Abstract

Firms engage in mergers for many reasons, some of which create value for both the firm’s shareholders and society, some that create value only for the firm’s shareholders, and some that fail even to do that. A considerable body of research concludes that most mergers do not create value for anyone, except perhaps the investment bankers who negotiated the deal. For a merger to create value, it will usually be necessary that one or both parties is below minimum efficient scale or has valuable underutilized assets. Furthermore, unless heavy coordination and long-term commitment are required, many sources of value from mergers can be achieved through collaboration agreements or other contracts, with less risk to the firms and to economic efficiency. This article outlines the major sources of potential value in mergers, and indicators that can give us insight into a merger’s true motives and its likelihood of creating value.

I. Introduction

A key focus of research in both corporate strategy and antitrust is whether mergers create or destroy value. In corporate strategy, “value” is typically defined as meaning shareholder value, irrespective of whether the firm is publicly held (where shareholder value refers to the total shareholder returns of investing in the firm) or privately held (where value can refer to anything that increases the utility of the owners). In antitrust, the main concern is whether increased market power will be used to raise prices and reduce economic efficiency and consumer welfare. In practice there are also other stakeholders who may reap value gains or losses from a merger: supplier prices (including wages to labor) may be forced downwards by a buyer who now has more bargaining power, communities may lose taxes and jobs if the merger results in layoffs, managers may reap higher wages and other benefits from being at the helm of a larger firm, and more.

Both the motives and outcomes of a given merger can be myriad, and disentangling the net effect on consumers, suppliers, competitors, and other stakeholders can be complex. There are often multiple competitive dynamics playing out in the industry simultaneously, making it hard to know the true counterfactual, that is, what would have happened to the companies or industry if the merger had not taken place? Furthermore, there may be multiple dimensions in which value has been impacted. Finally, when the true motive of a merger is blatantly predatory, for example to increase monopolistic pricing power or eliminate a potential competitor’s superior technology, firms will not readily note that motive in their public statements, and it can be hard to prove this was the firm’s intent.

Mergers in the airline industry provide an illustrative example. Kwoka and Shumilkina show that after the merger of US Air and Piedmont, prices rose between 9% and 10.2% on routes in which the two firms overlapped, and between 5% and 6% on the routes in which one competed and the other firm was a potential entrant. 1 This evidence appears consistent with a predatory market power argument. Hüschelrath and Müller similarly found that when Delta Airlines and Northwest Airlines merged in 2009, prices on their previously shared routes went up 11%. 2 Over time, however, as competition increased from other entrants (and potentially, Hüschelrath and Müller argue, because Delta and Northwest were able to achieve postmerger efficiencies), the prices on their overlapping routes came back down to a point that represented only a 3% net increase for consumers over the premerger pricing. Luo, who also examined the Delta and Northwest merger, concludes that the upward price influence of mergers among the large legacy airlines is small relative to the downward price effect of entry by low-cost airlines. 3

The picture becomes even more complex if we attempt to examine non-price effects of the mergers. The Delta-Northwest merger involved an intense integration effort. The two companies had to negotiate a new common contract with pilots and flight attendants. They merged 1,100 computer systems into about 600, and replaced more than 140,000 electronic devices, including printers, kiosks, and more. 4 By 2010, all of Northwest’s bookings had been cancelled and transferred to newly created Delta flights, a feat that required computer engineers to perform 8,856 separate steps. Parts inventory and maintenance processes also had to be merged, and Northwest’s assets had to be rebranded as Delta, including painting the planes—a task that was not completed until 2011. 5 It was a costly and lengthy process, but managers of the companies anticipated that the deal would yield savings that would climb from $200 million in 2009 to $1.2 billion by 2012. 6

The two airlines had route systems that were highly complementary—they had only twelve overlapping routes prior to the merger, accounting for just 2% of Northwest’s seats and 3% of Delta’s seats. 7 Not surprisingly, then, the savings of the merger were not premised on layoffs or hub closures. Furthermore, on eight of the overlapping routes there were at least two other competing carriers, restricting the ability of the airlines to raise prices. Overall, low cost carriers were growing 10% annually and accounted for almost one-third of domestic flights, so competition—domestically at least—was still high.

The bigger gains appear to have been upside potential in the quality of service and customer loyalty. Delta and Northwest had complementary international footprints: Delta was stronger in Europe and Latin America; Northwest had a stronger presence in Asia and a hub in Tokyo. After the merger, flights formerly branded as Northwest began to offer Delta’s higher-quality international service, including free alcoholic drinks on international flights, meals created by Delta’s celebrity chefs, a better in-flight entertainment system, and higher-grade amenities in bathrooms and onboard kits. For frequent business travelers, having a single airline with a more comprehensive global footprint and better business class services likely resulted in significantly higher willingness to pay and loyalty.

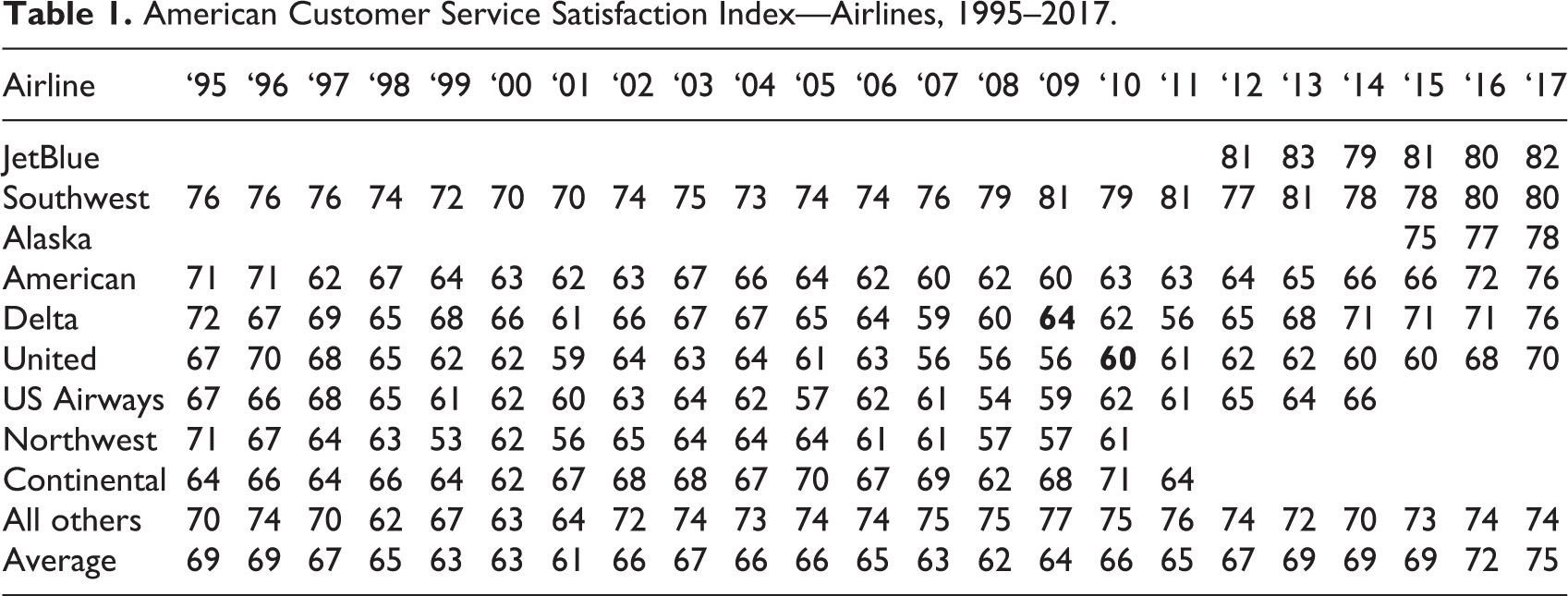

As shown in Table 1, in the decade prior to the merger, Northwest’s customer satisfaction rating was consistently below the industry average, and Delta’s rating hovered around the industry average. After the merger, Delta’s Customer Service rating initially fell for two years, and then climbed consistently from 2012 to 2017, achieving a 19% total improvement. Similarly, United, which merged with Continental in 2010, had significant gains in its customer service rating after its merger, achieving a 17% total improvement by 2017. Both companies, however, still lag industry leaders Jet Blue and Southwest Airlines in customer service satisfaction, highlighting the performance pressure that major airlines are under from low-cost competitors. The preceding suggests that perhaps the mergers were not intended to achieve monopolistic pricing power, but rather to help them to invest in customer service improvements that would help them to achieve parity with low-cost competitors on customer satisfaction, while also increasing their differentiation from low-cost competitors through larger global footprints and enhanced service features. That differentiation would enable them to charge higher ticket prices.

American Customer Service Satisfaction Index—Airlines, 1995–2017.

It is also telling to look at the profitability of the companies before and after the mergers. Both net margin and return on assets for Delta decreased sharply in the years after the merger, only climbing back up to their premerger levels by 2017. This outcome does not support arguments about monopoly pricing power. United Airlines’ return on assets and net margin rose significantly after its merger, but interpretation of this outcome must be tempered with the knowledge that both ratios were exceptionally low prior to the merger. Even with the improvements United Airlines subsequently achieved, its net margin and return on assets in 2017 sit at a paltry 6.09% and 5.5%, respectively. Both United and Delta have lower net margins and return on assets than Southwest Airlines and Jet Blue.

So should we conclude that the airline mergers were to eliminate a competitor to increase pricing power? Or should we conclude that the objective of the mergers was to enable investments in quality and services that would yield increases in customer satisfaction that more than offset the increase in prices? Or perhaps we should conclude that the mergers were to gain scale advantages that might help defend against more efficient rivals? It is clear that by only looking at price changes, or any other single outcome, we are likely to come to an incorrect—or at least incomplete—conclusion.

Firms engage in mergers for many reasons, some of which create value for both the firm’s shareholders and society, some of which only create value only for the firm’s shareholders, and some that fail even to do that. In fact, a substantial body of research on whether mergers create value for the firm’s shareholders concludes that most mergers do not create value for anyone, except perhaps the investment bankers that have negotiated the deal. In this article, I will first briefly review the research on whether mergers create or destroy value. I will then outline the three main ways in which mergers may be used to create value through improving the firm’s effectiveness and/or efficiency and indicators we can look at to give us some insight into a merger’s true motives and its likelihood of creating value.

A. Do Mergers Create or Destroy Value?

The total value that is created by a firm is typically defined as the spread between the willingness-to-pay of its customers, and the opportunity costs of the resources it employs. 8 The spread between opportunity costs and the price the firm can charge is the firm’s value capture, and the difference between price and customer willingness-to-pay is the value captured by customers, or consumer surplus. We can break this down still further by defining the value that is created and captured by other stakeholders such as suppliers that create and capture value in the form of goods and services they sell to the firm; employees and management that create value through their labor and capture value in the form of salaries and other benefits; and debt providers and stockholders that create value by providing capital to the firm that it can use to finance its operations, and capture value in the form of interest, dividends, and capital gains. 9 In Western developed economies, it is common to define the portion of value captured by the firm as the portion that is available to pay out to its owners—the shareholders.

A considerable body of research has attempted to assess whether, on average, mergers create or destroy shareholder value. Studies have used a wide range of methodological approaches (e.g., event studies, large panel analyses, case studies), samples (e.g., mergers in particular industries, mergers where both the acquirer and target are U.S. publicly held firms, mergers that vary in the share that is taken by the acquirer), and performance measures (e.g., stock price reactions, long-run cumulative abnormal returns, accounting performance, productivity, patenting outcomes). It should be clear that there are large number of parameters that may vary in the construction of a research design to study the performance of mergers, and, not surprisingly, the research has fallen well short of a consensus.

Overall, the evidence for mergers having negligible or negative effects on value 10 appears to outweigh the evidence for clearly positive or mixed effects on value. 11 As a result, leading luminaries such as Michael Porter and Aswath Damodoran have concluded that merger results are more often bad than good. In fact, Damodoran is quoted as saying, “More value is destroyed by acquisitions than any other single action taken by companies.” 12

Whether mergers create or destroy value was, of course, the wrong question all along. A merger, like any other strategy, has to fit the objectives, resources, and context of the agent using it, and it has to be executed very well if it is to have potential for value creation. In most situations, there are many more ways for a merger to fail than for it to succeed: preacquisition screening can be inadequate, synergies are often overestimated, postacquisition integration is often more complicated than expected, and so on. The merger process itself is also costly—time and money must be spent on postmerger integration, productivity and research and development (R&D) may be disrupted, assets may need to be shed at below book or market value, and the new entity is often considerably less lean and flexible than the entities were prior to the merger.

It is also important to note that many mergers are undertaken for motives that do not look like value creation from the shareholder or market’s perspective. A merger may serve the interest of the top management team, for example, by putting them at the helm of a more diversified portfolio of businesses, even if doing so does not benefit the shareholders (who may diversify their own portfolios more efficiently). In general, there are substantial benefits for managers to control a larger pool of resources, including greater power, status, pay, security, and perquisites. 13 Requiring top managers to hold large quantities of stock does not solve this problem because the wealth and future prospects of top managers are already tied closely—perhaps too closely—to the future of the firm. This means that top managers are underdiversified relative to the “average” shareholder and, thus, more likely to engage in actions that cause the firm as a whole to become more diversified than would be optimal for appropriately diversified shareholders. Making top managers hold large quantities of stock or stock options is more likely to exacerbate this problem than to solve it. The topic of agency problems and the potential governance mechanisms to reduce them is large, and I cannot do it justice here. It must suffice to say that many mergers may occur in absence of any motive to create shareholder or social value at all. In the remainder of the article, I am going to focus on those motives that are, ostensibly, for the purpose of creating shareholder and/or social value.

II. Main Potential Sources of Value in Mergers

A. Economies of Scale (and the Challenges of Reaping Them)

The most oft-cited benefits of mergers are scale effects—through pooling of resources and functions, the partners are expected to drive down production costs or achieve wider distribution and marketing than either could achieve on its own. Though not a merger, the Renault-Nissan alliance provides an excellent example. One of the objectives of the Renault-Nissan alliance signed in 2002 was to consolidate their collective product range onto ten shared platforms (at the time of signing, Nissan had eighteen platforms and Renault had eight). Cars built on the same platform have the same basic body core and can use the same range of engines, gear boxes, and other parts. 14 Consolidating their car models onto ten shared platforms meant that many of the two companies’ car models could be manufactured on the same production lines, enabling them to consolidate their factories, shuttering underutilized plants and increasing capacity utilization of factories that remained in operation. It also meant that the two companies could jointly purchase many of their parts in common, enabling them to achieve bargaining power over suppliers on par with much larger automakers.

The Renault-Nissan alliance also illustrates an example of two firms attempting to achieve greater economies of scale in innovation. When firms pool their R&D efforts, they can take on bigger or riskier projects than either would be willing to bear alone. Renault and Nissan, for example, pooled their efforts in developing fuel cells and zero-emission vehicles. By combining their efforts, the companies were able to spend $4 billion developing a platform that led to two all-electric Nissan models and four all-electric Renault models.

While R&D alliances are often used to achieve such pooling (Renault-Nissan achieved it under a cross-shareholding partnership), it may often be difficult to achieve significant innovation pooling through arms-length contracts: large, long-term projects with heavy R&D investment and deep knowledge exchange usually require significant commitment and incentive alignment. Such extensive exchange, commitment, and incentive alignment may, in some instances, warrant a merger. If two firms are undertaking a merger to pool innovation resources, we would expect to see consolidated R&D centers, the initiation of significant new projects, and potentially a higher ratio of patents to R&D spend. Evidence suggests, however, that higher ratios of patents to R&D spending after a merger are relatively rare and depend on numerous factors such as the industry and the relatedness of the firms. 15

Notably, to achieve the economies of scale sought in the Renault-Nissan alliance required the two firms to invest in significant integration and commitment to merging their technologies and car models. Renault and Nissan thus formed a partnership with substantial cross-shareholding investments: Renault has a 43.4% (fully voting) stake in Nissan, and Nissan has a 15% (nonvoting) stake in Renault. The companies also formed a 50-50 joint venture called Renault-Nissan BV to oversee the cross-company teams that were formed for each function (e.g., procurement, marketing, R&D) in which consolidation gains were sought. The savings achieved by the Renault-Nissan alliance could not have been achieved through allowing the companies to continue operating independently. This is true of many efforts to achieve economies of scale through a merger: If savings are to be achieved through pooling resources, we should generally expect to see significant changes in where and how operations are conducted, and typically assets and personnel must be reduced.

It is important to note that potential savings from economies of scale are often overestimated. It is not uncommon, for example, for companies to state that savings will be achieved by reducing duplications of resources, such as eliminating the need for two sets of corporate head offices, two separate sales teams, and so forth. If, however, two companies are operating their functions above minimum efficient scale, there should be few opportunities to achieve economies from consolidating them. For example, suppose two companies operate customer service call centers: If each center was already optimally utilized, the consolidated call center should require just as many service people, computers, phone lines, and real estate as the two call centers previously required. Furthermore, if the centers were not optimally utilized prior to the merger, it is likely that problem can be solved without the merger, and it is not obvious that a merger will make the solution any easier. An excellent illustration is provided by the consolidation of banks during the late 1990s. One of the justifications for consolidation was that the banks could save money by sharing their information technology (IT) resources. Ultimately, however, most of the merged banks realized that their potential savings were meager at best, and the costs of attempting to harmonize their information systems were high. In the end, most of the merged banks continued to run the separate legacy systems the banks had prior to merging.

Even increased bargaining power over suppliers or customers is not a guaranteed source of economies from greater scale. For increased bargaining power to result in lower costs from suppliers (or higher margins paid by customers), suppliers (customers) must have enough bargaining power prior to the merger to command significant margins (surplus). This is not always the case. Consider, for example, the implications between a merger of two major athletic shoe companies such as Nike and Adidas. Shoes for both giants are produced in a labor-intensive process by contract manufacturers in developing countries. Manufacturing is routinely relocated to take advantage of lower labor costs in different countries, and competition among suppliers to get a contract from a major athletic shoe brand is high. The suppliers have little bargaining power to begin with; there is not much profit left to squeeze out of them by being an even larger athletic shoe company. The direct customers of these shoe brands—specialty fitness shoe retailers, department stores, online retailers, and so forth—are in a slightly better position than the contract manufacturers because they are more differentiated and have achieved some brand loyalty of their own, but they have many substitutes, are exposed to heavy price competition, and clearly do not have the brand loyalty that the shoe makers themselves have. Here too, then, the shoe maker already has the lion’s share of the bargaining power, and it is not obvious that additional bargaining power will be rewarded by higher prices paid to shoe brands. Whether consumers will be willing to pay more if a Nike-Adidas conglomerate raised prices depends on their price sensitivity and how close they perceive competing products to be. So long as there are other athletic shoes available (and the lack of entry barriers ensures that there will be), Nike and Adidas will have to compete on both quality and price irrespective of a merger.

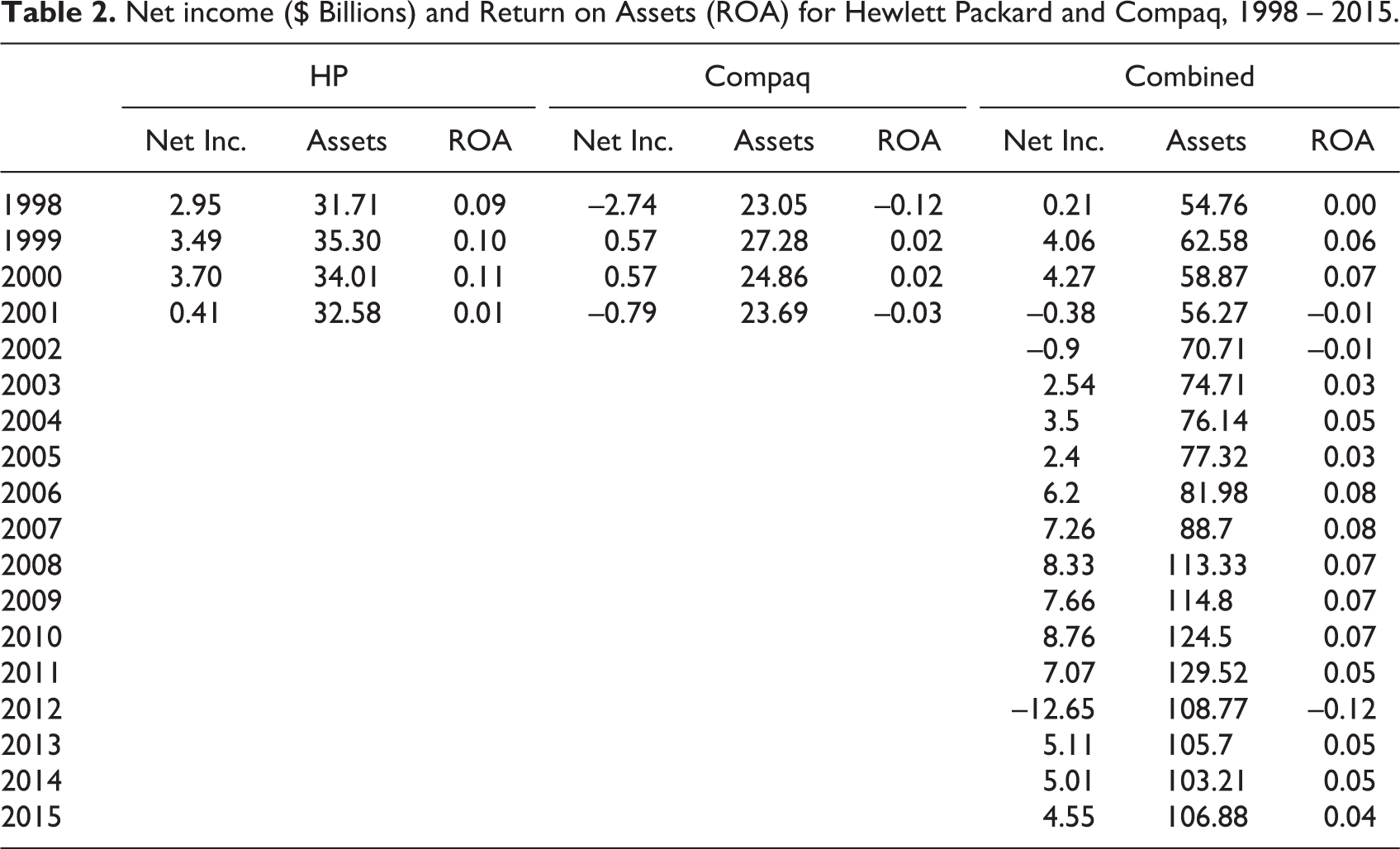

The high-profile mergers of HP and Compaq, or Heinz and Kraft, provide illustrative examples of illusory arguments for economies of scale gains. In the case of HP and Compaq, both companies were already huge personal computer manufacturers at the time of their merger in 2002. They were both well above minimum efficient scale, both had tremendous bargaining power over distributors and most suppliers (though a few components makers still possessed greater market power—notably Microsoft and Intel), and were well known in the market. Consolidating their functions was unlikely to either reduce their costs or increase their brand awareness or bargaining power. The merger did not increase the value of the combined entity; in fact, from 2003 to 2005, the combined entity earned less total net income than HP earned alone in the year before the merger (2001), and HP was never again as profitable as it was in the years prior to the Compaq merger (see Table 2). However, the merger had the effect of “rescuing” assets, knowledge, and jobs that might have been lost had Compaq continued its performance slide. This rescue likely had little benefit for HP shareholders, but it had significant benefits for Compaq shareholders, employees, and the communities of which they were members. This is an apt example of a counterfactual that is difficult for us to assess.

Net income ($ Billions) and Return on Assets (ROA) for Hewlett Packard and Compaq, 1998 – 2015.

The Heinz-Kraft merger seemed to pose an opportunity to improve innovation: Both companies were suffering from the economy-wide shift away from processed foods. Advocates of the merger claimed that it would help the companies develop more modern, healthier food products. This claim is difficult to defend. Neither company had expertise in healthier food lines. Furthermore, food line development does not require large R&D expenditures relative to the size of either company, and the companies that Heinz and Kraft were losing share to were almost uniformly smaller companies. Both the HP-Compaq and Heinz-Kraft mergers are more likely examples of companies that hoped that by combining their market power they would stave off the losses of holding enormous asset positions in declining industries.

In sum, then, for a merger to yield economies of scale, one or both of the parties should be significantly below minimum efficient scale, or in a situation where suppliers or buyers have enough bargaining power to extract economic rents above their opportunity costs. The merged entity should exhibit significant consolidation and/or reduction of assets and personnel: It is rare that a “bolt on” acquisition (where the acquisition is left largely intact and independent from the acquirer) will help the merged entity to achieve economies of scale, and in those rare instances (e.g., if an acquired firm would achieve substantial economies of scale from a joint purchasing arrangement of standardized products with the larger firm), it is likely that such benefits could be achieved through a less permanent arrangement such as alliance. Furthermore, even if such economies of scale exist, they must be compared to the costs and loss of flexibility that may be imposed through greater size and complexity of the firm.

1. Indicators

As noted previously, for a merger to increase economies of scale, one or both firms must be below minimum efficient scale in one or more important business activities before the merger. This is thus the first criterion we would use to assess the potential for value creation: What do costs-per-unit look like at different levels of output volume in the industry, and how much could costs realistically be driven down by the merger? This question is often addressed vacuously in announcements about the merger—managers may convey that millions are to be saved by “consolidation of back office activities.” However, to credibly argue this, the inefficiencies in those back office activities should be demonstrated. How much more is the firm paying for back office activities (customer service costs per customer in a call center, or IT expenses per dollar of revenue, for example) than competitors? How will savings be achieved? Ideally we could measure the change in expense (e.g., cost of goods sold: selling, general and administrative costs, marketing expense) per unit sales for the companies both before and after the merger to assess the savings achieved, but in practice this is not always straightforward. If one or both of the entities is privately held, the financial information may not be readily available. Furthermore, even if both entities are publicly held, their financial data may not be reported separately after the merger, and if their products are not sufficiently alike to warrant consolidating their unit sales, it can be challenging to attribute changes in expense ratios to savings versus changes in the product mix. The complications are greater still for assessing economies of scale in innovation activities. The standard method in the existing literature is to assess whether there is a change in the ratio of patents per R&D dollar (often called patent intensity). However, not all innovation is patented (or patentable), and standards for reporting R&D, the quality and contribution of patents, and strategies for patenting (whether claims are lumped into one patent or apportioned over ten patents, for example) are all variable. Collectively, this means there is plenty of room for error in interpreting a change in the ratios.

Fortunately, there are other—more qualitative—indicators that we can use to assess whether at least the intention of the merger is for achieving economies of scale. Because achieving economies of scale often requires significant integration of assets, activities, and personnel, the following questions should be asked: Which functions will be consolidated, and which assets will be disposed of? Which activities will be moved geographically? How many jobs will be eliminated? If the answer to these questions is trite, it is likely that the savings will be as well. While it is possible for two parties to gain economies of scale through coordination while still operating independently, for example through jointly purchasing from a common supplier, in most instances these gains can be achieved without a merger. A merger, rather than an arms-length contract, becomes necessary precisely because of the integration required. If no integration is required, an alliance or contract is likely to serve the purpose equally well and impose far lower costs.

B. Complementation Benefits

Sometimes two firms merge because they possess complementary assets that are more profitable in combination than alone—this is what is typically invoked by the notion of economies of scope or “synergies.” One firm may have a valuable brand, customer base, or technology that can be profitably utilized by the other, for example. 16 Google’s acquisition of ITA Software provides an illustrative example. ITA’s travel search software would enable Google to develop a state-of-the-art flight search and reservation system that it could serve up to its massive search customer base.

Sometimes the valuable complementary asset that is being leveraged across two firms may be the scale or expertise of one of the firms, highlighting the fact that the economies of scale and complementation sources of value are not mutually exclusive. For example, Coca Cola can buy new and small beverage brands and rapidly scale them up, plugging them into its vast distribution system, getting them prime shelf space by wielding its considerable clout with retailers, and applying its marketing expertise to build their brand. Notably, these acquisitions do not meaningfully affect Coca Cola’s economies of scale, but rather transfer some of Coca Cola’s scale advantages to other firms.

In many cases where complementary assets are argued to be the justification for a merger, arms-length relationships such as supply contracts, licensing agreements, or alliances would suffice to achieve the benefits of combining the assets, making the excess cost and risk of a merger unnecessary. 17 For example, in anticipation of the famous AOL–Time Warner merger, managers and investment analysts extolled the gains that would be achieved by deploying Time Warner’s content on AOL’s portal, advertising AOL’s service to Time Warner’s customers, and consolidating the customer service call centers of both companies. The first two of these motives, however, clearly did not require a merger: AOL was already in the business of distributing content produced by others using market contracts, and Time Warner was already in the business of selling advertising space to others using market contracts. Tying either company to an exclusive relationship with a single partner could only lower the value created by these businesses by preventing them from transacting with whomever would have been the highest bidder for any individual advertisement or content placement. The third motive, consolidating customer service call centers, was illusory: Aside from the fact that customer service for an Internet service would require vastly different expertise from customer service for a magazine subscription service, both companies were already well above minimum efficient scale to fully utilize a customer service call center. That is, there should have been little idle capacity in either call center, meaning that consolidation would not enable a reduction in personnel or other assets.

In the end, the merger became one of the most notoriously value-destroying mergers of all time; the true motive appeared to be AOL cashing in its bubble-inflated stock price for Time Warner’s durable and revenue-producing assets. Arguably, AOL shareholders benefited by the deal—even though their share prices ultimately dropped catastrophically when the Internet bubble burst, they did not drop as much as they would have without the Time Warner assets. However, these benefits came directly out of the Time Warner shareholders’ pockets. Those who sold their shares soon after the deal went through made profits; those who held onto the stock collectively lost billions. If you held $10,000 worth of Time Warner stock at the end of 1999 (just before the merger), it was worth less than $1,800 by the end of 2002. Retirement accounts were decimated, countless jobs lost, and by 2003 the CEOs of both companies had left the merged firm. 18

In other instances, complementation requires irreversible investments that would be at risk if either firm fails to uphold their end of the agreement. If these investments can be priced in advance of the agreement and contracts put into place to protect the parties, arms-length contracts may still suffice. However, often such investments are difficult to price ex ante, or the ex ante price would be too large for the other party to bear. Similarly, if complementation requires transferring valuable knowledge to a partner that cannot be taken back, nor adequately priced in advance of its use, a contractual arrangement may not adequately protect the party that provides the knowledge. In these situations, joint ownership may be the only (or best) way to ensure the parties’ interests are aligned and the investments are made.

For example, consider the Google–ITA Software merger mentioned previously. ITA’s flight search, pricing, and reservation programs were some of the most advanced in the industry; at the time of Google’s acquisition of ITA in 2011, ITA was licensing its software to major travel search companies like Orbitz, Kayak, TripAdvisor, and Bing Travel. Google, on the other hand, had a tremendous advantage in customer reach. Google has the number one search engine in the world, and many people begin their travel planning by searching destinations on Google. This put Google in a prime position to be the first stop for flight search. Furthermore, in the long run, the two companies planned to create a system that would organize a customer’s entire travel experience (e.g., book the trip, deliver customer’s bags to his or her hotel, reroute the customer automatically if there is a problem with her or his connection, etc.). For Google, knowing more about customers’ travel plans and experiences enables them to serve up more targeted advertising. Together the companies could develop a flight search service that surpassed what either could do alone; however, it required investments and exchange of proprietary information.

ITA was most at risk: In a partnership, Google might have had the ability to assimilate ITA’s proprietary technology and provided its own competing alternative. ITA, on the other hand, could not credibly threaten to counter Google’s advantage in capturing buyers. This highlights the difference between the Google–ITA Software acquisition versus the Renault-Nissan alliance. In the Renault-Nissan case, both companies were large viable competitors that could use what they learned from each other to compete with one another. A failed partnership would be painful, but likely not fatal, and both parties were approximately equally motivated to ensure the success of the collaboration. In the case of Google and ITA, there was more asymmetry of power and size, and more asymmetry in the appropriation risk of what each partner contributed: ITA’s technology could be completely transferred to (or replicated by) Google; Google’s advantage could not be completely transferred to (or replicated by) ITA. The benefits of collaborating were potentially large, but the risk of doing so via an arms-length contract were even larger. Thus, ITA agreed to be acquired by Google so that their interests would be irrevocably aligned.

1. Indicators

It is often easy to identify sources of complementation benefits; what is harder is to validate that a merger is really necessary to achieve them. To assess this, we should examine whether sharing the asset requires extensive cooperation and commitment, entails deep knowledge exchange, and/or poses a high risk of expropriation. Consolidation of functions, brands, personnel, and locations are again good indicators here. It is also useful to examine whether the asset being leveraged poses an appropriation risk because of incomplete intellectual property protection (e.g., trade secrets, or technologies where patent protection is weak). To make the claim that a merger was necessary to achieve complementation benefits, the firms involved should be able to explicitly define the market failure that prevents exchanging the complementary assets via an arms-length contract.

C. Solving Ecosystem “Hold-Up” Problems

In many markets, different players are woven together in a complex ecosystem that collectively delivers value to customers. For example, a smartphone operating system is more valuable to consumers when there is both exceptional hardware and a rich library of high-quality applications available for it. A crowdfunding platform like Kickstarter is only valuable when there are many individuals with high-quality innovations and a robust community of potential investors. When there are strong interdependencies between different players in such a product ecosystem, there can be a risk of “hold up” if a necessary part of the product bundle is not available at an attractive quality and price level. In this situation, sometimes joint ownership might solve coordination problems that would otherwise impede innovation deployment and adoption. The canonical example is in video games: Video game consoles must launch with a number of high-quality video games or consumers will not buy the console. However, developing a video game to be compatible with a particular console is a significant investment; thus, a video game console with a small installed base will not attract video game developers, leading to a serious chicken-and-egg problem. To solve this problem, every successful video game console producer has entered the industry with in-house games development in addition to encouraging third-party games development. Nintendo and Sega had popular arcade games before entering the video game industry; Sony and Microsoft acquired games developers when they entered the video game industry to ensure that games for their consoles would be available at launch (Microsoft already had a strong position in computer games, but these were more cerebral than the action-packed games that drive console sales). NEC, 3DO, and Philips, by contrast, had no in-house games production, and the strict reliance on external developer support proved fatal to their consoles. 19

In the video game industry there are two main types of players (console producers, games developers) that must coordinate to produce a bundle that is valuable to consumers. There are other enabling technologies (e.g., Internet access) and suppliers (e.g., microprocessors and graphics chips) that are also necessary, but their products are typically not specialized for a particular video game console, and thus the interdependencies between console makers and microprocessors, for example, are not as strong, and the market has provided these resources adequately. However, some ecosystems have more complex webs of players with strong interdependencies, and more possibilities for the market to fail.

Consider, for example, the electric vehicle ecosystem. Current electric vehicles require specialized batteries (or in the case of Tesla Motors, a specialized system for connecting thousands of standard 18650 lithium ion batteries together). These specialized batteries require large technological and production capacity investments. Furthermore, the charging of the batteries has not been standardized; currently there are three main charging standards (CHAdeMO, SAE combo, Tesla Supercharger). Even though customers may do most of their charging at home or workplace, the quantity and availability of fast charging stations has a large effect on their sense of “range anxiety,” and thus the value proposition of purchasing an electric car. Customers must perceive stations to be ubiquitous; the fear of being stranded even once is enough to prevent many potential consumers from adopting an electric vehicle. However, a charging station that offers CHAdeMO fast charging (for the Nissan Leaf or Kia Soul EV, for example), cannot charge cars that use the SAE combo (e.g., BMW i3, Chevrolet Spark EV, and Volkswagen eGolf), and neither CHAdeMO nor SAE combo charging stations can charge a Tesla vehicle. To make matters worse, it is not obvious that a profitable business model exists in charging. Electricity is cheap, and so long as consumers have the option of charging at home there is a limit to how much stations can mark up the price of providing electricity. Much of the value of having a large charging infrastructure is, as noted before, symbolic—it serves to assuage the customer’s fear as opposed to being the dominant means by which they charge their vehicle.

Trying to sell an electric vehicle into a market that does not have an adequate number and distribution of charging stations is as difficult as trying to sell a video game console for which there are no games. This intense interdependency, which requires significant and specialized investments, might only be resolved through joint ownership. Thus, Tesla Motors made the decision to build charging stations itself, in order to ensure that a “hold up” in charging infrastructure did not prevent adoption of its cars.

Most hold-up problems can be recast as complementation problems: Tesla has a market for electric vehicles that makes charging more valuable (and vice versa); video game developers make games that make consoles more valuable (and vice versa). The main difference is that in the instance of ecosystem hold up, we might not expect to see the degree of postacquisition integration that we would expect to see in a more typical complementation scenario. The main resource that the acquirer is buying is cooperation; there may be little product integration across the two firms.

1. Indicators

Ecosystem hold-up problems may warrant a merger when the timing of activities must be near simultaneous and the costs or risks of investment are large. Thus, when there are large “chicken-and-egg” problems in an industry, we might expect mergers to be used to resolve them (although they can also often be solved via alliances, joint ventures, or subsidies). Strong indicators include the existence (or need for) cross-subsidization in an ecosystem (as in the case of electric vehicles and charging stations, where it is unclear that market forces would induce the independent development of adequate charging infrastructure and electric vehicle firms have much to gain by subsidizing its development). The presence of strong cross-side network externalities (i.e., when the availability of complements strongly determines the value of a platform, or the installed base of a platform strongly determines the value of complements) is generally a good indicator of the risk of ecosystem hold-up problems. These problems will be exacerbated when large up-front investments must be made well before revenues begin to accrue.

D. Consolidating Market Power

The previous three sources of value suggest ways that firms can create increase total value creation, that is, the spread between customer willingness-to-pay and opportunity costs. The amount of total value created, in turn, limits the total amount of value that can be captured by the firm (in the form of profits) and its customers (in the form of consumer surplus), and that split will be based on the competitive forces and strategy that determines the prices paid by the customers. However, merger motives can also be focused strictly on increasing value capture for shareholders rather than value creation. Mergers might, for example, be used just to eliminate a competitor, shut down competing paths of technology, or foreclose a competitor’s access to a key supply. These types of mergers do not intend to create value per se; they merely intend to help the firm capture a larger share of the value created. As discussed in the beginning of the article, it is often easier to accuse a firm of these motives than it is to prove them—firms may go to lengths to conceal a market power motive, and the multidimensionality of both merger motives and outcomes often provides ample camouflage.

It is also often hard to make a market power strategy pay off. It is easy to assume that if more competitors leads to lower prices, fewer competitors must lead to higher prices. This is, however, a biased artifact of human cognition to infer a linear relationship between two points. While it is true that a monopolist can often charge a price that captures all of the consumer’s willingness-to-pay whereas markets with a large number of close competitors often have prices close to the opportunity cost of employing their factors of production elsewhere, there is not a linear—and possibly not even monotonic—relationship between those two extremes. In absence of collusion, it may take only one close competitor to compete prices down to the opportunity cost of producing the good. In a situation of extreme concentration—a true duopoly or oligopoly—it is not uncommon to see price wars where the price goes well below the opportunity cost. The extreme sensitivity each firm faces to its competitor’s actions sets the stage for a tit-for-tat downward spiral in price that ensures that no competitor captures value. It is precisely because there are few competitors, and because each competitor can watch the other’s actions closely, that price retaliation can be swift and severe.

There are strong incentives to collude in such markets, but it is important to point out that there are relatively few true oligopolies. In most markets that appear to be oligopolies, there is a competitive fringe (dozens or hundreds of smaller players) that exert price discipline on the large players and make it very difficult to sustain collusion. In the accounting industry, for example, there is a handful of extremely large global players, and thousands of smaller accounting firms. The global accounting firms have an advantage in attracting global clients, but if they raise their prices too much above those of the next size tier of accounting firms, those global clients will find ways to use smaller accounting firms. This reveals that the price premium charged by the large players in accounting (or in most other oligopolies with a competitive fringe) is not due to monopoly power but, rather, the higher willingness-to-pay afforded to them by their differentiated position.

It is similarly difficult to kill a competing technological option via acquisition. Technological knowledge is hard to suppress. Once the market has ascertained that there might be a better technological solution for a given market, innovators producing versions of that solution tend to sprout up like weeds until one or more has become successful enough to achieve dominance in the area. There are many technology acquisitions where the acquired technology is discontinued because it failed to pan out, but it is unlikely that many technology acquisitions are made with the intention of discontinuing the technology—that is an expensive strategy with a low probability of success. In 2011, when Microsoft announced that it would buy Skype for $8.5 billion (even though Microsoft had its own voice-over-internet-protocol, i.e., VOIP, and video calling applications), there was considerable speculation that the acquisition was simply to eliminate a competitor, or to prevent Google from having access to it. However, such accusations appear to have been baseless; Google had no difficulty offering its own VOIP and video calling service (and other competitors also exist—notably Facetime by Apple and WhatsApp by Facebook). Instead, Microsoft discontinued most of its original VOIP and video calling programs because Skype’s were better. This suggests the Microsoft acquisition of Skype was primarily a complementation acquisition.

1. Indicators

As noted above, and illustrated in the opening example about airlines, it can be difficult to establish conclusively that a merger was solely for the purpose of achieving greater market power to capture value from consumers or suppliers rather than to create value. However, a good place to start is to first assess the degree to which there are close competitors that, in absence of collusion, will make it difficult to exert pricing power. It is also important to look at relative changes in price versus willingness-to-pay. 20 If willingness-to-pay remains the same and price goes up, this can help to buttress arguments that the effect of the merger was to increase market power. Notably, we could also see market power exerted in the form of decreased willingness-to-pay while price remains the same, as in the situation where market power enables a firm to stop providing the level of quality, service, or innovation that it provided previously while still commanding the same price. We would also expect to see firm profitability go up in both of these instances, so profitability should be examined. If both willingness-to-pay and price change (whether this movement is up or down), this suggests that the firm has moved to a new positioning strategy, and is likely to be competing for a different segment of customers. It will be difficult to conclude anything about market power based on price in this instance, even if the spread between willingness-to-pay and price has changed. Symmetrical arguments and indicators can be used for assessing market power effects on suppliers.

III. Conclusion

There are many ways in which mergers can significantly increase consumer welfare. They could provide scale that enables firms to lower prices or invest in increased quality of products and services. They could provide complementation benefits that enables firms to bring better innovations to market faster, and more. However, for a merger to yield these sources of value, it is usually necessary that one or both of the entities involved is below minimum efficient scale or has valuable underutilized assets. The gains should be specific and quantifiable—nebulous sources of value are almost always overpriced. Furthermore, a merger (rather than a less costly and disruptive form of cooperation) is likely only necessary to achieve these gains if the assets and activities must undergo significant integration and consolidation. Unless heavy coordination and long-term commitment are required, many sources of value from mergers can be achieved through collaboration agreements or other contracts, with less risk to the firms and to economic efficiency.

A significant body of research indicates that most mergers fail to create or capture value for the firms that undertake them. There may have never been any true intention of creating or capturing value for anyone other than management (i.e., agency problems), or there may have been intention to create value for shareholders, but that goal was not realized. On the one hand, this is partially good news for antitrust: Even when mergers are intended to appropriate value from consumers through greater bargaining power, they usually fail to achieve that. On the other hand, it should also be clear that mergers rarely generate large efficiency gains for customers or other stakeholders. Overall, our default perspective probably ought to be against mergers—we should require abundant and specific evidence of large potential gains to convince us that a particular merger is in the best interest of anyone other than management and the investment bankers constructing the deal. When those gains are large, it will usually not be due to a simple change of ownership boundaries around the firms involved but, rather, will typically require significant restructuring of the parties and/or shedding of assets.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.