Abstract

This article analyzes the process of organizing collective action by studying the role of the organizational platform provided by the United Nations–backed Principles for Responsible Investment (PRI) initiative in supporting institutional investors’ collaborative engagement with corporations on environmental, social, and governance issues. The authors combine stakeholder and collective action theory to explain how institutional investors influence corporations through collective engagement. A unique access to data from the PRI secretariat on two cases of collaborative campaigns allows evaluation of our framework. The findings clarify how investors enhance their sources of power, legitimacy, and urgency and attract managers’ attention through collaborative engagement, and show how they manage these attributes to reshape the legitimacy and urgency of their claims in the eyes of managers. Our data suggest that “enabling organizations” such as the PRI initiative facilitate the emergence of collective action by lowering barriers to entry and providing a mobilizing structure, support collaborative efforts by adding their own legitimacy, normative power, and persistence to the collaborative engagement, and create conditions for a lasting dialogue between investors and managers by providing a hybrid organizational space.

Keywords

The Principles for Responsible Investment (PRI) initiative is one of the most promising projects launched by the United Nations Global Compact (UNGC) and the United Nations Environment Programme Finance Initiative (UNEP FI) to promote the consideration of environmental, social, and governance (ESG) issues by institutional investors. 1 Since the launch of the Principles by the ex-UN Secretary-General Kofi Annan in 2006, more than 900 financial organizations from 48 countries, representing approximately US$ 25 trillion of assets under management, have joined the initiative (PRI, 2011a). According to Rasche (2009, p. 532), these Principles “can help to set the right institutional framework for responsible investment decisions (. . .) If institutional investors start acknowledging the PRI as a guideline for their decisions, the business case for the UNGC will become more obvious.”

The growing number of investors’ collaborative engagements aiming at fostering dialogue with companies in relation to the UNGC principles is an indication of the strategic connection between the UNGC and the PRI initiative under the common UN umbrella. 2 The PRI initiative has supported the UNGC agenda in pushing companies toward sustainability. It has also spearheaded collective actions by institutional investors on ESG issues. Institutional investors, such as pension funds, asset managers, and insurance companies represent nowadays a sizeable proportion of assets in financial marketplaces (Useem, 1996). Their market power allows them to influence corporate practices in ESG domains through various governance mechanisms (Del Guercio & Hawkins, 1999; Ryan & Schneider, 2002, 2003). For instance, they can exercise their shareholders voting rights, file resolutions at Annual General Meetings (AGMs), or engage with corporate executives through written communications, phone calls, or meetings (Collier, 2004; Solomon, 2007). Academics and practitioners regard these investors as the driving force behind the development of Responsible Investment (RI) markets (Eurosif, 2008, 2010; Guyatt, 2006; Jurvale & Lewis, 2009).

Although institutional investors’ engagement with investee companies on ESG issues can move responsible investment “from margin to mainstream” (Sparkes & Cowton, 2004, p. 49), little is known about the organizational processes underlying this practice, especially when it is undertaken collaboratively. Prior research has clarified the conditions under which specific categories of institutional investors are likely to engage with investee companies (Del Guercio & Hawkins, 1999; Rubach & Sebora, 2009; Ryan & Schneider, 2002) and has identified which corporations are likely to be targeted (Rehbein, Waddock, & Graves, 1997). However, these works usually adopt a “variance perspective” that does not allow the capture of the organizing processes of engagement. Moreover, empirical studies on engagement have primarily focused on company managers’ attitudes and perceptions, for instance by analyzing the content of letters sent by executives to investors (Vandekerckhove, Leys, & Van Braekel, 2008). As a result, the organizational context surrounding the emergence of collective action remains understudied.

In addition, although prior theory has clarified how investors enhance their salience through activism (Agle, Mitchell, & Sonnefeld, 1999; Mitchell, Agle, & Wood, 1997; Ryan & Schneider, 2003), it has overlooked the processes by which investors reshape managerial perceptions of their claims’ legitimacy and urgency through engagement as it has failed to distinguish between the attributes and salience of investors and of their claims (Gifford, 2010a).

This article aims to address the above identified gaps. First, the authors explore and evaluate the roles played by the PRI’s organizational platform that supports institutional investors’ collaborative engagements with corporations on ESG issues. We approach the PRI initiative as an enabling organization that may help to overcome barriers to collective action by providing an infrastructure for investors to work with one another and through maintaining time-continuity of investors’ engagement, thus resulting in continued pressure on targeted firms. In so doing, we demonstrate that this organization facilitates the emergence, deployment, and maintenance of collaborative actions.

Second, the authors highlight the process whereby institutional investors use their increased power, urgency, and legitimacy to renegotiate the managerial perceptions of their claims’ legitimacy and urgency. In adopting a process perspective, our analysis specifies the dynamics of salience enhancement through investors’ engagement (Gifford, 2010a; Ryan & Schneider, 2003) and shows how enabling organizations can facilitate deliberative negotiation over the legitimacy of ESG issues (Palazzo & Scherer, 2006).

Theoretically, the authors combine insights from collective action theory (Hargrave & Van de Ven, 2006; Olson, 1965; Ostrom, 1990) and stakeholder theory (Freeman, 1984; Mitchell et al., 1997) with works on communicative legitimacy (Palazzo & Scherer, 2006; Scherer & Palazzo, 2007, 2011) to explore the processes whereby institutional investors reshape executives’ perception of both institutional investors and ESG issues attributes and explain how an enabling organization can facilitate, enhance, and maintain these processes. Empirically we draw on two in-depth qualitative case study analysis from the PRI engagement Clearinghouse, an opt-in online platform for signatory investors to propose and be involved in collaborative engagement activities. Our research benefited from unprecedented and unique access to data from the PRI secretariat that allowed us to evaluate our framework.

Organizing Processes for Institutional Investors’ Collective Action

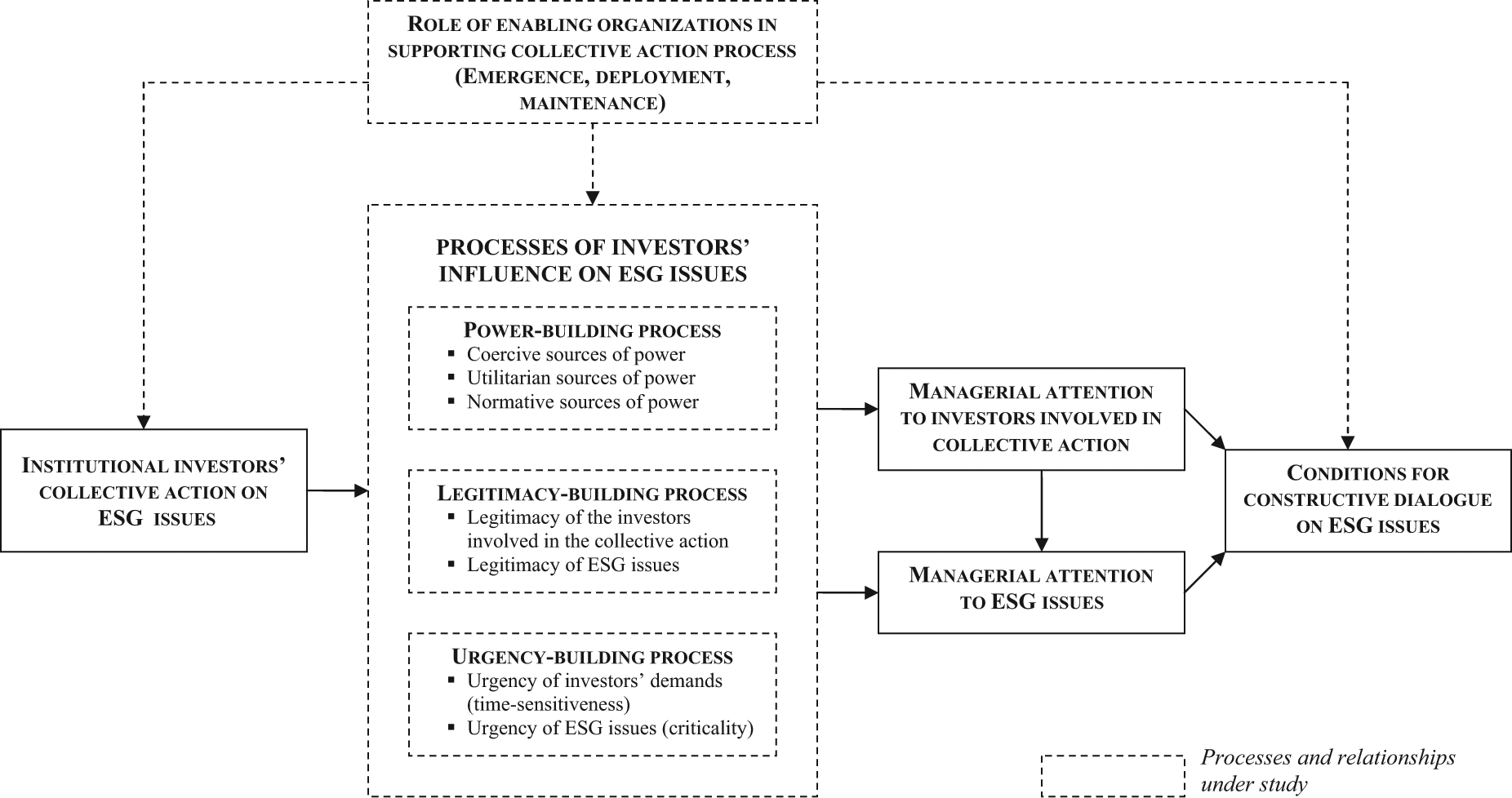

Although the influence of shareholders on corporations has traditionally been analyzed through the perspective of agency theory (Jensen & Meckling, 1976), recent research suggests that this framework does not capture changes resulting from the rise of institutional investors’ power in the financial marketplace (Clark & Hebb, 2004; Davis, 2009; Ryan & Schneider, 2002, 2003). In this context of “investor capitalism” (Useem, 1996), a “deep view” on stakeholder theory is more relevant to explain the influence of various types of institutional investors on corporations (Ryan & Schneider, 2003, p. 425). The authors rely on this stakeholder perspective to outline three processes whereby institutional investors accumulate attributes of power, legitimacy and urgency (Mitchell et al., 1997) and can mobilize their enhanced salience in the eyes of managers to reshape the legitimacy and urgency of the ESG claims they support (Gifford, 2010a). Figure 1 summarizes the overarching framework that supports our examination of the PRI secretariat and platform in facilitating the organizational processes of institutional investors’ collective action.

Organizing Processes for Investors’ Collective Action: An Overarching Framework.

Processes of Institutional Investors’ Influence

Because corporate managers have limited cognitive capacities (Simon, 1955) and cannot focus their attention on all the issues emerging in the corporate environment (Ocasio, 1997), they prioritize stakeholders and issues according to their mental map (Lucea, 2010) and their perception of the stakeholders’ importance (Mitchell et al., 1997). In pooling symbolic and material resources through collective actions, institutional investors can increase their own salience in the eyes of managers and in doing so create a context for shaping the salience of the ESG issues they promote (Agle et al., 1999; Mitchell et al., 1997). Prior research on institutional investors’ influence on corporations has highlighted the central importance of power, legitimacy and urgency in enhancing investors’ salience in the eyes of managers. Yet, it has failed to distinguish the attributes of the investors from the attributes of their claims (Gifford, 2010a) and has focused on a variance approach that can not account for the processes of attributes accumulation (Ryan & Schneider, 2003). To address these two shortcomings, the authors conceptualize institutional investors’ influence over ESG issues as a set of three processes of power-building, legitimacy-building, and urgency-building and outline whether and how these processes relate to investors or the claims they make.

Power-building process

A first process of institutional investors’ influence can be conceptualized in reference to the attribute of power. Building on Etzioni (1964), Mitchell et al. (1997) distinguish three sources of stakeholder power:

coercive power, based on the physical resources of force, violence, or restraint (i.e., threat of using a physical sanction); utilitarian power, based on material or financial resources (i.e., material rewards consisting of goods and services or money to acquire them); and normative power, based on symbolic resources which are normative symbols such as prestige and esteem, and social-symbols, those of love and acceptance. (p. 865)

In the context of the investor–corporate relationship, coercive power corresponds to the use of formal shareholder governance powers, such as the right to vote in annual general meetings, file resolutions, or rely on legal proceedings to enforce shareholder rights (Gifford, 2010a; Solomon, 2007). Utilitarian power reflects the ability of institutional investors to dispense or withhold material rewards, for instance by selling shares of a company (Ryan & Schneider, 2003). Normative power refers to investors’ symbolic actions aimed at damaging corporations’ reputation (Gifford, 2010a). These actions may involve the mobilization of mass media (Den Hond & de Bakker, 2007) to shame corporations and attract other investors’ attention to corporate misbehaviors.

The power-building process refers to the method whereby investors, through collective action, combine and leverage their various sources of power to be perceived as a more salient stakeholder in the eyes of managers. Collective action from institutional investors on ESG issues can have a multiplicative effect by reinforcing the various forms of power (Gillan & Starks, 2000, 2003). For example, it can increase the percentage of holdings owned in the targeted companies, the voting rights available to a specific resolution as well as the likely impact of a public statement or a threat of a public statement. Because power is a relational concept (Hardy, 1995; Pfeffer & Salancik, 1978) that reflects the nature of the interactions between a group of investors and the targeted corporation, the process of power-building relates to the number of investors involved rather than to their actual claim. However, the power-building process may orient managerial attention to the ESG issue raised by investors because they may be perceived as having a higher priority than other groups.

Legitimacy-building process

A second process whereby a group of institutional investors can shape managerial attention relates to legitimacy (Mitchell et al., 1997; Ryan & Schneider, 2003). Legitimacy has been defined as “a generalized perception that the actions of an entity are desirable, proper, or appropriate within some socially constructed systems of norms, values, beliefs, and definitions” (Suchman, 1995, p. 574). According to Suchman (1995), three different types of legitimacy can be distinguished. Pragmatic legitimacy is based on audience self-interest and refers to the possibility of manipulation by a corporation or its stakeholders through impression management (Palazzo & Scherer, 2006), moral legitimacy involves a conscious moral judgment, whereas cognitive legitimacy refers to the taken-for-granted nature of legitimacy, that is the fact that something is accepted as “natural” (DiMaggio & Powell, 1983).

In the context of investor collective action, all three dimensions of legitimacy may be at play: an ESG issue can have moral dimensions (e.g., child labor), the management of ESG issues point to pragmatic aspects and concrete cost savings (e.g., energy efficiency), and lack of cognitive legitimacy from the corporations’ side is usually the reason for justifying the engagement process in the first place.

Although the legitimacy of a stakeholder group and the legitimacy of its claims have sometimes been conflated in prior research (e.g., Agle et al., 1999), it is crucial to distinguish between both dimensions (Gifford, 2010a) when adopting a process perspective in the context of investors’ collective action. On one hand, a group of investors can reshape its own legitimacy as perceived by corporate managers in accumulating various forms of legitimacy related to their status because different stakeholders may derive their legitimacy from various sources depending on the institutional sphere within which they operate (Boltanski & Thévenot, 2006; Friedland & Alford, 1991; Walzer, 1983). On the other hand, the corporate managerial perception of the legitimacy of the ESG claim can be reshaped by the organizations involved in the collective action process as they may decide to enhance the pragmatic or moral legitimacy of their claim (Palazzo & Scherer, 2006; Patriotta, Gond, & Schultz, 2011). In so doing, those organizations can rhetorically enhance the taken-for-grantedness of an issue that was not even perceived as a problem by managers before the engagement process and thus reshape the cognitive legitimacy of this issue itself (Green, 2004, Green, Nohria, & Li, 2009).

Conceptualizing the legitimacy-building process in the context of engagement highlights the interplay between investors’ legitimacy and the legitimacy of their claims while uncovering the processes whereby the pragmatic, moral, and cognitive legitimacy of ESG issues is shaped by the group of investors.

Urgency-building process

A third process of institutional investors’ influence on ESG issues refers to the construction of the feeling of urgency on an issue or the group of stakeholders advocating this issue. Although urgency initially refers to “the degree to which stakeholder claims call for immediate attention” (Mitchell et al., 1997, p. 867), it can be specified through the two dimensions of time-sensitiveness and criticality to determine whether urgency refers to stakeholders or to their claims. Time-sensitiveness is a first dimension of the urgency-building process and it is expressed through the use of deadlines or ultimatums by investors when communicating with the companies to pressure the management to respond to their requests (Gifford, 2010a).

Within the context of the investor–corporate relationship, criticality refers to investors’ evaluation of the importance of the claim and its link to their vital economic interests (Ryan & Schneider, 2003, p. 419). Criticality is thus an attribute of the ESG issue that can be enhanced through deliberate action during the engagement process. The level of criticality of an ESG issue does not depend solely on investors but may reflect public policy agendas (Mitnick, 2000) or broader societal and environmental trends (e.g., global warming and obesity). Yet, in the context of engagement, it can be influenced by investors through their tone or assertiveness when interacting with the management of the targeted corporations. According to Gifford (2010a), criticality of investors’ issues can be evaluated in considering the willingness to apply human resources to the engagement process and persistence in raising the claim over a long period of time.

The process of urgency-building captures the various dimensions whereby investors influence their level of priority in the eyes of managers from targeted corporations and hence the priority granted to their claim on ESG issues.

Shaping the Organizational Context for Investors’ Collective Action

The roles of enabling organizations in the processes of engagement can be conceptualized in reference to collective action theory (Olson, 2000; Ostrom, 1990, 1998) and to works adopting a communicative perspective on organizational legitimacy (Palazzo & Scherer, 2006; Scherer & Palazzo, 2007). These roles can be theorized in distinguishing the stages of collective action’s emergence, deployment, and maintenance over time.

Facilitating collective action emergence

Although institutional investors collective actions on ESG issues can benefit all participants in terms of enhanced managerial salience and capacity to influence corporations, these actions are unlikely to emerge spontaneously. First, these actions can be prevented by institutional investors’ heterogeneity in terms of social, governance, and environmental goals, regulative constraints, and most valued modes of engagement (Ryan & Schneider, 2002, 2003). Second, even though heterogeneous institutional investors have a common interest in ESG issues, each of them can be tempted to act as a free rider to benefit from the collective action without bearing the engagement costs (Olson, 1965; Ostrom, 1990). Corporate behavior improvements obtained through institutional investors’ activism usually benefit all shareholders (Clark & Hebb, 2004; Gillan & Starks, 2000, 2003) and such free riding behaviors are not uncommon in the financial marketplace (Williamson, 1995). Lastly, the coordination costs for collective action may be perceived by each individual investor as too high compared to the benefits gained.

Collective action theory suggests organizational and institutional solutions for overcoming these barriers and avoiding such a “tragedy of commons” (Hardin, 1968). These solutions range from relying on coercive rules guaranteeing participants’ involvement (Olson, 1965) to self-governance through shared resources, valorization of the future, trust in each other and common understanding of the issue or organizational experience (Ostrom, 1990, 1998). Collective action issues can be addressed by designing organizations and institutions that can enhance cooperation, reciprocity, and trust among participants (Ostrom, 1998). Research on collective action in social movement theory (McAdam, McCarthy, & Zald, 1996) and technology studies (Van de Ven & Garud, 1993) highlights the crucial roles of network construction and institutional arrangement building to facilitate the emergence of collaborative initiatives (Hargrave & Van de Ven, 2006).

An enabling organization such as the PRI secretariat and the engagement Clearinghouse platform can facilitate the emergence of collective actions from institutional investors because it can play the role of a “mobilizing structure” (McAdam et al., 1996) that enhances institutional investors’ activism (Waddock, 2008b, 2009). Such an enabling organization can provide and shape the organizational context in which the three processes of investors’ influence emerge, are deployed, and maintained.

Specifically, enabling organizations help to overcome barriers to collective action through identifying ESG issues of interest to heterogeneous institutional investors and classifying them together. Second, granted an enabling organization has a good reputation; it signals and attracts firms more likely to cooperate and hence generates trust among participants when collaborating under its umbrella (Fehr & Fischbacher, 2002; Fombrun & Shanley, 1990). Lastly, it can partially bear coordination costs (Ostrom, 1998).

Supporting collective action deployment

The influence of an enabling organization on a collective action is not necessarily limited to the emergence of the process. In providing an organizational context for investors’ action deployment over time, this organization can contribute to enhancing the three processes of investors’ influence. First, it can bring to collective action its own sources of power and legitimacy while enhancing the group time-sensitiveness. Second, its mobilizing structure can attract organizations with other kinds of legitimacy or different sources of power that are not in the financial marketplace but share the ESG goal of investors (McAdam et al., 1996). Lastly, in facilitating communications and in playing a monitoring and coordinative role, an enabling organization can enhance trust among the participants in the collaborative engagement. Trust triggers higher levels of cooperation and benefits in the collective action context (Ostrom, 1998, pp. 12-13).

Maintaining conditions for constructive dialogues

The investors’ collective action process usually promotes a dialogue with corporate management on an ESG issue at stake. The dialogue can be then followed by concrete steps from targeted companies to address those issues. However, creating conditions for a discussion on the legitimacy of an ESG issue or of a corporate behavior is a demanding task, especially when the issue involves moral dimensions (Palazzo & Scherer, 2006; Scherer & Palazzo, 2007). Relying on the theory of deliberative democracy (Dryzek, 2001; Habermas, 1996, 1998), Palazzo and Scherer (2006) argue that public arenas offer relevant contexts for the negotiation of organizational legitimacy as they allow civil society actors to engage corporations. In such public contexts, corporations have to justify their behaviors, and they may rely on a variety of sources of legitimacy to do so. Although public debate on ESG issues is valuable and needed, corporate actors may be reluctant to engage in such public discussions if they are at an emerging stage of advancement of the ESG issue management and faced with confrontational nongovernmental organizations (NGOs) (Baron, 1995). Institutions such as the PRI initiative may offer an intermediate position between public and private arenas in providing a communicative space for discussing the legitimacy of ESG issues. An enabling organization can design a communication space for investors seeking to enhance corporate responsibility through the discussion of ESG legitimacy and the definition of a common position with other investors, and also between investors and managers from targeted corporations.

In the remainder of this article the authors will draw on the above processes of investors’ influence to examine in detail the role of the PRI secretariat and its engagement Clearinghouse platform, in the emergence, deployment, and maintenance of investors’ collective action (see the dotted arrows in Figure 1).

Context, Method, and Data

Research Context and Design

The authors adopted a case study research strategy to understand the processes underlying the relationships emerging from the raw data and to capture the investors’ experience in collaborating and dialoguing with company management representatives (Eisenhardt, 1989; Yin, 2003). The two case studies were selected following both literal and theoretical replication criteria (Miles & Huberman, 1994; Yin, 2003). In terms of literal replication, both cases show the presence of the PRI secretariat and the Clearinghouse platform in coordinating the efforts of participants through a formal network; and each engagement process is characterized by a high level of activity, beyond letter writing.

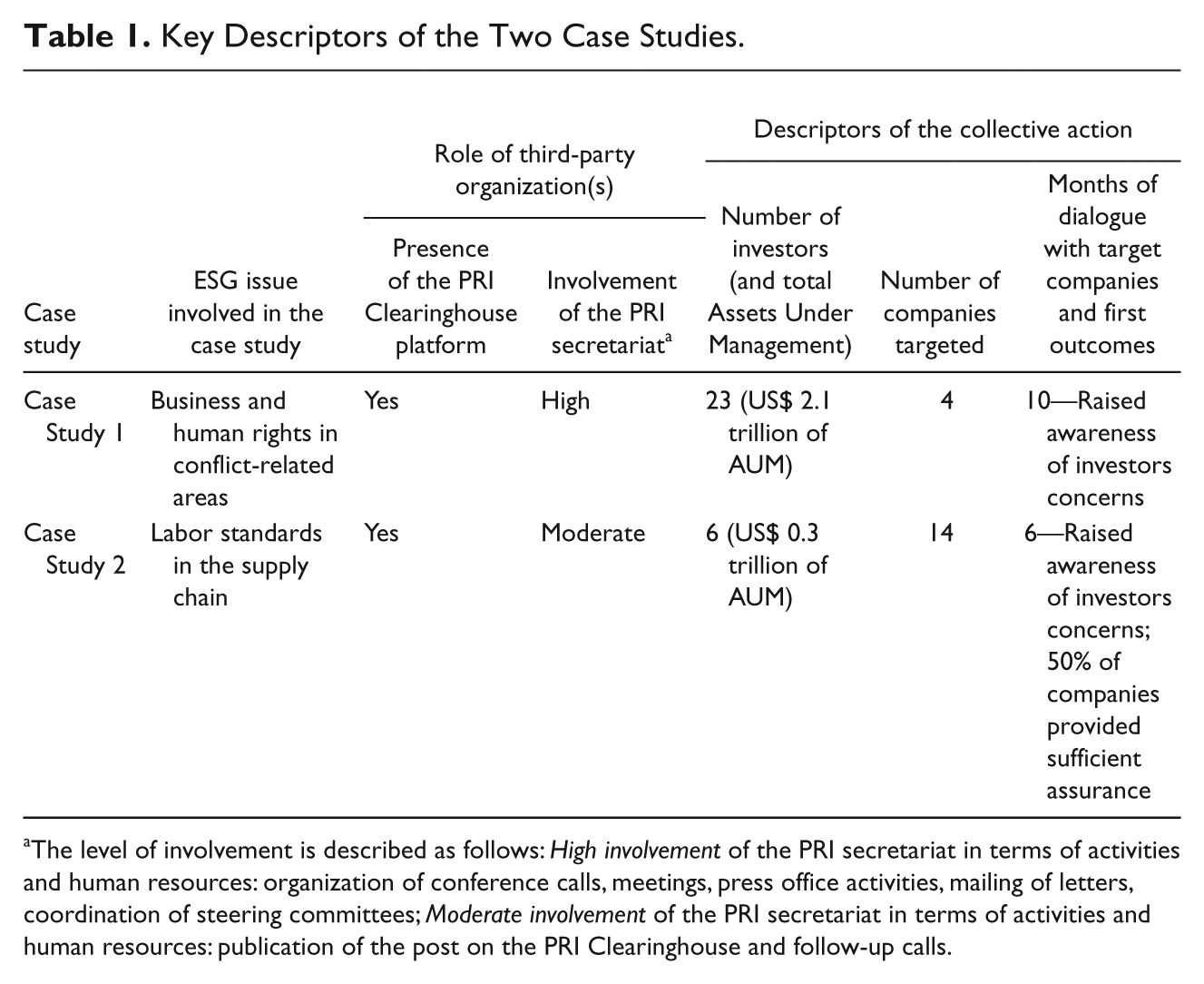

With regard to theoretical replication, the two initiatives differ on a number of viewpoints. First, the cases cover different ESG issues with companies, namely, human rights in a conflict zone and labor standards in a supply chain in a developing country. Second, the cases vary in terms of the number of investors’ involved (from 23 to 6) and total amount of assets under management (AUM) by the coalition of investment firms. Third, the composition and number of target companies differ across cases. Fourth, the level of involvement of the PRI secretariat varies between cases, a fact that allows for theorizing complementary dimensions of the process. Lastly, the level of progress and dialogue had with targeted corporations varies. Table 1 summarizes the characteristics of the investors’ collaborative engagements under study.

Key Descriptors of the Two Case Studies.

The level of involvement is described as follows: High involvement of the PRI secretariat in terms of activities and human resources: organization of conference calls, meetings, press office activities, mailing of letters, coordination of steering committees; Moderate involvement of the PRI secretariat in terms of activities and human resources: publication of the post on the PRI Clearinghouse and follow-up calls.

Data Collection

Data were collected through several methods such as archive analysis, interviews, and observations to follow a corroboratory mode. Using multiple sources of evidence provides stronger substantiation of constructs and allows for the triangulation of the various facts mentioned by the interviewees. The unit of analysis of each case study is the collective process of institutional investors’ engagement with companies, approached at a global level. However, the data were collected only from institutional investors, highlighting their perspective on the phenomenon. While this could be a limit of the investigation, the choice was justified for the following reasons. First, in most cases the partial and still ongoing development of the dialogue with the companies prevented the researchers from contacting them. Investors expressed a common fear of ruining the initial dialogue and relationship with the companies if an external researcher raised questions to the management about their current engagement activities. Second, the exclusion of interviews with company representatives ensured more openness and ease by the investors during the investigation process. Third, interviewing institutional investors was coherent with our theoretical focus on collective action’s emergence and deployment through the involvement of an enabling organization such as the PRI secretariat and its platform. Finally, to balance this unilateral perspective on the engagement process, interviews were completed with several sources of data, such as letters received from companies and notes taken during meetings, which allowed indirect evaluation of the corporate perception of the process.

Interviews

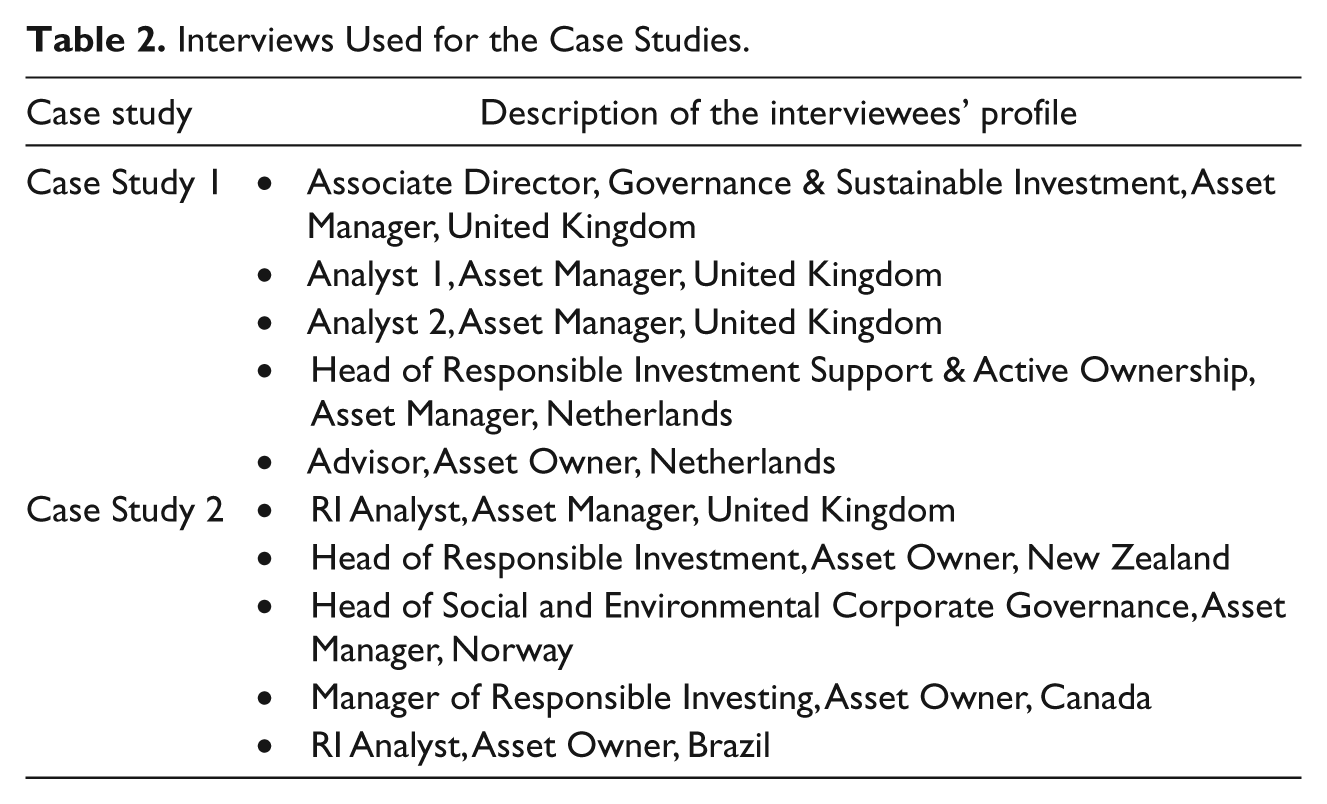

Five interviews were conducted with institutional investors involved in each collaborative engagement case study. Interviewees were from different regions (United Kingdom, Netherlands, New Zealand, and Norway) and different types of organizations (e.g., asset owners and asset managers; mainstream and niche SRI funds) with different sizes (e.g., for amounts of AUM) to capture the diversity of investors’ perspectives (Eisenhardt & Graebner, 2007). The investors interviewed were also actively involved in the projects and had participated in the dialogue with the targeted companies. Table 2 describes the profiles of the interviewees.

Interviews Used for the Case Studies.

These 10 interviews were conversational, semistructured and open-ended not only to allow for cross-case comparisons but also to leave room for specific explanations. The questions mainly followed the core categories of the inquiry although the interviews were adapted to specific contexts and discussions. Each interview was recorded and archived in the case study database.

Internal documents

The authors collected handwritten (subsequently scanned) and typed notes, internal confidential documentation (i.e., meeting notes, Power Point presentations, letters to and from companies) and publicly available material (reports from investors and companies, web sites, and media articles). Each piece of data was also categorized in the case study database to ensure that the documentation used could be easily referred to in the case study report and be available for later access.

Participatory observation

One of the researchers works for the PRI secretariat and has professional relationships with many of the investors interviewed. On one hand, the privileged researcher’s position allowed for gathering insiders’ insights on the functioning of the Clearinghouse platform, observing interactions between members of the investor network, and accessing confidential data as well as documentation not publicly available. This unique position allowed interviews to be conducted in a frank and trust-based mode.

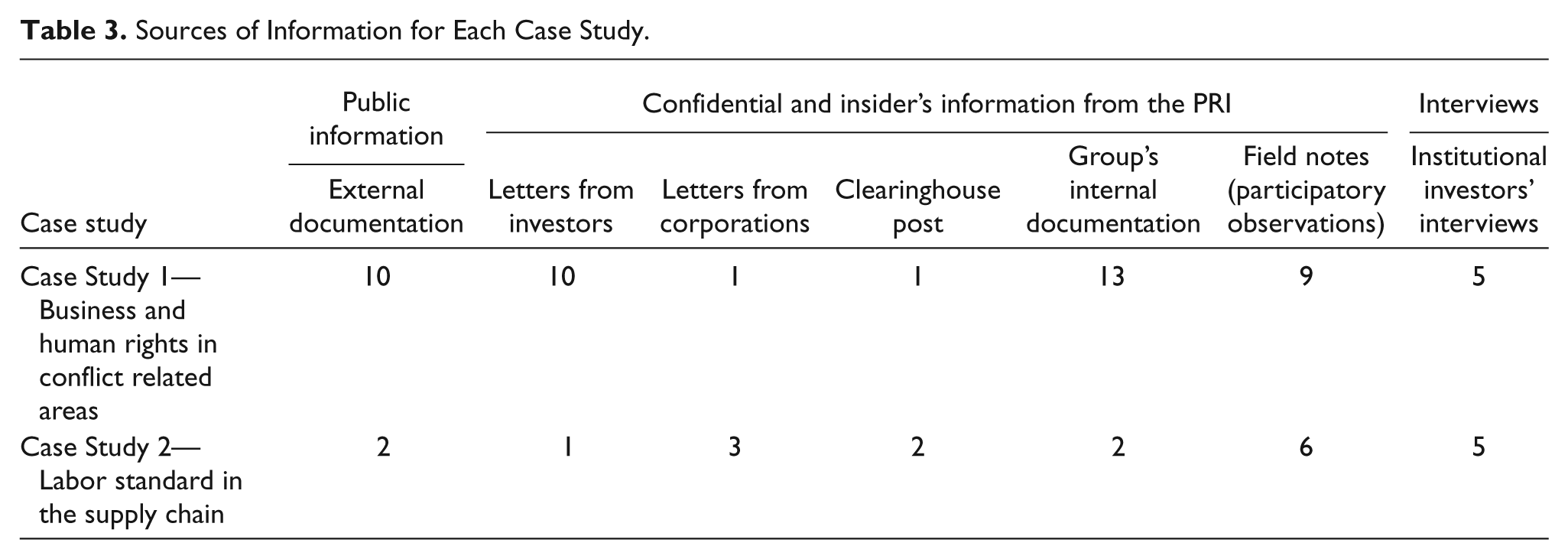

On the other hand, the researcher could have been more easily inclined to support the initiatives being studied and investors could have been influenced in their responses and provision of relevant documents. To control this bias, two approaches were adopted. First, multiple sources of evidence on the same phenomenon were provided whenever possible. Second, a researcher who coauthored the article and was not involved in the data-collection process carefully reviewed the interpretation of the data from an outsider’s perspective and was responsible for the recoding and rewriting of the case study narrative. Table 3 describes the sources of data used for each case study.

Sources of Information for Each Case Study.

Data Analysis

The analytic strategy used in the investigation consisted of the inductive evaluation of the dimensions of the framework to make sense of the processes of collective engagement (Langley, 1999). Moving back and forth between data and theory through a process of constant comparison (Charmaz, 2006; Glaser & Strauss, 1967), the “eclectic data” collected were grouped according to the dimensions of the overarching framework (processes of investors’ influence and various roles of the enabling organization). The authors relied on organized data to build a narrative account of the engagement process as it unfolded. The differences in the PRI secretariat’s involvement between both cases allowed us to study the variety of roles that an enabling organization can play.

We carried out content analysis and codification of all the relevant documentation in the case study database. Codes were initially suggested by the overarching framework and then developed further through the collection of raw data. New themes and codes were added in the analysis until theoretical saturation of additional categories was reached (Cassell & Symon, 2004; Eisenhardt, 1989).

Case Study 1—Business and Human Rights in Conflict Zone

Facilitating Collective Action Emergence

After unsuccessful individual engagements with companies operating in a postconflict country in Africa regarding human rights violations and peace promotion, and the increasing presence of campaigns pressuring investors to divest assets linked to the country, a group of PRI signatories contacted the secretariat asking to facilitate a collaborative engagement and proposed it through the Clearinghouse. Such a need for a coordinated action emerged from prior failures of investors’ individual attempts at engaging corporations in the issue at hand:

(. . .) Basically for a number of those companies we did not receive any response at all or, when we did receive a response, it was not a satisfactory response, or a response that we could not really build on in a further engagement. So working together with other investors, trying to get further and hopefully deeper into dialogue with these companies was the main reason for us to start our involvement in the collaborative engagement. (CS1, Interview 2)

This phenomenon was further described by another investor from this group as a “market failure” calling for external help to enhance coordination:

The second motivation that we’d have for being involved in collaborative engagement is, if you look at a good example at the moment is obviously what’s going on with the financial crisis, where you see a sort of systemic market failure, which one individual investor is not going to fold in 1-1 dialogue with the companies but which actually requires a more coordinated response (. . .). (CS1, Interview 3)

In this context, the PRI secretariat and the engagement Clearinghouse platform were instrumental in offering an organizational context that could support collective actions from signatories. As result, 23 investors from different regions decided to form a coalition to seek dialogue with four Asian extractive companies operating in the country. The data suggest that the PRI secretariat and platform provided a “mobilizing structure,” which gave an opportunity for investors to interact and coordinate their actions with actors they would not have contacted otherwise.

(. . .) the PRI network offers you the opportunity to work with other investors you have not necessarily worked with or have thought of working with before, simply because you are not aware that they are also looking at an issue, and it has been very useful to share that information (. . .) Being part of the PRI network facilitated collaboration between investors because working together with likeminded investors is a very safe environment and it is easier to stick to what you agree on. (CS1, Interview 1)

The “safe environment” refers to the notion that the PRI initiative offers an organizational context that is neither public nor private and that creates the conditions for an open dialogue between investors on ESG issues. The minutes from the group’s various meetings held in the context of this case study show the slow process of investors’ organizing and coming to an agreement on a common position. Specifically, the group negotiated on elements such as the number of corporations to target and to engage, the discursive framing of the human rights issues to be brought to the attention of managers, as well as the level of pressure to be brought to bear on corporations at various points in time. The identification of a common position is a time-consuming process that involves many compromises.

(. . .) Sometimes it takes too long to have everyone on board to reach some sort of conclusion on how to proceed and I sometimes fear that some investors will eventually decide that they will continue on their own. (. . .) It is effective to have a broad agenda but with a collaborative engagement it’s even more difficult to define a broad agenda than an agenda that only focuses on one issue. This has become a problem. (CS1, Interview 4)

The organizational support of the PRI secretariat and platform facilitated the achievement of an agreement on these key parameters.

The secretariat role is critical in pulling it all together, setting the agenda for the next time and saying what we need to do, what we believe and what the next agreed steps are. (CS1, Interview 3) The PRI’s crucial work is to motivate the parts, organise the meetings, have the stewardship of the engagement and move things forward. (CS1, Interview 5)

In supporting communication amongst investors, the PRI secretariat facilitated the emergence of a collective identity and enhanced the group dynamics underlying the engagement process. In providing a hybrid institutional structure neither purely private nor public for the engagement, the PRI secretariat enhanced trust and mechanically diminished the tendency of investors to free ride (Olson, 1965), not to actively participate in the engagement process or leak information about the process that could jeopardize the collective efforts to put pressure on corporations.

I looked back to one of the earliest collaborations that I was involved with (. . .) that was about five or six different investors trying to tackle the issue of you know investments in Burma and the big challenge that we kept coming up against was resources and times for someone to keep playing the secretariat role and setting the agendas and pulling it together and providing a forum. So what I think we’ve learnt over time is the importance in collaboration of having, if possible, an independent secretariat to kind of like, you know, organize things. (CS1, Interview 3)

As explained by an interviewee, this monitoring role of the PRI secretariat was maintained during the whole process of engagement.

I think that the ongoing facilitation of the process by the UN-PRI is very important to keep it moving because for someone in this group to assume a real leader role is very difficult to find one who would want to do it and second the problem would be that other investors would think “OK, you’re the leader, when action has to be taken you’ll be the one to do it” and I think that will lead to lower involvement of other investors. (CS1, Interview 4)

Supporting Collective Action Deployment

The role of the PRI initiative on this collective action can be further analyzed with reference to the three processes whereby institutional investors may influence managers from the targeted corporations.

Power-building process

Our data show that collective action is effective in enhancing investors’ perceived power as a group. In pooling the financial weight of more than 20 institutional investors, the collective action could have a significant impact on targeted corporations. Mechanically, their sources of coercive and utilitarian power are increased, as they can speak from one voice during meetings and AGMs, organize proxy voting campaigns, and divest or threaten to divest a larger amount of money from corporations: “These engagements are much more effective if you consider the weight collaboratively thrown on the table” (CS1, Interview 1).

The group could also cumulate normative power, as, for instance, a public statement published by a group of mainstream investors from different locations in the world can attract more attention in the media than a statement issued by a single investment firm. The PRI secretariat may contribute to increasing this normative power by bringing in signatory investors who are not committed to actively participating in the group’s activities but are pleased to contribute symbolically to the action:

it was agreed that the active involvement of everyone is not so crucial as having their signatures on the letter. (CS1, field notes)

Our data suggest that the PRI initiative could potentially add its own normative power in this process, due to its connection to the UNGC: the investors’ public voice could put in doubt or criticize UNGC companies’ effective implementation of the Compact’s Principles.

Although the group’s enhanced sources of power could be directly used to attract managers’ attentions to the ESG issue, the authors observed from the conversations with participants that investors considered their power to be used only as a last resort. The threat of filing resolutions or divesting was regarded by most investors as more effective than the actual use of these means. These threats were carefully distilled in a subtle diplomatic manner in letters, following an underlying logic of escalation.

I think we are doing an escalation strategy I mean we’ve been trying to engage with some of these companies without any success for over a year now, I guess. We’re doing the escalation strategy now, but it depends on if it’s possible in that organization, if that’s the right move. (CS1, Interview 3)

The actual use of power, by filing a resolution, for example, was generally considered to do more harm than good, and was regarded by most of the participants as too aggressive and “counterproductive” a strategy to be considered in the first stage of the engagement process. Similarly, investors generally believed that going public about their concerns on ESG issues may cause loss of trust between management and investors as well as loss of the opportunity to create an effective space for discussion:

(. . .) we are not seeking public profile for this work as we believe it would be inappropriate and counter productive to our long terms aims. As such, we will not be circulating any further details of the engagement, which will remain confidential. (Extract from a letter to one of the target corporations)

Although the enhanced potential power of the group of investors was not mobilized directly, the letter sent to the corporations specified exactly the values of the shares of the companies as well as the total AUM of the group. This mention clearly communicates to managers the potential utilitarian power of the investors’ group.

The PRI secretariat and platform allowed investors to bring together their sources of power while adding its own normative power. Yet the power-enhanced group could mobilize its threats to use power to direct managerial attention to ESG claims.

Legitimacy-building process

During the process of engagement, the participants accumulate and mobilize pragmatic, moral, and cognitive sources of legitimacy to reshape the perception of the legitimacy of their concern for human rights. The legitimacy of the group was derived from the composition of the coalition, primarily made of big mainstream investors. This granted the group some cognitive legitimacy to speak “in the name of the financial market,” as explained by an interviewee: “We’re not some crazy lunatics from some backward area, we’re twenty major international investors and you just have to answer” (CS1, Interview 4).

It also provided pragmatic legitimacy in the sense that investors were expected to take action to maximize their wealth and, in the present case, long-term search for profit. Moral legitimacy was also present through the presence of more ethically oriented investors and some participants’ connections with NGO experts on the issue at stake. The group did not insist on this source of legitimacy to avoid being perceived as similar to NGO campaigners, even though references to NGO information and reports had been mentioned in communications and dialogue with companies. The PRI organization also brought to the group its own source of moral legitimacy that derives from the fact that the principles are based on a multistakeholder dialogue (Gifford, 2010b) and are backed by the United Nations. The United Nation institution embodies higher order norms or principles that reflect the collective good, therefore it is perceived as more “trustable” than businesses or even governments (Gallup International, 2003). Specifically, the authors observed a use of the UN-PRI “umbrella” to distinguish investors’ collective engagement process from other forms of collective action:

When talking with [targeted corporation Y], a large part of the conversation went to explain what the UNPRI group is and that we are mainstream investors, and that were something different from the [name of a divestment campaign launched by a group of NGOs]. (CS1, Interview 4)

The PRI initiative was systematically mentioned in the letters sent to the corporations and, according to one of the participants, “making a reference to the UN initiative really makes a difference” (CS1, Interview 4).

The enhanced sources of legitimacy were combined together to shape the legitimacy of the group’s claim on human rights during the engagement process. First, in line with their role as investors and the related pragmatic and cognitive legitimacy attached to this role, the participants mainly focused their discourse on building a “business case” for the corporation to take into account human rights issues in their operations. This logic included several categories of arguments well reflected in extracts from the following letter and the position paper of the group:

We believe this [issue] creates a reputational risk for [Corporation Y]. (Letter to Corporation Y) We should recognise the underlying sentiment behind their point but stress that a sophisticated approach to political risk management is necessary to the creation of long term shareholder value. We expect the companies that we invest in to be able to engage with the issues that impact on the business, understand the risks, and develop a management approach that mitigates them. This is the basis of our concern. We would welcome the opportunity to discuss this widespread and complex issue. (Conference call N° 8 minutes, first position paper)

Beyond these pragmatic and utilitarian arguments, the group of investors also mobilized the moral sources of legitimacy, sometimes in combination with the reputation argument:

In some cases of course you use the argument that it is material to the company and material also to investors but I do not hesitate, if it is necessary, to say that this is also a moral issue and that the reputation of the company and our reputation as investors is at risk. (CS1, Interview 4)

The strategic mobilization of the United Nations and reference to other norms also allowed moral legitimacy to be embedded within the pragmatic business case logic, as shown in the following letter:

In general, when investing in companies that have strategically important operations in countries with weak governance, we analyze how well the company is responding to the challenges they face, including how they manage risks relating to human rights issues. While compliance with human rights norms and standard is difficult to quantify, it is possible to assess how proactively companies are managing the risks. For example, we take some reassurance from the publication of a human rights policy that references the Universal Declaration of Human Rights, and other appropriate norms such as the United Global Compact. (Letter to corporation X)

Urgency-building process

The engagement process also aims at enhancing the perceived emergency of the investors’ group demand by corporations. Our findings corroborate the idea that the collaboration process increases the general level of urgency. Yet this needs to be interpreted according to two facets of the urgency-building process. In terms of time-sensitiveness, the group of investors did not indicate specific deadlines for the companies to respond to the letters. However, the group agreed to give corporations an ultimatum if a feedback from the management was not received by a certain date. The relative level of legitimacy and power accumulated by the group may explain why actors did not put more pressure on the corporations in the first place.

In the context of this case, the authors did not observe attempts at shaping the perception of human rights’ criticality, beyond the assertion of the urgency of this issue from the perspective of investors that was embedded in their approach to this claim. This may be related to the nature of “human rights” as a category of issue, or to the fact that the engagement processes are generally long term activities (e.g., 2 or 3 years).

The tone of the engagement was clear and honest rather than assertive. As in the case of power, the escalation strategy emerged as an approach stressed by the group to increase salience:

Maybe the time has come to stop playing so nice because clearly they are not really paying any attention and we could start to be a little bit more assertive. (CS1, Interview 3)

Persistence was recognized by the interviewees as necessary for both the continuous participation in the group’s activities by members and the long time frame for engagement activities. In relation to the human resources applied to enhance perception of criticality, there is no clear evidence that the collaboration among the investors added more effort because approximately all the organizations in the group were already engaging individually with the targeted companies. However, interviewees recognized that the division of tasks amongst investors meant adopting a more efficient combination of efforts. Here the context provided by the PRI initiative to sustain collective effort seems to have played a background yet crucial role.

Maintaining Conditions for Constructive Dialogues

In providing an appropriate context for the maintenance of collective action, the PRI secretariat contributed to putting in place some of the conditions for a constructive dialogue between investors and corporations over the legitimacy of corporate behaviors in relation to human rights in specific countries. In June 2008, the group agreed on the final text of a letter to be sent to the chairmen of the targeted companies. 3 Subsequent meetings with the boards were held, based on responses to the letter.

At the time of the analysis, all the target companies replied to the investors’ letter with information concerning their requests; 11 meetings with senior management representatives took place in different locations and one trip to the country of the companies’ operations was organized by the PRI secretariat and the UNGC office. The occasions of dialogue with the company management represented an opportunity to clarify investors’ perspective and acquire additional information on corporate practices not in the public domain. However, the investors in the group agreed that the goals of the engagement still had to be fully achieved. As a final outcome of this engagement, the group would like the companies to have a robust policy on the issues raised, disclose relevant information on the effective application of the policy, and undertake an external verification of their activities.

These initial positive outcomes suggest that a certain level of trust has been achieved between investors and corporate managers from the respective target companies. The communicative space provided by the PRI Initiative for the process engagement, which has a hybrid status (neither public nor private), may partially explain the relative success of this process as it avoids both the challenging corporate confrontation with NGOs’ campaigns focused on public shaming and the failure of investors’ attempts to have one-to-one conversations with target companies.

Case Study 2—Labor Standards in the Iron and Steel Supply Chain

Facilitating Collective Action Emergence

In December 2006, allegations of inappropriate labor practices in the iron and steel industry came to the attention of investors through an article published by Bloomberg (Smith & Voreacos, 2006). The corporations involved were some of the largest manufacturers and users of iron and steel in the world. The allegations were not about the companies themselves violating international standards on human rights and workers’ conditions but their indirect use of forced labor at charcoal plants in Brazil via their suppliers.

A U.K. asset manager, a signatory of the PRI initiative, identified 14 firms in the automotive sector by size and geographical location (United States, Japan, and Brazil) that were known to purchase steel from Brazil. The invitation to collaborate on the dialogue with those companies was posted to the Clearinghouse and six investors decided to cooperate.

We had identified the issue in the press, we decided that it was sufficiently serious for us to look into further, we felt it was a severe risk to many of the companies that we and these other people would be invested in, so we then visited the PRI website, gathered all the investors, discussed target companies, and the wording of the letter . . . (CS2, Interview 1)

The group led by the U.K. investor used the PRI platform to facilitate the involvement of relevant participants from all over the world thanks to its large network of signatories. Although the small number of investors involved considerably diminished the risk of free riding (Olson, 1965), our data suggest that the level of commitment from the participating investors differed greatly. The leading investor was perceived as carrying the majority of the workload. Additionally, it was suggested that a more active coordination by a third party would have been ideal to have “some sort of supports or arrangements, so that it [the coordination cost] splits between all the signatories, rather than one on one” (CS2, Interview 1).

According to the lead investor, the context of the PRI initiative helped to define a common position among the group of investors:

Common position, that’s one of the crucial aspects of this kind of engagement, we speak with one voice. And the key to doing that is to manage people’s expectations, deal with problems before they arise. (. . .) you’ve got to manage the expectations of the people you are working with, before, and sort of frame what you want to achieve by the engagement, and sufficiently draw up terms that satisfy everyone, but sufficiently narrow terms so that you have a common approach. (CS2, Interview 1)

In April 2007, the group of investors wrote to the companies’ chairmen specifying their concerns and asking them to provide assurance that they had established processes to guard against connection with “inappropriate labor practices in their supply chain and related brand and reputational damages” (Letter sent by investors in CS2).

Supporting the Deployment of Collective Action Processes

In the context of this engagement, the PRI secretariat and Clearinghouse platform helped the three processes of attributes accumulation to happen but played only a minor role in enhancing those processes.

Power-building process

The enhanced utilitarian and coercive power of the investors’ group was reflected in the total size of assets that was clearly mentioned in various communications with corporations about the ESG issue at hand.

First of all, we decided to see how much funds under management between us we had to make the point that this was a mainstream group of investors with considerable assets. (CS2, Interview 1)

However, as in the prior case, investors were reluctant to activate and use their utilitarian and coercive power sources during the engagement process, as investors agreed on the fact that “once you divest, you no longer have any influence over the company” (CS2, Interview 3). The implicit threat of divestment was regarded as more effective than divestment in itself in attracting managers’ attention to the group’s demands and for creating the conditions for a constructive dialogue with corporations on the issue. Finally, the group was also reluctant to mobilize its normative power, for instance in making the existence of the engagement public, considering that “you’ll get better results changing how the company goes about its business by having discussions behind closed doors” (CS2, Interview 3).

Legitimacy-building process

Similarly to Case Study 1, cognitive and pragmatic forms of legitimacy of the group were enhanced in the engagement process, as the “collaborative engagement was led by some quite large and well known funds” (CS2, Interview 1). Arguably, the investors represented a far larger amount of total shares in target companies collectively, and as a result this enhanced their cognitive legitimacy as they could be perceived as speaking in the name of the financial marketplace.

In contrast to the prior case, the moral legitimacy of the PRI initiative was mobilized discursively rather than formally to support the claim. The PRI label and logo were not used in written communications to the companies, yet the fact that the collective action was supported by the PRI initiative was mobilized in discussions with corporate managers and constituted leverage to strengthen investors’ demand:

Obviously it also performs a major part of discussions with companies that all the investors involved were signatories to the PRI. And that carries a lot of weight. (CS2, Interview 3)

The various dimensions of perceived power and legitimacy were mobilized by investors to shape the legitimacy of the claim of the use of slave labor in Brazil when engaging corporations. Again, pragmatic legitimacy dominated the discourse, as the investors mobilized the business case argument to convince corporations of the existence of important reputational risks associated with poor standards of labor in the supply chain.

Our angle is obviously responsible companies are better companies. We’re investors and we want to be actively involved and make you a better company, more responsible, more environmentally sound, more socially sound, more financially sound, more government sound. (CS2, Interview 2) We’d much prefer to say that we’re a long term shareholder in your company and we believe that what you’re doing is bad or could increase risk of that to the long term performance, and we believe that you should manage the company well. (CS2, Interview 5)

Corporations quickly embraced this rhetoric, and most of their response to investors’ demands reflected the integration of a business case logic. Investors and corporations alike mobilized the moral legitimacy of international standards, such as the standards of the International Labour Organisation (ILO), as shown in this answer from a targeted corporation:

I would like to start by giving you the assurance that [corporation Y] not only shares your concerns regarding inappropriate employment practices, but also that [corporation Y] will never tolerate any actions or behaviours against the most fundamentals and internationally recognized human rights and labour standards. (Letter from Corporation Y)

In contrast to Case Study 1, investors deliberately added to this engagement process a different tactic to strengthen the cognitive legitimacy of their claim in mobilizing benchmark and mimetism (DiMaggio & Powell, 1983). They did so in mentioning during the engagement process the best practices from the competitors of targeted corporations to enhance the legitimacy of their demands on the ESG issue.

Urgency-building process

In the context of this engagement process, the group’s time-sensitiveness seemed important as most corporations replied promptly to investors’ demands although deadlines were not specifically applied by investors. As in the prior case, the authors did not observe specific approaches aimed at enhancing the criticality of the claim, maybe due to the fact that once acknowledged, human rights issues are regarded as a top priority by corporations due to their potential impact in the media. As a result, investors were not especially assertive in their relationship with corporations:

Obviously, you’ve got to be diplomatic, you can’t just ring up and shout at them, like some American funds do. You’ve got to build relationships, because we remind people we’re on the same side as management, we want the thing. (CS2, Interview 5)

Overall, the data show that the collective action enhanced the resources dedicated to the engagement and thus the possibility of making the claim more critical. Continuous monitoring and support of the PRI secretariat also afforded investors the opportunity to keep engaging corporations over the longer term. According to the interviewees, such persistence is crucial to altering attitudes and behaviors from reluctant corporations: “You have to keep on working it year by year” (CS2, Interview 2).

Maintaining Conditions for Constructive Dialogues

The engagement process has been successful in creating a high level of awareness among most of the corporations dealing with the issue. In some cases the companies themselves initiated the conversations after learning of investors’ concerns. When this did not happen, the U.K. asset manager, who took the lead in the collaboration, contacted the companies. A number of companies were aware of the risks and had already put in place an audit system to deal with these concerns. Other companies had not considered the impact of such allegations and decided to examine the issue and refer to the group during later discussions. In half of the cases the group received a sufficient degree of assurance, while in the other cases the investors agreed that a second follow-up would be necessary to hold the companies to the actions they had agreed to carry out. According to the investors, rising awareness of the issue by the companies was the first achievement of this collaboration.

The PRI secretariat’s role in promoting the maintenance of investors’ activities took place through communications with the lead investor to keep a continuous flow of information on the progress of the initiative. Regular updates on the interim and final goals achieved were also posted on the engagement Clearinghouse to increase awareness amongst the wider PRI community. The PRI secretariat shared information on this collaborative engagement in the 2008 PRI Report on Progress with the scope of setting the scene for an eventual second phase of the initiative. As a direct result of this initiative, in 2009 there was another collaborative engagement through the engagement Clearinghouse platform by Brazilian investors on slave labor in the supply chain of Brazilian companies.

Discussion, Implications, and Conclusions

Organizational Processes Underlying Investors’ Collective Action

A first key contribution of our analysis is to advance the stakeholder salience model in the context of the investors’ collective actions. The authors highlight the organizational processes that underlie the deliberate management of their salience by investors. In line with Gifford’s (2010a) research, our two cases show the importance of distinguishing the attributes of investors (power, legitimacy, and urgency) from the attributes of their claim (legitimacy and urgency) and to consider their interplay in a process perspective.

We observed in both cases that through collective action, investors pool together their various sources of power, legitimacy, and urgency to be perceived as a priority in the eyes of corporate managers. Yet there was no linear transformation of these enhanced attributes into salience. Rather, investors carefully managed their attributes and use them strategically and parsimoniously to shape the legitimacy of their claim in the eyes of the managers. Our analysis exemplifies of this fact in the context of the three subprocesses of power-building, legitimacy-building, and urgency-building.

First, in the case of power-building, investors adopted a deliberate logic of escalation avoiding any direct mobilization of their increased utilitarian, normative, and coercive sources of power, yet communicating subtly to corporations their enhanced position at the first stage of the engagement process. If unsuccessful, then, the progressive mobilization of these collectively enhanced sources of power to push corporations on the ESG issue was systematically considered by investors. This temporal pattern of power source mobilization confirms the idea according to which the threat of an action may be more powerful in influencing organizations than that of the action itself (Alinsky, 1971). Future research could investigate how investors learn collectively how to manage their sources of power.

Second, in the context of the legitimacy-building process, collective action allows for a diversification of the sources of legitimacy that are dynamically mobilized by investors to reshape the legitimacy of the issue in eyes of corporate managers. In both case studies, investors saw their cognitive legitimacy enhanced as they could speak “in the name of the marketplace.” The pragmatic legitimacy was expressed through the business case rhetoric that has dominated investors’ discussions on how to frame the ESG issues. This pragmatic approach was dominant in the letters sent to corporations in both cases. Although moral legitimacy was not absent from this process, it was either embedded in the utilitarian rhetoric according to which caring for the ESG issue would enhance corporations’ management of risk and performance, or brought into the conversation through direct and indirect calls for international norms. In the second case study, the cognitive legitimacy of the claim was enhanced in mobilizing mimetism (DiMaggio & Powell, 1983). Lastly, the authors did not observe deliberate attempts at reshaping the claim’s criticality and the mobilization of time-assertiveness was also limited in both cases. However, the persistence of the investors’ group effort and the maintenance of its deployment over time were regarded by all actors in both cases as a critical success factor.

These findings have important implications for future variance studies aiming to explain which variables may account for the success of collective investors’ engagement. First, our findings suggest that proxy assessment of investors’ legitimacy, power, and urgency may not be sufficient to achieve collective action successes as the changes in patterns of use (or “nonuse”) of these attributes may explain the success of the process. An implication of this finding for stakeholder theory is that changes in “patterns of stakeholder attributes” could better predict organizational and individual outcomes than changes in the strength of attributes. Building on this insight, future stakeholder research could theorize a configurative approach to stakeholder salience (Fiss, 2007). Second, our results suggest that the temporal dimension has to be integrated to account for the effectiveness of the engagement process, as persistence was a crucial element in both cases.

Our perspective on investors’ collective action is a first step in opening the “black box” of the collective engagement process. It moves beyond a variance perspective linking investors’ attributes to outcomes and points to the actual practices mobilized by investors as well as the micro-strategies followed to move forward their agenda on ESG issues and to engage reluctant corporations. Future studies could develop this process perspective on collective engagement to explain how investors collectively elaborate the micro-strategies of engagement that underlie their mobilization of power, legitimacy, and urgency. The practice perspective provides useful concepts for conducting such investigations (Reckwitz, 2002; Whittington, 2006).

How Enabling Organizations Influence Collective Action

A second contribution of this article is to uncover the various roles of enabling organizations such as the PRI secretariat and its Clearinghouse platform in the process of investors’ collective engagement. Our two case studies explain how this organization has stimulated, deployed, and maintained institutional investors’ engagement.

First, our findings suggest that enabling organizations can facilitate the emergence of collective action from institutional investors. They do so in various ways: (a) by triggering the initiative for collective action; (b) by offering through their networks mobilizing structures that allow potentially interested investors to network and to identify partners in engaging the collective action; (c) by diminishing incentives to free ride in engaging the reputation of investors as PRI signatories; and (d) by providing a monitoring context and an administrative structure that bear a significant amount of the coordination cost for the collective engagement process. Although these various organizational and institutional elements form the background of the engagement process, they can significantly diminish barriers to collective actions in the financial marketplace (Olson, 1965; Ostrom, 1998).

Second, our case study findings also suggest that enabling organizations can play a more or less active role during the process of collective action deployment in supporting the processes of institutional investors’ influence. Case study 1 showed that the enabling organization may not only act as a recipient for the action and an organizing context but can also add its own weight to the unfolding of the process, especially in the case of power-building and legitimacy-building. The fact that the PRI initiative is backed by the United Nations helps enhance the symbolic power of the group of investors, providing in itself sources of moral legitimacy as well as the possibility of attracting and capitalizing on the legitimacy of organizations perceived as legitimate on these issues (e.g., governments, NGOs). Even in the second case study, within which the PRI secretariat played a more “background” role, investors discursively mobilized the PRI and UN names to facilitate corporate engagement. In both cases, the PRI secretariat helped maintain investors’ commitment to their promotion of the ESG issue, hence ensuring the crucial persistence of the engagement process.

Third, our findings suggest that enabling organizations not only provide a forum for investors to communicate in engagement processes but also create a different institutional space—neither fully public nor fully private—within which communication on ESG issues may emerge between investors and corporations. Communication is essential to the emergence of trust and cooperative behaviors (Fehr & Fischbacher, 2002; Ostrom, 1998, pp. 6-7). In the context of investors’ collaborative engagement, communication may trigger attitudinal and behavioral changes on the corporate side. Both cases have shown the increased awareness on the ESG issue by targeted corporations’ managers after the engagement process as well as first behavioral and attitudinal changes from corporations. In providing a lasting “infrastructure” for investors’ collective action (Waddock, 2008a, 2008b), the PRI secretariat and Clearinghouse platform may thus create conditions for maintaining constructive dialogues on ESG issues between institutional investors and corporations.

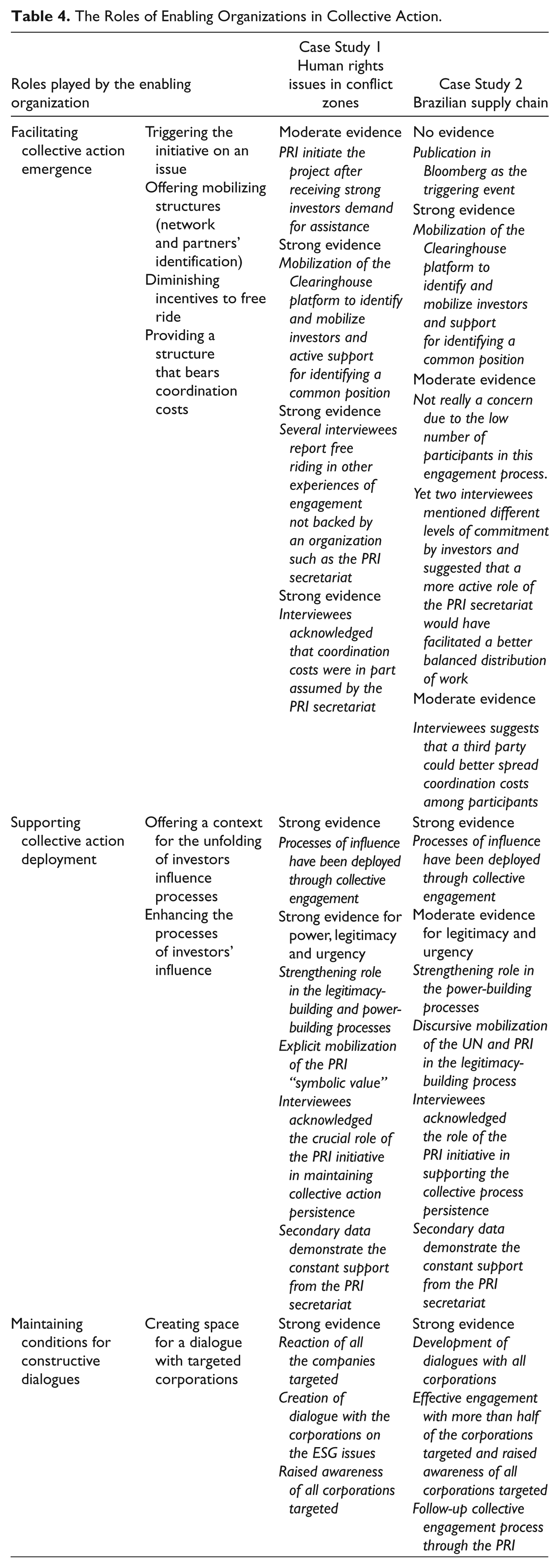

Table 4 summarizes the main findings from the two cases in regard to the role played by the PRI secretariat and the Clearinghouse platform and shows the level of empirical evidence regarding the role of the enabling organization.

The Roles of Enabling Organizations in Collective Action.

Overall, our results suggest that scholars interested in investors’ collective engagement should focus more on both the organizations facilitating these processes and the internal organizing of these processes. In line with Ostrom’s (1998) ideas that collective action researchers should spend more time documenting how actors have created institutional solutions that overcome barriers to collective action and prevented more tragedy of commons to happen, the authors propose to investigate the new emerging professional SRI institutions as candidates for solving common pool resources problems.

According to our findings, the PRI initiative did not only act as a set of useful “principles” for investors but also as an effective catalyst enabling collective action. In this regard, the PRI Clearinghouse platform can be considered as a “necessary supplement” from an organizational and institutional viewpoint (Rasche, 2009). The organization acted as a supplement to the lack of incentives for collective action in the financial marketplace while it added a new organizational space for communication between investors, and between investors and managers on ESG issues. In line with Waddock’s (2008a, 2009) assertions that principles such as the PRI form the ground of a new infrastructure for the development of a CSR movement, our study suggests the PRI engagement platform and secretariat play an important institutional role in consolidating new forms of investors’ activism focused on ESG issues. As a result, the implications of our research are not limited to the contexts of the PRI secretariat and Clearinghouse platform. In uncovering the mechanisms that support collective action, our findings can enhance processes of collective action in other areas of focus for the UNGC, such as the fight against corruption in Egypt or India. 4 Future studies could investigate whether and in what manner the enabling capacities of organizations, such as the UNGC, can be deployed in spheres other than the financial marketplace.

Designing Organizational Space for the Negotiation of ESG issues’ Legitimacy

Lastly, our findings point to the role of enabling organizations in providing an institutional context for triggering processes of deliberative negotiation between investors and managers over claims’ moral legitimacy. In so doing, the authors contribute to a recent stream of research in this area (Palazzo & Scherer, 2006; Scherer & Palazzo, 2007, 2011). Our findings suggest that enabling organizations such as the PRI secretariat and platform can provide “communicative spaces” allowing for a dialogue and negotiation over the (moral) legitimacy of ESG issues and involving corporations. The effectiveness of this space depends on its “nonpublic” nature that allows for enhancing trust among investors and managers from targeted corporations (Ostrom, 1990, 1998).

However, as in diplomatic contexts, the effectiveness of communication is related to the possibility of shifting at any moment within the public space. Hence, such hybrid “private–public” organizational spaces may benefit from some of the properties of public spaces as actors still have to justify their positions and actively discuss and negotiate their claim’s legitimacy by relying on different sources of legitimacy (Palazzo & Scherer, 2006; Patriotta et al., 2011). Future studies could develop these insights and build on frameworks such as Boltanski and Thévenot’s (2006) orders of worth theory to specify further how legitimacy is shaped by investors and corporate managers by convoking and combining a variety of orders of worth in these new institutional settings.

Footnotes

Acknowledgements

The authors are grateful to the PRI signatories interviewed and the PRI secretariat for having granted them an access to an important set of data on the process of investors’ collective engagement. They also wish to thank Aurélien Acquier, Luciano Barin-Cruz, James Gifford, and Jameela Pedicini for their helpful comments on the article. Finally they thank the editorial team of the present special issue for their helpful guidance through the revision process.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.