Abstract

Although an important feature of firms’ corporate social responsibility (CSR), the strategic pressures behind firms’ corporate philanthropy (CP) are not well researched or understood. This research note argues that firms’ CP and firms’ corporate political activity (CPA) may share common strategic antecedents; forces in firms’ political environment may shape both CP and CPA. Using S&P 500 data in a longitudinal analysis (1997-2004), the authors find evidence suggesting that industry-level political uncertainty increases firm propensity for engaging in both CP and CPA, above and beyond the propensity to engage in either as a stand-alone strategy. The authors use this preliminary evidence to explore political marketplace contingencies for the relationship between CP and CPA. CSR literature indicates that CP can benefit firms by creating and enhancing their relational wealth and institutional legitimacy. Such benefits may also serve firm interactions with government policy makers—a dynamic largely ignored until recently. The authors’ findings may indicate that, due to its institutional signaling ability and impact on firms’ reputations, CP may allow firms to differentiate themselves or stand out from others when faced with political uncertainty, and that these outcomes should be considered when firms engage in CP.

Corporate social responsibility (CSR), in particular corporate philanthropy (CP; Carroll, 1999), has become a popular strategic approach helping firms deal with external pressures for expected corporate conduct (Brammer & Millington, 2008). CP is a non-obligatory and voluntary transfer of wealth or resources from the firm to outside entities and is an important, if not central, aspect of CSR (Saiia, Carroll, & Buchholtz, 2003). Most research on CP explores its impact on financial performance or the characteristics of this relationship (Brammer & Millington, 2008; Dennis, Buchholtz, & Butts, 2009; Godfrey, Merrill, & Hansen, 2009). However, current scholarship still does not fully understand what prompts firms to engage in philanthropy (Dennis et al., 2009; Young & Burlingame, 1996); systematic exploration of CP’s strategic antecedents is lacking. Scholars exploring the antecedents of CP focus on industry characteristics and external pressures from different stakeholder groups such as employees, consumers, active shareholders, or the public at large (Carroll, 1999).

However, by and large, previous research generally overlooks political antecedents for CP. This omission is alarming because both in past (Navarro, 1988) and, more so in present scholarship (Baron, 2010, Richter, 2011; Werner, 2011) there is a growing realization that CP may be part of a firm’s portfolio of political strategies, or may be impacted by similar strategic considerations. As noted by Richter (2011) one can assume that CSR (including CP) and corporate political activity (CPA) are opposites—the former signaling positive corporate attributes and the latter negative ones. However, this view is overly simplistic, given that both CSR and CPA may be motivated by common strategic considerations and pressures (Richter, 2011). Though some scholars report that CP and aspects of CPA are statistically associated (making a tentative case for a common strategic lens; Hansen & Mitchell, 2000), few systematically explore what forces shape both corporate strategies. Indeed, Lyon and Maxwell (2008) call for research to untangle how aspects of CSR (including CP) and CPA relate to each other.

Thus, in this exploratory note, the authors investigate how conditions in firms’ political environments impact firms’ engagement in both CP and CPA. The key methodological issue is that firm heterogeneity exists in both firm CPA (Rehbein & Schuler, 1999) and firm CP (Saiia et al., 2003) making it difficult, yet important, to explore when the two strategic behaviors co-vary (Richter, 2011). Some firms engage in both CPA and CP, some firms engage in either CPA or CP (but not both), and some firms engage in neither activity. There are two tentative reasons why CP and CPA may reflect common, nonmarket strategic pressures. First, although the purpose of CPA is to obtain access to public policy makers (Moe, 1990), such access is often difficult to achieve given uncertainty in the political marketplace (Bonardi, Hillman, & Keim, 2005; Smith, 2000). Such uncertainty is often spurred by intense competition for limited political access (Baumgartner, Berry, Hojnacki, Kimball, & Leech, 2009; Baumgartner & Jones, 2005; Gray & Lowery, 1997). These conditions make firms’ CPA more uncertain in its ability to achieve political access (Hart, 2004). Second, CSR scholarship has established the ability of CP to enhance firms’ reputational wealth or assets (Fombrun & Gardberg, 2000; Fombrun, Gardberg, & Barnett, 2000). Such enhancement increases firms’ legitimacy and reputation with policy makers, such as the government, either directly or indirectly (Ashforth & Gibbs, 1990; Dahan, 2005; Fisch, 2005; Fombrun, 1996; Godfrey, 2005).

As noted by Werner (2011), CSR activities send a signal to a firm’s institutional environment that the firm stands apart from its competition. This signal can help with access to public policy makers, as the firm is able to differentiate itself among other politically active firms. Therefore, given the intangible benefits associated with CP, the authors argue that conditions existing in firms’ political environment pressure firms not only to pursue political activity (as traditionally assumed in scholarship dealing with the topic), but also to pursue CP above and beyond its traditionally explored antecedents. The converse may also be true, as firms that already engage in CP and face political uncertainty would be more likely to leverage their existing CP, compared with firms without CP expenditures. This study finds that across eight years (1997-2004) of data collected for S&P 500 firms, political uncertainty is positively associated with firms engaging in both CP and CPA, compared with firms that engage in just CP or CPA alone.

The contribution of this research to extant literature is its focus on nonmarket political precursors for corporate philanthropy. The authors primarily contribute to the literature on corporate philanthropy by extending the work of Godfrey (2005), Carroll and Shabana (2010), and others, and by exploring novel precursors for philanthropy (i.e., Dennis et al., 2009). CP should bolster a firm’s nonmarket and institutional standing and provide a form of relational insurance against political uncertainty. Exploring a nonmarket rationale for firm philanthropy can improve the understanding of this strategy’s importance. This study also contributes to research on CPA, because it exposes how other nonmarket strategies are potentially associated with CPA. This additional knowledge can change traditional views of CPA (i.e., Hansen & Mitchell, 2000), and how forces in a firm’s political environment—traditionally associated with CPA (Bonardi et al., 2005)—also impact other nonmarket strategies.

The rest of this research note is organized in six more sections. The first section below explores the general implications of CP for firm outcomes, the second explores the nature of strategic philanthropy and its firm implications, and the third section focuses on the strategic characteristics of CPA. The fourth section below focuses on how CP’s intangible benefits can help firms in the political marketplace, which leads to the study’s single hypothesis. The study then moves to the methods section and, finally, discussion and implications.

Corporate Philanthropy: Outcomes and Firm Implications

A salient aspect of CSR is CP, which includes various charitable contributions made by firms (Carroll, 1999). CP is a common business practice involving voluntary, nonreciprocal transfer of goods (such as money, services, etc.) from a corporation to another entity (Griffin & Mahon, 1997; Porter & Kramer, 2002). Because CP is not an explicit exchange of tangible assets (Godfrey, 2005), most contributing firms, at least in theory, are not supposed to expect some form of return for their philanthropic activity (Bruch & Walter, 2005; Godfrey, 2005; Saiia et al., 2003).

As noted by Godfrey (2005), three different theoretical approaches have been used to explore and explain CP. On the one hand, critics of CP argue that a firm’s use of its own monies for charitable causes is wasteful and represents a misallocation of funds, ultimately increasing the opportunity cost of capital (Friedman, 1970). In this view, firms are not task specialized to address social needs, and managers likely give to charities based on personal agendas or incentives, rather than objective societal priorities (McWilliams & Siegel, 2000).

The opposite view argues that businesses have societal and ethical obligations not only to their shareholders, but to other stakeholders as well (Wood & Logsdon, 2002). Managers control significant resources that can help address societal challenges and provide benefits to different firm stakeholders. Thirdly, as noted by Godfrey (2005) and others (Post & Waddock, 1995), there is a middle road—strategic philanthropy—which can impact a firm’s image and, consequently, its institutional impression. The provision of public goods will not only reduce regulatory pressures, but also positively impact the image of the firm (Brammer & Millington, 2005; Carroll & Shabana, 2010). This middle road may provide a theoretical link between CP and CPA.

Strategic Philanthropy as a Signaling Mechanism

The term “strategic philanthropy” connotes an action that influences social welfare, thereby generating intangible benefits (such as trust, reputation, and legitimacy) for the philanthropic organization; in turn, this should enhance shareholder wealth (Fry, Keim, & Meiners, 1982; Orlitzky & Benjamin, 2001; Post & Waddock, 1995). By engaging in strategic philanthropy, firms differentiate themselves in the minds of local communities and/or beneficiary institutions.

Specifically, Godfrey (2005) argues that CP can impact firms’ relational wealth by providing a form of reputation and legitimacy insurance within their institutional environment. This insurance can help firms maintain their image among different firm constituents, and also buffer firms from negative actions or threats taken by powerful stakeholders (such as, but not restricted to, government agencies). As such, CP can enhance the relational assets of a firm.

CP significantly influences how the contributing firm’s environment perceives the firm’s activities (such as the firm’s reputation; Saiia et al., 2003). Although reputation—or the views others have of the focal company—in itself does not directly impact firm outcomes, it can create a favorable reaction from firm stakeholders (Brammer & Millington, 2005; Suchman, 1995). Specifically, emerging research provides evidence that policy makers take into account firms’ CP. For example, Miller (2008) finds that CP enhances firms’ legitimacy in their response to organized labor and their regulatory environment (such as regulatory agencies). Tesler and Malone (2008) provide evidence supporting the view that government decision makers consider firms’ CP activities when interacting with them (see also Fisch, 2005).

Richter (2011) and Werner (2011) in recent working papers report direct evidence supporting that firm CSR and CPA are associated. CSR and CPA combined can increase firm value (Richter, 2011); CSR and CPA can be viewed as economic complements. Werner (2011) reports that some aspects of firms’ CSR activities (among which are charitable donations to local communities) can impact political access; CSR can serve a political function, much like a firm’s other corporate political activities. The key question that remains unanswered is: When are firms more likely to use both CPA and CP for political motivations? The authors argue that conditions emanating from firms’ political environment shape this outcome.

Corporate Political Activity: Uncertainty in a Nonmarket Context

The public policy making process can strongly influence firms’ operational environments; consequently, firms attempt to influence this process by engaging in a variety of corporate political activities (Schuler, Rehbein, & Cramer, 2002). The interaction between firms and legislators reflects an exchange process between policy makers (e.g., legislators and their staff) and those affected (e.g., firms, interest groups, and individuals) by public policy (Hillman & Hitt, 1999; Moe, 1990). The key currency in this exchange is the ability to achieve access to public policy makers (Austen-Smith, 1987, 1993; Hillman & Hitt, 1999). However, the ability of firm CPA to generate access is constrained due to two related issues. First, firms compete with other firms and interest groups for limited political access; they compete for the limited attention of policy makers (Gray & Lowery, 1997). Legislators receive donations and information from multiple sources—with different political preferences—that provide varying levels of information (Bonardi et al., 2005; Gray & Lowery, 1997). Second, there is uncertainty as to how the legislative process itself unfolds (i.e., Keim, 2001; Kersh, 2002; Wright, 1996).

Hence, achieving political access is highly uncertain, given the competitive and ambiguous nature of the political marketplace (Hart, 2004). Previous studies show that firms that give continuously—as a means to create long-term relationships and channels of access that will be used if the need arises—are able to maximize political access (Hansen, 1991; Kroszner & Stratmann, 2000, 2005). Stable giving, then, is associated with a higher probability of public policy access. This notion is supported in a variety of public policy arenas (Kroszner & Strahan, 1999, see also Lord, 2000). However, firms may be uncertain regarding how public policy makers behave (Keim, 2001), how political processes unfold (Hart, 2004), how issues change saliency (Bonardi et al., 2005), and how other firms behave (Gray & Lowery, 1997). In other words stronger industry variation in firms’ CPA will deviate from the more optimal continuous CPA giving. Given that continuous giving is more likely to maximize access and thus is more optimal for political access, deviation from such giving, which will be visible in higher intra-industry firm variance in political giving, can be seen as a rough proxy for political access uncertainty. At the same time, given CP’s ability to generate relational wealth insurance (Godfrey, 2005; Godfrey et al., 2009), CP may help firms complement such uncertainty by helping create positive relational assets (or positive image) with policy makers over time. This dynamic aspect of CP and CPA is important and difficult to analyze.

Corporate Philanthropy: Political Uncertainty and Relational Insurance Implications

The authors argue that a firm’s ability to signal unique characteristics to its environment—such as high levels of philanthropic behavior—can help increase its social status and reputation (Fombrun & Shanley, 1990). Indeed, Werner (2011) finds direct support for this view as he reports that firms’ CSR strengths (including CP) are positively associated with political access to public policy makers. The ability of CP to increase legitimacy and reputation has additional benefits for firms—in particular, those firms dealing with political uncertainty. As argued by Godfrey (2005), Miller (2008), and others (Brammer & Millington, 2005; Smith, 2005), firms’ charitable giving can be viewed as a form of relational risk insurance or uncertainty insurance. Godfrey et al. (2009) note that CP can generate goodwill (e.g., Knauer, 1994) and the perception that the firm has moral capital, in terms of its ability to fulfill ethical or moral obligations to society (Gardberg & Fombrun, 2006). In this case, the use of CP is initiated to further preserve or maintain existing relational assets in a firm’s institutional environment. This effect is due to two related dynamics: trust and the nature of reputation.

First, public policy makers prefer an exchange partner that reduces their need to verify or search for costly information, thereby reducing their transaction costs of information search (Wright, 1996). In this exchange process, firms perceived as more legitimate and trustworthy in providing information are more likely to be preferred as exchange partners (Kroszner & Stratmann, 2000; Wright, 1996). Policy makers rely more on partners that are perceived as legitimate, trustworthy, and reputable when the interaction is repeated (Schuler et al., 2002). As argued in the literature on trust, policy makers who trust their exchange partners are also less likely to second guess them (i.e., Mayer, Davis, & Schoorman, 1995). To the extent that CP can increase stakeholders’ trust in giving to corporations, this condition should allow such corporations to have a more influential voice with policy makers.

Second, reputation is an intangible asset that is difficult to imitate (Barney, 1991), can increase the commitment of firm stakeholders (Fombrun & Shanley, 1990; Turban & Greening, 1997), and can reduce uncertainty or information asymmetry between the firm and its external environment regarding the nature of the firm (Fombrun, 2001). This condition, in turn, should provide the firm with greater relational insurance. Indeed, Schneitz and Epstein (2005) find that a reputation for CSR (including corporate giving) protected firms’ stock prices from decline during the 1999 Seattle World Trade Organization meeting failure and crisis. Here, the use of CSR signals the firm’s perceived higher moral capital (Godfrey, 2005), which should reduce negative consequences emanating from disgruntled firm stakeholders. Empirically, Godfrey et al. (2009) find support for this argument; firms that engage in institutional CSR (of which CP is a mainstay) manage to mitigate negative stock market reactions when they are targeted for legal or regulatory actions better than firms that do not engage in such activities. Thus, CP can buffer negative market or institutional responses to firms’ wrongdoing (or other forms of uncertainty) by enhancing their relational capital or wealth.

The authors extend this line of reasoning to the realm of political uncertainty or instability. Firms whose industrial contexts are exposed to changes in political agendas, issue salience, or party ideology are unable to give continuously or in a stable manner, because the targets of their giving may change. Roberts (1990) depicts how stock prices of contributing firms declined when they suddenly lost access to politicians. Others also show how, in different industrial contexts, firms’ fortunes rise and fall based on the changes in the political arena, and on the rise and decline of administrations and policy preferences (Banker, Das, & Ou, 1997; Bowman, Navissi, & Burgess, 2000). To maintain their ability to access and prevent erosion within their political standing, firms should be able to rely on CP to compensate for, or complement, such uncertainty. Therefore, when an industry’s CPA varies (signaling firms’ difficulty at creating stable access to policy makers), the use of CP may compensate as an additional form of insurance. As with other forms of insurance, this action may protect the downside of legislative uncertainty in the political marketplace. At best, firms may not need this insurance; at worst, it may buffer them from facing indifference on the part of policy makers in the future (which would prevent them from having the chance to present their views and provide information to public policy makers).

In this context CP may act as a signal of the firm’s moral or relational capital to less friendly, or less firm-knowledgeable, policy makers (i.e., Fombrun, 2001). Thus, when firms are politically active, they will benefit from CP when faced with political uncertainty. However, the converse is also true. If a firm is already engaged in philanthropy, it can use it as leverage or as a complement to CPA when faced with political uncertainty. Thus, the authors propose a single hypothesis for testing in this research note:

Hypothesis 1: Ceteris paribus, variance in industry-level CPA is positively associated with firms’ use of both CP and CPA, compared with the use of CPA or CP on its own.

Method

Sample

The data set includes S&P 500 firms over a period of eight years (1997-2004). Due to missing information from the different data sources (see below), 2,900 firm-year cases were used for the analyses. Each case provides firm data for a particular year. Data on corporate philanthropy is collected through the Taft Corporate Giving Directory. This directory is a national yearly publication that includes both for profit and not-for-profit corporate giving, obtained from both corporate data and IRS filings, and is a common source of such data in the literature on CP (Lev, Petrovits, & Radhakrishnan, 2010; Saiia et al., 2003; Seifert, Morris, & Bartkus, 2003, 2004). The directory data were augmented with actual corporate charitable giving data, found on Form 990, which firms must file with the Internal Revenue Service (IRS), the U.S. government agency responsible for tax collection and tax law enforcement, to ensure completeness of the data and to cross check accuracy. Data on corporate political expenditures is obtained through Federal Election Committee (FEC) filings and data compiled by the Center for Responsive Politics (i.e., Schuler et al., 2002), and data from the websites of the Senate’s Office of Public Records (http://www.senate.gov/legislative/Public_Disclosure/LDA_reports.htm).

Measures

Dependent Variable: Combined CP and CPA Expenditures

This study argues that firms are likely to engage both in CP and also in CPA when faced with uncertainty in their political marketplaces. To model this dynamic relationship, the authors collected data on firms’ philanthropic giving and firms’ corporate political expenditures as a first step in setting up the dependent variable. First, information on each firm’s total philanthropic expenditures was collected from the Taft Corporate Giving Directory and also directly through the IRS Form 990. Second, each firms’ total political expenditures were collected. Following extant literature, this measure includes all expenses associated with lobbying, and/or political action committee (PAC), and/or soft money expenditures, as well as any 527 related expenditures (expenditures related to nonprofit organizations that are nonetheless supported by corporate donations, for political purposes) (Hersch, Netter, & Pope, 2008; Hillman & Hitt, 1999). Finally, the authors set up the dependent variable combining CP and CPA. To do so, the authors created three new categories of firms’ strategic choices with regard to CP and CPA. The first category comprises observations from firms that have CPA expenditures, but no CP expenditures. The second category comprises observations from firms that have CP expenditures, but no CPA expenditures. The third category comprises observations from firms that have both CP and CPA expenditures; the dependent variable is combined CP and CPA spending (i.e., neither category is zero). Within the study’s sample, the subsamples for these categories are 1,198, 258, and 1,162. There is a residual category of 282 observations having neither CPA nor CP expenditures; there is no useful information in these firms for purposes of this study. This procedure creates two combinations of dichotomous variables. The first contrasts firms that engage only in CPA as one level of the dichotomous variable, and firms that engage in both CP and CPA as the other level of the dichotomous variable. The second contrasts firms that engage only in CP as the first level of the dichotomous variable, to firms that engage in both CP and CPA as the other level of the dichotomous variable.

Independent Variable and Control Variables

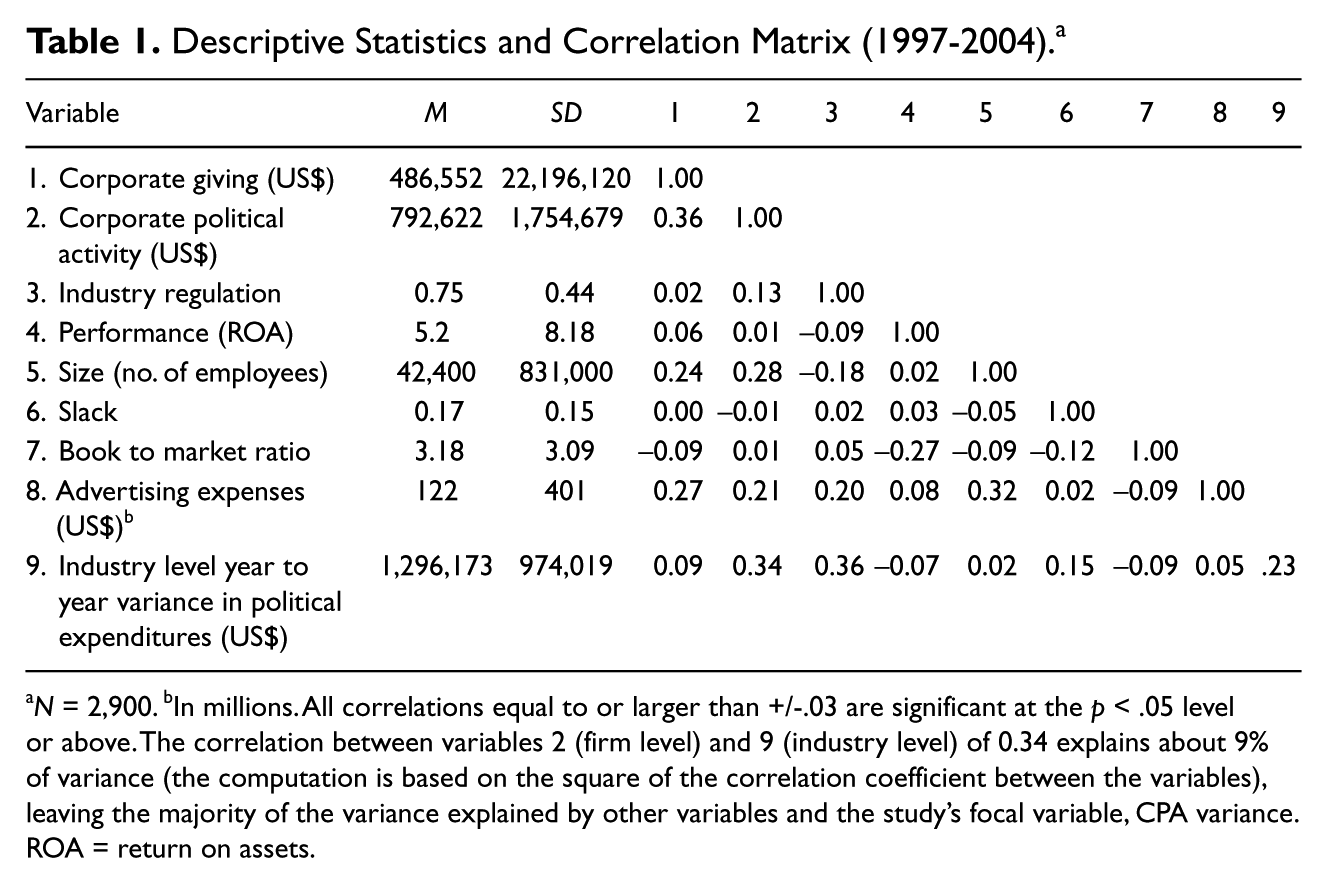

The analysis uses CPA uncertainty at the industry level as the determinant of combined CPA and CP spending at the firm level. The analysis uses a set of control variables to isolate this relationship for testing. As Table 1 indicates, the industry-level variable has a 0.34 correlation with CPA spending and a 0.09 correlation with CP spending (i.e., corporate giving). As a result, the authors expect to find a positive relationship between CPA uncertainty and CPA spending. What the study’s hypothesis investigates is the difference between firms that combine CPA and CP spending and firms that do not. The study does not use data on firms that have neither CP nor CPA.

Descriptive Statistics and Correlation Matrix (1997-2004). a

N = 2,900. bIn millions. All correlations equal to or larger than +/-.03 are significant at the p < .05 level or above. The correlation between variables 2 (firm level) and 9 (industry level) of 0.34 explains about 9% of variance (the computation is based on the square of the correlation coefficient between the variables), leaving the majority of the variance explained by other variables and the study’s focal variable, CPA variance. ROA = return on assets.

CPA uncertainty

The study measures CPA uncertainty as the industry-level CPA year-to-year variance of firms’ CPA expenditures (at the two digit SIC code). Because some scholars argue that policy making impacts industry-level outcomes (Hansen, 1991; Heinz, Laumann, Nelson, & Salisbury, 1993; Smith, 2000), variation in CPA giving at an industry level of analysis should also reflect political changes or uncertainty. The authors do not use a firm-level measure of CPA variance because firm-level CPA variance may be of an idiosyncratic nature and reflect variation that is unique to the firm, rather than reflecting political marketplace uncertainty. 1

Control variables

A main issue in explaining firm philanthropy is to control for alternative explanations for it. First, year dummies are included to account for possible annual economic effects. Second, different stakeholder groups may push the firm to contribute to charitable causes; such pressures likely vary by industry (Carroll, 1999; Godfrey, 2005). Therefore, industry dummies at the two digit SIC code level are included. Third, industry regulation is introduced as it may motivate firm CSR (Fisch, 2005). Moreover, at the firm level, several other relevant variables are included. First, the authors add firm performance, measured as a firm’s return on assets (ROA; Godfrey, 2005; Seifert et al., 2004). Second, firm size, measured as the number of firm employees, is included. Third, firm slack, which also impacts CP (Buchhholtz, Amason, & Rutherford, 1999; Seifert et al., 2004) is included. Slack is measured as the debt-to-equity ratio (Steensma & Corley, 2001). Fourth, book to market ratio is included, as others have shown it may impact philanthropy (Godfrey et al., 2009; Lev et al., 2010). Last, advertising expenses are included as they also have been shown to impact firm philanthropy (Lev et al., 2010). All firm financial data is obtained from COMPUSTAT.

Analyses

Given the nature of the dependent variable and the sample examined, this study uses a pooled cross-sectional logistic multinomial regression. This regression analysis takes into account both between (cross sectional) firm variance, and within firm variance to assess the impact of both unique firm-level and between-firm effects. This type of analysis requires the choice of a reference category used to compare the chosen level of the dependent variable: in this case, firms that have both CPA and CP expenditures, which constitute the reference category, to firms that engage in CP or CPA. The authors use a longitudinal firm-level random effects model using SAS Proc Genmod, which is appropriate for pooled, longitudinal cross-sectional logistic regression analyses (Diggle, Heagerty, Liang, & Zeger, 2002). This analysis uses maximum likelihood estimators to assess the effects of the independent variables on the dependent variable. For the analysis, the authors employ two models: a control model (i.e., without the independent variable), and a model with the independent variable included.

Results

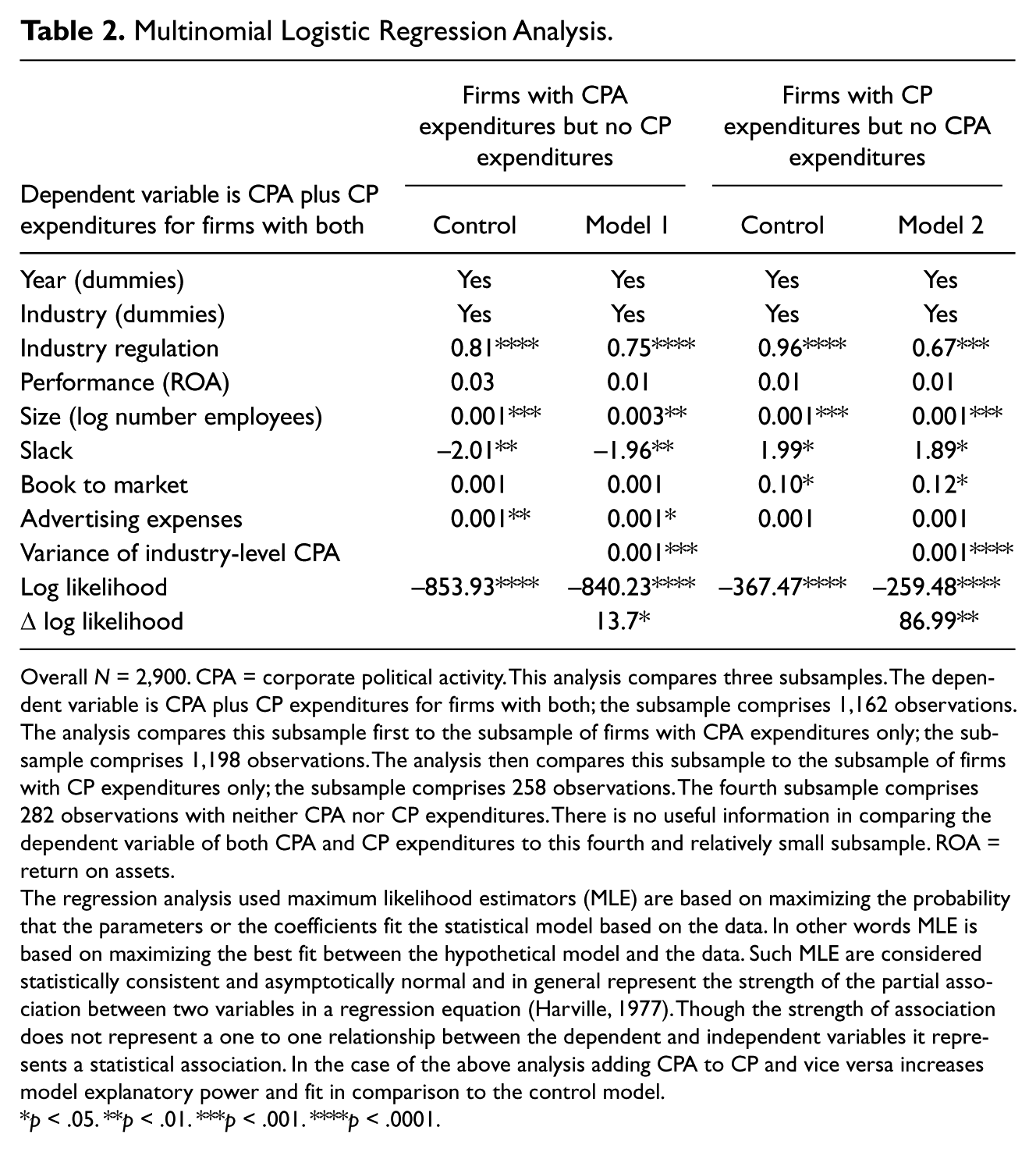

Table 1 provides the means, standard deviations, and correlations of all the variables across all sample years (1997 to 2004). Table 2 reports the analyses for the hypothesis. Table 2 is divided into two sides. The left-hand side includes the analysis in relation to firms that had CPA, but no CP expenditures, and includes the control model (without the independent variable) followed by Model 1 (including the independent variable). The right-hand side of Table 2 includes the analysis in reference to firms that had CP, but no CPA expenditures, and includes the control model followed by Model 2. In effect, the pool of firms with CP and CPA expenditures is compared with the pool of firms with CPA only, and then the pool of firms with CP only. 2

Multinomial Logistic Regression Analysis.

Overall N = 2,900. CPA = corporate political activity. This analysis compares three subsamples. The dependent variable is CPA plus CP expenditures for firms with both; the subsample comprises 1,162 observations. The analysis compares this subsample first to the subsample of firms with CPA expenditures only; the subsample comprises 1,198 observations. The analysis then compares this subsample to the subsample of firms with CP expenditures only; the subsample comprises 258 observations. The fourth subsample comprises 282 observations with neither CPA nor CP expenditures. There is no useful information in comparing the dependent variable of both CPA and CP expenditures to this fourth and relatively small subsample. ROA = return on assets.

The regression analysis used maximum likelihood estimators (MLE) are based on maximizing the probability that the parameters or the coefficients fit the statistical model based on the data. In other words MLE is based on maximizing the best fit between the hypothetical model and the data. Such MLE are considered statistically consistent and asymptotically normal and in general represent the strength of the partial association between two variables in a regression equation (Harville, 1977). Though the strength of association does not represent a one to one relationship between the dependent and independent variables it represents a statistical association. In the case of the above analysis adding CPA to CP and vice versa increases model explanatory power and fit in comparison to the control model.

p < .05. **p < .01. ***p < .001. ****p < .0001.

Hypothesis 1, which postulates a positive association between variance in CPA and firms’ use of both CP and CPA, compared with the use of either CPA or CP on its own, is supported. The coefficient of CPA variance is significantly associated with firms using both CP and CPA when compared with firms with only CPA expenditures (β = .001, p < .001, Model 1; Table 2) or firms with only CP expenditures (β = .0001, p < .001, Model 2; Table 2). The differences in log likelihood are also significant when moving from the control models to those with the independent variable.

With regard to the control variables, regulation, size, and advertising expenses (to some degree) are positively associated with firms’ combining CP and CPA. Slack is significantly associated with firms’ combining CP and CPA, but not consistently so in its sign. The authors also explored the possibility of collinearity but all variance inflation factors associated with the regression coefficients were below 4 in an OLS regression run to test for this eventuality.

Discussion and Implications

This study explores the novel possibility that conditions in firms’ political environment, specifically political uncertainty, would jointly impact firms’ CP and CPA. The assumption was that, beyond an economic rationale for philanthropy (which is partially supported in extant literature), firms also use philanthropy as a signaling mechanism in their nonmarket and institutional context. Moreover, the possible relational capital associated with CP may prove beneficial under conditions of uncertainty as a form of relational insurance aimed at public policy makers. In other words, it is possible that the use of CP complements firms’ use of political activity. The analysis finds that over a period of eight years (controlling for important antecedents of CP such as yearly effects, industry-level pressures, etc.), variance in CPA is positively associated with firms’ combining their CP and CPA spending. The findings of this study may indicate that firms’ use of philanthropy is more complex than previous literature suggests. Firms may use CP and CPA as complementary strategies to deal with uncertainty in the political marketplace.

Specifically, the tentative findings of this study suggest that by engaging in CP alongside CPA, firms signal to external stakeholders—in particular, public policy makers—that they are attentive to external stakeholder pressures; doing so can in theory increase their legitimacy, trust, and reputation (Ashforth & Gibbs, 1990; Godfrey, 2005; Miller, 2008). These attributes, in turn, should prove beneficial in bolstering a firm’s CPA standing relative to other firms’ CPA. This dynamic may be due to two related issues. First, engaging in philanthropy generates higher levels of trust among some of the firm’s various stakeholders. By investing resources outside its boundaries, a firm signals to its institutional environment that it intends to establish good relations with its environment, or that it “listens” to external constituents (Berman, Wicks, Kotha, & Jones, 1999; Rehbein & Schuler, 1999; Zucker, 1986). For example, Godfrey et al. (2009) finds that some aspects of CSR, including CP, result in a positive corporate image among corporate stakeholders; effectively providing the firm with a form of reputational insurance (see Ioannou & Serafeim, 2010). Second, to the extent that CP can enhance firms’ institutional legitimacy (see for example, Godfrey, 2005), firms that are perceived as more legitimate in their institutional environment should also enjoy improved political access (Boddewyn & Brewer, 1994; Hillman & Hitt, 1999). Legitimacy is an important “lubricant” in a firm’s interaction with its institutional landscape and other firms, and it is associated with improved reputation (DiMaggio & Powell, 1983; Suchman, 1995). Third, reputational and relational capitals are important resources in the political marketplace as they help differentiate between entities vying for access (Attarca, 1999, 2000).

The study’s findings contribute to the literature on corporate political activity (CPA). To better conceptualize the conditions under which CPA and CP relate to each other, the authors extend the work of political scientists and management scholars on the conditions under which firms will engage in different nonmarket approaches (for example, Baron, 1995; Schuler et al., 2002). Some scholars argue that competition for access and political uncertainty will likely contribute to firms’ CPA (Gray & Lowery, 1997). However, few researchers go beyond the concept of CPA to hypothesize how other relational benefits—such as those associated with CP—also result from increased barriers to political access (exemplified by uncertainty). The findings of this study hint at the possibility that firms wishing to improve their chances of being heard should engage in corporate giving (CP) to complement existing CPA, to bolster their image with policy makers.

The possible complementarity between CPA and CP may also address the reported disparity between firms’ CPA and CP expenditures. Ansolabehere, de Figueiredo, and Snyder (2003) and also Milyo, Primo, and Groseclose (2000) note that, in general, firms give more money to charitable causes than they invest in political strategies such as PAC contributions. These scholars view this disparity as indicating not only the weakness of CPA, but also the argument that CPA (like CP) may just be a form of voice or consumption rather than an investment-oriented strategy. They do not make any assumption as to whether the two strategies are otherwise related, but use the one to highlight the weakness of the other. Our exploration, however, raises the possibility that this supposed disparity (disparity between investment in CP and CPA) is not really a disparity at all—firms may combine CP and CPA, because both may be impacted by similar political marketplace considerations. Hence scholars may better understand how the political context of firm CPA impacts other aspects of a firm’s nonmarket strategy.

The findings of this study may also inform the ongoing debate on the complexity of corporate motivation for CP. Some scholars consider philanthropy and the general use of CSR as actions benefiting stakeholders and, thus, a benevolent or even an altruistic action (Gan, 2006; Godfrey, 2005). Firms, as citizens of their institutional arenas, may have a moral obligation to ensure social welfare and benefit their stakeholders (Waddock, 2001). Following this view, firms need to ensure that communities and society in general benefit from their operations. This view of corporate giving assumes that although firms might enjoy tangible returns from CP, this outcome should not be the main rationale for such activity. Others view CP as mere window dressing or, perhaps, cause-related marketing (Deshpande & Hithon, 2002; Drumright, 1996). This study’s findings indicate that CP may also have a strategic meaning exemplified by the strategic philanthropy view of CP (Post & Waddock, 1995), which focuses on the intangible and indirect benefits associated with CP. Although some criticize the notion that firms’ CP is not strategic—as firms do not truly understand how to leverage it (Bruch & Walter, 2005; Porter & Kramer, 2002)—the findings of this study temper this notion: firms may employ a multi-lens rationale for their philanthropy. The study’s findings seem to align reasonably with the strategic conception of philanthropy, which can have political effects through perceived legitimacy and reputation.

As noted at the onset of this study, the notion that firms may use CSR (specifically, charitable giving) to deal with their political environment is not completely new (see Neiheisel, 1994, for theoretical considerations). Yet, until now, this notion remains systematically unexplored with few recent exceptions (Richter, 2011, Werner, 2011). Previous studies do not explore when firms engage in both strategic approaches simultaneously, or the conditions that lead to such a joint outcome. The study’s point of departure is that CP enables firms to signal not only compliance with societal expectations, but also enhances their relational wealth; doing good can make the firm stand out and may provide a buffer against coercive forces or negative events (Godfrey et al., 2009). The two related benefits of CP, differentiation and relational reputation, are significant institutional signals that represent good will, and potentially help firms to receive preferential treatment from their institutional environment (Carroll & Shabana, 2010). Empirical support for this argument is growing (Brammer & Pavelin, 2005; Fombrun & Shanley, 1990; Miller & Guthrie, 2007; Miller, 2008). Much of this literature implies that, by doing good, firms not only establish a better reputation with increased legitimacy, but may also more effectively deal with disgruntled stakeholders. In other words, philanthropic activity may buy the firm relational credits with its larger environment.

Limitations and Future Research

This exploratory study examines the relationship between political uncertainty and conditions leading to firms’ decisions to combine their CP and CPA. This study’s working assumption is that firms wish to reduce political uncertainty (Kersh, 2002; Schuler et al., 2002). To do so, firms engage in multiple forms of nonmarket actions—CPA and CP—as this combination should assist them in these endeavors. However, the authors do not study the actual outcomes of this tendency in terms of access and influence; the impact of combining both CP and CPA needs to be explored in future research.

Furthermore, this study is based on U.S. firms and may not be generalizable to foreign contexts due to national variations in CSR and philanthropic expectations, and in demands for CPA transparency (for example, Faccio, 2006; Faccio, Masulis, & McConnell, 2006). In summary, this study reports a novel relationship between conditions existing in a firm’s political environment and CP; a finding that can shed new light on firms’ rationale for this important aspect of CSR.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no conflicts of interest with respect to the authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research and/or authorship of this article.