Abstract

The U.S. antitrust agencies’ Horizontal Merger Guidelines are approaching their half century mark, having progressed through three earlier versions to their current 2010 form. Recent reports promote the contention that the enhanced sophistication and transparency of the newer versions have led to improved policy results. This study questions this conclusion by examining recent retrospective merger case evidence as well as agency policy and practices, in light of long-held Supreme Court dicta.

I. Introduction

Over a nearly 50-year span, the U.S. antitrust agencies have developed four merger policy guideline statements designed to inform the business community and general public of the current interpretation of Section 7 of the Clayton Act, and the prevailing agencies’ intentions regarding enforcement. While significant changes have occurred across these four statements, one common thread is clear: that with each iteration, the Horizontal Merger Guidelines (Guidelines) have become progressively more sophisticated in their economic analysis of the potential competitive effects of mergers being examined. This study examines the question of whether the enhanced sophistication of the more modern Guidelines has added a significant positive contribution to merger policy. A description of the challenges facing the modern Guidelines is presented in Section II. Section III provides an alternative view of the Guidelines’ past success, and a proposal toward the redesign of the Guidelines. Part IV offers some concluding ideas.

II. Continuing Problems Remaining with the New Guidelines

Section 7 of the U.S. Clayton Act proscribes mergers which substantially may lessen competition. The language of the act leaves open to interpretation, by the courts and the antitrust enforcement agencies, the exact nature of the circumstances under which there exists a violation, and varying interpretations have been offered. In 1968 the Department of Justice presented the first set of Guidelines, which followed a strict structuralist approach whereby markets were classified as “highly concentrated” or “less highly concentrated,” and the decision to challenge a merger between rivals was based largely on this classification and the market shares of the firms in question. Subsequent Guidelines in 1982 and beyond refocused the analysis increasingly toward entry conditions and efficiency effects. With the advent of the 2010 Guidelines, market concentration and market definition had yielded their primacy to a heightened attention to the competitive effects of a merger.

A. Transparency, Simplicity, and Accuracy

The overview to the 2010 DOJ Guidelines states that the Guidelines are “intended to assist the business community by increasing the transparency of the analytical process underlying the Agencies’ enforcement decisions.” 1 In an effort to achieve this, the Guidelines offer extended lists of the types and sources of evidence that the agencies will consider; the components of the analysis (e.g., market definition); and the theoretical underpinnings of the role(s), definitions, and measurement tools (e.g., significant and nontransitory increase in price [SSNIP], upward pricing pressure [UPP]) of these components. The Guidelines also offer that the analysis of any merger “does not consist of uniform application of a single methodology,” and that reasonably plausible competing evidence, and hypotheses will be examined. 2 The agencies would also make use of various projections of future values (e.g., market shares) where necessary, and recognize that precise, detailed, unbiased information (e.g., for entry and efficiency data) may be difficult to acquire. Moreover the Guidelines offer additional analytical sections on new focal points (e.g., price discrimination, targeted customers, powerful buyers), which Assistant Attorney General Varney at the time described as “reflecting actual practice and…accumulated experience.” 3

Moreover, nearly a decade prior to the issuance of the latest Guidelines, the Federal Trade Commission (FTC) began issuing reports designed to enhance the transparency of their merger enforcement program. Additional studies from former FTC staff members have also been provided in academic journals. 4 These reports focus on the data collected by the FTC for nearly all horizontal merger cases filed and/or investigated by the agency over various years covered by the more recent sets of Guidelines. They provide statistical analysis of the outcomes of the investigations as well as correlations between various guideline data and case outcomes. These yield insights of a probabilistic nature into the importance of certain markers examined by the agency in their decision making. As one report indicated, “Government policy is more effective when the enforcement regime is transparent because the economy benefits from the resulting reduction in transactions costs.” 5

The statement above may not always be accurate. While transparency may constitute a necessary condition, it may not be sufficient. Such appears to be the case when examining the most recent Guidelines. Since the introduction of the first merger Guidelines in 1968, each subsequent set of Guidelines has demonstrated increasing complexity. The original Guidelines held a mere seventeen pages, over half of which were designated to vertical and conglomerate merger case analysis. This contrasts sharply with the 2010 horizontal guides which provide analysis for approximately 68 pages. 6

While transparency is a laudable goal for any government agency, and certainly provides some benefit to the interested parties, several authors have argued that the additional complexity imposes an implicit cost on the business community through the heightened risk assumed by merging partners due to the greater uncertainty of a challenge by the government, or explicit cost through the direct additional legal and consulting expenses firms face in an attempt to reduce the uncertainty. 7 Notably, with the advent of multiple methods of evaluating mergers, introduced in the 2010 Guidelines, the effect may be substantially to increase this cost. Here, transparent but increasingly complex Guidelines may provide costly (and perhaps poor) guidance, with the “benefit to the economy” in part proving to be a transfer to the expanded industry of consultants.

In addition, Brennan offers that the newest Guidelines indicate a broadly defined goal of maximizing welfare. As such, he demonstrates their poor guidance through an analogy to speed limit signs reading “drive at the speed that maximizes the expected welfare of all drivers. The police…will be taking all forms of evidence before writing a ticket.” 8 The analogy is apt. His primary focus is on the recognition that while accuracy in agency decisions is important, the ex ante benefits of (simpler) guidance needs to be balanced with the ex post costs of inaccuracy. Here the inaccuracy may take one of two forms: (1) challenges of benign mergers (a Type I error) or (2) clearance of mergers that have significant anticompetitive effects (Type II errors). He concludes that at the margin the Guidelines (and other areas of antitrust enforcement) can be simplified, perhaps with a limited decline in accuracy. Implicit here is an axiomatic assumption that there exists a trade-off between accuracy and simplicity. This assumption may or may not prove to be accurate, and will be examined more carefully below.

B. Theory and Legal Problems

Advances in the Guidelines have faced other challenges prior to and after their presentation. Meehan’s (1977) survey of the early literature defends the 1968 Guidelines’ rules approach versus the discretionary Guidelines approaches that were to follow. 9 In identifying one of several concerns, he argues a cost-benefit approach against the costliness of discretion in gathering and verifying information, and the diminished benefit arising from the uncertainty in much of the measurement involved. Miller (1984) takes a more forceful stance that the 1984 revision of the Guidelines, by incorporating efficiency in the analysis, bordered on executive branch legislation in that courts were unlikely to test this doctrine since the government was not bringing cases where efficiencies were seen to be great. 10

Paralleling these legal and economic criticisms are recent concerns by Carlton (2007), Keyte and Schwartz (2011), and others regarding the 2010 Guidelines. 11 Keyte’s principal concerns involve two issues. The first is the question of the Guidelines’ inconsistency with the legal standards established by the Clayton Act and subsequent case law. Here it is forcefully argued that market definition, which takes a diminished role in the latest Guidelines, is statutorily required by the Clayton Act. Moreover, the authors demonstrate that the Supreme Court has required that a relevant market be established, and has rejected as inadequate the acquired-acquiring test that focuses on the decline in competition between two merging firms. It is further argued that the new UPP test, used in the hypothetical monopoly analysis of mergers, moves substantially away from the well-established “reasonable interchangeability” standard by condensing the competitive effects analysis to the examination of as few as two firms rather than to a more appropriate market or submarket.

The second issue involves the economics and application of the new UPP technique. A principal concern lies in its ability to reliably screen for anticompetitive effects arising from mergers. Part of this is brought out by Martin, 12 who argues that the examination of whether a hypothetical monopolist can raise prices above current levels tends to ignore existing market power already being exercised. This further contradicts the court’s incipiency doctrine which aims to stop, early on, the trend toward a lessening of competition. Moreover, Keyte argues that the UPP measure relies on other statistics which are difficult to measure (e.g., diversion ratios), is unable to capture market dynamics, and is capable of yielding questionable results as to anticompetitive effects. 13 In addition, he poses the concern that the UPP measure does not face the “timely, likely and sufficient” requirement that is part of entry analysis and, as such, along with its unduly narrow market definition, may significantly expand the propensity for overzealous enforcement of otherwise benign mergers. In sum, the shift from market definition to UPP limits the proper scope of market definition and incorporates additional error-prone analysis. Moreover, as the new Guidelines allow for the discretionary use of either UPP or market definition, this enhanced agency flexibility may reduce clarity, transparency, and confidence of the business community.

In rebuttal, former Assistant Attorney General Christine Varney argued that UPP diversion ratios focused on two goods were consistent with the incipiency doctrine’s efforts to stop the anticompetitive unilateral effects of some mergers, citing the courts’ position that allows for narrowly defined markets. She also defends the 2010 omission of the 1992 Guidelines’ presumption that diversion ratios of merging firms with combined market shares in excess of 35% are significant. 14 She indicates that the lack of this statement does not indicate that below 35% constitutes a “safe harbor.” In light of the earlier standard, this claim rings as somewhat hollow support for incipiency. A statement indicating that above 35% (or some similar percentage) was presumptively significant would, if enforced, more powerfully endorse the doctrine.

Further issues arise with the incorporation of entry and efficiency analysis into the more modern Guidelines. Since 1984, the Guidelines have called for the examination and consideration of potential procompetitive benefits arising from cognizable, merger-specific efficiencies along with the potential anticompetitive effects arising from proposed mergers. This approach generates concerns on several well-known fronts. First it relies heavily on the expertise of the regulatory agencies and their ability to gather the appropriate (often firm-specific) data and correctly estimate future behavior of the firms in question. Meehan cites studies finding that efficiencies are often not a primary goal cited by managers involved in mergers and, more importantly, that in nearly half of the cases examined, no attempt was made to achieve potential economies. Moreover, he offers evidence that the gain in market power accrued from these mergers was a primary cause for the diminished desire to achieve the efficiencies that were available. His solution to the efficiency defense question called for a modification of the 1968 Guidelines to ignore mergers in which the industry four-firm concentration ratio fell below 50% wherein the threat of market power is diminished. In addition, this would allow for significant economies to be achieved where they are most likely to occur, that is, in mergers among small and medium sized firms. This approach was supported by numerous studies indicating actual concentration levels that often greatly exceeded that which was dictated by minimum efficient scale requirements, and by more recent studies by Sirower (1997) and others showing that many efficiency driven mega-mergers of the 1990s failed to achieve expected economies. 15

Recently, Kwoka has argued that the evaluation of conventional efficiencies (e.g., economies of scale) has been greatly improved during the past decade, and that the focus of efficiency claims has changed, turning more toward dynamic efficiencies, quality changes, and vertical economies, among others. While promoting substantial agency gains in cost-efficiency analysis, citing evidence from the AT&T and T-Mobile proposed merger, he nevertheless notes that ambiguity, uncertainty, and divergent analyses remain, and that “the newer types of efficiencies confront the Agencies with novel analytical challenges reminiscent of the difficulties faced many years ago.”

16

In fact, Kwoka points out that in dynamic (innovation) efficiencies cases the agencies often define an “innovation market” within which market shares and concentration of innovative effort can be calculated and competition and innovation output assessed. Of course, these concepts are easier to state than to work with: the definition of an innovative market…the meaning of market share…all defy easy explanation and measurement. The well-known difficulties include the lack of a reliable method for measuring the ultimate objective of technological progress.

17

Similar issues arise with the examination of market entry and its role in the analysis of mergers. The conventional wisdom that the condition of entry into a market influences the degree of competitiveness of that market, both before and after a proposed merger, is not in dispute. The estimation of condition of entry, along with the question of whether a measure of the degree of entry difficulty or a simple dichotomous “easy” versus “difficult” designation is necessary for a correct decision to be generated by the agencies remain as critical questions. Moreover, the appropriate weight to be given to these entry measurements as a factor in the overall evaluation of each case remains as a critical question. Given the evidence to be described below, these questions appear to be, to date, unsatisfactorily resolved.

C. The Evidence

In an exhaustive review of the literature to date Kwoka provides an examination of the effects of mergers and the effectiveness of merger policy. He compiles the works of forty-seven studies, examining 60 mergers wherein prices have been observed for over 100 specific products. These works, culled from a broader set of retrospective studies, included industries ranging from cereals to hospitals, with mergers occurring between 1976 and 2009. 20 All contained premerger and postmerger price data and held an appropriate control group, and used a difference in differences technique to examine the effect of each merger on prices. Kwoka reports that the mean price change for all studies was a 4% price increase (relative to the control group), indicating that overall the mergers were not competitively neutral. Moreover, more than 60% of these markets showed price increases, and the mean price increase in this group was 8.9%, which is considerably above the commonly used merger policy benchmark of 5% (e.g., for the SSNIP test). 21

In addition, Kwoka’s work compiles the data to achieve average price results for forty-two mergers wherein the FTC and DOJ either cleared the merger or challenged it (with a divestiture remedy, conduct remedy, conditions, or opposition which was overturned- e.g. by another agency). His results from the forty-two mergers appear in Table 1.

He finds encouragement in that thirteen of the fifteen cases wherein there exists an agency challenge to a merger, the postmerger price had increased, signifying that a challenge was appropriate, albeit insufficiently weak. In addition, in one of the two cases where price fell, a divestiture challenge had occurred. As a result, fourteen of fifteen (93%) of challenges had correctly identified problematic mergers. 22 In addition, the agencies correctly did not challenge six of the eight (75%) of the mergers where the postmerger prices had fallen. The conclusion drawn was that overall the agencies were highly successful in avoiding Type I errors (challenging benign mergers).

Where Kwoka finds weakness in agency enforcement lies in the fact that only thirteen of thirty-four anticompetitive mergers were challenged, resulting in a large number (62%) of Type II errors. Among several observations which he draws from the analysis are that the “policy practice is considerably more tolerant than the stated Horizontal Merger Guidelines would imply” 23 and that “remedies, generally fail to prevent post-merger price increases.” 24 Additionally, regarding structural characteristics of the industries in question, he finds a weak link between concentration measures, significant rivals and enforcement decisions. In a separate study, using the retrospective price data of the mergers examined above, he reports that the use of structural variables alone accurately predicted the vast majority of anticompetitive mergers, but significantly overpredict benign mergers to also be anticompetitive (creating a large number of Type I errors). 25 From this, and the agency success rates above, Kwoka concludes, that while “there is value to market structure criteria as an initial screen,” there is “considerable added value in the agency investigation and decision process.” 26 Given the nature of these highly mixed results, a reexamination and different conclusion will be offered in Section IV below. First, one additional important problem arising from the merger Guidelines and their enforcement needs examination.

D. The Growth of Industry Concentration

Concern over industrial concentration has been a focal point of the U.S. antitrust laws since their inception. The Sherman Act, written during a period of rapid industrial growth, had at its core the fear of emerging economic power by monopolistic and oligopolistic firms.

27

The Clayton Act, and its forward looking “where the effect may be” statement, identified a similar concern with respect to mergers and other business conduct. Chief Justice Warren, in the Supreme Court’s interpretation of the Cellar-Kefauver revised Section 7, wrote the following: It is apparent that a keystone in the erection of a barrier to what Congress saw was the rising tide of economic

The levels of industrial concentration and market competition in the U.S. have evolved unevenly over the past century. Earlier studies by several authors 29 demonstrated that an extended period of relative stability in concentration existed in the decades prior to the first Guidelines. These studies each endeavored to identify the proportion of the nation’s income arising from competitive markets and various other categories of monopolistic and oligopolistic markets wherein market power exists. The studies together demonstrated that while industry concentration may have increased rapidly during the first part of the 20th century, competitive markets steadily prevailed in generating roughly sixty percent of the national income between 1940 and 1960. Shepherd’s work furthered the analysis with two important findings for the next two decades. The first held that the share of national income generated by competitive markets had risen to over 75% by 1980, indicating a decline in industry concentration during the period. His second, more controversial finding was that 40% to 55% of that change was driven by heightened antitrust activity. 30 Similar studies for the 1980s and 1990s have not been developed, but during this period competing forces were in evidence. First, a wave of industry deregulation coupled with a sharp rise in foreign competition during the 1990s tended to further increase the role of competitive markets in the economy. This tendency was in part offset by a generally less aggressive antitrust policy stance and ensuing merger waves. A substantial portion of these mergers, as seen in the evidence below, would be classified as horizontal in nature and thus tending to increase market concentration during the two decades.

More recently, studies have examined concentration level changes during the early part of this century. Using a new data set of firm-based industry Herfindahl index measures created by Hoberg and Phillips, 31 a report by Francis and Knutson finds that the proportion of industries identifiable as highly concentrated had risen from 25% to nearly 33% between 1996 and 2015. 32 They also find that market concentration for nearly two thirds of the 1,700 publicly traded firms in the data had risen during those years. This result is supported by a similar study based on 900 U.S. Census industry sectors wherein four firm concentration ratios also rose in two thirds of the industries during 1997–2013. 33

Appropriately, each of the four sets of merger Guidelines has paid attention to various measures of market concentration. Under the earliest Guidelines where the focal points of this attention were industry four firm concentration levels (CR4) and the market shares of the two merging firms, these were determinative as to whether an agency challenge was to occur. As the Guidelines progressed, the concentration measure of choice moved to the Herfindahl index, and the focus of the guides increasingly moved toward other indicators of anticompetitive behavior. This refocusing has unfortunately relegated concentration from a sufficient (1968) condition to a necessary presumptive (1982–1984) or merely illustrative (2010) role. 34 One conclusion to be drawn from the evidence above is that the more recent Guidelines, or at least their enforcement, has been ineffectual in controlling the “rising tide of economic concentration.”

III. An Alternative View

A. A Reexamination of the Evidence

A further analysis of the earlier research allows for an alternative interpretation of the evidence presented and enables a more forceful conclusion regarding the Guidelines. First, as noted above the Guidelines have failed to arrest the increasing level of industry concentration in the U.S. In addition, FTC reports indicate that a high percentage of mergers remain unchallenged where only a few significant rivals remain postmerger. For mergers investigated in years between 1996 and 2011, one FTC report demonstrated that approximately one-third of mergers leaving only five significant rivals (6-to-5 mergers) were challenged, with 5-to-4 and 4-to-3 mergers being challenged in 64% and 77% of cases, respectively. 35 This indicates that incipiency concerns (perhaps) begin in earnest only when the effect of the merger is to leave three or four significant firms. Moreover, the data of a second FTC study show that during the 1989 to 2012 period, among the 150 cases of mergers having three or two remaining firms (within which 84% were also judged by the agency as having barriers to entry), 30% were not challenged, calling into question whether the incipiency doctrine is even present in the agencies’ decision making. 36

In addition, an alternative conclusion can be derived from Kwoka’s analysis of the success of the agencies in avoiding enforcement errors. Using his Table 1, above, he demonstrates that 93% (fourteen of fifteen) of agency challenges appear to be correct. Using this same study and methodology to examine agency cases that were not challenged, the table shows that fully 78% (twenty-one of the twenty-seven mergers) that were not challenged led to higher prices. Moreover, looking at the entire group (forty-two) in the study, the agencies challenged 36% (fifteen), while arguably they should have challenged 83% (thirty-five) of these cases that lie on the enforcement margin. In addition, of the fifteen challenged, 87% (thirteen) had ineffectively weak policy as seen by the postmerger rise in price. For the entire group, if we allow for all fourteen challenges and six nonchallenges to be judged as correct, this leaves more than half (52%) of the agencies’ judgements to be incorrect. Given that Kwoka’s own findings indicate that 45% percent of the entire group of mergers resulted in prices rising (relative to their control group) by more than 5%, this severely calls into question the position taken that the agencies’ analysis (beyond concentration levels) provide significant value added.

B. An Alternative Set of Guidelines

Numerous antitrust scholars have called for simpler Guidelines to merger policy. Shepherd 37 has called for a return toward the initial (1968) Guidelines using the market share of the newly merged firm as a central bright line. Brennan 38 notes that using FTC data on the number of significant rivals yields a strong prediction of agency challenge policy between 1996 and 2003. The decades-long debates surrounding theoretical and empirical elements of the discretionary Guidelines, coupled with the recent evidence of the agencies’ weak performance in their attempts to protect society from anticompetitive mergers provides compelling reasons for reconsidering a simpler, bright lines merger policy. Moreover as noted above, Brennan’s perception of the arc of merger analysis toward greater accuracy at the expense of simplicity implies an axiom that a trade-off exists between the two. Using the data compiled by Kwoka’s retrospective analysis in conjunction with the FTC’s “transparency” reports data, a reexamination of the evidence can demonstrate that a trade-off is not inevitable.

For purposes of exposition, a new proposal for the Guidelines is introduced. This very simple guideline incorporates a bright lines approach using only post-Herfindahl (H) and change in Herfindahl (ΔH) measurements. As such, the approach will return us toward the first step within the more uniform approach of the 1992 Guidelines and toward the original 1968 Guidelines themselves. Shepherd’s call for market share data and Brennan’s for significant rivals would also clearly simplify the guides, but the choice of H is made for several reasons. 39 The first is simply to maintain consistency with the enforcement agencies’ choice of H since 1982 as its measure for indicating industry concentration. While subject to its own shortcomings, the Herfindahl index may hold some greater connection to the theory of oligopolistic markets and thereby to concerns behind possibly anticompetitive mergers. 40 In addition, while FTC investigation data is provided for several different structural variables, the focus on H enables the use of data sources which are most directly capable of generating insights into the policy question at hand, namely, whether the current Guidelines can be simplified without any trade-off in lost accuracy. Finally, it is the Supreme Court’s stated concern regarding rising economic concentration upon which this study is focused.

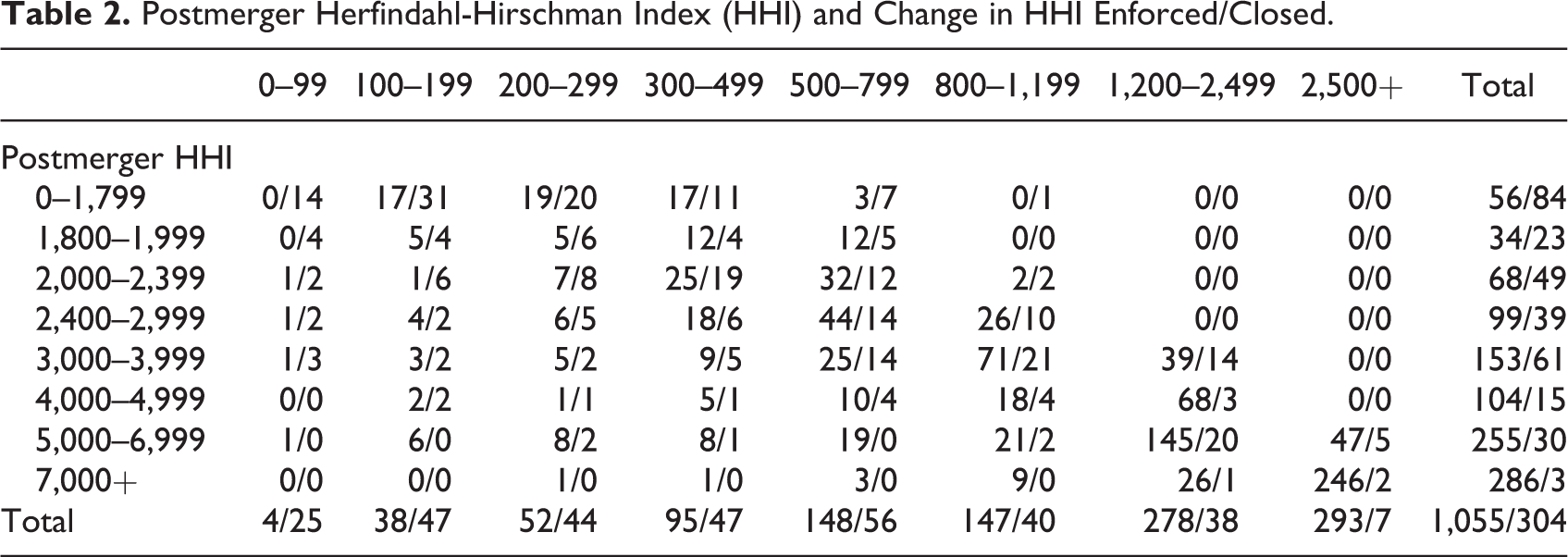

Above is introduced Table 2 from the FTC (2013) data examining those mergers receiving a second look which were subsequently either challenged or cleared by the agency. 41 The data is provided in a disaggregated form based on the mergers’ post-H and increase in H (ΔH) status. The data is an incomplete set of all mergers in that it does not include those mergers not warranting a second look. The latter mergers seem (and were judged) least likely to pose anticompetitive concerns and perhaps (for some) most likely to achieve cognizable efficiencies, and as such may have been appropriately cleared. Hence, the data does include those mergers seemingly at or near the margin of antitrust concern. The grid examines 1,359 markets impacted by 264 mergers where enforcement was questioned.

Postmerger Herfindahl-Hirschman Index (HHI) and Change in HHI Enforced/Closed.

Analysis of this data set by Kwoka (2015) finds that H is positively related to the likelihood of a challenge. The proportion of cases in each H group which were challenged rises from 40% for the 0<H<1,799 group to 99% for the H>7,000 group. A similar positive correlation is demonstrated between ΔH and the probability of a challenge, with the odds of a challenge ranging from 14% to nearly 99% as a merger’s expected increase in H rises. 42 While both correlations are positive, the less than universal challenge rates in high H and ΔH categories demonstrates the impact of further staff analysis.

A bright line at H>2,400 is now established as a new proposal for horizontal guidelines, wherein all such cases would be deemed to be subject to a challenge. This level of concentration maintains consistency with the 2010 Guidelines’ higher designation of H>2,500 as the threshold for highly concentrated markets, while enabling further empirical examination of the available reported data grouped above and below the H=2,400 level. Similarly, a second bright line is established at ΔH>200. Thus, in this proposal, either of two conditions, each indicating at least a partial failure with respect to the incipiency doctrine, would trigger a challenge. 43

During the 1996–2011 time period under study, the prevailing Guidelines led to second request investigations into the mergers encompassing the 1,359 markets indicated in the table. Of these markets, 78% (1,055) faced an agency challenge. Within the overall group, the new proposal establishes two categories, the first consisting of the 85 markets wherein H<2,400 and ΔH<200 (the upper left hand zone of the table), which would now fall into a “safe harbor” region, and the remaining 1,274 markets wherein a challenge would occur. In the first category, the FTC raised a challenge in twenty-four markets, while in the latter category, the FTC enforced a challenge in 1,031.

The proposed guidelines would, by definition, challenge none of the first category’s markets while challenging all in the second category. Assuming that the FTC’s past decisions were accurate in all cases, this would mean that the proposed approach would be in error 28% (24/85) of the time for safe harbor cases, while being in error slightly less than 20% (243/1,274) of the time in its challenges. Overall, the new proposal would be in error in 20% of the cases. Moreover, the error rates implied here would diminish, given any errors at all in the presumed perfect record of the agency.

These results appear to compare quite favorably with those resulting from Kwoka’s retrospective data analysis cited above, which demonstrated that an error was made in more than half of the cases wherein an agency decision occurred. 44 While the standard for measuring success has been changed here, the stated objective of the agencies’ 2010 Guidelines is “to reflect congressional intent” regarding incipiency, 45 and the Supreme Court’s interpretation of congressional intent was the desire to arrest “the trend…before it gathered momentum.” 46 As such, establishing quantifiable “incipiency guidelines” parallels, and likely lies in close proximity with, the goals of regulating postmerger prices, and the use of such a standard parallels, and may (as seen here) improve upon, the enforcement agencies’ success in achieving the desired results. 47

In short, the proposed guidelines would perform comparably with past agency performance with respect to Type I errors, generating 28% errors versus the 25% error rate shown in the retrospective studies. The proposed guides, though, would aggressively challenge 20% (243) more mergers in its more highly concentrated markets zone. While some of these might constitute erroneous Type I challenges, the evidence of Kwoka and others provides a clear indication that this is precisely where too many errors lie in recent decades of enforcement practice. As such, Type II errors can be substantially decreased. Moreover, to the extent that prevailing economic or legal analysis indicates that an adjustment needs to be made (as was the case with the higher H values used in the 2010 Guidelines) this modification can be made simply, clearly and transparently to the business community and general public.

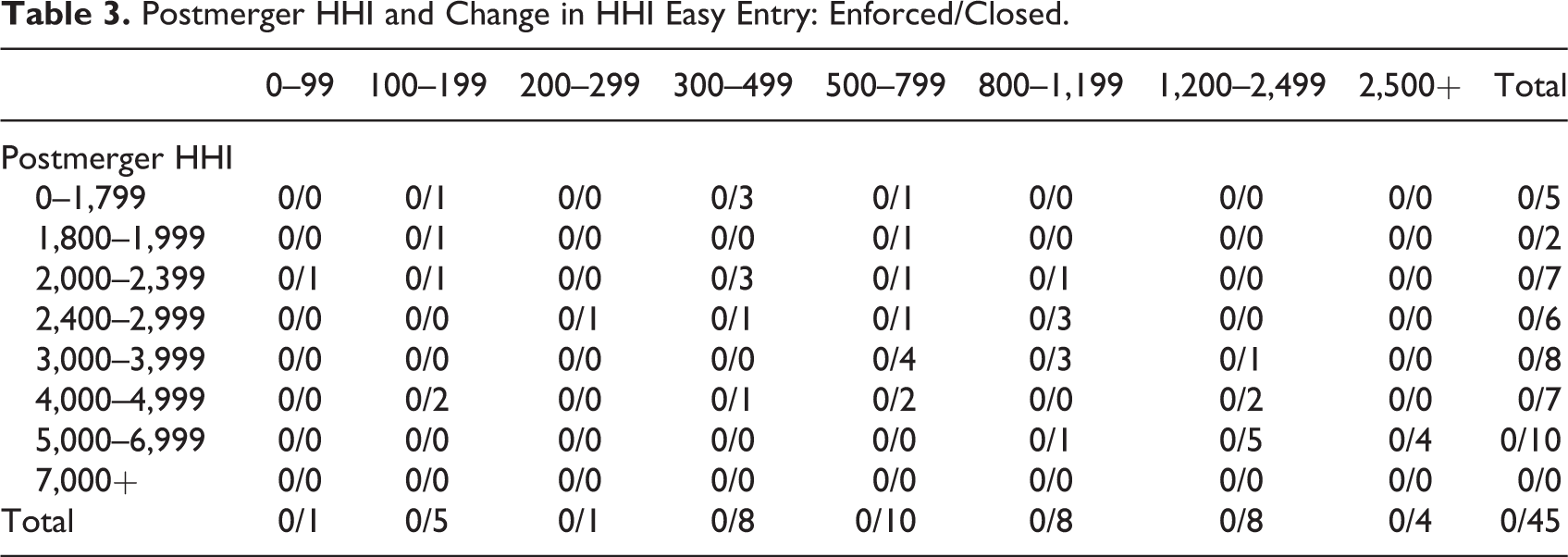

The value of this simpler approach can also be seen by reexamining FTC (2013) data concerning other variables and their roles in past enforcement decisions. The FTC data regarding the application of market entry analysis is provided in Table 3. 48

Postmerger HHI and Change in HHI Easy Entry: Enforced/Closed.

Here we find the enforcement record for all (forty-five) cases where markets were judged by the agency as being easy to enter. The most notable finding (also indicated by Kwoka) is that all of the above merger cases (1996–2011) were cleared. Given the earlier retrospective study data indicating a greater than 50% agency fail rate, along with the numerous difficulties cited above involved in accurately establishing market entry conditions, it is quite likely that some of these (Type II error) closed cases were driven by an erroneous easy entry evaluation, especially in the region beyond the safe harbor of the proposed guidelines. Applying the same H bright lines proposal as before, the new proposal would have called for a challenge in forty-one of the forty-five cases. Of those forty-one cases, twenty-nine (71%) were markets where both H>2,400 and ΔH>200 were indicated. Moreover, ten (24%) registered H>5,000 (nine of which also registered ΔH>1,200). In addition, within the proposed safe harbor, there were no cases where a challenge took place. This indicates a lack of any additional Type I errors for the proposed guidelines for these cases.

Similar results can be found for the 213 cases where entry conditions were judged to be difficult. 49 Here both the proposed and the prevailing guides resulted in high enforcement rates (99% vs. 82%) with thirty-five more cases which would have been challenged under the new proposal. Of these, twenty-six (74%) were markets where H>2,400 and ΔH>200 both occurred. One merger held both H>7,000 and ΔH>2,500. 50

Finally, with respect to the role which efficiency plays in the agency’s horizontal merger cases, a lack of data precludes an empirical analysis similar to that above. Kwoka’s examination of retrospectives in which he studies groups of mergers finds little support for the existence of widespread efficiency gains. His review finds a near zero average effect of mergers on efficiency (defined and measured in various ways by different authors). 51 This evidence is consistent with the at best weak support of efficiency gains from earlier studies cited above. Moreover, among several other salient questions, there exists ongoing debate over the proper weights to be placed upon different types (e.g., allocative, technical, dynamic) of efficiency in evaluating mergers, and its proper measurement (e.g., total vs consumer welfare) in merger cases and antitrust generally. 52 From this what remains clear is that the more recent Guidelines sacrifice simplicity and transparency for the sake of a presumption of enhanced accuracy. What remains unclear is any evidence that the well-intentioned efforts ultimately provide any meaningful benefit.

V. Conclusion

As a solution to the prolonged, ongoing (and increasing) problems arising with merger enforcement, Kwoka ultimately recommends the following: What is required is a better understanding of the a priori characteristics of incorrectly cleared mergers, and hence the sources of policy errors.

53

A simpler alternative has been offered here. This approach calls for a refocusing on the incipiency doctrine, as established by the Supreme Court, and on the defining objective of that doctrine, that of impeding the growth of economic concentration—as opposed to UPP or other measures—in an effort to deter a substantial lessening of competition. The approach supports this doctrine by making challenges less subject to error prone statistical and theoretical analysis in exchange for a reduced error inherent in relying on a simpler structural framework. Admittedly an imperfect test, it will tend to diminish errors by focusing on markets which are already nonatomistic or those where a significant change in concentration is proposed, thereby sharply curtailing Type II errors where most current mistakes occur. It also provides clarity to the business community, and other interested parties, as was the original intent of the 1968 Guidelines. This would be achieved in place of the perceived transparency that is currently obscured in a lengthy document that contains countless underlying models, analyses, data, and assumptions, much of which is hidden from view or found in numerous additional documents. The subsequent simplicity and clarity would be of benefit in that it would enhance the business community (and public’s) knowledge and trust in the agencies, and further remove any political or populist claims.

Using a simple “bright lines” guideline, involving post-Herfindahl index and index change measures only, improved performance in stopping anticompetitive effects of mergers in their incipiency can be achieved. This proposal is only suggestive. There exist other variants of this simple structural approach that could be chosen. 54 This approach calls for a significant step away from the three most recent sets of Guidelines and towards the original 1968 Guidelines and the Supreme Court dicta involving them. While there is substantial consensus that the Court erred in its earlier decisions to reject mergers where as little as 5% market control was achieved, and that the 1968 Guidelines’ rejection of mergers controlling only slightly higher market shares was also too restrictive, the proposed guideline would maintain the earlier structural framework, in conjunction with what has been the agencies’ selection over the past decade of more appropriate concentration levels.

Schwartz (1990) 55 has described cycles during the last century between peak periods of aggressive judicial enforcement of antitrust generally. Placed in historical context, the current proposal calls for a somewhat more aggressive policy toward horizontal mergers. Recent evidence of the leniency in enforcement coupled with the substantial loosening of the Guidelines, including the concentration standards and their role in the evaluation process, indicate that the antitrust pendulum has swung too far. Moreover, calls for more rigorous enforcement alone are insufficient. Whether the periods of lax enforcement are driven by limited resources or other motivations, a brighter lines policy is required. In short, the clarity and transparency of bright lines policy is needed to ensure greater compliance with the established standards, and the introduction of a new stronger enforcement period. Not only will this approach diminish efforts to manipulate and abuse the more complex Guidelines but it should also tend to limit the number of questionable merger proposals to begin with. This in turn will free the agencies toward a more efficient use of their limited resources.

Given the complexity of the latest Guidelines, the “guidance” provided by the 2010 Guidelines is stifled. Recently, even the Royal and Ancient Golf Organization, to the benefit of the professionals and amateurs (consumers) whom it seeks to serve, has proposed substantially simplified rules. The antitrust agencies’ drive for improved results should follow this approach. The time is right to step back to a stronger, simpler set of merger guidelines designed to effectively uphold the Supreme Court’s incipiency doctrine, and to reduce the extent to which far too many horizontal mergers taking place in the United States yield increasing economic concentration and anticompetitive effects in markets.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.