

The classification of the subsystems/components as explained in Figure 6 will also reduce single-party dependency, helping firms reduce the input costs further by holding the threat of substitution as an aggressive mechanism against the suppliers. Interchangeability is a crucial aspect of standardization not only in the backward chain but also in the forward chain, in terms of switching between the launchers.

To conclude, in the upstream space, a business owner can derive benefits in three sectors:

Reduced set up costs—With increasing commoditization, the market asymmetry existing because of increased dependence on a particular supplier can be reduced. The power of interchangeability may be leveraged suitably by the firms. To counter this force, the suppliers would provide more value-adds, including turn-key delivery, to better their position. This would, in turn, reduce fixed costs that include elaborate testing and inspection setups for the business owners. Reduced transaction costs and risks—Commoditization and increased relations with the suppliers will also lead to a reduction in the transaction costs—administrative, legal and the costs for information collection, processing, etc. The associated risks in the likes of price volatilities, supply disruptions, need for backward integration to protect a firm's specific assets, etc., derived primarily because of the unbalanced power system would reduce. Improved relationships—As studied by the Nobel laureate social scientist Oliver. E. Williamson, transactions are also greatly influenced by the human factors of bounded rationality, uncertainty, and opportunism. With increased standardization, the co-ordination environment between the buyer and the seller stabilizes, reducing the uncertainty. As transactions increase and asset specificity falls, the boundaries of the transaction equations diminish, and human rationalities would more or less cater to the resulting reduced complexities. Market opportunism can also be expected to fall because of the same reason, that is, reduced specificity. It may be noted here that, for the launcher interactions, there would be improved chances for opportunistic re-contracting for the firms by shifting across the launch vehicles.

It can be seen through these theoretical postulations that standardization can bring the players of the game onto an egalitarian palette through the evolution of less complex systems and a more equitable sharing of the associated economic surplus. The emergence of open market places—Space Impulse, hostmi, Orbital Transports, satsearch, to name a few—to connect the suppliers and the customers through a common platform with transparent prices, configurability, feature bundling, etc. will be attributed to being both harbingers and off-springs of this tectonic shift toward deeper standardization.

Need to Define the Boundary

Standardization as an Innovation Killer

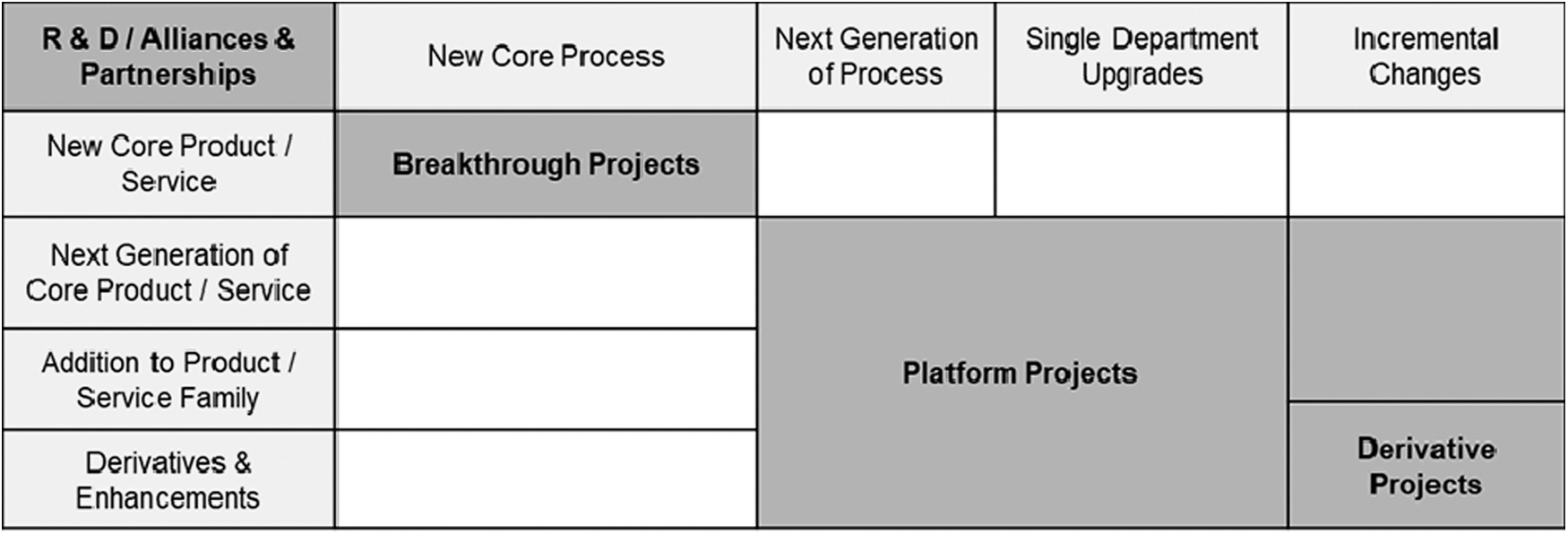

The main downside of this change of tide in the space market is that it might be a potent innovation killer. Price becomes the anchor to work on. Such a situation directs the focus on operational efficiencies but may become myopic on the bigger canvas of innovation. Focusing on bettering the operations triggers new derivative products but leaves less space for something ground-breaking such as radical or architectural innovations. In their classic study on project planning, Wheelwright and Clarke 10 classified the development and commercial projects in a firm into five types, as shown in Figure 7: Derivative, Platform, Breakthrough, R & D, and Alliances & Partnerships. It can be seen that, with more stress on process improvements, there is a strong chance that firms might get caught in the derivative space, with some overlap in the platform space, which is good, though not enough. The reasons for this can be summarized primarily as,

Aggregate project plan | Courtesy Wheelwright and Clarke, HBR.

Companies just have to make their products marginally better than the competition in the shorter time horizons under which they operate.

Improved pressure for giving better return on investment (ROIs) to be able to satisfy the various stakeholders.

Lack of significant funds for R&D. R&D, being outside the commercial projects, requires substantial management interference for ensuring a suitable allocation and adequate latitude to the workforce. Given the increased push for standardization and early-to-orbit business models, this might not be possible.

A sector such as space, in particular, has historically bred on impactful innovations with limited concerns on the finances. It would not be an understatement to claim that about 80% of the space technologies in use today evolved during the cold war. Being more of a competition for technological superiority than a market-driven one, the cold war, undoubtedly, acted as an impactful catalyst that triggered more architectural or radical innovations and not just derivatives.

Reduction in Overall Industry Profits

Undoubtedly, developing a space system is a technically and strategically challenging initiative, not to mention the scale of associated economics. However, the cut-throat competition that manifests in falling price trends and industry profitability might not justify the kind of efforts that need to be put in to enter the market. Publicly funded research by governments and other strategic bodies is one way to address this gap, but the government mode is not the most efficient means of getting things done. Also, there are chances for deterrence events such as the current Covid situation that may significantly alter the funding dynamics. Such perceived threats on reduction in potential returns can significantly affect the industry attractiveness over time.

Conclusion

In their iconic article “The art of Standard Wars,” Shapiro and Varian 11 have concluded that the key assets a firm should focus on to win standards game are

- Control over an installed base

- Intellectual property rights

- Ability to innovate

- Manufacturing abilities

- Reputation and brand name

- Strength in compliments

Bigger firms may tend to adopt pre-emption tactics (such as reduced design cycles, early deals with customers for manufacturing and launch, penetrative pricing), territorial wars, aggressive marketing campaigns, and lobbying for regulatory support to master the assets described earlier. However, considering space as a case in point, some of the assets just cited would get further boosted in a positive reinforcement loop through standardization, whereas some others would become irrelevant if the strength of standardization crosses a threshold that is somewhat uncertain at the moment. So, before the push for greater standardization overtakes the way we do things now, it is imperative to carry out a holistic study on the positives and negatives to delineate the boundaries between them and the industry knows where to stop.

The innovation quotient in the sector needs to be kept active, and governments will have to take up this responsibility by using public funding, which can be effected through various mechanisms such as contracting, infusion through government bodies, etc. There will also be appropriate rewarding mechanisms such as protection periods, enabling financial returns through pricing policies, direct rewards, etc., for the new innovators in the sector. Steps such as these from the government will have to be effectively implemented to bypass the inherent adverse effects accompanying standardization in the space sector. Table 1 gives a concise summary of the topics that were discussed in this article.

Comparison Summary—Standardization

Footnotes

ACKNOWLEDGMENTS

The author would like to record his deepest gratitude to Mr. Rakesh Sasibhushan, Chairman-cum-Managing Director, Antrix Corporation, for his invaluable guidance and reviews of the work streamlining the administrative formalities toward the publishing of this study. The author also would like to record his most sincere gratitude to Mr. S. Ramachandran, Principal Consultant, Infosys Knowledge Institute, for reviewing and giving valuable suggestions on the article. A record of gratitude is also due to Mr. Pawan Kumar Chandana, CEO, Skyroot aerospace, Hyderabad, India, for his constant encouragement and continued reviews and feedbacks on the article. The author also would like to place on record his most sincere indebtedness to Prof. Anshuman Tripathy, Strategy area, IIM-Bangalore, India, for his insightful tutelage on the strategic frameworks that are used in this article.

Author Disclosure Statement

No competing financial interests exist.

Funding Information

No funding received for the study.