Abstract

The idea of financing higher education with the income that comes afterward has been formally proposed and implemented in the United States, in various permutations, since at least 1971. The attractiveness of the concept is exemplified by the political diversity of its proponents, ranging from Senator Ted Kennedy to President Ronald Reagan, and from presidential candidates Michael Dukakis (Democratic governor who ran in 1988) to Jeb Bush (Republican former governor who ran in 2016). This article examines the design of the various proposals over time, the arguments in support and opposition, and the current state of affairs.

Keywords

Societies benefit enormously from postsecondary education and training. Advanced study contributes to artistic, cultural, and scientific discovery that benefits the population broadly. It prepares citizens for democratic involvement that is informed and constructive, and prepares people for leadership and trusteeship, whether in family, community, business, or government roles. And in the economy overall, higher education provides the specialized training that makes the nation’s workforce productive and efficient, increasing national wealth and well-being.

At the level of primary and secondary school, the United States has adopted a coercive approach to education. Until age 16 (in most states), attending school is required by law, and parents are expected to feed, house, and clothe their children. Businesses, meanwhile, are restricted from hiring children as employees in ways that would prevent them from attending school. After adolescence, society’s approach to education switches from completely coercive to totally voluntary. No further education is legally mandated; people are free to find paid work; and while higher education is frequently subsidized in various ways, rarely are all of the costs that a potential student would face—including food and shelter—fully provided for.

Instead of using coercion, the United States promotes higher education through exhortation, with the most common argument not about the social benefits, but instead about the individual earnings gains associated with college degrees. A college degree is said to be worth a million dollars more over a lifetime than a high school diploma. 1 Student loans, in turn, are portrayed as an appropriate method of financing college expenses because they are “a means for transferring wealth from a future period of relative prosperity to the present,” financing “an investment that pays dividends in the future” (Akers and Chingos 2016, 6).

In reality, borrowing (or lending) money for college is riskier than the exhortations imply. If all that a potential student needed was liquidity—moving future certain returns to the present—student loans would be widely available in the private market at very low interest rates. They are not, because liquidity is far from the only risk for the student or for the lender. When someone takes out a loan for a car or a house, she or he ends up with a car or a home, and the lender has the ability to repossess if necessary. When students take out a loan for college, neither the students nor the lenders have any assurance that the borrowers will benefit. Students may not survive the academic challenges, dropping out before they finish. The college may or may not provide the training that is actually needed in the workforce. Students often discover that their interests change through their studies and experiences, or that the jobs they were aiming for are not there when they graduate. Further, a graduate may choose a career, like teaching, that does not pay as much as the average for a particular major, or may choose to spend time raising a family. Lenders are reluctant because they are faced with all of these same uncertainties combined with the lack of any collateral.

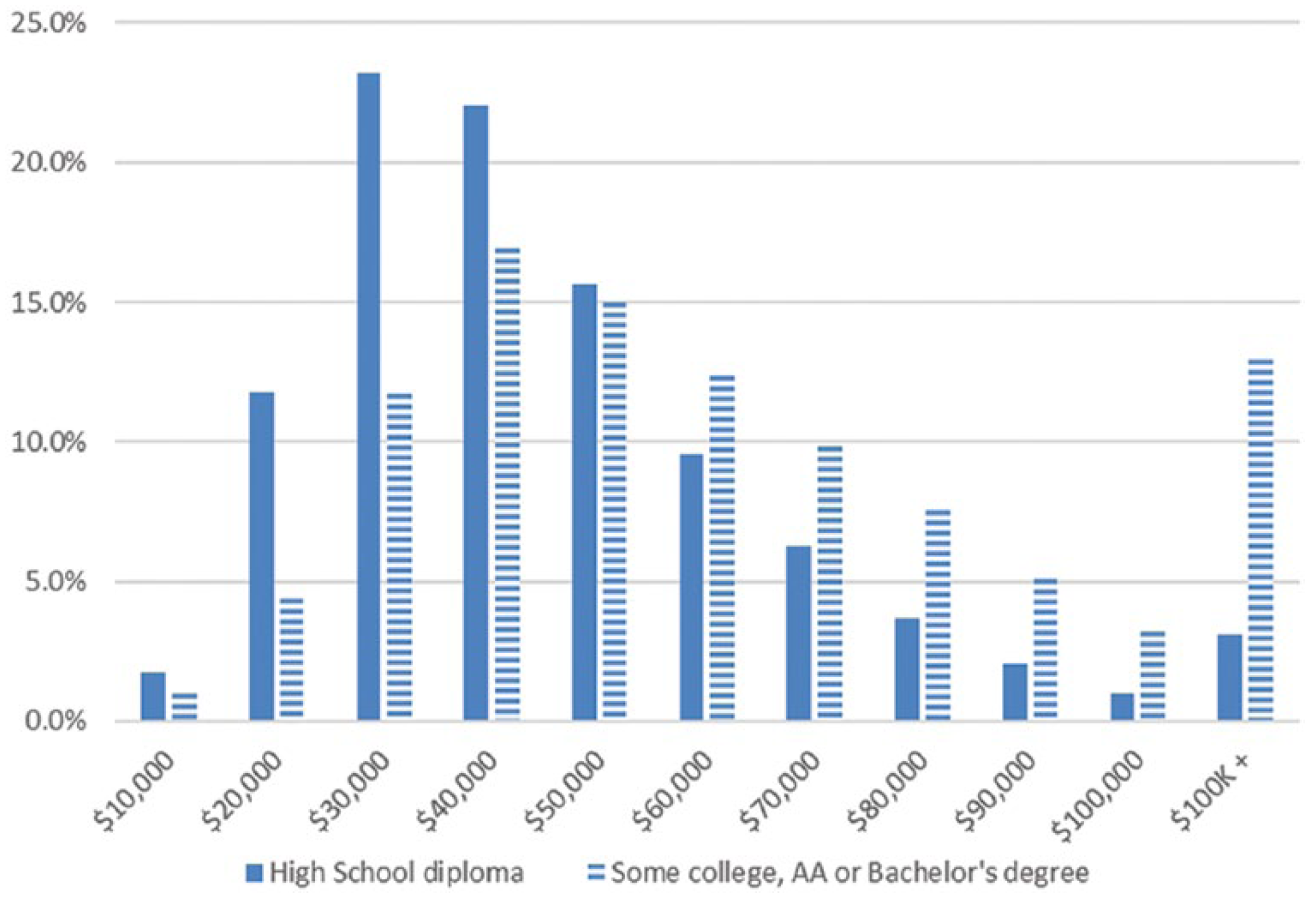

In 2011, workers age 35 to 44 with only a high school diploma had mean earnings of about $42,000, while the mean earnings of those with a bachelor’s degree were $76,000, or 81 percent more. But a more complete story would show the distribution of earnings, and would include all those who go to college whether or not they complete. Figure 1, which compares those distributions, still shows that going to college is more remunerative than not going, but it also shows why it is rational and appropriate to worry about borrowing to go: high earnings are not guaranteed for those who go to college, and earnings are not always low for those with just a high school diploma. In these 2011 data, a third of those who tried college, and a quarter of those with a four-year degree, earn less than the average high school graduate. Furthermore, these are earnings in the past. The amount and shape of future economic returns to education are unknown.

Distribution of 2011 Earnings of Full-Time Workers Age 35 to 44

Unless public policy somehow devises a safety net, asking students to borrow to go to college is like telling them to walk a tightrope to reach a pot of gold. The “wide variation about the average” (Friedman 1955, 137) makes traditional loans too risky for borrowers and lenders. This market failure was identified in 1935 by J. R. Walsh, who compared the financial returns of professional training and the returns to capital and found investments in the former to be lacking. The economy fails to generate adequate investments in training, he said, because unlike with capital, investors could not buy equity in humans. This meant that professional training was limited to young adults with wealthy parents, leading to a lack of opportunity that is “economically wasteful and socially deeply regrettable” (Walsh 1935, 277).

Walsh (1935) declared the lack of an equity market in human training “an insurmountable obstacle to the emergence of the conditions of an ordinary capital market in respect of college education” (p. 276). However, in 1945, after also finding inadequate investments in advanced education in a study of incomes in five professions, Milton Friedman and Simon Kuznets (1945) suggested a solution: “If individuals sold ‘stock’ in themselves, i.e., obligated themselves to pay a fixed proportion of future earnings, investors could ‘diversify’ their holdings and balance capital appreciations against capital losses” (p. 90, footnote 20). Friedman expanded on the idea in a 1955 paper, hypothesizing that administrative complications, such as monitoring incomes, explained why these types of contracts did not already exist. He also guessed there might be “irrational public condemnation of such contracts,” acknowledging that the contracts would be “economically equivalent to . . . partial slavery” (Friedman 1955, 138). He settled on a public sector approach: A governmental body could offer to finance or help finance the training of any individual who could meet minimum quality standards by making available not more than a limited sum per year for not more than a specified number of years, provided it was spent on securing training at a recognized institution. The individual would agree in return to pay to the government in each future year x per cent of his earnings in excess of y dollars for each $1,000 that he gets in this way. This payment could easily be combined with payment of income tax and so involve a minimum of additional administrative expense. (Friedman 1955, 140)

The remainder of this article chronicles the development of student loans of the type that Friedman described, what I call income-contingent loans, or ICLs. ICLs generally determine the amount students repay based on their postcollege incomes. Discussion of ICLs did not occur in a vacuum. It is weaved into the broader debate of the past half century, between public and private higher education and between approaches that rely on students to pay (usually through loans) as opposed to parents or the government. For much of that history, ICL was viewed suspiciously by supporters of government funding of higher education, as part of the conspiracy to undermine colleges financed through taxes. More recently, a debate remains about whether higher education finance has shifted too much in the direction of loans, and ICL is viewed broadly as a necessary component of any system that does rely on loans.

ICL Interest and Experiments in the 1960s and 1970s

America’s underinvestment in education became a frantic national issue with the Russian launch of the satellite Sputnik in October 1957. There had been a few small private and government student loan programs earlier in the century, so a larger federal role became part of the response (Wilkinson 2005). Less than a year after Sputnik, Congress sent to President Eisenhower the National Defense Education Act, which among other things provided colleges with money they would match and then advance to students for tuition, with colleges taking on the responsibility for collection themselves. A few years later, as part of the War on Poverty, Congress enacted the Higher Education Act of 1965, establishing indirect federal funding through a loan guarantee program. Both major federal efforts involved traditional repayment plans: fixed payments over a specific time period, paying off principal plus interest.

While not a major part of congressional deliberations, numerous ICL plans were proposed in the 1960s. Johnstone (1972) describes three different detailed plans in 1962 and 1963, as well as several bills introduced in Congress and state legislatures in that decade. A report from a federal advisory panel chaired by Jerrold Zacharias, a nuclear physicist working with President Johnson’s Office of Science and Technology, got national attention in 1967 for its Educational Opportunity Bank that would “enable students to sell participation shares in their future incomes” (Johnstone 1972, 73). The concept got a boost in reports from the Carnegie Commission on Higher Education and in a 1969 report prepared by the U.S. Department of Health, Education and Welfare under the direction of Secretary Alice Rivlin.

ICL did not get traction in Congress, though, because the concept—and loan programs in general—was viewed as potentially undermining support for direct aid to public colleges to keep tuition low. The institutions supporting ICL tended to be private nonprofit colleges, which during that period were facing financial difficulties that were predicted to worsen. One study conducted for the Carnegie Commission was titled, “The New Depression in Higher Education” (Cheit 1971). Against that backdrop, Yale, Harvard, and Duke all decided to try out their own versions of ICL. (Yale reached out to the Ford Foundation for financial backing but instead got Johnstone’s research, the seminal explication of the design issues surrounding ICL.)

Economist James Tobin, former chair of John F. Kennedy’s Council of Economic Advisers, designed Yale’s plan. In 1969, in the pages of the New Republic magazine, Tobin had proposed a federal ICL plan that he called a National Youth Endowment. Taking note of conservative Milton Friedman’s support of the idea, the liberal Tobin marveled at how the idea “is hard to locate . . . in the usual ideological and political spectrum. It can appeal to Republicans and Democrats, conservatives and liberals, old and young, rich and poor, black and white, it is adapted to the present mood of the country” (Tobin and Ross 1969, 21).

Tobin’s justification for action was twofold: a precarious financial future predicted for colleges and the unfairness of a system that fails to adequately serve people from low-income backgrounds. Under his plan, he argued, “The rich tycoon will pay back much more than he borrowed, the poor clergyman much less,” but overall the plan will break even. Emphasizing the importance of financing vocational and on-the-job training, not just bachelor’s degrees at prestigious colleges, he added, “Let these loans be available to all students” (Tobin and Ross 1969 19).

A conservative case for ICL was made a few months later. Arguing that lawmakers should “allow consumer choices to determine the allocation of resources within higher education,” Clurman (1970, 109) proposed tuition that more closely matched colleges’ costs, at public and private colleges. ICLs, meanwhile, would make it possible for students to “pay their college tuitions and living expenses out of their future incomes” (p. 107, emphasis in original). He continued: A loan program will distribute the burden of financing higher education more equitably. It will render it unnecessary for parents of modest incomes to foot most of the bill for an expensive investment which will deliver its return over their children’s entire working lifetime. This should remove a considerable source of anxiety from the financial plans of many middle income families. A loan program will also remove from students, with little parental financial support, the burden of working at a poorly paying part-time job while pursuing their education. (Clurman 1970, 109)

Clurman’s arguments certainly would have fed fears of public institutions that an ICL system “might come to be regarded as a panacea for educational finance,” stoking tuition increases and letting public officials off the hook for financing the social benefits of higher education. Tobin and Ross, in their article, had raised and dismissed these concerns as “probably exaggerated” (1969, 21).

The Design Parameters

In studying Yale’s and other ICL plans and proposals, Johnstone produced a useful guide to the policy choices that need to be made in the design of any plan. Here I offer a revised and expanded version of that list, with examples from different plans. See the online appendix for a chart that summarizes various proposals with regard to these parameters. 2

Which income counts?

All ICL plans involve some consideration of the borrower’s ability to pay, based on “income.” The logic of ICL is that it would only tax income gained from the training, but that counterfactual information is not known. The current dominant U.S. ICL plans protect just under $20,000 of an individual’s earnings. Australia’s plan leaves untouched an individual borrower’s income up to nearly $30,000 in U.S. dollars (Johnstone and Marcucci 2010).

Another policy choice involves how to handle a spouse’s income. Early proposals worried about a “negative dowry” problem: men shying away from women who carried a repayment obligation. In any plan that ultimately forgives some debts, failing to consider spousal income means a higher cost associated with nonworking spouses with debt.

How is the payment determined?

There are three basic approaches to basing payments on incomes: a variable percentage, a fixed percentage, and a payment cap. Under a variable percentage plan, the percentage of income that a borrower pays depends on the amount that is borrowed. A Yale plan from the early 1970s, for example, asked students to pay four-tenths of a percent of their income for every thousand dollars borrowed, so that someone who borrowed $10,000 would pay 4 percent of their income. A fixed percentage plan has borrowers pay the same proportion of income regardless of the amount borrowed, so the amount borrowed affects only the duration of repayment. That is how the newest federal plan, known as REPAYE, works. The other current federal ICL plan in the United States uses the third approach, a payment cap that prevents payments from exceeding a fixed percentage of income. Under the payment cap approach, there is a payment (such as the standard amount to repay a loan in 10 years) that is the amount the borrower pays unless that payment exceeds, say, 10 percent of income. If the standard payment would exceed the percentage cap, then the borrower pays only the capped amount.

Generally either the amount of a payment (standard or percentage) or the duration of payment is higher when the amounts borrowed are higher. If not, there can be unintended consequences, because if schools or students are able to predict that neither the payment size nor the duration of payments will be affected by the amount borrowed, they have little reason to restrain prices or borrowing.

How is interest handled?

With a traditional mortgage-style loan, interest that is not paid is usually capitalized. In other words, it is added to the amount owed, with interest in the next period charged on the new higher balance and the required payment increasing accordingly. In versions of ICL that monitor a balance owed, many borrowers will have periods during which their required payment does not cover the interest. Capitalizing interest can be distressing to borrowers (and to policy-makers). Waiving the interest, however, is costly to the system, because it reduces the amount that will be recovered from borrowers whose incomes ultimately recover.

In some conceptions of ICL (those that are most like an equity investment), there is no such thing as interest per se: a percentage of earnings is owed for a certain number of years, and then the borrower is finished whether or not the lender’s original investment was recouped. In such plans, borrowers with high incomes can end up paying what are, in effect, very high interest rates. The confiscatory nature of the approach can lead to the problem of adverse selection: students who expect to make a lot of money disproportionately opt out of the whole system, robbing the system of money that was expected to cover for lower-income students who did not fully repay.

A hybrid approach is to essentially front-load the interest. Borrowers pay based on their income but are finished when they have paid a total of, say, 50 percent more than the amount borrowed. 3 The effective interest rate in this approach is higher for those with high incomes (because they pay faster) and lower for those with low incomes (because their payments are stretched out longer).

When do payments end?

The longer the repayment period, the lower the payment can be and still have the program break even. Most plans end no later than when a borrower has repaid principal plus an interest or inflation charge. Many proposals also promise an end point of a particular number of years, with any remaining balance forgiven at that point. Forgiven amounts, since the payments are income-driven, go to borrowers with lower incomes (during the repayment period) relative to the amount borrowed.

Is the system meant to be self-financing or externally subsidized?

Most of the early ICL proposals were attempts to create completely self-financing systems. To the extent anyone was subsidized, revenue from high-income borrowers would cover assistance to low-income borrowers. There is no reason, however, that protections against excessive debt burdens must be financed by higher charges to other borrowers in the loan system. Instead of being self-financing, plans can rely on external funding or a net government subsidy. For example, other countries such as the United Kingdom and Australia that have adopted income-driven repayment have treated it as a way to partially recoup funds from what had previously been 100 percent government-funded universities (The Institute for College Access & Success [TICAS] 2014). In the United States, the 2007 creation of the income-based repayment program involved reducing some subsidies to banks to cover the projected costs of the new repayment plan.

Who is eligible, at which institutions, for how much money?

The creation or expansion of financial aid programs, of any type, can influence institutional decisions about programs, tuition charges and distribution of their own aid, and student decisions about borrowing and costs. In the UK and Australia, the ICL system was created for students predominantly at public institutions, by the same governments that also set caps on tuition and monitored access (TICAS 2014). The U.S. higher education system, in contrast, involves public, nonprofit, and for-profit institutions with a wide variety of incentive and control structures and no federal controls on tuition. Further, loans are available to undergraduate and graduate students, with wide ranges of loan limits. In 2006, a new federal loan program in the United States was launched for graduate and professional students. 4 Called Grad Plus, the loans can finance the entire cost of a student’s education with no set limit, meaning that the higher an institution raises tuition the more government loan money it can claim. 5 There is evidence that this moral hazard is causing tuition increases in some programs, such as law, that rely on borrowing for a large proportion of their students. The hazard can be made worse by ICL because borrowers expecting relatively low incomes have no financial incentive to limit their borrowing because the size of the loan does not affect the borrower’s repayment amount (Delisle and Holt 2015).

How are incomes to be documented and payments processed?

An oft-repeated lesson of implemented ICL programs is that documenting income can be a major administrative hurdle. Programs that base payments on tax filings showing prior-year income rather than the current income from which borrowers make payments create the need for additional procedures for borrowers whose incomes have declined. Payroll withholding from current income can be far more efficient but is not without its own complications: someone must still instigate the withholding and determine the right amount to be withheld, given the amount borrowed. There are additional complications for married borrowers (if the amount owed depends on joint income, as it does in the U.S. programs) and borrowers who are self-employed or have multiple sources of income.

How is the program treated in the income tax system?

The tax treatment of ICL programs has long created complications. Loans are generally not treated as income, but forgiven debts are generally considered income subject to taxation, while grant aid is usually taxable to the extent that it exceeds tuition and other course-related expenses. As it stands today, amounts forgiven in the U.S. loan program (except under service-related provisions) are subject to taxation, which means that the “end” of repayment under the loan formula may not actually be the end of payments for the borrower.

Plans from the Left and Right, 1977–1990

In a November 1977 speech about the future of higher education, John Silber, the dynamic and brash president of Boston University, proposed an ICL system with loan limits that would make private colleges broadly accessible, with payments collected through the income tax system (Silber 1978). Senator Edward M. Kennedy, the Massachusetts Democrat who chaired the Senate’s education subcommittee at the time, became an advocate of the Silber plan, holding hearings to gather input. 6 The plan was vigorously opposed by the nation’s public colleges, arguing that it would fuel tuition increases. The Carter administration argued that the plan would cost more than estimated, fuel tuition increases, and “intrude into the decision-making processes of private institutions.” 7 Silber kept pressing for his approach into the early 1980s, but it did not gain traction.

In 1986 and 1987, the Reagan administration proposed loan repayment based on postcollege income (Werner 1987). While labeling it “income contingent,” there was actually no contingency at all, as it offered no real break to those who end up having low income relative to their debts. Instead, while payments were capped at a percentage of income, repayment was extended forever, with interest. A contemporaneous assessment by an analyst at the Congressional Research Service noted with barely concealed alarm that the plan apparently did not even cancel debts in the case of a borrower’s death (Riddle 1986). Congress allowed the Department of Education to establish a demonstration program at ten colleges. The program was discontinued due to the terms of the program and the difficulty schools had documenting borrowers’ incomes (U.S. Congress, House of Representatives 2013).

In 1988, the Democratic nominee for president, Governor Michael Dukakis, proposed an ICL plan under which higher-income graduates would pay somewhat more, subsidizing those who end up with lower incomes. President Reagan’s secretary of education, William Bennett, criticized the approach as unworkable: “Somebody already laid this egg . . . the Dukakis proposal looks suspiciously like the old Yale University plan that proved unworkable a decade ago” (Walker 1988). Dukakis advisor Gene Sperling (who would serve later in both the Clinton and Obama administrations) responded, “The program will take some cross-subsidization, but we think we are drawing a proper balance.” 8 The Dukakis plan was based on a proposal developed by Brookings Institution economist Robert Reischauer, who presented his proposal at a 1988 symposium sponsored by the College Board. 9

At the College Board symposium, Joe Flader, an aide to Republican Congressman Tom Petri, discussed his efforts to develop a workable ICL approach (Gladieux 1989). 10 The Petri approach, first introduced in 1985 (National Direct Student Loan Coalition [NDSLC] 2015), was an impressive attempt to address adverse selection, reduce moral hazards, and allow for a wide variation in debt amounts, to ensure, as Petri said in 1992, that “the government doesn’t spend more on subsidies than people need” (U.S. Congress, Senate 1992). Petri’s smart, but complicated, design would form the basis of the first major federal ICL program in the United States, a repayment plan the borrower could choose called income-contingent repayment (ICR).

A Key Change in Government Budgeting

Prior to 1990, Congress could create a loan guarantee program and not worry about its costs until the bills came due in later years. Making a loan directly, on the other hand, would count as a total loss to the treasury as if it were the same as a cash gift, even though the borrower would be making payments back into the treasury in later years. This created a bias toward guaranteeing loans made by banks. An ICL program, however, particularly if it were going to involve collecting payments through the IRS, would be a direct loan. Any viable proposal, therefore, needed to include a plan for somehow capitalizing the initial loans and creating a revolving fund.

In a budget deal in November 1990, President George H. W. Bush and Congress placed guaranteed and direct loans on more equal footing under which all of the long-term costs of a loan or loan-guarantee program would be assessed at the time the program was established or changed, and estimates updated annually to account for actual program experience and economic conditions. 11 This change from a cash to accrual accounting method eliminated the need to establish a separate financing system for a loan program. Instead, the revolving fund would be essentially automatic, with budget estimates driving the amounts that Congress needed to set aside to subsidize the costs of the program over the long term. The accounting change created a political opening for advocates of ICL and advocates of eliminating the banks from the student loan program—forces that would unite in the next Congress. 12

The accounting change, while eliminating a bias toward guaranteed loans, did not change the fact that estimating the costs of a loan or guarantee program is inherently imperfect. Borrowers and institutions do not behave as initially predicted, and experts can only make guesses about future economic conditions such as interest rates or the earning trajectories of college graduates. The predictions themselves, and program experience that differs from the predictions, would drive debates about program design.

ICL Arrives and Is Buried in the 1990s

Even before the budget deal changed the accounting rules, officials in the Bush administration were contemplating a shift from guarantee to direct student loans. According to Charles Kolb, an appointee who worked at the Department of Education and then the White House: The program had become unmanageable, unauditable, and unaccountable with the growth of a cottage industry of banks, guarantee agencies, and secondary markets that grew rich off the generous federal subsidy. Every effort was needed to simplify and streamline the program’s operation. (Kolb 1994, 147)

The administration (and new Secretary of Education Lamar Alexander) backed away from the direct-loan idea. But the estimate of cost savings and simplification, and a favorable follow-up analysis from the Government Accountability Office, 13 fueled interest from House Democrats. Meanwhile, Petri, a Republican who viewed direct loans as integral to ICL, gained broad bipartisan support for his bill, with forty-nine Republican and forty Democratic cosponsors. Testifying at a Senate hearing in 1992, Petri argued that ICL with IRS collection would mean that loan defaults would be “defined out of existence.” His repayment formula, meanwhile, “provides subsidies to all those who need them, only to those who need them, and to the extent of their need” (U.S. Congress, Senate 1992, 35).

In the Senate, meanwhile, two ICL proposals were introduced in 1991. Senator Bill Bradley authored a plan, based on the EPI report, that was referred to the Senate Finance Committee (which had jurisdiction over the IRS). And Senators Paul Simon, a Democrat, and David Durenberger, a Republican, adapted Petri’s approach in a bill that they introduced together, which was referred to the Senate Committee on Labor and Human Resources (with jurisdiction over the Department of Education, and now chaired by Kennedy). 14 The Simon-Durenberger bill took the savings from interest subsidies and from eliminating the banks and proposed plowing that money back into Pell grants and state aid programs.

With leading Democrats and Mr. Petri supporting direct lending in the House committee, and Simon and Durenberger promoting their proposal in the Senate committee, the question of guaranteed versus direct loans became one of the major items of discussion in the 1992 reauthorization of the Higher Education Act (another being fraud and abuse by for-profit colleges). Most of the controversy, though, was not focused on the ICL concept but on ditching the role of banks, guarantee agencies, and Sallie Mae. With the Bush administration threatening to veto a full shift to direct loans, Congress ended up adopting a pilot direct loan program, with some schools testing ICL. 15 The repayment formula was left up to the secretary of education, with the proviso that it be cost-neutral and based on a review of the borrower’s income tax information, and forgive any remaining balance after not more than 25 years.

The 1992 reauthorization also, significantly, made federal student loans available to virtually all Americans. Previously, only students with “need” as calculated under the aid formula could get federal loans. The reauthorization created an “unsubsidized” version of the Stafford loan (interest was charged during school and deferment periods) that would be available to middle- and higher-income families without calculated need.

Meanwhile, then-governor of Arkansas Bill Clinton was campaigning for the Democratic nomination for president. In his stump speech, Clinton picked up the same themes that were being discussed in Congress: getting the banks out of the loan program, allowing anyone to borrow, and ICL. He added public service as another way to pay back: We ought to scrap the student loan program that exists now. I would put in its place a domestic G.I. Bill. . . . You would sign a contract to pay [your loan] back in one of two ways: your choice. Either as a small percentage of your income over time after you get out of school and go to work, paid at tax time so you couldn’t beat the bill. . . . Or what I would hope would happen: Every American who borrowed the money would have the option to pay it off with a year or two of national service.

16

With Clinton’s election, his plan became part of a budget bill in the first months of the administration, giving direct loan and ICL advocates another bite at the apple only months after the ideas had been relegated to a pilot program and before the direct loan program’s ICR formula had even been written. Waldman (1995) chronicles the political path taken by Clinton’s national service and ICL campaign promise (including my role). 17

The Clinton administration included in its plan a path to payroll withholding of payments on income-contingent direct loans, which was included in the Senate-passed version of the budget bill. 18 The House-passed version, however, only authorized the IRS to share information with the Department of Education. In the House-Senate conference to reconcile differences, Senate ICL advocates argued that IRS collection was essential. Senator Kennedy went along somewhat reluctantly, according to Waldman (1995), concerned that the IRS role could prompt the Senate Finance Committee to assert jurisdiction over the whole student loan program. On the House side, however, when the staff to the House Ways and Means Committee (which has jurisdiction over the IRS) saw the wage-withholding provision, they “freaked out,” telling the House education chairman that (in Waldman’s characterization), “If anyone was going to change the responsibilities of the IRS, it would be Ways and Means, thank you very much” (Waldman 1995, 143). The White House representative, Bill Galston, agreed to drop the IRS collection concept in the legislation: “It was made very clear to us that the opposition to going farther was staunch and unlikely to be moved by acts of persuasion.” Joe Flader, Petri’s expert on ICL, called Galston’s decision “a pathetic retreat on a crucial element of the whole thing.” 19

With the passage of the budget bill, the Department of Education redoubled its efforts to develop the ICR details, which would happen through an open regulatory process. The starting draft was the Petri proposal, with concerns revolving largely around the question of what should happen when borrowers’ payments are not enough to cover the interest charges for the year. Some advocates were concerned about debts ballooning as a result of interest. Flader, however, considered it important, as an equity matter, to let the debts grow so that in cases where borrowers’ incomes increase substantially, the program recovers at least some of the funds. Flader thought of the debt amount as an accounting mechanism rather than as a true amount due, since all debts get wiped out after 25 years anyway. 20 The formula that was ultimately adopted followed the Petri approach closely, with the addition of a limitation on the compounding of unpaid interest.

Just four months after a first set of 104 schools had become a part of the new direct loan program in July 1994, the Republicans, led by Newt Gingrich, gained control of Congress. Among Gingrich’s targets was the switch to direct student loans, which had come to be known as a Clinton “pet project” (see, for example, Manegold 1994). To prevent the new Congress from killing the new program in its infancy, Secretary of Education Richard Riley agreed in 1995 not to use his authority to draft schools into the direct-loan transition and not to promote the program over the bank-based guarantee system. Thus began a bizarre, 14-year détente in which schools could choose between two different federal loan administration systems. The loans themselves were essentially identical except for the ICR option. 21 Actually telling anyone about the benefits of ICR, though, was viewed by department officials as violating Riley’s promise because it would be seen as promotion of the direct loan program where the ICR option resided.

Reviving ICL, 2005–2010

In 2005, the Pew Charitable Trusts seeded a major new initiative, the Project on Student Debt, to be led by a nonprofit that I had launched the year before, The Institute for College Access & Success (TICAS). Working with a number of other advocates, TICAS set out to establish a federal ICL program that would be known, used, and useful. The direct loan’s ICR program posed problems in that regard. First, because it was linked to direct lending, anyone who did not want to upset the détente between direct loans and federal loans disbursed through banks would be reluctant to get involved. That issue would be gone by 2010 with the elimination of the bank role (Smith 2016). Second, the formula’s complexity and an income cap of 20 percent (which sounds high) made it difficult for advocates and public officials to promote the program, especially as the banks’ allies sought to discredit it. And for fans of ICR, such as legal aid groups who found it a useful option for victims of predatory schools, there was a worry that any effort to change ICR might result in its provisions worsening for those populations.

Because of those complications, the Project on Student Debt created a campaign for a new ICL option that would be available in both the direct and guaranteed loan programs. The effort included commissioned papers, surveys, and focus groups to prompt national discussion about student debt. A white paper showed the repayment burdens facing students in the U.S. loan programs and laid out a number of possible ways to address them (TICAS 2006). 22 A coalition formally petitioned the secretary of education to establish, by regulation, a new approach to ICL. 23 Limiting repayment to a maximum of 20 years, it would protect a larger amount of income than ICR and cap payments at 15 percent of income, making it possible to summarize the plan as one that would limit payments to no more than 10 percent of income for most borrowers. Ten percent of income seemed to be a magic number that students and the public felt comfortable with, but it was difficult to incorporate it as an absolute maximum without a significant budgetary cost. Twenty years was appealing because borrowers would generally be finished paying before being asked to help pay for their own children’s college education.

To raise awareness of loan reforms, student groups created a national student-loan debt clock, a student-debt yearbook, and campus rallies and other events where students were photographed next to a giant inflatable ball and chain representing their ballooning debts. Little balls and chains also appeared on students’ mortarboards at graduation. Students testified at the hearings of the Commission on the Future of Higher Education, a panel created by U.S. Secretary of Education Margaret Spellings.

The Department of Education denied the petition. But a few months later the broad support for the already-developed plan caught the eye of Democrats, who had regained control of Congress. Senator Kennedy incorporated income-based repayment (IBR), as it came to be called, into one of the first bills he authored in that Congress. 24 In the House, Rep. George Miller, the California Democrat chairing the Education and Labor Committee, also included IBR in the bill that his committee developed, the College Cost Reduction and Access Act (CCRAA). 25 President George W. Bush signed the final version into law on September 27, 2007.

The plan differed from what the coalition had proposed in three significant ways. For cost reasons, the maximum repayment period was extended to 25 years (the same as in ICR). Also for cost reasons—and because of the moral hazard discussed earlier—Grad Plus loans (which have no borrowing limit) were excluded from forgiveness in IBR. This latter change was reversed, probably by mistake, in the 2008 regulations (still the Bush administration) that implemented IBR. 26

The most significant difference was the addition of a Public Service Loan Forgiveness (PSLF) program, under which debts are forgiven after 10 years of ICR, IBR, or standard loan payments while working in government or for a nonprofit 501(c)3 organization. ICR and IBR had been built on a base assumption of full loan repayment within a 10- or 12-year window, with the payment term extended when borrowers face high payments given their incomes. For most borrowers, that period of heavy burden is limited, so payments are reduced during that period but the loan is fully repaid before reaching any forgiveness at 20 or 25 years. With the 10-year PSLF, borrowers whose payments are reduced under IBR or ICR for any length of time end up with an amount forgiven if they continue in an eligible job and even if their income increases dramatically. The benefit may promote public service careers but creates potential costs—especially for high-debt careers like law and medicine—and greater moral hazards.

The PSLF provision had been developed and pursued primarily by law schools (Schrag 2007), while IBR was promoted by a coalition more focused on undergraduate education. It is probably fair to say that the combination of the two new programs—especially with the still-new Grad Plus loans—had not been fully vetted.

In his first budget after being elected, President Obama proposed a larger Pell grant that would be a full entitlement program, financed in part by the budget savings from completing the transition from bank-based guaranteed loans to direct loans. (At the time I was working with the presidential transition team and then was an appointee at the Department of Education). The House of Representatives adopted the shift to 100 percent direct lending, using the savings for Pell grants (though not creating an entitlement) and other aid programs. 27 In the Senate, however, filibuster threats prevented action. The only route to major student loan and Pell grant changes would be if the plans were included in the budget reconciliation bill that also was to include health care reform (the Affordable Care Act, or what became known as Obamacare).

While the new IBR program was just being implemented, the recession elevated the issue of student debt. President Obama (personally, I was told by colleagues at the White House) wanted to ensure that student loan payments would not take more than 10 percent of a borrower’s income or extend beyond 20 years. The change to IBR would cost money but, given the savings from the move to direct lending, could be accommodated and was added to the negotiations on the budget bill. As budget/health care negotiations continued, the higher education provisions were dropped from the bill. But the provisions were revived due to obscure Senate rules regarding the balance of spending and budget reductions within various committee jurisdictions. 28 That is how IBR (and, by extension, PSLF) became more generous—too generous in the case of some graduate school loans—with little public discussion.

Stepping Back

Since 2010, student debt has exploded as a public issue. In regulatory actions (after my departure), the Obama administration attempted to both expand access to, and to some degree rein in the costs of, the more generous IBR. Meanwhile, analysts have held conferences and published numerous reports calling for refinements, some major and some minor, to the ICL programs and options that have evolved over the past 25 years. 29 I conclude not with an attempt to chart a path for ICL, but instead to suggest a look at the bigger picture.

Postsecondary education brings enormous benefits to communities and the economy overall, as well as to individuals, on average. Given the risks to individuals, some type of low-income protection is imperative to the extent that loans are the way that college access is made possible. At its core, however, an ICL system is simply a way to tax the higher incomes that result from higher education, as a way of financing the investment in the first place.

Direct government subsidies to higher education are portrayed as fundamentally different from a loan-based system. But as more people go to college, and if the whole economy benefits, the two approaches converge: the difference, in a sense, is more administrative than fundamental. And administratively it is much easier to tax high incomes in the income tax system than to administer an income-contingent student loan repayment system on top of an income tax system.

Footnotes

Robert Shireman is a senior fellow at The Century Foundation, where he focuses on issues of college accountability, consumer protection, and finance. He served as deputy undersecretary of education in the Obama administration, senior advisor at the National Economic Council in the Clinton administration, and chief education advisor to Senator Paul Simon (D-Illinois). He is the founder of The Institute for College Access & Success and has had roles in other nonprofit organizations.

NOTE:

I am indebted to Tariq Habash, a colleague at The Century Foundation, for his assistance in tracking down and poring through historical documents at the Library of Congress, and for constructing a comparison chart of all of the ICL proposal through history. Thanks also are due to others who reviewed drafts or answered queries, including Thomas Butts, Lauren Asher, Jason Delisle, Robert Gordon, Jamie Studley, and John Douglass. And of course the most important appreciation goes to Nicholas Hillman and Laura Perna for recognizing the gap in the literature and asking me to help fill it.