Abstract

Community reactions against organizations can be driven by negative information spread through a diffusion process that is distinct from the diffusion of organizational practices. Bank panics offer a classic example of selective diffusion of negative information. Bank panics involve widespread bank runs, although a low proportion of banks experience a run. We develop theory on how organizational similarity, community similarity, and network proximity create selective diffusion paths for resistance against organizations. Using data from the largest customer-driven bank panic in the United States, we find significant effects of organizational and community similarity on the diffusion of bank runs. Runs on banks are more likely to diffuse across communities with similar ethnicities, national origins, religion, and wealth, and across banks that are structurally equivalent or have the same organizational form. We also find stronger influence from runs that are spatially proximate and in the same state.

Disapproval of—or active resistance against—specific organizations is common and often spreads selectively. For example, during the diffusion of a bank panic, only a fraction of communities with banks actually experience bank runs (Greve and Kim 2014). The expansion of Wal-Mart stores has been met by the diffusion of protests against some of their store proposals but not others (Ingram, Yue, and Rao 2010). These studies have begun to examine diffusion of adverse reactions against organizations, but little is known about the mechanisms driving this process.

The spread of resistance against organizations can be seen as a selective diffusion process in which actions spread to a subset of organizations rather than the entire population. However, current research on selective diffusion emphasizes information that benefits organizations, such as technologies and innovations (Haveman, Rao, and Paruchuri 2007; Powell, Koput, and Smith-Doerr 1996); this work examines diffusion processes with organizations as active agents engaging in search and inter-organizational transfer of practices. In contrast, organizations are passive agents in the diffusion process driving resistance. The spread of negative news about an organization is driven by communication and interpretation among external stakeholders, such as individuals, groups, and communities opposing an organization or its practices. This distinction means that diffusion theory requires modification when applied to the diffusion of outcomes adverse to organizations. Notably, organizations try to counter the spread of resistance against them, often by spreading news about their good deeds (McDonnell and King 2013).

Disapproval of and resistance against organizations spread through the diffusion of potentially harmful information—for example, information about product quality problems and corporate misconduct—which we call “negative information.” External actors view this information as helpful, because it informs their decisions to avoid or act against an organization, whereas organizations view this information as negative. The diffusion of negative information involves the spread of information that organizations would prefer to keep concealed, or information wrongly associated with an organization, such as when misconduct by one organization puts similar organizations under suspicion (Jonsson, Greve, and Fujiwara-Greve 2009; Sharkey 2014). Interpersonal communication of negative information is seen in events ranging from product boycotts (Kamins, Folkes, and Perner 1997) to financial crises (Kaminsky and Schmukler 1999).

The diffusion of negative information is a cleanly defined phenomenon that allows us to test diffusion mechanisms involved in interpersonal communication. Specifically, it allows tests of the role of similarity judgments in the diffusion process. Interpersonal communication is also involved in the diffusion of information that benefits organizations, as seen in viral marketing (Berger and Milkman 2012), but this beneficial information spread is driven at least partially by organizational actions. Hence, organizations’ efforts would be endogenous to interpersonal communication among external stakeholders in the diffusion of beneficial information.

The diffusion of negative information is a phenomenon of interest because it has extensive consequences when it triggers reactions harmful to organizations. This diffusion can significantly undermine organizations’ viability, especially in sectors where reputation and legitimacy are of paramount importance, such as banking and pharmaceuticals. Also, spreading information about corporate misconduct can lead to “innocent” organizations losing customers (Jonsson et al. 2009). During a bank run, diffusion of rumors about runs on banks elsewhere can make external stakeholders decouple banks’ actual financial health from their likelihood of failure, putting healthy banks at risk of falling victim to a run (Dupont 2007).

Given the significant social and organizational consequences of diffusion of negative information, there is clearly a need to understand how it spreads, but research has not progressed beyond showing effects of recipient characteristics on diffusion speed (Greve and Kim 2014). In contrast, research on the spread of information beneficial to organizations has probed several mechanisms and processes by which diffusion takes place (Strang and Soule 1998). Our intention is thus to advance the literature by developing theory on how negative information about organizations spreads.

A good illustration of the diffusion of negative information is provided by the 1893 U.S. bank panic, the most prominent depositor-driven bank panic in U.S. history. A breakdown in trust between depositors and a bank may lead to mass deposit withdrawals, often referred to as a “bank run” (Smith 1991; Wicker 2000). For example, in 2008, depositors of two Swedish banks—Swedbank and SEB—rushed to empty their accounts after a rumor spread on Twitter that the banks were experiencing financial trouble. A bank panic occurs when runs quickly spread to a substantial number of banks, and this often triggers an economic crisis. An individual bank run is easy to explain, because banks typically have groups of customers who can communicate easily, and once some depositors start making full withdrawals, it is rational for others to follow suit (Diamond and Dybvig 1983). A bank panic is more difficult to explain, because bank runs spread not only to financially distressed banks but also to financially healthy ones. For a bank panic to occur, customers must judge that a run on a different bank means their bank is also vulnerable. Models of rational action are thus a poor fit to the spread of runs in the 1893 bank panic (Carlson 2005; Dupont 2007). 1

Diffusion of Negative Information

Diffusion Mechanisms

The release of negative information about firms is a common occurrence. On July 28, 2013, the online homepage of the Wall Street Journal carried news on the following: Glaxo employees being arrested for alleged bribery in China; Tepco being criticized for poor management of their nuclear accident site; J.P. Morgan retreating from its commodities business following regulatory attention; a Renfe train driver being held criminally responsible for a train crash in Spain; a political controversy around the latest movie from Ghibli Studios in Japan; and GM firing employees over a mishandled recall in India. Did any of these releases of negative information have an effect on the focal firm, on firms in the same industry, or on even unrelated firms? Given the frequency of such events, it is important to understand the effects of negative information and how it spreads, especially if it can lead to consequences as extreme as a bank panic.

Negative information associated with an organization spreads differently from information that offers direct benefits to an organization. Organizations actively seek out beneficial information, and may extract it by cultivating collaborative relationships and using inter-organizational ties such as alliances, exchange relations, and members’ interpersonal ties (Beckman and Haunschild 2002; Singh 2005; Whittington, Owen-Smith, and Powell 2009). The spread of beneficial information can be conceptualized as a diffusion process, with the organization as the focal actor, and the network centered on the organization as the main conduit for communication.

The spread of negative information follows a different path: it generally goes against an organization’s interests, undermines public trust, and leads to increased public scrutiny (Meyer and Rowan 1977). We thus conceptualize the spread of negative information as a selective diffusion process involving communication and interpretation by external stakeholders rather than the organization itself. This diffusion process is influenced by communication between external actors and the community within which the organization operates. Interpretation is crucial, because negative information about other organizations may or may not be seen as relevant to the focal organization. Relevance, in turn, is assessed according to measures such as similarity with the organization associated with negative information (Gaba and Meyer 2008; Wang and Soule 2012).

This theory on negative information spread does not newly introduce external actors to the diffusion process. External actors are also depicted in the diffusion of organizational actions seen as positive, as when occupational groups and social movement organizations contribute to adoption decisions (e.g., Briscoe and Safford 2008; Edelman 1990). Rather, the diffusion of negative information removes the organization as the driving force of the diffusion process. This is important for assessing whether external actors are effective sources of diffusion, and for examining the main features of such diffusion processes. To develop the theory, we consider the extent to which information is judged to be sufficiently negative to trigger action against an organization, and the routes of information transmission through which relevance judgments occur.

Whether a given piece of information is judged to be negative for an organization depends on multiple cues. Research on organizational misconduct emphasizes the role of social control agents—actors who represent a community and can impose penalties on behalf of that community (Greve, Palmer, and Pozner 2010). Much work on the spread of negative information about organizations has been conducted in contexts in which a legitimate social control agent, such as a regulator, exists to identify the negative information and the responsible organization. This is evident from research on automobile recalls (Rhee and Haunschild 2006) and the Enron scandal (Jensen 2006). However, stakeholders often make judgments on information using weaker cues, such as news reports or rumors. Negative information is especially damaging when the press reports it as scandal and it is associated with a high-status actor (Adut 2005). Both the conventional press and unedited information sources, such as online communities, can shape a negative view of an organization (Jonsson et al. 2009; Zhang and Luo 2013).

Once information about an organization is judged to be negative, stigma can spread to other similar organizations via a process of categorical judgment (Paetzold, Dipboye, and Elsbach 2008; Yu, Sengul, and Lester 2008). This is akin to the mechanism involved in the stigmatization of individuals (Pontikes, Negro, and Rao 2010). Negative information about an organization can have a contagion effect, because actors assess organizations they transact with based on multiple cues. This includes direct experience with an organization, but also perspectives shared by other stakeholders they interact with and observed outcomes from organizations with similar characteristics (Jonsson et al. 2009). A single adverse event experienced by an organization of a certain form can thus have a contagion effect, leading to a potential loss of trust in similar others (Iyer and Puri 2012; Jonsson et al. 2009). Categorical judgments should strongly influence reactions against organizations, because external actors lack the information necessary to accurately judge the relevance of information about one organization for another. Thus, external actors rely on informal stakeholder judgments about the similarity of easily observable characteristics.

As in any cue-based process, different individuals may draw different conclusions. Indeed, even organizations that are directly implicated in a negative event are subject to different reactions among their stakeholders, as opposed to blanket condemnation and withdrawal from transactions (Rhee and Haunschild 2006; Sullivan, Haunschild, and Page 2007). Organizations that are not directly implicated in the negative event will not be affected by it unless their stakeholders judge a connection to be important. This judgment is in part a function of sharing similar characteristics, and hence is outside the organization’s control. It is thus not surprising that even a major event, such as a bank panic, ultimately affects only a minority of banks.

The relevance of negative information about one organization to another is higher when the organizations are viewed as similar or closely related. When individuals evaluate whether negative information about another organization applies to the (focal) organization, they first assess how similar or related those organizations are. The key to understanding the diffusion of reactions against organizations thus starts with understanding how these judgments unfold (Larkey and Markman 2005; Tversky 1977). A sizable body of work examines how organizations choose target organizations for imitation (Strang and Soule 1998; Wang and Soule 2012), but surprisingly little is known about the mechanisms through which individuals judge an organization as relevant regarding negative information.

The judgment task can take many forms, but prior work on information diffusion suggests that people rely on three sources of information in assessing the relevance of organizations under scrutiny: (1) the similarity of organization-level characteristics between organizations; (2) the similarity of the communities in which organizations operate; and (3) the presence of observable links between organizations.

Each mechanism has distinctive strength in explaining the spread of negative information. The similarity of organization-level characteristics is consequential in the diffusion of negative information because external audiences use simplified heuristics in their judgments, due to the limited available information. This tendency to use heuristics should be weaker in the diffusion of beneficial information, because internal managers seeking such information likely have more fine-grained data that goes beyond simple organizational characteristics. The similarity of the communities in which organizations operate is another means to categorize organizations; links also help external audiences categorize organizations, because common links to third parties can be used to make similarity judgments.

Organizational Form and Relevance Judgments

A primary concern in judging negative information about a specific other (alter) organization is whether the information is relevant to the focal organization; that is, whether the latter is likely to be tainted by the reported adverse event. Seen as a prediction or heuristic task, this judgment should be shaped not only by categorical similarity of the alter and focal organization, but also by variance within categories (Hogg, Terry, and White 1995; Tajfel and Turner 1986). Heuristics in processing information strongly influence the diffusion of negative information. Individuals tend to overweigh the shared category and underestimate variance within the category (Higgins and Bargh 1987; Smith and Zárate 1992); this makes diffusion faster within same-category organizations (Kuilman and Li 2009; Strang and Soule 1998). This tendency is further amplified if the information being processed is negative, because individuals are risk averse (Thaler et al. 1997).

Individuals often use simple cues, such as categorization rules, that can have widespread effects in the case of negative information. Categorization can be shaped by the media (Roehm and Tybout 2006) and simple cues like geographic origin (Phillips 2011) and size (Jonsson et al. 2009; Love and Kraatz 2009). During a banking crisis, for example, small banks tend to be more vulnerable to runs than large ones, because big banks are thought to be “too big to fail” and are categorized as low-risk (FDIC 1997).

A frequently used rule in categorical judgment—of particular interest to organization theorists—is organizational form (Yu et al. 2008). Although many organizations could, in principle, experience the same outcome, finer subdivisions may provide cues to make judgments about their vulnerability. For example, all types of deposit institutions could experience a bank run, but if the observed runs are initially associated with one type of institution (e.g., savings and loans), only that type of institution may be considered vulnerable. This was seen in the 1985 Ohio savings and loan crisis, which spread to savings and loans in other states but not to other forms of financial institutions in Ohio (Cooperman et al. 1995). Similarly, during the 1873 banking panic in New York City, the loss of depositor confidence was confined to savings banks: nearly all savings banks experienced a run, but only one national bank did.

This suggests that individuals see organizational form as useful in categorizing the level of risk faced by deposit institutions. Categorical judgments are a common heuristic, but categories are a poor match with complex issues (e.g., estimating a bank’s failure risk). The greater influence of same-form members indicates that customers rely on heuristics rather than deeper reasoning when they assess a bank’s vulnerability. In line with these arguments, we posit the following:

Hypothesis 1: Negative information associated with an organization has greater influence on members of the same organizational (sub)form than on members of other (sub)forms.

Communities, Communication, and Relevance

A unique feature of the diffusion of negative information is that it is driven by communication and relevance judgments among an organization’s stakeholders. The communities in which organizations operate are therefore particularly important in the diffusion of negative information. Stakeholders not only have strong-tie networks with geographically proximate individuals in their local communities, but they also establish weak-tie networks that are more dispersed and can be used to obtain scarcer information from other communities (Granovetter 1974). The high salience of negative events activates these communication networks when an organization experiences a crisis (Pratto and John 1991). The question then becomes whether the transmitted negative information passes the relevance test required to trigger a reaction against the organization being evaluated.

For organizations heavily embedded in local communities, such as banks (Kono et al. 1998; Marquis and Lounsbury 2007), community characteristics are especially important for relevance judgments. Local community structure influences organizing attempts both for and against organizations, leading to either support of organizational founding or resistance against it (Greve, Pozner, and Rao 2006; Ingram et al. 2010; Marquis and Lounsbury 2007). Community connections through geographic space, as well as social and economic ties, drive communication and relevance judgments (Gaba and Meyer 2008; Hedström 1994). In addition, internal social structures that yield varying degrees of community support for organizational founding and operation (Greve and Rao 2012; Schneiberg, King, and Smith 2008; Sorenson and Audia 2000) affect how community members respond to negative information about external organizations. It thus makes sense for individuals to judge the relevance of negative information associated with nonlocal organizations with reference to the characteristics of the communities in which they are embedded. The more similar an organization’s community is to that of the individual’s local community, the more relevant the negative information for judging the risk that a similar adverse event will occur in one’s local community. Prior work shows that community similarity judgments affect the diffusion of adverse interpersonal actions such as ethnic violence (Braun and Koopmans 2010), and they may also affect adverse reactions against organizations.

Community-level characteristics are important for relevance judgments, because they shape individuals’ social context. Processing negative information associated with an organization influences (and is influenced by) the level of trust between stakeholders and organizations, so social characteristics that create division and distrust affect relevance judgments. Although these factors do not necessarily have diagnostic value for predicting actual relevance, they are well-worn cognitive paths for making categorical judgments about others.

We thus arrive at the issue of identity and in-group preference (Tajfel and Turner 1979). These preferences influence judgments, because individuals with out-group bias tend to ascribe the cause of a negative event in another community to its members if they have very different identity-relevant characteristics (Perdue et al. 1990). Stakeholders often assume that a negative event occurring in a dissimilar community will be less likely to happen in their own community. In contrast, it is harder to attribute blame for a negative event to a community similar to one’s own. Stakeholders will thus assign blame for the negative event to the alter organization when it belongs to a similar community, and conclude that a similar organization may cause a similar event to occur in their own community.

In addition, communities with similar members tend to exchange more information. Once members of a community have deemed another community as relevant due to shared characteristics, members of those communities observe each other more (Haunschild and Miner 1997), resulting in increased information exchange among them. Also, similarity of demographic and cultural characteristics between communities can directly influence information flow through social ties. Residents of communities with similar characteristics are more likely to be connected through one or more social networks than are people who reside in communities with different characteristics. For example, individuals living in two communities with large groups of immigrants from the same country may be connected through family, school, or regional ties (Kelly and Ó Gráda 2000). These ties facilitate communication, increasing the information flow between them. Such increased information flow may enable the diffusion of negative information in a bank panic, prompting the spread of bank runs. This leads to our second hypothesis:

Hypothesis 2: Negative information associated with an organization has a greater influence on organizations in communities with similar identity-relevant characteristics.

To judge whether two communities have similar identity-relevant characteristics, people must first identify characteristics that are identity-relevant and then assess how the communities differ on those characteristics. The distribution of population characteristics is informative, because people differ along identity-relevant dimensions; community members are usually aware of the most common population group in a community and the diversity of the community. We examine four identity-relevant characteristics: ethnicity, national origin, religious affiliation, and wealth. Ethnicity is fundamental to individual identity and communication boundaries, and it affects interpersonal influence. Ethnic diversity negatively affects trust and other attitudinal indicators of social cohesion (Miguel and Gugerty 2005). Similarly, national origin is important in a nation with a large immigrant population, such as the United States, as reflected in community structures (e.g., clubs) having uniformity of national origin (McPherson, Smith-Lovin, and Cook 2001). Religion supports intragroup trust (i.e., interpersonal trust within the religious group) and reduces intergroup trust (i.e., interpersonal trust across religious groups) (Iannaccone 1994). Religion can thus play a critical role in the diffusion of negative information because it affects whose opinions one trusts. Church services also offer a time and physical space for people to meet, affirm their shared identity, exchange information, and interpret ambigious situations to arrive at a shared understanding. Finally, wealth differences are related to social divisions within a community (Alesina and La Ferrara 2000) and are an important way to characterize similarity between communities.

Network Ties, Communication, and Relevance

Inter-organizational networks play a part in the diffusion of negative information, but their role differs from that in the diffusion of innovations, where inter-organizational ties facilitate the transfer of beneficial information. In the diffusion of negative information, stakeholders draw inferences from visible network connections and interpret a connection as indication that a negative event in an alter organization increases the risk of the focal organization experiencing a similar event. Organizations linked in the same network are perceived to share similar characteristics, and hence have higher risk of experiencing a similar event.

For a network to have effects, it needs to be visible enough to link organizations in the minds of stakeholders regardless of whether there is actual risk transfer between them. Because stakeholder judgments are based on similarity considerations rather than actual risk transfer, predictions are not driven by centrality or brokerage, although these network concepts typically affect information-transfer. Rather, what matters is how individuals categorize organizations based on their connections to a third party. An organization connected to an alter organization involved in a negative event may be seen as having contributed to the event, or as being at risk of being influenced by the event. Awareness of such judgments can be inferred when organizations attempt to escape from tainted third parties (Jensen 2006) as a way of avoiding categorical judgment. Based on such a categorization, it is natural to conclude that organizations connected to the same third party are also at risk.

In network terms, the focus on third-party connections highlights the role of structural equivalence in a network (White, Boorman, and Breiger 1976). Blocks of structurally equivalent organizations can be assumed to share risks for two reasons. First, firms establish network ties primarily to support economic activities. Thus, it is reasonable to assume that visible network ties represent economic dependencies—which in turn imply shared risk (Chung, Singh, and Lee 2000; Gulati 1999). Second, organizations typically make similarity judgments when vetting alters with whom to establish network ties (or stakeholders can assume they do), which also implies shared risk (Jensen and Roy 2008; Stuart 1998).

In banking, structural equivalence is seen through correspondent banking networks. A national correspondent banking system, centered on New York, first emerged in the 1850s. Banks could enter into correspondent relations with other banks to secure check clearance for checks from banks in other localities. This system simplified check clearance: such services were handled by correspondent banks located in more central banking areas, instead of having each bank correspond directly with the bank issuing the check. The correspondent banking network dramatically increased the efficiency of the banking system, but many believe it also facilitated bank disturbances (Tallman and Wicker 2010). Because banks in correspondent banking networks are linked through bank balances, one bank’s failure could make other banks in the network vulnerable. Indeed, the correspondent banking network has been blamed for the diffusion of bank runs in the bank panic during the Great Depression (Wicker 1996).

The correspondent banking system did not directly transfer financial vulnerabilities between banks during the 1893 bank panic (Carlson 2005), but customers may have viewed the links between their banks and correspondent banks that experienced a run as a threat. Bank customers were usually aware of the correspondent banks associated with their banks, because the location and reputation of correspondent banks were important factors in choosing a bank. Bank customers may not have been aware of all runs on the entire correspondent network, but runs on nearby banks with shared correspondents must have been highly visible. Runs on geographically proximate banks with shared correspondents could make bank customers concerned about a chain reaction and prompt them to act. Building on these arguments, we posit the following:

Hypothesis 3: Negative information associated with an organization has greater influence on structurally equivalent organizations.

The Bank Panic of 1893

The bank panic that occurred in the United States between April and August of 1893 triggered a devastating economic crisis that saw real earnings decline by 18 percent from 1892 to 1894 (Hoffmann 1956). It provides an appropriate setting for testing our hypotheses on information diffusion among individual stakeholders, because it was primarily caused by panicked depositors rather than weaknesses in the banking system. Scholars consider it the most purely customer-driven bank panic in history (Carlson 2005). Despite the efforts made to control the panic and limit the consequences for individual banks, 503 banks were suspended between May and August 1893. Two thirds of these banks failed; the rest recovered. The bank panic was concentrated in the Western and Midwestern states and diffused quickly (see Figure 1).

Diffusion of the 1893 Bank Panic

The direct cause of a bank run is doubt about its liquidity, which prompts depositors to withdraw their savings before the bank runs out of funds. Illiquidity means having insufficient cash to meet anticipated requirements now. Banks lend money for longer terms (e.g., mortgages) than they borrow it (e.g., current accounts or interbank loans), making them vulnerable to liquidity problems unless reserve loans or interbank loans can step in. 2 A rational customer would join an ongoing bank run (Diamond and Dybvig 1983), because a run can leave any bank illiquid, including banks that would otherwise have been financially sound in the long term. Because information that a bank run is ongoing spurs justified fears of illiquidity, runs are accelerated by interpersonal communication networks among depositors (Iyer and Puri 2012). Studying a run on a New York bank, Kelly and Ó Gráda (2000) found that networks of personal acquaintance play a crucial role in propagating runs: they describe one anecdote in which neighbors living on the same street all showed up at the bank on the same day to close their accounts. A bank panic is different from a bank run, however, because a bank run does not necessarily spread to other banks.

The 1893 bank panic has been attributed to diffusion among depositors at different banks (Wicker 2000). Research shows that the number of runs experienced by other banks increases the probability that a focal bank also experiences a run, and a bank in a less diverse community has a greater probability of a run (Greve and Kim 2014). Using data on banks in Kansas during the 1893 bank panic, 3 Dupont (2007) reports that financial indicators for solvency and liquidity did not predict deposit movements, suggesting that the financial health of individual banks had little impact on their risk of experiencing a run. These studies reflect that deposit withdrawals are a reaction to distrust in banks, as opposed to a calculated response to actual financial risk.

For the relevance judgment mechanisms we proposed to take place, depositors in 1893 should have had access to information about bank runs elsewhere. Local newspapers were an important source of news and were central to the diffusion of bank runs in the 1893 bank panic. For example, a search of a digital archive of old Colorado newspapers using the keyword “bank run” yielded 1,661 results for 1893. These articles offered relatively comprehensive information about the bank runs, although the thoroughness in their geographic reach and reporting varies.

One potential issue in studying bank runs is the presence of deposit insurance. Deposit insurance guarantees the safety of deposits in the event of bank failure, which makes a run on a bank less likely even when customers perceive a high risk of failure. This is not a concern for our study, because no deposit insurance plans existed in 1893. Six states had implemented deposit insurance plans as early as 1829, but all were terminated by 1866, and states did not attempt deposit insurance again until the early 1900s (FDIC 1998).

Another issue to consider in studying bank runs is banks’ responses. Ample anecdotal evidence shows that banks take actions to avoid being stigmatized by the news of runs on other banks, which could slow down or even put a brake on the contagion of bank runs. An article published in the Aspen Daily Times on July 21, 1893, offers an example: “There is no reason why Aspen people should get excited over the situation here. All of the Aspen banks are backed by conservative business men whose business careers have not been marked by wild speculations or daring ventures. There is a growing feeling that the financial houses of Aspen are all right.” This quote, which is typical of newspapers at the time, underscores the efforts made to counter negative information about banks. Their effectiveness is unclear, because newspapers supporting local banks against a panic can be seen as a form of elite mobilization, which does not always work (Yue 2015). However, banks’ efforts to combat negative information imply that the diffusion of negative information occurred despite their resistance, making our empirical test more conservative.

Data Sources and Variables

Sample and Data

We collected data on all bank suspensions that occurred in 1893 from Bradstreet’s January 1894 issue. Rand McNally’s Bankers’ Directory (the 1892 volume) furnished us with the name of the village, town, township, or city of the 6,600 banks in our sample. We collected data on banks from 22 Midwestern and Western states (Arizona, California, Colorado, Idaho, Indiana, Illinois, Iowa, Kansas, Minnesota, Missouri, Montana, Nevada, New Mexico, North Dakota, Ohio, Oregon, South Dakota, Utah, Vermont, Washington, Wisconsin, and Wyoming) to reflect the distribution of the bank panic, which was more pronounced in the Midwest and the West relative to the East. We matched banks’ locations from this data source to our census data.

The 1890 census provided us with county-level demographic information, which we then mapped to each bank’s location through two steps: (1) We matched 1890 places and counties to 2000 places and counties, respectively. This was coded automatically when names remained unchanged, and by hand when name changes occurred due to mergers or splits. (2) We calculated an allocation factor based on the census and used this to map county-level demographics to each place. Most places were fully inside one county and hence are assigned a factor of 1; places that spanned county boundaries were assigned factors of less than 1. This allowed us to allocate county data in proportion to the place populations inside each county. Finally, we obtained stock and bond values from monthly issues of Bradstreet’s.

Measures

Dependent variable

Our dependent variable is the event of a bank in the sample experiencing a run. Because direct records of bank runs are not available, we used bank suspensions to identify runs, consistent with prior studies on bank runs (Calomiris and Mason 1997; Carlson 2005; Dupont 2007). A suspension of convertibility, also known as a bank suspension, occurs when banks experience a run and temporarily abstain from deposit withdrawals but persist in activities that do not negatively affect their liquidity. Bank suspensions help targets of runs avoid immanent failure by giving them time to acquire capital to repay their depositors. A bank suspension is not the same as a bank failure. Bank suspensions occur when a bank loses liquidity due to mass withdrawals (Calomiris and Gorton 1991; Carlson 2005; Dupont 2007), whereas bank failures occur when banks become insolvent.

Bank suspensions are a well-accepted indicator of bank runs in finance, economic history, and banking research (Calomiris and Mason 1997; Carlson 2005; Dupont 2007), but they do not always indicate runs because they can also be caused by other financial and regulatory reasons. In the 1893 bank panic, historical evidence and banking research explicitly attribute the vast majority of suspensions to bank runs. For example, the regulating agency reported that “[m]any banks after paying out all the money in their vault were suspended and passed into the hands of the Comptroller. With a full knowledge of the general solvency of these institutions and the cause which brought about their suspension, the [suspension] policy was inaugurated” (Annual Report of the Comptroller of the Currency 1893:10). In addition, 503 bank suspensions occurred in only four months during the 1893 bank panic, the highest frequency in U.S. history. Because bank suspensions rarely occur, this dramatic increase in the number of bank suspensions can be unambiguously linked to bank runs.

Same-form bank runs

To test Hypothesis 1, we created same-form runs using the four types of banks that existed in 1893: (1) national banks, (2) state banks, (3) commercial banks, and (4) savings banks. We measured this variable using the distance-weighted cumulative number of prior runs on banks of the same form as the focal bank since the start of the bank panic.

Similar-community bank runs

To test Hypothesis 2, we created a variable operationalized as the number of prior runs weighted by the social similarity of the two communities. For each community characteristic, we used the following formula:

Here, Wij is the weight applied to the count of runs in alter community j for ego community i. The term inside the summation is the social distance between communities, defined as the sum of the squared difference of proportions in each category of the community characteristics. The summation is done over all categories k of the characteristics. The maximal distance is 2, which occurs when individuals in both communities are completely in two separate single categories. The distance measure produced by the summation is divided by 2 to scale between 0 and 1, and is subtracted from 1 to yield a proximity (rather than distance) measure.

Using census data, we calculated ethnic similarity, national origin similarity, religious similarity, and farm size similarity. Ethnic similarity uses the distribution among five ethnic groups (white, African American, Chinese, Japanese, and American Indian). National origin similarity uses the 40 census categories of national origin, which is precise for large origin groups (e.g., European nations such as Ireland or Germany) and regional for less frequent national origins (e.g., Central America). Religious similarity is based on the census categories of churches; there are 58 categories of churches, reflecting the highly diverse religious life at the time and the high priority given to accurate church mapping. Many of these subcategories belong to Protestant churches, but the distinction among Protestant churches mostly disappeared after the Protestant religious revival movement, the Second Great Awakening. This fine-grained delineation may overlook broader similarities across churches, so we recoded it to six categories using the religious classification schedule developed by Steensland and colleagues (2000): Catholic, Mainline Protestant, Evangelical Protestant, Black Protestant, Jewish, and other. 4 Farm size similarity uses the distribution among seven farm sizes, ranging from less than 10 acres to more than 1,000 acres. These measures are highly correlated (above .95), so we made a joint measure of community similarity by taking the sum of the four measures. We also estimate some models probing which dimension of community similarity is more influential. A potential concern in the analysis is whether community similarity would be conflated with distance. This is not likely to significantly affect our analysis, because there is little shared variance between the similarity and distance measures (10 percent), and we control for distance by weighting the effect of each bank run. However, we cannot separate these effects with complete accuracy.

Correspondent-group bank runs

To test Hypothesis 3, we created the correspon-dent group bank runs variable using data on the network of correspondence banks. In establishing correspondent banking relationships, banks had several central banking areas to choose from and could choose among banks within each area. For example, banks in the Midwest and West could choose between nearby financial centers (e.g., San Francisco) and those located further East (e.g., New York). Many banks maintained multiple correspondent relationships. The joint choices of correspondent locations and banks produced a network that we coded and partitioned into structurally equivalent components using the Concor algorithm, as implemented in UCINET (Borgatti 1996; White et al. 1976). This grouping captures diffusion patterns if customers perceived that different localities or correspondent banks represented different levels of security (or alternatively, risk). Bank customers were likely aware of runs on geographically proximate—but not distant—banks with shared correspondents, because only a small portion of bank customers did business beyond the state boundary. We therefore considered only bank runs within the same cluster of correspondent banks that occurred within the same state as the focal bank. Concor creates components by dividing the network into half each time based on the structural equivalence of nodes. Because the banks and correspondents were so numerous, we used a fine partition with four Concor divisions in the analysis, but our results were robust using a coarser partition of three divisions. Correspondent-group runs was operationalized by the cumulative number of runs experienced by banks located in the same state as the focal bank and belonging to the same partition of the correspondent bank network. The names of correspondent banks were unreadable for 39 banks; we omitted these banks from the analysis.

Control variables

Because different types of banks were subject to different regulations, there could be a systematic difference in the likelihood of experiencing bank suspensions among them. The bank type could also affect customers’ confidence and risk assessment. We thus controlled for the type of bank: national bank, state bank, and savings bank. Our sample has 24.1 percent national banks, 10.5 percent state banks, 5.7 percent savings banks, and 59.7 percent commercial banks (used as the baseline category in our analysis).

Customers may be less likely to run on an older bank, because they may have more confidence in its financial security. Hence, we used bank age as the natural logarithm to control for this attribute. Similarly, customer perceptions may be shaped by their banks’ size; customers may assume that larger banks have more resources and thus less financial challenges, which could affect the probability of a run. A bank’s level of capital is particularly important during a banking crisis (Curry et al. 1999). Thus, we used paid-in capital to control for the effect of bank size as it refers to the funds banks acquire from equity.

Bank density is the number of banks in a place, and we used this together with its squared term (bank density squared/100). This would reflect a U-shaped relationship if the pattern of bank runs in bank panics paralleled that of organizational failures predicted by the literature in organizational ecology (e.g., Carroll and Hannan 2000). Urbanization is the proportion of people living in urban areas in a county. Proportion farm families is the proportion of families in a county who are farmers. Individuals with a mortgage loan as well as a deposit account with a bank are less likely to run on the bank, because the loss of their deposits could be offset by their loans, so we added proportion families with mortgages, which is the proportion of families with mortgages in a county. We also considered other county-level control variables, but we omitted them from the model because they did not have significant effects and did not affect our findings.

We also included a monthly stock value factor that we calculated using three stocks with the largest market capitalization at the time (Atchinson, Topeka, and Sante Fe Railroads; Southern Pacific Company; and Western Union Telegraph) and government bonds (Government 4s coupon 1907 expiry; and Government 6s currency 1898 expiry). We used the monthly stock value factor to control for the overall economic climate during the time period. This factor is the first that emerged from the principal factor analysis and accounted for .764 of the total variance when all variables loaded positively.

We created variables to measure the social composition of a community in case there was a main effect of social composition in addition to the composition similarity effect posited in the hypothesis. We used the same categories as in the similarity measures, and we calculated each variable using the Blau index (1 – Σp2, where p is the category proportion). Thus, ethnic diversity is the Blau index of the distribution of the same five ethnic groups as the similarity variables. Religious diversity is the Blau index of the membership of six categories of churches in the county. National origin diversity has no effect on the likelihood of a run; hence we omit this variable to present more parsimonious models.

Finally, we used farm size inequality, which we calculated using a Gini index adjusted for categorical data (Gastwirth 1972). This reflects the uneven economic distribution by encapsulating the average gain an individual would make if given the chance to switch places with someone else. We calculated the Gini Index using farm size categorizations from the census (less than 10 acres, 10 to 19 acres, 20 to 49 acres, 50 to 99 acres, 100 to 499 acres, 500 to 99 acres, and 1,000 acres and over):

Here,

If the type of customers associated with different types of banks were substantially different, their reaction to news about other same-form banks experiencing runs might have been systematically different, influencing our test for Hypothesis 1. This calls for controlling for the types of customers of each bank, but such fine-grained data are not available. However, our analysis is likely unaffected by this, because examination of communities with only one or two bank types did not show significant association of the type of customers and the bank type.

We arrived at a final analysis dataset of 6,600 banks that were at risk of experiencing a run over a time period of 153 days after removing missing data. The average time at risk was 149.6 days, and banks had a 5.9 percent probability of being the target of a bank run: 391 banks out of the 6,600 banks experienced a run. Our dataset yielded 707,304 observations after splitting spells to update the covariates (the covariates are updated every time a bank run occurs).

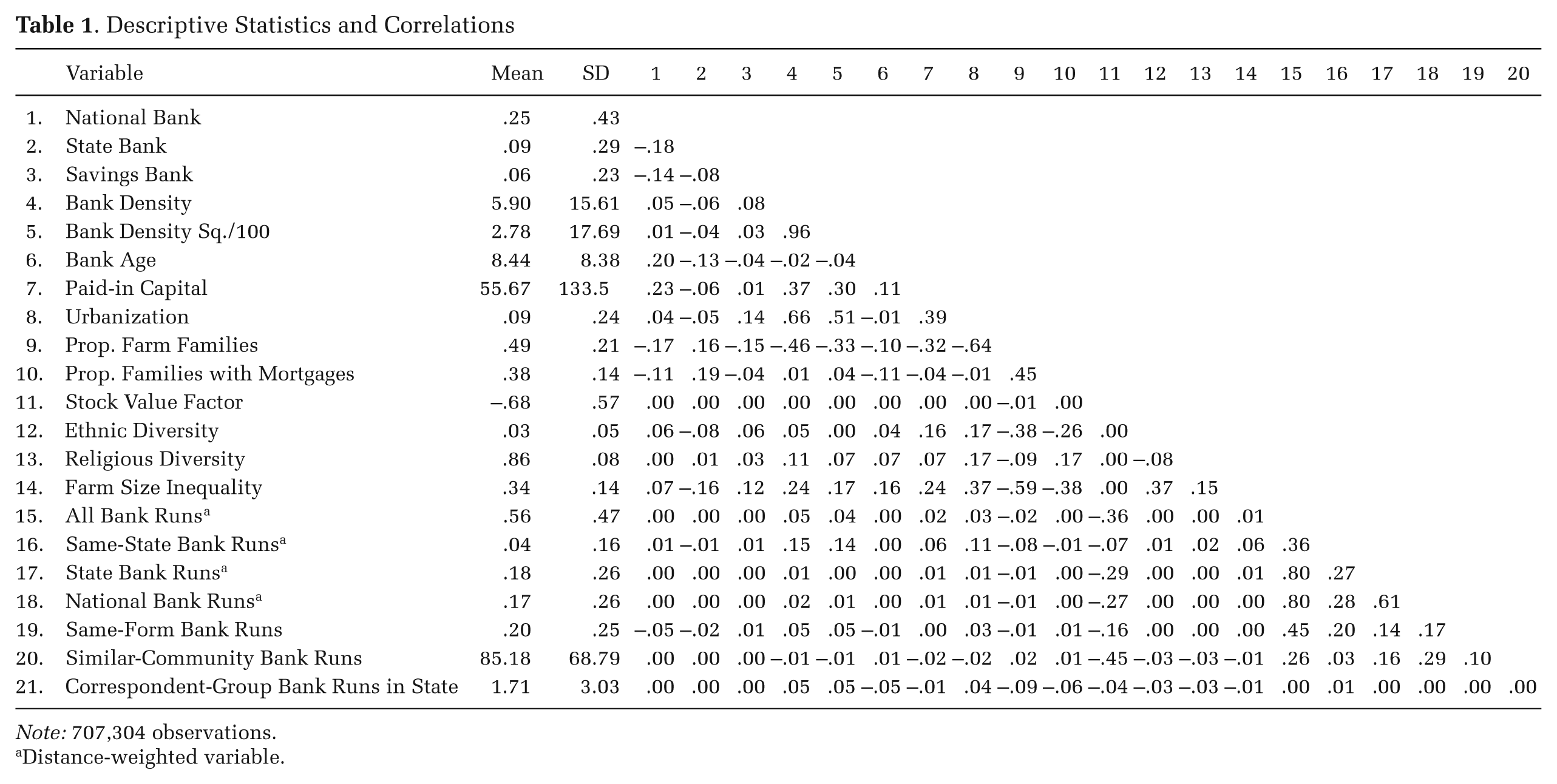

Table 1 provides the descriptive statistics and zero-order correlations of all variables. The diffusion variables change over time, and as a result have low correlations with the control variables but positive correlations with each other. For the last two variables in the specification, correspondent-group runs and community-similarity weighted runs, the correlation coefficients of the untransformed variables are sufficiently high that it is appropriate to use orthogonalization (Stata command orthog), which is a transformation that expresses correspondent group orthogonally to community similarity. With this transformation the variables are not correlated, as the table shows, and it is not necessary to consider correlations of the variables when assessing the effect of each one.

Descriptive Statistics and Correlations

Note: 707,304 observations.

Distance-weighted variable.

Methodology

The bank panic of 1893 occurred between April 1 and August 31: 391 of the 407 bank suspensions in the sample states occurred during that time period. Our analysis lets each bank be at risk of being the target of a bank run from the first day of that time period until it experiences a run or is right-censored. We use an exponential hazard rate model and factor in the distance-weighted influence of all prior bank runs (distance-weighted all bank runs). This is akin to a multiplicative heterogeneous diffusion model (Strang and Tuma 1993) where the probability of a bank run is calculated by multiplying the earlier runs’ contagion effect and each bank’s susceptibility. To prevent bias due to estimating the model on a sample of states rather than the entire population, we included bank runs outside the 22 sample states when calculating the independent variables (Greve, Tuma, and Strang 2001).

We determined the distance-weighting of the influence of runs empirically. Using a kernel regression on city-pair fastest-jump infection routes, we confirmed that the contagiousness of a run significantly decreased as the distance between a city-pair increased. We applied multiple forms and parameter values before choosing the best fit by the Bayesian Information Criteria (BIC) value (Raftery 1995). In the final analysis, we specified the best-fitting inverse-log specification of the distance-weighted influence:

Here, p refers to prior panics and the influence variable has the associated coefficient γ. X is the conventional regression function of bank and community variables with associated coefficients β.

We created new spells for all banks when a new bank run occurred and recalculated the contagion term to factor in all prior runs. This results in many observations of short duration but with accurate independent variables, because the contagion term was immediately updated. We also split the spells at the beginning of each month to factor in the financial market variable. We adjusted our standard errors for clustering on the bank as a result of repetition of the same bank across many spells. We alternatively adjusted the standard errors for clustering on counties and found consistent findings.

Results

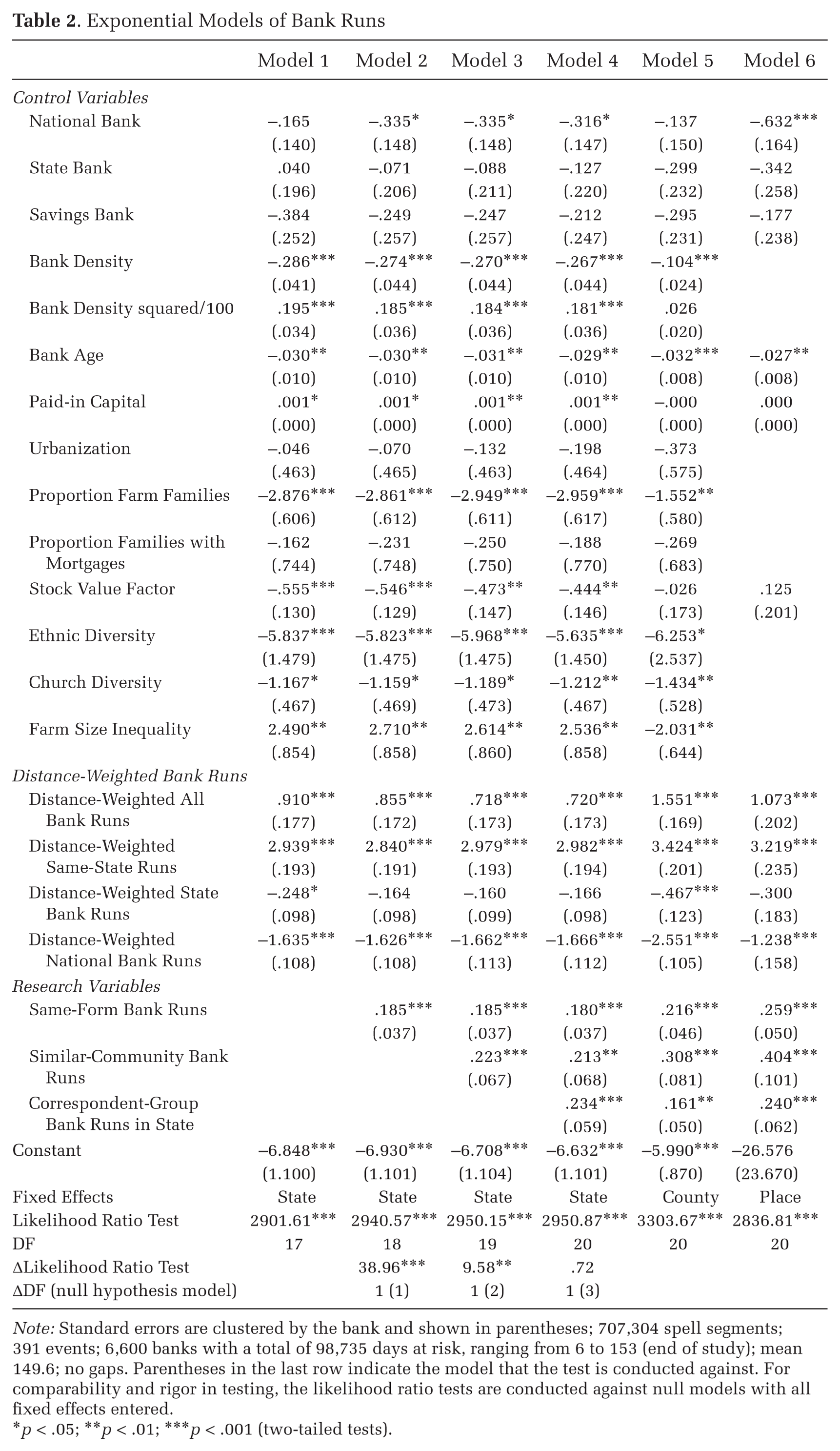

Table 2 shows results of the hazard models on bank runs. The model is built up hierarchically, from Model 1 with only control variables to Model 4 with all hypothesis-testing variables. Models 4, 5, and 6 are the same except the fixed effects are progressively finer. Model 4 has state fixed effects, Model 5 has county fixed effects, and Model 6 has place fixed effects. In Model 6, all covariates that do not vary at the place level are dropped, because they are perfectly collinear with the fixed effects. This approach of adding covariates first and then refining the fixed effects allows a check for whether the coefficient estimates are stable when the model is extended. This indeed holds, except the distance-weighted state bank runs lose significance in Models 2, 3, 4, and 6.

Exponential Models of Bank Runs

Note: Standard errors are clustered by the bank and shown in parentheses; 707,304 spell segments; 391 events; 6,600 banks with a total of 98,735 days at risk, ranging from 6 to 153 (end of study); mean 149.6; no gaps. Parentheses in the last row indicate the model that the test is conducted against. For comparability and rigor in testing, the likelihood ratio tests are conducted against null models with all fixed effects entered.

p < .05; **p < .01; ***p < .001 (two-tailed tests).

The control variables mostly show expected findings. The density dependence of bank runs is the same as regular competitive density dependence for failures (U-shaped); higher stock market value produced a lower rate of bank runs; and national banks (which had greater reserve requirements) had fewer bank runs. It is surprising that paid-in capital increased bank runs, because this indicates that banks with more financial resources were more vulnerable to runs, but this would be consistent with the effect of heuristics on bank runs. Larger banks were more prominent and consequently more vulnerable to runs, even if they were also financially more secure. The distance-weighted bank runs shows the expected positive effect. Runs on national banks had a weaker effect than runs on other types of banks, possibly because national banks were so different from other banks that customers did not consider them much when making categorical judgments. Communities with high ethnic diversity were less likely to have bank runs, perhaps because weaker social ties across ethnic groups reduces the likelihood that community members will agree a bank is in crisis (Greve and Kim 2014).

The hypothesis tests provided consistent results across the models, so it is enough to discuss Model 6. Runs on the same form of banks as the focal bank show a significantly stronger effect than the combined bank runs, indicating that customers did in fact see the four types of banks—national, state, commercial, and savings banks—as different. Customers were more likely to run on their banks if the same type of bank had experienced a run elsewhere. This supports Hypothesis 1. Similar-community bank runs had a positive and significant coefficient. This indicates that bank runs in communities with similar characteristics as the focal community had greater influence in the probability of the focal bank’s experiencing a run, compared to runs in communities with dissimilar characteristics. This provides support for Hypothesis 2. Finally, correspondent-group runs in the same state also show a positive and significant effect. This indicates that diffusion of bank panics was influenced by a shared position in the network of bank correspondent relations, supporting Hypothesis 3.

Note that these coefficient estimates are of similar magnitude. The orthogonalization gives the last two variables a unity standard deviation, so similar coefficient magnitude directly implies similar effect strength for similar-community and same-correspondent group runs. Same-form runs have one-quarter the standard deviation, so the similar coefficient estimate means the effect is weaker. This suggests that form, the broader (but possibly more relevant and salient) organizational characteristic, is less influential than the finer distinction of community characteristics and shared network ties.

A question left unresolved by the high correlation of the different community characteristics is which is more important for diffusion. We examined this issue in more detail but do not report the models here to save space. First, all four characteristics had a statistically significant effect when entered on their own. In these models, the Bayesian Information Criterion gave positive evidence that religious similarity had worse fit than the other three characteristics. Models with two similarity variables at a time show that ethnic and national origin similarity remain significant most often, but economic structure is also significant. Although this is a crude approach for identifying which of a set of highly correlated variables gives the best model fit, it provides consistent evidence that ethnic and national origin similarity are the most important identity-related characteristics in these data. This result could be context specific, but the consistent empirical support from multiple community similarity measures implies that the finding that similarity of communities affects the diffusion of negative information is likely generalizable.

The magnitude of these effects is moderate for a single bank run but increases substantially when there are many bank runs. For example, Chicago is 1,023 miles (1,647 km) from Aspen, Colorado, so a bank run at a Chicago bank will increase the hazard rate of a bank run in Aspen by exp(1.073/ln[1647]) – 1 = 15.5 percent. These effects accumulate quickly as a bank panic progresses, and five runs in Chicago would double the hazard rate in Aspen. Although this is a large effect, it is not unrealistic. Bank runs are extremely rare under normal conditions, but in a bank panic they become epidemic. The 1893 bank panic we modeled here was one of the most contagious in U.S. history in terms of the speed of contagion and the number of banks involved in runs.

Figure 2 illustrates the other variable effects as a function of proximity between the focal bank and a bank with a run. For ease of interpretation, the effect of a bank run two standard deviations of the distance away from the focal bank is set to zero, but the actual number would depend on the distance. The horizontal axis varies the distance by two standard deviations, and the solid line shows how the effect increases as the bank run comes closer, peaking just below a 3.5 percent increase in hazard rate. Any run will have this effect, so the other curves incorporate the influence of one bank run and add the effect of same form, similar community, or same correspondent group one at a time. The dot-and-dash line shows the effect of a bank in the same group of correspondent banks. Although statistically significant, the effect is substantively small and peaks only just above a 3.5 percent increase in the rate. The dotted line shows the effect of a similar community, where “similar” is cautiously taken to mean a community one standard deviation above the mean similarity. Even at this low level, the effect is strong, with a peak at a 4 percent increased rate. If the similarity were increased to two standard deviations above the mean, it would peak at 4.6 percent. Finally, the dashed line shows the effect of a panic in the same form. This effect is also distance dependent, and as a result it is greater than the similar-community effect up to .5 standard deviations greater distance but smaller thereafter. The graph clearly shows that the effects modeled here have similar magnitudes, but the correspondent effect is weakest.

Bank Run Hazard Rate Increase from a Single Bank Run

We note three final points about these effects. First, Figure 2 was made assuming that the bank runs occur in a different state. As the large coefficient for same-state bank runs shows, the increase in rate is much greater for bank runs in the same state. A graph showing the same-state effect would have steeper slopes than Figure 2, with curves peaking at an over 14 percent increase in risk. Second, each curve in Figure 2 is made by adding the covariate effect to the effect of a single bank run, which means that for a bank with multiple effects (e.g., similar-community and same correspondence group) the hazard rate would increase further. Third, many distances are outside the two standard deviation interval, so the horizontal axis of the graph could have been made wider. For example, a four standard deviation difference in distance would mean the closest same-form bank run had an 8.7 percent greater effect instead of the 4.3 percent greater effect shown in the graph.

These findings are interesting because they move beyond the mechanical view of diffusion as the social equivalent of an epidemic. Instead, they clearly display how human judgments produced by individuals with bounded rationality channeled the diffusion process behind the spread of bank runs. The findings show that similarity judgments, which are known to affect smaller and less consequential decisions than whether to withdraw all of one’s savings from a bank, are so habitual that they are also seen in the spread of a bank panic. It is difficult to argue that this judgment identifies weak banks. First, a bank panic is in itself a demonstration of imprecise judgment, as evidenced by the fact that most banks continued to operate after experiencing a run. Second, the particular similarity judgments displayed here are not well linked to bank financial risk. The most reasonable similarity judgments are probably those based on same-form and correspondent-group, but even these look arbitrary. There is no apparent reason that a savings-bank run in Minnesota should affect a savings-bank run in California, but on average it did. There is no reason for the ethnic similarity of communities to be a signal of bank financial risk, but it can be interpreted based on information transmission or discriminatory judgments. There is no reason for correspondent-bank network positions to guide runs, because the correspondent networks functioned well in this panic and were not a source of bank failures.

Discussion and Conclusions

The diffusion of negative information that reduces trust in organizations is a serious event with potentially harmful effects. It can be triggered by a wide range of actors, including activists, customers, suppliers, lenders, and stockholders, each of whom can resist the organization. Considering these significant consequences, and recent findings on how negative information spreads beyond the organization from which it originates, we think it is important to embark on rigorous study of how negative information spreads. Bank panics are an ideal setting because they are consequential events with a weak economic rationale for each run, and they have well-documented adverse effects on banks, communities, and society at large (Hoffmann 1956).

The severe economic and social consequences and clear role of customers in the 1893 bank panic made it a good starting point for examining the diffusion of resistance against organizations, but the phenomenon and theoretical mechanisms developed in this study have broad applicability. Resistance against specific forms of organizations spreads through patterns that suggest diffusion processes and leads to the foundation of organizations with opposing objectives (Carroll and Swaminathan 2000; Greve et al. 2006), legal resistance (Ingram and Rao 2004; Ingram et al. 2010), and simple avoidance (Jonsson et al. 2009). Some of these diffusion processes have been associated with social movements, suggesting that the diffusion of negative information and reactions against organizations can take an unorganized (e.g., bank panics) or a more organized form (Briscoe and Safford 2008; Ingram and Rao 2004). Indeed, resistance movements are often associated with diffusion processes and negative information about the target of resistance, suggesting that the link between social movements and resistance against organizations or specific organizational practices needs further empirical investigation (Soule 1997).

The mechanisms explored here are also important theoretical contributions. A key insight is that the diffusion of negative information driving actions against organizational interests removes the organization as a driving force in the diffusion process. This is important because it leads to a change from the highly specific and value-seeking diffusion mechanisms used by organizations—such as network ties and alliances—to the cruder diffusion mechanisms used by individuals making heuristic judgments of which organizations are relevant to each other. This change does not make the diffusion process less selective, as our theory and evidence indicated, because judgments also distinguish sharply between organizations. However, we find that individuals make distinctions based on easily observable, even if superficial, characteristics, which can lead to an arbitrary distribution of reactions against organizations.

It is important for the empirical contribution that each hypothesis is founded on similarity judgments that customers are likely to make, and they are not predicated on financial or business similarities of banks or communication among similar banks. This is intrinsic to the diffusion of negative information, because organizations hit by negative events do not spread this news through inter-organizational communication; on the contrary, organizations that experience a traumatic event usually try to hide information pertaining to it (Kim and Miner 2007). Instead, stakeholders spread the information, and the interpretation that the negative event may affect similar organizations they transact with. Same-form banks, similar-community banks, and structurally equivalent banks were more influential because customers judged them to be more relevant.

Our findings reveal that bank runs were driven by characteristics unrelated to a bank’s financial health. Extant work leveraging banks’ financial attributes show that they fail to predict a bank run (Calomiris and Gorton 1991; Dupont 2007). During a bank panic, many financially sound banks become the target of runs, whereas most financially-weak banks remain unharmed. Limitations in individual judgments can explain this puzzle. Individuals use the information and interpretations available to them to make decisions. Thus, when intimidating and fast-moving events occur, negative information about pertinent organizational forms, like banks, spreads rapidly, and information from one’s peers becomes more easily accessible and salient than internal bank attributes. Our findings imply that, in the diffusion of negative information, the salience of the information plays a greater role than the accuracy of the information or the validity of interpretation.

Stigmatization processes are central in this theory, because the study focused on damaged stakeholder trust (Jonsson et al. 2009; Pontikes et al. 2010; Zuckerman 1999). This is distinctive from the diffusion of positive information, a process we did not examine in this study. The broad mechanisms for the diffusion of negative information we uncovered likely apply to the diffusion of positive information among stakeholders in a similar way, although they differ in their reliance on inter-organizational diffusion. Specifically, the three relevance judgment rules will likely be activated when an organization’s stakeholders try to understand the relevance of an external positive event and its potential impact.

However, there are several important differences between negative and positive information, which could give rise to significantly different diffusion processes. First, one of the most enduring findings in social science is that individuals are risk-averse, and they change only when faced with a problem. Stakeholders proactively react to negative information because they see a possibility of loss. A bank run is a perfect example. Positive news, however, is not a problem for stakeholders, because there is no threat from positive news associated with their organization. It is thus less clear that positive news will spur action. Second, individuals tend to make categorical judgments in interpreting negative information, consequently attributing the negative information to the category itself. By contrast, individuals do not seem to use categorical judgment when they evaluate positive information; instead, they tend to attribute positive information to the specific organization or entity. For example, the charge against Eli Lilly for bribing and promoting drugs for unapproved uses in 2009 triggered public scrutiny of the entire industry, which resulted in similar charges against Pfizer and GlaxoSmithKline. The efforts of the same companies, Pfizer and GlaxoSmithKline, to provide inexpensive AIDS medication to Africa, however, do not seem to have enhanced the industry’s overall reputation. Taken together, these two features of positive information may significantly dampen the diffusion of positive news, implying that stakeholders’ reactions to positive news may be slow or limited. Because these data lack information on positive news, we were unable to examine these potential countervailing effects. If these conjectures are true, future research should examine such effects. Many industries offer a blend of negative and positive information; for example, the same carmakers that installed air bags now thought to be unsafe are also pioneers in developing emission-free vehicles. Volunteer organizations show similar tensions, as when churches’ scandals stand in sharp contrast to their goals.

Another feature distinguishing stakeholder-driven diffusion from organization-driven diffusion is the transfer of practice. In organization-driven diffusion, practices often diffuse directly; organizations receive information about a practice and act on the information to decide whether to adopt it. By contrast, in stakeholder-driven diffusion, practices tend to diffuse indirectly—often as a consequence of behavioral changes induced by the diffused information.

The importance of these insights for organizations is clear. Negative events beyond an organization’s control can cause significant resistance against the organization. Nonetheless, organizations can gauge their susceptibility to such processes. This susceptibility is based on the probability that an associated organization will engage in actions that decrease trust in the organizational form. The dilemma is that organizational similarity is a source of association, but similarity is also a means for organizations to signal their legitimacy. Thus, being similar to other organizations has the short-term advantage of establishing one more readily in the marketplace, but the possible long-term disadvantage of being a target of negative information spread. These arguments suggest it may be beneficial for organizations to deviate from the general organizational form in some dimensions, because doing so could help them become less vulnerable to the actions of other similar-form organizations.

Organizations that are members of a group associated with negative news often fight back to avoid being a victim of the news. In the 1893 bank panic, banks countered the spread of negative information by trying to assure depositors of their financial health and the soundness of the banking system. Our reading of newspaper articles suggests the press collaborated: news coverage generally had a reassuring tone and sometimes printed statements known, from earlier bank runs, to be false (e.g., bank failures would lead to quick and complete reimbursement). Bank runs spread widely despite banks’ efforts, but our analysis cannot determine to what extent these efforts were effective, because we do not know how serious bank runs would have become if banks had not countered the spread of negative information. Further investigation of whether and when organizations’ resistance to negative information is effective could offer useful insights into how organizations try to avoid being stigmatized by categorical negative information. Research drawing from newspaper coverage or new data sources, such as communications in social media and organizational responses through press releases and other media, could examine these processes in greater detail. For example, the recent scandal of expired meat being sold to some fast-food chains in Asia, resulting in customer flight from those chains and unrelated restaurants, likely involved customer communications in social media as well as organizational responses in conventional and social media. Research on such phenomena would help distinguish the role of the press and other media outlets in driving reactions against organizations. Our theoretical model has a significant component of interpersonal diffusion, but more research is needed to distinguish interpersonal, mass media, and modern social media routes in the diffusion of negative information.

Bank panics are wide-ranging events that illustrate how the diffusion of negative information generates actions against organizations. The processes that facilitate the spread of such information significantly affect individual organizations as well as the organizational form as a whole. When these processes affect keystone marketplace organizations, like banks, the broader economy is adversely affected. Despite the gravity of these occurrences, major gaps exist in our understanding of the causes of such diffusion processes, in particular with regard to the selectivity of which organizations are targeted. We investigated similarity judgments, but alternative explanations of this phenomenon are possible. Novel findings could be gleamed from a more extensive examination of the spread of the loss of trust as a diffusion process in which organizations have heterogeneous vulnerability.

Footnotes

Acknowledgements

We thank Michelle Ie for research assistance and INSEAD for financial support. Four reviewers and the editors provided very helpful comments on earlier drafts.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.