Abstract

Antitrust analysis of mergers focuses heavily—some would say, almost exclusively—on price effects. That focus does not reflect the lesser importance of quality, variety, cost, and technological progressiveness in mergers, but rather reflects better analytical tools and predictions for price effects. This article first provides an overview of the distinctive, often problematic, issues raised in evaluating nonprice effects. It then surveys the available empirical evidence on these from merger retrospectives. The evidence suggests that mergers on average may not cause either significant improvements or significant harms in terms of nonprice outcomes. While that might seem to suggest that policy need not be unduly concerned with nonprice effects, sufficient data do not exist for statistical testing. Moreover, variation in the average effects appears large, so that in particular cases nonprice concerns may dominate.

I. Introduction

To many observers and practitioners, merger analysis seems to have a singular focus on price effects, with scant attention to such nonprice outcomes as the quality of the good or service, technological change, or other product features. Indeed, the 1992 Merger Guidelines issued jointly by the Antitrust Division of the Justice Department and the Federal Trade Commission acknowledged nonprice effects in a single sentence buried in a footnote. That sentence reads thus: “Sellers with market power also may lessen competition on dimensions other than price, such as product quality, service, or innovation.” There was literally no further discussion of such effects—no details of what these effects might consist of, or how concentration and mergers might affect them, or how they were to be weighed against price effects, or what kind of remedial action might be appropriate.

The 2010 Merger Guidelines—the first major revision since 1992—sought to correct this imbalance at least in part by stating that “market power can also be manifested in non-price terms and conditions” and declaring that in evaluating nonprice effects the agencies “employ an approach analogous to that used to evaluate price competition.” There also is a new subsection on “Innovation and Product Variety” that discusses some factors that the agencies consider in evaluating a merger for its effects on these particular outcomes. No one, however, would mistake this treatment of the nonprice effects of mergers as symmetric with the attention to price outcomes. And few would subscribe to the view that product variety, innovation, or certain other nonprice outcomes can be adequately evaluated in an “analogous” fashion to the approach used in evaluating price. Perhaps most obviously, the effects of a merger or rising concentration on these outcomes are not necessarily the same as for price.

As a result, there remains a significant gap between the price effects and the nonprice effects of mergers in terms of the relevant economic analytics and the associated antitrust implications. This article provides a brief overview of the distinctive issues raised by nonprice effects of mergers, and then surveys the empirical evidence with respect to those effects. We argue that, in contrast to the effects of mergers on price, their effects on quality, innovation, variety, costs, efficiencies, and other nonprice outcomes are less determinate in theory and less predictable in practice. Moreover, we find that the empirical evidence underscores this ambiguity. While it generally suggests that mergers do not improve these nonprice outcomes, the evidence is too sparse for definitive conclusions.

We conclude that considerably more research is needed to upgrade both the analytics and the empirical understanding of the nonprice effects of mergers. From this, it may be hoped, a more complete development of nonprice issues may find its way into antitrust enforcement and into some future version of the Merger Guidelines.

II. The Analytical Issues

The antitrust analysis of the effects of mergers on prices is relatively straightforward in principle. A merger increases the likelihood of a price increase either through its effect on market concentration and the resulting enhanced likelihood of coordination among firms, or as a result of unilateral effects that arise as the merged firm internalizes some of the sales otherwise lost to the rival due to a price increase. Well-developed analytics, supported by a large body of empirical evidence, corroborate these implications and form the basis for the Merger Guidelines treatment of mergers that substantially increase concentration. Those guidelines state that mergers in moderately concentrated industries that raise concentration by some modest level “potentially raise significant competitive concerns and often warrant scrutiny,” while in more highly concentrated industries, more stringent conditions apply. There, a merger raising concentration significantly “will be presumed likely to enhance market power.” 1

In this context, nonprice effects are critically important for several reasons. One reason is simply that price is not necessarily the key strategic variable in all industries. In sectors such as pharmaceuticals, R&D is a—if not the—key variable of interest to competition. In airlines, there is concern over service quality as well as price. In electricity, costs and efficiencies as well as price are of interest. Merger analysis that focused on price in these and other sectors would be seriously incomplete. Moreover, mergers in most every industry from retail to manufacturing incorporate some nonprice dimensions likely to affect consumer welfare.

Greatly complicating matters is the fact that the effect of a merger or concentration on these nonprice dimensions of competition do not necessarily correspond to, or even correlate with, their price effects. Several examples illustrate this fact. Product quality. A standard economic model shows that a monopolist might either undersupply or oversupply quality. It is possible to identify conditions under which a monopolist undersupplies product quality, but those conditions hold neither in general nor under readily observable circumstances.

2

Product variety. A simple model shows how an additional variant of a product may either increase or decrease total economic surplus, the latter when the additional product variant, while privately profitable, mostly steals customers from existing suppliers.

3

Innovation. A more highly concentrated industry might provide greater returns to innovation, although at the same time a reduction in the number of firms may diminish the competitive threat that stimulates innovation.

4

Costs and efficiency. While mergers can help achieve scale economies and avoid duplication of costs, they may also insulate firms from the competitive pressures that hold costs down. Managers may prefer a “quiet life” to aggressive cost-cutting and profit-maximizing strategies in the absence of existential threats. Patronage, enabling incompetence, or strategic investments can also offset real efficiency gains in other areas.

5

As these examples demonstrate, the relationship between concentration and nonprice effects is not necessarily the same as the relationship between concentration and price effects. While higher concentration quite generally raises concern over price increases, the same increase in concentration might not result in worse product quality, variety, innovation, or costs. 6

As a result, a merger may have divergent, even opposing, effects on these various outcomes, leading to the need for some balancing of benefits and costs on different dimensions. Difficult under any circumstances, such balancing faces the further complication that the relationships of concentration to various nonprice effects are complex in theory, may even be nonlinear, and are not supported by the same body of empirical confirmation as is price.

Under these conditions, it may be no surprise to find that the more readily quantifiable price effects get disproportionate attention in merger analysis. Of course, this might even be appropriate if, for example, the price implications are clear, and the nonprice effects are small and difficult to evaluate. In such cases, assuming a zero effect may be the harmless best guess. On the other hand, if the range of possible nonprice effects is large, then an assumption of zero effect may still be the single best guess; but it now carries more risk of producing an erroneous overall decision if it needs to be weighed against predictable pricing effects.

This discussion highlights the usefulness of an understanding of what we do know about the effects of higher concentration on these various nonprice outcomes. It is to that empirical evidence that we now turn.

III. The Economic Methodology

While there is a variety of sources of evidence with respect to these nonprice effects, here we focus on merger retrospectives. We do so because merger retrospectives are particularly powerful methods for isolating the effects of events like a merger from other possible causes and, therefore, have become a frequent choice in the research literature. Indeed, there is now a substantial body of reliable and comparable evidence on the effects of mergers and some noteworthy compilations on which we shall rely. In addition, these retrospectives focus specifically on the effects of mergers, rather than from all increases in concentration. Since a merger is a deliberate pairing of specific firms, a merger that is intended to increase market power will have an impact on, say, price that is greater than the average price difference associated with all increases in concentration since the latter includes increases in concentration having nothing to do with mergers, as well as mergers without market power as their purpose.

For these reasons, merger retrospectives provide the best source of relevant insights into the effects of mergers on price and nonprice outcomes. Here we begin with a brief review of this methodology, followed by a summary of the effects of mergers.

A. Merger Retrospectives

Perhaps the key challenge in evaluating the effects of mergers is to avoid attributing to a merger the effects of other influences over the same time period. There are a number of methods for controlling for these other effects in economics. Structural modeling fully specifies the underlying causal forces and then undertakes the econometrics necessary to estimate them. A reduced form approach simplifies this by estimating the net effects of the various forces and thereby identifying the one factor of interest. The standard method used in merger retrospectives—so-called difference in difference analysis—simplifies this further. It avoids the need to specify any of the other possible demand, cost, and other forces by comparing the change in the outcome variable of interest for the merged firm to its change for firms not party to or affected by the merger but otherwise subject to these other forces. The difference between these two differences, if done correctly, measures only the effect of the merger.

This methodology may best be illustrated by example. Suppose some quality outcome can be measured by an index value, which for the merging firms begins at 100. Further suppose that after the merger, the firms’ quality value is observed to be 110—that is, to rise by 10%. Before attributing this increase in quality to the merger, one needs to be sure that, absent the merger, quality might have increased by 10% anyway—or, for that matter, by more, or less, than 10%. As described above, one possible method to determine what might otherwise have happened is to set out a full model of the determinants of quality and then proceed with the necessary estimation-structural or perhaps reduced form modeling.

The difference in difference alternative approach would identify other firms whose products or services are subject to the same demand and cost forces as the firms in question, but operate in other markets not subject to the merger itself. The service quality change observed for those latter “control” firms picks up all the other influences without having to specify or estimate them. As such, it can be used to net out all other effects from the total change observed for the merged firm, thereby isolating the effect of the merger. Thus, in the numerical terms set out in this example, suppose the change in the service quality index number for all the control firms over the same time period rose from an initial value of 100 to 108. Then it can be inferred that the 10% increase in the quality index registered by the merged firm was not entirely due to the merger, but rather only 2% should be attributed to the merger, the other 8% likely to have happened anyway.

Not surprisingly, difference in difference analysis is rarely quite this straightforward in practice. The control group must be correctly chosen. Certain other assumptions must be satisfied. 7 The econometrics has some pitfalls that need to be avoided. And, by design, it offers scant insight into the forces other than the merger that affect the outcome. Yet this approach is considerably less complicated and demanding than the alternatives, and it has become the most common method for evaluating key outcomes from mergers.

B. Price Effects of Merger

The usefulness of merger retrospectives, and of difference in difference analysis in particular, is made clear from its role in evaluating the price outcomes of mergers. Here the literature is most abundant, has been carefully synthesized, and has yielded some compelling insights. As background to our focus on nonprice effects, these are worth briefly noting.

There are hundreds of studies of the price effects of mergers, but most fall short of some reasonable criterion for further examination. Three criteria that have recently been used in a meta-analysis by one of the present authors are as follows: A qualifying merger must be a horizontal merger in a U.S. industry, in order to avoid the confounding effects of varying merger types and settings. (Joint ventures and airline code-shares, while representing partial consolidations, are evaluated separately.) The analysis must use one of the previously described research methods, although in practice virtually all use difference in differences. And the study must have been published in a refereed journal or in a highly regarded working paper series, to ensure the study meets some objective quality standards.

The result of these criteria is a group of nearly 50 qualifying merger retrospective studies, covering nearly 60 mergers and yielding more than 100 individual price outcomes by product or geography. Kwoka’s meta-analysis of these mergers has come to a number of significant conclusions with respect to the price outcomes. Perhaps most notably, the overall average price change is a 7.2% increase. Bearing in mind that these results control for all other influences, this implies that the typical merger outcome involves nontrivial harm to consumers. Moreover, more than 80% of all these mergers resulted in price increases, with 31% raising price in excess of 10%. The increases range up to 29.4%. By any standard, these careful studies suggest concern with the outcomes of mergers.

These results on price illustrate the potential of retrospectives to cast light on the effects of mergers. This same technique has been applied to certain nonprice outcomes of mergers—the issue to which we now turn.

IV. Nonprice Outcomes: Overall Results

The merger retrospective literature examining nonprice effects is considerably sparser than with respect to price. The reasons for this, as suggested above, include the dearth of data and the difficulties of measuring outcomes such as “innovation” or “technological progressiveness.” In addition, some outcomes such as the number of product variants may have ambiguous efficiency implications, so that even successful measurement does not answer the real question. These impediments have limited the number of studies in the literature examining nonprice outcomes. They are perhaps too few for robust conclusions, but arguably in some cases sufficient to merit examination in this meta-analysis framework. Moreover, when the results of these studies are aggregated, it becomes harder to defend the conclusion that on balance most mergers improve nonprice outcomes.

We divide this meta-analysis of studies in three ways. First, we separate studies by outcome, specifically, quality, research and development (R&D)/technology, costs, and efficiency. The reason is simply that these are fundamentally different outcomes, so there is no need in theory or empirical work for them to align. Second, we distinguish single-merger studies from grouped merger studies—the latter aggregating mergers in a single industry for unified examination. We do so since the grouped merger studies might aggregate 10 or 20 or 100 mergers and determine that collectively they resulted in a specific measured outcome. While informative and, of course, helpful in terms of numbers of observations, this latter summary is less informative than studies examining distinct mergers. And third, we distinguish published versus unpublished studies, since the latter generally have not (yet) passed an objective test of quality. For this reason, our attention in these latter studies is limited to those clearly meriting consideration.

As will also be evident, despite the relatively modest numbers of studies in each category, two features allow us in some cases to draw certain tentative conclusions—or, what might be a better description, some better supported hypotheses. One of these helpful features is that all studies report multiple results—different entities, time periods, control groups, data sets, and so forth—rather than a single result. Consequently, there actually are many more results than there are studies—though some caution needs to be exercised since some results are not likely independent of each other. In addition, there is often—but not always—broad consistency in the results in the same study and across studies. This lends some credence to certain conclusions, again with appropriate caveats.

Despite the idiosyncrasies of nonprice analyses, it is nonetheless informative to summarize their overall findings before considering each in detail. Utilizing a methodology similar to Kwoka’s analysis of price effects, the relevant nonprice outcomes were extracted from each study. In studies where multiple nonprice estimates are reported, we take guidance from the author as to the most reliable/central single estimate. When such guidance is not forthcoming, other criteria are used. After calculating a single estimate of each nonprice effect—that is, short/long term or variety and durability—these effects are in the last stage aggregated by study. This type of aggregation has many drawbacks that are discussed in great detail below, yet nonetheless it provides a good starting point by ruling out any obvious trends.

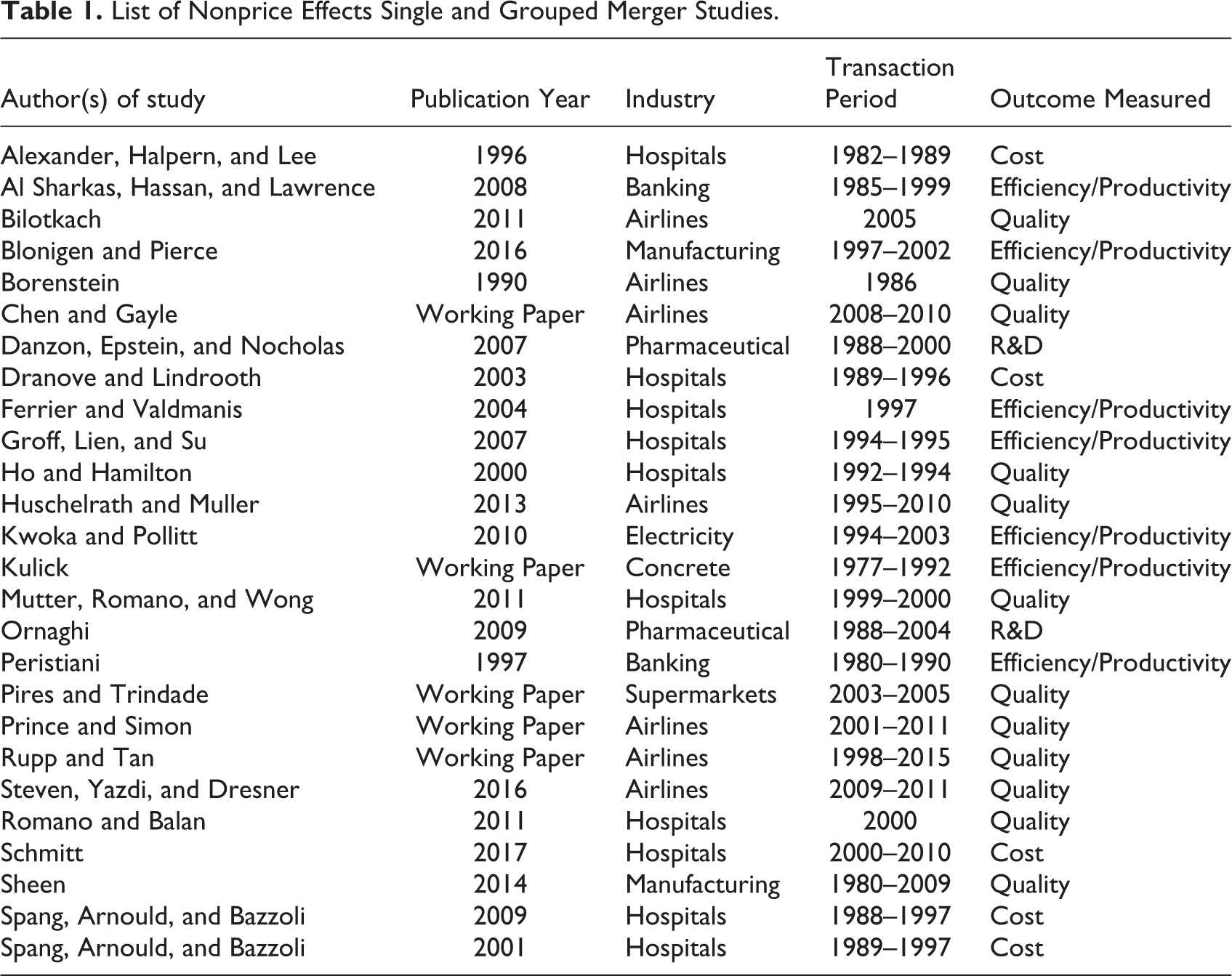

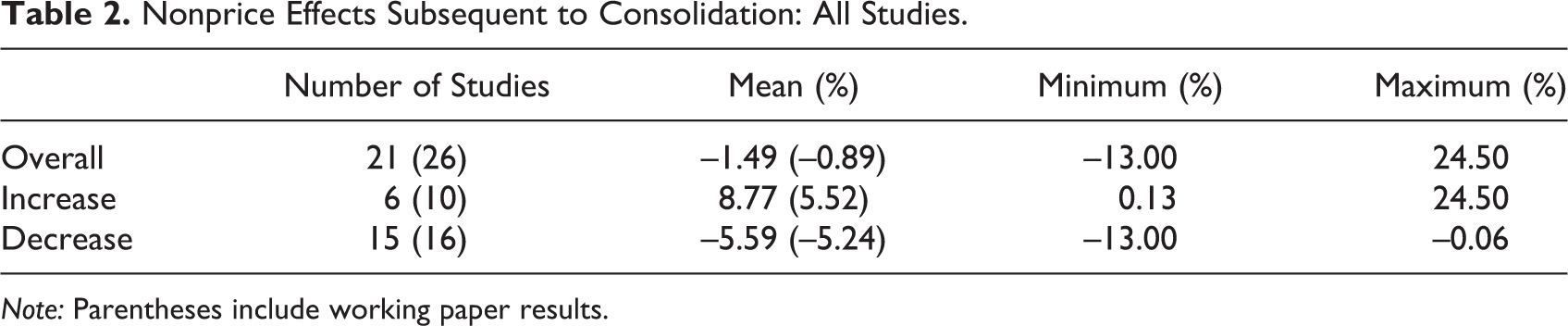

Table 1 presents an overview of the twenty-one published and five unpublished studies that merited inclusion in the preliminary review of nonprice retrospective studies. Of these, there are only five that focus on single-merger outcomes—three published and two working papers. This dearth of quality merger-specific analyses further underscores the need for further research. Nevertheless, when considered alongside the larger body of grouped merger studies, the data suggests that mergers do not clearly improve nonprice indicators, with the weight of evidence leaning towards the opposite conclusion. In Table 2, aggregating the nonprice outcomes by study yields six finding net merger-induced improvement but fifteen reporting adverse outcomes, which averaged together yield a negative 1.49% for all nonprice measures. The range of reported effects is also considerable, from a 13% decline to a 24.5% increase. When these studies are separated by the type of outcome, only the productivity/efficiency literature, discussed in detail below, reports an equal number of published studies concluding efficiency improvement subsequent to consummated mergers. Meanwhile, the literature on quality and cost effects is more likely to report harm to consumers, with seven out of eight published studies finding quality deterioration subsequent to merger. When the sample size of studies is increased by including working papers, this overall impression remains unaltered, with twelve reporting adverse outcomes against four suggesting some improvements. The R&D literature is limited to two studies, both finding decreases in R&D investment postmerger.

List of Nonprice Effects Single and Grouped Merger Studies.

Nonprice Effects Subsequent to Consolidation: All Studies.

Note: Parentheses include working paper results.

Aggregating the nonprice outcomes by study has numerous drawbacks and is far from conclusive. While nonprice indicators tend to correlate within each study, there are several that report a mix of positive and negative effects. It is entirely possible that a net improvement (harm) of 1% in nonprice outcomes could result in overall consumer welfare harm (improvement) in the likely event that consumer preferences are not uniform across quality indicators. Acknowledging this does not detract from the finding that a comprehensive overview of nonprice studies does not indicate likely nonprice dividends following the typical merger.

V. Nonprice Outcomes: By Effect

Despite these caveats, a case-by-case review of these nonprice merger retrospectives does not rebut this overall impression. Quality effects represent the largest body of the literature and so will be a starting point for this discussion.

A. Quality

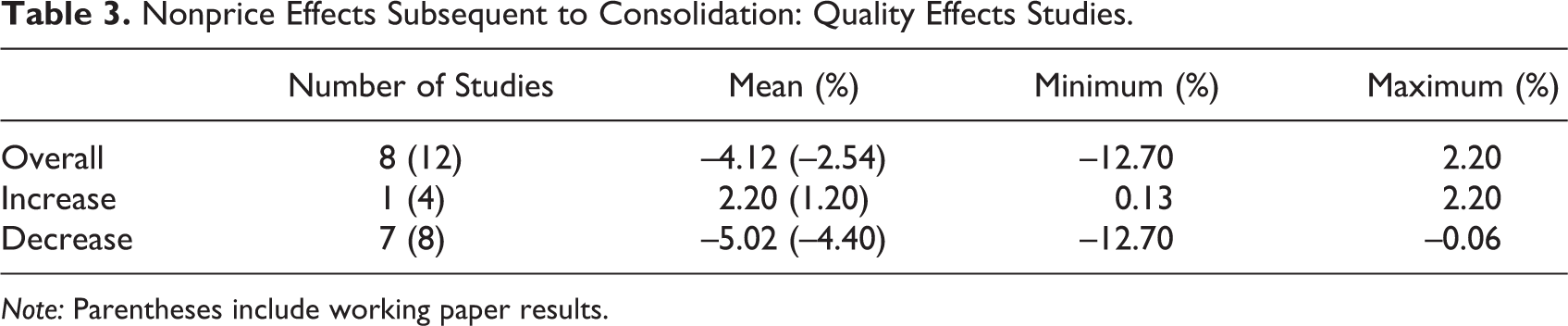

There are three single-merger published retrospectives on quality outcomes, two on airlines and one on hospitals. The airline studies measure different dimensions of quality-flight frequency, which is valued by consumers, and load factor, widely viewed as indicating passenger discomfort. Bilotkach 8 reports that flight frequency on major routes declined as a result of the US Air–America West merger, while Borenstein’s 9 study of two earlier airline mergers finds that load factors increased on seven of eight studied routes. The average increase was 6.6%, the sole decrease 3.4%. With that one exception, airline service quality is generally found to decline after merger. Romano and Balan 10 study the quality effects of the Evanston–Highland Park hospital merger using detailed patient outcome data on such things as stroke mortality rates, postoperative hip fractures, and birth trauma to newborns. With a total of seventeen different outcome measures for each of three hospitals, they find no evidence of a quality increase due to the merger. This evidence is summarized in Table 3.

Nonprice Effects Subsequent to Consolidation: Quality Effects Studies.

Note: Parentheses include working paper results.

When we expand this limited sample to include qualifying working papers, the overall picture changes little, while the variety of quality indicators under investigation increases. Chen and Gayle 11 evaluate the impact of two recent airline mergers on “route quality”—a measure of travel time between destinations. While nonoverlapping routes experience moderate increases in quality, overlapping routes see an equivalent decrease, and as a result the aggregate effect on consumer welfare is ambiguous. In contrast, Rupp and Tan 12 observe clear improvement in on-time performance and travel times in three of five major airports having recently undergone a merger-induced de-hubbing event. However, the authors are careful to qualify that their conclusions extend only to a subset of routes and not the mergers as a whole.

In sum, there is scant evidence from these single-merger studies that consolidation leads to service quality increases, and considerable evidence to the contrary. This conclusion is corroborated by four studies of groups of mergers, two each for airlines and hospitals. Ho and Hamilton 13 examine 140 hospital mergers and acquisitions in California using detailed patient outcome data. Among the findings of their study, consolidation had no effect on most measures of mortality, increased the probability of readmission of heart attack patients, and had varied effects on forty-eight-hour newborn discharge rates depending on the exact type of merger. Mutter, Romano, and Wong 14 have twenty-five measures of quality for forty-two hospitals in sixteen states. For twenty-one of the twenty-five measures, consolidation again had no statistically significant effect, whereas for the remaining four, two were positive and two negative. Returning to airlines, Adams et al. 15 study three recent airline mergers and find significant short term increases in delayed flights and cancellations of 6.6% and 13.6%, respectively. This harmful effect declines yet remains significant in the long run for delayed flights yet reverses sign for cancellations after one year. Additional quality measures including mishandled baggage and involuntary boarding denials exhibit a similar consistent harmful effect as late flights. Huschelrath and Muller 16 meanwhile find persistent and growing harm resulting from six airline mergers over the past two decades. An aggregate 3.3% decline in number of departures on overlapping routes is observed six months after the mergers, which falls further to 4.7% after two years. Surprisingly, a similar harmful trend is documented on “switching routes” where the acquired carrier did not directly compete with the acquirer premerger.

Against those grouped merger studies revealing merger-induced quality decreases, there are relatively few studies purporting to show quality improvements. Sheen 17 takes an innovative approach examining the Consumer Reports reviews of a wide arrange of consumer goods and finds a statistically insignificant increase of 2.2% in relative quality rank for the merging firms’ goods. On the other hand, Pires and Trindade 18 do find a statistically significant quality increase of 1.24% product variety in markets experiencing a supermarket merger, but this is offset by a concurrent 3% decline in discount frequency. This discrepancy further underlies the importance of taking a careful comprehensive approach to quality measures. Predictions of quality enhancements along certain dimensions may be offset by omitted quality variables uncorrelated with those under study. Moreover, in the face of contradictory results, it is impossible to weigh the indicators appropriately without a good understanding of consumer preferences. Improvements along two quality indicators does not necessarily outweigh one showing a decrease. Illustrating this problem is a working paper grouped study of five airline mergers in which Prince and Simon 19 find a small 1.4% long-run improvement in travel time, which is offset by a 3.6% decrease in flight frequency and a large short-run increase in baggage handling complaints.

As with the single-merger retrospectives, these grouped-merger studies vary a bit in their findings, but as shown in Table 3, overall there is no real evidence of improvement in quality. Indeed, the vast majority of results from hospital studies show the absence of any systematic quality effects from mergers. By contrast, the bulk of evidence from airlines suggests a quality decrease. The small number of ambitious forays outside these heavily studied industries report either inconclusive or contradictory results.

B. R&D/Technological Change

As noted at the outset, the innovation effects of mergers are both important but also complex in terms of their relationship to mergers and concentration. While some of this ambiguity might be dispelled by a body of empirical work, unfortunately, there appear to be only two retrospective studies of the effects of mergers on some measure of innovation. Preliminarily, it should be noted that empirical work labors under the burden of finding observable and quantifiable metrics for innovation. Counts of patents or of important patents, numbers of employees in R&D divisions, and R&D expenditures themselves are typically relied upon, but each has well-known limitations. Those should be borne in mind in discussing and synthesizing the following findings of the relevant studies.

Danzon et al. 20 analyze the effects of 165 mergers in the pharma and biotech industries that were sufficiently large and important as to be “transformative.” For the largest of these mergers, they report little effect on the growth of R&D expenditures (or of enterprise value, sales, or employees), but some slowing of profit growth. For smaller firms in the sample, merger reduced the growth rate of R&D, sales, and employees by 29%, 10%, and 11%, respectively, in the first postmerger year, but that effect dies out over time. If all results (large and small firms) were to be averaged, the effect is a decrease of 7.0% in R&D, but all in all, the authors themselves simply conclude that there is no evidence mergers are beneficial.

Ornaghi’s 21 study analyzes twenty-seven significant mergers in the pharmaceutical industry, including the major mergers in the 1990s and early 2000s. He finds that mergers have a statistically significant negative effect on R&D dollars, patents as a measure of output, and research productivity. By the third postmerger year, the growth rates of these three measures have declined by 6.3%, 26.8%, and 1.46%, respectively, for an average decline of 11.5%. Ornaghi describes his results as contradicting the notion that consolidation can deliver benefits in terms of innovation.

While these are only two retrospective studies of the effect of mergers on R&D or innovation, together they cover a total of more than 200 mergers and, moreover, arrive at broadly similar conclusions.

C. Costs

The remaining two nonprice outcomes are somewhat different than those just reviewed. In particular, cost decreases are direct offsets to price increases, rather than a different outcome dimension altogether (as with innovation). As such, cost savings have their own place in the Merger Guidelines, specifically, the section that addresses efficiencies. Here we review a total of five studies of the cost effects of mergers, all from grouped merger studies and, as it happens, all examining hospitals and all summarized in Table 4.

Nonprice Effects Subsequent to Consolidation: Cost Effects Studies.

Alexander, Halpern, and Lee 22 examine numerous performance effects of ninety-two merged hospitals. They report that mergers result in considerable short-term reductions in the growth of operating expenses per admission—nearly 25% reduction—but no change with respect to scale or staffing practices. Dranove and Lindrooth 23 follow this with a study of 122 hospital mergers. For acquisitions of one hospital system by another, they find small cost decreases in each of the first three years after a merger, none statistically significant. But for mergers of individual hospitals, costs fall by 14.1% after two years and by similar amounts in the third and fourth postmerger years. Summarizing these diverse results in Dranove et al. suggests an overall cost decrease of 8.4%.

Spang, Bazzoli, and Arnould 24 analyze the effects of mergers on the costs (and prices) of 204 merging hospitals during the 1990s. They find that merging hospitals have a 6.6% to 13.0% lower rate of growth of costs, somewhat greater in markets that are more competitive and those with high HMO penetration rates. A more recent study by Spang, Arnould, and Bazzoli 25 focuses on a different set of hospital mergers, namely, 1,165 nonrural public and for-profit hospitals. They report that consolidating hospitals lower their costs by a statistically significant 1.6%, but they report no differences between public and for-profit hospitals. The most recent study—by Schmitt 26 —is the most comprehensive and encompasses 337 hospital mergers occurring nationwide in the 2000 to 2010 period. He employs a diverse range of controls and propensity score matching to find an aggregate 5.3% decrease in cost per patient among target hospitals. In sharp contrast to Dranove and Lindrooth, cost savings are especially robust in acquisitions involving large multihospital system while significantly less following small independent hospital mergers.

An interesting corollary finding of Spang, Bazzoli, and Arnould is that for-profit hospitals in highly competitive markets pass cost savings on to consumers, whereas those in high concentration markets do not. This finding speaks to the important antitrust question of the disposition of any cost savings: The Merger Guidelines appear to require that cost savings not be fully retained by producers, but at least in part be passed onto consumers. Another important corollary finding is made by Schmitt where only out-of-market transactions generate significant cost savings, while in-market transactions that are likely to increase real market power see no significant benefits. If true, this would vindicate regulators’ skepticism of efficiency claims when the merger involves nearby hospital systems as with the recently challenged Advocate-Northshore merger. Cost decreases from hospital mergers are well documented in the literature but by no means a given when pursuit of market power is the primary motive for the merger decision.

D. Productivity/Technical Efficiency

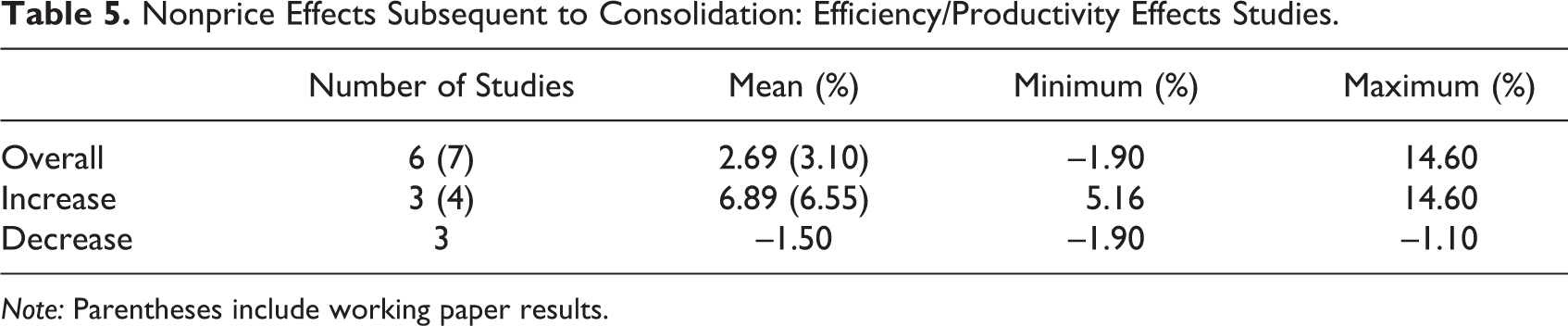

A few studies have also examined the effects of mergers on productivity and technical efficiency. These two outcomes lie in a gray area for antitrust policy since they do not directly benefit consumers and, unless they do, may not weigh much or at all in merger review. Two of these studies address hospitals, two others banking, one manufacturing, and one additional study examines the electric power industry. All are grouped-merger studies, summarized in Table 5.

Nonprice Effects Subsequent to Consolidation: Efficiency/Productivity Effects Studies.

Note: Parentheses include working paper results.

Of the two hospital studies, Ferrier and Valdmanis 27 analyze nineteen mergers in the late 1990s using data envelopment analysis to derive efficiency scores for technical efficiency, scale efficiency, and productivity change. They report that merged hospitals outperform the control group by these criteria in the first year, but that differential disappears in the second year, and then reverses in the third and fourth years. A summary statistic for these various effects would indicate an overall decline of 1.9%. Groff, Lein, and Su 28 also use data envelopment analysis to evaluate the efficiency effects of hospital mergers, in their case some 166 mergers in the 1990s. They find no effects in the first year after merger, but in the second year there are significant efficiency gains to the merged hospitals. The overall average effect can be summarized as a 14.6% gain in efficiency.

Two additional studies examine the efficiency consequences of mergers in the banking sector. Peristani 29 compiles data on 395 one-time bank mergers plus an additional 786 cases of multiple mergers in the 1980s. Using a translog cost function to estimate cost efficiency, he finds that one-time and multiple-merger banks lost 2.9% and 1.4%, respectively, in cost efficiency relative to the control group. He concludes that bank mergers do not generally appear to be beneficial but that one-bank structures seem inferior to multibank holding companies. Al-Sharkas, Hassan, and Lawrence 30 use stochastic frontier analysis as well as data envelopment analysis on 440 bank mergers in the 1990s, finding that such merger over time were more likely to result in efficiency gains and that small bank mergers achieved greater gains than large bank mergers.

Blonigen and Pierce 31 attempt to isolate productivity measures from the Census of Manufactures for over 3,000 plant-level merger events from 1997 to 2007. In addition to traditional productivity measures such as log labor productivity and log revenue total-factor productivity (TFP), the authors also employ De Loecker and Warzynski’s (DLW’s) methodology for estimating markups and efficiency from the translog production function. While these three indexes are in principle supposed to measure more or less the same thing—productivity—the authors find an aggregate 9% decrease using DLW’s methodology and a 10% to 14% increase utilizing log revenue and log labor measures. Furthermore, the results are highly inconsistent with respect to the choice of controls and degree of significance, so averaging can be misleading. Results like these highlight the need for careful robustness checks and alternate controls before reaching any conclusions on nonprice effects.

Even if productivity shows unambiguous increases, pass-through of any merger-induced gains can still be a major concern to regulators. In an analysis of 180 plant-level merger events in the D.C.-area ready-mix cement industry from the late 1970s to early 1990s, an unpublished study by Kulick 32 finds evidence for a 5.6% increase in total factor productivity across a wide range of controls. Nonetheless mergers between colocated plants, which are a majority of the sample, exhibit large price increases which more than offset any productivity gains. Relaxation of antitrust enforcement in the industry during the mid-1980s also caused a sharp discontinuity in the results as pass-through fell significantly. Productivity gains in and of themselves are a poor predictor of the net effect on consumer welfare.

Finally, Kwoka and Pollitt 33 study electricity distribution mergers in the 1990s and early 2000s, using data envelopment analysis to measure efficiency changes in twelve acquiring and twenty acquired companies. They report the subsequent to merger, acquired companies’ efficiency scores—which had begun above the norm—declined by nearly 7%, whereas the reverse happened for acquiring companies: Having begun below the norm, their efficiency scores rose by more than 8%.

The productivity/efficiency category reports the greatest share of positive nonprice effects of any indicator, yet a case-by-case review of the relevant studies reinforces the earlier impression that results are at best mixed. Within the banking and hospital industries, a majority of this small sample, different analyses yield conflicting outcomes. As with other indicators, the results cannot support definitive conclusions.

E. Joint Ventures and Airline Code-Sharing

The relationship between joint ventures, code-sharing, and market power is much less straightforward than mergers and so deserves separate consideration. With respect to prices, Kwoka’s meta-analysis revealed that joint ventures and airline code-sharing agreements did not exhibit the same trend as merger retrospectives and were overall price-neutral. While theory suggests that such arrangements may facilitate collusion among firms, it also suggests that this is less likely than with fully consummated mergers. The literature examining quality effects from code-sharing is extremely new and, as of yet, far too limited to form many conclusions. Nonetheless, two recent studies on code-sharing between airlines are worth mentioning.

Yimga 34 performs a difference-in-differences analysis of the 2002 Delta-Northwest-Continental code-share agreement and concludes that both on-time departures and on-time arrivals significantly improve for the alliance carriers, by 7.8% and 4.4%, respectively. Alliance carriers’ performance with respect to nonalliance carriers was even more significant when examining the proportion of “very late” flights with departure or arrival delays at thirty minutes or more. These results remained significant even when on-time departure was taken as a control for on-time arrival, suggesting that not only were alliance carriers more efficient getting off the ground but in flight as well. Juxtaposed with Chen and Gayle’s analysis of the same code-share agreement, which finds no harmful price effects, this seems to suggest that this code-share agreement was welfare enhancing. Armantier and Richard 35 employ a discrete choice approach to estimate consumer demand before and after the earlier 1999 Continental-Northwest code-sharing agreement. In sharp contrast to Yimga, they find that changing flight characteristics subsequent to the agreement likely caused a decrease in estimated passenger welfare despite fare decreases. While more complex than other referenced studies, this approach does have the benefit of simultaneously weighing multiple dimensions of product quality.

Joint venture and code share studies are a promising new direction in nonprice retrospective studies. It remains to be seen if the conclusions will trend toward the more benign outcomes cited in the price effects literature.

VI. Summary and Conclusions

For many years, merger analysis was characterized by a singular focus on price effects, while largely excluding nonprice dimensions. Antitrust practitioners were understandably more comfortable addressing a single concise metric—prices—that correlated relatively predictably with market power and consumer welfare. Despite this, the interplay between market power, nonprice investments, and consumer welfare was not ignored in the theoretical literature. Recent empirical work, along with the 2010 revision to the Merger Guidelines, signal a new willingness by researchers and regulators to systematically address this dimension.

We noted at the outset that the heavy emphasis in current antitrust policy on price effects might be warranted if nonprice effects seemed to average to little effect and if the range of estimated outcomes was not particularly large. This preliminary meta-analysis of empirical literature provides some tentative evidence for the former: There is little indication of systematic favorable or unfavorable outcomes on any of the criteria examined. This might provide some reassurance that, on average, nonprice effects seem unlikely to outweigh price effects on a systematic basis.

On the other hand, the variation in the findings is quite large. Even the sign of the effects is unpredictable within industries and types of indicators. Within studies, contradictory nonprice effects are sometimes reported, and their net effect on consumer welfare difficult to interpret. Even where an ex ante case for merger-induced efficiencies seems clear—that is, hospitals achieving cost-efficient scale—the actual results are mixed. Meanwhile, those few studies reporting benefit to consumers must be weighed against a larger body of work suggesting inconclusive or harmful effects.

The implication of this variation is that, despite the average effect, policy cannot be too confident that nonprice effects might not be important in particular cases. They can indeed be substantial. The challenge for economics is to be able to identify those cases ex ante, so that policy can focus analytical tools and investigative attention on nonprice effects precisely where necessary. One path for progress would seem to be further refinements in the empirical work along the following lines: Theory makes clear that the effect of concentration and mergers on these nonprice outcomes is the result of complex causality. By working to identify and specify these other causal factors and introducing them into new empirical work, it may be hoped that the unique effect of mergers can be isolated. Then, in turn, those other factors can serve as screens in the investigatory process for nonprice effects in specific mergers. 36

The work already done in this field serves to highlight the potentially large influence of mergers on quality, efficiency, and R&D. And it underscores the importance of expanding this limited body of empirical research in order to narrow this important gap in merger analysis.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.