Abstract

This study examines the effects of culture, gender, and function on orientation toward corporate social responsibility (CSR) among 416 employees of an international financial service organization. The main objective of the study is to investigate the variation of corporate social responsibility orientation (CSRO) across national cultures. The authors draw on a theory of cultural value orientations to identify three culturally distinct transnational clusters: West Europe, the English speaking countries, and South Asia. These clusters coincide with the business units (BUs) and markets of the organization under investigation. By employing a framework of CSRO, the study reveals substantial differences across clusters within one single internationally operating organization. The English-speaking and the South Asia clusters were found to be most concerned with legal regulations and economic performance. In contrast, the West Europe continental cluster was found to be more concerned about business conforming to ethical norms than achieving high levels of economic performance or conforming to legal regulations. Furthermore, the study reveals gender differences in CSRO and differences among random employees and employees who are professionally active in the area of CSR. This article concludes by discussing implications of these findings for internationally operating organizations in the light of the recent global financial crisis.

Keywords

Multinational enterprises (MNEs) constantly encounter divergent pressures from global and local stakeholders. The management of these pressures is one of the major challenges concerning corporate social responsibility (CSR) activities that MNEs are facing in global business (Galbreath, 2006; Muller, 2006; Sachs, Rühli, & Mittnacht, 2005). CSR can be defined as meeting “the economic, legal, ethical, and discretionary expectations that society has of organizations at a given point in time” (Carroll, 1979, p. 500). Conflicting pressures and expectations from various stakeholders can lead to serious dilemmas. Such dilemmas, involving not only CSR but also politics and even corruption (Rodriguez, Siegel, Hillman, & Eden, 2006), reflect the absence of a simple right or wrong in international business. Policy that may be commonplace and legal in one country may be illegal in another, and business practices that are considered normal in one country may be considered unethical in another (Matten & Moon, 2008; Vitell & Paolillo, 2004). Cultural differences exist in international business. Different national cultures exhibit different value systems (e.g., Chokar, Brodbeck, & House, 2007; Hofstede, 1984, 2001; House, Hanges, Javidan, Dorfman, & Gupta, 2004; Schwartz, 1999, 2006). MNEs have to take into account these differences to conduct business successfully within diverse cultural environments (e.g., Matten & Moon, 2008; Sachs et al., 2005).

Differences in cultural value systems also affect orientation toward CSR (e.g., Burton, Farh, & Hegarty, 2000; Pinkston & Carroll, 1994; Scholtens & Dam, 2007; Shafer, Fukukawa, & Lee, 2007; Vitell & Paolillo, 2004). As Matten and Moon (2008) state, the perception of what is corporate responsibility or irresponsibility is deeply embedded in a nation’s institutional context. MNEs have discretion regarding the CSR activities they choose to conduct. A culturally absolutist approach in CSR assumes that value systems, and, by extension, orientation toward CSR (Burton et al., 2000), will be similar across cultures. MNEs following an absolutist approach transpose their CSR policy to all the countries in which they operate. A culturally relativistic approach in CSR, in contrast, implies adaptation of the CSR policy to the value orientation of the respective countries in which they operate. Gardiner, Rubbens, and Bonfiglioli (2003), however, state that CSR will only make a visible difference if the concept is fully integrated into corporate practice. Global CSR then reflects an MNE’s obligation to conduct worldwide business in a way that preserves the welfare of the people, both in the home country and the host country, while simultaneously pursuing its own interests (Donaldson & Dunfee, 1999; Hillman & Keim, 2001; Luo, 2006). As Mohan (2006) posits, global CSR management thus involves a cross-border transfer and implementation of the headquarters’ CSR practices to its different subsidiary units (more or less assuming cultural absolutism) as well as the management of local CSR practices suited to the local context of the subsidiary units (reflecting cultural relativism). By ignoring differences and uncritically adopting widely promoted American and (West) European CSR policies and practices, MNEs risk failure in pursuing and achieving the goals of their CSR activities (Galbreath, 2006; Matten & Moon, 2008; Sachs et al., 2005; Weaver, 2001). Hence, it is of great importance for MNEs to have a profound understanding of the differences and similarities in orientations of stakeholders toward CSR among countries and cultural environments.

Over the last decades, researchers in the business and international management literature have discussed and explored the concept of CSR (cf. Egri & Ralston, 2008). Most studies seem to support the contention that adequate CSR policy is essential for MNEs to be successful. However, there is relatively little empirical insight into the consequences of differences in cultural value orientations toward CSR for MNEs. Matten and Moon (2008) argued that “little attention has been dedicated to the question regarding how and why CSR differs among national settings” (p. 406). In addition, Egri and Ralston (2008) concluded that “there is an urgent need to widen the geographic and cultural scope of international management research on corporate responsibility” (p. 325). Moreover, except for some notable exceptions discussed later, even less is known about cross-cultural differences in stakeholder orientation toward CSR. This orientation is typically called corporate social responsibility orientation (CSRO: Aupperle, 1984).

The main objective of this article, therefore, is to advance the understanding of international, cross-cultural CSR policy in general and cross-cultural CSRO in specific. The authors combine two predominant theoretical conceptualizations, namely, Carroll’s (1979, 1991a) framework of CSR and Schwartz’s (1999, 2006) theory of cultural value orientations. First, by reviewing the literature, the authors discuss CSR and the importance of cultural awareness regarding CSRO in internationally operating organizations. Then, the authors draw on Schwartz’s theory of cultural value orientations to identify three culturally distinct transnational clusters. The authors argue that cultural value orientations held by an MNE’s stakeholders influence orientations toward CSR relevant to the successful conduct of business of the MNE. This study focuses on one specific stakeholder group, namely, an MNE’s employees. By drawing on results from a quantitative survey, the article examines orientation toward CSR across clusters within one single MNE. Moreover, the authors explore the significance of gender and functional area with regard to CSRO. The authors continue by discussing implications of the results of this study for internationally operating organizations in the light of the recent global financial crisis. The article concludes by discussing limitations and suggesting directions for future research.

CSR

Over the last decades, research on CSR has undergone continuous development and the concept of CSR contains a great proliferation of theories, definitions, approaches, and terminologies (e.g., Carroll, 1979, 1991a, 1991b, 1999; Garriga & Melé, 2004; Lee, 2008; Moir, 2001; Sahlin-Andersson, 2006; Wood, 1991). An accepted conceptualization of CSR is the framework developed by Carroll (1979, 1991a, 1991b). He depicted the complexity of a broadly interpreted corporate responsibility by positing four basic components (Carroll, 1979, 1991a): (a) economic responsibilities (producing goods and services that society wants, being profitable), (b) legal responsibilities (operating under the laws and regulations of society, playing by the rules), (c) ethical responsibilities (conforming to the expectations of society over and above legal requirements, doing what is right, just, and fair), and (d) discretionary responsibilities (contributing to society and improving the quality of life, being a good corporate citizen).

Carroll (1979) assumed there was a clear and consistent order of priority among the four components. According to this four-component definition of CSR, the responsibilities were expected to have approximate relative weightings of 4:3:2:1 for economic, legal, ethical, and discretionary responsibilities, respectively. This weighting implies that the economic, legal, and ethical components are seen to be, respectively, four times, three times, and twice as important as the discretionary component. Several researchers have sought to provide empirical evidence of the weightings in the CSR dimensions proposed by Carroll (e.g., Aupperle, Carroll, & Hatfield, 1985; Pinkston & Carroll, 1994). The framework is unique in that it recognizes that economic responsibilities do not come totally at the expense of other types of social responsibility (Pinkston & Carroll, 1996; Wood, 1991). According to Carroll (1979, 1991a), a socially responsible firm thus fulfils its economic, legal, ethical, and discretionary responsibilities by earning a profit, obeying the law, acting within the prevailing industry and societal norms, and using its resources to promote the overall welfare of society.

Carroll’s (1979) original pyramid framework received a number of criticisms and several alternative views of CSR have been offered (Lee, 2008; Wood, 1991). Notwithstanding these admonitions, substantial research continued to be conducted based on Carroll’s framework (Schwartz & Carroll, 2003) and numerous researchers have used the framework for empirical studies (e.g., Angelidis & Ibrahim, 2004; Burton et al., 2000; Burton & Goldsby, 2009; Gössling & Vocht, 2007; Ibrahim, Angelidis, & Howard, 2006; Ibrahim, Howard, & Angelidis, 2003, 2008; Maignan & Ferrell, 2000, 2001, 2003, 2004; Maignan & Ralston, 2002). Such use suggests that Carroll’s four CSR components and framework remain a leading paradigm of CSR. In addition, the wide range of empirical research based on this conceptualization allows for a comparison between the results of different studies on the basis of Carroll’s typology.

CSRO

As organizations have discretion regarding the domain in which they choose to operate, basic value orientations toward the responsibilities distinguished by Carroll become significant in international business. Aupperle (1984) labeled these orientations as CSRO. He saw the comprehensive quality of the Carroll framework and its definition of CSR as particularly conducive to the construction of a research instrument. The work of Aupperle (Aupperle, 1984; Aupperle et al., 1985) has culminated in the development of an instrument designed to assess individual CSRO, measuring individual orientation toward the relative importance of the economic and noneconomic components of CSR. Results from studies using Aupperle’s instrument lend it credibility. As Burton et al. (2000) state, because CSR encompasses the total of all types of responsibilities firms have to society, it makes sense to discuss an individual’s relative weighting to the types of responsibility. Different individuals will thus use different relative weightings and, in addition, different societies may promote different relative weightings and therefore influence individual’s actions. Research has been conducted using the Aupperle instrument to explain differences in the CSRO of individuals. Findings have been reported as to the effects of various factors influencing CSRO including degree of religiousness (Angelidis & Ibrahim, 2004; Ibrahim et al., 2008), gender (Burton & Hegarty, 1999; Ibrahim & Angelidis, 1994), practitioners versus students (Ibrahim et al., 2006, 2008), corporate and individual influences (Marz, Powers, & Queisser, 2003), business students versus nonbusiness students (McDonald & Scott, 1997), managerial values (Ibrahim et al., 2003; Sharfman, Pinkston, & Sigerstad, 2000), and organizational attractiveness (Smith, Wokutch, Harrington, & Dennis, 2004).

Culture

Research on CSR has burgeoned over the last decades. Although a multitude of related studies has been reported in the business and international management literature, the significance of culture, and especially cross-culture, with regard to CSR remains somewhat unexplored (Egri & Ralston, 2008). Nevertheless, there are some studies that remind us to anticipate variance in orientation toward CSR across cultures. Several researchers examined the significance of culture in the communication of CSR by organizations (e.g., Chapple & Moon, 2005; Hartman, Rubin, & Dhanda, 2007; Maignan & Ralston, 2002). Others explored cross-cultural value orientations with regard to the existence and perceived importance of business ethics (e.g., Scholtens & Dam, 2007; Shafer et al., 2007; Vitell & Paolillo, 2004), leadership decision making (e.g., Waldman et al., 2006), and the adoption of codes of conduct in MNEs (e.g., Bondy, Matten, & Moon, 2004; Van Nimwegen, Soeters, & Van Luijk, 2004). Few researchers addressed perceived corporate citizenship across cultures (e.g., Maignan & Ferrell, 2000, 2003). Although different theories and frameworks of CSR have been employed, virtually all of these studies support the significance of international, cross-cultural differences in CSR. With respect specifically to Carroll’s (1979) framework and cultural differences, Crane and Matten (2007) argued that “whilst the four levels of responsibility are still largely valid in a European context, they take on different nuances, and may be accorded different significance” (p. 52). Whereas Crane and Matten point at differences in CSR between countries within Europe, others indicated differences between Europe and other regions. Maignan and Ferrell (2003), for instance, suggested that in France and Germany, legal and ethical responsibilities are believed to be more important than in the United States. The importance placed on conforming to social norms in the former countries contradicts the prominence of economic responsibilities, that is, economic performance, in the United States. It has also been proposed that in developing countries, the order of priorities may be different. Visser (2008) argued that in these countries, philanthropic responsibilities are assumed to have the second highest priority after economic responsibilities, but preceding the legal and ethical responsibilities. The prominent place of philanthropic responsibilities is related to indigenous traditions and a general reliance on donor assistance.

Although aforementioned studies provide valuable insights on the significance of culture with regard to CSR, they are not examinations of orientation toward CSR. Only very few studies have explicitly attempted to explore CSRO across cultures. Pinkston and Carroll (1994) examined whether CSRO would be different for international corporations. They investigated a sample of US-based multinational chemical subsidiaries using a sample of 131 managers at the headquarters level of firms and/or the plant managers of the subsidiaries, of which 49 were US firms and 82 were non-US firms. Managers perceived the four components in different relative priorities across countries of origin, but these orientations were not significantly different from one country to another. The foreign affiliates were found to have orientations that were quite similar to the domestic respondents in the US chemical market. Burton et al. (2000) examined CSRO among a sample of 322 US and Hong Kong business students and found some differences in the components of responsibilities considered most important. Respondents from both countries viewed CSR as a construct in much the same way, although Hong Kong students gave economic responsibilities more weight and the total of the noneconomic responsibilities less weight than did the US students.

Both studies focused on comparing cultural differences between a small number of countries (seven in Pinkston & Carroll, 1994 and two in Burton et al., 2000) and relied either on data provided by respondents representing different multinational organizations that were all US based or on student samples. These approaches must be qualified not to be appropriate to ascertain global culture- and institution-related differences in CSRO. This study therefore attempts to reveal cross-cultural differences in CSRO by investigating a substantial number of employees originating from a number of different countries, working within a single MNE.

Gender

Besides the influence of culture on CSRO in MNEs, gender also is assumed to affect orientation toward CSR. Gender differences in moral orientation are prevalent in the literature since the seminal work of Kohlberg (1981) and the assertion of Gilligan (1982) that moral reasoning of women and men is different, with women emphasizing care and men emphasizing justice. Research indicates that moral orientations of men and women do not differ very much (e.g., Jaffee & Hyde, 2000). However, business and organizational contexts have an impact on moral behavior. Although a variety of studies on gender difference in ethical orientation have been reported in the literature, the explanation of behavioral differences is rather underdeveloped. Gender differences in orientation toward CSR have been examined only rarely. Previous research (Ibrahim & Angelidis, 1994; Smith et al., 2004) has demonstrated that men tend to allocate more emphasis on economic responsibilities, whereas women regard discretionary responsibilities as more important. Burton and Hegarty (1999) showed that men saw economic responsibilities as relatively more important and ethical responsibilities as relatively less important than did women. Also, McDonald and Scott (1997) revealed that women endorsed ethical responsibilities more strongly than men. Concluding, these studies suggest the existence of differences in CSRO due to gender. MNEs may, besides taking into account differences in value orientations due to culture, also need to pay attention to diverging value orientations due to gender in their CSR and diversity strategies.

Function

Finally, differences in CSRO are believed to exist in MNEs across different professional functional areas. Sharfman et al. (2000) indicated the existence of a relationship between values of managers and their orientations toward CSR. McDonald and Scott (1997) explored differences in CSRO across business students and nonbusiness students. They demonstrated that business students had a stronger economic orientation, whereas nonbusiness students endorsed ethical and discretionary responsibilities more strongly. The MNE under investigation in this study is a financial service organization and therefore also consists of different professional functional areas. Accordingly, differences within one single organization may exist due to differences in the respective functional area of its employees. Similarities of CSRO dependent on the respective function of an employee are related to the phenomenon of isomorphism, referring to “the constraining process that forces one unit in a population to resemble other units that face the same set of environmental conditions” (DiMaggio & Powell, 1983, p. 149). Matten and Moon (2008), pursuing DiMaggio and Powell (1983), distinguish three sources of institutional isomorphism, of which normative isomorphism may serve as an explanation for the distinction between random employees and CSR professionals. Normative isomorphism assumes that units within a population adopt organizational structures and practices which are considered legitimate and socially acceptable by other units in their field and recognizes how individuals of a similar calling organize in a professional organization to promote a cognitive base, diffuse shared orientations and organizational practices, and legitimize their activities (DiMaggio & Powell, 1983). Normative isomorphism is associated with professionalization. As DiMaggio and Powell acknowledge, professionalization creates a pool of almost interchangeable individuals who occupy similar positions across the organization and possess a similarity of orientation. Functional area–related differences in orientation toward CSR are thus likely to exist within one single organization.

Cultural Value Orientations

Managing CSR becomes more complex in culturally different contexts representing different cultural value orientations. Different cultures have different value systems. This condition implies that the discrete values, or the ranking of the values, may be different across cultures (Chokar et al., 2007; Hofstede, 1984, 2001; House et al., 2004; Schwartz, 1999, 2006). What is important to one culture may be less important to another culture, and what is normal in one country may be unethical in another. Cultural value orientations have been identified in the literature through a number of multination studies, whereby the value patterns have been plotted on cultural dimensions. Geert Hofstede pioneered and elaborated the study of various national cultures to ascertain how cultures could be described in several dimensions. The seminal work of Hofstede (1984) has provided a basis for many subsequent studies, although reviewers have noted limitations on its validity (e.g., Smith, Peterson, & Schwartz, 2002). Consequently, Schwartz (1999, 2006), using data from 73 different countries, proposed another theory of cultural value orientations. (the theory has become known as the Schwartz Value Survey [SVS]). Value orientations are defined as concepts or beliefs about desirable end states or behaviors. These concepts or beliefs transcend specific situations, guide selection or evaluation of behaviors and events, and are ordered by importance in relation to one another to form a system of values (Schwartz, 1992). The framework provided by Schwartz, viewing cultural dimensions as forming an integrated, nonorthogonal system, differs from Hofstede’s (1984, 2001) conceptualization which views dimensions as independent and orthogonal factors.

Schwartz (1999, 2006) distinguished seven types of cultural value orientations comprising three polar cultural value dimensions: (a) embeddedness versus autonomy, (b) hierarchy versus egalitarianism, and (c) mastery versus harmony. Embedded cultures stress the importance of social relationships and identification with the larger group. Individuals are viewed as embedded in the collectivity. Autonomous cultures, on the contrary, emphasize the advisability of individuals to pursue their own ideas, directions, and experiences. Hierarchy cultures rely on hierarchical systems and accentuate the importance of social power and wealth, whereas egalitarian cultures emphasize equality, social justice, and responsibility. Mastery cultures stress the importance of ambition, success, competence, and entrepreneurship to master and direct the natural and social environment. Harmony cultures, in contrast, emphasize the importance of harmoniously fitting into the environment instead of changing or exploiting it. These cultural dimensions contribute uniquely to the explanation of important social phenomena. Schwartz suggested that the harmony/mastery dimension may be especially distinctive, adding a unique element to the understanding of attitudes toward unselfishness and competition. Taking the above into account, there is thorough reason to expect that CSRO of individuals differs across cultures. This cultural theory can therefore provide MNEs with insight into the differences and similarities in value patterns between the cultures in which they operate and subsequently explain possible differences in the CSRO of their employees.

Both theoretical arguments and empirical analyses suggest the existence of culturally distinct world regions (e.g., Hofstede, 2001; Huntington, 1993; Inglehart, 1997; Inglehart & Baker, 2000; Ronen & Shenkar, 1985). Schwartz (2006) employed coplot multidimensional scaling techniques to identify transnational cultural groupings of 76 distinct national cultures. He mapped distances between cultures on each of the seven value orientations. Unlike other classifications (e.g., Inglehart, 1997) of national cultures into world regions that map cultural groupings on two orthogonal variables, that is, dimensions, Schwartz’ computation maps cultures on seven variables, that is, cultural value orientations, simultaneously. As Goldreich and Raveh (1993) explain, this method of multivariate analysis is an integration of mapping concepts and a variant of regression analysis that enables the simultaneous exploration of observations and variables for a set of data.

On the basis of the seven cultural value orientations, Schwartz (2006) mapped and discerned seven transnational cultural groupings: (a) continental West Europe (emphasis on autonomy, egalitarianism, and harmony, low on hierarchy and embeddedness), (b) English-speaking countries (high on autonomy and mastery, especially the United States, average on hierarchy and egalitarianism), (c) South Asia (high on hierarchy and embeddedness and low on autonomy and egalitarianism), (d) East Europe (emphasizing harmony, low on mastery), (e) Confucian (emphasis on hierarchy and mastery, rejection of egalitarianism and harmony), (f) Africa and the Middle East (high on embeddedness, low on autonomy), and (g) Latin America (close to worldwide average on all dimensions). The clusters discerned by Schwartz show striking parallels with the zones Huntington (1993) suggested and those Hofstede (2001) and Inglehart and Baker (2000) found.

Schwartz and Ros (1995) and Schwartz and Bardi (1997) provided initial theoretical explanations for the existence of these transnational clusters. The clusters reflect some geographical proximity. Accordingly, some of the cultural similarity within the clusters is doubtless due to diffusion of values, norms, practices, and institutions across national borders (Naroll, 1973). Furthermore, shared histories, language, religion, level of development, and other factors also play a part. Nevertheless, and as also acknowledged by Schwartz (2006), the frame of comparison is of importance here. The culture of a cluster may look different when viewed in a worldwide perspective than when inferred from narrower perspectives. In the light of cross-cultural CSR, this assertion is supported by arguments of Crane and Matten (2007) and Chapple and Moon (2005). Crane and Matten argued the existence of CSR-related differences between countries within Europe, and Chapple and Moon found some differences in CSR between countries in Asia. Notwithstanding these admonitions, and following the empirical evidence on distinct world regions (Hofstede, 2001; Inglehart & Baker, 2000; Ronen & Shenkar, 1985) in general, and on those discerned by Schwartz (2006) in specific, the authors argue the seven transnational clusters to be highly relevant as a frame for analysis of cultural differences within a single MNE. Namely, the geographical dispersion of the MNE under investigation that is reflected in the locations of its regional business units (BUs) closely resembles Schwartz’s transnational cultural groupings.

Method

The main objective of this study is thus to ascertain whether differences in cultural value orientations between transnational clusters affect the orientation toward CSR within a single MNE. In addition, an attempt is made to broaden the scope with regard to influences of employees’ gender and function on their CSRO. ABN AMRO, a prominent international bank originating from the Netherlands, served as the MNE for this study. During the study, ABN AMRO ranked eighth in Europe and 13th in the world based on total assets. It had more than 4,500 branches in 56 countries, a staff of more than 105,000 full-time equivalents, and total assets of EUR 987 billion (ABN AMRO, 2007a). Important to notice here is that during the period of data collection, ABN AMRO was under heavy fire from several hedge funds demanding a breakup or sale of the business and two rival groups of banks aiming for a hostile takeover. Today, after an intervention of the Dutch government, the bank has become independent again, although its operational scale has been reduced considerably. These developments, however, had a substantial influence on the research project and will be discussed in some more detail later in this article. Moreover, they shed light on the findings of the study.

During the research project, the bank’s regional BUs were located in Europe, North America, Latin America, and Asia. The banks’ home markets involved the Netherlands, the United States, and Brazil, while BUs Europe and Asia were successfully exploiting opportunities that were opening up in several emerging markets. BU Europe was expanding to the Eastern part of Europe, whereas BU Asia was focusing specifically on Greater China (encompassing the People’s Republic of China, Hong Kong, and Taiwan), India, Pakistan, Singapore, and Indonesia. As a major financial service organization, present in many countries, ABN AMRO constantly faced complex global and local pressures with regard to CSR. The bank, however, considered that through its role in allocating capital to businesses and individuals, and through its unique insight into many sectors and companies, it had both the responsibility and the opportunity to promote CSR in all countries where it operated (ABN AMRO, 2007b). ABN AMRO’s CSR strategy therefore aimed at being both locally, that is, culturally relativistic, and globally, that is, fully integrated, valid and applicable. However, local cultural values and stakeholder pressures across its home and emerging markets were often found to be very different, sometimes resulting in dilemmas with the absence of a simple right or wrong (see ABN AMRO, 2007b). The bank therefore wanted to have more information on the differences and similarities in orientations toward CSR among countries and approved the research project.

A worldwide online survey was used for data collection. The potential population of the research project comprised all ABN AMRO employees worldwide (105,000 employees). An online questionnaire was sent to two independent samples: one random sample, containing 4,020 employees divided over 18 countries, and one expert sample, encompassing 134 employees employed in different countries and professionally active in the area of CSR. The latter sample was selected to compare CSRO for random employees and the bank’s CSR professionals. The research project had full support from the head of the CSR department that supervised the study. Questionnaires were accompanied by a cover letter explaining the objective of the study and informing participants that they would receive the results of the study. The cover letter was signed by the principal researcher and the respective CSR department head. Participants were ensured that their individual responses were treated strictly confidential and anonymous to minimize socially desirable reporting. The countries were spread all over the world to make the international research project indeed a global one. This single case approach, that is, studying one MNE’s subsidiaries all over the globe, is assumed to represent the best way to demonstrate differences in cultural value orientations because it homogenizes all other factors such as technology, educational level of employees as well as organizational structure and strategy (d’Iribarne, 1989; Hofstede, 1984, 2001). Comparable research designs have often been applied in cross-cultural organizational research, irrespective of their quantitative or qualitative character.

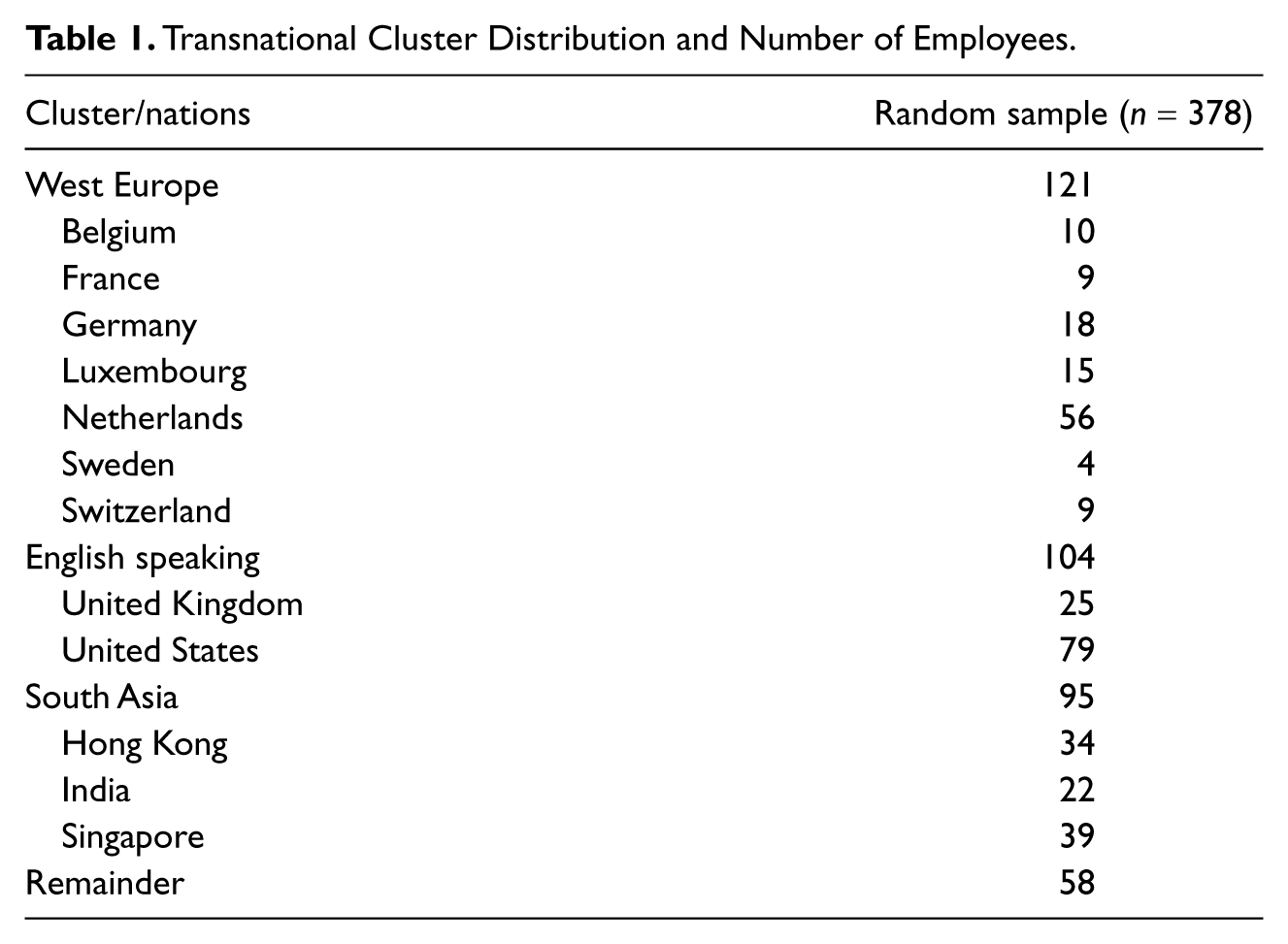

The first electronic mailing and the follow-up mailing generated 378 (9.4%) usable responses from the random sample and 38 (28.4%) usable responses from the expert sample. Fifty-three other responses of the random sample and one of the expert sample were unusable because of their incompleteness. Eighteen respondents indicated that they did not wish to participate in the survey. There was a final sample size of 416, with an overall response rate of 10.0%. The response rate is considerably lower than in comparable studies conducted at ABN AMRO (i.e., De Gilder, Schuyt, & Breedijk, 2005; Van Nimwegen et al., 2004). The lower response rate was expected, given developments during the research project mentioned previously, leading to a high degree of uncertainty resulting in a lessening of organizational commitment within the bank. However, the size of the random sample was sufficient to produce reliable research findings at the level of three transnational clusters: Western Europe (n = 121), the English-speaking (i.e., Anglo-Saxon) countries (n = 104), and South Asia (n = 95). The clusters East Europe and Latin America yielded too little response and were therefore left out of consideration in the cluster comparison. Table 1 summarizes the distribution of respondents.

Transnational Cluster Distribution and Number of Employees.

The questionnaire included the revised Aupperle survey, consisting of 44 statements measuring CSRO. The Aupperle (1984) instrument operationalizes Carroll’s (1979) typology of social responsibility, addressing individual value orientations toward the relative importance of the four components of CSR. Eleven sets contained four statements each, each of which corresponds to one of Carroll’s four responsibilities. An example of such a set of statements is shown in the appendix, as well as the operationalization of the four scales. Aupperle’s instrument uses a forced-choice methodology to minimize the social desirability of responses. Respondents were asked to allocate 10 points to each of the 11 sets of statements measuring CSR. They had to respond constantly to a slightly varying situation referring to CSR; each set thus sought the same basic information. Aupperle’s instrument is an example of an ipsative scale in which the level of importance given to each type of responsibility is measured not in absolute terms but relative to the levels of importance given to the other types of responsibilities. In an ipsative scale, respondents compare options and give importance to the more desirable or preferred ones. The ipsative or forced-choice methodology minimizes response bias including socially desirable reporting (Carroll, 1991b). The psychometric properties of the Aupperle instrument have been thoroughly examined and the questionnaire has been tested for its content validity and reliability and has proven to be reliable in the past (e.g., Angelidis & Ibrahim, 2004; Aupperle et al., 1985; Burton et al., 2000; Burton & Hegarty, 1999; Marz et al., 2003). Using the Aupperle instrument also enabled the authors to compare their results with prior studies using this instrument.

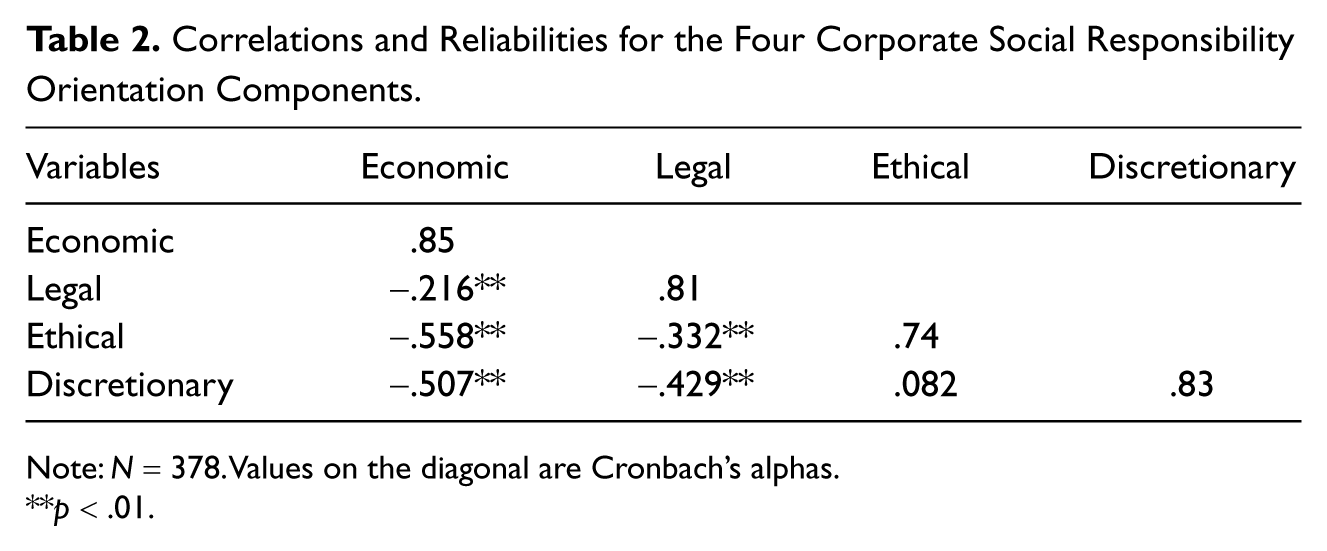

To identify the structure underlying the responses and to measure equivalence across transnational clusters, a two-stage procedure was employed. First, responses to the instrument were subjected to exploratory factor analysis using principal components analysis with varimax rotation. Results of the factor analysis confirmed the framework described by Aupperle (1984). Then, similarity of factor structures across transnational clusters was evaluated in a target rotation procedure. As Van de Vijver and Leung (1997) suggest, this procedure is recommended to establish structural equivalence across groupings in cross-cultural research. After the target rotation, factorial agreement was evaluated using Tucker’s (1951) phi. Tucker’s phi values ranged between 0.94 and 0.98, thereby providing a strong indication of factorial similarity (Van de Vijver & Leung, 1997) across the transnational clusters. The reliability of the instrument was tested using Cronbach’s (1951) alpha. Cronbach’s alphas calculated for each of the four components are depicted in Table 2. These coefficients are consistent with those reported by other researchers (e.g., Angelidis & Ibrahim, 2004; Aupperle et al., 1985; McDonald & Scott, 1997) and judged adequate (Nunnally, 1978). To measure for consistent reliability across the transnational clusters, separate Cronbach’s alphas were calculated for each of the clusters. All coefficients ranged between 0.70 and 0.87, ensuring consistent reliability across the clusters. The above analyses justified comparing CSRO across the three transnational clusters.

Correlations and Reliabilities for the Four Corporate Social Responsibility Orientation Components.

Note: N = 378. Values on the diagonal are Cronbach’s alphas.

*p < .01.

Results

Table 2 depicts the reliabilities and correlations among the four CSRO components. A significant negative correlation was found between the economic component and the other three components. The strongest correlations (r = -.558 and r = -.507) were between the economic component and the ethical and discretionary component respectively.

Further analysis of the results was conducted in two stages, both at the level of transnational clusters. As each of the four components of CSRO were correlated with at least one other type in the total sample, first a multivariate analysis of variance (MANOVA) was conducted to test whether there were significant overall differences between the transnational clusters. As previous research indicated gender differences in CSRO, the authors controlled for gender. The results indicated differences between the transnational clusters, with F = 3.071, p = .006; Wilks’s Λ = .944 and partial η2 = .028. That is, the clusters exhibited different CSROs and separate orientations thus could be examined for differences across the clusters. Then, to detect differences in orientations across transnational clusters, four one-way analyses of variance (ANOVAs) were conducted. Post hoc tests were conducted to locate the differences. As the analysis incorporated three clusters, Fisher’s (1971) least significant difference (LSD) technique was used as post hoc comparison method. As Maxwell and Delaney (2004) suggest, this method for data analysis is recommended in the specific case of three groups.

Three of the four components showed significant differences between the clusters. More specifically, the univariate analyses showed significant differences between the clusters with respect to the legal, ethical, and discretionary components (see Table 3). Compared with West Europe, the English-speaking cluster exhibited significantly greater emphasis on the legal component of CSRO. Furthermore, the results demonstrated that the English-speaking cluster and the South Asia cluster have a weaker orientation toward the ethical component compared with the West Europe cluster and that the English-speaking cluster has less concern about the discretionary component than the West Europe cluster. As Aupperle’s CSRO instrument used a forced-choice format, the means for the four components reflect the relative degree of importance placed on each component by the respondents.

Analysis of Variance Results for Transnational Cluster Corporate Social Responsibility Orientation.

Note: Figures in parentheses are standard deviations. Figures in square brackets are relative rankings.

Economic Responsibilities

No significant differences between the clusters were observed with respect to the economic component. However, both the English-speaking cluster and South Asia ranked the four responsibilities in order of importance as legal, economic, ethical, and discretionary, respectively, whereas West Europe ranked the economic responsibility third after the ethical and legal responsibilities. This difference would be expected based on cultural value orientations. Affective autonomy and mastery in the English-speaking cluster point to an orientation that encourages an assertive, pragmatic, entrepreneurial, and even exploitative orientation to the social and natural environment. Mastery and hierarchy, in the English-speaking and South Asia cluster respectively, justify the differential distribution of resources to which competition is directed, whereas their opposing poles, egalitarianism and harmony (as emphasized in West Europe), call for cooperative regulation of interdependence between multiple stakeholders such as government, trade unions, corporate associations, shareholders, and employees (Crane & Matten, 2007). Employees in the English-speaking cluster and South Asia are thus more likely to view competition as good and economic performance as most important as they live in countries with cultures that emphasize mastery and individualism, and hierarchy in the Asian context. People in the English-speaking cluster are expected to strive mainly for their own prosperity and well-being by achieving high economic performance while simultaneously paying attention to legal issues.

Legal Responsibilities

Compared with West Europe, the English-speaking cluster exhibits significantly greater concern about the legal component of CSRO. This greater concern may result from the legalist and “explicit” nature of doing business in liberal market economies such as the ones in the United States and the United Kingdom. As literature suggests (Burton et al., 2000; Matten & Moon, 2008; Vogel, 1992), the United States and the United Kingdom display more legalistic perspectives on business ethics, where the British emphasis on law coexists with a tradition that stresses duties more than rights. Thus, it would be expected that the English-speaking cluster would weight legal responsibilities higher than the other clusters, and the results confirm this assumption.

Ethical Responsibilities

West Europe demonstrates a stronger orientation toward the ethical component than the English-speaking cluster and South Asia. This stronger orientation would be expected based on the egalitarian cultural value orientation of West Europe, calling for social justice, responsible behavior, and honesty (Schwartz, 2006). This emphasis is in contrast with the South Asia cluster emphasizing hierarchy, calling for wealth and social power. Burton et al. (2000) support this assumption suggesting the emphasis on materialism and pragmatism in South Asia, leading to less importance of ethical responsibilities and more importance of economic responsibilities. Regarding the English-speaking cluster, affective autonomy and mastery suggest an entrepreneurial orientation to the social environment, implying a relative smaller priority for ethical responsibilities. Besides the above explanations, prior research (Brammer, Pavelin, & Porter, 2006; Sharfman, Shaft, & Tihanyi, 2004) suggests that CSR has received by far the greatest level of attention in the developed world and particularly in Western Europe. This greater attention might also explain the high exhibition toward ethical responsibilities in the West Europe cluster.

Discretionary Responsibilities

The English-speaking cluster showed relatively less concern about the discretionary component than did the West Europe cluster. This finding emphasizes the lesser importance allocated to responsibilities toward society in the English-speaking cluster. An explanation could be found when looking at the cultural value orientations emphasized in West Europe. Intellectual autonomy and egalitarianism both entail a cultural view of individuals as independent actors with rights and responsibilities to express these interests through discretionary or philanthropic actions. Furthermore, harmony calls for selfless concern for the welfare of others fitting into the natural and social world rather than striving to change it through assertive action. This assumption is supported by the findings of Ester, Halman, and Seuren (1993) characterizing West Europe as a region of democratic welfare states where concern for the environment is especially high. In contrast, affective autonomy and mastery in the English-speaking cluster encourage an entrepreneurial and even exploitative orientation to the social and natural environment. Such value orientations would not prioritize discretionary or philanthropic actions.

Netherlands

As ABN AMRO has its roots in the Netherlands, the West Europe cluster was dominated by Dutch respondents (n = 56). Additional analyses, distinguishing the Netherlands from the rest of the West Europe continental cluster, revealed no significant differences on the four components of CSR. However, the Dutch were found to rank the ethical responsibility as the most important, whereas the rest of the West Europe continental cluster ranked the ethical component of CSR only as second. The significant differences across clusters with respect to the legal and the discretionary components hold when excluding the Netherlands from the West Europe cluster. The difference on the ethical component, however, became nonsignificant when excluding the Netherlands. This effect indicates the relative importance placed on ethical responsibilities exhibited by the Dutch compared with the rest of continental West Europe, but especially with the rest of the world. Implications of these findings will be discussed in some more detail later in this article.

Gender

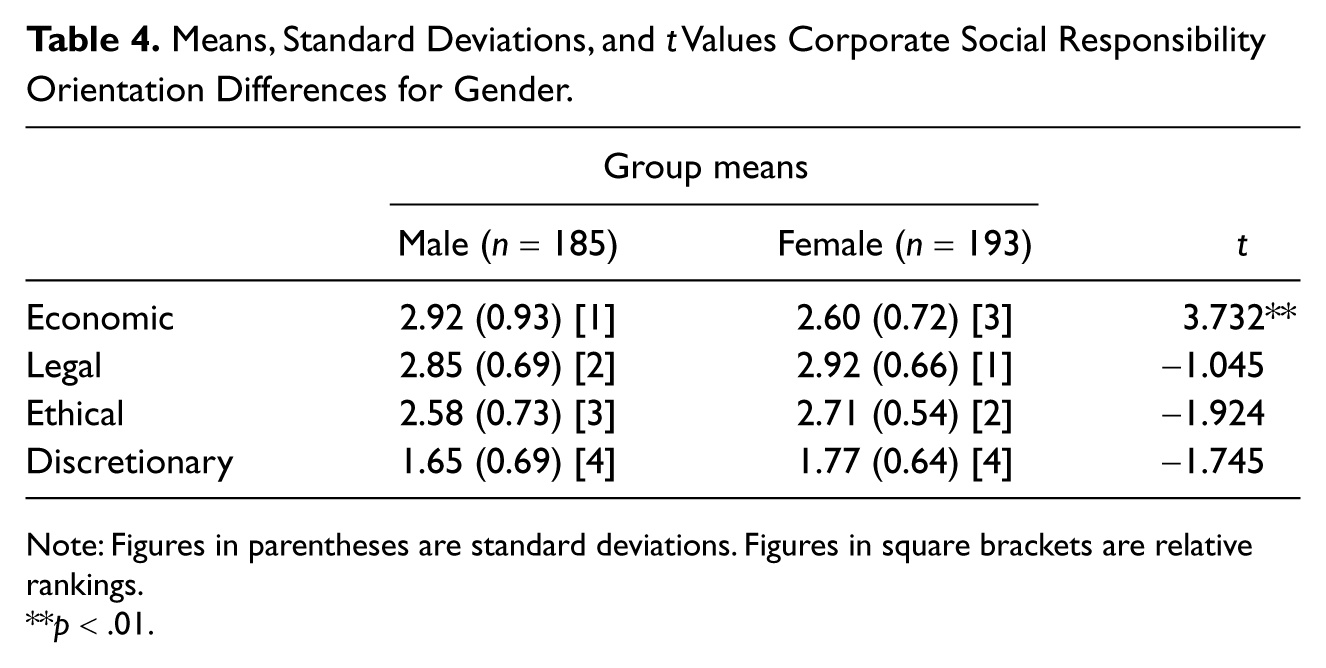

Besides the differences in CSRO due to cultural differences, the authors also tried to broaden the scope regarding the discussion on gender differences in CSRO. To determine if the orientations in CSRO were significantly different for the other independent variables, again a two-stage analysis was conducted. First, a MANOVA indicated that there were differences in responses between men and women, with F = 4.689, p = .003; Wilks’s Λ = .964; and partial η2 = .036. Subsequently, four independent samples t tests were conducted to compare the CSROs for men and women (see Table 4).

Means, Standard Deviations, and t Values Corporate Social Responsibility Orientation Differences for Gender.

Note: Figures in parentheses are standard deviations. Figures in square brackets are relative rankings.

*p < .01.

The orientations of men and women appeared to be significantly different from each other for the economic component. Moreover, men ranked the four responsibilities in order of importance as economic, legal, ethical, and discretionary, respectively, whereas women ranked the economic responsibility only third after legal and ethical responsibilities. The results of the current study thus provided support for gender differences with respect to the four components of CSR and seem to indicate a difference in views of economic, ethical, and discretionary responsibilities, with men being more economically driven than women and women exhibiting more legally aware and caring attitudes than men. These findings confirm the results of prior research (Burton & Hegarty, 1999; Ibrahim & Angelidis, 1994; McDonald & Scott, 1997; Smith et al., 2004). However, this study expands previous results by providing support for the existence of gender differences in CSRO across different cultures.

Function

Finally, the authors investigated possible differences in CSRO due to the professional functional area of employees. More specifically, this study explored potential differences among random employees and CSR professionals. MANOVA indicated differences in responses between random employees and CSR experts, with F = 4,934, p = .002; Wilks’s Λ = .965; and partial η2 = .035 The four independent samples t tests revealed significant differences in both the legal and the ethical component. As can be seen in Table 5, employees from the random sample were found to deem legal responsibilities significantly more important than the CSR experts, whereas those experts considered ethical responsibilities more important. This difference in CSRO could be explained by what DiMaggio and Powell (1983) labeled institutional isomorphism (see also Matten & Moon, 2008). Apparently, isomorphism is at stake in the case of employees within ABN AMRO who are professionally active in the area of CSR, exerting normative isomorphism through the elaboration of professional networks that span the organization on a global scale and facilitate the rapid diffusion of CSR-specific knowledge and practices.

Means, Standard Deviations, and t Values Corporate Social Responsibility Orientation Differences for Functional Area.

Note: Figures in parentheses are standard deviations. Figures in square brackets are relative rankings.

p < .05.

The actual findings are in accordance with what would be expected, considering the ambitions of the CSR professional group demonstrating the importance of ethical responsibilities. Interesting to see however is the lower orientation of the CSR group toward the discretionary component. Random employees weighted this component as more important than CSR professionals did. This difference might be explained by the fact that CSR professionals are more knowledgeable of the arena of CSR and are more aware of the fact that the commitment of organizations to visible and popular activities such as volunteer programs, donor assistance, and sponsorships (the discretionary component) is not necessarily positively correlated with CSR and that organizations also have to pay attention to their economic, legal, and ethical responsibilities.

Conclusions and Discussion

Consistent with extant business and international management literature, the results of this study have shown that MNEs, like ABN AMRO, have to take into account differences in cultural value orientations within the international networks of their organizations. Employees across the globe will potentially act different in specific CSR or ethics-related dilemmas. This study showed significant differences in CSRO across cultures within one single internationally operating organization. The CSRO of employees reflects an important element of their value perspectives and may predict actual business behavior, as employees who are confronted with social dilemmas are guided by internal values.

Furthermore, the results imply that meeting ethical and discretionary demands does not come at the expense of economic performance levels or legal limitations. By combining their economic, legal, ethical, and discretionary responsibilities, organizations may be best able to address the different pressures assigned to them by their employees as well as by other stakeholders worldwide. The results also point at potential difficulties that MNEs may encounter when trying to be good corporate citizens, especially in continental West Europe, where the achievement of high levels of economic performance could actually be perceived negatively. Organizations may therefore sometimes even have to undervalue their economic achievements and emphasize primary and foremost their preparedness to exhibit ethical and discretionary aspects of CSR toward their stakeholders.

Overall, the findings of this study indicate potential tensions concerning the implementation of a uniform global CSR strategy across national and cultural borders. MNEs need to investigate carefully the country markets or regions in which they operate as those locations are likely to reflect different expectations of stakeholders toward CSR. This consideration is especially important when transposing the CSR strategy and activities from the home-country headquarters of the MNE to its host-country subsidiaries.

As mentioned previously, some major developments took place at ABN AMRO during the research project. Due to a chronically underperforming share price of ABN AMRO, several Anglo-Saxon hedge funds demanded a breakup or sale of the business and ordered the bank to halt its own strategic plans. As a result, Barclays, another prominent European bank originating from the United Kingdom, made a tentative merger approach to ABN AMRO, offering a deal that could help the bank see off break-up demands from the hedge fund investors.

Recognizing the existence of a multitude of other possible interpretations, the authors argue that the recent acquisitions in the financial service sector, as well as the exceptional allowances and bonuses, are substantially influenced by differences in cultural value orientations with regard to CSR. Moreover, looking at these developments, a question about possible side effects of CSR could be posed. The Netherlands, home country of ABN AMRO, can be characterized by its caring, ethically responsible attitude (e.g., Zahn, 1989) and its emphasis on “consultation, consensus, and compromise” (Van Iterson, 2000). Dutch people generally have a great social consciousness, emphasize collective responsibility, and expect from industry a responsible behavior. The acquisition approaches, however, were initiated by hedge funds and banks originating from the English-speaking cluster. Here, institutions emphasize exactly the opposite, namely, individual responsibility and entrepreneurial behavior, justifying a differential distribution of resources to which competition is directed. The approaches from the Anglo-Saxon organizations underline that employees from the English-speaking cluster value competition as good and see economic performance as most important. This economic orientation is reflected in flexible allowances and bonuses that may have exceptional dimensions, at least in the eyes of the Dutch. This difference in orientations is discussed in a recent Dutch newspaper article (Klok & Van Uffelen, 2009), drawing on the acquisition of Barings, a former UK based investment bank, by ING, another bank originating from the Netherlands a decade ago. The enormous exit allowances that the British arranged for themselves were considered unethical by the Dutch. As Vitell and Paolillo (2004) stated, business practices that are perceived normal in one country may be perceived unethical in another. However, and as acknowledged by Matten and Moon (2008), the perception of what is corporate irresponsibility is deeply embedded in a nation’s institutional context.

In another newspaper article (Obbema & Zonderop 2008), Robert Reich, former US Secretary of Labor, noticed the trend that Dutch companies are more committed to CSR than enterprises in the United States. In his work on “supercapitalism,” Reich (2007) also suggests that companies that exhibit a higher concern for the social and natural environment, and that spend more money on social responsible activities, are likely to eventually lose market share and risk hostile takeover attempts by hedge funds or competitors.

Although much has been written on the necessity of ethical and discretionary responsibilities, considering the approaches of the Anglo-Saxon hedge funds and financial institutions, the authors could pose a question about the side effects of being socially responsible. That question is whether CSR-oriented organizations (such as Dutch organizations) will survive in the long term in the whirlpool of supercapitalism (Reich, 2007) and hypercompetition (D’Aveni, 1994), strongly emphasizing shareholder satisfaction. This whirlpool consists of companies from countries that position the ethical and discretionary component of CSR only as subordinate to legal, but particularly to economic responsibilities.

Limitations

Having discussed the findings of this study and their implications, several limitations need to be mentioned. Data for this research project were collected within international subsidiaries of a multinational bank originating from the Netherlands. This focus might have led to a bias, given the assumption that a strong corporate culture superposes the national culture of the local respondents. However, even though there is a tendency toward ethnocentrism within the Netherlands, Dutch multinational corporations appear to be rather multiculturally oriented (Scheepers, Felling, & Peters, 1989). This orientation holds also for ABN AMRO which emphasizes the importance of diversity of the workforce.

A second limitation concerns the language of the questionnaire. The instrument was given in English to all employees. Therefore, some problems in understanding may have arisen, as some respondents were able to complete the questionnaire in their native language while others needed to complete it in a nonnative language. This language issue may have caused a bias, lessening the validity of the results.

The study was conducted among employees of one financial sector MNE only. Arguments could be made for both single-case approaches and multiple-case approaches in demonstrating cultural differences. Employing a multiple-case study involving multiple organizations or MNEs provides increased generalizability but puts the research at risk of uncontrolled organization and sector differences affecting the results. By conducting a single-case study at one single MNE, some generalizability is lost, but this approach reduces the risk of uncontrolled organization and sector effects. A single-case study homogenizes organization effects such as technology, educational level of employees as well as organizational structure and strategy and therefore allows for cross-cultural comparison. Nevertheless, future research could address this limitation by relying on research designs incorporating multiple organizations from different sectors.

In addition, the nature of the stakeholder group under investigation might need some further consideration. The data gathered measuring CSRO relied solely on the information provided by employees. However, employees are not the only ones who can impose pressures and responsibilities on organizations, and their orientations may not be representative of other stakeholders. Other groups of stakeholders may have a differentiated orientation toward CSR. It would certainly be beneficial to focus on shareholders, customers, and public stakeholders in further research.

Using Carroll’s (1979) framework for measuring CSRO in this study represents another limitation. The results of the study report employees’ orientations toward CSR based on four predefined responsibilities. When surveyed about CSRO in an unaided approach, respondents may reveal different responsibilities. Future research could overcome this limitation by the use of qualitative methods.

A final limitation concerns the countries used to explore differences in CSRO. Although the sample selected in the current study was geographically dispersed and cultural differences were highlighted, only three clusters consisting of different countries were included in the analysis. To make the findings more meaningful, additional clusters or countries should be considered. Furthermore, although the classification in clusters is based on a respected framework (Schwartz, 2006), it can be assumed that there exist within-cluster variations and cultural differences between the different countries. This assumption finds support by the additional analysis excluding the Netherlands from the West Europe continental cluster. The culture of a cluster may look different when viewed in a worldwide perspective than when inferred from narrower comparisons (Chapple & Moon, 2005; Crane & Matten, 2007; Schwartz, 2006).

Future Directions

Acknowledging the limitations mentioned above, some future directions can be identified. Further research on the differences in CSRO across cultures should be undertaken, incorporating various populations in different countries, as mentioned in the previous section. Another interesting topic of future research would be a link between the Aupperle (1984) instrument for measuring the CSRO of individuals and the SVS for operationalizing the value priorities of individuals.

Furthermore, it would be highly interesting to repeat this research project with the same clusters or a comparable cross-cultural project in about a decade. The current study indicated a difference in relative priorities than Carroll’s (1979) proposed 4:3:2:1 weighting for economic, legal, ethical, and discretionary responsibilities, respectively (see Table 3). A movement can be seen toward a lessening of economic aspects of CSR and an increase in legal, ethical, and discretionary responsibilities. In addition, the variance between the components seems to be lessening, revealing a leveling of economic, legal, and ethical responsibilities. People may no longer believe in an explicit trade-off between being profitable and meeting legal, ethical, and discretionary responsibilities. Instead, at least according to the stakeholder group of employees of the organization under investigation, MNEs may be best able to address the different social and natural pressures of their environments by combining their economic, legal, and ethical responsibilities followed by discretionary activities. Indeed, CSRO may be changed in response to society’s changing expectations. These findings seem to be congruent with Carroll’s (1991a) enhanced framework, suggesting that all four responsibilities always have existed to some extent, but that, in recent years, the ethical and discretionary components have taken a more significant place, pointing at certain isomorphic tendencies in CSRO occurring presumably across the globe (Matten & Moon, 2008). Although a potential explanation of this trend may pertain to the specific MNE or financial service sector under investigation, a future reexamination might find evidence for this trend.

Footnotes

Appendix

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.