Abstract

This article extends the corporate social performance (CSP) model by studying the role of governance structures and governance systems in shaping corporate social responsibility. The authors argue that a governance perspective offers a fruitful research strategy both to study empirically how firms balance the competing moral frameworks and political philosophies that are part and parcel of defining their role in society and to further the theoretical integration of the descriptive and normative perspectives in the business and society field. They illustrate the potential of this research strategy with a comparative case study of processes of responsiveness at four Dutch banks with markedly different governance structures. This study shows how governance systems and structures both enable and constrain corporate responsibility and responsiveness. The authors conclude with a proposal to reorient the CSP model to harness the integrative potential of studying corporate social responsibility through a governance lens.

Corporate social responsibility (CSR) has long been recognized as an important management topic, and over the past 30 years, a steady stream of theoretical papers has clarified the concept (e.g., Carroll, 1979, 1999; Jones, 1980; Schwartz & Carroll, 2008; Wartick & Cochran, 1985; Windsor, 2001; Wood, 1991). At the same time, reviews of the literature show a continuing struggle with the CSR concept, both theoretically and empirically (Griffin, 2000; Griffin & Mahon, 1997; Margolis & Walsh, 2003; Rowley & Berman, 2000; Windsor, 2006). For instance, Rowley and Berman (2000) concluded that CSR analysis has not advanced much beyond a clarification of the concept and that much of the empirical research has been limited to legitimizing the business and society field. More recent, Windsor (2006) observed that CSR remains an embryonic and contestable concept. These critical evaluations of the CSR literature have led to calls for more descriptive research to study in detail how firms’ roles in society are actually shaped in the interactions between firms and their stakeholders (e.g., Freeman, 1999; Griffin, 2000; Margolis & Walsh, 2003; Rowley & Berman, 2000).

The purpose of this article is to propose a research strategy for such descriptive studies. This proposal is based on incorporating governance systems and structures into the corporate social performance (CSP) model (Carroll, 1979; Swanson, 1995; Wartick & Cochran, 1985; Wood, 1991). We argue that a governance perspective on CSR can help focus research on the ways in which firms’ roles in society take shape. We illustrate the potential of this research strategy with a comparative case study of four Dutch banks with markedly different governance structures. We studied how these banks evolved over a 14-year period that was triggered by the deregulation of their industry and characterized by an internationalization process that increasingly exposed the banks to competing stakeholder claims. The study demonstrates the central role of the stakeholder-oriented Dutch governance system as well as the banks’ different governance structures in shaping their responses to these competing claims.

In addition to offering a fruitful strategy to focus empirical research, we believe that our proposal to incorporate governance into the CSP model can also help the business and society field to make progress on two theoretical problems. The first problem is the “integration dilemma” (Swanson, 1999), or the lack of unification of the normative and descriptive approaches to CSR (Weaver & Trevino, 1994). The second problem is the contested nature of CSR, or the inherent incompatibility of the moral frameworks and political philosophies that compete for the attention of firms (Matten & Moon, 2008; Mitnick, 2000; Windsor, 2006). The crux of our proposal to study CSR through a governance lens is the argument that governance systems and structures both enable and constrain the processes in which competing moral and political claims play out. The corollary of this argument is that the normative and descriptive approaches to CSR can meet in studies of the sociopolitical construction of CSR, or the way in which the results of “value attunement” (Orlitzky & Swanson, 2002; Swanson, 1999) become institutionalized in governance systems and structures that shape firms’ responsibilities and responsiveness.

The article proceeds as follows. The next section develops in more detail our argument for a governance perspective on CSR. We then introduce our empirical study and report its results, which show how governance interacts with firms’ social principles and policy outcomes. We subsequently discuss these results in terms of the integrative potential of studying CSR through a governance lens. We conclude with a proposal to reorient the CSP model from a taxonomic framework toward a model to guide descriptive research.

A Governance Perspective on CSR

CSR has a long and varied history as the, at times more and at other times less, central concept in the business and society field (Carroll, 1999; Windsor, 2001). The mission of the business and society field has been described as finding and developing a constructive business relationship with society (Swanson, 1999). In light of this mission, CSR can be construed as any concept that speaks to how managers should handle public policy and social issues (Windsor, 2006). Frederick (1987) identified three historical stages in the development of the CSR literature, broadly construed. The first phase called attention to the need for corporate responsibility, the second elaborated on managerial tools for responsiveness, and the third and current phase is primarily concerned with ethics and values. In the course of these three phases, there has been a changing emphasis on developing new perspectives on the business and society relationship, on one hand, and consolidation of research topics, on the other hand.

As Carroll (1999) has noted, the early years of modern CSR scholarship, from the 1950s onward, were marked by a proliferation of definitions of CSR, whereas the 1980s and 1990s were a time of consolidation, even while alternative perspectives on the business and society relationship were emerging. The emergence of these alternative perspectives, such as stakeholder management, business ethics, sustainability, and corporate citizenship, marked the advent of the third phase of CSR. Although this latest phase has enriched the business and society field, it has also raised concerns about an increasing fragmentation of the field and the need for renewed consolidation (Schwartz & Carroll, 2008; Windsor, 2001; Wood, 2000).

The main focus of consolidation efforts in the business and society field has historically been the CSP model (Carroll, 1999; Jones, 1995; Windsor, 2001). Wood (1991) articulated this model on the basis of her definition of corporate social performance as “a business organization’s configuration of principles of social responsibility, processes of social responsiveness, and policies, programs and observable outcomes as they relate to the firm’s societal relationships” (p. 693). Based on earlier work by Carroll (1979) and Wartick and Cochran (1985), and subsequently extended by Swanson (1995), the purpose of the CSP model is to organize pertinent CSR-related research topics into a framework that can further theory development and point to relevant questions for empirical research (Swanson, 1999; Wood, 2000).

However, although the CSP model has been successful as a focal point for conceptual integration of core CSR themes, it has not been used much to develop theory (Wood, 2000) or guide empirical research. This circumstance may be explained by the expansive nature of CSR, which involves such fundamental and wide-ranging phenomena that it relates to virtually all of the firm’s principles, policies, and stakeholder interactions. As a conceptual framework that seeks to capture all relevant aspects of CSR, the CSP model therefore offers only limited guidance for empirical studies. The typical suggestion to circumvent this problem is to focus on firm–society interactions on particular social issues in particular contexts (e.g., Griffin, 2000; Margolis & Walsh, 2003; Rowley & Berman, 2000). But, although such research could indeed help provide much-needed insight into the processes that are central to CSR, picking up on single social issues also means a narrower conception of CSR than the one implied in the CSP model (Carroll, 2000).

The problem of giving direction to empirical CSR research has been partially addressed by putting processes of responsiveness at the center of empirical inquiry. The responsiveness of companies to social developments has long been regarded as the crux of CSR (e.g., Ackerman, 1973; Carroll, 1979; Margolis & Walsh, 2003; Wartick & Cochran, 1985; Wood, 1991), and the central role of processes of responsiveness in the CSP model has subsequently opened up the possibility to use stakeholder theory (Clarkson, 1995; Donaldson & Preston, 1995; Freeman, 1984; Jones, 1995; Jones & Wicks, 1999; Mitchell, Agle, & Wood, 1997) to inspire theory development on the relationship between firms and society.

However, empirical research into how CSR is actually shaped in interactions with stakeholders faces similar problems as research based on the CSP model. In addition to the problem of where to focus, these also include the general problems of process research, such as the difficulty of analyzing the effect of managerial actions, or deriving a logic to compare companies or situations (Eisenhardt, 1989; Mintzberg & Waters, 1990; Pettigrew, 1990). As a consequence, how CSR is actually shaped in the interactions between companies and their stakeholders is still a question that needs to be studied in much more detail (Frooman & Murrel, 2005; Jones, Felps, & Bigley, 2007; Jones & Wicks, 1999; Luoma & Goodstein, 1999; Margolis & Walsh, 2003).

The research strategy that we propose in this article is to use governance structures and systems as a focusing device for empirical inquiry into how firms’ roles in society take shape in the interaction with their stakeholders. We define a governance structure as the sum total of all formal procedures according to which a firm’s decisions are made (de Graaf & Herkströter, 2007; Luoma & Goodstein, 1999) and a governance system as the legal context in which the firms’ governance structures are embedded. Although it has been shown that we can expect governance structures and systems to affect CSP (Halme & Huse, 1997; Hillman, Keim, & Luce, 2001; Kassinis & Vafeas, 2002; McKendall, Sanchez, & Sicilian, 1999; Mitchell et al., 1997), governance has not yet been given a central place in CSR analysis. An important advantage of governance structures and systems for CSR research is their formal nature, which makes the nature of the interactions of firms with their stakeholders much easier to identify. For instance, stakeholders may exercise control over a company either through their position in the firm’s governance structure or through the legal means offered by the governance system. Governance structures and systems therefore provide a useful lens to help make processes of responsiveness amenable to empirical research.

In addition to offering a useful empirical research strategy to study process of responsiveness, we also believe that a governance perspective can help the business and society field face up to two fundamental theoretical problems that are inherent in integrative efforts in CSR research. Swanson (1999) referred to the first of these problems as the integration dilemma, or the tension between normative and descriptive approaches to CSR (Jones & Wicks, 1999; Mitnick, 1995; Quinn & Jones, 1995; Weaver & Trevino, 1994). On one hand, there is the view that moral concerns take primacy over outcomes and that CSR needs to be evaluated in terms of a priori universal principles that are only open to philosophical inquiry. On the other hand, there is the view that CSR is about goals and outcomes that are subject to managerial intervention and that the relationship between corporate goals, managerial actions, and social outcomes is open to social science research aimed at causal explanation. Theoretical integration across the gap, defined by David Hume, between “is” (what firms do) and “ought” (what firms should do) is seen as inherently problematic (Trevino & Weaver, 1999).

The second problem may be called the “incompatibility dilemma.” The incompatibility between competing moral claims on business means that CSR is essentially a contested notion (Margolis & Walsh, 2003; Matten & Moon, 2008; Mitnick, 2000; Windsor, 2006). This problem is orthogonal to the first, in the sense that neither the normative nor the descriptive approaches to CSR entail a specification of the universal principles (in the case of a normative approach) or goals (in the case of a descriptive approach) that should guide firms’ relationship to society. In practice, these principles and goals are contested in ideological markets and are therefore, by their very nature, subject to sociopolitical processes (Mitnick, 2000; Windsor, 2006). This contestability is apparent not just in the competing moral frameworks and political philosophies that firms confront when shaping their role in society (Windsor, 2006) but also in the development of what Margolis and Walsh (2003) described as a “preoccupation” in the business and society field to establish the value of a stakeholder model of the firm in the very terms of the shareholder model that this stakeholder model purports to challenge. Although this preoccupation is easily understood against the backdrop of the conception of the firm’s role in society that dominates the Anglo-Saxon business system, it is indeed puzzling from the perspective of other business systems that would simply accept the stakeholder model on its own terms.

It is doubtful if the nature of these problems allows for real theoretical integration of the different views on the business and society relationship (Trevino & Weaver, 1999; Windsor, 2006), nor is there necessarily a need for a single paradigm in the business and society field (cf. Wood, 2000). However, integrative efforts toward a symbiosis of the normative and descriptive approaches to CSR (Weaver & Trevino, 1994) would certainly benefit empirical CSR research. Two research strategies to achieve such a symbiosis have been proposed. The first strategy is to adopt an instrumental view of stakeholder relationships (Freeman, 1999; Jones, 1995; Jones & Wicks, 1999). 1 This approach means that, given a particular normative stance on the role of the firm in society, empirical analysis can focus on the causal links between the goals that follow from this normative stance, the managerial actions that follow from these goals, and the social outcomes that follow from these actions. The second research strategy is to study processes of responsiveness in terms of value attunement (Orlitzky & Swanson, 2002; Swanson, 1999). This approach means that CSR is seen in terms of when, why, how, and how much managers align organizational behavior with broad-based social expectations of responsibility.

We believe that a governance perspective on CSR can further these two research strategies and integrate them. In our view, the particular normative stance that informs the social goals of a firm is the result of value attunement. Value attunement, in turn, is the result of the processes of responsiveness in which firms pragmatically balance competing moral claims and political philosophies. And, these processes of responsiveness are embedded in governance structures and systems. On one hand, governance structures and systems are the result of past value attunement. On the other hand, governance structures and systems both enable and constrain future value attunement. In other words, governance structures and systems institutionalize CSR at the level of firms and society, respectively.

Ackerman (1973) already stated that CSR is not only a matter of the good intentions of managers but that it needs to be institutionalized in business processes and anchored in society. Luoma and Goodstein (1999) argued that if a company’s responsiveness to the social interests of stakeholders is regarded as important and legitimate, one may assume that this view is institutionalized in the firm’s social structures. Likewise, institutional theory suggests that the institutional environment in which a firm operates may have a substantial effect on the nature of processes of responsiveness (Matten & Moon, 2008; Mitnick, 2000; Rowley & Berman, 2000). On these arguments, governance systems and structures present themselves as a focal point for studies of how firms’ roles in society take shape.

A Research Strategy for Studying CSR

We applied a governance perspective on CSR in a retrospective comparative case study of four Dutch banks over a 14-year period, from the beginning of 1990 to the end of 2003. The four firms that were studied are ABN-AMRO, ING Group, Rabobank Group, and Triodos Bank. Together, ABN-AMRO, ING, and Rabobank control approximately 80% of the Dutch banking market. In 2001, these three banks ranked 14th, 25th, and 31st in the world in terms of total assets, respectively. 2 Triodos is a niche player that specializes in investments that make a positive contribution to the social and natural environment and has a share of around 1% of the Dutch market. The central question in the study was how the firms’ roles in society evolved as a result of their interactions with four stakeholder groups: customers, shareholders, employees, and government and regulatory bodies. In keeping with the CSP model, we studied the banks’ principles, processes of responsiveness, and policies and outcomes. In keeping with a governance perspective, we studied process of responsiveness by focusing on changes in the banks’ governance structures and the Dutch governance system.

There are two features of the research design that allow for interesting comparisons among the four banks. The first feature is that the four banks have markedly different governance structures: both ABN-AMRO and ING are publicly quoted firms, but ING initially had strong ties to the government; Rabobank is a cooperative; and Triodos is privately held. This variation allowed us to study the effects of different governance structures on CSR while controlling for differences in the governance system. We focused our study on how interactions with stakeholders were related to changes in stakeholder positions, principles, and policies at each of the four banks. Stakeholder positions were studied in terms of the formal positions of different stakeholder groups in the governance structures of the firms. The principles of the firms were studied as they were reflected in written documents such as the corporate profile, mission statement, and statements of corporate values and corporate identity. The policies and their outcomes were studied as the companies reported them in external and internal documents.

The second feature of the research design is that the starting point of the study is a major change in the Dutch governance system as it applied to the finance industry. In 1990, the Dutch government decided to deregulate this industry. This change enabled Dutch banks and insurance companies to merge and to subsequently become more active on international markets. This internationalization, in turn, exposed the banks to other political philosophies and more widely divergent stakeholder claims than before 1990. The Dutch governance system is stakeholder oriented (cf. de Graaf & Herkströter, 2007; Nooteboom, 1999), but as the banks became more international, they increasingly had to respond to Anglo-Saxon shareholder-oriented views of their role in society. The longitudinal and comparative nature of the research allowed us to study the different responses of the banks to the changes in stakeholder claims that were the result of the deregulation, their subsequent growth strategies, and the internationalization of their industry.

The risk of a case study of four firms over a 14-year period is that an overwhelming amount of data is generated. But, in addition to suggesting the use of formal governance structures as a focusing device for data collection on processes of responsiveness, a governance perspective on CSR offers a second research strategy to avoid data asphyxiation. By assuming that firms are subject to external pressures that lead to institutional isomorphism (DiMaggio & Powell, 1983), it suggests that research can concentrate on critical differences between them. On this assumption, we were able to highlight the nature and effects of relatively complex processes of responsiveness by focusing on differences in the ways in which the principles, policies, and governance structures of the four firms evolved in response to changing stakeholder claims.

Data were gathered over a 2-year period in 2003–2004. Data collection involved both extensive document analysis and a series of interviews. Document analysis involved both public documents (such as annual reports, statutes, and publications of business principles) and internal documents (such as CSR-related discussion papers and policy documents) for all four banks. A total of 49 semistructured interviews was conducted with (former) senior executives and board members of the four banks (14 at ABN-AMRO, 16 at ING, 13 at Rabobank, and 6 at Triodos). The reliability of the data obtained from the interviews was checked by contrasting the data collected in the interviews with an exhaustive analysis of all the articles published on the four banks by the two leading Dutch financial newspapers over the period studied (NRC Handelsblad 1991–2003 and Het Financiële Dagblad 1995–2003). The data collection resulted in case study reports for each bank that were reported back to the firms to check their validity.

Processes of Responsiveness in Dutch Finance

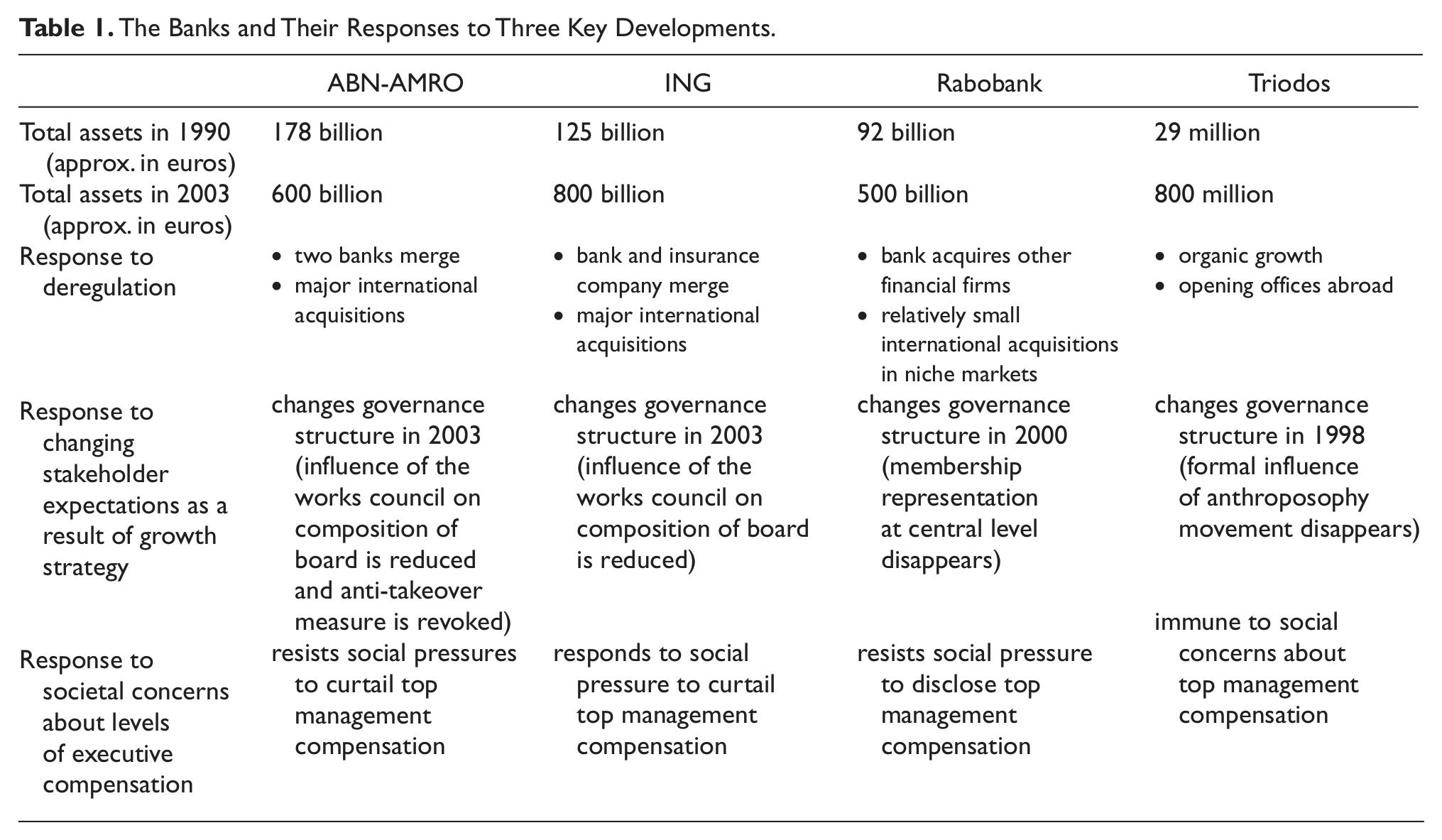

We report the results of our case study in four interrelated steps. We first highlight how the banks responded to the deregulation of their industry in 1990. As will become clear below, they played a proactive role in the process of deregulation and used it to increase the scale of their activities to better position themselves for the expected increase in international competition. We then detail how the four banks responded to the rapid internationalization of their industry and the increasing influence of the Anglo-Saxon shareholder model that resulted from this internationalization. We subsequently report on the banks’ responses to mounting concerns in Dutch society about the effect of Anglo-Saxon governance views on executive compensation that were the result of this internationalization. Table 1 summarizes the banks’ responses to these three developments, which will be detailed below. Last, we provide a short postscript to the case study that highlights the divergent fates of the four banks since 2003, notably in the face of activist shareholders and the credit crisis.

The Banks and Their Responses to Three Key Developments.

Processes of Responsiveness in Relation to Deregulation

Until 1990, a web of implicit and explicit agreements connected the different players in the Dutch financial sector. Banks were tied together by cross-holdings, and the major players met in the Dutch association of bankers where, if needed, any misunderstandings between them could be cleared up. A number of important societal changes in the late 1980s changed the political context in which banks were operating. One of these was that privatization became a government objective. In 1986, the formerly government-owned Postbank was privatized and quoted on the Amsterdam stock exchange, and 3 years later, it merged with NMB, another bank in which the Dutch government had long had a stake. Another important development was that the European Union announced the development of a common market. This announcement led the Dutch bankers, government, and supervisory authorities to develop a more or less coordinated internationalization policy focused on consolidation of the national industry to build strong players for the European market.

ABN bank and AMRO bank were the first to react to these changes in their sociopolitical environment. Although they had not supported the privatization of the Postbank, the subsequent merger between NMB and Postbank did offer them an opportunity. With the Postbank–NMB merger in place, government and regulatory authorities could no longer argue that mergers between large players were not allowed, and merger negotiations between ABN and AMRO were started immediately. Two months later and only just before the intended merger was officially announced in the press, government representatives, regulators, and the works council 3 were informed. This course of action was based on an understanding of the political arena at that moment. Regulatory authorities had already hinted at approval for the deal. In fact, the Ministry of Finance contacted the major political parties to ensure that they would support the necessary regulative change in parliament. Only after the announcement, and already sure of the support of government and regulators, did top management start talks with its main shareholders, among which were its main competitors. Although some had objections, they eventually chose not to oppose the merger.

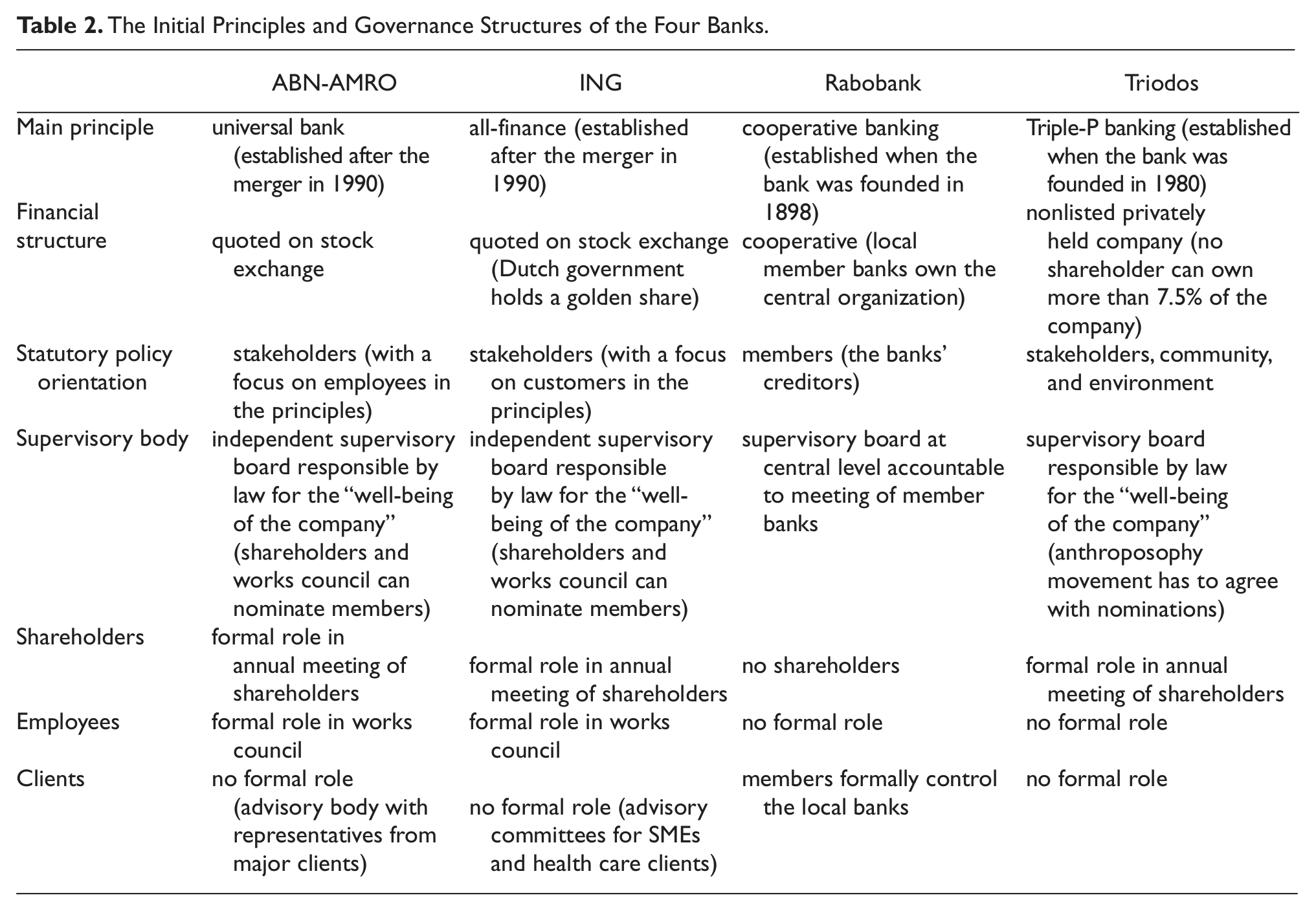

The announcement of the merger between ABN and AMRO triggered a consolidation of the Dutch financial sector. Half a year later, NMB-Postbank and insurer Nationale Nederlanden merged into ING, and the cooperative Rabobank bought insurer Interpolis. This consolidation led to the situation that from 1990 onward, 80% of the Dutch market was controlled by these three firms, with the remainder of the market divided among substantially smaller players. The result of firms’ responses to the deregulation was that the bulk of the market was now divided among three players with markedly different histories, identities, and views of their role in society. Table 2 summarizes the Big Three’s views of their role in society, as well as the views of one of their smaller competitors, Triodos.

The Initial Principles and Governance Structures of the Four Banks.

As Table 2 shows, in 1990, none of the four banks studied had a shareholder orientation. This circumstance was largely the result of the stakeholder orientation that is embedded in the Dutch governance system. In the Dutch two-tiered governance system, the executive board is accountable to a separate supervisory board. The legal responsibility of the supervisory board is to “act in the interest of the company,” which means balancing the interests of different stakeholder groups in a way that furthers the continuity of the company. To be able to do so, the supervisory board is independent: Although both shareholders and the works council can nominate new members to the supervisory board, these members are appointed by cooptation (the sitting members appoint the new members). In this system, consensus is a key characteristic of decision making and members of the board have a shared responsibility for all decisions made.

Although all four banks had a stakeholder orientation, there were nevertheless important differences in their social principles and the way in which these principles are embedded in their respective governance structures. As the product of a merger between two comparable banks, ABN-AMRO became a “universal bank” that combined all the main banking activities: retail banking, wholesale banking, and asset management. The bank was traditionally seen as the leading bank for business in the Netherlands, and its predecessors ABN bank and AMRO bank already had a long tradition of overseas activities. The bank’s statutory orientation was toward stakeholder value, whereas its business identity (published after the 1990 merger) and business values (published in 1998) emphasized the professional competencies of its employees.

As a result of a merger between NMB-Postbank and insurance company Nationale Nederlanden, ING was one of the first large companies in the world to combine banking and insurance activities into an “all-finance” firm. NMB-Postbank, in turn, was the result of a merger between NMB, historically a bank targeted at small businesses that was partially controlled by the government, and Postbank, a formerly government-owned retail bank. As a result of this history, until 1994, the Dutch government owned a “golden share” in the bank that gave it a veto in the supervisory board, which decided about the agenda of the shareholder meetings. After the mergers, the main objective stated by ING was stakeholder value, whereas mission statements and business principles published during the period studied emphasized the importance of customers. Whereas the core values of ABN-AMRO were centered on the professionalism of its employees, ING emphasized cooperation, both among colleagues and with clients.

In contrast to ABN-AMRO and ING, which are both publicly quoted, Rabobank is a cooperative bank with historical roots in rural areas. Rabobank is the market leader in the Dutch retail banking and mortgage markets as well as in the agribusiness market. As a cooperative bank, what distinguishes Rabobank most clearly from its competitors is that it has no shareholders and that its statutory orientation is toward customer value. This orientation is reflected in the rather complex governance structure of the bank. In 1990, Rabobank consisted of 750 local member banks, although by 2003, this number had been reduced to 350 as a result of local mergers. The bank’s customers (more specific, its creditors) governed these local banks. Rabobank’s customers do not have shares but can become members of the foundations that own the local banks. The local member banks, in turn, own the central organization. At the level of the central organization, there was a managing board, responsible for the daily operations, and an executive board representing the members and responsible for setting the firm’s policies. Both boards were accountable to a supervisory board, which was in turn accountable to the yearly meeting of the local banks.

Triodos was founded in 1980 to promote socially responsible and environmentally friendly investments. Its founders were active in the anthroposophical movement. 4 Its statutory orientation is toward “Triple-P” banking, or banking that balances idealistic and commercial objectives. This principle is reflected in the governance structure of the bank. To ensure that the company’s management and shareholders would not lose sight of the social objectives of the bank, its founders forged strong links with the Dutch anthroposophical movement. This movement had to approve of nominations for the supervisory board and executive board. 5 Moreover, Triodos shareholders have limited rights. No shareholder can own more than 7.5% of the company, and independent of the proportion of shares, no party has more than 1% of the vote at shareholder meetings. The amount of dividend that any shareholder could earn was also subject to restrictions.

Processes of Responsiveness in Relation to Internationalization

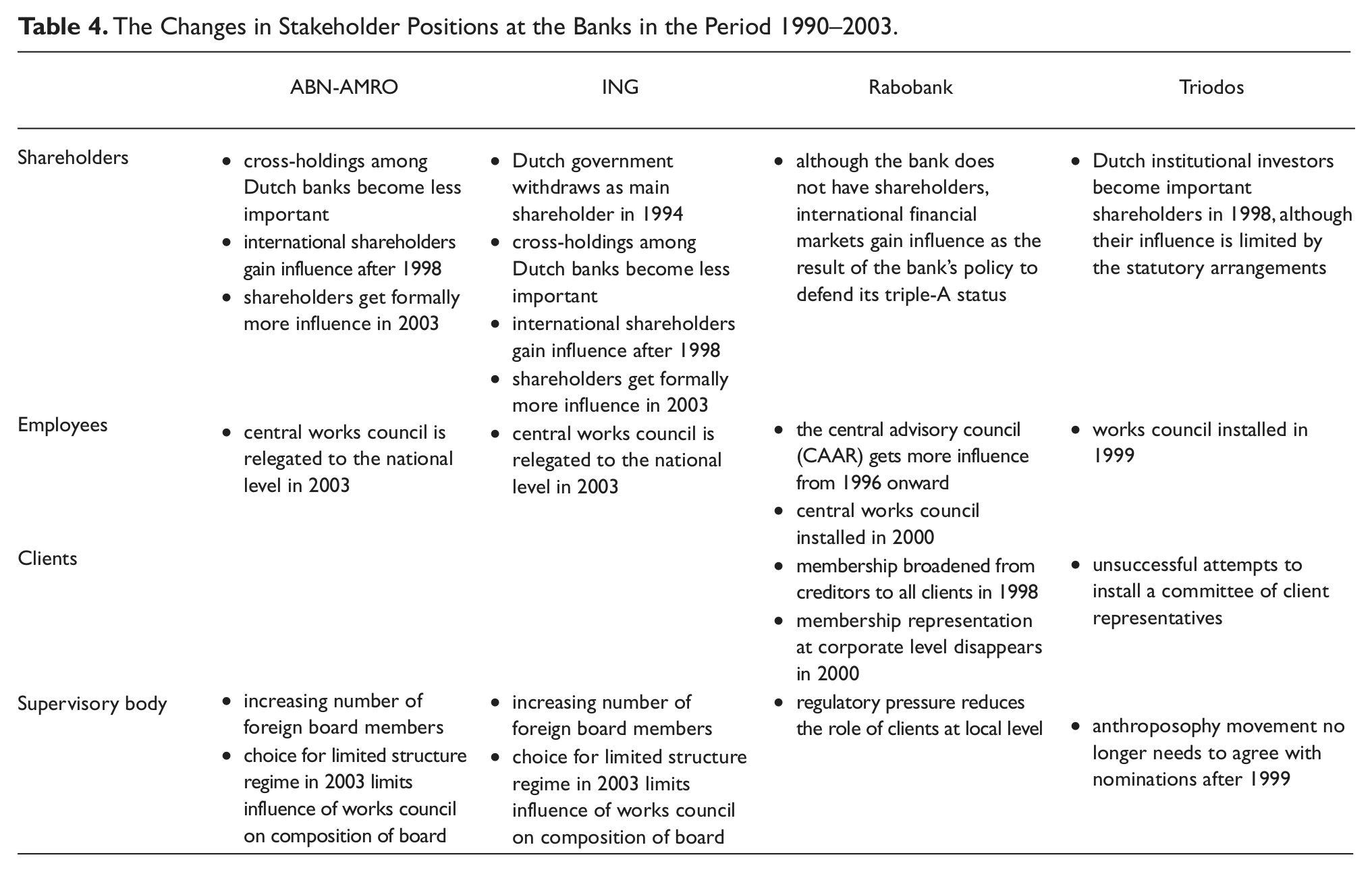

After the consolidation wave in response to the deregulation of the industry, the main focus of the banks was on their international growth strategies. As a result of both the rapid globalization of financial markets and their own growth ambitions, the banks were increasingly exposed to shareholder-oriented views of their role in society, although their different governance structures exposed them in different ways. Changing stakeholder claims put a strain on the banks’ principles, and although three of the four banks upheld their basic principles, all of them responded to changes in stakeholder claims with changes in their governance structure. Tables 3 and 4 summarize their responses.

Major Changes in the Principles and Policies of the Banks in the Period 1990–2003.

The Changes in Stakeholder Positions at the Banks in the Period 1990–2003.

ABN-AMRO and ING

Both ABN-AMRO and ING successfully expanded internationally, and as a result of this expansion, both companies were listed on the New York Stock Exchange in 1998. Listing, in turn, put some pressure on the firms to reconsider their ways of dealing with their stakeholders. The traditional outlook of managers in the Dutch stakeholder model is nicely captured in the following interview quote from a former ING CEO. Commenting on the reactions of the firm’s stakeholders after a year with particularly good results, he said,

All our stakeholders were disappointed. Shareholders had wanted more dividends, employees higher wages, creditors lower interest rates, and retail clients more interest on their savings. Such criticism was a signal that we had done a good job. We would have had a problem if one of the groups had not complained. That would have meant that we had favoured one of the groups over the others.

The internationalization strategy of ABN-AMRO and ING put a strain on such views. As the banks became more dependent on international financial markets, the influence of shareholders steadily increased, not so much through the formal meeting of shareholders but because of the growing importance of meetings with analysts, where the banks typically had to confront the dominant Anglo-Saxon view that the role of firms in society is to increase shareholder value. This confrontation forced the banks to reconsider their role in society. An interesting episode in this regard was ING’s aborted attempt to become a so-called “Banque d’Affaires,” a business model that is common in France and Germany. Banks that are run on this model are active as both major shareholders and creditors of the same company and typically operate in dense social networks with other banks, and sometimes the government, to control critical business decisions and shape industry policy. It is clear that this model is at odds with the preference of international financial markets for transparency and clearly separated roles for shareholders, creditors, and regulators.

As a result of mounting pressures from analysts and activist shareholders, ABN-AMRO substantially raised its profit targets, and ING proclaimed shareholder value as its main goal in the annual report of 2000, only to change this goal back to stakeholder value a year later. Starting in 2000, both companies also accommodated shareholder expectations by giving clear quarterly profit forecasts, not a tradition in Dutch banking and something that especially ING had long opposed. However, by the end of 2003, both banks had abandoned this policy again. The most important outcome of ABN-AMRO’s and ING’s attempts to accommodate the changes in stakeholder demands that resulted from their internationalization was a change in governance structure in 2003.

In the Dutch governance system, an “international company” with more than 50% of its operations outside the Netherlands has a choice between a so-called “full structure regime” and a “limited structure regime.” A limited regime gives shareholders more and the works council fewer rights than a full regime. However, for most of the period studied, both banks voluntarily operated under the full regime. In 2003, the law was changed. Shareholders got more rights, but the full regime also gave the works council the right to nominate one third of the members of the supervisory boards (instead of one or two). Following this change in the governance system, both banks opted out of the full regime on the argument that an increase in the influence of the works council would be difficult to explain to foreign shareholders. Henceforth, the formal influence of the works council at both banks was limited to the national level. In contrast to ING, ABN-AMRO also took another step to accommodate international shareholder claims and abandoned a crucial anti-takeover measure. Until 2003, only certificates of shares handed out by a trustee’s office were publicly traded, so that the trustee could take over power as the holder of the actual shares in the case of a hostile takeover attempt. Under Dutch law, such a measure is allowed when the statutory orientation of the trustee is to protect stakeholder interests. In that sense, even though the bank’s stakeholder orientation was formally upheld, giving up on the protective measure could be interpreted as a de-facto change of its principles. Abandoning this measure would eventually have major consequences.

Rabobank

In comparison with its main Dutch competitors, Rabobank was held back in its attempts to grow internationally by its cooperative structure, which complicated foreign takeovers because the bank could not issue shares. Nevertheless, the company’s growth strategy in response to the deregulation of the industry, the increasing internationalization of the finance industry, and the Dutch governance system also led to tensions with respect to balancing stakeholder claims. Although the cooperative principle of the Rabobank was upheld, the pressures ultimately resulted in changes in the bank’s governance structure that gave managers and employees more, and customers less, influence.

Throughout the period studied, there were discussions about the bank’s cooperative principles initiated by customer representatives at different levels in the organization. Cooperatives had originally been founded with the objective to stimulate economic growth in rural areas by creating opportunities for small business (not unlike current microfinance initiatives). However, after the economic growth that followed the Second World War, this objective had largely lost its relevance. In a society in which the publicly held company was increasingly becoming the standard, there was a strong tendency to become more and more like a “regular” bank. The traditional business model of Rabobank consisted of a strong local presence and low cost. This model had originally allowed the bank to offer better conditions than commercial banks to small business debtors. But, by the time of the period studied, the bank had accepted that it was no longer able to offer debtors more attractive interest rates than noncooperative competitors.

The Dutch governance system was also a source of pressures to become more like a publicly quoted bank. The Dutch Central Bank, for instance, was no longer willing to accept large differences in governance structures between banks and became especially critical of supervision by customer representatives (initially often volunteers). A typical complaint among Rabobank executives was that they were forced into an “ABN-AMRO mold.” As a result, the central Rabobank took over substantial parts of the supervisory role of the customer representatives at the local banks. Similar pressures to conform to the “normal” model of a bank came from the financial markets. Although the bank had no shareholders as such, it earned a quite exceptional triple-A credit rating around 1990, and maintaining this rating was quickly adopted as part of the bank’s principles. Whereas this principle further complicated its international growth strategy (takeovers would typically jeopardize the credit rating), both this growth strategy and maintaining its credit rating meant that the influence of financial markets and their attendant practices increased and compelled Rabobank to become more like a regular bank.

Because Rabobank had originally been a credit cooperative, commercial credit clients were historically central to the bank’s principles and policies. Despite the fact that an intensive internal discussion in 1988 had reconfirmed the bank’s cooperative principles, other customer groups increasingly complained that creditors were the only customer group that was given membership rights. In 1994, another broad-based discussion about the cooperative principles was started. Customer representatives discussed the roots and the future of the cooperative organization in a series of conferences, and new cooperative principles were formulated in a collective effort of the bank’s managers and its customer representatives. It was decided that all clients would be allowed to become members, and customer value became the cornerstone of the new Rabobank principles, a choice of principles that implied criticism of the growing dominance of shareholder value thinking. In the wake of this decision, the company tried to develop specific activities for its members. This approach led to customer relationship projects as well as new products. Members were offered corporate bonds with very attractive interest rates, and on the back of a successful marketing campaign, these new bonds led to a growth from about 500,000 members in 1998 to more than 1.2 million in 2003. However, these new members do not really seem to be active in the cooperative structures of the bank.

When the cooperative structure was finalized in 1998, the debate was still not over. In fact, tensions among the local banks and the central organization, as well as between the various boards, only increased. The managing board—the group’s executives—wanted less influence from the member banks, whereas the executive board—representing the member banks—was concerned that the policies of the managing board would undermine the cooperative character of the bank. In 2000, local bank representatives, the managing board, and the executive board clashed. The executive board and the managing board were fundamentally at odds, and at the same time, the local banks did not feel that either board adequately represented their interests. This crisis resulted in the resignation of the CEO (the title reserved for the chairman of the executive board; the chairman of the managing board had the title of managing director) and a change in the governance structure. The old management board was renamed as executive board and the old executive board formally ceased to exist. This new governance structure gave both the new executive board and the local banks more power. Customers were now only represented at the corporate level by the supervisory board, whereas this supervisory board was, in turn, accountable to the meeting of the local banks. To compensate for the loss of a special board representing the customer interests at the central level, the local banks were given more influence on a number of policy matters. As a result of this change, by 2002, Rabobank was more or less structured like a publicly quoted firm. The main difference that remains is that the local banks, rather than shareholders, own the company and that the member associations that represent customers, in turn, own the local banks.

Lacking a central works council, employees played only a minor role in the discussions of the cooperative principles. In 1996, however, employee representatives organized in the so-called CAAR 6 spoke up and demanded that their interests be taken into account. Their message was that employee value was as important as customer value: Only satisfied employees could satisfy customers. After this signal, business principles were developed in which the role of employees was strongly emphasized. At the same time, there was an interesting tension among various groups of employee representatives. An important internal group was the association of directors, the executives of the local banks. For local executives, the governance structure offered many opportunities to develop their own policies. They were for long opposed to employee representation at the corporate level, because they thought that central employee representation would undermine their local autonomy. In their resistance against employee representation at the corporate level, they found the member representatives of the local banks on their side. But, as more and more local banks started to compete for employees, there was a growing awareness that central policies were in fact necessary. Moreover, with the new governance structure in place in 2002, the cooperative structure could no longer be an excuse for not having a central works council. Because the new structure more closely resembled the structure of a publicly quoted company, the central Rabobank organization was now legally obliged to install a works council.

Triodos

Triodos’s response to the deregulation of the financial industry was a steady growth strategy. This growth called for additional capital, and this infusion resulted in a different mix of shareholders and, ultimately, in a change in the company’s statutes that decreased the influence of the anthroposophical movement and increased the rights of shareholders. Given the growth of the company, the Dutch government system also forced the company to give employees a formal position in its governance structure.

Throughout the period studied, the Triodos’s Triple-P principles united management, clients, employees, and shareholders, and there were ongoing discussions of the social value-added of the projects that were financed. An important part of the bank’s strategy was that it tried to proactively develop new markets with clients and partners. One of the big successes was the bank’s influence on the establishment of a new fiscal regime that made investments in environmental projects and wind energy more attractive. Together with clients and Mees Pierson, a small and somewhat exclusive company specialized in private banking, Triodos also succeeded in developing a market for investing in land for organic farming. And, together with insurance company Delta Lloyd, Triodos developed the first mutual funds in the Netherlands with specific social and environmental objectives. Such new products also meant that the bank developed from a traditional savings and loan bank to a broader based firm.

Employees were strongly attached to the Triple-P principles and heavily involved in the ongoing discussions about these principles, even though they were initially not formally represented in the governance structure. Given its limited size, Triodos was not obliged to install a works council. Instead, the organization established its own particular model of employee participation, which centered on plenary meetings with all personnel. However, due to the subsequent growth of the company, it was legally obliged to establish a works council in 1999. It is interesting that there was initially some resistance to this new institution within the firm. Because of its tradition of informally involving employees, the establishment of a formal institution seemed overdone. Clients had no formal position in the governance structure of Triodos Bank. The bank attempted to start a client committee at least two times, once in the 1980s and once in the 1990s, but not enough clients could be involved. As the bank grew, it became ever more difficult to keep close relationships with clients, and especially after 1995, the company actively invested in events to meet clients.

Especially in its first years of operation in the early 1980s, some important clients had become shareholders because they supported the principles of the bank. The growth of the bank in the 1990s made more capital necessary, and as a result of an emission of shares in 1998, a number of big Dutch institutional investors became shareholders. Although this shift did not lead to significant changes in the principles of the bank, it did lead to a change in the ties with the Dutch anthroposophical movement. A statutory change in 1999 meant that the movement no longer had to approve nominations for the supervisory board and top management positions. Henceforth, the movement was only mentioned as an important inspiration in the preamble of the statutes. Moreover, the statutory change also included lifting the restrictions on the distribution of dividends. After the statutes were changed in 1999, the discussion about the bank’s principles subsided. There seemed to be a growing consensus about how the bank was putting its principles into practice. However, this consensus did not satisfy the executive board, which went on to stimulate discussions about how the bank could maintain a leadership position in social innovation.

Processes of Responsiveness in Relation to Societal Concerns

An important social issue that arose out of the effect of the internationalization of financial markets was a dramatic change in the nature of executive compensation. Even though executive compensation at Dutch banks did not quite rise to the heights that were the norm in Anglo-Saxon firms (a typical quip was that London- or New York-based traders working for the Dutch banks earned more than their CEOs), there were nevertheless mounting concerns in Dutch society about the fairness of remuneration policies in the private sector. Given the traditionally stakeholder-oriented culture of the Dutch business system, the combination of increasing pay dispersion with reduced job security was a particular concern that was strongly voiced in politics and the media. Because of their particular principles and governance structures, the four banks responded to these concerns in quite different ways.

At ABN-AMRO, generous remuneration of employees was an explicit policy. This generous remuneration permeated the company and therefore included payment at the highest levels. When Dutch public opinion began to criticize high levels of top management compensation, the supervisory board of ABN-AMRO resisted public pressure to curtail salaries. At the same time, the company also went through a number of staff reductions that were relatively drastic in the Dutch sociopolitical context. The works council did not oppose these reorganizations, in part because they went hand in hand with excellent outplacement policies. For example, employees were paid for 1½ years after they had left the company if they did not succeed in finding another job.

At ING, the basic terms of employment were largely comparable with those at ABN-AMRO, in part as the result of so-called collective work agreements that apply to the entire industry. 7 But, despite these collective agreements, there were nevertheless differences in the human resource policies of the two companies, and remuneration at ING was less generous than at ABN-AMRO. On the other hand, ING did not reduce its staff when it faced an economic downturn. These differences can be linked to ING’s historical ties to the government and the strong position of labor unions in one of ING’s predecessors, the Postbank. There was more polarization between the works council and management at ING than at ABN-AMRO. The ING works council went to court twice over a conflict with management about work conditions and payment. In contrast to ABN AMRO, in 1998, ING changed its remuneration policies after mounting public criticism on the salaries and bonuses of top management. One of its supervisory board members at the time was a former union leader. In 2002, another former union leader joined the supervisory board: former Prime Minister Wim Kok, who had publicly opposed excessive top management salaries during his last term as prime minister for the social democrat party.

Rabobank was an interesting outlier in terms of the way in which it dealt with the mounting public criticism of top management salaries. Because of its cooperative structure, it was not legally obliged to disclose top management compensation, and it consistently refused to do so on the argument that client representatives were informed about the salaries and that they were free to disclose them to the press if they would feel the need to do so.

In view of its principles, Triodos offered very specific conditions of employment. Because of its initially limited size, during part of the period studied, it could even opt out of the collective work agreements, and new employees had to sign an agreement that they accepted terms of employment that were not in line with the rest of the industry. For the lowest paid personnel, this agreement was typically not a problem, because their pay was actually better than what was laid down in the collective agreements. However, middle managers and the upper echelons were typically paid less than at other banks. The policy was that the best-paid employee could not earn more than five times the lowest salary. The company also rejected a bonus system because, as one manager argued in an interview, “if people are not motivated enough by their basic salary, we are not interested in employing them.” Its remuneration policies obviously made Triodos immune to public criticism on top management compensation. However, whereas the bank remained an outlier in terms of its remuneration policies, during the period studied, the differences with other banks were reduced. By 2003, middle management salaries were comparable with those at other banks, and the fixed relationship between the lowest and highest salary levels was being questioned.

Postscript

Our findings document the sociopolitical nature of the business and society relationship and the important role of governance in shaping firms’ CSR. A short postscript about the fate of the banks after 2003 completes the picture.

In 2007, ABN-AMRO, the bank that had been most responsive to both the deregulation and the pressures from financial markets to give more priority to the interests of shareholders, became the target of activist shareholders and was subsequently taken over by a consortium of three foreign banks. Royal Bank of Scotland (RBS), Banco Santander of Spain, and Fortis of Belgium paid the record sum of 70 billion euros to buy the bank and split its activities among them. Fortis would merge the Dutch retail operations of ABN-AMRO with its own, but at 24 billion euros, it overpaid for its share of the takeover, and as the credit crisis took hold, it subsequently became the target of speculation about its pending bankruptcy. This speculation prompted the Dutch and Belgian governments to nationalize the bank to avert a systems crisis. The Dutch government paid 16.8 billion euros for the Dutch activities of Fortis and ABN-AMRO, leading to the ironic outcome that ABN-AMRO now exists as a free-standing firm again, into which the Dutch banking activities of Fortis will be integrated, instead of the other way around. However, ABN-AMRO is now (temporarily) government owned and much reduced in size because it has lost its international activities to Santander and RBS. ING was not hit as hard by the credit crisis but did receive financial support at the cost of two government-appointed members of the supervisory board and the imposition of constraints on top management compensation. Rabobank was not affected much and gained a lot of customers as the result of the takeover of ABN-AMRO and the subsequent problems at Fortis. Triodos seems not to have been affected at all. Its Web site states, “Triodos Bank has never invested in structured products, or complex financial constructions based on derivatives. Triodos Bank has always considered those products too abstract and too far removed from the real economy and the Triodos Bank’s mission.” 8 In fact, the bank launched an advertising campaign with the motto “my money is doing well” that explicitly links its focus on sustainability to its resilience to the credit crisis.

Discussion

The central message of this article is simple, yet fundamental. If CSR is about finding ways to develop a constructive relationship between business and society, then governance structures and systems present themselves as a natural focal point for CSR research. The case of the four Dutch banks reinforces this message by documenting the central role of both the Dutch governance system and the banks’ different governance structures in shaping their responses to changing stakeholder expectations. We see three ways in which a governance perspective on CSR can contribute to research in the business and society field: first, by offering a research strategy that can inform both descriptive research and normative analysis; second, by suggesting a reorientation of the CSP model from a conceptual framework to organize research topics to a causal model that can inform empirical research; and third, by furthering theory development in stakeholder theory. Each of these is discussed in turn.

A Governance Perspective as Research Strategy

Our case study illustrates the potential of a governance perspective as a strategy to focus empirical CSR research. Although calls for in-depth research of processes of responsiveness have been made (Griffin, 2000; Margolis & Walsh, 2003; Rowley & Berman, 2000), the longitudinal and interactive nature of these processes makes them difficult to study. In fact, commenting on the CSP model, Wood (1991) remarked that the “third part of the . . . model, social outcomes, is the only portion that is actually observable and open to assessment” (p. 711). In contrast to Wood, our case study illustrates that a governance perspective makes it possible to also assess principles and processes of responsiveness. Our claim is not that we were able to fully assess everything that is relevant about the CSR of the four banks. However, the formal mechanisms of their governance structures did allow us to go beyond the measurement of outcomes and observe “CSR in action.” This observation leads to the proposition that CSR can be understood as an evolving configuration of principles, processes of responsiveness, governance structures, and policy outcomes.

A governance perspective also offers help in dealing with the dilemma of integrating descriptive, normative, and instrumental views of CSR. Consider the following descriptive questions formulated by Wood (2000): What is the nature of the firm? What is the structure of the firm’s relationship with stakeholders and the larger environment? What is the nature of the business institution? What mechanisms of change exist and are used; how do they work? These questions all point to governance systems and structures and how they organize stakeholder interactions. At the same time, how stakeholder interactions are organized is also both a normative and an instrumental issue. On one hand, governance structures and systems enable the basic instrumental goals of firms, such as access to markets, to employees, to capital, and to regulatory approval. On the other hand, they are deeply intertwined with normative views of firms’ roles in society.

The case of the four Dutch banks corroborates the central role of governance in both an instrumental and a normative view of how firms’ roles in society take shape. On an instrumental view, the main conclusion from the case is that although the banks upheld their principles, they all accommodated changes in stakeholders’ claims by changing their governance structure. Their respective governance structures thus emerge as pragmatic solutions to dealing with competing stakeholder claims. Moreover, considering the banks’ CSR in terms of a configuration of principles, processes, governance structures, and policy outcomes facilitates more specific instrumental analysis. For instance, given the fact that ABN-AMRO formally upheld its stakeholder principle, we must conclude that it did not meet its social responsibility. The Dutch governance system defines the continuity of the organization as the central goal of a stakeholder orientation. In view of this goal, the takeover of ABN-AMRO and the subsequent loss of 8,000 jobs as its activities were divided among its competitors are an obvious failure. The direct cause of this failure was the change in the bank’s governance structure in 2003, when it abandoned a crucial anti-takeover measure. Of course, on a shareholder view of the role of the firm in society, an assessment of ABN-AMRO’s CSR leads to a very different conclusion. Abandoning the anti-takeover measure then emerges as a salutary decision that allowed for the creation of shareholder value by reallocating resources to more profitable activities.

The example of ABN-AMRO shows that instrumental considerations naturally lead to normative questions. On a normative view, the main conclusion of the case is that governance structures and systems are the major battleground for competing claims on firms’ roles in society. The case vividly illustrates the inherently sociopolitical nature of CSR (cf. Matten & Moon, 2008; Mitnick, 2000; Windsor, 2006). This nature is clear not just from the struggle of ABN-AMRO and ING to reconcile their stakeholder orientation with the shareholder-oriented expectations of international financial markets but also from the developments at Rabobank and Triodos. Although the principles of these two banks are more explicitly oriented toward social goals than at ABN-AMRO and ING, the net result of the changes in their governance structures was that the influence of their social constituents (clients in the case of Rabobank, and the anthroposophical movement in the case of Triodos) was reduced in favor of more managerial discretion.

In short, we believe that our study shows that a governance perspective can contribute to the understanding of CSR. In fact, when the governance dimension of CSR is overlooked, it is easy to lose sight of the essential fact that CSR is a contested phenomenon. Different sociopolitical constellations and histories may lead to the institutionalization of very different conceptions of firms’ roles in society, both at the level of individual firms and entire business systems. When the values-in-use of a particular governance system are taken for granted, say the principle-agent logic that dominates the U.S. business system (Quinn & Jones, 1995), potentially viable alternatives to organizing the relationship between business and society are easily overlooked (cf. Matten & Moon, 2008).

Reorienting the CSP Model

Our study leads us to propose a reorientation of the CSP model that is visualized in Figure 1. The purpose of this reorientation is threefold. First, the model reflects the central role of governance systems and structures in shaping firms’ roles in society. General principles of CSR become institutionalized in the governance system (relating to what Wood referred to as institutional principles), whereas more specific principles are institutionalized in the governance structures of individual firms (relating to what Wood referred to as organizational principles). Managers have discretionary powers to shape policies according to their own values within the constraints of the governance structure and system (relating to what Wood referred to as individual principles). Although we agree with Wood’s conception of CSP as a configuration of elements, we see the firm’s governance structure as a central element of this configuration, alongside its principles, processes of responsiveness, and policies and outcomes.

A Reorientation of the Corporate Social Performance (CSP) Model.

This conceptualization also clarifies the nature of the relationship between three different aspects of responsibility, on one hand, and responsiveness, on the other. First, there are the values that are institutionalized in the governance system, where the basic responsibilities of firms are defined in terms of legal obligations. Second, there are the principles of a company that reflect its identity. It is in adopting specific principles that a company can be seen to take responsibility for certain things (Bovens, 1998). These responsibilities may or may not go beyond its legal obligations. Mitnick (2000) referred to this aspect of CSP as commitment. Third, there are the policies of a company that reflect how it acts on its responsibility. It is for the observable outcomes of its policies that a company can be held accountable (Bovens, 1998). Mitnick (2000) referred to this aspect of CSP as revelation. Stakeholders have recourse to the formal mechanisms of the governance structure and the governance system to redress policy outcomes that go against their interest. Fourth, there are the processes of responsiveness by which a company responds to social demands. It is in these processes that value attunement (Orlitzky & Swanson, 2002; Swanson, 1999) between firms and stakeholders takes place. This value attunement is where what Mitnick (2000) referred to as the beliefs aspect of CSP plays out. Value attunement, in turn, is both enabled and constrained by the governance system and governance structure. The governance system puts constraints on the governance structure of a firm, which in turn constrains managerial discretion to shape firms’ policies on the basis of the particular values-in-use of firms’ managers.

Second, the model is meant to locate stakeholder theory, which has arguably become the main inspiration for theory development on CSR, squarely within the CSP model. Processes of responsiveness are seen as two-way interactions between firms and their stakeholders in which the social control of business (Jones, 1983) meets firms’ attempts to manage stakeholders and social issues (Wood, 1991). These processes are embedded in the obligations that governance systems impose on both firms and their stakeholders, on one hand, and enabled and constrained by firms’ governance structures, on the other hand.

Third, whereas the model retains the major components of Wood’s (1991) model (viz., principles, processes of responsiveness, and policies and outcomes), it organizes these components in a way that is primarily meant to inform empirical research. Whereas the original purpose of the CSP model was to integrate conceptual advances in CSR research in a framework that would allow “scholars to ‘locate’ works within a broad model of business-society relationships” (p. 691), the purpose of the reoriented model is to more directly inform descriptive research on how firms’ roles in society take shape. In other words, the model may serve as a template to study the causal relations that lead to the evolution of the configuration of principles, governance structures, and processes of responsiveness that shape a firm’s policy outcomes.

Theory Development

Our proposal to reorient the CSP model toward a specification of causal relationships that can guide empirical research follows earlier suggestions along these lines (e.g., Mitnick, 2000; Swanson, 1995; Windsor, 2001). Although there is a price to pay for such reorientations in terms of giving up on the model’s ability to integrate relevant research streams in the business and society field, an important advantage is that a focus on causal relationships can better inform theory development. This advantage can be illustrated by deriving some tentative propositions about the role of governance in CSR on the basis of our case study and the reoriented CSP model.

At the most general level, the main proposition of a governance perspective on CSR is that governance systems and structures affect firms’ CSR. Somewhat more specific, governance systems and structures interact with firms’ principles, processes of responsiveness, and policy outcomes to determine their role in society. As the case of the four Dutch banks illustrates, different governance structures go hand in hand with very different configurations of principles and policies. A yet more specific proposition is that governance structures mediate the effect of institutional pressures and managerial values on CSR. Institutional pressures take the form of “top-down” legal obligations that the firm must meet. 9 Within the constraints of these obligations, there is “bottom-up” managerial discretion to shape a firm’s CSR. The case of the four Dutch banks documents the important additional role that a firm’s governance structure plays in shaping its CSR. Although all four banks were subject to the stakeholder-oriented Dutch governance system, their different governance structures played a central role in explaining how managers could shape the particular policies of their firms.

As stakeholder interactions have a central place in the reoriented model, it is also worthwhile to briefly consider how a governance perspective can further some promising strands of stakeholder theory. For instance, in relation to stakeholder salience theory (Mitchell et al., 1997), a governance perspective suggests that governance systems and structures are causally related to stakeholder salience because they affect the power and legitimacy of stakeholder claims. Managers’ perceptions of stakeholder salience are likely to change as a result of a legal obligation to have monthly consultations with the works council or having governments as shareholders or a supervisory board with members who were appointed by social organizations.

In relation to stakeholder culture theory (Jones et al., 2007), a governance perspective suggests the proposition that governance systems are causally related to stakeholder cultures but that this relationship is moderated by governance structures. The stakeholder-oriented nature of the Dutch governance system had an obvious effect on the stakeholder cultures of the four banks, which could all initially be classified as “broadly moral,” but this effect was mediated by their respective governance structures. Triodos’s stakeholder culture was most clearly “altruist,” whereas the change of governance structure at ABN-AMRO in 2003 seems to have resulted in a change from a “moralist” to an “instrumentalist” culture. 10 A related proposition that is of particular interest for instrumental stakeholder theory (Jones, 1995) is suggested by the postscript to our study that documents the different fates of the banks in the face of activist shareholders and the credit crisis. This proposition is that moralist stakeholder cultures that are institutionalized in governance structures result in more resilient firms than shareholder cultures.

Whereas theories of stakeholder salience and stakeholder culture focus on the managerial side of the business and society relationship, theories of stakeholder action (Rowley & Berman, 2000) and stakeholder influence strategies (Frooman, 1999) focus on the stakeholder side of the relationship, or the social control of business (Jones, 1983). By focusing on the formal roles that stakeholders have in governance structures, on one hand, and on the formal mechanisms that governance systems offer stakeholders to influence firms, on the other hand, a governance perspective can also enrich these theoretical perspectives. Both the likelihood and nature of stakeholder action will depend on these roles and mechanisms. A case in point is the actions of Rabobank employees to demand recognition for their interests in the discussions about the bank’s cooperative principles. Coming at a time when Rabobank was not yet legally obliged to install a central works council, these actions suggest that the likelihood of stakeholder actions may increase when their interests are not formally represented in a firm’s governance structure.

Conclusion

The crux of our argument for a governance perspective on CSR is that governance structures and systems institutionalize the outcomes of value attunement. We do not claim that CSR is only about governance, but we do believe that governance systems and structures are the natural focal point for understanding how the relationship between business and society is shaped. Governance structures and systems are the pragmatic solutions of firms and societies to balance the interests of different stakeholder groups. They are the result of past sociopolitical construction of the relationship between business and society and enable and constrain processes of responsiveness to changes in stakeholder expectations. On this view, a governance perspective offers a fruitful research strategy for CSR scholarship. The formal mechanisms that structure the interactions between stakeholder groups present themselves as a logical starting point for descriptive studies of CSR. Moreover, they facilitate comparative and instrumental studies by allowing researchers to focus on the effects of critical differences between governance systems and structures on pertinent social outcomes. And, by focusing normative inquiry on the different ways in which governance systems and structures balance stakeholder interests, a governance perspective is also a natural starting point for ethical reflection.

Footnotes

Authors’ Note

The authors are grateful for detailed comments on previous versions of this article by Ans Kolk, Jonatan Pinkse, Donna Wood, the editor and three anonymous reviewers, and participants at an accounting seminar of Aarhus Business School. They thank Cor Herkströter and the Corporate Responsibility Foundation for both financial and nonfinancial support.