Abstract

This report presents a detailed update to our 2008 publication on the tissue engineering (TE) and stem cell industry. Data are reported through mid 2011 showing an almost three-fold growth in commercial sales over the past 4 years. In addition, the number of companies selling products or offering services has increased over two-fold to 106, and they are generating a remarkable $3.5 billion in sales. Overall, the TE and stem cell sector is spending $3.6 billion and employing almost 14,000 employees. These data suggest the TE and stem cell industry has stabilized and is on a path pointing toward continued success.

Introduction

Lysaght et al. describe, in detail, the history of the name “TE” and the emergence of both the research field and the industry in the 20th century. 3 However, it is interesting to note that the ancient Egyptians may have been the first to apply TE principles to wound care around 1500 B.C. 8 In the Papyrus of Ebers, there is a description of how skin wounds were treated with lint, grease, and honey. It is believed that the lint served as a fibrous scaffold to guide wound regeneration, the grease provided a barrier to environmental pathogens, and the honey acted as an antibiotic. 8 It is not clear how this product was sold in ancient Egypt and whether they had any competitors, but it is clear that the field might be much older than we think.

Centuries later, in 1993, Langer and Vacanti defined TE as an “interdisciplinary field that applies the principles of engineering and the life sciences toward the development of biological substitutes that restore, maintain, or improve tissue or whole organ function”. 9 Generally, the term TE is now accepted to include regenerative medicine and stem cell therapeutics. In this report, TE and regenerative medicine are used interchangeably. Further, stem cell therapeutics are included, consisting of both cell-based therapies and stem cell banking. These terms have become rather commonplace in today's mass media culture. Google searches for the term “TE” produces 3.3 million hits and “regenerative medicine” 2.8 million hits, roughly double the hit rate compared to 4 years ago. 3 Likewise, a Google search of “stem cell” produces over 23 million hits.

Several other authors have evaluated the progress of the TE field. Most recently, Mason examined the cell therapy industry and characterized it as a distinct health care sector rapidly growing and transitioning into a successful multibillion dollar industry.10,11 It is important to note that Mason makes a clear distinction between regenerative medicine and cell therapy, which we do not. Therefore, it is difficult to compare the two analyses, other than to say that Mason's findings represent a portion of our findings. Similarly, Martin et al. have done a comprehensive survey focused on the cell therapy sector. 12 To the best of our knowledge, others have not done a broad TE and stem cell industry analysis as we have defined it.

Here we present an update to our 2008 publication (containing data analysis for 2007), which was coauthored by the late Michael J. Lysaght, in our continued efforts to follow the progress of this industry. Data are reported through mid 2011 and confirm that the industry is moving onward and upward. Compared to 2008, the current data show significant increases in commercial stage spending, number of FTEs and sales.

Methods

Compiling of company list

A list of companies in the TE space was prepared from the following:

1. The 2008 version of this report,

3

where the existence of each company was verified by checking the website and doing an internet search. Companies that no longer exist or were bought by another company were removed. 2. Daily Google Alerts derived from the terms “regenerative medicine,” “stem cell,” or “TE” between April and June 2011. Company names were found in news articles that were reported in these alerts. 3. Internet searches.

Company inclusion/exclusion criteria

Contract research organizations (CROs) that provide services for other TE firms were included. Organizations selling goods (e.g., laboratory equipment) or unrelated services (e.g., financial service firms) to operating firms were not included. Bioaesthetic products were excluded (e.g., creams prepared from conditioned media), except those products involving cell transplantation. In addition, the following were fully excluded: not-for-profit cord blood banks, veterinary firms, clinical services, organ or tissue allografts, conventional bone marrow transplantation for blood-borne cancers, transfusion medicine, and educational, media-based, or financial services.

The line between TE technology and other types of medical technology is often not clear and highly dependent upon the definitions imposed at the time. Although Dendreon's recent success with Provenge®, a cell-based immunotherapy for cancer treatment, is often touted as a breakthrough TE technology, we have elected not to include this type of product in our analysis. We excluded this because the cell-based therapy does not provide any regenerative or reconstructive function to a damaged organ or tissue. Dendreon is at the commercial stage and generates about $72M in sales. Had they been included, the industry market cap would have been drastically increased by $1.86B. Further, we have excluded those research efforts focused on “cancer stem cell” therapy and all medical technology in the cancer space.

It is important to note that we included stem cell banking companies in our industry analysis as commercial entities in the stem cell sector. The therapeutic potential of these stored cells to provide future regenerative function clearly enables this technology to fall within our definition.

Gathering company data

The following data were collected for each company from their respective websites. Founding year, location, and website address were obtained. Companies' underlying technology, or sector, was categorized as biomaterials, cells and biomaterials, stem cells (adult and embryonic), or other. These characterizations were based on the company's regenerative medicine portfolio and not by an individual product. For example, Genzyme (Sanofi) has three products, Carticel (cells), Epicel® (cells), and Maci® (cells and biomaterials), and therefore was classified as a “cells and biomaterials” company. Further, companies with products containing synthetic or biologically-derived materials, including proteins such as growth factors, were labeled as “biomaterials.” Cell type used (autologous, allogeneic, and/or xenogeneic), development status (preclinical, clinical trials, or commercial), clinical trial status (phase I, phase II, phase III) if applicable, and focus (e.g., wound healing, orthopedic, platform, etc.) data were also collected.

The size of a TE company was quantified by the number of FTEs and by overall operating expenditure. FTE counts were found in SEC reports, on company websites, and through email communication with companies. When not available by these methods, FTE counts were found on professional networking sites like LinkedIn. In the case where FTE counts were reported as a range (e.g., 1–10) the high and low ends of the range were averaged.

In those instances where overall operating expenditure was not available, estimates were calculated based on comparables with FTE counts. We determined a ratio of $265,900 spending per employee based upon a linear regression of annual spending against the number of employees for 39 TE companies for which both sets of data were available (R 2 =0.96). Excluded from this regression were diverse companies with a primary function other than TE, such as medical device companies and pharma.

For those companies with diverse product lines spanning TE and non-TE areas, we scoured SEC filings and press releases for revenue, spending, and FTE figures for the TE portion of the company. Only TE portions of diverse company statistics were included in any analysis. We estimated the percentage of the diverse company focused on TE mainly based upon revenues and used these percentages to calculate any applicable market caps. Spending and FTE were calculated using the aforementioned regression curve when both figures were not independently available from reported data.

We recognize that the data set presented is not perfect; companies may have been overlooked, estimates of FTE and/or sales values based on our regression may not be truly representative of actual data, data for some companies are missing, data may be outdated as the field is moving rapidly, and estimates of the percentage of company involvement in TE for companies researching in diverse areas of science may have a degree of error, among other things. However, we are confident that the data are representative of current trends and, if anything, are an underestimate. The field is growing and certainly these numbers will change in future analyses.

Results

Appendix A contains 202 companies that met the inclusion criteria. The company's name, location, sector (biomaterial, cells & biomaterial, stem cells, other), stage (preclinical, clinical trials, commercial, and service), and website are listed. For subsidiaries, the parent company name was included in parenthesis.

Table 1 summarizes key industry parameters for the TE and stem cell companies. Total sector activity is defined as total spending by companies on TE or stem cell products or services. Our analysis estimates this at $3.6 billion, which constitutes a 1.5-fold increase since our last analysis of data from 2007. 3 Total spending for commercial TE products or services is almost twice (1.8-fold) that of 2007, at $2.8 billion. The number of employees in the TE industry has increased by just over two-fold (2.3 ×) from 6100 to 13,810. Most of the remaining parameters had only slight increases since 2007. There are now 202 companies in this sector and 62% of them are U.S. based. A total of 122 companies are either in commercial or clinical trials stage, while 44 companies are providing services such as stem cell banking and CROs. The only parameter that showed a decrease in value, since the previous study, was development stage spending. Table 2 lists sales of TE or stem cell products by focus. Orthopedics leads the field at $1.7 billion in sales, followed by wound healing at $0.74 billion. Companies focused on multiple areas (e.g., wound healing and orthopedic) have $554 million in sales, while stem cell banking sales are at around $312 million. Specialties such as cardiovascular and fertility are grouped together as “other” and have $144 million in sales.

FTE, full time employees.

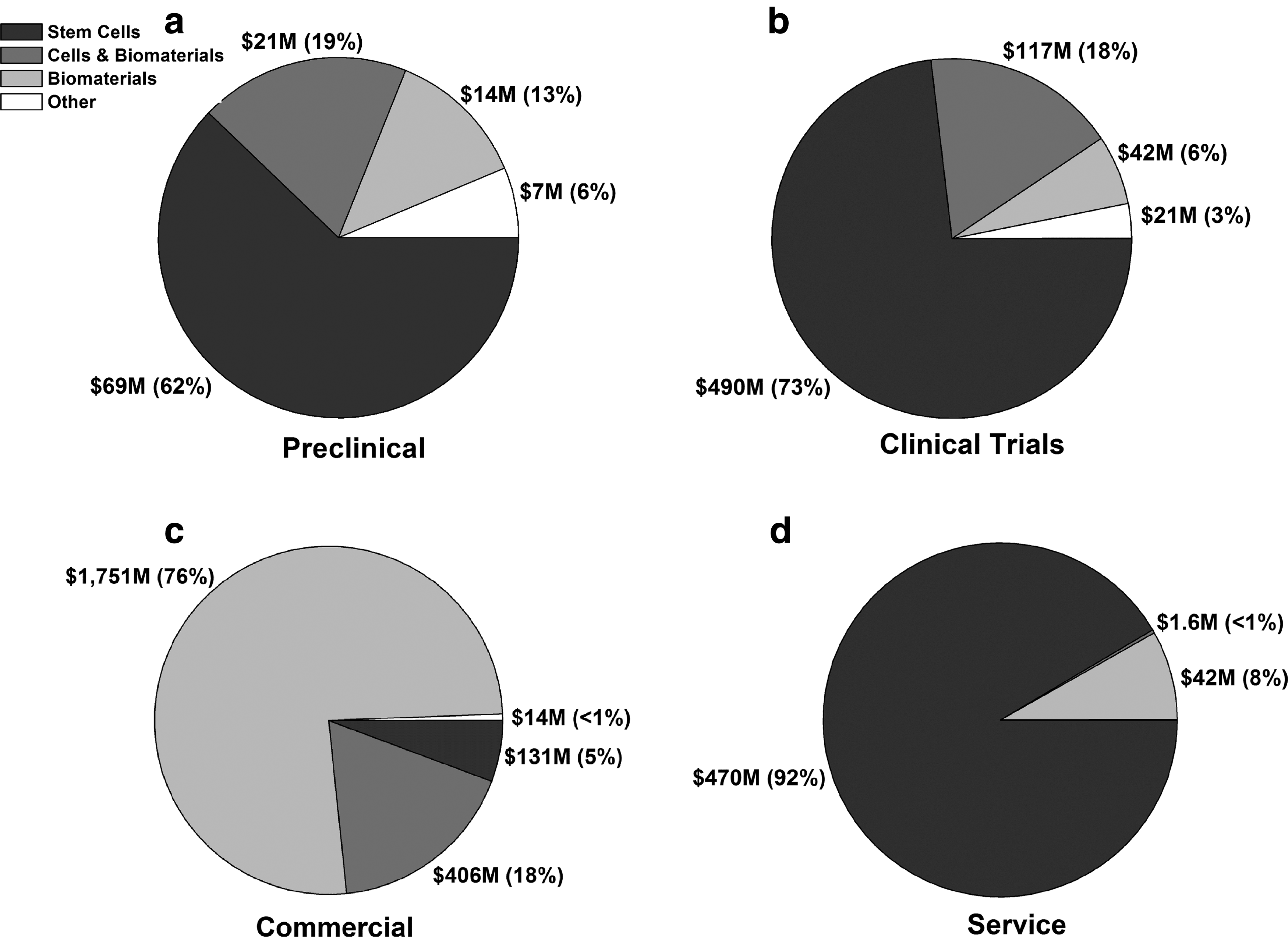

Figure 1 summarizes spending data listed in Table 1 and compares it to commercial sales for 2007 and 2011. In 2007, sales were half that of spending for the industry, while in 2011 sales nearly equaled spending (0.96 ×). In addition, sales increased almost three-fold (2.7 ×) in the 4 year period depicted. Figure 2 shows a detailed breakdown of spending by industry segment and stage. Preclinical (62%) and clinical trial (73%) stages of company development are dominated by stem cells, while the commercial (76%) and service (92%) stages are overwhelmingly populated by biomaterials and stem cell banking, respectively. Figure 3 illustrates total spending and number of companies with respect to stage. Spending is dominated by commercial stage companies (64%), while the number of companies operating in the four stages is about even. Figure 4 details the worldwide distribution of companies by spending, highlighting that the United States is leading the field with 81% of the worldwide investment.

Spending and sales (black) in billions for tissue engineering and stem cell therapeutics for 2007 and 2011. Preclinical and clinical trials stage spending is shown in ash gray while commercial stage spending is light gray.

Breakout of spending (in millions) by product platform for the four development stages: preclinical

Tissue engineering and stem cell therapeutics developmental stages by total spending (in millions)

Worldwide geographical distribution of spending.

Discussion

Perhaps the most important result of the presented data analysis is that sales for the TE and stem cell industry are $3.46B, which is approaching total spending ($3.6B) (Fig. 1). For the first time since Michael Lysaght started these analyses, the TE and stem cell industry is essentially breaking even.1–5 These data are in stark contrast to 2007 data, where product sales were about half of the spending volume. 3 Not only is TE a billion dollar industry, it is now close to operating in the black. This is quite an accomplishment considering the recent U.S. and global financial meltdown over the last 4 years.

As indicated in Table 1, almost all key industry parameters for this sector have increased compared to our 2007 data. 3 Overall spending for the field has increased from $2.4B to $3.6B, including a 1.8-fold increase in commercial stage spending from $1.6B from $2.8B (Fig. 1). Total spending increased 1.5-fold in the last 4 years, however, sales have increased 2.7-fold, indicating that sales increased at almost twice the rate of spending. Interestingly, development stage spending is the only industry parameter that has decreased over this time period. This could be due to several factors, including firms gaining market clearance and transitioning from development to commercial status, firms being bought out by larger commercial partners, and firms shutting down altogether. Only time will tell whether this decrease in the development sector will have an impact on pipelines and the number of products entering the market in the future. After all, it takes spending money in the short term to make money in the long term.

Even though development stage spending has decreased, there is still significant growth as the industry has generated over 7710 jobs in the last 4 years, a 2.3-fold increase compared to the 2007 analysis. Moreover, the total number of companies in TE has increased from 171 to 202 and in each stage of development indicating that the field is not only progressing but also sustaining itself. That is, as companies are moving products to market, others are entering the space with new technologies. Currently, 31% of the companies are in commercial product stage and another 21% of the companies are service based (e.g., stem cell banking), resulting in over 52% of the companies generating revenue for the industry. Another 30% of the companies are now in the clinical trial period, indicating a robust TE pipeline and a field that is expected to grow. However, the number of companies with products in clinical trials did not grow at the same rate as those with commercial products (1.1×vs. 1.3 ×, respectively). One reason for the larger growth of the commercial sector could be due to the poor economy. Perhaps financially transitioning from a successful clinical trial to a commercial product is easier compared to transitioning into clinical trials, where the risk is much greater. In addition, commercial-stage firms might be acquiring preclinical and clinical trial companies, which would deplete the number of companies in these two categories from our analyses.

It should be noted that we deviated from previous analysis methods and made a distinction between commercial-stage companies and service-based companies, that is, stem cell banks and CROs. We felt that this designation was more appropriate as these service companies do not follow a traditional product pipeline. In our previous analysis we included these companies at the commercial stage and had we done the same here, the increase in commercial stage companies would have been 2.2-fold higher, emphasizing again the successful integration of TE products into the health care market. It is no surprise, then, that the capital value of publicly traded companies in this space increased from $4.7B to $6.6B. This 1.4-fold increase in economic activity from 2007 to 2011 is not as dramatic as the five-fold increase from 2002 to 2007. However, previous accelerated growth has been attributed to the industry reorganizing itself and getting back on track from a low point. Today, the industry has begun to understand how to manufacture and market TE and stem cell products, sustaining itself and still growing.

Focusing just on commercial stage companies, the breakdown of sales by application specialty is summarized in Table 2. Orthopedics dominates the field at 49% or $1.7B in revenue with 19 companies. Not surprisingly, a large portion of this revenue is from Medtronic, which brings in an estimated $750M in sales with their bone graft product Infuse®. It is difficult to predict the future of Medtronic's dominance in this space as there has been a controversy regarding this blockbuster product. The scientific community recently raised concerns that clinical studies conducted with Infuse overstated benefits and understated risk. 13 One thing is for sure: a flurry of legal action will persist for years to come. There are certainly others that will be greatly affected—one way or the other—by the outcome of these developments. Baxter's bone graft product Actifuse® and their regenerative medicine business group show $527M in sales. Depuy, Orthovita, and Olympus Biotech report the next highest revenues in this specialty area, generating around $95M each. Depuy, a Johnson & Johnson company, has seven bone graft products on the market. Orthovita sells Vitoss™, a bone graft substitute, and Olympus, after acquiring Stryker Biotech in 2010, has two commercial products, OP-1™ Putty and OP-1 Implant.

Wound healing is the second largest specialty area by sales at 21% with 15 companies and $738M in revenue. There are three major players in this area: Kinetic Concepts, Advanced BioHealing, and Organogenesis. Kinetic Concepts generates $340M in revenue with Graftjacket®. Advanced BioHealing, a Shire company, lists about $150M in sales with their Dermagraft® skin product. Organogenesis, one of the original TE companies founded in 1985 and whose progress has been well documented in earlier analyses, 3 is making around $100M in revenue with Apligraf.

The category “multiple” includes 16 companies that have products in more than one application specialty and their estimated sales are $554M. For example, Integra Life Sciences has both orthopedic products (Accell Evo3®, Mozaik™ and Allograft Cancellous Sponge) and a wound healing product (Dermal Regeneration Template) and brings in around $170M annually. Similarly, Covidien has DuraSeal™ for wound healing and Collagen Repair Patch for orthopedic applications, generating revenue around $95M.

Stem cell banking is the third most profitable specialty area with sales at $312M. These companies have a very efficient service business model based upon liquid nitrogen storage capabilities and limited personnel oversight. Typically, they collect one-time initiation fees and subsequent annual storage fees for up to 20 years. The utility of this service is not clear as little evidence exists about the viability of cord blood cells (or fat stem cells, dental stem cells, and other types of stem cells that can be banked) over a 20 year span. Further, it is not yet known how banking can significantly help the elderly population, who arguably have the most need for TE engineering therapies. Nevertheless, these businesses thrive and make 9% of the industry revenues in our analysis.

Finally, five companies were listed under “other” as they are focused on cardiovascular, fertility, or platform technologies. This group brings in around $144M in sales and is dominated by Cryolife ($116M in sales) which has SynerGraft® platform for cell transplantation.

Overall, these data are encouraging and indicate that the TE and stem cell industry is alive and well. About 42% of the companies at the commercial stage are generating a profit, which leaves 58% that are not. This breakdown will most likely shift in the future as the health care field becomes more familiar with TE and stem cell technologies and these products become common therapeutic options. Further commercial success will also depend on companies having a better understanding of the FDA approval processes. 14 Even with the introduction of the FDA Office of Combination Products in 2002, a recent survey found that one of established companies' (defined as companies with ongoing, predictable product sales and growth) most difficult hurdles is working with the FDA. 15

A detailed breakdown of spending by industry segment (i.e., product platform) and stage is illustrated in Figure 2. The preclinical stage is dominated by stem cells at 62% ($69M), followed by cells and biomaterials at 19% ($21M). Biomaterials and other constitute 13% ($14M) and 6% ($7M), respectively. A very similar trend follows for the clinical trials stage, indicating that stem cell-based therapies are dominating the product pipeline (Fig. 2a, b). These data suggest that stem cell-based products and combination products (cells and biomaterials) will be entering the market in the next 5–10 years. Their entrance into the commercial space will be interesting to watch as recent actions within the FDA and with the 510(k) process will greatly affect the commercialization of these products.

Of particular note is the entrance of embryonic stem cell (ESC)-based therapies into clinical trials for the first time. Geron's Phase I clinical trial for GRNOPC1 in spinal cord injury was given a green light in the summer of 2010 and the first patient was enrolled later that year. 16 Advanced Cell Technology (ACT) quickly followed behind with two Phase I/II trials with their human ESC (hESC) derived retinal pigment epithelial (RPE) cell therapy for dry age-related macular degeneration and Stargardt's macular dystrophy. The first patients for these studies were dosed in July of this year. 17 Interestingly, on November 14, 2011 Geron announced on their website that they are discontinuing their stem cell program to focus on their cancer therapies. Geron was considered a leader in the stem cell industry; their clinical trial experiences are of great interest not only to industrial competitors but also to academics. Regardless of their outcomes, these stem cell trials are the first of their kind and they are likely to have a large impact on the future of ESC-based therapies.

A breakdown by cell source shows that companies with stem cell-based products favor autologous cells (59%), followed by allogeneic (39%) and only 2% utilize xenogeneic cells. In addition, the majority (58%) of stem cell companies are utilizing adult stem cell technologies, while only 10% are specializing in ESCs. The remaining 32% are focused on stem cell banking services. Again, the outcome of the Geron and ACT hESC clinical trials could initiate a shift in trend for autologous versus allogeneic stem cells and for adult stem cell versus ESCs.

Biomaterial-based products are overwhelmingly present in the commercial stage with 76% ($1.8B) in spending. Combination products and stem cells follow at significantly lower volumes of $406M and $131M, respectively. Such products are generally classified as devices and have an easy path to market through the FDA, so it is not surprising that they are the frontrunner in this industry sector. Hopefully, as the cell-based sector gains more experience with the FDA, and vice versa, the path to market will be clearer for these products.

The FDA has started responding to the emergence of the TE field and is adapting quality systems and regulatory pathways to the specialized nature of TE products. Importantly, it was not until 2005 that current good tissue practices were mandated ensuring quality manufacturing procedures for human cell, tissue, and cellular and tissue-based products. Since the regulatory aspects of this industry are only beginning to develop and distinguish from other health care products, we believe that there will still be some uncertainty as more complex TE products move through the pipeline and the policies are refined and adapted accordingly. With this in mind, we think that the CROs for the TE industry will thrive when R&D firms find it difficult to keep up with these regulatory changes and the very specialized nature of the manufacturing and quality systems necessary for TE market approval.

Though we have paid particular attention to the role of the FDA approval process in achieving sales, it is important to consider that simply gaining FDA approval does not guarantee success. Another critical element of commercial success is achieving reimbursement. 18 As the TE industry is gaining experience with the FDA process, reimbursement is becoming the new grand hurdle. The “black box” of coverage, payment, and coding associated with reimbursement can lead to the failure of an FDA-approved TE therapy. Once reimbursement has been decoded (if reimbursement can be decoded), perhaps the sky is the limit!

Finally, service is dominated by stem cell banking firms and CROs performing the manufacturing for TE companies (Fig. 2d). As mentioned above, the stem cell banking business model is rather simple and one might expect that it will grow and continue to lead in this area.

Spending in the TE and stem cell sector by developmental stage is shown in Figure 3a. Here, commercial stage spending is at $2.3B (64%) and is separated from service ($514M, 14%), in contrast to the analysis in Table 1 and Figure 1. As one would expect, most of the spending is done by companies that have products on the market, followed by companies in clinical trials and service. Finally, the least amount of spending is done by companies at the preclinical stage. This is expected as one proceeds down the regulatory pathway for product approval, the costs for product development increase. The number of companies at each stage of development are not as skewed (Fig. 3b). Both clinical trials and commercial stage companies are approximately equal at 30%, and service and preclinical are even at about 20%. This further emphasizes the increase in spending at the clinical trial and commercial stages of product development. Comparing these data with our 2007 analysis, we note some interesting changes. For example, the number of commercial companies (including service) increased two-fold from 47 to 106 and the number of preclinical stage companies decreased almost two-fold from 67 to 36. As discussed above, this increase and decrease could be attributed to more products flowing down the pipeline to the market. Other possibilities include acquisitions by larger firms or going out of business. The spending distribution by geographic region (Fig. 4) still shows that the United States is leading by over 81%, a 7 percentage point increase from 2007. This indicates that the distribution of spending for the TE and stem cell industry has not drastically changed and that the United States is still the dominant player in this area.

The analyses presented show that the TE and stem cell industry is just attaining profitability and that it appears to be on a positive trajectory. Although it seems that the industry is on a smoother path now than it probably ever has been, we do anticipate that there may be growth pains as the industry matures.

Footnotes

Acknowledgments

This work would not have been possible without the late Dr. Michael Lysaght, who was a deep source of inspiration and knowledge. Dr. Lysaght was a force in the TE community and is sorely missed. Dear Michael, we dedicate this work to you.

Disclosure Statement

No competing financial interests exist.

Appendix

| Company | Location | Sector | Stage | Website |

|---|---|---|---|---|

| 3DM | Boston, MA | Biomaterials | Preclinical | www.puramatrix.com |

| Aastrom Biosciences | Ann Arbor, MI | Stem Cells | Clinical trials | www.aastrom.com |

| ACell | Columbia, MD | Biomaterials | Commercial | www.acell.com/ |

| Advanced Biohealing (Shire) | New York, NY | Cells and Biomaterials | Commercial | http://advancedbiohealing.com |

| Advanced Cell Technology | Worcester, MA | Stem Cells | Clinical trials | www.advancedcell.com |

| Advanced Technologies and Regenerative Medicine | Raynham, MA | Cells and Biomaterials | Clinical trials | www.atrm.com/ |

| Aldagen | Durham, NC | Stem Cells | Clinical trials | www.aldagen.com |

| Allocure | Burlington, MA | Stem Cells | Clinical trials | www.allocure.com/ |

| Altrika (Ilika) | United Kingdom | Cells and Biomaterials | Commercial | www.altrika.co.uk/ |

| American CryoStem | Red Bank, NJ | Stem Cells | Service | www.americancryostem.com/ |

| Amni Bioscience | Lebanon | Stem Cells | Preclinical | www.amnibioscience.com/ |

| Amorcyte | Allendale, NJ | Stem Cells | Clinical trials | www.amorcyte.com/ |

| Angioscaff | Switzerland | Biomaterials | Preclinical | www.angioscaff.eu |

| Aquamed Technologies (Alliqua) | Langhorne, PA | Biomaterials | CRO | www.aquamedinc.net/ |

| Arbios | Los Angeles, CA | Cells and Biomaterials | Clinical trials | www.arbios.com |

| ArBlast USA | Japan | Cells and Biomaterials | Clinical trials | www.arblast-usa.com/index.html |

| Arteriocyte | Clevand, OH | Stem Cells | Clinical trials | www.arteriocyte.com/ |

| Arthro Kinetics | Germany | Cells and Biomaterials | Commercial | www.arthro-kinetics.com |

| Athersys | Clevland, OH | Stem Cells | Clinical trials | www.athersys.com/ |

| AuxoCell Laboratories | Cambridge, MA | Stem Cells | Service | auxocell.com/ |

| Avita Medical | Australia | Other | Commercial | www.avitamedical.com/ |

| Axcelon Biopolymers | Canada | Biomaterials | Commercial | www.axcelonbp.com/ |

| Azellon | United Kingdom | Stem Cells | Preclinical | www.azellon-ltd.com/ |

| Bacterin International | Belgrade, MT | Biomaterials | Commercial | www.bacterin.com/index.htm |

| Baxter | Deerfield, IL | Biomaterials | Commercial | http://baxter.com |

| Bayer Innovations | Germany | Stem Cells | Preclinical | www.bayer-innovation.com |

| Beike Biotechnology | China | Stem Cells | Clinical trials | www.beikebiotech.com/ |

| BetaCell | Belgium | Cells and Biomaterials | Preclinical | www.beta-cell.com |

| Biocell Center | Boston, MA | Stem Cells | Service | www.biocellcenter.com/ |

| Biocomposites | England | Biomaterials | Commercial | www.biocomposites.com/ |

| Bioheart | Sunrise, FL | Stem Cells | Clinical trials | www.bioheartinc.com |

| Biomerix | Fremont, CA | Biomaterials | Commercial | www.biomerix.com/ |

| Biomet | Warsaw, IN | Biomaterials | Commercial | www.biomet.com/corporate/index.cfm |

| Biomimetic Therapeutics | Franklin, TN | Biomaterials | Commercial | www.biomimetics.com |

| Bionova | Australia | Cells and Biomaterials | Commercial | www.bionova.com.au/ |

| BioParadox, Inc | Menlo Park, CA | Other | Preclinical | http://plateletcelltherapy.com/ |

| Biosurface Engineering Technologies | Rockville, MD | Biomaterials | Clinical trials | www.biosetinc.com/ |

| BioTime, Inc | Alameda, CA | Stem Cells | Preclinical | www.biotimeinc.com/ |

| BioTissue AG | Miami, FL | Cells and Biomaterials | Commercial | www.biotissue.com/ |

| Biotissue Technologies | Germany | Cells and Biomaterials | Commercial | www.biotissue.de |

| BrainStorm Cell Therapuetics | Israel | Stem Cells | Clinical trials | www.brainstorm-cell.com |

| California Stem Cell | Irvine, CA | Stem Cells | Preclinical | http://californiastemcell.com/ |

| Cardio | Japan | Cells and Biomaterials | Preclinical | www.cardio.co.jp |

| Cardio3 BioSciences | Belgium | Stem Cells | Clinical trials | www.c3bs.com/ |

| Cardiocreate | San Diego, CA | Stem Cells | Preclinical | www.cardiocreate.com |

| Cardium Therapeutics | San Diego, CA | Biomaterials | Clinical trials | www.cardiumthx.com/ |

| CBR Systems | San Bruno, CA | Stem Cells | Service | www.cordblood.com/ |

| Celgene | Summit, NJ | Stem Cells | Service | www.celgene.com/ |

| Cell Care Australia | Australia | Stem Cells | Service | www.cellcareaustralia.com/ |

| Cell Matrix AB | Sweden | Cells and Biomaterials | Commercial | www.cellmatrix.se |

| Cellerant Therapeutics | San Carlos, CA | Stem Cells | Clinical trials | www.cellerant.com |

| Cellerix | Spain | Stem Cells | Clinical trials | www.cellerix.com/ |

| CellGenix Technologie Transfer GmbH | Germany | Stem Cells | Commercial, CRO | www.cellgenix.com |

| Celling Technologies | Austin, TX | Stem Cells | Clinical trials | www.cellingtechnologies.com/ |

| Cells for Life | Canada | Stem Cells | Service | www.cellsforlife.com |

| Cephalon | Frazer, PA | Stem Cells | Clinical trials | www.cephalon.com/ |

| Cerco Medical llc | San Francisco, CA | Cells and Biomaterials | Preclinical | www.cercomedical.com |

| Co.don | Germany | Cells and Biomaterials | Commercial | www.codon.de |

| Cognate BioServices Inc | Baltimore, MD | Stem Cells | CRO | www.cognatebioservices.com |

| Cook Biotech Ltd | West Layfayette, IN | Biomaterials | Commercial | www.cookbiotech.com |

| Cord Blood America | Los Angeles, CA | Stem Cells | Service | www.cordblood-america.com/ |

| Cord Blood Bank of Canada | Canada | Stem Cells | Service | www.cordbloodbankofcanada.com |

| Cordbank | New Zealand | Stem Cells | Service | www.cordbank.co.nz |

| CordLife Limited | Singapore | Stem Cells | Service | www.cordlife.com/ |

| Covidien | Ireland | Biomaterials | Commercial | www.covidien.com/ |

| Cryo-Save | Netherlands | Stem Cells | Service | www.cryo-save.com |

| CryoCell | Oldsmar, FL | Stem Cells | Service | www.cryo-cell.com/ |

| Cryocord | Malaysia | Stem Cells | Service | www.cryocord.com.my/ |

| Cryolife | Atlanta, GA | Biomaterials | Commercial | www.cryolife.com/ |

| Cryosite | Australia | Stem Cells | Service | www.cryosite.com/ |

| Cytograft | Novato, CA | Cells and Biomaterials | Clinical trials | www.cytograft.com |

| Cytomedix | Gaithersburg, MD | Cells and Biomaterials | Commercial | www.cytomedix.com/ |

| Cytonet Hannover Gmbh | Germany | Stem Cells | Clinical trials | www.cytonet.de |

| Cytori Therapeutics | San Diego, CA | Stem Cells | Commercial | www.cytoritx.com |

| Depuy (Johnson & Johnson) | New Brunswick, NJ | Biomaterials | Commercial | www.depuy.com/ |

| Educell | Slovenia | Cells and Biomaterials | Commercial | www.educell.si |

| EndGenitor Technologies | Indianapolis, IN | Stem Cells | Preclinical | www.endgenitor.com |

| Escape Therapeutics Inc | San Jose, CA | Stem Cells | Preclinical | http://escapetherapeutics.com/ |

| Eticur | Germany | Stem Cells | Service | www.eticur.de |

| Eufets AG | Germany | Stem Cells | CRO | www.eufets.com |

| Euroderm Biotech | Switzerland | Cells and Biomaterials | Commercial | www.euroderm-biotech.de |

| Exactech Inc | Gainesville, FL | Biomaterials | Commercial | www.exac.com/ |

| Excorp | Minneapolis, MN | Cells and Biomaterials | Clinical trials | www.excorp.com/ |

| Eyegenix (Cellular Bioengineering) | Honolulu, HI | Biomaterials | Clinical trials | www.eyegenix.com/ |

| Family Cord | Los Angeles, CA | Stem Cells | Service | www.familycord.com/ |

| Fate Therapeutics | San Diego, CA | Stem Cells | Clinical trials | www.fatetherapeutics.com/ |

| FCB-Pharmicell | Korea | Stem Cells | Service | www.fcbpharmicell.com/english/ |

| Forticell | Englewood Cliffs, NJ | Cells and Biomaterials | Commercial | www.forticellbioscience.com/ |

| Future Health | United Kingdom | Stem Cells | Service | www.futurehealth.co.uk |

| Gamida Cell Ltd | Israel | Stem Cells | Clinical trials | www.gamida-cell.com |

| Genegrafts Ltd | Israel | Other | Preclinical | www.genegrafts.com |

| Genevrier (Endocell) | France | Cells and Biomaterials | Commercial | www.laboratoires-genevrier.com |

| Genzyme (Sanofi) | Bridgewater, NJ | Cells and Biomaterials | Commercial | www.genzyme.com/ |

| Geron | Menlo Park, CA | Stem Cells | Clinical trials | www.geron.com |

| Healthpoint Biotherapeutics | Fort Worth, TX | Stem Cells | Commercial | www.healthpointbio.com/ |

| Histogen Inc | San Diego, CA | Biomaterials | Clinical trials | www.histogen.com/ |

| Histogenics | Waltham, MA | Cells and Biomaterials | Clinical trials | www.histogenics.com |

| Histostem | South Korea | Stem Cells | Commercial | www.histostem.co.kr/english/english_1.htm |

| Humacyte | Research Triangle, NC | Biomaterials | Preclinical | www.humacyte.com |

| Hybrid Organ GMBH | Germany | Cells and Biomaterials | Clinical trials | www.hybrid-organ.com |

| Inion Ltd | Finland | Biomaterials | Commercial | www.inion.com/ |

| Innovacell | Austria | Other | Clinical trials | www.innovacell.at |

| Integra Life Sciences | Plainsboro, NJ | Biomaterials | Commercial | www.IntegraLife.com/ |

| IntelliCell BioSciences | New York, NY | Stem Cells | Preclinical | www.intellicellbiosciences.com/ |

| Intercytex (Regenerative Solutions) | United Kingdom | Cells and Biomaterials | Clinical trials | www.intercytex.com |

| International Stem Cell Corporation | Carlsbad, CA | Stem Cells | Preclinical | www.internationalstemcell.com |

| International Stem Cell Institute | San Diego, CA | Stem Cells | Commercial | www.istemcelli.com/ |

| InVivo Therapeutics | Cambridge, MA | Stem Cells | Preclinical | www.invivotherapeutics.com/ |

| iPierian Inc. | San Francisco, CA | Stem Cells | Preclinical | www.ipierian.com/ |

| ISTO Technologies Inc. | St Louis, MO | Cells and Biomaterials | Commercial | www.istotech.com |

| Ivy Sports Medicine | Franklin Lake, NJ | Biomaterials | Commercial | www.regenbio.com/ |

| Japan Tissue Engineering Co | Japan | Cells and Biomaterials | Commercial | www.jpte.co.jp/english/ |

| Kensey Nash | Exton, PA | Biomaterials | Commercial | www.kenseynash.com/ |

| Keranetics | Winston-Salem, NC | Biomaterials | Preclinical | www.keranetics.com |

| Kinetic Concepts Inc | San Antonio, TX | Biomaterials | Commercial | www.kci1.com/KCI1/home |

| Kuros Biosurgery | Switzerland | Biomaterials | Clinical trials | www.kuros.ch |

| Lazaron Biotechnologies | South Africa | Stem Cells | Service | www.lazaron.co.za |

| Lifeforce Cryobanks | Altamonte Springs, FL | Stem Cells | Service | www.lifeforcecryobanks.com/ |

| Lifeline | Cyprus | Stem Cells | Service | www.lifelinecordblood.com/ |

| Living Cell Tehnologies | Australia | Cells and Biomaterials | Clinical trials | www.lctglobal.com |

| Medistem Laboratories | Tempe, AZ | Stem Cells | Preclinical | www.medisteminc.com |

| Medtronic | Minneapolis,MN | Biomaterials | Commercial | www.medtronic.com/ |

| Mesynthes | New Zealand | Biomaterials | Commercial | www.mesynthes.com/ |

| MiMedx Group, Inc | Marietta, GA | Biomaterials | Commercial | www.mimedx.com/ |

| Miromatrix | Eden Prairie, MN | Biomaterials | Preclinical | www.miromatrix.com/ |

| Morphogenesis | Oldsmar, FL | Stem Cells | Preclinical | www.morphogenesis-inc.com |

| Nanotope | Skokie, IL | Biomaterials | Preclinical | www.nanotope.com/ |

| NeoMend | Irvine, CA | Biomaterials | Commercial | www.neomend.com/ |

| NeoStem | Agoura Hills, CA | Stem Cells | CRO, Service | www.neostem.com |

| Neotherix | United Kingdom | Biomaterials | Preclinical | www.neotherix.com/index.php |

| Neuralstem | Rockville, MD | Stem Cells | Clinical trials | www.neuralstem.com |

| NeuroGeneration | Beverly Hills, CA | Stem Cells | Clinical trials | www.neurogeneration.com |

| Neurotech | Lincoln, RI | Cells and Biomaterials | Clinical trials | www.neurotechusa.com |

| New England Cord Blood Bank | Newton, MA | Stem Cells | Service | www.cordbloodbank.com |

| NsGene | Denmark | Cells and Biomaterials | Clinical trials | www.nsgene.dk |

| Olympus Biotech | Hopkinton, MA | Biomaterials | Commercial | www.op1.com/ |

| Opexa Therapeutics | The Woodlands, TX | Stem Cells | Clinical trials | www.opexatherapeutics.com |

| Organogenesis | Canton, MA | Cells and Biomaterials | Commercial | www.organogenesis.com |

| Organovo | San Diego, CA | Cells and Biomaterials | CRO, Preclinical | www.organovo.com/ |

| Oristem (Pharmacells Ltd.) | Scotland | Stem Cells | Service | oristem.com/ |

| Orthovita | Malvern, PA | Biomaterials | Commercial | www.orthovita.com |

| Osiris | Baltimore, MD | Stem Cells | Clinical trials | www.osiris.com/ |

| Pathfinder Cell Therapy | Iselin, NJ | Biomaterials | Commercial | www.pathfindercelltherapy.com/ |

| Pervasis | Cambridge, MA | Cells and Biomaterials | Clinical trials | www.pervasistx.com |

| Pioneer Surgical | Marquette, MI | Biomaterials | Commercial | www.pioneersurgical.com |

| Plasticell | United Kingdom | Stem Cells | CRO | www.plasticell.co.uk/ |

| Plureon Corporation | Winston-Salem, NC | Stem Cells | Preclinical | www.plureon.com |

| Pluristem Therapeutics | Israel | Stem Cells | Clinical trials | www.pluristem.com |

| PrimeGen Biotech Corporation | Irvine, CA | Stem Cells | Preclinical | www.primegenbiotech.com |

| Provia Labs | Lexington, MA | Stem Cells | Service | www.provialabs.com/ |

| Q Therapeutics | Salt Lake City, UT | Stem Cells | Preclinical | www.qthera.com/ |

| Q-Med | Sweden | Biomaterials | Commercial | www.q-med.com/ |

| Regenerative Medical Systems | United Kingdom | Cells and Biomaterials | Commercial | www.rmsbio.net/ |

| Regenicin, Inc. | Little Falls, NJ | Cells and Biomaterials | Clinical trials | www.regenicin.com/ |

| Regenics A/S | Norway | Stem Cells | Preclinical | www.regenics.no |

| Regenocyte | Bonita Springs, FL | Stem Cells | Commercial | www.regenocyte.com/ |

| Regentec | United Kingdom | Cells and Biomaterials | CRO, Preclinical | www.regentec.net/ |

| Regentis Biomaterials | Israel | Biomaterials | Clinical trials | www.regentis.co.il |

| Reneuron | United Kingdom | Stem Cells | Clinical trials | www.reneuron.com |

| RhinoCyte | Louisville, KY | Stem Cells | Preclinical | www.RhinoCyte.com |

| RNL Bio (EHE Biocell) | Korea | Stem Cells | Clinical trials | www.rnl.co.kr/eng |

| SanBio | Mountain View, CA | Stem Cells | Clinical trials | www.san-bio.com/ |

| Scil Technology | Germany | Biomaterials | Clinical trials | www.sciltechnology.com/ |

| Secant Medical | Perkasie, PA | Biomaterials | CRO | www.secantmedical.com/ |

| Securacell | Canton, OH | Stem Cells | Service | www.securacell.com |

| Soluble Systems | Newport News, VA | Cells and Biomaterials | Commercial | www.solublesystems.com/ |

| SpineSmith | Austin, TX | Cells and Biomaterials | Preclinical | www.spinesmithusa.com/ |

| Stem Cell Assurance | Jupiter, FL | Stem Cells | Service | www.stemcellassurance.com/ |

| Stem Cells for Hope, Inc | Calverton, NY | Stem Cells | Commercial | www.stemcellsforhope.com/ |

| Stemagen | San Diego, CA | Stem Cells | Preclinical | www.stemagen.com |

| StemCells | Palo Alto, CA | Stem Cells | Clinical trials | www.stemcellsinc.com |

| Stemcyte | Arcadia, CA | Stem Cells | Service | www.stemcyteinc.com |

| Stemedica Cell Technologies, Inc. | San Diego, CA | Stem Cells | Clinical trials | www.stemedica.com/ |

| Stemlife | Malaysia | Stem Cells | Service | www.stemlife.com/ |

| Stemnion Inc | Pittsburgh, PA | Stem Cells | Clinical trials | www.stemnion.com |

| Stempeutics | India | Stem Cells | Clinical trials | www.stempeutics.com/ |

| StemSave | New York, NY | Stem Cells | Service | www.stemsave.com/ |

| TEI Biosciences | Boston, MA | Biomaterials | Commercial | www.teibio.com/ |

| Tengion | East Norriton, PA | Cells and Biomaterials | Clinical trials | www.tengion.com/ |

| Tepha | Cambridge, MA | Biomaterials | Commercial | www.tepha.com |

| Tetec | Germany | Cells and Biomaterials | Commercial | www.tetec-ag.com/ |

| Theradigm | Baltimore, MD | Stem Cells | Preclinical | www.theradigm.com |

| Theregen | San Francisco, CA | Cells and Biomaterials | Clinical trials | www.theregeninc.com |

| TiGenix | Belgium | Stem Cells | Commercial | www.tigenix.com |

| Tissue Genesis | Honolulu, HI | Stem Cells | Clinical trials | www.tissuegenesis.com/ |

| Tissue Regeneration Therapeutics | Canada | Stem Cells | Commercial | www.verypowerfulbiology.com/ |

| Tissue Regenix | United Kingdom | Biomaterials | Commercial | www.tissueregenix.com/ |

| TissueGene | Gaithersburg, MD | Other | Clinical trials | www.tissuegene.com |

| Tornier | Edina, MN | Biomaterials | Commercial | www.tornier.com/ |

| TotipotentRX Cellular Medicine | Los Angeles, CA+India | Stem Cells | CRO, Service | www.totipotentrx.com/ |

| Tristem Corporation | United Kingdom | Stem Cells | Clinical trials | www.tristemcorp.com |

| VasoTissue Technologies | Germany | Cells and Biomaterials | Clinical trials | www.vasotissue.com |

| Veltion Cell Therapeutics Limited | United Kingdom | Stem Cells | Preclinical | www.veltioncell.com/ |

| Vescell | Thailand | Stem Cells | Commercial | www.vescell.com |

| ViaCord (PerkinElmer) | Cambridge, MA | Stem Cells | Service | www.viacord.com/ |

| ViaCyte Inc. | San Diego, CA | Stem Cells | Preclinical | www.viacyte.com/ |

| Virgin Health Bank | United Kingdom | Stem Cells | Service | www.virginhealthbank.com |

| VistaGen Therapeutics Inc. | Durham, NC | Stem Cells | Clinical trials | www.vestatherapeutics.com |

| Vita 34 AG | Germany | Stem Cells | Service | www.vita34.de |

| Vital Therapies | San Diego, CA | Cells and Biomaterials | Clinical trials | www.vitaltherapies.com |

| ViviCells International | Evanston, IL | Stem Cells | Service | www.vivicells.com |

| Zimmer | Warsaw, IN | Cells and Biomaterials | Commercial | www.zimmer.com/ |