Abstract

The Child Tax Credit (CTC) delivers more economic benefits to children than any other federal program. Under its current design, the CTC provides a benefit of up to $2,000 per child under age 17: almost 90 percent of families with children receive at least some benefits, and families with the lowest incomes receive the least. In 2021, a temporary expansion of the program increased the maximum benefit, delivered up to half the credit as a monthly payment, and allowed families with the lowest incomes to receive the full benefit: millions of families that typically received a partial benefit saw greater economic returns, and the nation saw substantial drops in poverty and hardship. Even in a highly polarized political climate, policymakers continue to consider changes to the CTC that could reclaim some of the benefits that were observed in 2021. This article describes reform options and who would benefit most from various reform approaches.

The federal government invests more than $500 billion in children annually through direct cash payments, including tax credits, and in-kind goods such as child care, education, food subsidies, and health care coverage. The Child Tax Credit (CTC) represents more than 20 percent of that investment (Maag, Lou et al. 2023).

The CTC began in 1998 as a relatively modest $400 credit that could be used only to offset taxes owed. Since then, Congress has altered the credit in myriad ways—increasing the credit amount, making the credit refundable (allowing families to receive a credit in excess of taxes owed), and expanding the income range over which families could be eligible (Greenstein, this volume). The most significant expansion of the credit for families with low incomes occurred in 2021 in response to the COVID-19 pandemic. Unlike every other expansion to the CTC (even those initially enacted as temporary), the 2021 expansion was allowed to expire as other pandemic spending expired.

The future of the CTC is uncertain. Some legislators continue to push for its return to 2021 levels, while others are interested in no reform or more modest changes. Absent any legislative action, the maximum value of the CTC is set to be cut in half after 2025, returning the credit to its value prior to 2018.

We analyze a variety of options to reform the credit, discuss who will benefit from each reform, and forecast the 10-year budget cost of those policy change options. We find that there are several ways to reform the credit to target additional resources toward families with very low incomes, though they all fall short of delivering benefits to those families that would equal the 2021 expansion. Other reforms would deliver benefits to families more broadly or to middle- and high-income families. Most would reduce child poverty, but the magnitude of the reduction varies across proposals.

Background

In its current (2023) form, the CTC is worth up to $2,000 per child under age 17. Families first use the credit to offset taxes owed. If their allowable credit exceeds taxes owed, families may receive the excess amount as a “refund,” up to a defined limit. To receive the CTC as a refund, families must earn at least $2,500. The refundable portion of the total tax credit is calculated as 15 percent of earnings in excess of $2,500. Families can receive up to $1,600 per child as a refundable credit (Figure 1). The maximum amount of CTC refund that families can receive is scheduled to grow with inflation until the total refundable benefit equals the maximum CTC.

Child Tax Credit for Single Parent with One Child, 2023

The credit phases out starting at $200,000 in family income, or at $400,000 for married couples filing their taxes jointly. Children must have Social Security numbers valid for work and be under age 17 at the end of the year to qualify for the credit. Children ineligible for the CTC, including older dependents, typically qualify for the $500 nonrefundable credit for other dependents. The CTC and credit for other dependents phase out together as one credit.

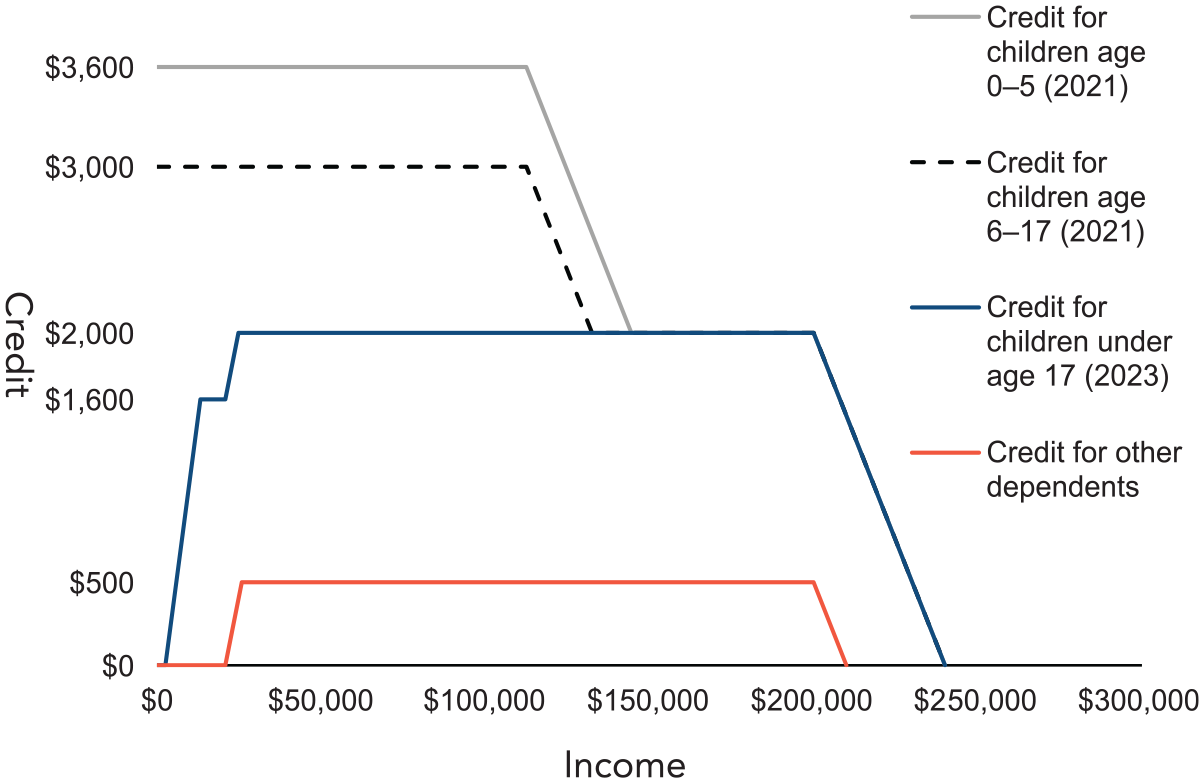

In 2021, the American Rescue Plan Act temporarily increased the CTC maximum credit to up to $3,000 per child ages 6 through 17 and $3,600 per child under the age of six. The phase-in for the CTC was eliminated, making all families under the phase-out thresholds eligible to receive the maximum credit without regard to earnings or taxes owed. The expansion also changed how the credit was delivered: almost all families eligible for the credit received half of it in monthly payments from July through December. They received the remainder when they filed a tax return the following spring, the time they normally would have received their full credit. As a result of this temporary expansion, the maximum benefit was available to almost 19 million children in families with low incomes who typically do not receive the full CTC because their parents do not earn enough. The temporary expansion expired after 2021.

The CTC offsets part of the cost of raising children for working families. The Tax Policy Center (TPC) estimated that just under 90 percent of families with children would benefit from the credit in 2023 (TPC 2022a). 1 In 2022, with similar rules in place, TPC estimated that 1.8 million children under age 17 were left out of the credit entirely because their parents with low incomes did not have earnings. An additional 16.8 million children in 2022 lived in households that received less than the full $2,000 per child credit because their parents’ earnings were too low to qualify them for the full credit (TPC 2022b). A disproportionate share of children not getting the maximum credit were Black and Hispanic, likely a reflection of historical discrimination in the labor market (Collyer et al. 2023; Goldin and Michelmore 2022). Meanwhile, 2.7 million children under 17 lived in families that received less than a $2,000-per-child credit because their income was too high to qualify for the full benefit.

On average, middle-income families received the largest average benefits in 2023. If the credit were made fully refundable, as it was in 2021, the lowest-income families would receive benefits on par with those of middle-income families (Figure 2).

Average Child Tax Credit Benefits by Income Quintile, 2023

Although families with the lowest incomes receive lower average benefits than higher-income families do when the CTC is not fully refundable, the CTC still serves as a powerful tool to reduce poverty. In 2022, researchers estimated the child poverty rate of 12.4 percent would have been 15.2 percent absent the CTC (Koutavas et al. 2023). Under 2021 law, the impact of the CTC in reducing poverty was much more dramatic, with some estimates suggesting child poverty reductions as high as 45 percent (Burns, Fox, and Wilson 2022). Because the payments were delivered monthly and to households with very low incomes in 2021, the CTC smoothed income among families that often face month-to-month spending constraints (Bitler, this volume).

Some scholars argue that the near-universal nature of the credit improves its popularity and makes the program more politically sustainable (Burman 2020). But extending the CTC to a relatively large share of families with higher incomes also opens the credit up to criticism from those who argue benefits should be targeted more efficiently (Akabas et al. 2021; Edelberg and Kearney 2023; Sawhill and Pulliam 2019).

Unlike programs targeted to families with low incomes, the near-universal nature of the CTC makes it relatively straightforward to design expansions that largely benefit families with middle and high incomes. Prior to 2018, when the credit was more targeted to middle-income families, increasing credit limits would have little effect on higher-income families. 2 Now, it is possible to extend benefits to very high-income families by increasing the credit or slowing the rate that the credit phases out.

Reforming the CTC

The temporary expansion of the CTC in 2021 was lauded by many advocates and policymakers for reducing child poverty. A robust body of evidence documented that when all but the highest-income children became eligible for the full credit, food insecurity declined (likely a product of both increasing credit amounts for families with low and moderate incomes and delivering up to half the credit on a monthly instead of an annual basis from July through December), racial disparities in who benefits from the credit narrowed, and families reported an increased ability to meet their basic needs (Curran 2022; Hamilton et al. 2022; Karpman et al. 2022; Marr, Cox, and Sherman 2021; Parolin 2023; Perez-Lopez 2021). Among Supplemental Nutrition Assistance Program (SNAP) recipients living in poverty, the declines in food insecurity attributed to the CTC were particularly pronounced (Pilkauskas et al. 2022).

Although an extension of the expanded CTC passed in the House, it fell one vote short in the Senate (DeParle 2022), failing to become law. Since them, many policymakers, including President Biden, have continued to support an expansion of the CTC, though in some cases, the proposed expansion would be more modest than the 2021 expansion (U.S. Department of the Treasury 2024; Watson 2024). We first describe the major levers that policymakers can shift with respect to the CTC and then demonstrate the effect of a sample of reforms.

Phasing the credit in

Conditional on having eligible children, the design of the credit phase-in is the most important determinant of how large the benefit will be for families with low incomes. The phase-in describes how the CTC grows from a starting point of no credit eligibility to the maximum credit. It is possible to have no phase-in period, as was the case in 2021, when the phase-in was eliminated and families with low incomes received the maximum benefit. This has not been true in any other year. In every other year, families either needed to owe taxes to benefit from the CTC (when the credit was largely nonrefundable and could only be used to offset income taxes owed for almost all families) or needed to earn money from working (which determined how much of the credit could be received in excess of taxes owed as a refundable credit).

There are three primary rules related to tax credit phase-ins that often serve to reduce benefits for families with low incomes. First, the phase-in rate determines how much credit a family (that is ineligible for the full credit) will get for each dollar they earn. A higher rate means that, all else being equal, families will receive a higher benefit than they would receive if the rate were lower (Maag, Marron, and Huffer 2019). Second is the refundability threshold, which determines how much of a family’s earnings will count toward calculating the credit. When the CTC was first made broadly refundable in 2001, most families needed to earn at least $10,000 before they could begin to get the credit. Over time, that amount has dropped to $2,500 (Greenstein, this volume). Third, the current CTC is partially refundable, meaning that only some of the credit can be received as a refund (often referred to as the limit on refundability). If a family qualifies for a refundable credit amount that exceeds the refundability threshold, the excess amount is forfeited.

Credit phase-out

For higher-income families, the credit phase-out drives how much benefit they can receive. The phase-out rate determines how quickly the credit will decline from the maximum benefit to the minimum benefit. A higher phase-out rate means that the benefit declines faster for each dollar earned by a higher-income family. Slowing the rate has the opposite effect. The second component of the phase-out is the phase-out threshold—that is, the income level at which the credit begins to decline. A lower threshold results in a more targeted benefit, while a higher threshold distributes the benefits to a broader population. The phase-out threshold varies according to marital status: the credit starts phasing out at higher incomes for married couples than for single parents.

Maximum credit amount

The most well-known parameter of the credit is probably the maximum credit amount. Typically, all children under age 17 qualify for the same maximum benefit. In 2021, benefits were extended to children who were as old as 17, and the maximum benefit for children under age six was higher than the maximum benefit for children ages 6 to 17.

Sample Reform Options

Taken together, the phase-in rate (how quickly the credit phases in), the threshold at which the CTC begins to phase in, and the amount of credit that can be received as a refund determine the extent of the benefits among families with low incomes. Making any (or all) of these parameters more generous can provide substantial benefits to families with low incomes at a relatively modest fiscal cost. Setting a minimum refundable benefit could also direct higher benefits to families with low incomes. Other reforms, including changes to the maximum credit amount, would have the effect of delivering the most benefits to families with higher incomes.

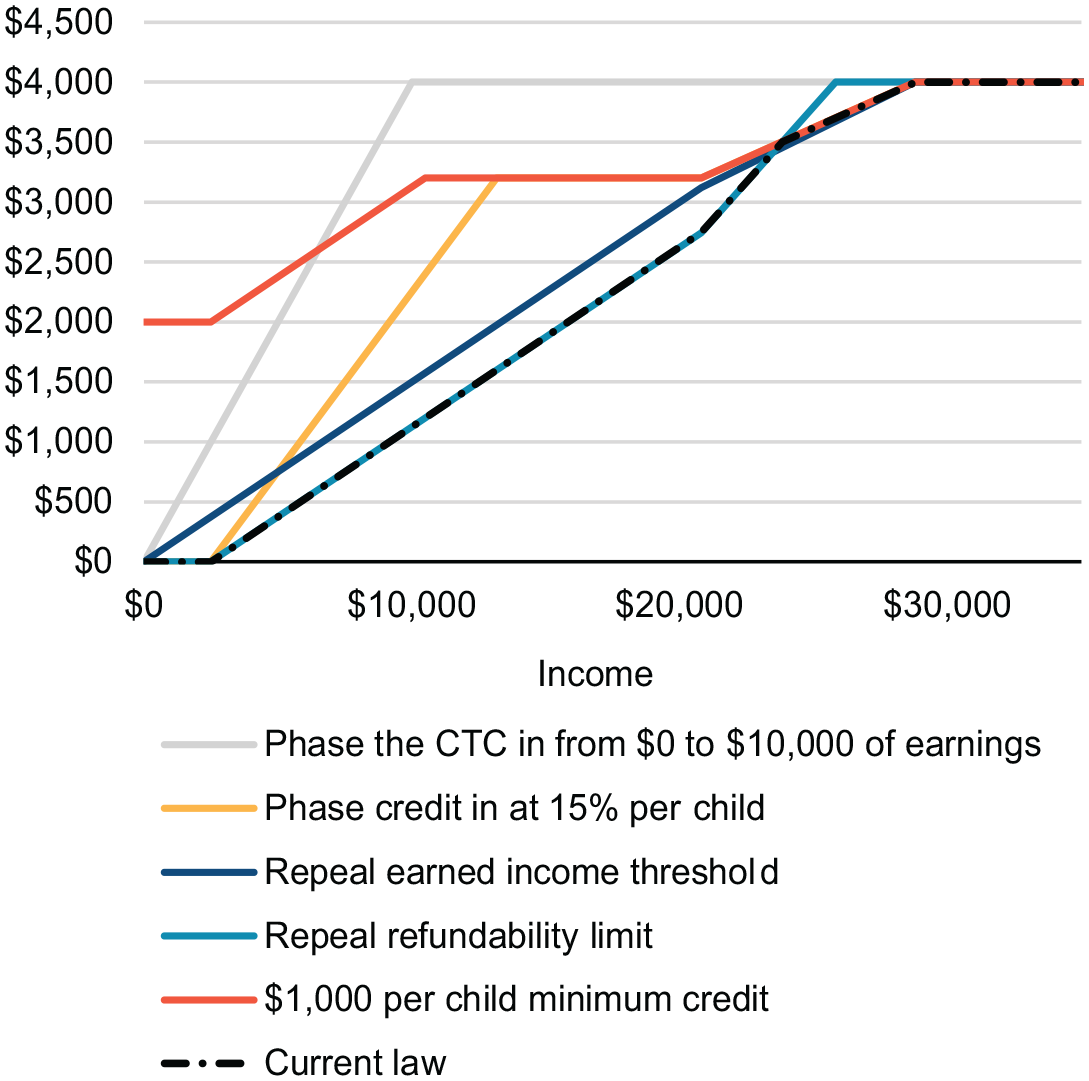

Some policymakers have objected to a fully refundable credit that delivers the maximum benefit without regard to earnings. We highlight several options that would reform one or more of the phase-in parameters while still maintaining an earnings requirement to access the full benefit. These include repealing the earned income threshold, repealing the limit on refundability, phasing the credit in at a faster rate for families with more than one child, delivering a $1,000 minimum refundable benefit, and phasing the credit in fully once a family earns $10,000 (Figure 3). All would focus new benefits on families with low incomes, though none would deliver as large a benefit as would be delivered if the credit were made fully refundable as it was in 2021. We describe each of these reforms to the phase-in, as well as full refundability, in more detail below.

Child Tax Credit Phase-In Reform Options, Single Parent with Two Children, 2023

Reforming the phase-in

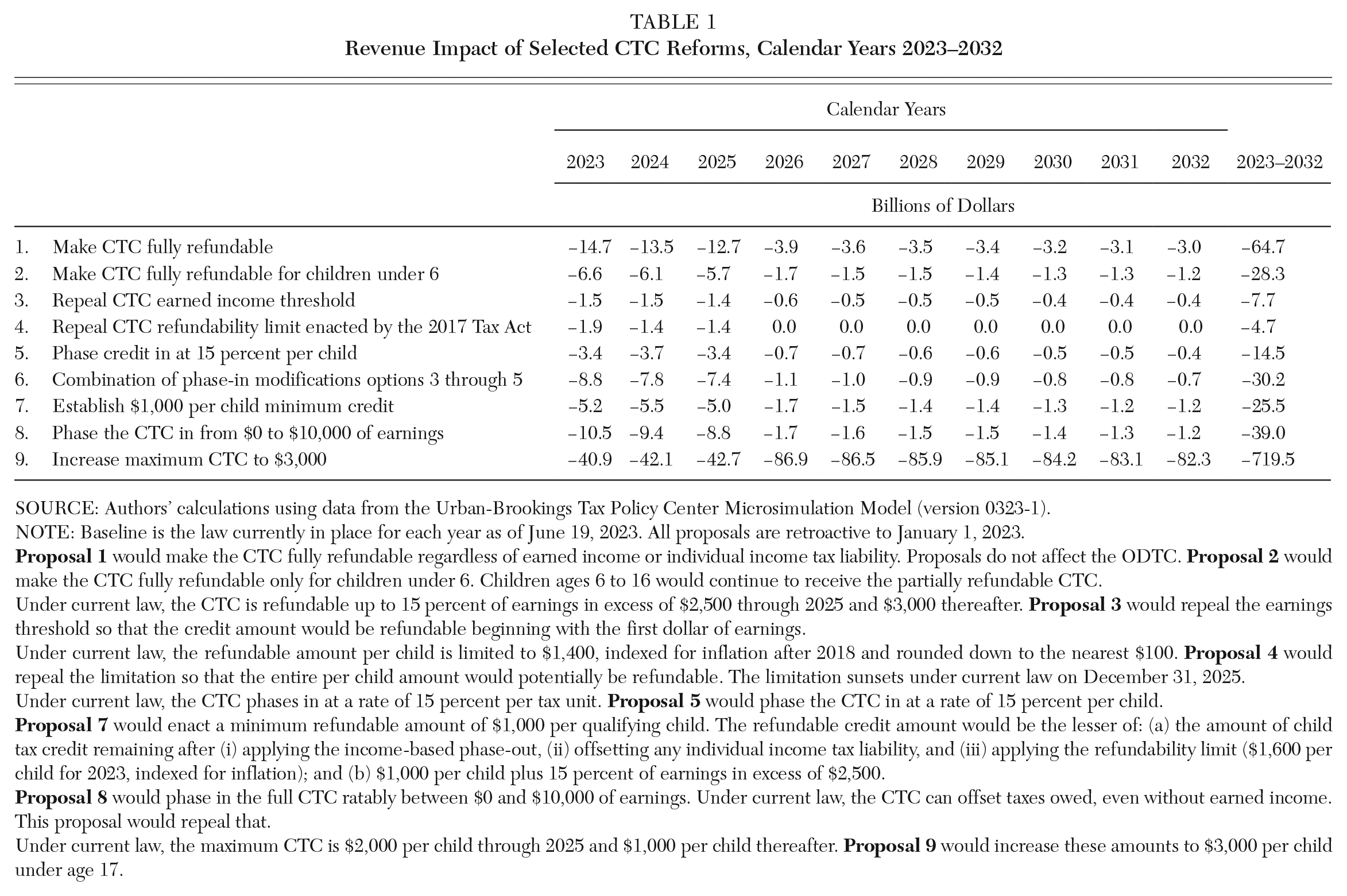

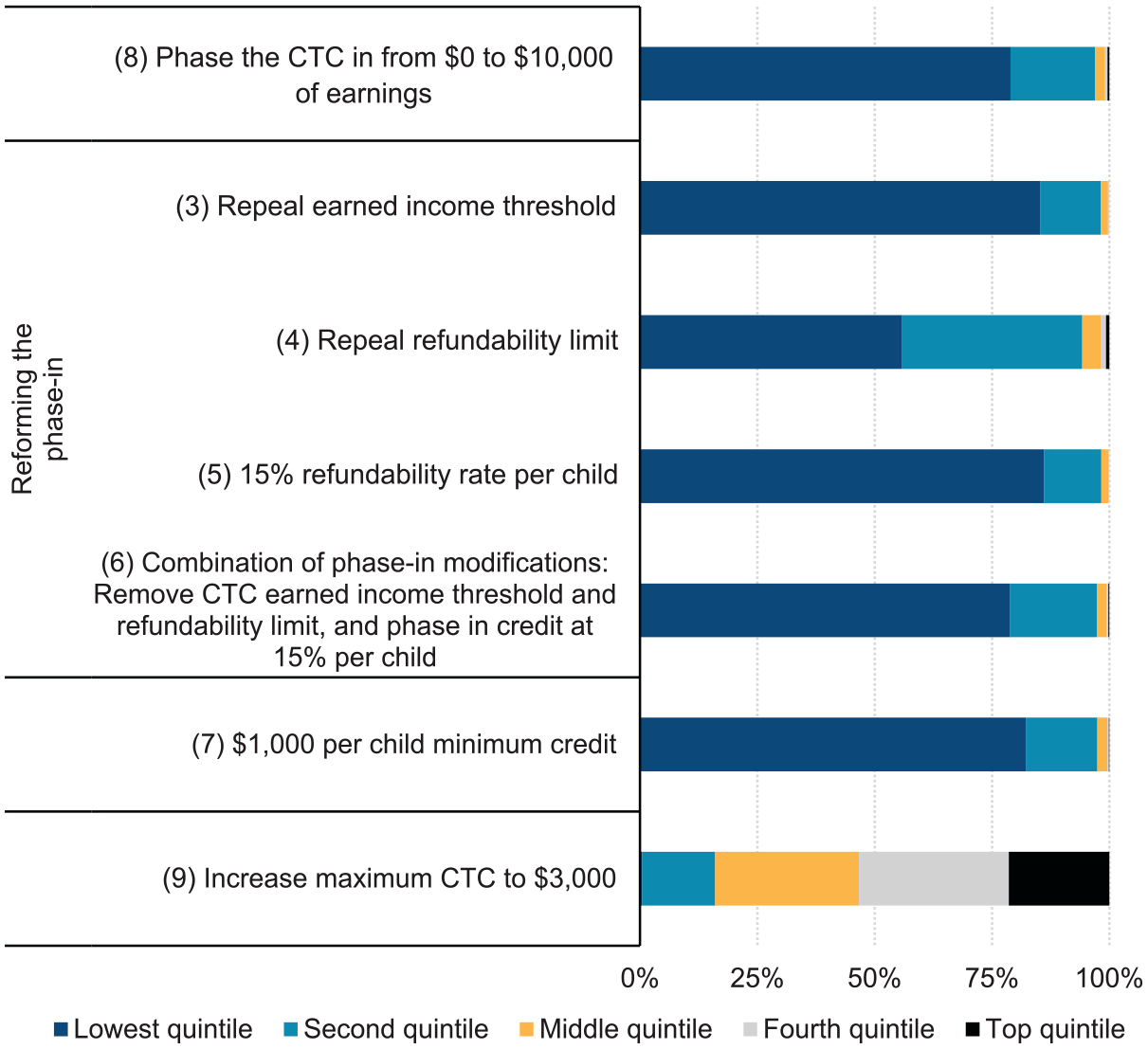

We present multiple options to reform the generosity of the phase-in. We describe each option (shown in Figure 3) and use the TPC microsimulation model to estimate the average benefits received by families in the bottom 40 percent of the income distribution, that is, the bottom two income quintiles (Figure 4); the share of each reform that would go to each income quintile (Figure 5); and the proposal’s cost in 2023 and over the 10-year budget window from 2023 to 2032 (Table 1).

Benefits of Child Tax Credit Phase-In Reforms, Tax Units with Children, All and with Benefit, 2023

Share of Child Tax Credit Increases Delivered to Each Income Quintile, Tax Units with Children, 2023

Revenue Impact of Selected CTC Reforms, Calendar Years 2023–2032

SOURCE: Authors’ calculations using data from the Urban-Brookings Tax Policy Center Microsimulation Model (version 0323-1).

NOTE: Baseline is the law currently in place for each year as of June 19, 2023. All proposals are retroactive to January 1, 2023.

Under current law, the CTC is refundable up to 15 percent of earnings in excess of $2,500 through 2025 and $3,000 thereafter.

Under current law, the refundable amount per child is limited to $1,400, indexed for inflation after 2018 and rounded down to the nearest $100.

Under current law, the CTC phases in at a rate of 15 percent per tax unit.

Under current law, the maximum CTC is $2,000 per child through 2025 and $1,000 per child thereafter.

Eliminating the phase-in and providing full refundability

In 2021, the CTC was temporarily expanded to allow all families with low incomes with a qualifying child to receive the full credit, regardless of earnings or taxes owed. This came to be known as “full refundability.” Analyses showed that this aspect of the 2021 expansion was critical to both reducing poverty and to reducing racial disparities in who receives the full credit (Acs and Werner 2021).

About 70 percent of families with incomes in the bottom 20 percent of the income distribution, the lowest income quintile, would benefit from this proposal. We estimate that families with eligible children in this income quintile would receive an average benefit of $1,500. About one-quarter (27 percent) of families in the second-from-the-bottom quintile would receive a benefit from making the CTC fully refundable, receiving $860 on average. Many people would receive no additional benefit from making the credit fully refundable typically because they already receive the full credit.

Making the CTC fully refundable would cost approximately $15 billion in 2023. Over the 10-year budget window, we estimate the cost of this reform would be $65 billion.

Full refundability for young children

A substantial body of research suggests that early childhood is the most critical period of development for children and that providing additional resources during that time can improve brain activity (Troller-Renfree et al. 2022). It is also the time when parents, particularly mothers, are most likely to have their employment interrupted by caregiving needs (Congressional Budget Office [CBO] 2018). Others have identified substantial payoffs from investments in very young children (Heckman and Masterov 2007).

Policymakers could opt to make the credit fully refundable only for young children, perhaps those under age six or even those under age three. The distribution of benefits of full refundability for children under age six and under age three are very similar, with proportional declines in the total fiscal cost of the policy change (Maag and Isaacs 2017a, 2017b). The cost of full refundability scales roughly proportionate to the share of age-eligible children. A fully refundable credit for children under age six would cost about $7 billion in 2023 and $28 billion over the 10-year budget window (not shown in table). Making the credit fully refundable just for children under age three would cost roughly half that amount.

Modifying the phase-in

Short of full refundability, the CTC phase-in could be modified in several ways to deliver additional benefits to families with low incomes. One option would phase the credit in more quickly by providing the full credit for families that reach a defined amount of earnings (we test $10,000 here). Lawmakers could also increase the rate at which the credit phases in (for all families or only for families with more than one child [we test 15 percent per child here]), remove the earned income threshold so that the credit would begin to phase in at the first dollar of earnings, remove the refundability limit so that more families could receive the full credit in excess of taxes owed, or provide a minimum credit to all low-income families with children and then phase-in the remaining credit with earnings. Each of these options retains an earnings requirement to access the full credit, which may make an expansion more politically feasible.

Phase the credit in by $10,000 of earnings

Senators Mitt Romney (R-UT), Richard Burr (R-NC), and Steve Daines (R-MT) proposed phasing the full credit in once earnings reached $10,000 in their Family Security Act 2.0. If the credit were fully phased in once earnings reached $10,000, 67 percent of families in the lowest income quintile would benefit, as would 25 percent of families in the second-lowest quintile. Among families who benefit in those quintiles, average benefits would be $1,230 and $670, respectively. We estimate this would cost about $10.5 billion in 2023 or $39 billion over the 10-year budget window. A version of the proposal included offsets to this benefit. Here, we estimate only the impact of changes to the CTC.

Phase the credit in at 15 percent per child

The CTC has always been phased in at the tax-unit level rather than the child level. This means that a parent with $10,000 of earnings and one child will receive the same benefit as a parent with $10,000 of earnings and two children. The credit could instead phase in at a per-child rate. Phasing in the refundable portion of the CTC faster for larger families would result in more low-income families receiving the maximum $1,600 refundable portion of the credit. If the credit phased in at 15 percent per child, 23 percent of families in the lowest income quintile would benefit by an average of $1,180. We estimate this would cost about $3.4 billion in 2023 or $14.5 billion over the 10-year budget window.

Repeal the earned income threshold

Removing the earned income threshold and beginning the CTC phase-in at $1 of earnings delivers modest tax cuts to 35 percent of families in the lowest income quintile. On average, these eligible families would see a benefit of $320 from this change. Few families with higher incomes would benefit because they already receive the maximum credit. We estimate this would cost $1.5 billion in 2023 or $7.7 billion over the 10-year budget window.

Repeal the limit on refundability

The refundability threshold limits the credit amount for many low- and moderate-income families. In 2023, assuming a family’s taxable income comes entirely from earnings, a single parent filing as “head of household” can earn $20,800 before owing tax (a married couple can earn $27,700 before owing tax). With a 15 percent phase-in rate, a single parent earning $15,833 could qualify for the full $2,000 credit if they have one child, but a credit for these parents is still limited to $1,600 by the refundability threshold. We estimate that removing the refundability threshold would reduce taxes for 28 percent of families in the lowest income quintile and 19 percent of families in the second-lowest income quintile. Among families who would receive a tax cut, families in the lowest income quintile would receive an average benefit of $320, and families in the second-lowest would receive an average of $380. We estimate this would cost $1.9 billion in 2023 or $4.7 billion over the 10-year budget window.

Combination of phase-in modifications

It is possible to combine a 15-percent-per-child credit phase-in with removal of the earned income threshold and elimination of the refundability threshold. Doing so would increase the CTC for 63 percent of families in the lowest income quintile, with eligible families getting an average benefit of $980. We estimate this would cost $8.8 billion in 2023 or $30.2 billion over the 10-year budget window.

CTC floor

Another targeted option to expand the CTC is to set a credit floor. For example, the refundable portion of the credit could begin at $1,000 per child for all families with low incomes, with the remaining credit amount phasing in with earnings or tax liability. Most of the benefits from this reform (80 percent) would go to taxpayers in the lowest income quintile. We estimate that about 35 percent of families with children in that quintile would receive an average benefit of $1,100 from implementing this credit floor. In 2023, this would cost $5.2 billion, and it would cost $25.5 billion over the 10-year budget window.

Reforming the maximum credit

Those with incomes in the phase-in range of the credit would not benefit from an increase in the dollar value of the credit unless other reforms discussed above are included. As a result, options that solely increase the credit generally benefit middle- and higher-income families, while phase-in reforms benefit the lowest income families.

Increasing the maximum credit

We estimate who would benefit from increasing the credit to $3,000 per child under 17. More than half (56 percent) of all families with children would benefit, including more than 80 percent of families in the middle and second-highest income quintile—those families would receive tax cuts of over $1,000 on average. Unlike the phase-in reforms, where most new benefits accrue to families with low incomes, about 30 percent of all benefits from this proposal would go to families in the middle income quintile, 32 percent would go to families in the fourth income quintile, and 21 percent would go to families in the highest income quintile (Figure 6). Higher-income families become eligible for the credit because a larger credit phases out over a longer income range, assuming the phase-out rate stays the same.

Share of CTC Increases Delivered to Each Quintile, Tax Units with Children

In 2021, two credit levels were implemented: $3,000 for children ages 6 to 17 and $3,600 for children under age six. The benefits of raising the credit for children under six to $3,600 are similarly concentrated in the third and fourth quintiles (not shown), though a smaller share of families benefit overall.

Raising the credit for all children to $3,000 would cost $40.9 billion in 2023, or $48 billion with the addition of the $3,600 credit for children under age six (not shown). Over the 10-year budget window, increasing the credit to $3,000 per child under age 17 would cost almost $720 billion. Increasing the credit to $3,000 for children ages 6 to 17 and to $3,600 for children under six would cost $801 billion. Costs relative to the baseline rise after 2025, when the base credit will be $1,000 per child rather than $2,000 per child.

Effect on poverty

A much-discussed outcome of the 2021 CTC expansion was the 40 percent reduction in child poverty, including a narrowing in the child poverty rate by race and ethnicity. Researchers estimate that poverty rates for Black and Hispanic children would be cut in half (Acs and Werner 2021). Importantly, half of the reduction in poverty was driven by making the $2,000 per child CTC fully refundable. The remaining reduction in poverty came from expanding the group of children eligible for the credit and from increasing credit amounts. The analysis was based on a $2,000 credit in 2018, a year that was not affected by changes in economic conditions caused by the COVID-19 pandemic.

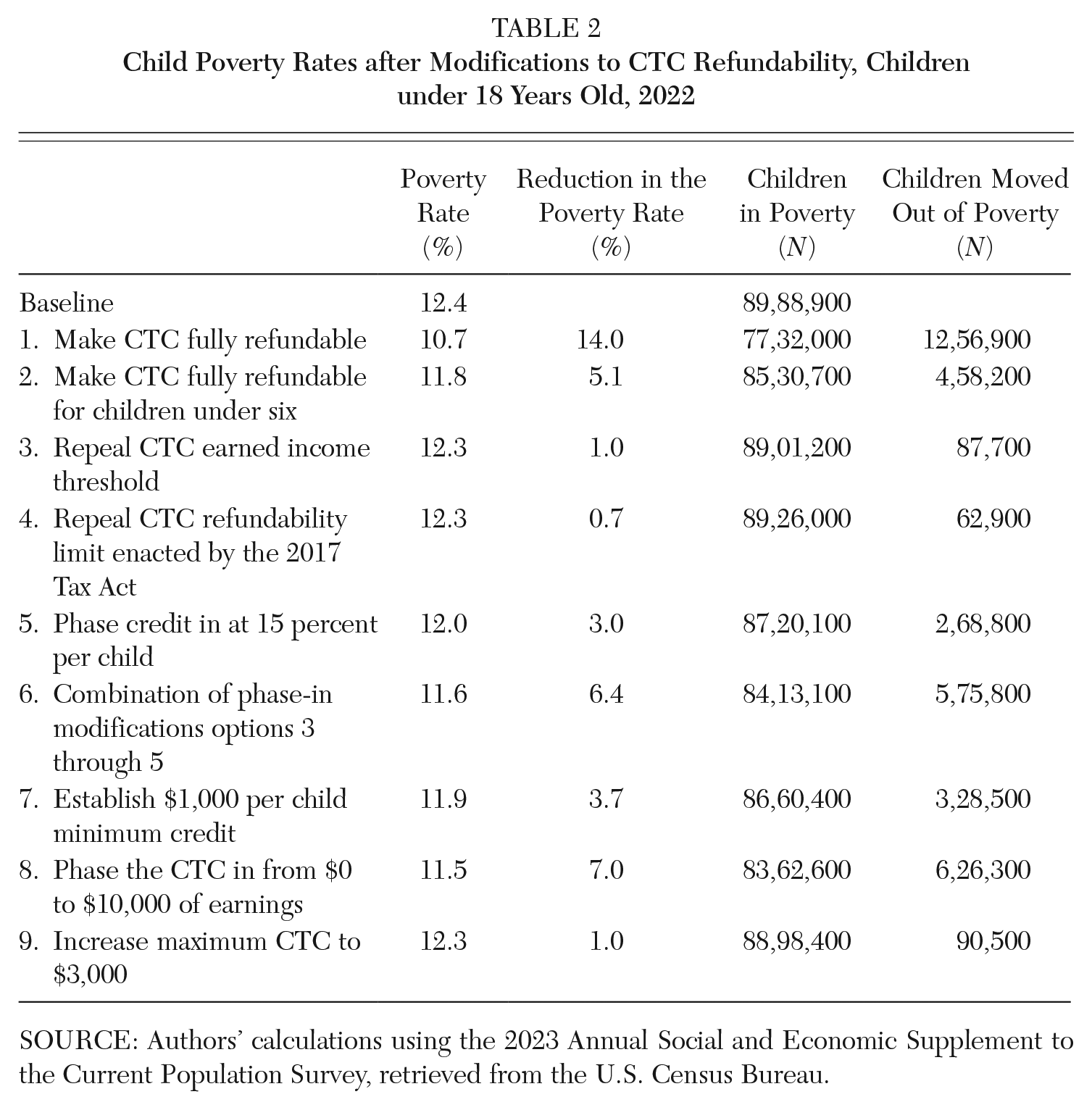

Unlike many other tax provisions, the CTC is not automatically adjusted for inflation. As a result, the credit has lost significant value since it was first expanded in 2018 (McClelland 2023). Today, using the microsimulation model developed at the Center on Poverty and Social Policy at Columbia University, we estimate that making the credit fully refundable would reduce child poverty by about 14 percent (Table 2). Other reforms would have a more modest impact on poverty.

Child Poverty Rates after Modifications to CTC Refundability, Children under 18 Years Old, 2022

SOURCE: Authors’ calculations using the 2023 Annual Social and Economic Supplement to the Current Population Survey, retrieved from the U.S. Census Bureau.

While it is still the case that expanding the phase-in of the credit would provide important, targeted relief—and seems like a necessary first step toward making the credit more inclusive—policymakers should not count on the CTC having the same poverty-fighting power of the earlier credit today without also adjusting the credit for changes in inflation (Collyer, Wimer, and Harris 2022).

CTC timing

The tax system is designed to deliver annual benefits after the relevant information from the year has been processed. Eligibility for the CTC is determined based on the age of the child on December 31 of the tax year. Any child who turns 17 before this date is not eligible for the CTC in that year.

Typically, families with low incomes file a tax return in the spring and receive their credit, along with any other refund owed, a few weeks later. Higher-income families can receive the CTC throughout the year by adjusting their tax withholding—and indeed, higher-income families adjust their withholding in response to changes in the number of children more frequently than do low-income families (Jones 2012). As a result, higher-income taxpayers are less likely to over-withhold and thus receive their CTC as an offset to taxes owed throughout the year instead of as a single payment at tax time.

Delivering credits annually as a single payment creates a blunt instrument for delivering economic assistance and differs from more traditional transfer programs, such as the Temporary Assistance for Needy Families program and Social Security—both of which deliver monthly benefits. Annual payment also subsidizes a single family over the course of the year, even though some children move between homes throughout the year or reside with multiple potential caregivers. Both situations have become more common over time (Cavanagh and Fomby 2019; Maag, Peters, and Edelstein 2016; Raley et al. 2019).

If people prefer to use the CTC for the purchase of large items, or as a form of forced savings, a single payment at tax time may be most useful. But a more regular payment schedule could better allow the CTC to be used to cover basic needs or to pay down debt (Maag, Congdon, and Yau 2021). Consumer-spending data among families with CTC-eligible children indicate that additional income from the monthly CTC payments was largely used on housing and food (Schild et al. 2022).

In 2021, most families received half of their CTC in monthly increments from July to December. Although it was possible to opt out of these payments, relatively few families appear to have done so (Government Accountability Office [GAO] 2022). After payments had been received, 45 percent of parents reported preferring the monthly payments, while 27 percent preferred to receive the credit as one payment at tax-filing time. The remaining parents expressed no preference. Families with low incomes were more likely to report preferring monthly payments than were other income groups (Maag and Karpman 2022).

An issue with delivering monthly payments is determining when payments begin and end. Some proposals suggest that monthly payments would begin at birth and proceed through a child’s 16th birthday. That system would deliver the same total benefits over a child’s lifetime as the existing CTC, but the timing of benefits will differ, particularly for children born later in the year. For simplicity’s sake, assume a benefit is available only during the first year of a child’s life and everyone files their tax return and receives any refund due on April 15. With an annual payment, the child receives the full year of benefits on April 15 in the tax year after the child’s birth. A child born on December 31 would receive the full year of benefits in just four and a half months, on April 15. At the other extreme, a child born on January 1 does not receive the full year of benefits for 16 and a half months under this system.

Under a monthly payment system, many children would receive less in their first year of life than under the annual payment system. That contradicts the evidence presented earlier on the importance of income for families with young children.

On the other hand, under a monthly delivery system, many children will receive more resources in their last year of credit eligibility. They would receive the remaining months of the CTC they are eligible for and begin receiving the smaller other dependent tax credit the year they turned 17, rather than receiving only the other dependent tax credit that year. That boost would likely increase their tax refund. To the extent that it corresponded to the end of high school, it could encourage college enrollment (Manoli and Turner 2018).

To offset losses in the first year of life for some children, policymakers have proposed providing larger CTCs at the time children are born. Under current law, adding a $2,000 “baby bonus” per newborn child to the CTC would cost about $6 billion each year.

Advancing payments also risks administrative errors. Eligibility for the CTC is determined retrospectively, after the tax year has ended. At that point, a family can properly determine their filing status, who will be in their tax unit, and the income attributable to the tax unit. Determining who was eligible to receive monthly payments in advance of filing a tax return could follow the practice used in 2021, which relied on the IRS using the latest information available to them at the time the payments were made. It could also allow families to fill out special forms to indicate their likely eligibility, as was the case for the Earned Income Tax Credit (EITC) prior to 2010, when an advanced option was available to some families. Either of these can lead to payments ultimately deemed errant when a tax return is filed after the year has ended. CTCs can change from one year to the next because of changes in a family’s income or the number of children eligible for the CTC.

In prior analysis, among families with children and with incomes below twice the poverty level, about 20 percent experienced a drop in the CTC of at least $500 from one year to the next (Maag, Airi, and Hunter 2023). Declines in income or the number of children in the family each account for about half of these situations. Most often, the drop in the number of children was because children aged out of credit eligibility, something that can be predicted.

Fully reconciling how much tax is owed with how much tax is paid would mean that families who received excess advanced CTC payments would be required to pay them back when they filed their tax returns. This happened when the advanced EITC was in place (Holt 2008). At the other extreme, families could be allowed to keep any errant payments. When the CTC was fully refundable in 2021, most families with low or moderate incomes were not required to repay errant credit payments. Not requiring families later deemed ineligible to repay the credit will increase the cost of any proposal to advance the credit (an example of this is documented in Splinter 2023).

Eligibility for the credit could also be based on prior-year information. The upside of this is that the risk of errant payments can be significantly mitigated. The downside is that payments are based on information that is potentially less reflective of a family’s current situation than the existing CTC.

Prioritizing Reforms

Research suggests that targeting benefits to children in lower-income families is a cost-effective investment (Ananat and Garfinkel, this volume; Garfinkel et al. 2022; Maag, Lou et al. 2023). As policymakers grapple with the CTC in the coming years, the most helpful reforms for families with low incomes are those that remove the phase-in of the credit entirely or focus on phasing in the credit faster for some or all people. Reforms that simply increase the maximum value of the credit will have minimal impact on families that already see their benefits limited by CTC rules around benefit phase-ins and refundability. However, for the CTC to have the same poverty-fighting effect as it did in 2021, both will be necessary. Families with low incomes must be given access to larger credits, and the credit must be increased to keep pace with inflation.

Reforming the credit to a monthly benefit is important to many families. But considerations need to be given to who is made better off, the administrative implications of changing the payment frequency, and rules for families who receive payments in advance for which they are later found to be ineligible.

Footnotes

Notes

Elaine Maag is a senior fellow in the Urban-Brookings Tax Policy Center and codirector of the Innovations in Cash Assistance for Children project. She is temporarily serving as tax policy advisor in the U.S. Department of the Treasury’s Equity Hub. Work for this article was completed prior to her joining Treasury.

Nikhita Airi is a research associate in the Urban-Brookings Tax Policy Center and a contributor to the Innovations in Cash Assistance for Children project and the State and Local Finance Initiative.

Sophie Collyer is a doctoral student in social welfare policy at Columbia University. Her research focuses on antipoverty policies at the national and local levels.