Abstract

This study reexamines organizational learning theories to reconcile the conditions under which prior internationalization experience leads to performance gains for multinational corporations (MNCs) with varying host-country institutional experiences in different regulatory environments. Using field studies on telecommunications regulation, executive interviews conducted in Brazil, Spain, Portugal, Canada, and the U.S., and foreign direct investment data for 96 subunit operations investing in the Brazilian telecommunications industry from 1997 to 2004, I develop an experiential-learning theoretical framework to explain the mechanisms driving MNCs’ performance in subsequent host-country institutional environments given the prior experience they acquired in 80 heterogeneous regulatory environments. I predict and find that MNCs with highly similar institutional experience compared with the target country’s institutional environment will succeed. Empirical evidence suggests that similarity, breadth, and depth of prior regulatory experience significantly prolong survival. In contrast, firms with institutional experience unrelated to the target country’s regulatory environment experience learning penalties and are six times more likely to fail. These findings suggest that variations in learning contexts affect organizations’ learning curves.

Keywords

International business scholars have long been interested in understanding the role of experience in foreign direct investment entry, entry mode, valuation, and survival. Some have established that prior experience in a host-country context leads to positive performance gains from increased market-specific knowledge (Johanson and Vahlne, 1977; Li, 1995; Shaver, Mitchell, and Yeung, 1997). When the learning environment is stable, these findings parallel more general experiential learning theories that predict performance benefits (e.g., productivity, quality, survival) as the overall level of experience increases (Levitt and March, 1988; for a review, see Argote, 1999). Several empirical studies in the organizational learning literature demonstrate similar learning effects of prior experience mainly by replication of routines in the same contextual environment (Dutton, Thomas, and Butler, 1984; Darr, Argote, and Epple, 1995; Epple, Argote, and Murphy, 1996).

Theoretical predictions are more questionable, however, when the environmental context of learning changes. Institutional environments, generally characterized by idiosyncratic laws, regulations, political hazards, and cultural norms, are known to affect strategic decision making (e.g., Kogut and Singh, 1988; Henisz and Delios, 2004; Zhao, 2006; Siegel and Larson, 2008) and performance outcomes (Barkema, Bell, and Pennings, 1996; Shaver, Mitchell, and Yeung, 1997; Henisz and Delios, 2004; Berry and Sakakibara, 2008). In the global context, where keen distinctions define heterogeneous country-level institutional environments (see Henisz, 2004; and Guillén and Suarez, 2005, for reviews), it is unclear how prior experiences acquired in other countries contribute to multinational corporations’ (MNCs’) performance in new host countries. Despite the growing body of knowledge about organizational learning in the global context, this puzzle remains unsolved. What firms learn from heterogeneous host-country environments, and whether all types of prior experience have the same propensity to lead to future performance improvements, remains unknown. This study builds on experiential learning theories in both the organizational learning and international business literatures to explore the boundaries of learning across heterogeneous institutional contexts and to examine the effects on subsequent performance. I unravel the conditions in which prior experience leads to positive performance outcomes and quantify the learning penalties from unrelated institutional experience.

Experience is most broadly conceptualized as an organization’s historical memory of routines (Cyert and March, 1963; Nelson and Winter, 1982; Levitt and March, 1988) that, when retrieved and replicated, improve organizational performance by reducing uncertainty. Organizational benefits derived from accumulated experience are collectively referred to as organizational learning curves (Yelle, 1979; Argote and Epple, 1990; Argote, 1999) or experience-based learning curves (Huber, 1991: 94). Organizations’ prior experience with routinized tasks in a homogenous context is associated with performance improvements derived from learning-curve benefits in settings as diverse as U.S. aircraft manufacturing (Dutton, Thomas, and Butler, 1984), shipbuilding (Argote, Beckman, and Epple, 1990), truck assembly (Epple, Argote, and Devadas, 1991), shift workers (Epple, Argote, and Murphy, 1996), pizza production (Darr, Argote, and Epple, 1995), and cardiovascular surgical procedures (Pisano, Bohmer, and Edmondson, 2001).

In the international context, foreign investment theorists have examined the role of prior experience in organizational learning. The seminal theoretical perspectives established by scholars such as Johanson and Vahlne (1977) and Kogut (1983) suggest that MNCs’ investment capacity depends on the sequencing patterns and deployment of knowledge gained from previous investments. Such experiences of internationalization allow organizations to acquire market-specific knowledge that decreases uncertainty, which is a constraint on learning and is considered a liability of foreignness (Zaheer, 1995), and therefore to invest more successfully both in a country and across successive new countries (Johanson and Vahlne, 1977). Research in the international business literature in the last two decades has demonstrated performance benefits from prior experience learning curves such as subunit survival (Li, 1995; Shaver, Mitchell, and Yeung, 1997) and increases in shareholder value (Berry and Sakakibara, 2008). But the learning effects identified in the extant literature are often confounded between routinized skills being adapted in new host-country environments, learning from the internationalization processes, and learning from the host-country context. Clear distinctions among these differing types of prior experience that MNCs acquire are not well established.

To solve the puzzle of learning effects in the international context, one must first disentangle these confounded aspects of prior experience. The literature suggests that there are three types of prior experiences that effect MNCs’ organizational learning curves. Scholars from one school of thought examine learning from the perspective of a firm’s skills-based capabilities. These studies are focused mainly on the internalization of markets and how the strategic deployment of an MNC’s intangible assets can be a source of competitive advantage (Dunning, 1980; Kogut and Chang, 1991; Morck and Yeung, 1992; Chang, 1995; Caves, 1996; Delios and Beamish, 2001). These skills-based capabilities are representative of intangible assets that include routines like technology transfer, product portfolio management, business model imprinting, brand strategy, property, and plant and equipment planning. This view of learning is focused on how to deploy assets in the right combination to maximize the firm’s value. Chang’s (1995) research, for example, revealed that MNCs deploy their strategic capabilities across their subunits to benefit from prior experiences with learned manufacturing routines in other countries. He found MNCs more likely to sequentially invest in markets in which their capabilities have an advantage over local competitors or are more central to their core businesses.

According to the second school of thought, MNCs learn from competitors’ and their own prior entries into host countries (Mitchell, Shaver, and Yeung, 1994; Shaver, Mitchell, and Yeung, 1997). For example, Li (1995) showed that first-time foreign entrants into the U.S. computer and pharmaceuticals industry are more likely to fail than are repeat entrants. Moreover, Shaver, Mitchell, and Yeung (1997) showed that foreign manufacturing firms entering the U.S. learn through knowledge spillover effects acquired in prior local experiences. These firms are more likely to survive than firms with no U.S. investment experience. Similarly, Barkema, Bell, and Pennings’ (1996) research suggested that MNCs with prior expansions in the same country and that are entering by means of double-layered acculturation entry strategies (e.g., international joint ventures and international acquisitions) are more likely to succeed. Both of these studies, as well as others (Chang, 1995; Berry and Sakakibara, 2008), have measured prior experience as the number of investments in the same host country. More recently, Berry and Sakakibara (2008) also found that MNCs in more-advanced stages of internationalization (i.e., with a larger number of subsidiaries) are valued more by shareholders than those in the initial stage of international expansion. These studies, consistent with interorganizational learning-curve studies in homogeneous environments (Argote, Beckman, and Epple, 1990; Miner and Raghavan, 1999; Pisano, Bohmer, and Edmonson, 2001), demonstrated that learning-curve effects appear as MNCs increase their investment presence in the same host-country environment or with increased international expansion experience, as reflected in the total number of global subsidiaries (Li, 1995; Barkema, Bell, and Pennings, 1996; Shaver, Mitchell, and Yeung, 1997; Berry, 2006; Berry and Sakakibara, 2008). Generalizing the learning-curve effects of repeat investments in a single host country to increased frequency of MNC investment across countries could be misguided, as studies that have examined the internationalization experience across countries has provided less-consistent evidence. Barkema, Bell, and Pennings (1996) found no general learning effects as MNCs increase their level of foreign investments across host environments. Conversely, Chang (1995) revealed patterns in sequential foreign investments suggesting that firms are using their prior experience to inform subsequent host-country choices. This suggests that accounting for the complexities of cross-country variation requires further explanation.

The third view is based on experiential learning derived from knowledge acquired in the host country’s institutional environment. This perspective emphasizes learning from the contextual heterogeneity among institutions (Kogut and Singh, 1988; Barkema, Bell, and Pennings, 1996; Delios and Henisz, 2000). Success in host-country environments hinges on organizational knowledge of institutional dimensions that are likely to affect firm performance. Several studies on institutions and world society have underscored the necessity of understanding institutional variations and the interrelatedness among nations (Hirsch and Lounsbury, 1996; Guillén and Saurez, 2005; Henisz, Zelner, and Guillén, 2005; Dobbin, Simmons, and Garrett, 2007). Recent empirical studies of foreign investment have specified institutions that have a direct effect on firms’ foreign investment strategies. Henisz (2000) found that country-level political hazards directly affect strategic entry choice and local partner selection, and Kogut and Singh (1988) demonstrated the effects of cultural distance on foreign investment entry mode. Henisz and Delios (2004) revealed that political hazards and regime change influence foreign-owned subsidiary failure, Zhao (2006) demonstrated that property-rights protection affects global R&D sourcing strategies, and Siegel and Larson (2008) showed that unfriendly labor market institutions negatively affect manufacturers’ profitability. All these studies found that MNCs strategically navigate the institutional environment to avoid the market uncertainties and expropriation risks their local subunit operations face. The challenge for foreign investment managers is to accurately predict the institutional variations that exist between their home country and the target host country of subsequent investment.

Effectively solving the prior-experience puzzle requires distinguishing between these learning effects and the other types of prior experience, including skills-based experience and internationalization experience from both repeat entries in the same host country and total number of different countries entered. Does a firm benefit more from having multiple investments in the same country or multiple investments across countries with similar institutional environments? Do varying types of institutional experience or the depth of institutional experience matter? Are there differences in the learning-curve effects of institutional experience versus more-routine experiential learning? These are all open questions. To begin to answer them, I empirically examined the entire population of MNC foreign investments in the Brazilian telecommunications industry from 1997 to 2004. By using field studies, interviews with executives and regulators in Brazil, Spain, Portugal, Canada, and the U.S., and a foreign investment database, I develop an experiential learning framework to codify and examine the effects of MNCs’ prior home and host-country experiences on subsequent investment in Brazil.

Prior Experience and the MNC Learning Curve

MNCs’ prior institutional experiences are conceptualized here as the sequential combination of subunit investments that allows firms to create unique knowledge patterns acquired across and within heterogeneous institutional environments. The transition from a domestic to an international, multinational, and transnational organizational form forces firms to learn to efficiently acquire knowledge and adapt to local market environments to survive. The institutional knowledge acquired from prior experiences can be used to reinvest in new subunits in the same country or to transfer knowledge to the home-country organization, or it can be transferred to operations based in other foreign markets. Unlike the skills-based routines derived from intangible assets (Dunning 1980; Kogut and Chang, 1991; Caves, 1996), which are more easily codifiable and transferable (Zander and Kogut, 1995), features of institutional environments are less predictable and observable given the vast variation in practices globally. Similar to skills-based capabilities, which evolve through replication and search, institutional experience can also be a firm-specific resource. A multinational’s knowledge acquired from institutional experiences can evolve into firm-specific competencies that become a source of experience-based capabilities of the firm. Firms that are more adept at retaining and transferring knowledge from their institutional experiences across subunit organizations can find these capabilities to be a source of competitive advantage. This reframing of experience focuses more keenly on the active role the organization plays in learning from the environment.

Institutional Similarity

Each institutional experience can be thought of as a type of knowledge the organization acquires across a range of institutional environments. In a host country, the institutional environment includes multiple dimensions from which an organization learns. For example, dimensions of formal government regulation include the statutory laws of the competitive market structure, entry barriers, and industry standards, as well as the regulators’ power to influence the market or the stability of the regulatory governance structure. Akin to these are the widely explored informal institutional dimensions of culture, including individualism versus collectivism, masculinity versus femininity, power distance, etc. (Hofstede, 1980). As a firm’s investment portfolio expands into new countries, the scope of experiential knowledge types likely broadens.

Experiential learning studies in the international business and strategy literatures have predicted that familiarity with relevant dimensions of the institutional environment leads to subsequent success in similar types of environments. Delios and Henisz (2003) found that firms with more experience in countries with high political hazards are less sensitive to such hazards in their subsequent foreign entries. Barkema, Bell, and Pennings (1996) used cultural distance to demonstrate that MNCs learn from host-country institutional environments through the stages of internationalization. They found that a foreign subunit’s longevity is associated with cultural similarity between the MNC’s home country and the targeted host country. Therefore logic suggests that the cumulative experiences of MNCs in institutional environments similar to those of the target host country should outperform MNCs without similar experience. Related institutional experiences afford firms a more precise ability to predict and mitigate new institutional conditions. Firms with similar experience also have an advantage in understanding the context of business codes, regulatory rules, and practices, resulting in more efficient and effective strategic decision making. Thus it is reasonable to expect that firms with acquired experience from similar institutional environments will be more likely to succeed:

But not all types of knowledge acquired from multiunit organizations’ experiences are relevant when transferred between subunits. Although recent organizational learning studies have demonstrated that similarity between prior and current experience has positive effects on performance, learning discounts also exist. For example, through SIC code matching, Haleblian and Finkelstein (1999) found that acquisition success is highly correlated with similar prior acquisition experience in the same industry, but acquiring firms are more prone to fail when new acquisition partners have dissimilar types of acquiring experience. Likewise, Ingram and Baum (1997) found that Manhattan hotel chains with nonlocal experience were more likely to fail despite the benefits gained from hotel chain affiliation. These findings are consistent with the international business “liability of foreignness” theory (Zaheer and Mosakowski, 1997), which suggests that failure risks increase with dissimilarity between foreign and host countries’ institutional environments. Without relevant experience, firms are more likely to grossly misestimate the effect of the institutional environment on their business operations until they have better knowledge of it. This “learning penalty” can accelerate the time to failure because inappropriate knowledge from dissimilar contexts is applied. Thus I hypothesize:

Learning from Breadth of Institutional Experience

The debate in the literature remains open as to whether variability in experience has positive implications for a firm’s performance and whether the outcomes are significantly different from repeatedly exploiting existing knowledge. Some international business studies (Erramilli, 1991; Chang, 1995; Delios and Henisz, 2003) on sequential foreign investment entry have found that similarities in entry can fuel future entries of the same type. Chang (1995), for example, examined sequential foreign investment entries of Japanese firms into the U.S. market and found evidence that learning from early entries into core businesses enabled firms to launch future entries in more-risky noncore businesses with less experience. In Erramalli’s (1991) investigation of the foreign investment entry behaviors of U.S. service firms, initial patterns of international expansion were most evident in similar cultural environments. As organizations gained experience with investing abroad, they became increasingly likely to choose less-similar markets. These empirical studies confirmed Davidson’s (1980) theoretical view that inexperienced MNCs are likely to select foreign investment locations that are more similar to those of their host country than firms with a broader range of investments. Organizational learning theories of repetitive momentum (March, 1991; Amburgey and Miner, 1992) also predicted that organizations are more likely to repeat routines with which they are familiar. If the predictions of the extant literature prevail, a logical performance implication is that firms will reap the greatest benefits from reinvesting repeatedly in the same host-country institutional environment. This strategy is bounded, however, as investment opportunities diminish in a host country over time, and there will always be variations at the country level. As MNCs internationalize, the range in the types of experience acquired is likely to expand their knowledge base. Expansion into institutional environments that vary significantly from the home-country institutions increases the learning barriers for multinational organizations but also possibly offers greater rewards.

Cyert and March (1963) anchored the learning argument with a more expansive view by asserting that more learning experiences lead to more possible combinations and a broader range of future choices. Applying this logic to an MNC’s cumulative breadth of prior institutional experiences yields a reasonable rationale that organizations that expand into new and uncertain markets have the advantage of a greater knowledge pool. Firms potentially gain more from these difficult learning environments, particularly in emerging market economies, which typically have more-volatile and weaker institutions. Further, MNCs that possess greater variation in knowledge-retrieval sources are likely to benefit from generating a greater number of combinative experiences to leverage in future subunit investments. In another context, Beckman and Haunschild (2002) showed that heterogeneity in the interorganizational network structures of acquisition partners leads to better performance outcomes. Pennings, Barkema, and Douma (1994) provided evidence that firms successful in diversification have persistent success with subsequent firm expansions. This suggests that organizations assuming greater risks in investing in varying types of host-country institutional environments should reap benefits derived from their breadth of knowledge.

Experience-based Capabilities

The inherent heterogeneity of country-specific institutional dimensions creates a challenge for firms to identify and build in-depth capabilities across each type of institutional experience over time. Kogut and Zander (1992) argued that the creation of new knowledge stems from the recombination of existing capabilities. These recombination opportunities exist for MNCs learning from their experience in a host-country environment and their ability to recombine it appropriately to be relevant to a subsequent host-country environment. Organizational routines developed by replicating prior institutional experience of the same type are what I refer to as experience-based capabilities. Because recombination is needed, developing experience-based capabilities differs from replicating the entire set of host-country routines that would be required of repeat investments in the same country. In this case, firms are parsing out a specific institutional dimension that has relevance in another country and combining it with an experience from yet another country. For example, regulatory market structure rules for telecommunications are similar in Brazil, Israel, and New Zealand. If an MNC acquired experience-based capabilities while navigating the regulatory market structure in any of these countries, the specific capability could be used in another market and be recombined with another experience-based capability that fit the subsequent institutional environment. Organizations capable of building more in-depth capabilities in specific institutional dimensions (i.e., regulatory strategies to navigate entry barriers or political strategies to mitigate political hazards) can then uniquely combine prior experiences to replicate any institutional environment, provided the firm has prior experience of that type. Kogut and Zander (1992) suggested that organizations with strong combinative capabilities are able to generate new knowledge and seek out market opportunities more readily.

Achieving a balance in exploiting existing types of learning capabilities while exploring new dimensions of the institutional environment allows MNCs to maximize the benefits of existing knowledge. Firms that stage the sequence of foreign subunit investments across countries that overlap with their existing knowledge are also likely to experience learning-curve effects comparable to the learning rates achieved by having repeat investments in the same host country. Both represent a depth of relevant types of knowledge—one combined in the host country, the other recombined across host countries. Thus I hypothesize:

Methods

Sample and Data Collection

The empirical setting I examined was the entire population of foreign subunit investments in the Brazilian telecommunications industry from 1997 to 2004 following market privatization and liberalization. This setting is ideal for empirical investigation for several reasons. First, MNCs face considerable complexity and heterogeneity in environmental contexts (Ghoshal and Westney, 2005) as they internationalize. Second, the global telecommunications industry, rife with government interventions and regulation, provides codifiable “rules of the game” to measure learning constraints. Because of the tractable nature of government regulations and the fact that firms’ compliance is compulsory, reasonable inferences can be made about organizational learning in this setting. Last, Brazil’s economy, representative of many emerging market economies, is known for an exceedingly difficult institutional landscape to navigate because of strong development dependencies between the government and industry (Evans, 1979; Schneider, 2008; Schneider, 2009) and other non–market factors (i.e., weak rule of law, weak investor protections, and high ownership concentration) (Musacchio, 2008: 7). This setting provides a valid reference point for gauging firms’ abilities to navigate institutional differences.

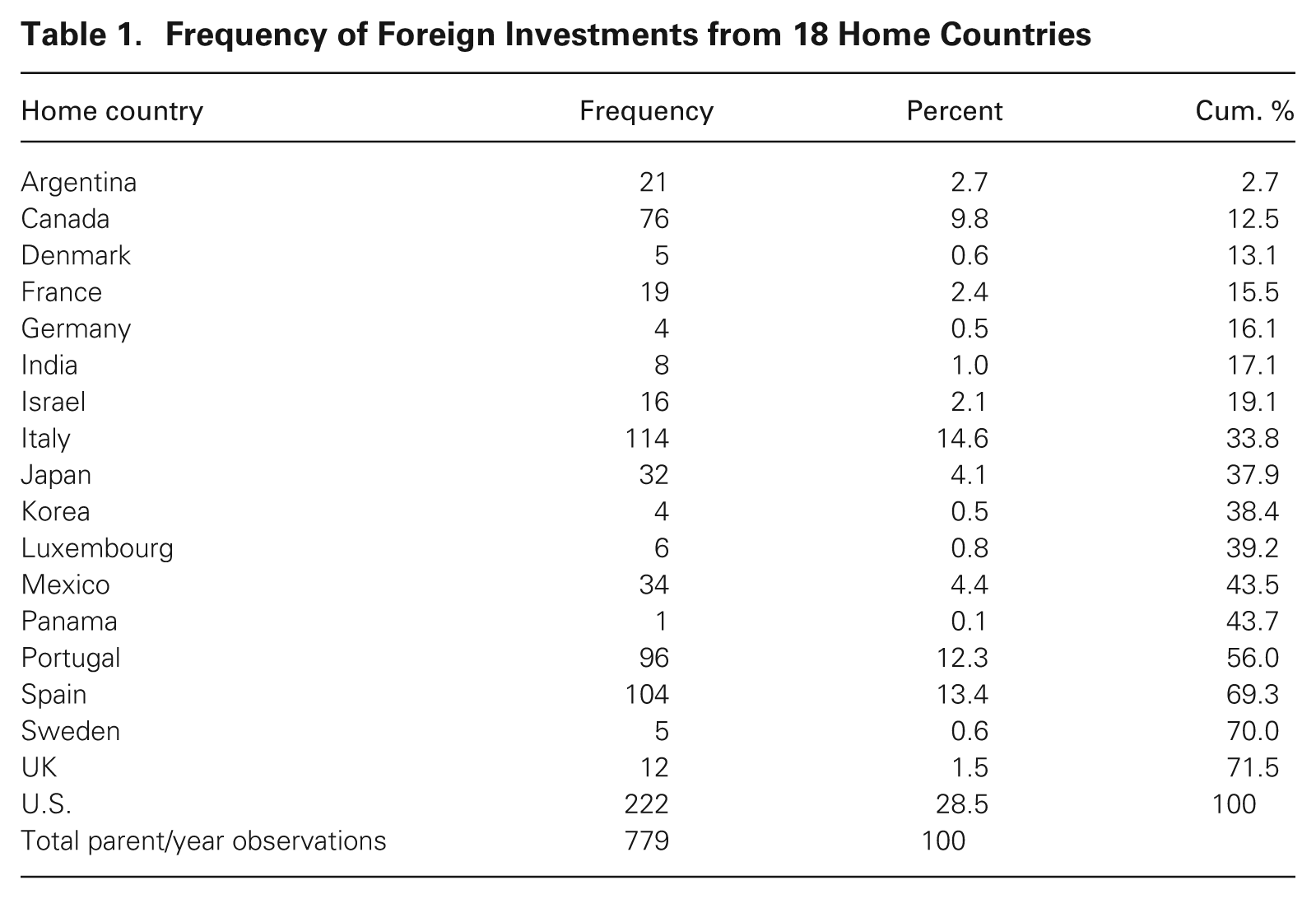

There were 110 firms providing telecommunications services in Brazil in Standard Industrial Classification (SIC) codes 4812—wireless; 4813—fixed; 4822—messaging; and 4899—misc. and satellite. Ninety-six of the 110 telecommunications firms were foreign-held subunits with equity participation through joint ventures or wholly owned subsidiaries. The average ownership stake of these foreign firms was 54 percent. Subsidiaries ranged in size from R$225,000 to R$13,308,630 annually. 1 The subunit firms were owned by 66 parent firms from 18 host countries, broadly ranging from developed countries (e.g., U.S., UK) and emerging markets (e.g., South Korea, Mexico), with an average of eight prior foreign experiences spanning 80 countries in total. Table 1 presents the frequency of parent firms’ investments by host country. These subsidiary data were disaggregated at the firm/parent/year level of analysis in order to capture the time-varying experience effects of each parent firm. This generated 1,193 observations. I dropped 414 firm/parent/year observations, 348 of which were observations of domestic equity participation, including both joint venture participation and totally domestically owned subsidiaries, and 60 were observations with no telecommunications participation (e.g., investment banks). Three observations were duplicates because of multiple entries in less than one year, and five were observations of exits that were not failures (Headd, 2003). 2 The remaining 779 firm/parent/year observations were used for empirical examination.

Frequency of Foreign Investments from 18 Home Countries

I constructed this dataset by using a broad selection of data collection and triangulation techniques, including several firsthand data sources in Brazil—Conselho Administrativo de Defensa Economica (CADE), BNDES (Development Bank of Brazil), ANATEL (the Brazilian telecommunications regulatory agency), and Comissão de Valores Mobiliários (CVM), Brazil’s securities and exchange commission. Secondary archival data sources included ISI Emerging Markets, Espicom Business Intelligence, BuddeComm Telecommunications Reports, and Dunn & Bradstreet Million Dollar, Hoover’s, Gale, and Orbis databases. I used other publicly available periodicals acquired through Factiva, company reports, and press releases to validate each subunit’s entire event history and subsidiary locations for its parent’s prior experience. I augmented these data with interview data from 30 telecommunications and regulatory agency senior executives, who recounted market events.

Dependent Variable

I analyzed the time to failure event, a firm’s exit from Brazil, at the firm/parent/year level, where firm survival in period t was (0) or failure was (1). Defining failure can be problematic in event history studies because some market entries are not designed for longevity (e.g., organizational learning) (Nakamura, Shaver, and Yeung, 1996), and some market exits are not the result of organizational failure (e.g., capital gains) (Headd, 2003). Therefore I examined each exit to determine the reason for it. I limited failures to exits driven by financial underperformance in earnings projections, difficulty securing capital to continue the investment, lack of understanding of local institutions, or related situations. Three independent coders tested the reliability of the assessment of failure cases. Interrater reliability was 100 percent in all cases.

Independent Variables

Regulatory distance

A distinct challenge of this research was to develop an approach that precisely measured the differences in institutional environments across nations and captured MNCs’ prior experiences in all host nations before entry into Brazil, the subsequent target host country. Although scholars have studied selected dimensions of international institutions such as political hazards (Henisz, 2000), intellectual property rights (Zhao, 2006), legal origins (La Porta et al., 1998), labor laws (Siegel and Larson, 2008), and cultural distance (Hofstede, 1980; Schwartz, 1994), little is known about the effects of formal regulation on foreign subunit performance. I examined these effects by developing a methodology to create regulatory distance measures precisely characterizing the telecommunications industry regulatory context in 80 countries. On the basis of analysis of 131 regulatory agencies, I deduced that industry regulation is a function of six institutional dimensions that explained 78 percent of the variation among 28 key comparative regulatory measures, such as practices in the regulation of prices and market structure, the duration of licensing, the regulation of standards and subsidies to specific consumer groups, the term limitations of regulators, and so forth. I used confirmatory factor analytic techniques to validate the six theorized regulatory dimensions, which include (1) key aspects of statutory laws related to the regulatory competitive market structure (e.g., pricing, territorial assignments, technology utilization, asset sharing), (2) regulatory standards (e.g., quality standards, safety guidelines) and (3) regulatory entry barriers (e.g., foreign ownership limitations, WTO compliance requirements), two additional dimensions related to the regulators’ political power— (4) regulatory political competition and (5) regulatory governance structure, which capture the terms under which regulators came into office and their authority to provide public goods—and a final dimension, (6) regulatory stability, which captures the effectiveness of the institutions’ organizational form. 3 This dimension includes factors related to how the institution was established, such as funding, jurisdictional coverage, autonomy from state-owned enterprises, number of regulatory agencies, and frequency of reforms. These six dimensions of industry regulation are arguably the knowledge gaps of highest risk for MNCs entering highly regulated services-oriented industries such as telecoms, energy, mining, banking, and insurance. Firms that are not as dependent on government regulation are less constrained by institutional knowledge of this sort (e.g., consumer products, durables such as automotive products). Online Appendix A (http://asq.sagepub.com/supplemental) details the 28 measures across these six dimensions of regulation; Online Appendix B provides more details on the regulatory framework used to compare countries, and Appendix C provides more details on the coding of regulatory scores and methodology for constructing the dimensions.

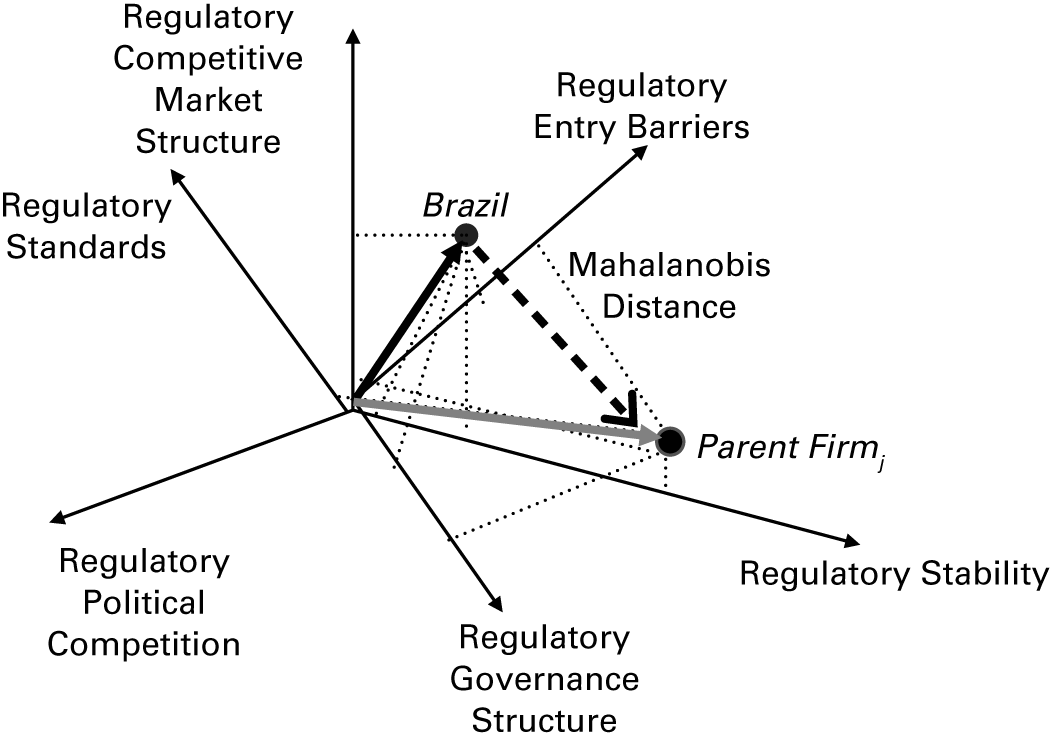

To construct a similarity measure for each organization’s prior regulatory experience, I used these six dimensions of industry regulation to calculate the distance between a firm’s home and prior host-country regulatory experiences versus that of Brazil’s regulatory environment by using a Mahalanobis distance measure. First, regulatory distance (di ) is captured by measuring the level of similarity between each country, j, and that of the reference country, Brazil. 4 Each country’s regulatory dimensions are captured in the column vector Xj such that

and the target country’s dimensions are captured in the vector Yj such that

Online Appendix D presents regulatory dimensional scores for all 80 countries. A Mahalanobis measurement technique was specified instead of a Euclidian distance because of the non-orthogonal relationships between the six regulatory dimensions (see Online Appendix E for a detailed review of Mahalanobis distance). For instance, a country’s regulatory laws are not completely independent of the government’s ability to enforce the laws through sanctions that typically come from the formal regulatory institutional structures. The Mahalanobis specification adds robustness by taking into account the means across countries and accounts for the variances and covariances within each dimension of regulation in the inverse covariance matrix S-1(6x6). The calculation captures the squared distance

The regulatory distance scores between Brazil and other countries are presented in Online Appendix F.

This regulatory distance, dj

, is piled up across each country such that

where i = 1, 2, …, k and k is the number of firms, j = 1, 2, …, n and n is the number of countries, one (1) equals headquarters or subunit investment presence, and zero (0) means no investment presence of firm i in country j. The portfolio was updated annually to include any new subunits acquired globally during the time of this study. To determine a firm’s overall regulatory distance score relative to Brazil, I multiplied the P

(kxn)

matrix by the D(n

x1)

vector. Using the following weights, w, Regulatory

where h = home country and j = all other countries with prior experience, and the

Mahalanobis distance of regulation.

I used three weighting approaches, described below, to capture the home-country effects, host-country effects, and combined regulatory effects.

Home-country effects

A multinational’s home-country experiences represent the organization’s inherited knowledge of the business practices and norms existing since the organization’s inception (Huber, 1991). Inherited knowledge contains the knowledge of the initial organizational environment as established by the organization’s creators and passed on to the organization. These inherited routines are especially important for foreign investment managers who originate from the headquarters location, as the goals, approach, and culture of organizations are greatly shaped by their founders (Stinchcombe, 1965). Multinationals’ home-country knowledge imprint has a stronger proportional effect on a firm’s performance than subsequently acquired host-country knowledge because of the prevailing institutional practices of the organization and the internal pressures to maintain the legitimacy of the MNC in the context of a foreign host (Meyer and Rowan, 1977). Most scholars in the foreign investment research tradition (Kogut and Singh, 1988; Erramilli, 1991; Benito and Gripsrud, 1992; Barkema, Bell, and Pennings, 1996) have used solely home country of origin to measure proximity to the target country. Home-country knowledge effects are represented by using the above regulatory distance measure for each firm, where wi,h

= 1 and wi,j

= 0

Host-country effects

Firms’ decisions to enter a country are largely based on congenital knowledge (Huber, 1991: 91), which is a combination of both inherited knowledge from the organization’s foundation and other information the firm acquires prior to the birth of a new organization. For multinationals, new organization events are subunit investments in host countries. The other sources of information include acquired knowledge from MNCs’ prior experiences in institutional environments globally. In Huber’s (1991) knowledge acquisition framing, organizations rely on congenital knowledge for information retrieval to assist future decision making about which countries to invest in, what inherent capabilities the firm will deploy relative to market needs, and what resources will be needed in the targeted country’s institutional environment. To capture congenital knowledge, regulatory distance is weighted (wij) to include the entire set of host countries a firm has previously entered, with all host-country investments weighted equally. In this case, the weight wi,h = 0 and

Combined experience effects

An MNC’s intraorganizational knowledge flows bidirectionally between the home and host countries. Frequently, knowledge is transferred in these firms through the movement of managers from one subunit location to another (Almeida and Kogut, 1999; executive interviews). To model this assumption prudently, both the inherited knowledge of the home country and congenital knowledge of the host-country experiences are weighted equally in the regulatory distance calculation, where wi,h = 0.5 and

Admittedly, using a distance measure that aggregates experiences presents challenges in interpreting the influence of firms’ overall experiences. Firms that have multiple foreign investment experiences that might be both similar and dissimilar to the investment in Brazil can potentially be underspecified by examining the mean experience overall. Thus a downward bias exists for firms with broad variations in foreign investment experience. To account for this bias and provide more accurate depictions of each firm’s experience at the extremities, I created a measure of minimum distance for more empirical precision. Moreover, because the squared distance term in the Mahalanobis calculation provided only a positive measure of distance, I also developed a measure, sign of regulatory distance, to capture the directional effects from either stronger (scores higher than Brazil’s) or weaker (scores lower than Brazil’s) industry regulation. For example, comparing Germany and Romania, both of which appear to have comparable regulatory distances to Brazil, 20.9 and 16.5, respectively, the actual regulatory environment in Germany is more stable (standardized regulatory score of 28.0) than Romania’s (standardized regulatory score of −9.26). This variable helps distinguish between the two differing environments.

Breadth

Breadth of experience measures the amount of dispersion according to types of host-country regulatory experience prior to entering Brazil (t < 1998). I used a coefficient of variance approach (Martin and Gray, 1971: 496; Beckman and Haunschild, 2002) to measure heterogeneity of experience because it adequately focused on the central tendency of dispersion in experience rather than on the simple standard deviation. This relative measure of breadth is preferable to a standard variance term for isolating the range of experiences independent of the number of countries a firm has entered. The coefficient of variance is

where d represents the dispersion of host-country regulatory experiences, and N represents the number of countries of prior experience. I used standardized regulatory scores (see Online Appendix F) to compute the dispersion in types of regulation across all home and host-country regulatory environments. This time-varying measure is updated annually to include new host-country subunit entries.

Depth

To test hypothesis 3, I developed a depth measure of the frequency of each of the six regulatory dimensions summed across countries that exactly matched (± .1 of the regulatory dimensional scores) the regulatory environment in Brazil. Firm scores were based on the fraction of replication of Brazil’s regulatory environment (100 percent redundancy = 1) and the depth within each of the replicated dimensions (1/6 for each replicated dimension). For example, America Movil’s prior regulatory experience in 1998 included Spain, Mexico, and Argentina, which combined, replicated five of the six (.83) regulatory dimensions in Brazil. Conservative estimations were used to add fractional redundancies of the same type only after all six dimensions were replicated. Depth scores ranged from 0 (e.g., SK Telecom, 1998) to 2.5 (e.g., Telefonica, 2004).

Control Variables

Host-country experience and internationalization experience

To first replicate the predicted theory and findings of the conventional wisdom on MNC experience, I developed two variables. Host-country prior experience captures the number of subsidiary investments in Brazil. This count variable replicates the methodology used in the existing literature on foreign investment (Barkema, Bell, and Pennings, 1996), which suggests that a firm’s own experience in a host-country affects performance. The second variable, internationalization experience, measures the number of foreign host countries each multinational has entered prior to entering Brazil.

Skills-based capabilities

In the telecom industry, network operators’ (e.g., AT&T’s, Nextel’s, Sprint’s) business units are organizations based on highly routinized skills-based capabilities. The industry terminology for the highly transferable, codifiable business models is the “organizational imprint,” which includes technology platforms, exclusive supplier contracts, and global manufacturing agreements, for example. Such skills-based capabilities in telecommunications are conveniently segmented by four, 4-digit SIC codes: 4812—fixed, 4813—wireless, 4822—messaging service, and 4899—satellite services. I developed fixed-effects indicator variables for the firm’s primary SIC code. I obtained data from the Dunn & Bradstreet Million Dollar database.

Skills-based prior experience

Like prior internationalization experiences, I quantified the number of each firm’s skills-based experiences in previous home and host-country investments. Previous studies have typically confounded these two types of experience (frequency of country experience versus frequency of routine organizational imprinting). I used country-level 4-digit SIC code matching (Hayward, 2002), collecting data for each company from a variety of sources (primarily Dunn & Bradstreet Million Dollar database, Compustat, Orbis, Factiva, Gale, and Buddecom telecom reports). On average, parent firms had four preexisting investments in the same SIC code. This time-varying measure is reported annually.

Institutional controls

Similar to Siegel, Licht, and Schwartz (2011), I included several institutional comparative measures in the analysis to rule out alternative explanations. I used Hofstede’s (1980) cultural dimensions (power distance—PDI, collectivism versus individualism—IDV, femininity versus masculinity—MAS, and uncertainty avoidance—UAI) to calculate cultural distance, replicating the methodology used by Kogut and Singh (1988: 422). 5 Differing from their study, Brazil was the reference point, not the U.S. I also used the POLCON V data (for the year 1998) (Henisz, 2000) to develop a political-hazards institutional distance measure for each home country versus Brazil. This variable, POLCON distance, along with the subsequent two measures, used a Euclidian distance formulation. 6 I also computed La Porta et al.’s (1998) legal origin measure as a distance measure to control for institutional variations in legal structures of each parent firm’s home country. I categorically scaled the variable from the weakest to the strongest legal protections (1 = French civil law; 2 = Scandinavian civil law; 3 = German civil law; and 4 = common law). 7 I constructed a language distance variable by using Grimes’ (1992) language family trees to measure a country’s level of closeness in language to Portuguese, the official language of Brazil. For example, a code of 1 represents other sibling-related countries in which Portuguese is also the official language (e.g., Portugal); 2 represents other Ibero-Romance languages (e.g., Spanish and French); 3 represents Gallo Romance languages (e.g., Italian); 4 represents other Indo-European languages (e.g., English, German), and so on. For each of these institutional controls, the distance measures represent the gap between each firm’s home country and Brazil.

Firm controls

Firm size is a time-varying covariate based on annual sales revenue (log) at the subunit level. Data come from the Comissão de Valores Mobiliários and company annual reports. Nominal revenue numbers were adjusted to real on the basis of the CPI (Índice nacional de Preços ao Consumidor Amplo—IPCA) for telecoms provided by the Instituto Brasileiro de Geografia e Estatística. Subunit telecom market share (percentage of total Brazil telecom revenues) was also included to control for the firm’s size relative to the overall telecom market size. Because observations of failure were coded at the firm/parent/year level, it was important to capture the percent equity ownership of each parent in a subunit firm. Ownership percentage is a meaningful indicator of control rights. I also included an indicator variable of whether the subsidiary was affiliated with a business group (0/1), as previous studies have revealed that business group affiliations can affect firm performance (Khanna and Rivkin, 2001; Chang, 2003; Khanna and Thomas, 2009).

I collected additional time-varying firm performance measures germane to the telecom industry, including (annually) ARPUs (average revenue per subscriber) in reais, number of subscribers, number of employees, and purchase price. But missing data was an issue in up to 60 percent of the cases, so these variables were not included in the main analysis to preserve the sample size.

Auction and industry controls

A variable geographic region was constructed to measure the territorial effects of firms’ jurisdiction of licensure in Brazil (e.g., São Paulo, Rio de Janeiro, etc.). This categorical variable ranked the regions on the basis of the telecom regulator’s (ANATEL’s) population count and projected subscriber base. An indicator variable, auction FDI restrict, coded foreign subunits that participated in the first privatization licensing auction in Brazil. Of the nine privatization auctions, only the first imposed foreign investment ownership restrictions and local consortium partnerships on entrants, a market imperfection that may have been cause for exit (Kogut, 1983). A fixed-effects specification with indicator variables for each auction produced similar results. Relative industry size (annual total telecommunications industry revenues in home country / total telecommunications revenues in Brazil) was included to capture home-country market attractiveness relative to Brazil. Firms from smaller telecommunications markets may find Brazil most attractive. Conversely, firms from larger telecom markets are at an advantage in dealing with competition. Hill and Thomas (2005) showed that asset bubbles fueled by external social factors were correlated with the relative position of firms in the industry. Through the lens of another important global utilities industry (electricity), they posited that firm performance is negatively correlated with the firm’s entry sequence. In an asset bubble, significant overinvestment is most likely to occur at the most distant points in the information cascade. To control for this alternative explanation, I developed an asset bubble variable, entry order, to capture the sequential entry number of firms entering the telecommunications industry in Brazil.

Robustness

For robustness, I disaggregated Hofstede’s (1980) dimensions of culture and tested each dimension separately to address the measurement criticisms of dimensional aggregation and lack of generalizability to national culture, given that these data were derived from a single multinational corporation (IBM) (Shenkar, 2001). Alternatively, I used Schwartz’s (1994) one-dimensional egalitarianism measure, which has known effects on international investment flows (Siegel, Licht, and Schwartz, 2011). Political capital and other institutional knowledge of the “rules of the game” can be lost through exogenous shocks such as regime changes (Siegel, 2007) and governmental reforms (Henisz and Delios, 2004). I used regime-change indicator variables to capture presidential regime changes—Fernando Henrique Cardoso (1995–2002) versus Luiz Inacio Lula da Silva (2003–2010). The president of Brazil appoints the ANATEL commissioners and the minister of communications in Brazil. I included additional regime-change indicator variables for shifts at the ministerial level. During this period of the study, there were five ministers of communications in Brazil (Sergio Motta, Luiz Carlos Mendonça de Barros, João Pimenta da Veiga Filho, Juarez Martinho Quadros do Nascimento, and Miro Teixeira).

Empirical Model

A log-logistic parametric duration-dependence model was specified to both accommodate the time-varying covariates and account for the liability of adolescence and life-cycle-oriented factors of these new subunit organizations (Carroll and Huo, 1986; Hannan and Freeman, 1989; Brüderl and Schüssler, 1990). I confirmed the expected nonmonotonic distribution (i.e., inverted-U shape) using nonparametric estimates to determine the appropriateness of fit of a log-logistic form. A time-to-fail event, exit, was predicted by

at a given point in time t for every subunit/parent firm observation i. The covariates were parameterized in λ so that the functional form fit the expectation that the covariates positively or negatively affected the baseline survival rate, a convenient feature of the accelerated failure time (AFT) models. A concern that requires attention when using survival models is both left and right censoring. The majority of subunit entries (more than 80 percent) occurred in the first two years of market privatization, which alleviated concerns of left censoring. In the periods prior to this study, the telecom industry was 100 percent state owned and operated by Telebras. Right censoring is an obstacle in interpreting the outcome of foreign subunits that are between states of success and failure. The AFT model specification allows for greater emphasis on predictions of the organizations’ time to fail beyond the life of this study. It is also worth noting that counterintuitive to proportional hazard rate models (i.e., Gompertz and Weibull), AFT coefficient interpretation is consistent with the direction of the sign. That means a positive and significant coefficient translates into a deceleration in time to fail with each unit increase; negative coefficients accelerate time to failure.

Results

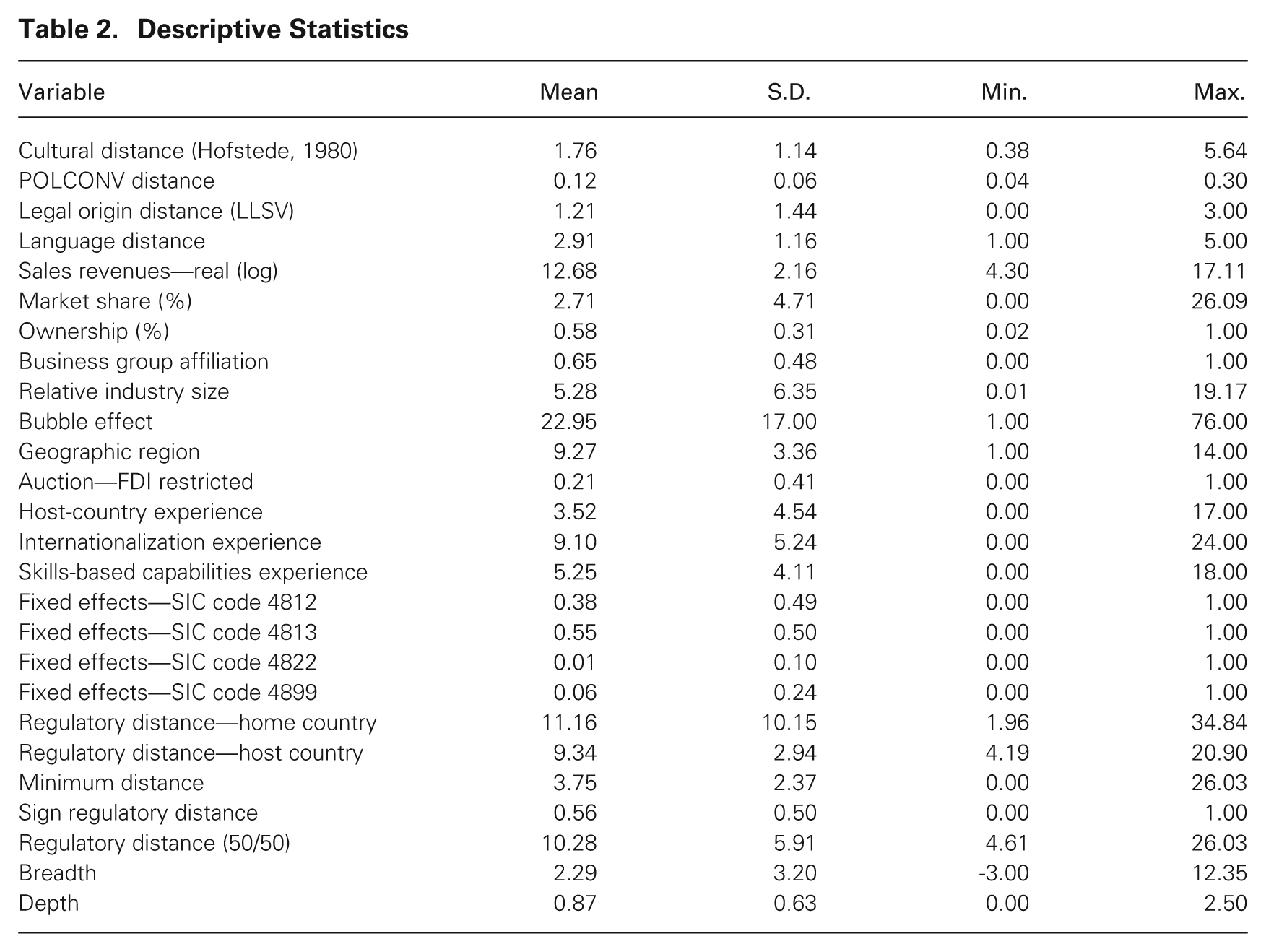

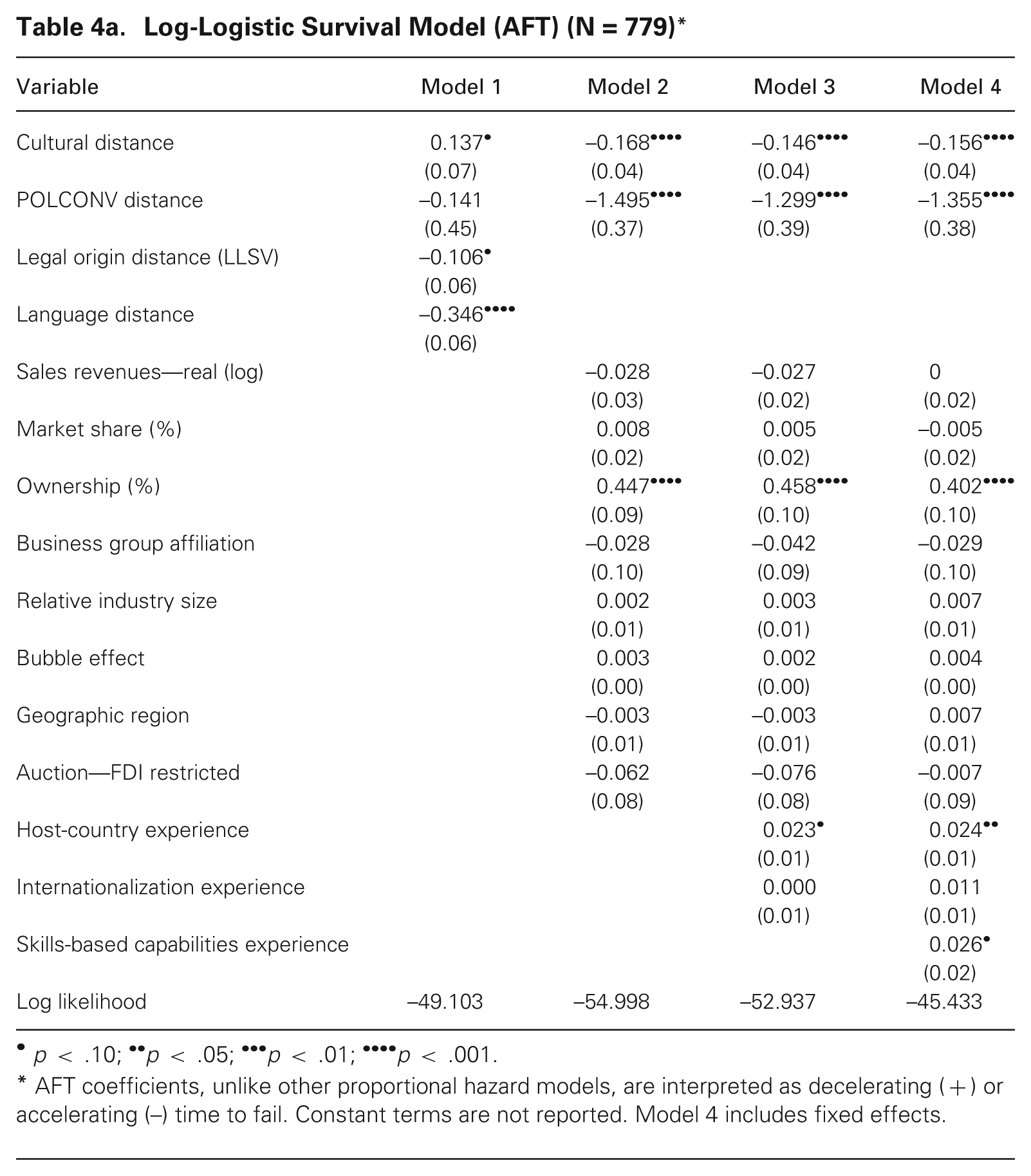

Tables 2 and 3 provide descriptive statistics for all variables and a correlation matrix for variables included in the analysis. On average, MNCs’ prior host-country regulatory experiences (mean = 9.3) are more proximate to the regulatory environment in Brazil than to their home countries (mean = 11.2). Table 3 reveals multicollinearity issues (indicated by correlations > .80) between the institutional control variables of culture distance, legal origin distance, and language distance, at .84, .85, and .83, respectively. This is consistent with the extant literature, which revealed that cultural distance and language factors are nonorthogonal (Shenkar, 2001). Classic multicollinearity problems arose, such as erratic coefficient signs and inconsistency in significance (Greene, 2000: 256), when these institutional variables were included together in model 1, table 4a, which summarizes the survival model results. Using multicollinearity confirmatory techniques, principal component (Greene, 2000: 258) and factor analysis demonstrated that these five institutional measures all load on one factor. Further multicollinearity tests were used. Variance inflation factor (VIF) results over 2.5 also suggest problems and that these variables be eliminated (Allison, 1999). In subsequent models, language distance and legal origin distance, with VIF scores of 3.4 and 3.3, respectively, were removed to alleviate concerns of redundancy and multicollinearity.

Descriptive Statistics

Correlation Matrix for Variables Included in the Analysis

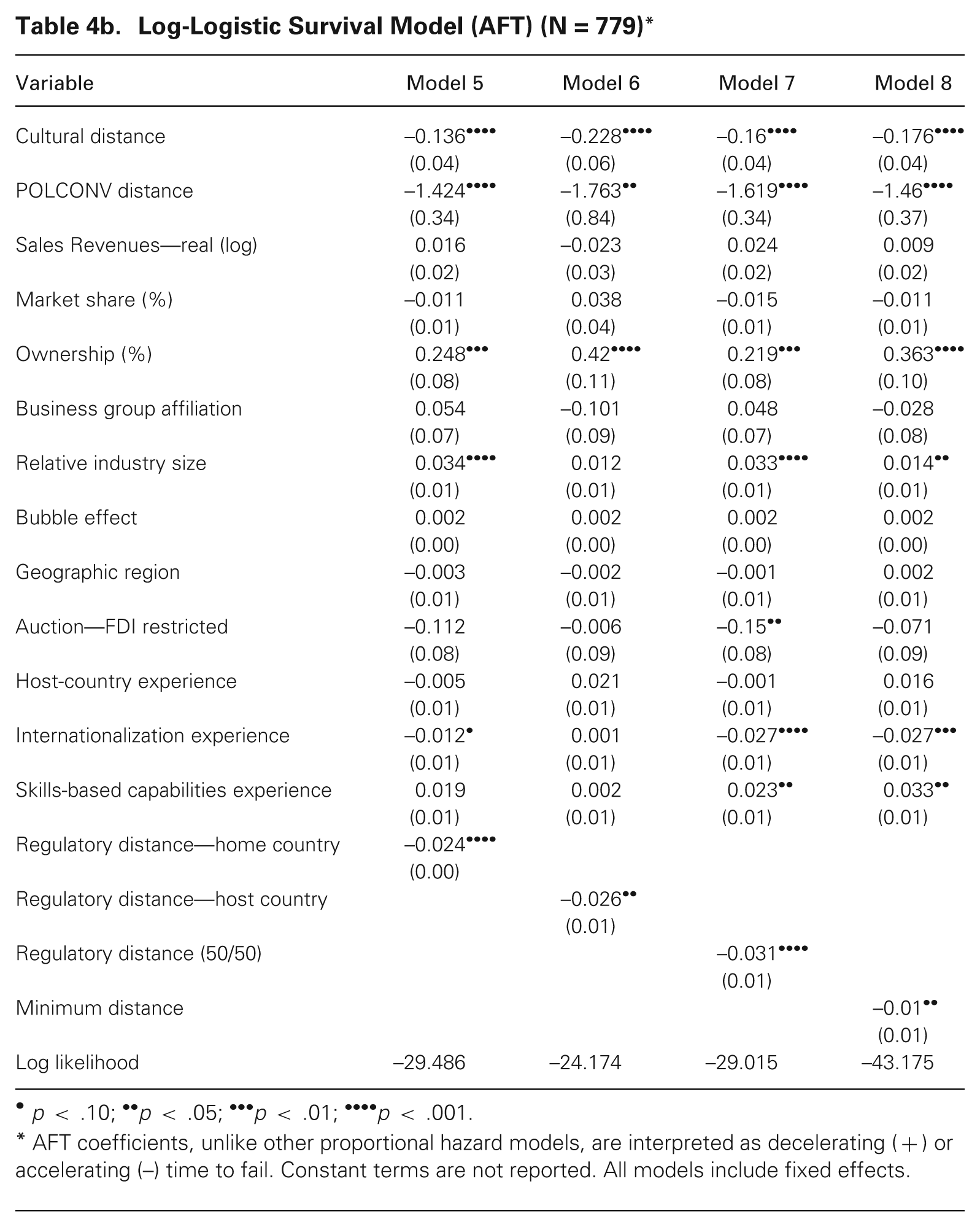

Log-Logistic Survival Model (AFT) (N = 779)*

p < .10; •• p < .05; ••• p < .01; •••• p < .001.

AFT coefficients, unlike other proportional hazard models, are interpreted as decelerating (+) or accelerating (–) time to fail. Constant terms are not reported. Model 4 includes fixed effects.

Log-Logistic Survival Model (AFT) (N = 779)*

p < .10; •• p < .05; ••• p < .01; •••• p < .001.

AFT coefficients, unlike other proportional hazard models, are interpreted as decelerating (+) or accelerating (–) time to fail. Constant terms are not reported. All models include fixed effects.

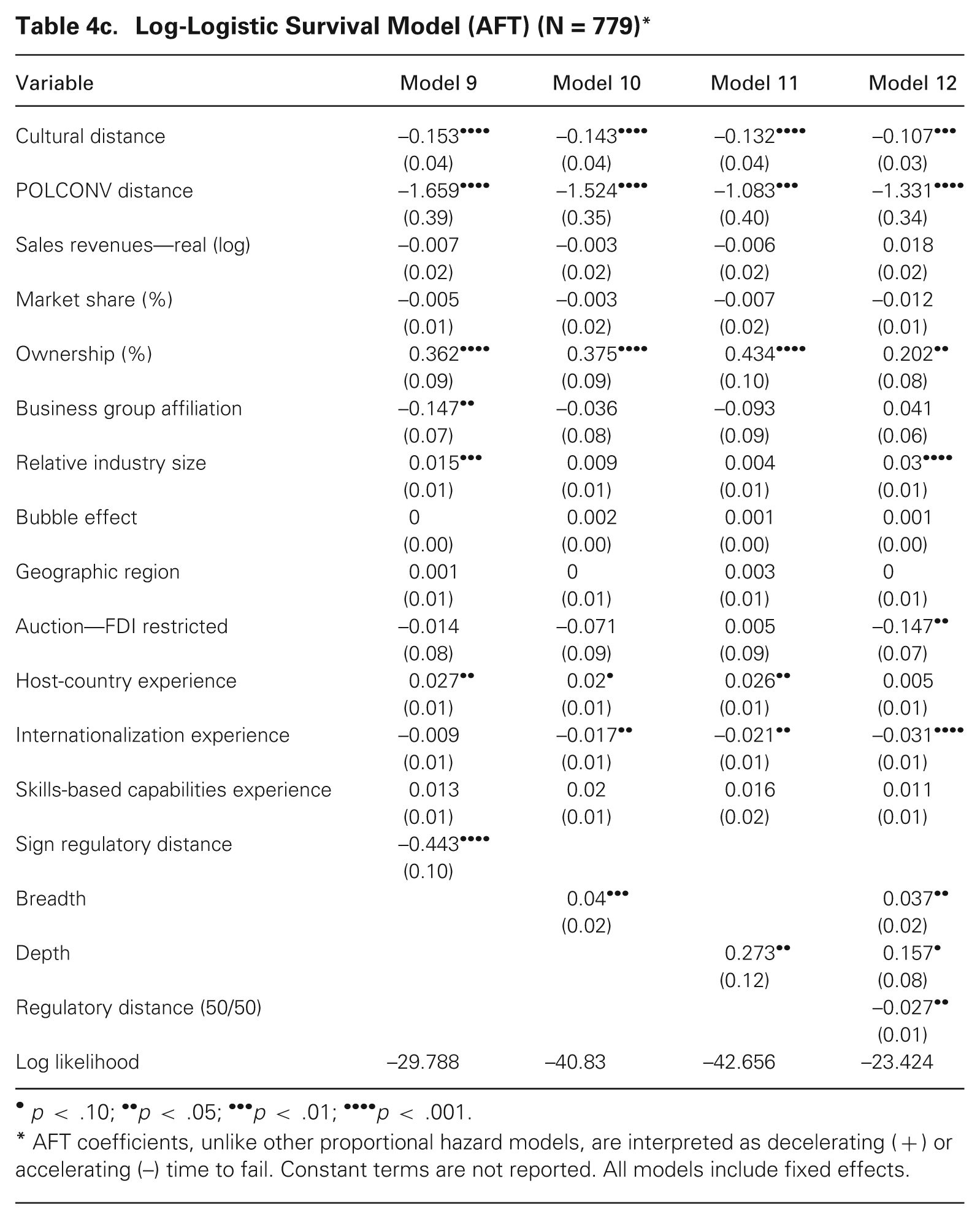

Log-Logistic Survival Model (AFT) (N = 779)*

p < .10; •• p < .05; ••• p < .01; •••• p < .001.

AFT coefficients, unlike other proportional hazard models, are interpreted as decelerating (+) or accelerating (–) time to fail. Constant terms are not reported. All models include fixed effects.

Model 2 first examines the statistical significance and relevance of institutional-, firm-, industry-, and auction-specific controls. All the included institutional distance variables (i.e., culture distance and political hazards distance) consistently are associated with an increase in time to failure, which is consistent with the predicted directional effect in the extant literature. Many of the firm-level, industry-level, and auction controls were not significant, but two demonstrated relatively consistent significance throughout. Both percentage ownership and relative industry size in proportion to the home-country telecommunications market significantly increase survival times. Though many studies have shown firm size is a significant predictor of success, I found that the parent firm’s equity participation in the subunit firm is a more important factor, as dominant equity owners (percentage ownership) survive longer. The entry order variable, a proxy for asset bubbles, is consistently positive but insignificant. This suggests that perhaps later entrants fared better because they entered after the significant industry overinvestments in acquiring licenses were made and benefited from industry consolidation.

Model 3 measures the effects of prior foreign investment experience, operationalized as the number of host-country investments in Brazil, and internationalization experience, the number of prior countries of investment. These variables reveal some support for the argument that prior experience does pay, as firms increase their market-specific investment commitment. Model 3 empirically replicates Shaver, Mitchell, and Yeung’s (1997) finding that foreign entrants into U.S. manufacturing increase the likelihood of survival as the number of prior U.S. subsidiaries increases. In the same host context, be it Brazil or the U.S., prior experience does pay; frequent reinvestment in the same host country significantly (p = .052) increases survival time. The results become inconsistent, however, once other experience variables are included. Model 3 does not provide any supporting evidence that firms with more internationalization experiences survive longer. Although this relationship is not significant in model 3, later models reveal that once other types of experience, both skills-based and experience-based, are accounted for, then having gone to more countries significantly accelerates the time to fail. Results of this experience measure suggest there are learning discounts from adding more countries to the host-country portfolio. Model 4 reveals significant learning-curve benefits from firms with skills-based experience. Repeat investments using the same telecommunications technology skills (4-digit SIC code) significantly (p = .08) decelerate time to fail. This relationship is consistently positive across all models and becomes increasingly more significant when experience-based measures are subsequently included. Fixed effects are also included in models 4 to 12 to account for the telecommunications technology used in each subunit investment.

Institutional experience-based learning effect

Models 5 to 9 in tables 4b and 4c test hypothesis 1a using the regulatory distance variables. For all five of the weighted measures, I consistently found that greater distance (less similarity) in the regulatory institutional environment accelerated the time to fail. The home country, regulatory distance, and sign of distance were the most significant, at p < .001. The magnitude of the sign of distance coefficient (–0.4) is more than tenfold that of the other regulatory distance measures. This suggests that the most difficult of these learning hurdles is learning to adapt from a highly regulated environment to a much less regulated environment.

Figure 2 provides strong support for hypothesis 1b. To investigate differences in failure rates for similarity versus dissimilarity, I stratified the regulatory distance data categorically based on the mean regulatory distance from Brazil, holding all other variables constant at their means. Deviation below the mean was coded (1) for similar experience and (0) for deviation above the mean for dissimilar experience. The stratified hazard rates reveal intriguing magnitude differences. Firms with dissimilar experience are six times more likely to fail (0.6 hazard rate) than firms with similar experience (0.1 hazard rate). Figure 2 suggests that not only does similar experience pay, but the learning penalties from dissimilar experience have disproportionally greater negative impacts on performance.

Stratified hazard rate by similarity.

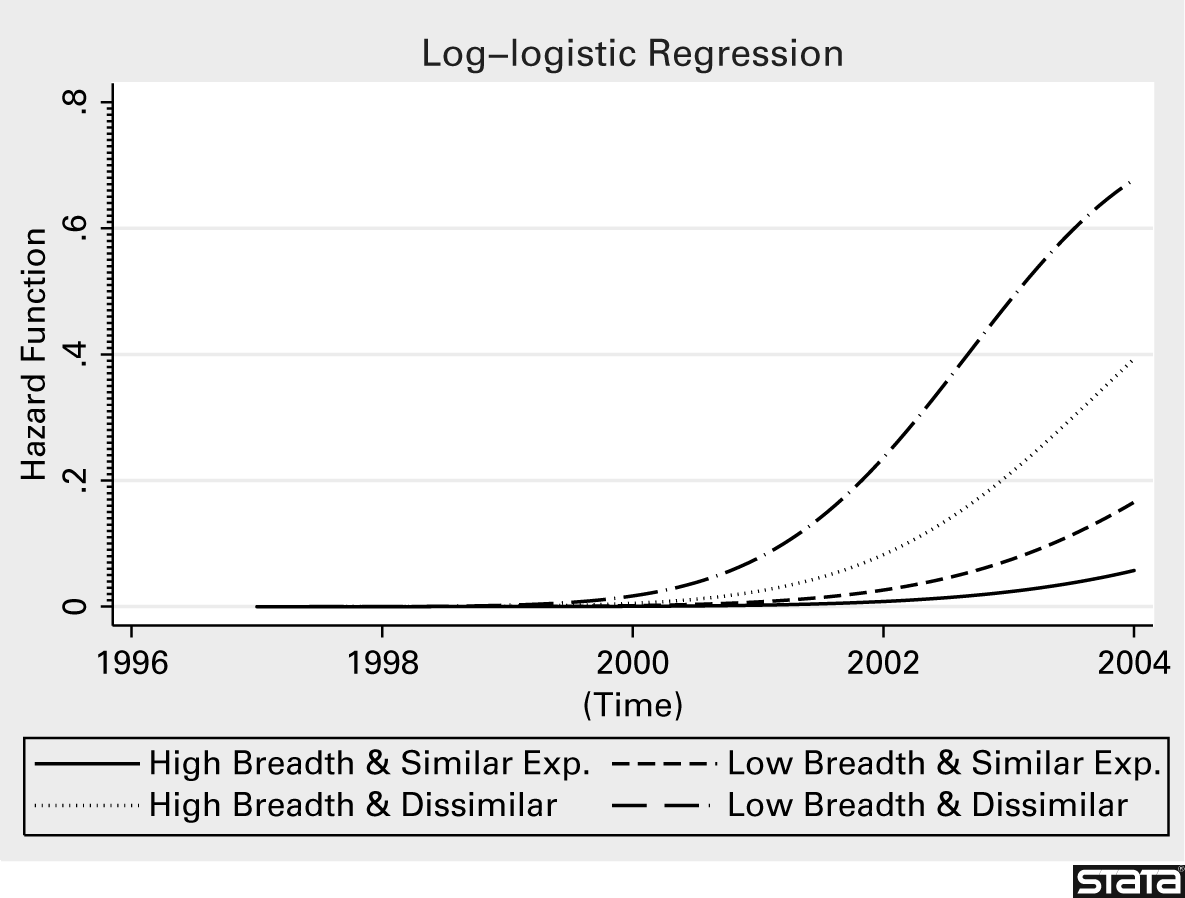

Model 10 in table 4c provides support for hypothesis 2. Breadth of experience has a positive and significant effect on firm survival. I also conducted further hazard-rate stratification analysis to examine whether there are conditions in which breadth of experience can hinder performance. Similar to the analysis above, I stratified the breadth variable to create two categories of high (1) and low (0) breadth split on the mean and further stratified the high/low breadth observations by the stratified distance measure above, creating four categories in total. Results, in figure 3, reveal that firms that acquired breadth and had experience similar to Brazil had the lowest failure rate. This suggests that firms experience learning penalties when the breadth of experience is not relevant to Brazil. The implication is that firms are better off having similar experiences and limited breadth. When irrelevant institutional knowledge is introduced into dissimilar environments, breadth penalizes performance.

Stratified hazard rate by breadth/similarity.*

Model 11 confirms hypothesis 3. Depth of prior experience in regulatory environments matching Brazil across the different dimensions has the most positive and significant effects on the subunit’s survival of the three hypothesized institutional experience effects. The magnitude of the coefficient is six times more powerful than breadth in decelerating time to fail. These results are supportive of the argument that learning-curve benefits can also be achieved from experience-based capabilities that are derived from recombining learned routines across institutional environments in highly applicable target host countries. The full model 12, including all control variables, conventional prior experience variables (number of prior investments in Brazil and number of host countries of investment), skills-based experience variables, and explanatory variables for hypotheses 1 to 3 (regulatory distance, breadth, and depth), maintains consistent directional and significance levels of the explanatory variables. When all the experience types are considered simultaneously in the full model, the host-country experience and skills-based capabilities experience variables are not significant in MNCs’ learning curves. This suggests that repetitive entry with dissimilar intuitional experience negates the benefits of repetition. Model 12 also reveals that positive learning-curve effects associated with depth are strong enough to negate the negative learning curve effects of both regulatory distance (β = –.03) and cultural distance combined. Among all the models in tables 4a–4c, the two leading explanatory variables that have the greatest effects on survival are the sign of direction of regulatory distance, which accelerates failure time by a factor of .44, and the depth of experience, which decelerates failure time by a factor of .27. This suggests that the learning gaps created by dissimilar institutional environments can be overcome to a great extent by recombining related prior institutional experiences.

Sensitivity Testing, Endogeneity, and Selection Bias

I conducted a sensitivity test using the full model (model 12) to test the fit of the log-logistic model versus other hazard-rate specifications. The model and test results are presented in table A12 in the Online Appendix. On the basis of the log likelihood scores, the log-logistic, Gompertz, and Weibull specifications produce a similar fit. The results are consistently significant across these model specifications, though AFT models and non-AFT models have opposite coefficient signs.

Another empirical concern is the selection bias of observable outcomes. In the models presented, the empirical limitations assume that the endogeneity of the firm’s ability to acquire institutional experience is randomly selected. Previous studies (Zajac and Westphal, 1996; Shaver, 1998), however, have demonstrated that firms’ strategic choices are not indicative of the random treatment model specifications; presenting such results can be sorely misleading when unaccounted-for factors affect the selection process. In this context, I observed survival of firms based on the similarity of institutional experience relative to the industry regulations in Brazil. What is unobserved is that in this industry, the most valuable assets are auctioned by governments and competed for by the most adept MNCs. Therefore there are three types of firms that could potentially be acquiring institutional experience around the world: firms that entered Brazil, firms that wanted to enter Brazil (auction bidders) but did not win a license from the government, and firms that could have entered Brazil but chose not to. Multinational firms that are highly skilled at winning these auctions for the newest technologies globally are likely to have greater access to institutional experiences around the world and are likely to be more sophisticated in using this knowledge for subsequent investments.

To account for the unobserved variable bias, I used a partial identification strategy to identify instrumental variables (IVs) that meet the exclusion restriction requirement of being correlated with a firm’s ability to acquire institutional experience but not significantly correlated with the performance outcome. 8 I identified two IVs that met these criteria for a valid instrument: auction wins, a count variable of firms’ prior successful auction wins globally, and geographic distance. Auction wins is a time-varying (annual) measure of the frequency of each firm’s participation in government telecommunications spectrum licenses that they bid on and won. Only the cases in which firms bested their competitors are counted, as this select set of firms is most successful in competing for market entry and has overcome market constraints imposed in the government auction process. In short, the survival of the experienced firms can be observed only for those firms that were able to navigate their way through the industry entry barriers. I used geographic distance, a second IV, because of the well-established relationship with reducing foreign entry (Shenkar, 2001). Geographic distance could also affect the propensity to invest in certain countries, which may have an indirect effect on how firms acquire regulatory experience. To confirm the exclusion restriction requirement (Greene, 2000: 672) of not being correlated with success/failure, I separately added auction wins and geographic distance to the probit models in table A13 in the Online Appendix. Neither was correlated with firm survival.

To address the potential sample selection bias resulting from the heterogeneity in firms’ decisions to enter Brazil or not, I used these two valid instruments and the three explanatory variables in the Heckman probit selection models in table A13 (modified version of Heckman, 1979; adequate techniques for event-history analysis have not yet been developed) (Boehmke, Morey, and Shannon, 2006) to test whether the error terms of the two equations were correlated (ρ). To make the coefficients comparable, I replicated model 12 specifications, fitting a maximum likelihood probit model on the 779 observations used in the survival analysis, and found similar results to those in model 12. I constructed three selection models to address all possible unobserved heterogeneity concerns. Ideally, selection should include the entire population of multinational telecom firms that ever won a license that could have entered Brazil during this period. The first selection model, global entry, examined this entire population of firms. A more precise approach is to test for selection biases among the firms that expressed an interest in entering Brazil. This set of firms was examined in the next model, Brazil entry. The last model used a combined approach to address both selection and endogeneity identification problems together. I used a double-selection model (Amemiya, 1985) in which the first selection equation is conditioned on having regulatory experience or not (0/1 dummy splitting the explanatory variable on the mean), and the second selection model is conditioned on the decision to enter Brazil or not. I included the inverse Mill’s ratio from the first selection model in the latter to account for the endogeneity of regulatory distance. Results across all three selection models revealed there was no significant selection bias among the entering firms. The coefficient estimates remain consistent for both the global entry and Brazil entry models, though the significance of the regulatory distance variable has weakened in the global entry model. Conditioning the results on both sample selection and endogeneity only strengthened the magnitude of the coefficients. Mainly, these selection bias results provide internal validity to the explanatory power of the hypothesized effects.

Robustness Checks

I conducted 18 separate robustness checks in models 13 to 30; results are available upon request. Models 13 to 15 tested the institutional control variables with multicollinearity concerns in lieu of the institutional controls used in models 2 to 12, including language distance (Grimes, 1992), egalitarianism (Siegel, Licht, and Schwartz, 2011), and legal origin distance (La Porta et al., 1998). 9 I also tested whether the results are robust during presidential and ministerial regime changes (Siegel, 2007) in models 16 and 17. The disaggregated Hofstede (1980) cultural distance composite measure was included as the four dimensions of culture—PDI, IDV, MAS, and UAI—separately (Kogut and Singh, 1988; Shenkar, 2001) in models 18 to 22. Robustness checks in models 23 to 27 provided additional firm-level performance measures, including the number of subscribers, purchase price, ARPU (average revenue per user), and number of employees (alternative proxy for firm size). A robustness check in model 28 tested the first entry-year observations only. Two final robustness checks in models 29 and 30 tested alternative measurements of regulatory distance including Euclidian distance and standardized regulatory scores found in Online Appendix F. Results revealed that the regulatory distance variable remains consistently significant (p < .001) in all robustness checks except model 28 (first entry-year observations). The breadth variable was significant across all robustness checks except in model 14 (legal origins) and model 28. Similarly, the depth variable was significant in all robustness checks except in models 14 (legal origins), 15 (egalitarianism), and 28. Alternative measurements in models 29 and 30 also produced similar coefficient estimates and significance levels. Model 31, the final robustness check, examined the results including an economic distance measure from Online Appendix F. These 18 robustness checks indicate mostly consistent and repetitive support for the explanatory variables. Moreover, the results from the robustness check in model 25 are consistent with the egalitarian distance measure used in Siegel, Licht, and Schwartz (2011); Hofstede’s (1980) uncertainty avoidance (UAI) index (used by Kogut and Singh, 1988) was tested in model 21 and was consistently negative but not significant.

Discussion and Conclusions

This paper addresses a fundamental and necessary question in organizational learning: When does prior experience pay? Organizational learning theorists (Dutton, Thomas, and Butler, 1984; Epple, Argote, and Murphy, 1996; Pisano, Bohmer, and Edmondson, 2001) and international business scholars (Li, 1995; Barkema, Bell, and Pennings, 1996; Shaver, Mitchell, and Yeung, 1997) have demonstrated learning-curve effects in several studies, primarily when the environmental context was relatively homogeneous (i.e., same plant location or same host country of investment). This study reveals that when the learning context, namely, the institutional environment, is unaccounted for, firms experience an accelerated path to exiting the market. This study provides clear evidence that prior experience pays most consistently when the institutional environment is similar.

This paper advances experience-based learning theory by demonstrating that the environmental context is integral to the organizational learning process. The core contribution to both the organizational learning and international business literatures is that similar contextual factors are critical to learning outcomes. Experience that lacks relevance is most harmful to an organization’s performance. This also suggests that firms can benefit strategically by learning from contextual environments and using that knowledge in seemingly unrelated subsequent investments. This study provides a unique empirical methodology to examine the types of institutional experience organizations acquired by using specific dimensional measures of industry regulation that vary across host nations. A Mahalanobis distance measure was used to capture the gap in each firm’s prior regulatory experiences across 80 host countries to determine the level of applicable knowledge possessed when entering Brazil. Similar methodological approaches to capturing contextual variation may be beneficial to future organizational learning and internationalization studies.

The above findings provide evidence of the trade-offs between breadth of institutional experience versus depth of knowledge (i.e., repetition). Variation in types of experience is a more significant indicator of learning in more-complex environments (e.g., idiosyncratic institutional environments, highly variant regulatory environments) than the frequency of repetition of investment in the targeted host country or the frequency of investing abroad. Breadth also has a greater impact when the organization has prior experience relevant to the environmental context. Without experiential relevance, breadth is associated with learning discounts. These results provide more clarity on the trade-offs between repetition-based learning versus contextual learning.

This study also introduces the learning concept of experience-based capabilities, which firms acquire from gaining competencies in a specific type of institutional experience. Firms’ depth of experience, when recombined in relevant contextual environments, is associated with performance gains. This finding provides support for the position that experience-based learning-curve effects can also be achieved across heterogeneous institutional environments. Firms achieve this learning benefit by strategically deploying recombined experience-based capabilities that replicate the targeted learning environment. Future research in this direction could explore more-fine-grained measures of depth of knowledge based on the duration and frequency of investments in each sequential host-country environment.

Another contribution to organizational learning theory is identification of the conditions under which learning discounts might occur. The demonstrated effects of inappropriately applied prior experience that is not relevant to the targeted context not only hurt performance, but the associated losses are often greater than the benefits derived from having relevant prior experience. Inappropriate knowledge applied from dissimilar experiences increases the risk of failure because managers grossly overestimate performance outcomes and inflate expectations. Such managerial overconfidence often results in a pattern of underperformance. This learning hurdle potentially leaves investment managers more risk averse in subsequent investments. The unlearned manager assumes the lack of success is the consequence of exogenous market factors when, in fact, the poor performance is largely a result of the manager’s inefficient decision making. The inability of organizations to adapt to select institutional environments is perhaps indicative of learning competence traps (Levitt and March, 1988; Levinthal and March, 1993) arising from selected and inherited knowledge. Myopic managerial thinking potentially prohibits adaptation to dissimilar institutional environments. This point is best illustrated by a telecom executive I interviewed who described the decision-making myopia of his peer: “These guys think they have seen everything. They find a solution that worked in the U.S. and try to use it in Brazil. The problem is, this is not Indiana!”

This paper also provides a foundation for a more critical review of internationalization theory (Johanson and Vahlne, 1977) by distinguishing the role of market-specific knowledge acquired within countries versus across countries. The analysis presented suggests that learning across countries can be more complex than previously theorized. The evidence that higher frequencies of investment are associated with learning discounts when other similarities are accounted for is another indication of dissimilar experience as a learning hindrance. These finding are counter to the theoretical predictions of Johanson and Vahlne (1977), who also argued that benefits of reduced market uncertainty should also be derived from investments across successive new countries. These results suggest that adding country-level experiences that neither have regulatory similarity nor exploit skills-based capabilities of the firm are taxing to subsequent foreign investments. Perhaps this refinement to the existing theoretical view is needed. Future studies should take into account the learning discount when knowledge that may not be relevant to the targeted institutional environment is transferred across countries.

In exploring types of experience, this study provides a framework to identify the unique and inimitable regulatory experiences that firms gain from idiosyncratic patterns of sequential foreign investments. One future extension of this research could explore how such knowledge can be leveraged as a source of competitive advantage. The challenge for organizations is to recognize the similarities that subunit organizations can experience across key institutional dimensions and that can subsequently be retrieved in related knowledge situations. The informed investment manager is able to select investments that appear to be risky to the inexperienced by deploying unique institutional knowledge based on related country characteristics (Davidson, 1980). These investment benefits may appear intuitive; however, interviews with 30 telecommunications executives conducted for this study revealed that many foreign investment managers do not make such underlying connections and are more frequently blindsided by institutional differences. Perhaps the heterogeneity in organizations’ regulatory experience provides a plausible explanation for the unresolved variation in organizational learning rates. The learning-curve differences among industry competitors could result from the sequence and frequency of types of experience acquired across learning environments. Organizations with investment patterns that reduce the knowledge gaps across investments are likely to learn at a faster rate than firms with fewer synergies.

This study also presents another key distinction in the variation in institutional environments between countries. The six dimensions of the telecom regulatory framework explored in this study can be generalized to other regulatory contexts, including energy, mining, and other utilities, pharmaceutical patent protection and drug content regulations, state and local health care regulations, and the banking industry. Subsequent studies assessing cross-country comparisons should include such regulatory dimensions in the same tradition as more-established institutional measures such as culture.

Limitations and future research

Generalizations from this study may be more limited when considering the level of foreign direct investment (FDI) that is permitted in host-country industries. This varies greatly across both developed and developing countries in the telecommunications industry (i.e., Canada requires 80 percent domestic ownership in telecom firms, whereas Croatia requires none). In the case of Brazil, telecommunications FDI was restricted only in the first privatization auction; therefore the dominating foreign ownership in this industry is perhaps more representative of host countries that do not restrict foreign ownership.