Abstract

Conventional research in organizational theory highlights the role of board interlocks in facilitating business collective action. In this article, I propose that business collective action affects the evolutionary path of interlock networks. In particular, large market players’ response after a collective action to the classic problem of the “exploitation” of the great by the small provides a mechanism for interlocks to evolve. Through studying the two types of collective action that banks organized during the Panic of 1907, I find that the experience of issuing currency substitutes, a course of collective action that needed to mobilize community support, made bankers more aware of their responsibility for community welfare. In the post-crisis period, bankers were thus more supportive of the market stabilization strategy of assisting small banks. In contrast, the experience of organizing mutual lending, a course of collective action that highlighted the power of businesses independent of the communities in which they were located, led bankers to focus more on their sectional interest and favor the market stabilization strategy of eliminating small banks. These different attitudes toward small banks affected the evolution of the interlock networks between large and small banks.

Board interlocks are important for business collective action. Interlock ties provide a channel for business leaders to build a united front and recruit collective action participants. Researchers have demonstrated that the potential for businesses to mobilize depends on the structure of interlock ties in their group (Burris 2001, 2005; Mizruchi 1992, 1996). Despite the importance of interlock ties, they are usually treated as preexisting, and researchers have not investigated whether the experience of organizing collective action will result in structural changes in board interlocks.

This is an important gap in the literature, and several scholars have suggested that prior collective action experience has a spillover effect on the development of mobilization infrastructures. North (1990) argues that solving collective action problems entails a feedback loop: once an initial collective action has been successfully completed, participants have information on coordination benefits and mobilization capabilities. Thus, prior experience of collective action induces changes in complementary structures and generates path dependence. In support of this argument, Putnam, Leonardi, and Nanetti (1993) suggest that different solutions to the collective action problem in the Middle Ages led to divergent development trajectories of civil society in the north and south of Italy. Similarly, Greve and Rao (2012) find that the experience of organizing collective action affects the development of nonprofit organizations. These studies provide valuable evidence of the impact of collective action on mobilization infrastructures, but they are missing an account of how collective action is a mechanism that can affect the evolution of board interlocks.

In this article, I reverse the direction of causality—that is, social networks as the source and collective actions as targets—by exploring how large market players deal with the classic problem of the exploitation of the great by the small in the post-collective action period. In The Logic of Collective Action, Olson (1965:35) observed that, when a group realizes a collective good, “the largest members, the member who would on his own provide the largest amount of the collective good, bears a disproportionate share of the burden of providing the collective good”; therefore, “in small groups with common interests there is accordingly a surprising tendency for the ‘exploitation’ of the great by the small” (italics in original). Since Olson, scholars studying collective action have widely recognized this problem, but they have used it mainly as an explanation for why large players in a group are more likely to provide collective goods, and have not investigated how large players deal with free-riding problems after the collective action. The lack of studies is somewhat surprising, because this is a problem that large players should have incentives to mitigate. Large players’ responses to this problem in the post-collective action period may affect their relationships with small players.

Small market players often perform an important role in serving a community: they help intensify market competition and bring down commodity prices; they add to market diversity and enrich consumers’ choices; and they often serve niche markets, such as ethnic groups, ignored by the large players who cater to the mainstream. As such, large players’ treatment of small players in the post-collective action period may reflect their willingness to support their community’s welfare. A rational response to the free-rider problem may lead large market players to take an anti-small player position; a willingness to support their community may lead them to take a more favorable attitude toward small players or a long-term view of rationality. I suggest that experiences of business collective action that require society support make business leaders more aware of the importance of their community; consequently, in the post-collective action period, they are more likely to support small market players. In contrast, collective action experiences that highlight what businesses can do independently of their community may make them less likely to care about community well-being; in the post-collective action period, they may thus be more likely to propose eliminating small market players. These different attitudes affect the relationship between large and small market players: networks between large and small market players tend to become more robust and cohesive when the former type of collective action has been organized, but they are usually fragile and fragmented following the latter type of collective action.

The collective actions organized by banks to survive the Panic of 1907 provide a good context for testing these propositions, because they constitute situations in which small banks could not effectively be prohibited from free riding. The Panic of 1907 was the largest nationwide financial crisis before the Federal Reserve was established in 1914. 1 Lacking support from the government, banks in many communities sought private solutions to alleviate the cash scarcity problem, such as organizing mutual lending or issuing currency substitutes to the public. Mutual lending and issuing currency substitutes typically involved all banks within a community, but mutual lending involved only banks, whereas issuing currency substitutes required mobilizing support from the public, government, and other businesses.

Studying 145 U.S. cities with populations at the time larger than 25,000 residents, I found that two opposing strategies surfaced in the post-crisis debate about how to stabilize local financial markets. Bankers and regulators who supported one strategy viewed small banks as the cause of financial instability, proposed to eliminate them, and urged leading bankers to focus on their self-interest rather than that of the community. Proponents of the second strategy highlighted the responsibility of banks to their hosting community, urged bankers to be public-spirited gentlemen, and supported the deposit guarantee law, which disproportionately benefited small banks. In addition, board interlocks loomed large in the post-crisis debate, as bankers viewed them as a tool to prevent risky operation or mismanagement. Of course, collective action does not happen randomly. An unobserved heterogeneity might affect both the incidence of a certain type of collective action and the evolution of board interlocks. Thus, I adopt the Conditional Mixed Process (CMP) model (Roodman 2011) to control for biases that arise from the fact that certain unobserved variables may affect several outcomes. After controlling for banks’ tendency to adopt a certain type of collective action, I find that large and small banks were more likely to form interlocks in cities where currency substitutes had been issued, but they were less likely to do so in cities where mutual lending had been organized.

Theory and Hypotheses

Board Interlocks and Business Collective Action

A long research tradition demonstrates that inter-organizational ties through shared board memberships are an important channel for businesses in organizing collective action. Following pioneering work by power elite theorists (e.g., Domhoff 1967; Mills 1956; Zeitlin, Neuman, and Ratcliff 1976), researchers have shown that board interlocks serve as vehicles for firms to combine their efforts to influence political elections (Burris 1987, 2005; Mizruchi 1992), government decision-making (Mizruchi 1992), and public policy formation (Akard 1992; Dreiling and Darves 2011; Vogus and Davis 2005). Besides political activities, interlock ties also enable firms to coordinate private regulation (Yue, Luo, and Ingram 2013): dense interlock connections contribute to coordinated economic decision-making and facilitate the formation of strategic alliances.

Researchers have also recognized that interlocks are dynamic (for a review, see Mizruchi 1996; Palmer and Zafonte 2011). Shaped by the debate on whether interlocks are primarily inter-organizational or intra-class phenomena, early studies on the evolution of interlock ties examined the effects of resource dependence (e.g., Burt 1983; Pfeffer and Salancik 1978) and class cohesion (e.g., Palmer 1983; Palmer, Friedland, and Singh 1986) on the existence and reconstitution of interlock ties. Recent studies of the evolution of board interlocks emphasize the spatial feature of interlocks (Kono et al. 1998) and examine how institutional environments shape the evolution of board interlocks (e.g., Marquis 2003; Yue 2012).

Among the studies that examine the institutional determinants of the structure of board interlocks, Stark and Vedres’s (2012) investigation of how Hungarian firms’ political affiliations affect their business networks deserves special attention. Stark and Vedres (2012) show that, although political sociologists traditionally document how businesses affect politics by examining the impact of business networks on corporate political behaviors, politics also affect businesses, in that political divisions create holes in business networks. Corporate political behaviors often take the form of collective action, but business collective actions include more than political activities. As such, an intriguing question is whether the organizational form of business behaviors, not just their content, may affect the evolution of business interlock networks. In addition, because business interlock networks tend to be stable, they have been treated primarily as a predictor of business collective action, and researchers have so far not examined whether the experience of organizing collective action may affect the evolution of business interlocks.

Some writers point out that collective action has spillover effects beyond the directly intended project. North (1990) articulates the general idea that solving a collective action problem generates path dependence because the experience induces the formation of complementary institutions. Emphasizing factors such as fixed costs, learning by doing, and self-fulfilling expectations, he argues that once a prior collective action is successfully organized, it lowers the threshold for adding similar institutions. Coleman (1961:573–74) similarly argues that past collective action experiences shape a community’s subsequent response: “Each problem successfully met leaves its residue of sentiments and organization; without these sentiments and organization, future problems could not be solved.” North and Coleman both point to effects of prior collective action on subsequent rounds of action, but when referring to the process to explain the evolution of interlocks, we still need a mechanism through which to explain the effects of collective action on the relationships between businesses.

Exploitation of the Great by the Small

The exploitation of the great by the small is fundamentally a free-riding problem. Olson (1965) argues that because individuals in any group attempting collective action will have incentives to free ride on the efforts of others, free-riding behavior often leads to non-production or under-production of the relevant collective good. This problem, however, can be mitigated if the privileged players in a group find it worthwhile to provide the collective good themselves, regardless of how much other group members contribute. As Olson (1965:34) suggests, “in groups of members of unequal ‘size’ or extent of interest in the collective good—there is the greatest likelihood that a collective good will be provided.” In such a situation, large players typically pay for the collective good; small players contribute little but nevertheless consume it.

This problem has been widely discussed, but in doing so, researchers typically focus either on how the presence of large players enhances the chance of collective goods being provided (e.g., Bowman 1989; Ruef 2010), or on specifying the conditions under which a critical mass within a group chooses to make big contributions to its collective action (e.g., Marwell and Oliver 1993). Relatively little is known about how large players deal with this problem in a post-collective action period. The lack of attention is somewhat surprising, because large players should have an incentive to address small players’ free riding. If large players address the free-riding problem, their responses will likely affect their relationships with small players. As a result, large players’ responses may provide a mechanism for collective action to affect the evolution of business networks.

Small market players tend to be local and community based. They can break large market players’ monopoly over a local market, intensify competition, and consequently benefit consumers by lowering market prices. Small market players also tend to be more innovative and entrepreneurial, offering unique products or services. In addition, many small market players specialize in serving niche markets, such as certain ethnic groups that are often ignored by large players who cater to the mainstream. In the banking industry, small community banks have long been viewed as a bulwark that protects local residents and businesses (Marquis and Lounsbury 2007). As such, the attitude of large market players toward their smaller counterparts in a post-collective action period reflects their weighing their respective commitments to community welfare and their own short-term self-interest. I suggest that the collective action experience of being supported by one’s community may motivate business leaders to take an interest in their community; consequently, in the post-collective action period, these leaders will be more likely to support small market players. In contrast, collective action experiences that highlight what businesses can do independent of their community leads business leaders to put their own sectional interest above that of the community; in the post-collective action period, these leaders may thus be less favorable toward small market players. These different attitudes, in turn, affect the formation and dissolution of social networks between large and small market players.

For Olson, the central condition making possible the exploitation of the great by the small is the principle of non-excludability, according to which small players cannot effectively be excluded from benefiting from a collective action. The collective action that banks organized to survive financial crises during the Panic of 1907 provides a good context for studying this problem. The Panic of 1907 happened in an era before the Federal Reserve was established. With little support from the government, banks in many communities organized collective actions to enable them to survive the financial crisis. Due to the contagious nature of bank runs, the failure of one bank could poison the public’s confidence in a whole market; these collective actions were thus typically organized to involve all banks within a community.

Banks’ Collective Action during the Panic of 1907

The Panic of 1907 was triggered by an exogenous event—the failure, on October 16, 1907, of a stock speculation financed by several financial institutions in New York City. These institutions suffered immediate bank runs as depositors rushed to withdraw money. Because the New York Clearing House Association 2 failed to take action in time to rescue the market, contagious bank runs spread to other financial institutions in New York. One week later, the Knickerbocker Trust Company, the third-largest in New York, collapsed. Within weeks, the panic spread across the nation as vast numbers of people ran to their regional banks to withdraw their funds.

The financial crisis spread so quickly to the rest of the country because the banking reserves of the whole country were concentrated in New York City banks. The National Banking Act, passed in 1863, required banks in central reserve cities (i.e., banks in New York City, and after 1887 in Chicago and St. Louis as well) and reserve cities (i.e., banks in other cities with populations over 500,000) to keep 25 percent of their notes and deposits in reserves. Reserve city banks were allowed to keep half of their reserves in vault cash while depositing the other half in central reserve city banks. Country banks (i.e., all other national banks) were only required to keep a minimum reserve ratio of 15 percent, and they were also able to deposit 60 percent of the reserves in reserve city or central reserve city banks. This set of requirements resulted in a pyramid structure, with banking reserves concentrated in New York City banks. In this way, the unrest in the New York money market quickly developed into a nationwide financial crisis.

As people ran to their regional banks, country banks and reserve city banks all attempted to withdraw their deposits from New York banks. Less than 10 days after Knickerbocker’s failure, withdrawals from banks in the nation’s interior resulted in a $53 million deficit in banking reserves (Sprague 1909). The New York Clearing House Association suspended cash payments on October 26. 3 This led to a nationwide restriction of cash payments. Unable to obtain cash from other regions, banks everywhere faced the problem of currency scarcity. This scarcity could not be relieved by increasing currency supplies, because the National Banking Act tied note issuance by national banks to the purchase of federal government bonds.

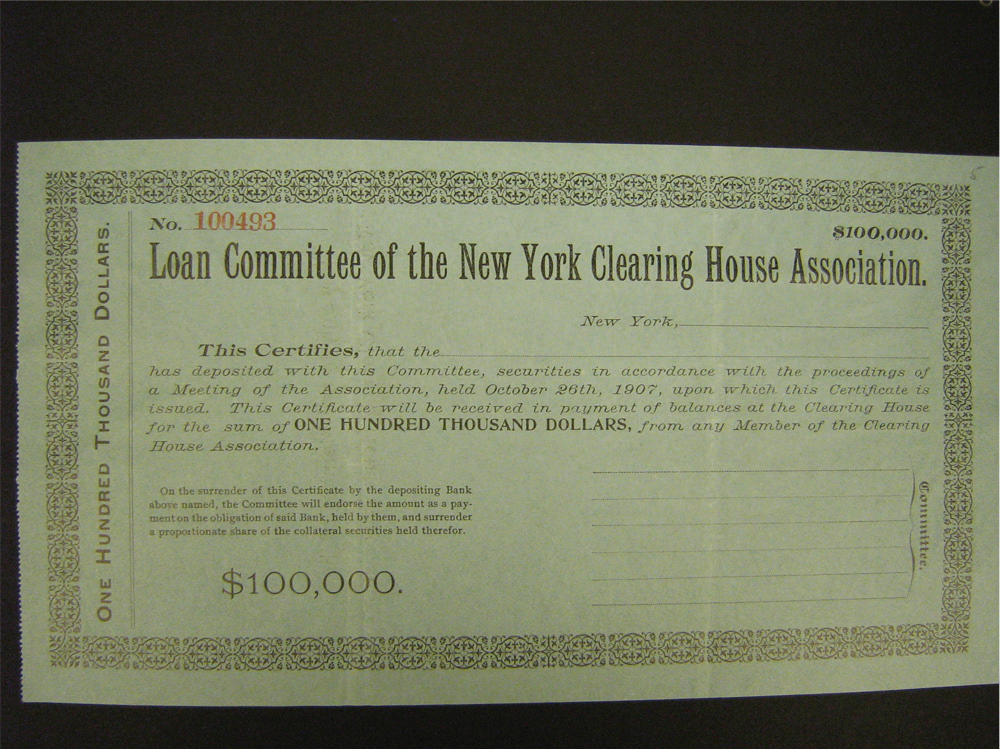

Because the note issuance was inelastic and there was no central bank in the United States at the time to regulate the market, banks in some cities organized collective actions to meet depositors’ demands for currency. One type of collective action was organizing mutual lending among banks by issuing clearing house loan certificates. Financially stressed members of a clearing house could borrow loan certificates by collateralizing their assets and paying interest. They in turn used the loan certificates in place of currency in the clearing process, freeing cash to satisfy depositors’ demands. Other banks accepted loan certificates as a form of payment. If a borrowing bank failed, the losses would be shared by allocating liabilities to all clearing house members in proportion to their banks’ capital (Gorton and Huang 2003). In this way, loan certificates served as a medium for transferring cash from banks with surpluses to stressed ones, so they all could survive the bank panic. Banks not affiliated with the local clearing house (typically those too small to afford the clearing cost) participated through their agent banks in the clearing house that cleared payments for them. As the San Francisco Call (1907:7) reported, “while the certificates are delivered only directly to banks in the clearing house association, banks outside the association can secure them through their connection by the deposit of proper securities.” Thus, mutual lending was not a dyadic activity but a community-wide collective action mediated by a local clearing house. Clearing house loan certificates were used exclusively for settlements between banks, and issuance constituted banks’ attempts to stabilize a local market by mobilizing among themselves. Figure 1 shows a $100,000 loan certificate issued by the New York Clearing House Association during the Panic of 1907.

Sample of Clearing House Loan Certificates Issued during the Panic of 1907

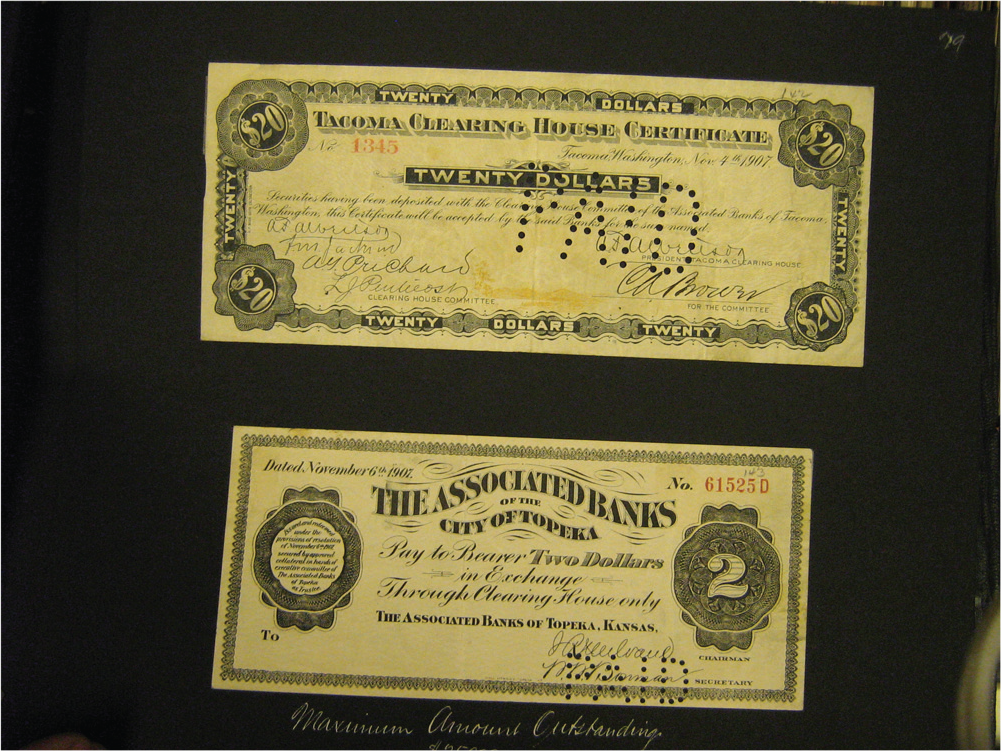

The other type of collective action involved issuing small denomination currency substitutes intended for public circulation. These currency substitutes were issued by clearing houses or by temporarily united associated banks in places that had no clearing house. They were similar to loan certificates in that the borrowing banks had to use their banking assets as collateral to obtain them. They were paid directly to local depositors, however, and had to be used for daily purposes, such as payroll, goods purchases, and tax payments. They were mostly in convenient denominations of $5, $10, and $20; in some places the denomination was as low as 25 cents. These currency substitutes were “real” money created by banks for the public to use. The issuance of currency substitutes was a course of business collective action that needed to be supported by other stakeholders within the community, such as other businesses, ordinary citizens, and the government. In addition, issuing small denomination currency substitutes typically involved all banks in a community. A single bank or a small number of banks would not issue currency substitutes, because this action might be construed as indicating unsound conditions. But once the currency substitute program was established in a given community, all the banks would have an incentive to participate, because they would otherwise run the risk of being drained of money, as depositors would prefer legal money. Figure 2 shows two examples of small denomination currency substitutes issued during the Panic of 1907.

Sample of Small Denomination Currency Substitutes Issued during the Panic of 1907

Banks’ dependence on the support of other social groups was even more remarkable because issuance of currency substitutes was largely illegal. Banks’ currency substitutes were backed not by the purchase of government bonds, as required by the National Banking Act, but by all kinds of banking assets. In addition, the National Banking Act imposed a 10 percent tax on notes issued by state banks, although none of the issuers of these currency substitutes paid the tax. The currency substitutes were technically illegal, but this was not a semi-covert or secretive action involving a conspiracy by bankers. The government was aware of the currency substitutes, but the lack of public remedies for the currency scarcity problem led it to tolerate and even encourage their issuance. For example, the public banking examiner and superintendent of South Dakota called on the state’s bankers to pay attention to the issuance of currency substitutes in neighboring states and recommended they do likewise:

I would suggest and recommend that where there is more than one bank in a town they get together and agree along similar lines, for the protection of themselves as well as the public. . . . I would also suggest that you get the business men of your town together and explain to them the situation and the proposed plan, and in this way secure their approval and support. (Andrew 1908:499–500)

The government’s tolerant attitude toward currency substitutes is partially explained by the alignment of interests between banks and other social groups within a community during a financial crisis. Communities had a stake in the issuance of currency substitutes, because maintaining a healthy currency flow was important for sustaining the prices of commodities, paying out wages, and keeping the wheels of the local economy running. Despite its illegality, some community members perceived the issuance of currency substitutes as necessary to assist the public during the crisis. Yet, the issuance of small denomination currency substitutes did not go without resistance. Thousands of workers went on strike to protest currency substitutes (Bakersfield Californian 1907). Major newspapers published editorials highlighting the danger of emergency currency and denouncing the practice of allowing banks to issue unsecured notes.

Bankers adopted various strategies to mobilize support from their communities. They highlighted the importance of maintaining monetary order and issued public statements in local newspapers. They painted a picture of a “cash war,” justifying the issuances as necessary to defend the whole community from being drained of money. They urged people to “help themselves and help the communities in which they live by becoming the backers of the banks for the present” (Bend Bulletin 1907:2). Bankers called it “a patriotic duty to help banks by leaving funds in them” (Daily Capital Journal 1907:1). Banks also formed alliances with leading local merchants and industrialists to endorse the currency substitutes. In summary, the successful issuance of currency substitutes was a matter of collective business action that was enabled by the support of other stakeholders in a community.

Market Stabilization Strategies and the Evolution of Interlocks

Both mutual lending and issuing currency substitutes were subject to the problem of the exploitation of the great by the small. The organization of mutual lending depended on large banks’ deep pockets, whereas the successful issuance of small denomination currency substitutes depended on the public’s trust in large banks. This point is clearly illustrated by the statement of New York banks on the priority of returning funds to interior banks: “it is realized that they (small interior banks) are not in a position to count upon co-operation and the use of the clearing house certificates, as in the case of communities having a number of strong institutions” (Cairo Bulletin 1907:1).

The relationship between large and small banks figured prominently in the post-crisis debate on how to stabilize local financial markets. Two opposing strategies emerged. One strategy proposed to eliminate small banks. Bankers and regulators who favored this strategy viewed small banks as the cause of financial instability, preferred large banks’ domination of local financial markets, and opposed the deposit guarantee law, which benefited small banks more than large ones. They argued that bankers should care only about their sectional interest rather than that of the community. For example, when addressing the convention of the Arizona Bankers’ Association in December 1908, Sims Ely, the Arizona Bank Comptroller, said: “A bank is not operated for the purpose of booming a community” (Arizona Republican 1908:8). The Washington State Bank Examiner, J. L. Mohundro, said:

The best interest of the state lies in seeing that the banks we have are not crippled by the organization of weak banks. . . . I believe that if fifty financial institutions of the state would go into voluntary liquidation the banking conditions would be materially strengthened. . . . The whole tendency should be to make stronger banks and discourage the formation of small institutions. (Wenatchee Daily World 1910)

In Chicago, a prominent banker, James B. Forgan, opposed the guarantee of bank deposits, arguing that “it would make all banks safe, one just as good as another and for that reason a man would go to any bank with his money” (Commoner 1908:1). Forgan was sharply criticized by the Commoner (1908:1): “It is difficult to conceive of a more selfish argument than that which Mr. Forgan presents, and no one can be expected to endorse his argument without putting the interest of the big banker above the welfare of the community.”

In places where mutual lending had been successfully organized, businesses’ own efforts at stabilizing a market might have enhanced the perceived power of business independent of the community. The enhanced perception of self-efficacy reduced the perceived need for community support. After the financial crisis was over, bankers were more likely to support a market stabilization strategy that put their sectional interest above that of the community. Therefore, they were more likely to adopt the anti-small bank position.

Board interlocks also loomed large in the post-financial crisis debate about how to maintain market stability. The Columbus Journal (1910:4) reported, “When the banks of the whole country in 1907 gave us clearing house certificates instead of cash, private investigations showed an alarming laxity of bank directors in the management of their institutions.” Regulators and bankers clearly realized that directors were experts of the trade, had first-hand information about a bank’s operations, and should therefore play an important role in monitoring banks. In 1909, the Comptroller of Currency, Lawrence O. Murray, issued an order that directors of national banks must set monthly meetings, appoint an examining and discount committee, and all loans and discounts must be approved by directors at the monthly meeting. In the Kansas State Bankers’ Association meeting in 1910, the State Bank Commissioner, J. N. Colley, argued that “bank failures would become almost unknown if the directors attended closely to their duty in connection with their bank” (Topeka State Journal 1910a:1). Similarly, at the Arizona State Bankers’ Association meeting, it was suggested that “directors who fail to discharge their duties as directors should get off the board and make way for others who will do the work” (Arizona Republican 1908:8). As a result, directors were held responsible for their banks’ operations. In Abilene, Kansas, where a bank cashier embezzled $70,000, the bank’s directors had to provide a written guarantee for deposits (San Francisco Call 1910). Thus, by sitting on the boards of small banks, the executives and directors of large banks bore the risk of being held responsible for small banks’ operations. In addition, their knowledge and expertise kept small banks from risky operations or mismanagement.

Small banks clearly realized the advantages of having executives and directors of large banks sitting on their boards. In small banks’ advertisements, it was common practice to list bank directors’ names and highlight their prominence. In addition, having executives and directors of large banks sitting on the boards of small banks was construed as an indicator of progressiveness, suggesting that banks took an active interest in building up the local community (Monett Times 1910). For example, an advertisement of the Citizens State Bank in Roundup, Montana, reads (Roundup Record 1910:5):

The directors of this bank are successful business men. Men experienced in the handling of financial affairs. They give time and care to the workings of the bank—the safe-guarding of all funds entrusted to its care. Fully realizing that each and every account on our books, be it large or small, has its influence, in the building of our town and community, they respectfully solicit your account.

The evolution of banks’ board interlocks was likely shaped by the post-crisis debate on market stabilization strategies, and I expect anti-small bank sentiment would have made board interlock networks between large and small banks fragile. Previously unconnected banks were less likely to form ties with each other, and existent ties between them were more likely to fail. 4

Hypothesis 1a: Large and small banks were less likely to form interlock ties in a community where mutual lending had been successfully organized.

Hypothesis 1b: Existent ties between large and small banks were more likely to fail in a community where mutual lending had been successfully organized.

The other market stabilization strategy was to assist small banks. Bankers and regulators who favored this strategy called attention to the fact that banks’ fortunes were rooted in the community’s prosperity, they urged bankers to be publicly minded gentlemen, and they endorsed the deposit guarantee law. During the Utah Bankers’ Association conference in June 1910, bankers reviewed the public’s support of their use of currency substitutes during the Panic of 1907. Speaking on behalf of members of the association, J. F. Tolton, a prominent local banker, said: “If we were to attend our own business strictly, we would soon go out of business”; he suggested that “[i]t is our business to look after the business of our friends and to see that it is taken care of” (Ogden Standard 1910:7).

Similarly, bankers in Oregon, Missouri, acknowledged that “the banker owes a whole lot to the community in which he lives . . . his first obligation is loyalty to his community” (Holt County Sentinel 1908:1). In Topeka, Kansas, where the $2 bill in Figure 2 was issued, C. N. Prouty, the President of the State Bankers’ Association, suggested that “three fourths of the State Banks are ready and willing to grant their depositors the benefit of the Guaranty Law”; he noted that “we invite new accounts” and vowed that “small accounts [will be] given the same careful attention as the larger ones” (Meade County News 1909:2). When the Kansas Governor, W. R. Stubbs, addressed the State Bankers’ Association in 1910, he said, “I believe a banker ought to be a public spirited generous man who takes an interest in his community. He can be worth to the people more than all the fortunes he may amass” (Topeka State Journal 1910b:1).

The successful organization of business collective action through the mobilization of community support may remind business leaders that, to promote their institutional projects, they need to secure the backing of their community. Under such a condition, we would expect business leaders to be more aware of their responsibility toward their community. Therefore, they may be more likely to favor the market stabilization strategy of assisting small banks. Such a sentiment toward small banks would have affected the evolution of board interlock networks between large and small banks. Previously unconnected banks were more likely to form ties with each other, and existent ties between them were less likely to fail.

Hypothesis 2a: Large and small banks were more likely to form interlock ties in a community where currency substitutes had been successfully issued.

Hypothesis 2b: Existent ties between large and small banks were less likely to fail in a community where currency substitutes had been successfully issued.

Methods

Data

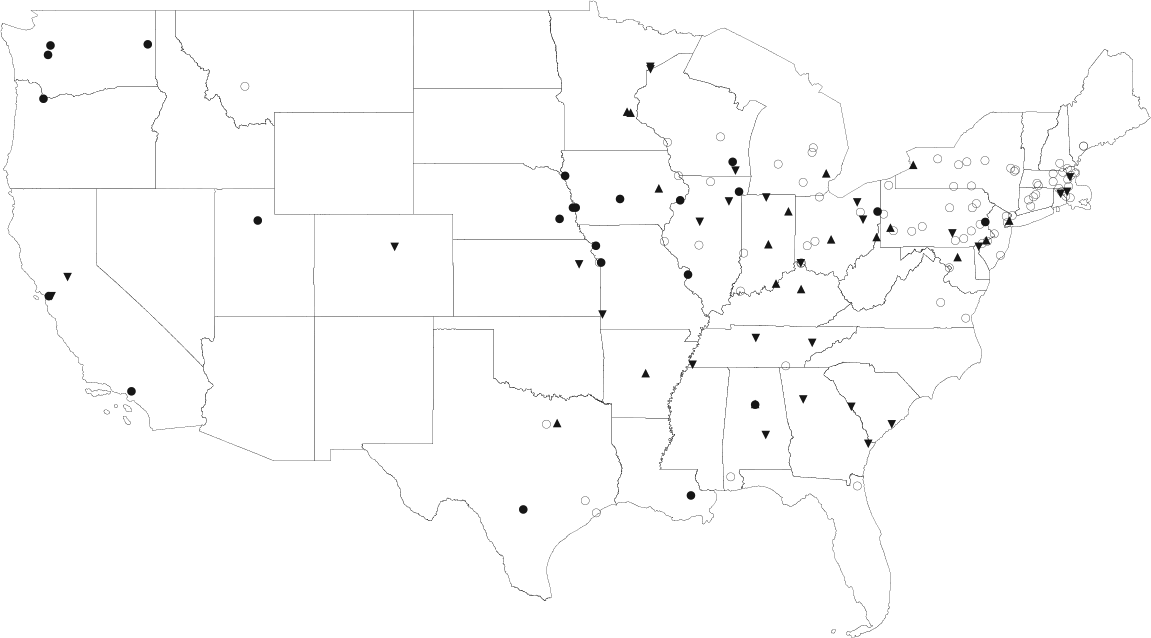

I collected data on collective actions that banks organized during the Panic of 1907 from Andrew (1908) and the report by the Commercial and Financial Chronicle published on May 30, 1908. Andrew surveyed all 147 independent cities 5 with a population above 25,000 and received responses from 145 of them. The Chronicle reported the New York Clearing House Association’s survey of 106 clearing houses in the United States regarding their issuance of loan certificates and received responses from all but nine. The cities covered by these two surveys largely overlap, and only six cities reported by the Chronicle were not covered by Andrew. Thus, I used the 145 independent cities with a population larger than 25,000 reported by Andrew as the sample for this study. Figure 3 shows the geographic distribution of the cities where the two types of collective action were organized, and banks in each city could take either, neither, or both types of collective action.

Geographic Location of Mutual Lending and Issuances of Currency Substitutes

Because adding or dropping board directors takes time, prior studies of board interlocks adopt a relatively long time window (two to four years) for observing the evolution of interlocks (e.g., Palmer 1983; Palmer et al. 1986). I collected two waves of data on banks’ board interlocks in the 145 cities, in January 1907 and July 1910, from the Rand-McNally Bankers’ Directory. There were 2,145 banks in January 1907, and 2,254 banks in July 1910. I coded the names of the executives and directors for all these banks. I defined two banks as sharing an interlock tie if some executives or directors from one bank sat on the other bank’s board of directors. I also collected data on each bank’s characteristics from the Rand-McNally Bankers’ Directory. I gathered city-level data from the 1900 Census.

Dependent Variables, Independent Variables, and Estimation

I have two dependent variables, the formation of a new tie between two previously unconnected banks in a city, and the dissolution of an existent tie between two banks in a city. I created a dummy variable that equals 1 if any pair of banks in a city that were not connected through interlocks in 1907 formed a tie by 1910. For the purpose of robustness, I created two risk pools for network formation. The first risk pool includes the dyads of all banks that were not connected through interlock networks in 1907, except those that failed between 1907 and 1910. The second risk pool narrows the scope to exclude all dyads that involve newly founded banks between 1907 and 1910 (i.e., dyads among the newly founded banks and between them and all surviving banks). To measure the dissolution of interlock networks, I created a dummy variable that equals 1 if any pair of banks that were connected through interlocks in 1907 was no longer connected in 1910. The formation and dissolution of interlock ties are measured at the bank rather than the individual director level, because banks might occasionally replace a previous director with a new one.

One problem in estimating the dependent variables is that clearing house loan certificates and small denomination currency substitutes were not randomly issued. Therefore, unobserved factors might have simultaneously affected the incidence of the two types of collective action and the evolution of banks’ board interlocks. To deal with this concern, I adopted a new estimation method, the Conditional Mixed Process (CMP) model (Roodman 2011). CMP controls for selection biases that arise from the fact that some unobserved variables affect several outcomes, by building on the system of “seemingly unrelated” regression (SUR) equations and allowing errors to be correlated and to share a multi-dimensional normal distribution. It implements the Geweke, Hajivassiliou, and Keane (GHK) algorithm to simulate the multi-dimensional normal distribution and then compute the likelihood value. Exploiting the Maximum Likelihood SUR’s ability to consistently estimate parameters in a recursive simultaneous equation system, CMP is able to account for correlated error terms among outcomes and multi-stage selection (Greene 2011; Kashyap, Antia, and Frazier 2012). Moreover, CMP allows models to vary by observations, so that equations with different lengths of observation (i.e., city-level and dyad-level data) can be simultaneously estimated. In addition, for repeated observations, a sandwich variance estimator accounts for clustering.

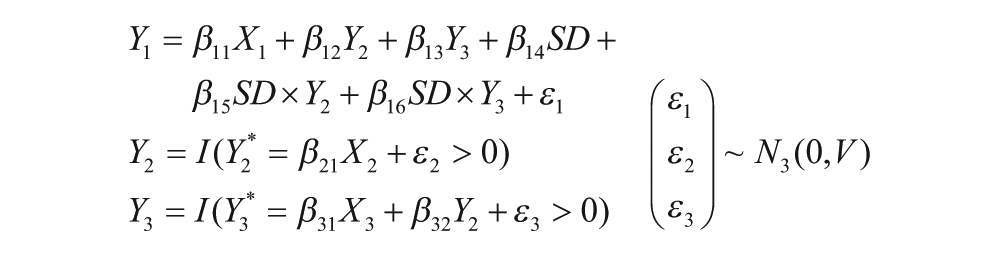

I simultaneously estimate three equations, concerning the formation or dissolution of an interlock tie (

Bank size is measured by the total resources controlled by a bank, which includes the paid-in capital, surplus and profit, and deposits.

8

Size difference is measured as the absolute difference between the total resources of two banks weighted by the average bank size in a city,

Finally, I include an additional set of dyad-level variables to control for other types of connections between banks. Specifically, I look at three types of membership: local clearing house, state bankers’ association, and national bankers’ association. For each type of membership, I have a dummy for only one of the two banks being a member, and a dummy for both banks being members; the reference category is neither bank is a member. To control for the size of two banks, I include the product term of the sizes of the two banks in a dyad. In unreported analyses, I also directly control for the sizes of the two banks and find that the basic pattern of results remains robust.

Table S1 in the online supplement (http://asr.sagepub.com/supplemental) provides a complete list of all control variables and their measures and sources. Table S2 in the supplement provides the tabulation of the means and standard deviations of the city-level variables in the places where both, either, or neither type of collective action took place. The results show that these cities were similar in basic characteristics, except currency substitutes tended to be issued in smaller cities with lower levels of economic inequality. In addition, organizational infrastructures appeared to be important for the organization of collective action: collective action was more likely to be organized in places with a clearing house, dense interlock networks, and more upper-class clubs. To save space, I report the descriptive statistics of all variables used in the analyses of the formation of interlock ties between unconnected dyads and the dissolution of interlock ties between connected dyads in Table S3 and S4 in the online supplement. Because the population of a city, the number of banks, and the number of upper-class clubs are highly correlated, I ran additional analyses by dropping any two of them; the hypothesized results remain similar. 9

Results

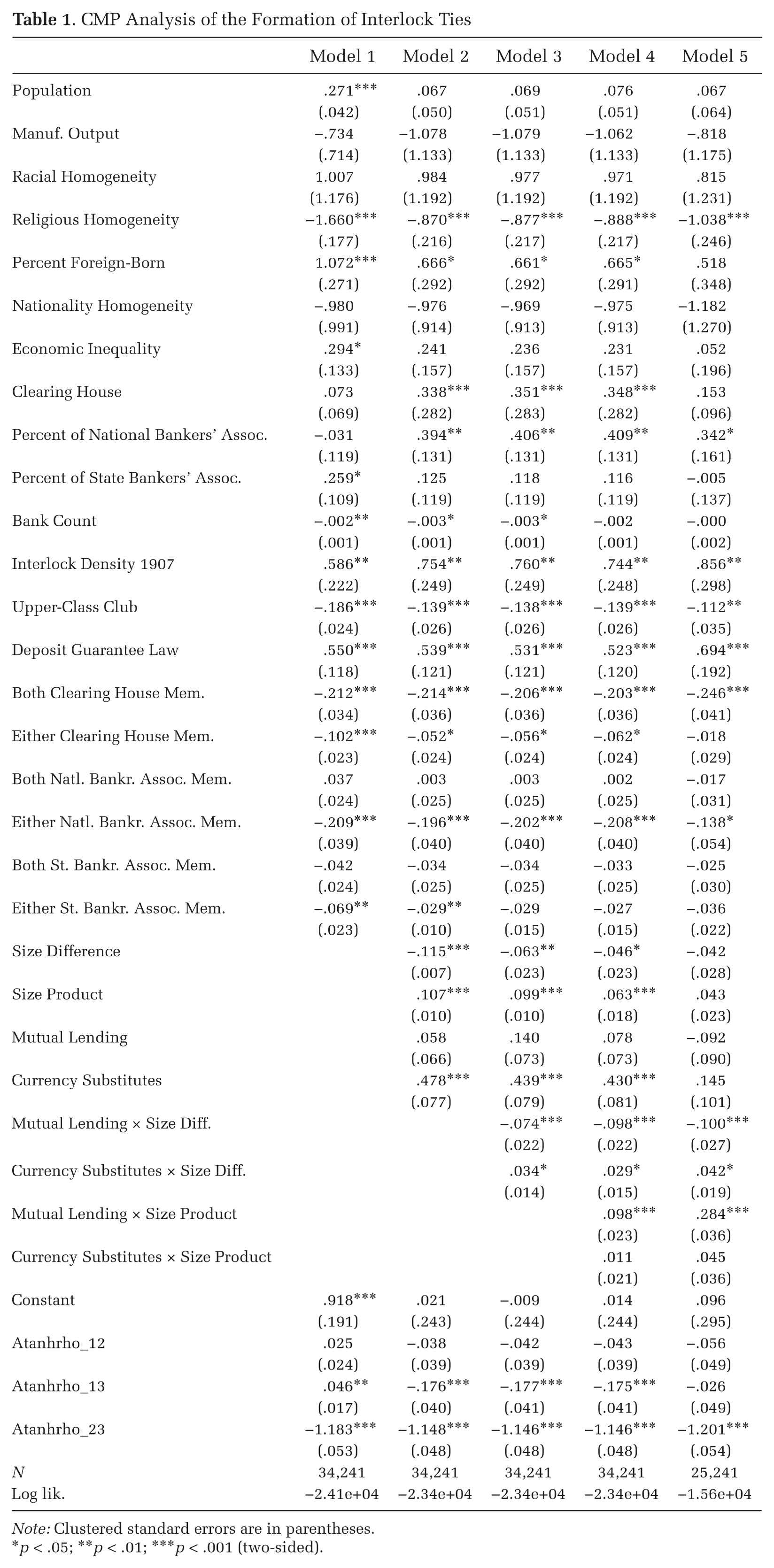

Table 1 presents the CMP analyses for the formation of interlock networks. To save space, I present only the equation predicting the dependent variable. Model 1 reports the baseline model, in which I include all the control variables. Banks in cities with a high level of religious homogeneity and a large number of banks were less likely to form an interlock tie. The presence of an upper-class club in a city reduced the chance of interlock formation, most likely due to a substitution effect. Banks were less likely to form an interlock tie if they were already connected through a local clearing house, or if only one party was associated with the clearing house, the state bankers’ association, or the national bankers’ association. Yet, two previously unconnected banks were more likely to form an interlock tie in a city with a large population, a high percentage of foreign-born residents, a high level of inequality, a high level of density of existent interlock networks, or a high percentage of banks affiliated with the state bankers’ association. In addition, banks located in a state where the deposit guarantee law had been passed were more likely to form interlock ties.

CMP Analysis of the Formation of Interlock Ties

Note: Clustered standard errors are in parentheses.

p < .05; **p < .01; ***p < .001 (two-sided).

Model 2 tests the main effects of the independent variables. Consistent with prior studies on board interlocks, banks of dissimilar size were less likely to form interlock networks, and large banks were more likely to form interlocks with each other. The results also show that the issuance of currency substitutes had a significant positive effect on the formation of an interlock tie (b = .478, p < .001). However, mutual lending did not significantly increase the chance of interlock formation (b = .058, n.s.). Model 3 tests the interaction effects between the two types of collective action and the size difference of the two banks in a dyad. The results show a significant negative interaction effect between mutual lending and bank size difference (b = −.074, p < .001), and a significant positive interaction effect between the issuance of currency substitutes and bank size difference (b = .034, p < .05), on interlock formation. Banks of dissimilar size were even less likely to form interlock ties with each other in places where mutual lending had been organized, but the negative tendency was mitigated in places where currency substitutes had been issued. These results lend support to Hypotheses 1a and 2a, suggesting banks in places where different types of collective action were organized show divergent tendencies of tie formation for bank pairs of dissimilar size.

To test for the robustness of the findings, Model 4 includes the interaction effects between the two types of collective action and the size product of two banks in a dyad. The significant interaction effects between size difference and the two types of collective action remain robust. Moreover, the interaction effect between mutual lending and size product is positively significant (b = .098, p < .001), showing that large banks had a significantly higher tendency to form interlock networks in places where mutual lending had been organized. But the interaction effect between the issuance of currency substitutes and size product is not significant (b = .011, n.s.). Overall, in places where mutual lending had been organized, large banks were more likely to form interlocks with each other but less likely to do so with small banks, resulting in a stratified tendency in the formation of interlocks. In places where currency substitutes had been issued, however, large and small banks were more likely to form interlocks.

To demonstrate the magnitude of the coefficients in Model 4, I graph the interaction effects between size difference and the two types of collective action in Figure S1 in the online supplement. Bank pairs in a city where mutual lending had been organized were more likely to form interlock ties than those in other places if their size difference was less than twice the average bank size in that city. When their difference in size was more than twice the average bank size, banks showed a lower likelihood of forming interlock ties. In cities where private money had been issued, banks had a consistently higher tendency to form interlock ties, regardless of their size difference. Finally, Model 5 further tests the robustness of the findings by excluding from the sample banks that formed between 1908 and 1910. The pattern of coefficients remains similar in this model.

The Atanhrho values reported at the bottom of Table 1 are the arc-hyperbolic tangents of rhos, making them unbounded by −1 and 1. A positive value of the Atanhrho indicates that unobserved factors are affecting two outcomes in the same direction. The Atanhrho value between Equations 2 and 3 is consistently negative, indicating that unobserved factors led to the organization of one type of collective action and reduced the chance of organizing the other. The Atanhrho value between Equations 1 and 3 is positive in Model 1 but turns negative after controlling for the main effects of independent variables. These results indicate that the previously omitted variables, such as the size product and issuance of currency substitutes, play a dominant role in contributing to the positive correlations between residuals of Equations 1 and 3 in Model 1. After controlling for the independent variables, the unobserved factors left in the residual terms affect the issuance of currency substitutes and the formation of interlock ties in opposite directions. Importantly, the CMP estimation accounts for such an unobserved effect and then tests the hypotheses. The hypothesis testing was robust, because I could check for support for the predictions even after controlling for correlated residuals between control equations and the main prediction equation.

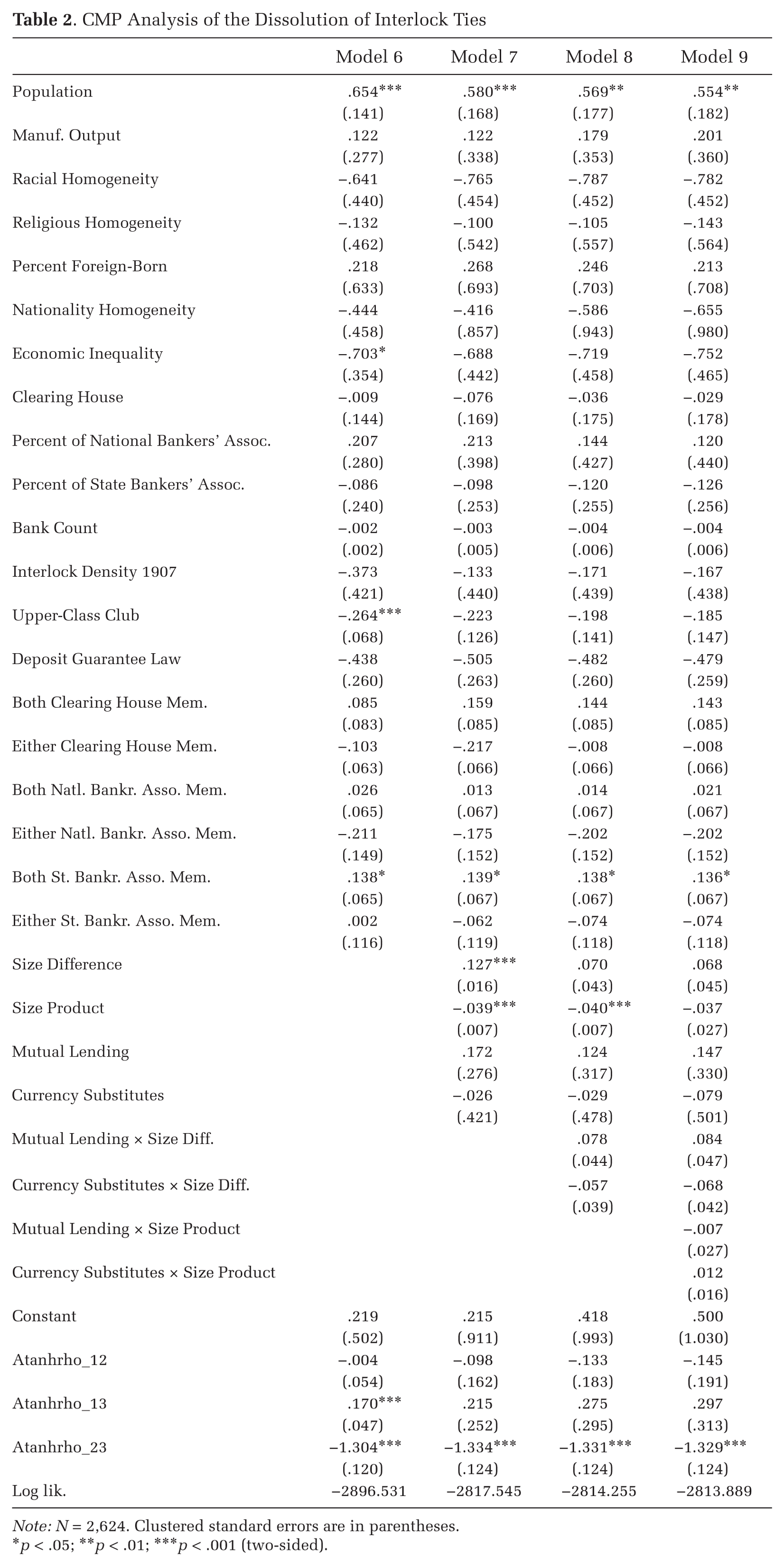

Table 2 presents the CMP analyses for the dissolution of interlock networks. Model 6 shows the baseline model. Interlock networks between two banks were more likely to dissolve if they were located in a large city and both were members of the state bankers’ association. On the other hand, the interlock networks were less likely to dissolve in cities where the inequality level was high and there were upper-class clubs. Model 7 includes the main effects of independent variables. Reversing the findings of network formation, it shows that interlock ties between similarly sized banks, especially large ones, were more robust.

CMP Analysis of the Dissolution of Interlock Ties

Note: N = 2,624. Clustered standard errors are in parentheses.

p < .05; **p < .01; ***p < .001 (two-sided).

Model 8 reports the interaction effects between the two types of collective action and the size difference. It shows that the interaction effect between bank size difference and mutual lending has a positive coefficient that, however, is not statistically significant (b = .078, n.s.). The coefficient of the interaction effect between size difference and the issuance of currency substitutes is negative, but it is also not statistically significant (b = −.057, n.s.). Hypotheses 1b and 2b are not supported. Model 9 further includes the interaction effects between the two types of collective action and size product and shows that neither interaction effect is significant.

Consistent with the estimation results of interlock formation in Table 1, the Atanhrho value between Equations 2 and 3 is negative; the Atanhrho value between Equations 1 and 2 is consistently insignificant; and the Atanhrho value between Equations 1 and 3 is positive in Model 6 but turns insignificant after controlling for the main effects of independent variables. These results indicate that, after controlling for these variables, the dissolution of interlock networks is no longer significantly correlated with unobserved factors that affect the incidence of the two types of collective action.

Two issues regarding these results merit further discussion. First, my results suggest that the formation of interlock networks was more sensitive to the collective action experience than was their dissolution. This finding is consistent with the asymmetrical character of network formation and dissolution processes that prior studies have shown (Broschak 2004; Yue 2012). Two lines of research help explain the asymmetry. One is the imprinting theory, wherein prior scholars have found that the influence of institutional forces is particularly strong during the formative stage of a relationship (Marquis 2003; Marquis and Tilcsik 2013). The other is “broken ties” studies, wherein researchers have found that a substantial proportion of broken interlock ties between firms are caused by accidents such as directors’ death, retirement, or change in place of employment (Palmer 1983; Palmer et al. 1986). Thus, after a relationship has been established, accidental factors may confound the impact of the institutional forces, making network dissolution a more complicated process than its formation. Future studies should test whether the dissolution of interlocks is sensitive to institutional forces by excluding accidentally broken ties.

Second, although controlling for the size product of the two banks in a dyad helps mitigate the concern that the analysis treats dyads between large banks in the same way as those between small banks, it is useful to directly analyze the chances of interlock formation for three groups, large and large banks, large and small banks, and small and small banks, in cities where the two types of collective action took place. I thus define large banks as those whose size is above the medium bank size in a city, and small ones as those whose size is at or below the medium. Table S5 in the online supplement clearly shows that large banks were more likely to form interlock ties, especially in places where mutual lending had been organized. Large and small banks were less likely to form interlock ties. This tendency was especially strong in places where mutual lending had been organized, and less so in places where currency substitutes had been issued. Finally, small banks showed a lower tendency to form interlocks with each other, but in places where mutual lending had been organized, they were more likely to form interlocks. The exclusion from large banks may have limited small banks’ candidate pool of directors to other small banks. Together, this set of analyses of the interlock formation between banks of different sizes provides additional support for Hypotheses 1a and 2a.

Conclusions

In contrast to the existent literature, which depicts interlock networks as the source and collective action as the object, this study portrays interlock networks as the target and business collective action as a source of influence. Building on the classic collective action problem of the exploitation of the great by the small, I argue that large market players have incentives to respond to this problem in the post-collective action period, and their responses should result in structural changes in the relationship between large and small market players. Yet, the type of collective action matters. The experience of being supported by one’s community during a collective action makes business leaders more aware of their responsibility toward their community. Therefore, in the post-collective action period, large market players tend to favor the strategy of assisting small players, and they are also more likely to build relationships with small players. In contrast, the experience of single-handedly controlling a market enhances the perceived self-efficacy of large businesses and reduces the perceived need for community support. In the post-collective action period, large market players are more likely to propose eliminating small players. Anti-small player sentiment leads to a stratified pattern of network formation, with large market players constituting a dense core that is increasingly distanced from their smaller counterparts.

My findings suggest that, rather than thinking of network structures as a static predictor of business mobilization, we ought to conceptualize them as dynamic and evolving in relation to the particular experience of business mobilization. As such, this article expands the reach of research on collective action and social networks, contributes to the literature on the spillover effect of collective action, and suggests an endogenous source of interlock evolution. It also has implications for the debate on the relationship between business and society broadly.

This article reveals a dynamic relationship between network structures and collective action. Just as network structures affect the incidence of collective action, collective action provokes changes to existent networks between business actors. Past research has actively examined the link between interlock structures and business collective action, but scholars tend to treat network structures as given and have not assessed the potential reciprocity between collective action and interlock structures. In addition, although a number of scholars allude to the spillover effect of collective action on mobilization infrastructures, it remains unclear whether and how collective action changes network structures. This article shows that large market players’ responses to the free-riding problem in collective action provide one mechanism through which collective action can affect networks. Future research studying the relationship between social networks and collective action should examine the entire causal system of how networks affect the incidence of collective action, which in turn generates feedback effects on the next-round development of network structures.

By studying organizational responses to the collective action problem in the post-collective action period, this article contributes to an emerging line of studies on the spillover effects of collective action. Some studies have examined the direct consequences of collective action, but an emerging line of work suggests that collective action has indirect and unanticipated consequences. Beyond intended projects, collective action mobilized by activists in a market can signal consumer preferences (Ingram, Yue, and Rao 2010), push untargeted organizations to act (Yue, Rao, and Ingram 2013), and promote the diffusion of social management devices (McDonnell, King, and Soule 2015). This article shows that collective action can have spillover effects on inter-organizational networks by shaping business leaders’ sense of their responsibility toward their community.

This article contributes to the literature on the evolution of interlock networks by emphasizing endogenous institutional forces as drivers of structural change. Prior studies have found that the institutional context within which organizations are embedded shapes the evolution of corporate interlock networks, but they focus on exogenous factors such as a city’s history (Marquis 2003), technological breakthroughs (Yue 2012), and political changes (Stark and Vedres 2012). My results show that the institutional factors that shape interlock evolution can also be driven by organizations’ own actions. This endogenous account has an important implication for understanding the dynamic relationship between collective action and network structures, as it suggests that forces of structural decline are sometimes built into collective action that seems robust (and vice versa).

Finally, scholars have debated the role of businesses in society generally. While some view corporations as an intrinsically social institution with the potential for public benefit (e.g., Dodd 1932; Elkington 1998; Kaysen 1957), others argue that they tend to promote mostly self-serving behavior and narrow interests (e.g., Berle 1931; Jensen 2002). The roles of business are related to the structures that link business elites. Judis (2001) argues that a cohesive group of U.S. business elites promoted the development of democratic reforms during the Progressive Era, the New Deal, and the 1960s, whereas Mizruchi (2013) finds that the lack of cohesion among business elites in recent decades has inhibited them from mobilizing to address issues such as tax increases and health care provisions that are of concern to their communities. If the collective action experience alters the formation of elites’ networks, banking elites who were helped by their community might have become more cohesive over time, and they might have utilized their stronger mobilization capabilities to pay something back to their community later. In these communities, the business sector serves as an essential social institution that contributes to the broad public benefit. But businesses that seek to independently control a market may become increasingly detached from their community, because business leaders may see little need to engage with it. As a result, business elites may gradually drift into a small, isolated group that promotes self-preserving behavior and narrow interests. Thus, altering the structure of business networks may be one mechanism through which early collective action sets the tone for the business–society relationship in the long run.

Footnotes

Acknowledgements

I thank seminar participants at MIT, University of Chicago, University of California-Berkeley, University of Southern California, the 2nd Economic Sociology Conference at Yale University, and the Social Movements and the Economy Workshop at Kellogg School of Management for their advice. I am grateful to the editors and anonymous reviewers of ASR for their helpful suggestions.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.