Abstract

Abstract

As companies' impacts on society receive increasing attention, higher expectations are placed on accounting systems to consider effects on internal and external stakeholders. With a broader sustainability perspective, impacts of external effects caused by companies' operations are made visible in financial reports. This article argues that externalities should be recognized in financial reports and proposes ways to extend traditional balance sheets and income statements with information on companies' environmental, social, and economic impacts on society.

Introduction

When the scope of financial accounting is expanded 1 from considering only financial aspects to incorporating sustainability aspects of a business, a starting point is to include alternative valuation and profit concepts.

The traditional financial reporting postulate of accounting entity is based on ownership and control. 2 In financial reporting, an entire company or consolidated group is treated as an accounting entity. This entity postulate provides a natural basis for concepts used in traditional financial accounting, such as reporting on company or group profit in income statements and reporting in balance sheets the value of assets, debt, and equity owned or controlled by companies or groups.

With a broader sustainability perspective 3 that not only considers profit but also people and planet, additional positive and negative values, or externalities, are included for a larger group of stakeholders than those expressed in traditional financial statements. This article proposes ways to include companies' external environmental, social, and economic impacts in traditional financial statements. Externalities are defined and discussed with respect to their consequences to society. A concrete simplified example demonstrates how accounting for externalities can be added to traditional financial statements. A final discussion summarizes recommendations.

Asset: any resource owned or controlled by the company

Debt: what the company owes to others

Equity: the difference between assets and debt

Balance sheet: a statement of the book values of a company's assets, debt, and equity at a specific point in time

Revenue: the value of all sales recognized by a company in a specified period

Expense: costs incurred in a period by a company in its effort to generate revenues

Profit: the difference between revenues and expenses

Income statement: a statement of a company's recorded revenues, expenses, and profit during a particular period

Entity postulate: states that an accounting entity, that is, a company or group, from an accounting standpoint is assumed to be separate from other stakeholders, such as customers, suppliers, creditors, and owners; this means that only transactions and events that affect the company or group should be recorded (the effects on other stakeholders should not be considered in the balance sheet and income statement)

Externalities

An economic transaction is an act in which parties exchange goods or services, means of payment, or claims of economic value. If an economic transaction affects benefits and/or costs, not only for the transacting parties but also for third parties, there is an externality. Externalities affect third parties positively or negatively. If a manufacturing company, for example, releases air pollutants and does not have to pay for these pollutants, surrounding communities bear the costs of the emissions in the form of environmental pollution, clean-up efforts, disease onset, etc.

Externalities lead to market failures. A market failure is present when production and use of resources is not economically optimal. For manufacturing companies to be motivated to reduce emissions, it is important that they, and indirectly their customers, pay a price that corresponds to the value of the negative externality, for example, the value of the air pollution. When people or organizations that cause externalities also bear the associated costs or receive revenues when there are positive externalities, the externality is internalized. The issue is that these principles, which in theory may sound reasonable, are difficult to apply in practice4,5 because valuing externalities is associated with a high degree of subjectivity.6,7

One way of internalizing externalities synthetically is to self-estimate the value of the externalities and then incorporate them into financial reports. In order for companies to make visible all costs and benefits that are caused by their activities, accounting systems must be able to capture externalities. 8 When externalities are captured, alternative income statements and balance sheets result.

Accounting for Externalities—One Example

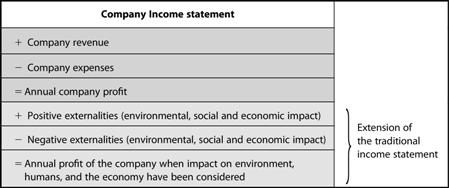

Accounting systems used by most companies do not adequately capture externalities caused by company activities. How could accounting systems be expanded to incorporate external effects? One possibility is to add three lines to the income statement, below the bottom line. The first additional line would show revenues from positive externalities, the second would show expenses from negative externalities, and the third would show the profit of the company when external effects have been considered (Table 1).

Traditional and Extended Income Statement

In the same way, it is possible to include in the balance sheet receivables and liabilities that are linked to future expected positive or negative externalities. Externalities enter the extended balance sheet in the form of externality assets and externality debt. The difference between externality assets and externality debt is externality equity (Table 2).

Traditional and Extended Balance Sheet

Example

During year X2, Company A reported revenues of 100, expenses of 80, and a profit amounting to 20 (Table 3). At the end of year X2 the reported value of assets is 250, the reported value of debt 170, and the reported value of equity 80 (Table 4).

Traditional and Extended Income Statement – Year 2

Traditional and Extended Balance Sheet – Year 2

When Company A prepares the income statement and balance sheet for year X2, management becomes aware that the company's operations have led to two external effects. The construction of a machine has led to emissions of a greenhouse gas that the company has not paid for. The greenhouse gas emissions will probably involve future negative effects in many forms, including higher sea levels. 9 For the sake of the example, the negative socioeconomic impact is assumed to be 15. (The measurement of externalities, i.e., the valuation issue, is beyond the scope of this article.) On the positive externality side, the company has invested in employees by offering them health education. The health education will lead to positive effects for society in the future as it improves the health of employees by increasing their knowledge and influencing their attitudes on health-related issues. The assessed positive socioeconomic effect of the health education is 17. Given these assumptions, the recording and reporting of externalities year X2 can be seen in Table 5, Table 6, and Table 7.

Recording of Externalities—Year X2

Traditional and Extended Income Statement—Year X2

Traditional and Extended Balance Sheet—Year X2

Continuing the example, if in year X3, it becomes apparent that the health education of the staff has little or no impact on society, externality assets are reversed or written down from 17 to 0 (see Table 9 and Table 10). Assuming that nothing else has happened during year X3 in Company A, Table 8 shows how Company A will record the new information.

Recording of Externalities—Year X3

Traditional and Extended Income Statement—Year X3

Traditional and Extended Balance Sheet—Year X3

Few companies incorporate externalities in their financial reports. One exception is Puma, a German multinational company that designs and manufactures footwear, accessories, and apparel. Puma records negative externalities in a separate income statement but not in a separate balance sheet. Positive externalities, however, are not considered. Puma's alternative income statement is called “Environmental Profit and Loss Statement” (EP&L), which the company describes and defines as follows.

An Environmental Profit and Loss Statement summarizes the externalized, i.e., not directly paid, cost to society caused by the environmental impact of an organization. The EP&L should not be mistaken with our financial P&L, which details our financial performance and results as publicly listed company. Our PUMA EP&L takes into consideration not only emissions from PUMAs own offices, stores and warehouses, but also from the whole upstream supply chain. This means we cover the impacts, for example, from the cotton farm until a T-shirt is sold in one of our PUMA stores. 10

Puma measures the environmental impact of its operations on water consumption, water pollution, waste, air pollution, greenhouse gas emissions, and land use, in monetary units. In 2017, the negative environmental impact was valued at €511 million ($572.8 million), according to Puma's EP&L. 11

Discussion and Summary

The example shows that it is possible to capture externalities in balance sheets and income statements. Accounting reports can thus act as instruments for internalizing the external effects caused by companies' activities. 12

The advantage of including externalities in the income statement is that it indicates how well the company has performed over a given period, from a societal perspective. The advantage of including externalities in the balance sheets is that it gives a snapshot of the company's 1.) accumulated liability to society when there are negative externalities and 2.) accumulated claims on society when there are positive externalities at the end of a period.

One argument against including externalities in accounting reports is that external effects are difficult to evaluate reliably and it is difficult to assess how externalities should be allocated in practice. In addition, there is a potential risk that record keeping and financial reporting could become too complicated and complex if externalities were included in accounting reports, and this complexity, in turn, negatively affects the comprehension and usefulness of financial reports. One possible way to avoid such issues is to present extended income statements and balance sheets in companies' sustainability reports and not in reports in which financial accounting information is presented.

Footnotes

Author Disclosure Statement

No competing financial interests exist.