Abstract

Do mergers raise substantial additional issues when the parties have significant innovation programs? To answer this, we examine the merger-related efficiencies that arise only with substantial innovation, arguing that innovation-intensive mergers should be treated more leniently than mergers without this dynamic dimension. We provide guidance on evidence that might determine the magnitude of such efficiencies. Next, we argue that where innovation is “directed” towards a product market, dealing with product line overlap should allay concerns about postmerger innovation. If research is not directed, we argue that theories of harm linked to the product market are unconvincing. Instead, one should look at theories of harms in the innovation market, which stem from the advantage in being first to innovate. Such first-mover advantages can be rooted in patent protection, switching costs, or network effects. This approach helps explain some of the remedies recently imposed on transactions such as Dow-Dupont and Bayer-Monsanto.

I. Introduction

The goal of encouraging technological progress and the diffusion of knowledge across the Single market has always been part and parcel of European Union (EU) competition policy. 1 However, the interpretation of this mandate and the weight given to innovation considerations has varied over time, as reflected most recently by mergers in mobile telephony and chemicals. 2 Until the mid-1990s, the dominant view was that innovation incentives were enhanced by treating intellectual property (IP)–based market power more leniently and by accepting restrictive licensing clauses as long as they were seen as necessary to ensure the distribution of technological knowledge. While this had implications for Article 101 (then 81) and 102 (82) cases, innovation was not a material factor in merger reviews.

The last twenty years have seen a notable shift in the antitrust treatment of intellectual property rights (IPRs). 3 Until a recent declaration, 4 the consensus seemed to be that, while competition policy should not expropriate IPRs, IP-based dominance should be treated just like any other type of dominance. At the same time, innovation has slowly crept into merger review 5 in a series of cases, becoming more recently a full-fledged aspect of the process, reflecting the European Commission’s (EC’s) concerns that mergers might have material systematic negative effects on innovation. In particular, the EC decision in Dow-Dupont has created a vigorous controversy.

A. The Current Controversy

The nature of the controversy has been fleshed out in a number of recent academic papers, authored by both academic observers and those involved in the EC’s decisions. It is useful to start with a paper by the former Chief Competition Economist at the EC, Massimo Motta, and his coauthor Emanuele Tarantino. 6

These authors draw several points out of a model that envisages a merger as a combination of assets among firms that can set both prices and investment levels. The merged firm offers multiple differentiated products upon combining the operations of multiple single product firms, whereas the “outsider” firms that do not participate in the merger continue to produce a single (differentiated) product. This structure attempts to capture the asymmetric nature of merger, in contrast to the stream of work that investigates changes in overall industry concentration and innovation investments. 7

This structure also implies that innovation by one firm hurts other firms in the market. As such, they find that the internalization of such a negative externality means that a merger reduces incentives to innovate. As we discuss further below, this can be seen as the mirror image of the reason why mergers put upward pressure on prices so that the observation effectively translates a well-understood effect into a new setting. The second point is that, because a merger leads to higher price-cost margins, it also affects the profitability of gaining sales through innovation. This effect is subtle, as it can work both for and against investment incentives. To see this, assume first that the merger increases profit margins but does not affect the difference between profit margins before and after innovations: because innovation helps to shift sales from rivals and those sales are now more valuable, the innovations incentives of the merged entity increase. However, there are no reasons to believe that a merger would increase pre-innovation and post-innovation price cost margins to the same extent. If the post-innovation margin increases more than the pre-innovation margin, then there is a further merger-related boost to innovation. In the opposite case, this second effect decreases the parties’ investment in innovation.

The main purpose of the Motta-Tarantino paper is to investigate these trade-offs to obtain a judgement on the overall effect, positive or negative, of merger on both prices and innovation. They find that the merged firm internalizes the effect of any price decrease of one of its products on its other product, which results in upward pressure on its prices relative to the case where firms did not merge. This price rise lowers sales for “insiders,” and this translates into lower investment incentives. While outsiders’ prices tend to increase, they increase by less, which tends to raise their demand and investment incentives. 8 This means that the net effect of the merger on the entire industry price and investment levels is a priori unclear; however, the authors do derive a sufficient condition for investments to decrease for the industry as a whole. Large efficiency gains or large spillovers in research that can be internalized by the merger can, of course, overturn this negative view. However, the authors also show that agreements that fall short of a full merger, such as research joint ventures, can help capture these beneficial effects.

There is therefore no reason to be lenient on mergers simply because the merging parties invest in innovation. In the authors’ words, “we find no support for the view that a merger—by relaxing competition—might increase incentives to invest.” 9 On the contrary, in the absence of innovation-specific efficiencies or research spillover effects, the traditional consumer harm from higher prices would be compounded by an additional loss of innovation, possibly at the industry level and not just at the level of the merged firm.

In the Motta and Tarantino set-up, innovation incentives depend directly on product market overlap between the merging parties and result from the investment implications of traditional static price effects. As pointed out by others, then, an alternative view of the paper is that it implies that “a traditional static assessment…suffices to determine, also the impact of the merger on dynamic efficiency.” 10 What is needed in order to determine if investment introduces additional considerations for those deciding merger cases is to determine if, where the price effects are modest or easily remedied, there are systematic grounds that remain for blocking the merger based on negative effects on innovation. This is a theme that we will reprise below, when presenting our own analysis and is not addressed by the Motta and Tarantino treatment, where investment is moderated by unremedied product market effects.

Two recent papers by Federico et al., 11 written by the current Chief Competition Economist and two senior members of his team, are both narrower and more general than the Motta and Tarantino treatment. Motta and Tarantino allow for either process or product innovation, whereas Federico et al. only allow for product innovation. At the same time, these papers consider quite a general research and development (R&D) process. Each company runs a single research lab that innovates with some probability and where there is a large premium to being a sole innovator but almost none to innovating simultaneously with a competitor. Effectively, innovations are modelled as substitutes in the product market. Merger allows the “insider” firms to perfectly coordinate their commercialization (or equivalently pricing) decisions so that if either—or both—of its labs innovate, the discovery continues to yield large profits. In turn, this means that any one “insider” lab can “free ride” on the success of the other insider lab so that in the face of decreasing returns to R&D, the insider labs reduce overall research effort. In sum, the innovation effects, while they operate via innovation behavior, arise because of traditional product market effects. 12 Therefore the question we pose of the additional effect of innovation despite any product market remedies remains unanswered.

Rephrasing this along the lines of Denicolò and Polo, 13 the question posed by the papers we have reviewed is, Should prices be allowed to rise due to a merger because such merger-induced price increases might help innovation? This motivates their approach of investigating the additional factors that might overturn the negative results of this line of work. In particular, they show that R&D coordination and the diffusion of knowledge across “insider” labs may well increase innovation incentives by allowing the merged firm to more efficiently manage the labs under its control or by allowing the output of one to extend to the entire range of output produced by the merged firm. Indeed, as we will see below, these factors can take multiple guises, from transfers of know-how within the firm, to external spillovers, to licensing, each of which deserve to be considered separately. It is in the assessment of the role of such elements, to which one can add the sequential nature of innovation, the nature of R&D, and the role of IPRs where we deem that the remaining challenges reside. As a result, we make these a focus of our own work, below.

Jullien and Lefouili 14 combine lessons from the existing literature with insights from their own formal analysis to distinguish among four main types of effects of merger in the presence of innovation. Their typology nests the effects already discussed above: the innovation diversion effect refers to the effect of one firm’s innovation on the profits of its merging partner, whilst the demand expansion effect is the increase in innovation incentives due to the merger-induced increase in profit margins. As we have seen, these are the factors analyzed by previous work. 15 To these, the authors add the spillover effect, which reflects the internalization of (positive) knowledge externalities; and the margin expansion effect, which we would rather call a scale effect, referring to the fact that the reduction in output due to the merger reduces the profitability of a fixed investment like R&D.

The last two factors complement the earlier analyses. The authors additionally point out that the innovation diversion effect is not necessarily negative. If, for example, firms invest in horizontally differentiating their products from rivals, this relaxes the intensity of price competition to the benefit of all firms. In this case, the innovation externality is positive so that a merger would likely lead to more innovation, not less. This is a valid theoretical point, but we will focus instead on the negative diversion effect as the greater policy concern. First, we take our cue from the industries identified by the papers we have reviewed to find mergers where policy makers have struggled with innovation effects. Such industries would include, and case review suggests that, chemicals, pharmaceuticals, and Information and Communication Technology (ICT) are where the diversion externality is likely to be (strongly) negative because competition-softening innovation tends not to be the form that innovation takes. This stands in contrast to consumer products like soft drinks or even cars, where innovation might be more likely to be “competition-softening” within the class of goods due to strong differentiation potential. Second, while a positive diversion effect would indeed imply that there is more innovation after the merger, it is not entirely clear that such an increase is positive for consumer welfare once price effects are taken into account. Moreover, the precise effects of a merger on this type of innovation are likely to be complex and depend on the precise specification of demand. 16 This sensitivity to the specification suggests that “positive externality” innovation 17 should not be a systematic part of merger review. Finally, we note that positive externalities between firms can also arise in terms of pricing. For example, when consumers face search costs, a firm can benefit from a decrease in the price of a rival located nearby as it draws more consumers to the area (as one might see in the context of a mall). In this case, a merger would lead to lower prices. 18 The fact that such a positive externality may occur in certain cases is not generally taken to be a reason for abandoning the usual presumption that mergers tend to put upward pressure on prices as a default. In the same vein, we believe that the presumption of a negative innovation externality between merging parties remains a useful default. Presumptions can always be refuted once an unusual case arises.

Hence, while we do not in any way dismiss the possibility of positive externality innovation, we will focus here instead on what we see as the most policy relevant case of “competitive innovation,” that is, innovation that imposes a negative externality on rivals. In the same spirit—and reflecting another point made by Julien and Lefouili—it is good practice to specify whether the arguments presented apply to product or to process innovation. Our own analysis refers to product innovation only.

B. Our Contribution

While the arguments presented here can be made fully rigorous, this note is more in the spirit of a stream of the literature that we have not yet discussed and that tries to isolate the main factors to be assessed when considering innovation in the context of merger review, without relying on a fully specified single model. 19 We do, however, attempt a more pronounced “policy” orientation than these authors: we do not limit ourselves to identifying the main factors to consider. Rather, we also discuss how to document whether these factors are likely to be important in a given case and further suggest a “policy algorithm” showing the sequence of steps that one needs to take when a given transaction might have significant effects on innovation. We hope that this framework for decision making fills a gap in the literature, between the contributions reviewed in Section I.A and the broader papers cited in this section, of capturing a relatively wide set of effects but doing so in a way that gives structure to decision making rather simply stating that “anything can happen.”

Our approach relies on three well-known elements: the conventional distinction between product, technology and innovation markets, the difference between “undirected” and “directed” R&D processes, and the traditional approach to dealing with the static effects of mergers. Our hope is that, by drawing on a comparison with the standard merger procedure, we will be able to highlight the aspects of innovation that call for special attention. We also focus on what we believe to be the correct policy counterfactual. The relevant question is not, “What are the effects of a merger on innovation?” but, rather, “What are the effects of a merger on innovation given that the static effects of the mergers are appropriately handled by the Competition Authority?” In other words, we know that competition authorities will (or at least should) address conventional static issues—and hence try to ensure that prices do not increase. It does not, then, seem particularly useful to analyze the effects of merger on innovation in a framework where the merger leads to higher prices and where it is through those higher prices that innovation incentives are affected. We wish to know what additional elements innovation brings, assuming that the rest of competition policy works well to control already identified static effects. A happy consequence is that ignoring such price effects greatly simplifies the analysis.

The article is organized as follows. In Section II, we review the effects that operate through the product market as well as the types of efficiencies that might be weighed against any negative effect on innovation. In Section III, we turn to the technology market. We argue that, while the effects of the merger on the sale of technology should be investigated, these are not really related to the incentives to innovate. Section IV analyzes the potential effects of mergers in innovation markets. We explain why divestment of research assets, in other words divestments in the innovation market, might be required to implement an effective remedy for overlap in product markets. We then draw a sharp distinction between this type of intervention in innovation markets, which is still motivated by (potential) overlap in the relevant downstream markets, and “innovation theories of harm,” which are not based on such overlap. These “innovation theories of harm” are based on some form of first mover advantage and might require the divestment of IPRs and other research assets. Section V discusses some additional aspects of the issue, including the relevance of the concept of “appropriability,” which has been identified as an important factor, 20 and potential harm from changes in the type of innovation pursued by the merged entity. Section VI summarizes our argument into a “policy-algorithm” explaining how authorities might proceed when a merger seems likely to have a significant innovation dimension. Section VII concludes.

II. Product Markets

As mentioned above, we proceed under the assumption that the Competition Authority ensures that the merger does not lead to significant increases in prices. Product innovation leads to new or better products. To keep the discussion simple, we consider a situation where each firm sells a single good that can be improved by investing in innovation. The incentives to make such investments come from two sources: the hope that a better product will help gain sales at the expense of rivals 21 and the possibility that the new product might also help expand the size of the market, that is, that it will also yield additional sales that do not come from reductions in the sales of competitors. The relative importance of the type of gain is larger if the products in the market are closer substitutes.

A. Incentives to Innovate

1. The innovation incentives of the merging parties

Consider a merger between two firms, A and B. Before the merger, each firm made its own, independent investment decision by comparing the cost of investment to the potential gains discussed above. In doing so, firm A would not care that some of its additional sales would correspond to a decrease in the sales of its rival. After the merger, though, A would take into account that part of the additional sales obtained because of innovation are in fact taken from the merging partner. 22 This means that the net benefits from investment are lower after the merger. Hence, if the merging parties sell products that are substitutes in the product market, then a merger tends to decrease the incentives to innovate of the parties.

This line of reasoning should be familiar as it mirrors the very reason why competition authorities worry about the static effect of mergers on prices or quantities. Postmerger, firm A would take account of the fact that some of the gains from lowering its price come at the expense of firm B and would therefore set its price higher than before the merger. Furthermore, the magnitude of the effect depends on the same factors in both the static and the dynamic story: mergers are more likely to have a sizeable negative effect if the products of the two merging entities are close substitutes and if profit margins are substantial. Indeed, under the assumption of no price change, one can easily derive a “measure of downward pressure on innovation,” 23 which is similar to common measures of “upward pressure on price.” For example, the GUPPI (gross upward pricing pressure index) for product A is

where

where

An important consequence of this parallel is that, in terms of product market overlap, static and dynamic harm from mergers go hand in hand: if there is no concern that the merger can raise prices materially, then there should be no concern that it would reduce innovation either. Moreover, any potential problem could be resolved through product divestments to reduce the overlap between the products of the merging parties. The appropriate remedies are the same as for purely static concerns: divestments in the product market to reduce the amount of overlap between the product lines of the merging parties.

The fact that static and dynamic harms from a merger proceed from the same mechanism and call for the same remedies does not automatically imply that the innovation aspects of a merger do not matter. The similarity only ensures that the harm from less innovation and higher price are similar. Two sources of harm rather than one remain, however. A projected price increase of 2% might be palatable, but a price increase of 2% and a 2% decrease in innovation might not be.

Does this mean that the “customary” GUPPI thresholds should be adjusted downward when innovation is also an important feature of competition in the industry? Not necessarily. The reason why small expected price increases are tolerated is that we believe that, even though these might be hard to demonstrate, mergers do create at least some small efficiencies that might benefit consumers. Hence, if the same order of “hard to measure” merger-specific efficiencies can reasonably be expected for innovative activities, then there is no reason to adjust the usual GUPPI thresholds. Indeed, if we were to believe that innovation activities tend to generate more “hard to measure” efficiencies than production activities, then we would want to use higher thresholds for an initial GUPPI-based assessment of the merger. We will come back to the issue of efficiency in Section II.B below.

2. The innovation incentives of the nonmerging parties

When we analyze the static effects of a merger, we know that the reaction of a nonmerging firm is a priori ambiguous: rivals might behave less competitively than before the merger, compounding the elimination of competition between the merging parties, or they might behave more competitively and partially alleviate the direct, harmful, effect of the merger. We also know that these indirect effects cannot fully compensate for the direct effect that the merger has on the price/output incentives of the parties. In that sense at least, ignoring the reaction of rivals—as measures of upward pressure on prices do—cannot lead us to an erroneous conclusion as to the net effect of the merger on prices or output levels.

The same principles apply if—as we do—one looks at the effects of a merger on product innovation under the assumption that prices do not change. While the merger also affects the innovation investments of other parties, whether other parties react by increasing or decreasing their own investment is a priori unclear. 27 Still, even if the change in third-party investment changes in the opposite direction from the investment of the merged parties, the sum of these changes in investment across third parties should fall short of fully making up for the change in the behavior of the merging parties. 28

B. Efficiencies 29

On the production side, efficiencies can arise because of economies of scale (“spreading fixed costs” over a greater total volume) or economies of scope (“spreading fixed cost” over more products). It is not hard to imagine how similar economies might also arise for innovative activities. In particular R&D resources such as equipment might be shared efficiently by researchers working on innovation relating to different products, once these products are housed under the same roof. 30 Unless the parties can provide convincing evidence that such efficiencies are substantial they are best treated as the “hard to measure” efficiencies discussed above, which justifies the use of customary thresholds in merger reviews. However, there are additional factors suggesting that a merger might indeed lead to an increase in innovation investments and/or outcomes.

These additional factors can be broken down into efficiencies and changes in investment incentives. Efficiencies refer to an increase in innovation outcomes for a given amount of investment. However, such efficiencies can also increase the parties’ incentives to invest. We therefore prefer to organize these additional effects according to the economic mechanism involved rather than use the efficiency/incentives distinction.

1. Knowledge diffusion within the merged entity

Assume that, postmerger, the R&D activities of the two partners are still run separately. In particular, there is no attempt to coordinate the type of research projects pursued to avoid duplication. Before the merger, the benefits from a successful project run by A came from A’s ability to use the innovation itself and whatever revenues it might get from licensing the technology to others (if this makes strategic sense for A). After the merger, A can still use the innovation itself and can still license it to outside parties. The only difference, then, is that now B can use the fruits of the innovation freely rather than get access to it at a price.

If A’s innovation was not licensed to B before the merger, then the merger has a clear efficiency benefit as B will be able to improve the quality of its product postmerger. This benefit applies both to existing technologies and to future innovation. If A’s technology was licensed to B before the merger, there is still a merger-specific benefit coming from increased incentives to invest. We know that IPR owners are typically unable to extract the full value of their technology through arms-length licensing. This implies that the private value of A’s innovation must have increased postmerger. An increase in the value captured for a given level of investment increases A’s incentives to invest in R&D. This is the first benefit from the internal diffusion of technology facilitated by the merger. This investment-increasing effect only applies to future innovation.

How could the relevance and strength of this effect be assessed in practice? For the effect to be sizeable, two conditions must be satisfied. First, A’s technological innovation must also be useful for B’s product line (and conversely). Whether this condition holds depends on the precise nature of the products and of the innovation involved. Assume, for example, that A and B are selling petrol-fueled and electric cars, respectively. If A finds a way of improving the car’s suspension, this new knowledge is also likely to be applicable to B’s electric car. On the other hand, any innovation regarding the petrol engine would be of no use to B.

The second condition is that, before the merger, A would have been unable to capture most of the value that its innovations might create for B. If technology markets work efficiently, then licensing is an effective—if still imperfect—manner of transferring technology. If this is the case, then one would expect the gains from transferring internally technology that would not have been transferred externally before the merger would be relatively small. On the other hand, the absence of premerger licensing or evidence that arms-length licensing does not provide high returns to the licensor would imply that the type of merger-specific benefits discussed in this section are likely to be substantial. An analysis of the pattern of licensing in the industry is therefore relevant to assessing the magnitude of this efficiency.

2. Spillovers. 31

Consider now a situation where, before the merger, part of A’s innovations “leaked” to its rivals, including firm B. Such leaks are referred to as “spillovers.” Spillovers decrease a firm’s incentives to invest because they imply that a given investment results in a lesser advantage over the innovator’s rivals than in the absence of spillovers. Assume further that the merger does not affect the size of these “leaks,” that is, that it does not lead to better diffusion of knowledge to the merging partner. This assumption ensures that the diffusion of innovation is exactly the same premerger and postmerger. Therefore, we do not have the benefits of internal knowledge diffusion already discussed above.

Before the merger, firm A’s incentive to innovate was decreased by the knowledge that its own effort would also help all or some of its rivals. Assume that B is one of the firms that would have benefited from the spillovers. After the merger, firm A still suffers from the spilling out of its knowledge to remaining rival, but it now actually benefits from the spillover to its merging partner B. Consequently, the larger the premerger spillovers to firm B, the more the merger is likely to increase the innovation incentives of the merged parties.

There is a subtle relationship between spillovers and the effect of internal diffusion of knowledge discussed in the previous section. While the effects are logically different—as we assessed spillovers under assumptions that rule out increased internal diffusion—the two sources of efficiency are related. High spillovers mean that the technology market does not work efficiently since the innovator cannot easily appropriate the value created by its innovation. So, just as for the internal diffusion of innovation, the less efficient the licensing market is the larger are the benefits from the merger.

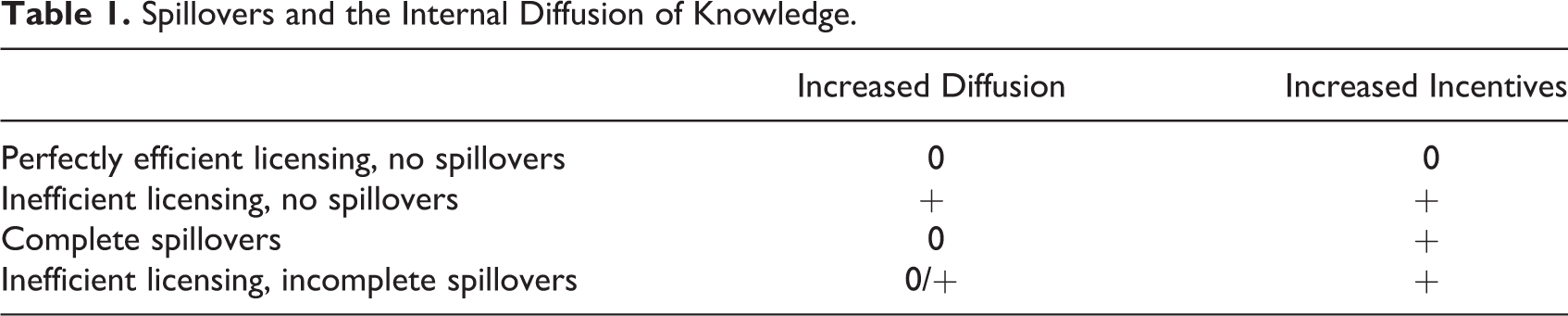

One must also consider the interaction between spillovers and internal diffusion of knowledge. This is explained in Table 1.

Spillovers and the Internal Diffusion of Knowledge.

In the first row, A can extract the full commercial value of its innovation through licensing. The technology should therefore be widely licensed premerger (no increased diffusion), and the merger should not increase A’s reward from innovation either (no incentive effect). As seen in Section II.B.1, inefficient licensing creates both a positive diffusion effect and a positive incentive effect.

In the third row we consider the polar case where rivals benefit completely from A’s innovation through spillovers. This means that A cannot monetise its innovation through licensing, i.e. complete spillovers kill off the licensing market. In this case the merger does not affect the diffusion of knowledge but, as explained above, it increases A’s incentives to innovate. We now turn to less extreme combinations of licensing efficiency and spillovers. In row 4, there are incomplete spillovers. This means that licensing cannot be perfectly efficient but it might still enable A to obtain some additional returns from its investment. If those additional returns are sufficient to induce A to license to B premerger, then the merger brings no benefits in terms of knowledge diffusion. However, the merger still increases A’s incentives to innovate as the merged firm is able to appropriate more fully the benefits of diffusing the innovation to firm B. If A does not license to B premerger, then the merger also brings about an additional diffusion benefit.

3. A remark on “appropriability.”

Several commentators 32 have identified “appropriability”—or an innovator’s ability to capture the benefits from the use of his innovation by others—as a crucial factor in the assessment of the effects of merger on innovation. Since the merger increases the innovator’s ability to benefit from the use of the innovation by the merging partner, greater appropriability is generally believed to decrease the positive effect of the mergers: if firm A can already capture much of the benefits from its innovation premerger, then the merger does not improve matters much. This is very much in line with our analysis in the two previous sections. These sections can be seen as a more detailed discussion of the appropriability issue, at two levels. Firstly, our approach allows us to distinguish between different types of limits to appropriation. Appropriation is limited both by the breadth and enforcement of IPRs (as captured by the importance of spillovers) and by the ability to write efficient licensing contracts, which itself depends on the nature of the technology 33 and on the types of contractual clauses that are allowed in the relevant jurisdictions. This should make it easier to assess the level of appropriability in concrete cases. Secondly, we distinguish between two types of effects: those on the diffusion of innovation and those on the merged parties’ incentives to innovate. The first type of effect applies to both existing and future technologies. The investment effect is only relevant for future technologies. 34

4. Coordination of R&D investments

Consider a situation without spillovers and—for simplicity—without licensing. Before the merger, A and B ran their own research programs in an uncoordinated manner. It is useful to distinguish between two polar types of research environments: “directed” research, where the type of innovation to be obtained is reasonably clear at the outset of the research program; and “undirected” innovation, where the nature of the invention is a priori ill-defined. The pharmaceutical sector, where research programs are often targeted at a specific condition or approach, is an example of a (mostly) directed innovation environment; while the chemical sectors, where large numbers of computer-generated molecules might be tested in search of useful properties, comes closer to an undirected research environment. If research is largely undirected, then bringing the research programs of firms A and B under the same roof does not make it easier to avoid duplicative efforts. Whether A and B’s R&D programs end up with overlapping results depends mostly on chance. By contrast, directed research investments can be organized more efficiently to avoid duplicating efforts. From a static perspective, such an efficiency only benefits the merging firm. Because the type of cost-saving involved is likely to affect mostly fixed costs, these benefits are unlikely to be passed on to consumers to any meaningful extent. The effect of duplication avoidance on the total amount of R&D investment by A and B is a priori ambiguous: on the one hand, avoiding duplication makes every pound (euro) invested in R&D more fruitful, increasing the firms’ incentives to invest. On the other hand, the merged entity eliminates the expense from duplicating efforts, which tends to decrease total investment. However, as we have formally shown elsewhere, 35 while the prospect of avoiding duplication has an ambiguous effect on total R&D investment, it has a positive effect on the expected amount of realized innovation. In other words, the parties might reduce total investment, but the investment used for nonduplicative research increases postmerger.

5. Sequential innovation

Innovation is a cumulative process. Successive generations of products are introduced. Some reflect only minor improvements, while others are true breakthroughs. In most cases, the current ability of an industry to innovate depends on previous innovations and accumulated experience. Such sequential innovation processes have been analyzed extensively in the economic literature. 36 While the main focus of this literature has been on how IPRs should be designed in order to ensure that all firms involved in the successive chain of innovation have sufficient incentives to invest, one can also draw some lessons about the impact of mergers.

Consider an initial innovation obtained by A. Without this first innovation, the next step would not be possible (or it would be much harder to get to). Assume for simplicity that A itself cannot undertake the next step and that B is the only likely follow-on innovator. The key insight is that the first and second innovations are both substitutes and complements. They are substitutes because the second innovation makes the first one obsolete (or at least less valuable), and they are complements because the second innovation could not emerge without the first one. We can now consider two different premerger scenarios.

In the first situation, both A and B can be patented, but B cannot be used without infringing A. For a given IPR regime, this would occur if innovation tends to be incremental rather than drastic.

37

If A and B are independent firms, there are three potential problems. The first issue is that, in order to get sufficient incentives to innovate, A must get rewarded not only for the benefits that its innovation brings directly to consumers but also for the fact that it makes subsequent innovation (and hence further benefits to consumers) possible. The second problem is that, because B might make A’s innovation obsolete quickly, and A would anticipate this, A might not have sufficient incentives to invest in the initial innovation. In other words, A would not be rewarded for the fact that its own innovation makes the following innovation possible. The third issue is that B might be fearful to invest in the second innovation knowing that it will likely infringe A’s patents and that, if licensing cannot be agreed ex ante, A would set a licensing rate that might not reward B adequately for its own (sunk) investment. In other words, if the parties cannot agree on licensing terms before B invests in R&D, then B might be a victim of hold up since its R&D costs will be sunk when the terms of the licensing contract are agreed. Since ex ante licensing often is not feasible, hold up is a concern. It leads to insufficient investment in the follow-on innovation. Furthermore, unless licensing allows the initial innovator to capture the full net value of the second innovation, A’s own incentives to innovate may remain insufficient. A merger between A and B resolves both issues if it intervenes before either firm has invested (i.e., this type of benefit applies only to future technologies). Therefore, if ex ante licensing is not feasible or the initial licensor cannot extract the full value of its innovation, then a merger between the two parties improves innovation incentives for

In the second situation, B does not infringe A’s initial IPRs. This leaves us with only the first two issues: the initial innovator is not properly rewarded for “opening up the field” with its initial innovation, and this is made worst by the fact that the second innovation eats into the profits from the first innovation. This time, the beneficial effect arises whether or not ex ante licensing is feasible and perfectly efficient. On the other hand, there is also a countervailing effect. If A and B belonged to the same firm, then B would consider the fact that its subsequent innovation “cannibalizes” the revenue flow of the initial innovation. B’s innovation incentives would therefore be lower within a merged firm than with independent companies. This creates a trade-off: a merger helps provide sufficient incentives for the initial innovation but might slow down follow-on innovation.

We now turn to the practical questions of when sequential innovation considerations should be taken into account and how the magnitude of the effects discussed above could at least be gauged. Clearly, the considerations above only apply if innovation is indeed sequential, in the sense that later innovations rely substantially on earlier ones. We also need A and B to have been/be/be likely to be active in the same technology area. 39 This second condition is easily verified based on patent data. The first condition can be checked, both for the industry as a whole and for the merging parties in particular, by looking at patent citation patterns. At the industry level, one would look at the number of citations that the main players make, in their own IPRs, to IPRs held by other firms. For the merging parties, one would look at the bilateral pattern of citations to each other’s IP. The larger the number of citations, the more likely it is that the effects discussed in this section would be significant. Importantly, because the possible benefits of mergers discussed here apply to future innovation, there are no reason to limit the investigation to recent patents. On the contrary, the overall pattern of innovations and citations over a significant period of time would likely be more informative. Furthermore, one might be able to get a grip on the issue of likely infringement by looking at the “X and Y” classification of patent applications at the European Patent Office (EPO), which tell us how likely—in the examiner’s opinion—a patent is likely to infringe on others. 40 Again, what matters is how often a firm’s patent might infringe the patent of another company, especially a patent of the potential merger partner. We will return to this issue when discussing legal certainty.

The final piece of evidence relates—again—to the efficiency of the licensing market. The better the licensing market appears to work, the less important considerations arising from sequential innovation are. In particular, these considerations would be much less relevant in industries where ex ante licensing appears to be common.

6. Legal certainty

A distinguishing feature of IPRs is that they are both probabilistic and vague, or at least more probabilistic and vaguer than other property rights. They are probabilistic 41 because there is a significant chance that they would not be upheld in court if challenged. They are vague because the object to which they apply—as described in the claims—leaves a significant margin for interpretation, meaning that infringement is itself uncertain.

These features make the process of investing in innovation, as well as the process of producing and selling innovative products uncertain and potentially perilous. It can be hard for a company to determine in advance whether its product might be subject to significant demands for royalties. From the other side, a patent-holder cannot be sure of getting a material monetary return for the corresponding innovation. This state of affairs has two main consequences. Firstly, it can have a chilling effect on both innovation and sales. Secondly, it tends to lead to fairly frequent—and expensive—litigation. Both of these effects are socially harmful. A merger helps reduce uncertainty and avoid conflicts, at least in relations to the IPR and products of the other merging party. This is an efficiency.

The magnitude of this efficiency is likely to be greater in industries where IPRs are not easily defined—software and some branches of electronics are examples—than in industries like pharmaceuticals where there is much less ambiguity. The frequency and cost of litigation could also help us assess the importance of the efficiencies involved. This type of consideration matters more if the merging parties innovate in the same technology areas and/or have been opposed in litigation in the past.

Another useful measure might be the citations-based metric of potential infringement that we have already discussed above. Unfortunately, this metric is only available for EPO patents. 42 Notice, however, that the overall “chilling” effect of uncertainty and vagueness on innovation and sales is much harder to measure. Assessments of the scale of efficiencies linked to increased legal certainty are therefore likely to be systematically too low.

C. Product-Market Effects and Innovation Efficiencies: Conclusion

We have argued that, once we assume that competition policy would deal effectively with the usual static effects of mergers and if we focus on effects in or mediated through the product markets, the innovative activities of the merging parties—and of their rivals—do not raise additional concerns. Having pointed out that, just as for productive efficiencies, there are likely to be scale and scope economies in the production of innovation that are hard to measure, we conclude that there is no reason for treating mergers more strictly simply because the merging partners have significant innovative activities.

We then reviewed a number of additional sources of potential merger-related efficiencies, which are specific to innovative activities, that is, they arise because of the peculiar “knowledge” nature of innovation and are therefore additional sources of efficiencies that would not arise in the absence of innovation. While it seems proper to let the parties bring evidence to support such efficiency claims—and we indicated the type of evidence that might be needed—it seems unavoidable that these inefficiencies cannot be fully documented. If so, then there is an argument for treating mergers with a significant innovative dimension more leniently than purely “static” transactions.

We now turn to merger-specific issues—other than efficiencies—that might arise in or through the technology and innovation markets.

III. Technology Markets

Technology markets are those where technologies are for sale, either as full transfers of IP or in the context of licensing agreements. In the usual hierarchy of markets from innovation markets to technology markets to product markets, technology markets concern the use of technology for the purpose of making and selling goods and services. This is why market shares and market power in technology markets are customarily assessed based on the market shares of the corresponding goods and services in relevant downstream product markets.

In this sense, then, technology markets have no direct bearing on how incentives to innovate might be affected by a merger. 43 This of course does not mean that competition authorities should not look the potential effects of a merger in technology market. It remains true, for example, that, as in any other market, horizontal overlap between the “product lines” of the merging parties would tend to increase the price at which these products are made available to others. Hence, a merger between two parties with IPRs on technologies that are substitutable in some use would be a concern and might require some IPR divestment.

Complementarities between IPRs would work the other way. So-called “patent thickets” arise when the production of a good or service requires access to IP held by a large number of independent entities. Thickets lead to the well-known “Cournot” double marginalization problem: when setting its licensing conditions, each IPR owner fails to consider that a higher variable royalty means lower sales of the product and hence lower receipts for other licensors. If two IPR owners merge, they take this complementarity between their respective IPRs into account and ask for lower royalties. While this mechanism is identical to the reason why mergers between firms selling complementary products are often thought to be benign, one should point out that this type of complementarities is likely to be more prevalent in technology markets than in product markets. This is not only because increasingly complex products tend to rely on a very large number of IPRs, but also because the probabilistic and vague nature of IPRs—discussed above—tends to create complementarities even between IPRs covering closely related technology. If patents A and B cover similar processes, and so normally would be regarded as substitutes, the fact that their respective validity and scope are uncertain means that potential users might actually want to acquire rights to both. In other words, they would want to treat them as if they were complements.

IV. Innovation Markets

Innovation markets are not really “markets” since they often do not correspond to the sale of any products or services and, accordingly, no prices are set within their confines. 44 In this sense, “innovation markets” are best understood as a stage in the vertical chain of activities where firms carry out a variety of research programs in the hope of obtaining new, commercially valuable knowledge. Since the intensity and efficiency of such research efforts are an important determinant of consumer welfare in the medium to long run, the potential effects of a merger on the activities of the merging parties and of their rivals are a proper focus of merger review. In Section II, we discussed the effects that might arise because of overlap between the product lines of the innovative parties. In Section III, we briefly examined the consequences of a merger for firms that might use the technologies produced by the merging parties in order to produce their own products or services. In this section, we will mostly focus on the effects that are not triggered by well-identified overlaps or complementarities between the product lines to which the results of R&D are applied.

A. Are There Horizontal Issues in Innovation Markets?

What does it mean to say that the innovative activities of the merging partners “overlap”? In Section II, we argued that innovation incentives came from the desire to improve the sale of particular products so that innovation incentives could only be affected by the merger if the product lines of the two parties overlapped. Hence, if product line overlap is already eliminated in order to deal with traditional static concerns, no additional “horizontal” issues should arise in innovation markets.

However, this argument needs to be nuanced for two main reasons. First, the link between R&D activities and the product market is not always as clear-cut as we have taken it to be. Second, evidence from the innovation market can be useful to help define what the relevant overlap in downstream markets might be.

1. The link between innovation and product markets: a “pure” innovation theory of harm?

Economists and specialists in management of technology distinguish between two polar types of research environment. 45 Directed research refers to situations where a given research effort is aimed at addressing a well-defined need that arises in well-defined product market(s). Examples would include the search for a malaria vaccine or improvements in car tires. Undirected research evokes a situation where the types of products to which the resulting innovation might apply is not well known ex ante. In its extreme form, undirected research would amount to “letting smart people do what they want” and then seeing what comes out. In practice, undirected research seems to be a better approximation when the commercial potential of research is not a priori well defined. For example, research in battery technology can lead to longer lasting batteries, faster charging batteries, or batteries relying on different active ingredients. Moreover, even if we limit ourselves to one of these dimensions of quality, the type of products in which the new technology would perform well (e.g., cars, smart phones, airplanes) cannot be identified clearly until the precise manner in which an improvement is achieved is known.

Undirected innovation modifies our previous analysis. While the eventual financial rewards to R&D will of course depend on the product markets in which the innovation is used, the chances that a particular R&D project would be useful in an area where the product lines of the two parties currently overlap can be so low as to be irrelevant. In such an environment, requiring the divestment of existing overlap in the product market would have no material effect on the innovation incentives of the merged entities. Static and dynamic efficiency then become separate issues, as addressing static concerns does not “automatically” address dynamic issues.

If horizontal overlap in innovation markets is to matter, it must work through a different mechanism than product line overlap. A main mechanism is the advantage of being first. Consider for example what economists refer to as “patent races.” Firms invest in R&D with a specific type of innovation in mind. We can think of this in terms of the battery example above: research is “directed” in the sense that it is targeted at a specific technological area; however, the link between this area and corresponding product markets is very weak. The first firm to innovate successfully obtains a patent. Unless the breadth of patent protection is very narrow, this means that lagging firms might find out that their own R&D efforts lead to an innovation that is no longer patentable (because of prior art) and/or infringes the patent obtained by the first innovator. There is therefore a premium on “getting to the technology first.” To see what this implies for the merger of two firms involved in similar research, consider the decision problem of one of the merging partners before and after the merger. Getting an innovation early is more costly than getting it at a more leisurely pace. By investing more in R&D, firm A increases its chances of getting there first. Of course, this also decreases B’s chances of winning the “patent race,” but A does not take this into account. After the merger, A does take into account the fact that increasing the speed of its R&D program decreases the expected return on B’s own R&D investment. This leads to a reduction in R&D investments after the merger and a corresponding delay in the speed of introduction of new technology. There can therefore very well be a theory of harm that arises in the innovation market and does not rely on the existence of overlap between the parties’ product lines.

In order to assess the relevance and magnitude of this effect, “horizontal overlap” is best defined in terms of the “technological areas” used by the relevant patent offices. In practice, then, this type of overlap ought to be assessed by an analysis of the long-term patenting behavior of the merging parties, relying on both technical areas overlaps and the prevalence of citations between their respective patent applications. This can be complemented with information on failed research projects if it is available.

A note of caution is needed. While patent races have provided fodder for a large number of academic papers, it is not clear that they represent the actual research environment very well. Often, research is motivated by a perceived need rather than by the pursuit of a particular type of solution. Moreover, patent breadth is rarely so large—or so well defined—as to prevent a laggard from also protecting the fruits of its own research. 46 In such cases, R&D competition does not look much like a race for a single prize. However, similar overlap issues arise, even without the likelihood of patent infringement, if there is another source of “first mover advantage.” This could, for example, be lock-in effects (once users have invested in the early technology they are reluctant to switch) or network effects. In this respect then, for example, “overlap” in the innovation market would tend to be a relevant concern when the parties are significantly involved in areas where most of the value of R&D outcomes comes from their inclusion in industry standards.

2. Remedies in innovation markets

In the polar case of fully “directed” research, divestment of overlap in the corresponding market is the obvious solution, as discussed in Section II. With fully “undirected” research, such an approach is not effective since investment decisions depend not on downstream overlap but on overlap in the technological areas where the parties undertake research. Moreover, even when there is some link between R&D and downstream markets, a given R&D investment might—ex ante—have potential applications in so many downstream markets that downstream divestment might not be a practical approach. When R&D is not clearly directed to specific downstream markets, then, we have to look at remedies in the innovation market themselves.

Without direct linkages to product markets, overlap in the innovation market only raises serious concerns if entry into these markets is impeded by the difficulty of accessing some inputs (see below). Otherwise, a reduction in the joint R&D activities of the merging parties should lead to entry. In some sectors, however, effective research requires costly and indivisible infrastructure. It also requires well-functioning research teams. Because the dynamics of research teams are still poorly understood, such teams might also be difficult to replicate even if labor markets are reasonably fluid. As these types of assets might be difficult to reproduce for an entrant, there is a case for divesting ownership of the assets themselves or—in the case of infrastructure—for providing fair access to the relevant infrastructure. In this perspective, requiring the divestment of research teams—as in Dow-Dupont—can be sensible. In a similar vein, the EC insistence that GSK keep an active oncology research team after transferring much of its oncological activities to Novartis in exchange for its vaccine business would appear to be justified.

3. Using innovation markets to help define product markets: research “pipelines.”

In pharmaceutical mergers, it has become customary for competition authorities to consider the “pipeline” of the merging parties. The pharmaceutical industry lends itself particularly well to such an approach as the regulatory process makes it easy to identify different stages in the development of a new product, from the patenting of a new compound or method to various levels of safety and effectiveness assessments. What is such evidence useful for?

In Europe, the EC concerns about “pipelines” seem to stem from product market effects of the type discussed in Section II. If two pharmaceutical companies, for example, have one drug each that is targeted at the same condition at some stage of the pipeline, competition authorities fear that a merged entity would simply decide to drop the less promising of these two research programs. As a consequence, competition in the corresponding market for treatment of the condition might end up being less vigorous than it otherwise might have been. This type of concern is greater if both programs are in the later stage of development since the possible loss of competition is both more probable (as each project has a significant probability of succeeding) and would take place within a shorter-term horizon.

There is a good argument for also using the analysis of “pipelines” as a window on horizontal overlap in product markets. Given the uncertainty inherent in research, looking at overlap between current products and current innovations might be too narrow. A better idea of the potential overlap between merging parties can be obtained by looking at the pattern of investment, successes, and failures over a significant period of time. In this sense, a snapshot of the merging parties’ pipeline suffices to evaluate likely, fairly immediate product market effects but a full retrospective is needed to assess effectively horizontal overlap over a longer time horizon.

4. The EC’s distinction between potential competition in product markets and “innovation” competition

In Section 3.3. of the Dow-Dupont decision, the EC distinguishes between “potential competition” in well-defined product markets and “innovation” competition. The EC’s views are most easily explained in the context of the pharmaceutical industry where clinical trials go through three well-defined phases. The probability that a product will eventually make it to market tends to increase drastically from one phase to the next. The EC concludes that overlap between projects in stage III or between these projects and existing products creates a risk of decrease in potential competition in the relevant product markets while overlap between projects in phase I and II means that a merger might reduce competition in the relevant innovation markets.

From our previous analysis, it should be clear that this framework does not match ours. For us, the relevant distinction is whether or not projects in stages I through III are “directed” towards a specific product market or whether the markets on which the eventual R&D successes will prove useful are as yet rather unclear. In this sense, all pharmaceutical projects having reached even phase I trials are already linked to a potential product market and would not be relevant to what we refer to as an “innovation” theory of harm. Whether the chances of success of the trials is 50%, 10%, or 0.1%, the merger matters because these projects—if successful—would yield products that overlap with those of the merging partner. The root of the problem is still product market overlap.

Of course, even issues stemming from (potential) overlap in the product market might require remedies farther upstream. In particular, going back to the pharmaceutical example, fears that the merged entity might abandon a phase II project that potentially competes with some of its products (or other projects) 47 can be minimized by requiring the divestment of this project with all relevant IPRs, crucial personnel, and essential facilities.

For us, however, such concerns are not an “innovation theory of harm” but a traditional theory of harm stemming from overlap in product lines that calls for remedies in the innovation market. In our own framework, an innovation theory of harm is one that refers to the likely effect of a merger on R&D projects—already started or not—and that does not rely on a clear link between innovation and product markets. As explained above, such theories of harm may be valid when R&D is not “directed” or is only vaguely so. In that case, the potential harm from the merger comes from overlap between the type of R&D conducted by the merging parties and the means required to conduct such research. Here, both the source of harm and the required remedies are found in innovation markets themselves.

Of course, the two types of theories of harm are not exclusive. In fact, the type of innovation theories of harm that we have discussed above can very well work on top of theories of harm grounded in product market overlap: once the overlap issue has been resolved through appropriate remedies, we are de facto back in an “undirected research” environment where innovation theories of harm might well be relevant.

B. Vertical Foreclosure

There are also relevant markets upstream of innovation markets: the markets for inputs into the innovation process itself. If one or more of the merging parties has significant market power over the supply of some inputs and there is overlap between the parties in innovation markets, in the sense defined above, then traditional foreclosure concerns come to the fore. Such concerns would then be addressed by some combination of divestment of research assets relating to overlapping activities—as in Dow-Dupont—and mandatory licensing—as in the Russian Bayer-Monsanto decision. 48 Indeed, the genetically modified (GM) crop industry provides good examples of how a transaction might raise foreclosure concerns in the innovation market. Innovation in GM crops comes from the application of GM technology to specific seeds. As of 2012, Monsanto controlled 27% of the world’s seed supply. While reliable numbers per crop do not appear to be available, the share of ownership in a number of relevant seed market is bound to be significantly higher. The merger could therefore lead to a refusal to license seeds needed for rival GM innovators to develop new products/new traits or to a worsening of the licensing conditions. This would impair the rivals’ ability to conduct research efficiently. 49

V. The Direction of Innovation

So far, we only analyzed how a merger might affect the total investment in innovation and the amount of distinct innovation that would arise from this investment. In this section, we propose extending this conventional approach to potential concerns about how a merger might affect the type of innovations being pursued. This is controversial. The profession is still divided about the aspects of the various Microsoft decisions dealing with the inclusion of additional features (Explorer, Mediaplayer) in the operating system as some feel that antitrust authority interferes with legitimate product design decisions. In this context, suggesting that authorities scrutinize the firm’s choice of how to allocate its R&D funds between various areas of research and/or various products might seem like a bridge too far.

We would certainly not recommend that the effect of a merger on the allocation of a given level of R&D investment be part and parcel of every merger review with a significant innovation dimension. However, there are specific circumstances where such an angle would be useful. Consider for example the case of GM crops. The genome of crops can be modified to change or enhance some “traits” such as resistance to disease or pest, resistance to herbicides, or drought tolerance. A lot of basic research has already been undertaken, and there are numerous patents dealing with many possible combinations of traits and popular crops. By contrast, the GM crops that have actually been introduced in the market exhibit little variety: herbicide resistance and pesticide resistance are traits that have been commercialized much faster and much more widely than other traits—such as resistance to environmental stress—that might well be socially more valuable. 50 One explanation for this bias is that several important GM crops companies are also large agro-chemical producers. Herbicide resistance, for example, is not generic: a crop is only made resistant to a specific type of herbicide (e.g., glyphosate-based). By developing this specific herbicide resistance, the company therefore also promotes the use of its own chemicals. This complementarity biases the firm’s development decisions towards these particular traits. While authorities should of course not interfere with the firms’ ongoing product development strategies, we believe that ensuring that harmful market biases are not reinforced by a merger is a legitimate concern for the reviewing authority. After all, why worry about possibly small effects on prices if the transaction is likely to deprive the local market of welfare-enhancing products, as a larger, discrete effect?

The Bayer-Monsanto acquisition provides an interesting example. The transaction would increase the weight of the “chemical” side in a major GM crop company. As such, it is very likely to further decrease the company’s incentives to invest in developing GM crops with nonchemical resistance traits even though the entity owns a number of relevant patents that could block others from going forward. This would be a concern for economies with a significant agricultural sector and local growing conditions that could benefit from some specific form of stress or disease resistance. Russia and Brazil are two such countries. It is therefore interesting that Russia has imposed remedies involving the licensing of technologies to local firms 51 and that Brazil has urged the EC to go further in its demands. Similar issues can arise in pharmaceuticals where different countries have different needs and a merger might bias the future plans of the entity away from locally required products.

Clearly, this is an issue that requires more thought. For example, one might argue that any significant bias could be addressed through a form of essential facility argument as the company has patents that might prevent others from delivering the needed product. If the patents are strong enough, and the unfulfilled need can be documented, a traditional essential facility argument could be made. However, essential facility cases are notoriously hard to bring and win. One would therefore understand if some countries—especially those without the market cloud of Europe or North America—would prefer to rely on the merger review process instead.

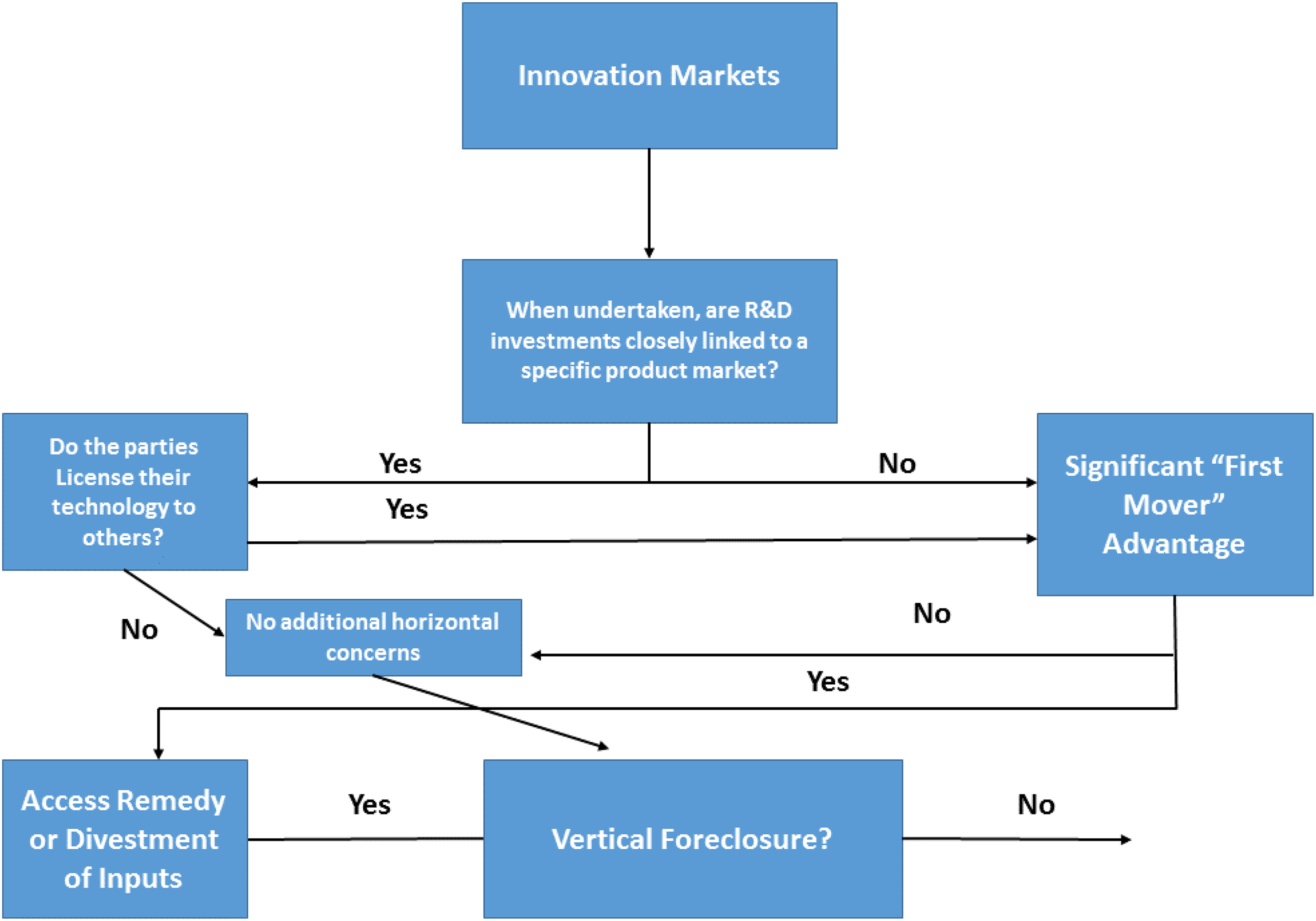

VI. A Policy Algorithm

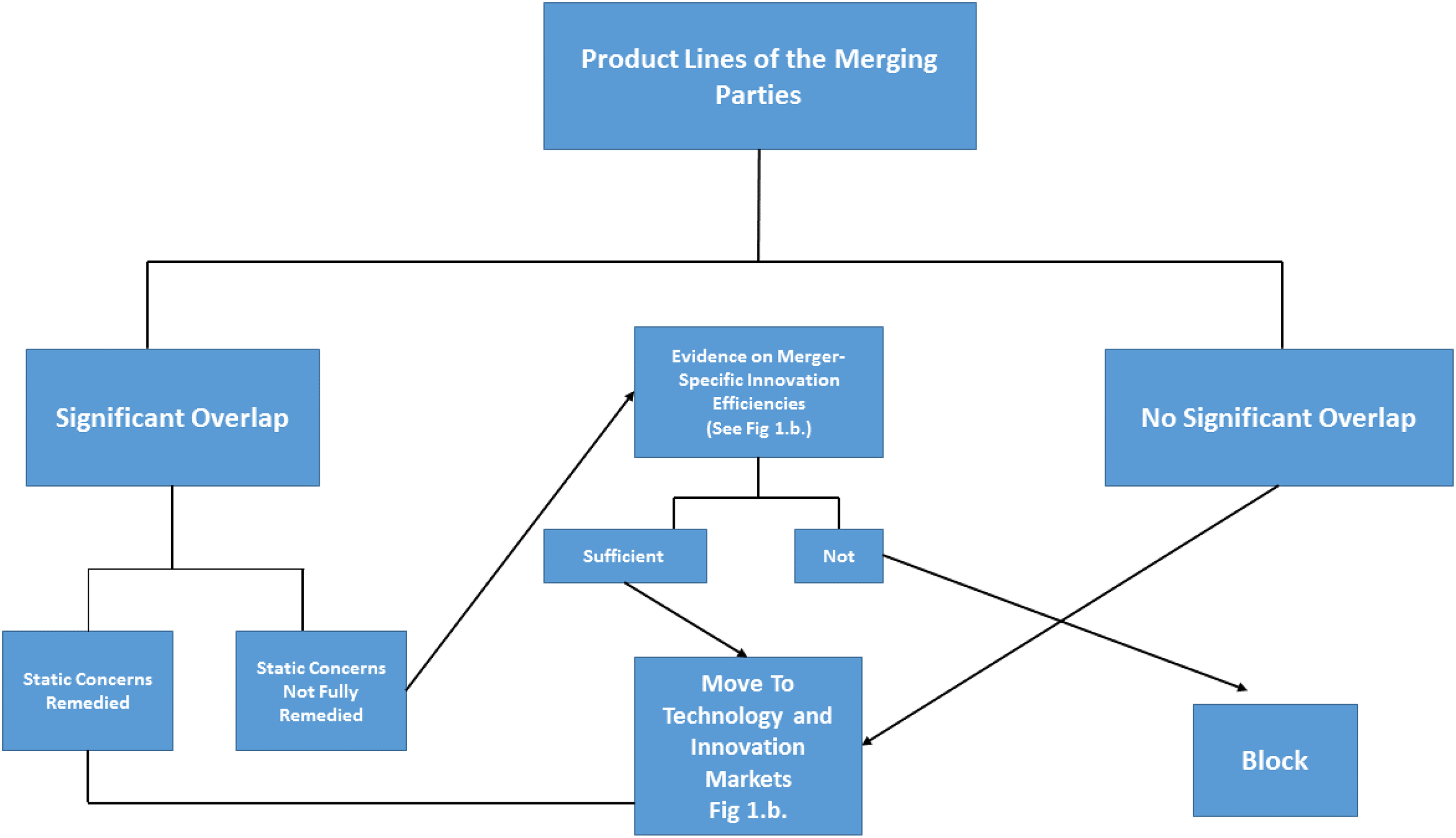

We are now in a position to summarize the main insights of this note in terms of a policy algorithm, that is, a simplified flow chart indicating how a Competition Authority might proceed, and what evidence should be gathered, depending on some identifiable characteristics of a specific case. Of course, such an algorithm can only provide some rather broad guidance, and one should always have an eye for case-specific features that might require us to deviate from the suggested approach. However, starting from a reasonable, well-understood approach still seems valuable.

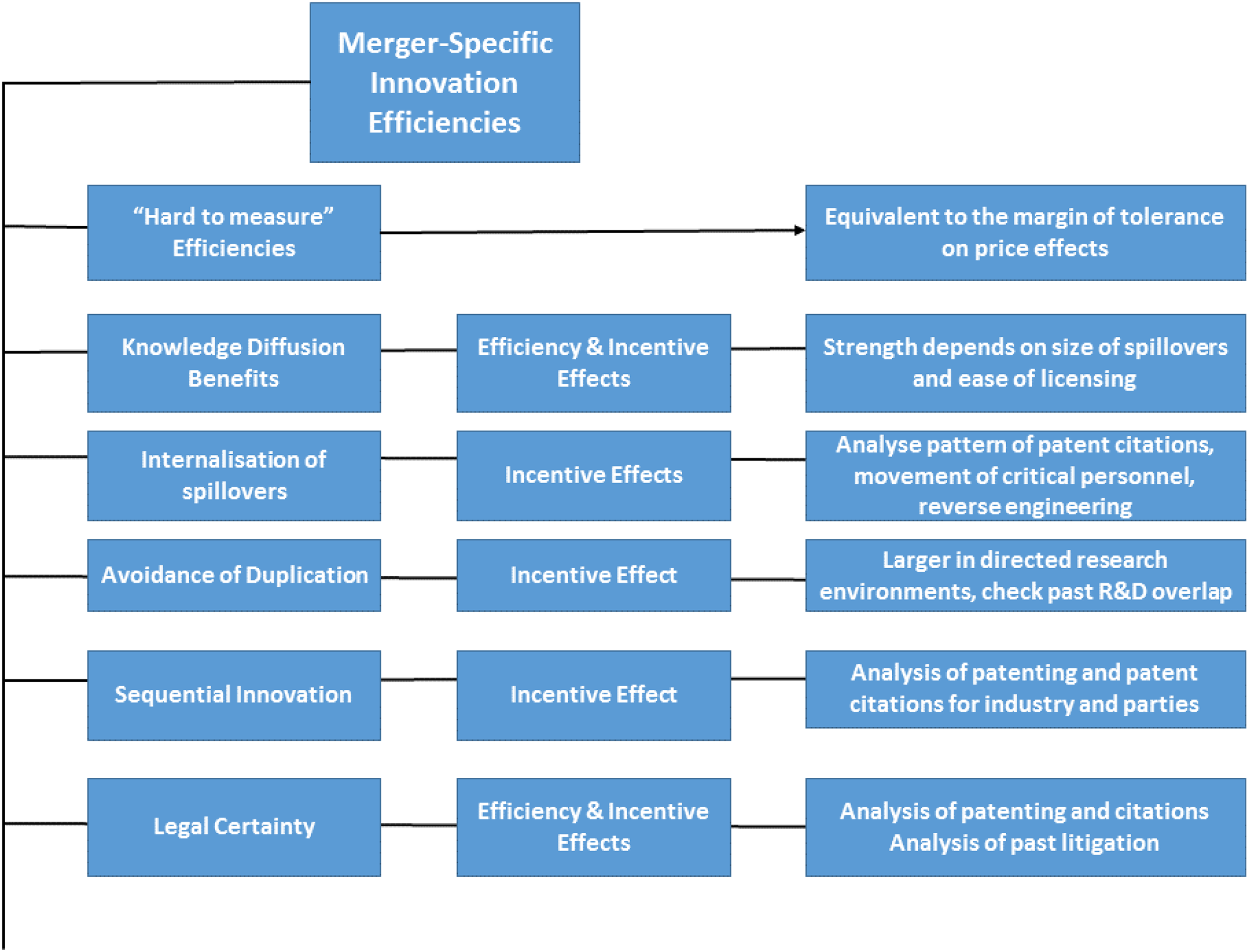

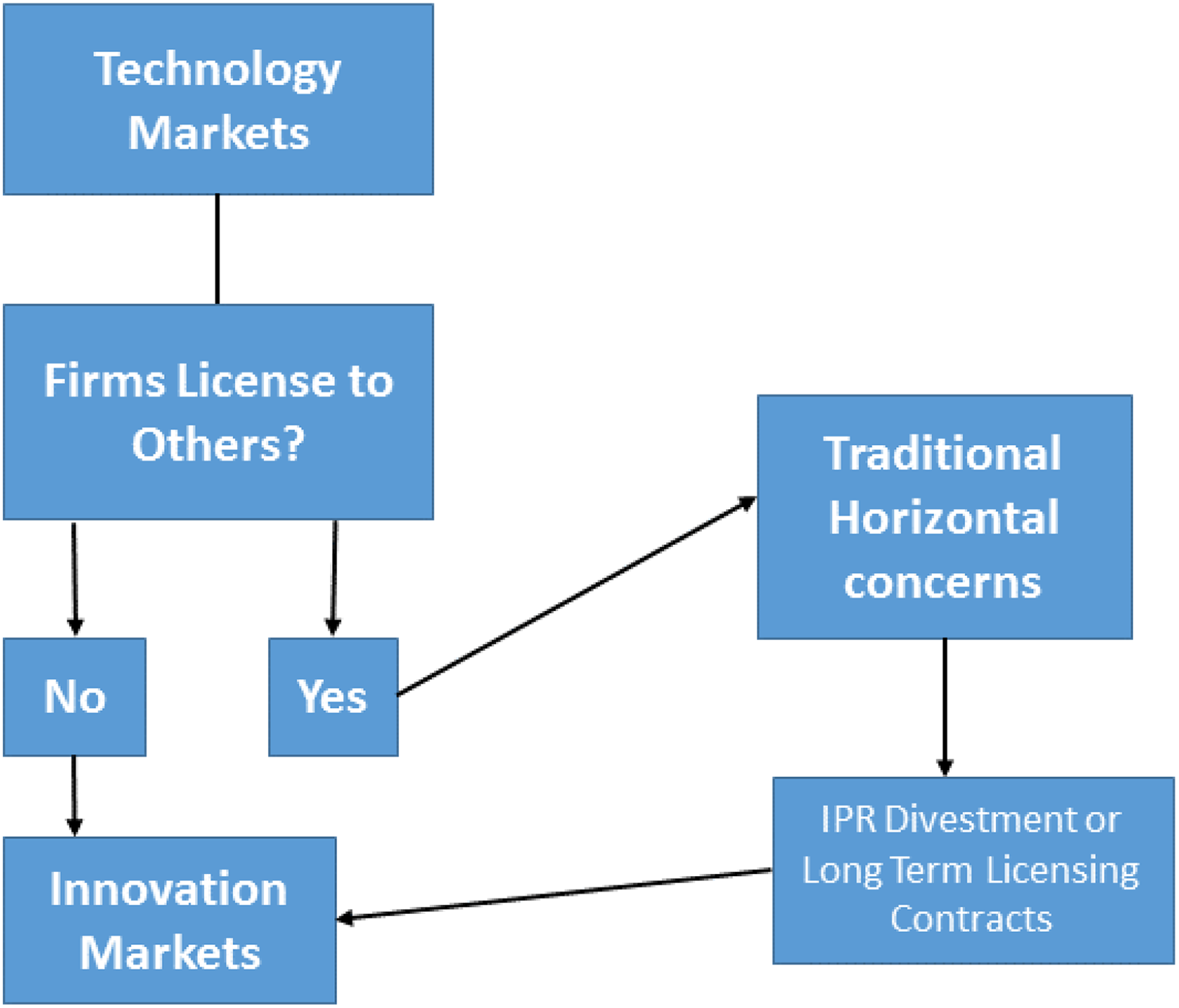

Figures 1.a and 1.b summarize our discussion in Section II. Figure 1.a illustrates how dealing with static concerns should also resolve innovation issues linked to the parties’ incentives to compete on product design. If overlap cannot be handled satisfactorily, then one must consider efficiencies. At this stage, we suggest looking at all sources of efficiencies, including those that might arise in technology or innovations market. This makes it possible to get closure if these efficiencies prove to be insufficient. Figure 1.b lists the main sources of efficiencies, indicating whether these results from cost reduction (“efficiency”) or/and from increased incentives to innovate. We also briefly mention the main factors affecting the likely magnitude of these efficiencies and the type of evidence that would be relevant to their assessment. Figure 2 summarizes technology market considerations, and Figure 3 provides guidance for the analysis of innovation market effects covered in Sections III and IV.

Product market analytical structure.

Product market analytical structure: sources of efficiencies.

Technology market analytical structure.

Innovation market analytical structure.

VII. Conclusion

In the wake of the Dow-Dupont decision, the debate about the role of innovation in merger review has been intense, sometimes even acrimonious. There is no good reason for this: the recent academic contributions prove to be remarkably compatible. For example, there seems to be little doubt that allowing mergers to lead to higher prices, because this will increase innovation incentives, is a bad idea. Where the authors differ is in the type and number of other factors included in the analysis. Clearly, the overall effect of mergers on innovation cannot be the same if one also considers R&D coordination, diffusion of knowledge, sequential innovation, and/or legal certainty.

In this perspective, we hope that this article can contribute to the debate on three fronts. First, in exchange for mathematical formality, we review the economics behind a more extensive set of factors that are likely to influence the effect of mergers on innovation than any other recent papers. Having as complete a list as possible is important if we are to deal effectively with mergers across a variety of innovation-driven industries. Moreover, the list of potential innovation-specific efficiencies is rather long. While such efficiencies should of course be assessed on a case-by-case basis, the sheer number of channels through which they operate suggests that mergers are more conducive to efficiency gains in industries where innovation is an important driver of competition. Second, these different factors are organized around a few well-known economic and legal concepts: (pecuniary and knowledge) externalities; scale effects; appropriability; and the distinction between product, technology, and innovation markets. Third, we move beyond a conceptual discussion to suggest types of evidence that might be useful to the assessment of the merger. We also propose a “policy algorithm” to help guide both antitrust authorities and parties to navigate the complexities of merger-specific innovation issues. Clearly, this algorithm is not supposed to be a rigid set of rules. Rather, we provide a framework intended to facilitate incorporation of the insights of the literature into current decision-making. We are certain that further discussions will modify some of our recommendations. Indeed, our own thinking is likely to evolve as new arguments are made and new cases reveal unexpected difficulties or new approaches.

A central theme of our analysis is that we need to distinguish between innovation effects that are grounded in (potential) product market overlaps and those that are not. Even though the first type of effect might require some divestment in innovation markets, this type is very similar to traditional static efficiency concerns and can be handled by remedies that reduce downstream overlap. By contrasts, one can build reasonable theories of harm that operate entirely within innovation markets. We have argued that such theories of harm are best understood in terms of “undirected” research and that they arise when R&D is characterized by significant first-mover advantages in technologies. Remedies typically involve the divestment of IPRs, of research teams, research facilities, or other essential inputs into the R&D process.

Finally, we suggest that competition authorities should pay attention not only to the effect of mergers on the level of innovation but also to the type/direction of R&D efforts. We know that this is controversial but believe it is a debate worth having.

Footnotes

Acknowledgments

This article further develops some of the arguments broadly outlined in Pierre Régibeau and Katharine Rockett, Mergers and Product Innovation: Seeds and GM Crops, in G

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.