Abstract

With growth in the quantity of business ethics journals in recent years, assessments of journal quality are helpful to ethics researchers and administrators, as researchers consider available publication venues, and administrators consider the value of faculty research. The few published evaluations of business ethics journals have predominantly utilized two methods of journal quality determination: citation analysis and surveys of active researchers. This study employs a novel method to assess business ethics journals: 83 Association to Advance Collegiate Schools of Business (AACSB) business schools provided their internally developed journal lists (IDJ lists) that were used to evaluate faculty research, and the submitted lists were then analyzed for the presence and assessment of business ethics journals. This analysis yielded a ranking of 24 business-ethics-centric (BEC) journals, and this ranking reflects the collective judgments of AACSB business school faculties. The results of this study are pragmatic in that the journal evaluation data employed metrics actually used by business schools to determine the quality of business ethics journals. These findings also provide additional impetus for the recognition of business ethics as a distinct business discipline and business ethics research as a unique field of scholarly endeavor. While studies of business ethics may be influential when they are published in non-BEC journals, such studies may be more powerfully impactful when published in BEC journals.

The current channels for disseminating research are extensive, including informal “blogs,” formal presentations, and published books, monographs, and articles in journals. Whereas the quantity and monetary value of grants may be indicators of research quality in some academic fields, a measure of research quality often used in business schools is publication in the most prestigious journals. Correspondingly, journal quality assessment is important in the careers of researchers, as deans, department heads, colleagues, and other evaluators frequently consider the quality of the researcher’s publication outlets when making career-affecting decisions (Meredith, Steward, & Lewis, 2011). More broadly, the assessment of journal quality also affects perceptions of the overall faculty quality of a department, school, and university, as professors of those faculties do or do not publish in the highest quality, or premier, journals.

Compared to other business disciplines, the universe of business ethics journals is relatively small. The cross-disciplinary nature of business ethics yields a limited list of recognized top-tier journals, specifically Business Ethics Quarterly (BEQ), Business & Society (BAS), and Journal of Business Ethics (JBE), and a lack of definition and understanding of appropriate publication outlets beyond those three (Albrecht, Thompson, Hoopes, & Rodrigo, 2010; Paul, 2004; Wicks & Derry, 1996). As noted by Serenko and Bontis (2009), previous research that compares the quality of business ethics journals tend to be categorized as stated preference studies or revealed preference studies. Those studies in the latter category typically have analyzed citations of journals, and those in the former have surveyed ethics researchers. Although certainly informative and valuable, this previous research has not considered the application of assessed journal quality: Previous studies of the quality of business ethics journals have not incorporated the practical and realistic utilization of internally developed journal lists (IDJ lists) of business schools to evaluate researchers’ publications.

Primarily for purposes of assessing faculty performance for tenure, promotion, and periodic evaluations, many schools and departments of business at colleges and universities have established hierarchical IDJ lists that assign value to specific journals according to perceived quality. The IDJ list of a business school, consequently, may indicate that a specific journal is considered high, moderate, low, or unacceptable in quality and may assign letter assessments to evaluated journals, such as “A+, A, A–, B+” (Adams & Johnson, 2008). Construction of such internal lists may be a contentious and subjective process, as administrators and faculty attempt to influence placement or ranking of specific journals on the list. Although both administrators and faculty ostensibly would attempt to place the premier or best-quality journals on the departmental IDJ list in a rank that accurately reflects journal quality, both groups may be biased. Administrators may prefer journals with name recognition, perceived prestige, and a research direction that reflects their desire for the faculty publication future, instead of the faculty publication status quo. Faculty may have similar biases in constructing departmental IDJ lists but may also be influenced by the journals that have or have not published their own research or the research of colleagues (Van Fleet, McWilliams, & Siegel, 2000). Nonetheless, although business school IDJ lists may be an imperfect result of internal bias and debate, they are, arguably, one of the most important determinants of research recognition and career progress of a faculty member.

Accordingly, this article contributes to business ethics literature by adding an alternative view of the quality of business ethics publication outlets from an applied perspective, as the study focuses on business school IDJ lists and the practical assessment of journal quality used in actual academic environments. A second contribution of this project is the provision of a comprehensive set of journals specifically focused on business ethics.

In an effort to understand the assessment of business ethics journals, the IDJ lists of business schools that are accredited by the Association to Advance Collegiate Schools of Business (AACSB) were obtained and analyzed. This method of journal assessment has been used to assess journal quality in accounting (Reinstein & Calderon, 2006), information systems (Lewis, Templeton, & Luo, 2007), marketing (Steward & Lewis, 2010), and operations management (Meredith et al., 2010). This study is the first to utilize such IDJ list data in the evaluation of business ethics journals. As such, whereas previous measures of business ethics journal quality were based on citation analysis and researcher perceptions, this project contributes a practical application dimension to journal assessment, as IDJ lists of journal quality are mechanisms through which departmental journal assessments are applied to decision making.

As business ethics is a growing area of research and publication, an accurate assessment of the quality of journals of the discipline is helpful for ethics researchers, their deans and department heads, practitioners, and accrediting agencies (Choi, Kim, & Kim, 2009). Although the previous research described in the following section is unquestionably helpful in understanding journal quality, the technique for journal evaluation described in this article may be more practical in assessing the quality of business ethics journals. In Paul’s (2004) citation analysis of business ethics journals, she stated: Pragmatically, in order to gain tenure, each scholar in a university must identify appropriate peer-reviewed journals, acknowledged as legitimate by colleagues and receptive to the kind of work the scholar wants to accomplish. (pp. 103-104)

Paul may be correct in that a major consideration in many tenure and promotion decisions is the internal list of target journals that colleagues have constructed. This study utilizes those IDJ lists to assess the quality of business ethics journals.

Previous Assessments of the Quality of Business Ethics Journals

Many assessments and rankings of academic journals have been published, although relatively few have assessed those journals that publish articles related to business ethics. A chronological review of these previous, relevant studies begins with Wicks and Derry, who were the first to author an assessment of the quality of various business ethics journals. In this pioneering study, opinion surveys were administered to members of the Society for Business Ethics (SBE) who were considered active researchers in business ethics. Utilizing a mailing and a survey distribution at an SBE meeting, the authors obtained 34 responses and used that data to rank business ethics journals. As a result, the universe of publications was narrowed to 14 journals, some of which focused exclusively on business ethics and some of which were management journals that had published some business ethics research, such as the Academy of Management Review and the Administrative Science Quarterly. Correspondingly, the authors’ findings contrast the merits of publishing ethics research in management journals, which typically publish a wide variety of articles related to management, or in business ethics journals, which are more narrowly focused on business ethics issues (Wicks & Derry, 1996).

Although the work of Wicks and Derry (1996) was ground-breaking in evaluating business ethics journals, their work was somewhat confounded by two significant factors. First, the study suffered from three different response biases. One bias resulted from selection of their sample solely from members of the SBE, an organization whose business ethicists may or may not have chosen to join. A second response bias was to identify “active researchers” from the roster of SBE, using criteria that were not explained in the article. A third response bias was to survey members of the SBE who chose to attend a meeting of the organization. With a small response group of 34 respondents, such response biases cause concern about the representativeness of the findings. In addition, while the number of business ethics journals in the 1990s was smaller than in current times, the inclusion of management journals that did not exclusively focus on business ethics introduced another cause for concern, because it broadened the journal population to include one business discipline that is active in publishing business ethics research but excluded others. Several accounting and marketing journals, for example, publish business ethics research, but these journals were not considered in this research. If journal evaluation research is intended to extend journal rankings beyond just those journals that are business ethics centric, then journals in all business domains (accounting, finance, and marketing, etc.) should be included so that all potential outlets for business ethics research are examined.

In conducting a study that did not directly focus on the relative quality of business ethics journals, Sabrin used publications to rank the productivity of business ethics researchers. Although the focus of the study was individual ethics scholars and not their publication venues, Sabrin did identify the “top thirteen business ethics journals” for use in evaluating the researchers, although his method of identifying those journals was not explained in the article, nor did he attempt to differentiate the quality of those journals from each other (Sabrin, 2002, p. 357).

Paul (2004, p. 108) discussed the extant field of business ethics publications and judged BEQ, BAS, and JBE to be the “premier” journals of the discipline. Utilizing citation analysis of publication data of one year, 2001, she assessed the relative quality of those three journals and compared their volume of citations of articles to two management journals. Paul concluded that each of the considered business ethics journals had merit to various groups of readers.

Although Paul’s study is helpful in understanding citation frequency of three influential business ethics journals, BEQ, BAS, and JBE, the data utilized in her study are now more than a decade old, and the current pool of business ethics journals is significantly larger than the three considered in her article. In addition, the universe of journals outside the focus of business ethics that was used in her citation analysis was defined as two journals in the management field (Paul, 2004). As stated in the previous arguments, this constraint limits the population of potential business ethics outlets in a way that biases the results, since management scholars are not the only academics in business schools interested in business ethics and conducting business ethics research.

In another, more recent, citation analysis, Serenko and Bontis used three citation sources to rank business ethics journals and found strong correlations among those sources. In developing a group of journals to include in the study, the authors performed a search of a periodicals directory for journal titles that utilized the words “ethics” or “morale” and identified 20 journals for analysis. In addition to ranking the journals in their analysis based on citation analysis, the authors also assigned a “tier” to each, ranging from “A+” to “D” and attempted to place approximately 25% of journals within the “A+” and “A” tiers, 50% within the “B” tier, and 25% within the “C” and “D” tiers (Serenko & Bontis, 2009).

Whereas Serenko and Bontis (2009, p. 393) contended that the benefits of the citation analysis technique for journal quality assessment were “unarguable,” other authors have questioned the validity of the method and its use. Amin and Mabe (2000) indicated that the calculation of citation impact factors is somewhat arbitrary and ambiguous and such factors are largely affected by the subject, the type of journal, and the period of time over which the relevant data are gathered. Leydesdorff (2008) and Nisonger (2004) were also critical of citation analysis; both, for example, suggested that self-citation is a shortcoming of citation analysis as articles often cite other articles published in the same journal, thereby enhancing that journal’s citation factors. Nisonger also listed several other problems with citation analysis such as an absence of reliable citation data for many disciplines and a related inability to validly use citation data across an array of disciplines.

Last, the most recent study of the quality of business ethics journals utilized opinion surveys of active business ethics researchers. Albrecht et al. developed an internet-based survey instrument and invited, through email, survey participation of listserv members of five academic organizations, including the International Association for Business and Society (IABS) and the European Academy for Business in Society (EABIS). To focus survey participation, listserv members were asked to disregard the email if they were not actively engaged in business ethics research. Although the response rate of the study could not be determined, 280 survey responses were obtained. The respondents were exposed to a comprehensive list of journals that included 25 business ethics journals, and from this list, they were asked to identify and rank the top four business ethics journals. Data analysis revealed two materially different lists of journals: one ranked the top ten business ethics journals, and the other ranked the top ten journals that published business ethics research. While the former list included journals that were focused on business ethics, the latter list had several journals that did not focus solely on that one type of research. The authors also noted differences in the demographics of those who favored certain journals (Albrecht et al., 2010).

Although the study of Albrecht et al. (2010) is helpful in understanding several of the factors associated with the evaluation of business ethics journals, their work suffered from some of the same limitations as the Wicks and Derry (1996) article discussed previously. The findings of the Albrecht et al.’s article are limited by several forms of response bias, some of which were acknowledged by the authors. First, email messages were sent to members of the listservs of five academic groups, asking recipients to participate in the survey if they were active business ethics researchers. Although those five groups likely included many ethics researchers, there may have been many ethics researchers who were not members of those specific groups, and their exclusion could have biased the findings. Furthermore, some of the business ethics journals evaluated in the study were published by those five academic groups, and members of a group may be biased toward the journal published by their group. In addition, the authors had no basis for concluding that those who participated in the survey were active business ethics researchers; some of the five groups surveyed were not exclusively focused on business ethics and those who did choose to participate may not have been engaged in business ethics research. The authors also introduced bias in their results by asking survey participants to identify the top 4 business ethics journals from a list of more than 25 journals and then presenting 2 lists of the 10 most preferred journals in their article. The request to identify four journals may have been arbitrary; the two resulting lists may have differed if respondents had been asked to identify and rank their 3, 4, or 10 most preferred journals. The list of more than 25 journals presented to the survey participants also may have introduced a bias in that several of the presented journals, such as Administrative Science Quarterly, Strategic Management Journal, and Harvard Business Review, were not focused on business ethics and may not have appropriately represented the universe of journals that publish business ethics research. Finally, the Albrecht et al.’s study is limited by the same unavoidable shortcoming as other opinion-based journal assessments: Ethics researchers may be biased. This bias may be directed toward journals that have published researchers’ work, and, as argued by Serenko and Bontis (2011), bias may stem from journal familiarity, as when researchers have served as manuscript reviewers or editors for journals.

More important, studies that attempt to assess the quality of journals by surveying those scholars who have published or have attempted to publish in those journals have difficulty avoiding the bias of those surveyed. An alternative method of evaluating journal quality may be to examine departments’ and schools’ criteria for evaluating faculty publications, such as departmental IDJ lists, which have been vetted by the faculty members and administrators of schools and departments. The additional perspective and value of such a method may help to avoid the bias of individual researchers and consider, instead, the collective judgments of journal quality of those who established the departmental IDJ lists. Although such journal lists may be affected by the biases of individual faculty and administrators, the deliberative process of construction of such a departmental or school list by a group of scholars within the academic unit may mitigate, but not entirely eliminate, those biases.

Method and Findings

Accordingly, this study utilized IDJ lists of AACSB-accredited business schools to assess the quality of business ethics journals. The project progressed through two phases. In the first phase, journals were identified as being potential outlets for business ethics articles, and the relative standing of these journals was then determined. In the second phase, the potential business ethics journals from the first phase were subjected to further assessment to establish a set of business-ethics-centric (BEC) journals whose primary focus is on the field of business ethics. These journals were then ranked. Following an overview of the sources of data used in the study, the methodology and results from both phases are presented.

Multiple sources of data were employed in this study to (a) classify journals as being in the realm of business ethics, and (b) rank those business ethics journals. For this classification, the project utilized published studies of business ethics journals, websites of professional business ethics associations and publishers, the ISI Web of Knowledge, and information about the specific journals from their websites. In addition, business school IDJ lists were used to both help classify the journals and to create scores from which their ranks were determined. The data from the school target lists are described in the following sections, as using these lists is a new resource for evaluating business ethics journals.

AACSB School Survey

As noted previously, journal assessments are often a routine and integral part of important decisions made in academia, and many schools maintain IDJ lists to assist in these processes. Van Fleet et al. (2000, p. 340) noted, “A list provides an explicit measure of how a department values research outlets.” As such, journal rankings based on data from school IDJ lists reflect the actual state of journal standing employed in academia, which is the practical application of journal quality assessments. Although previous studies of some other business disciplines have utilized data from departmental journal lists (Lewis et al., 2007; Meredith et al., 2011; Reinstein & Calderon, 2006; Steward & Lewis, 2010), this type of information has not been used in research regarding the journals in business ethics.

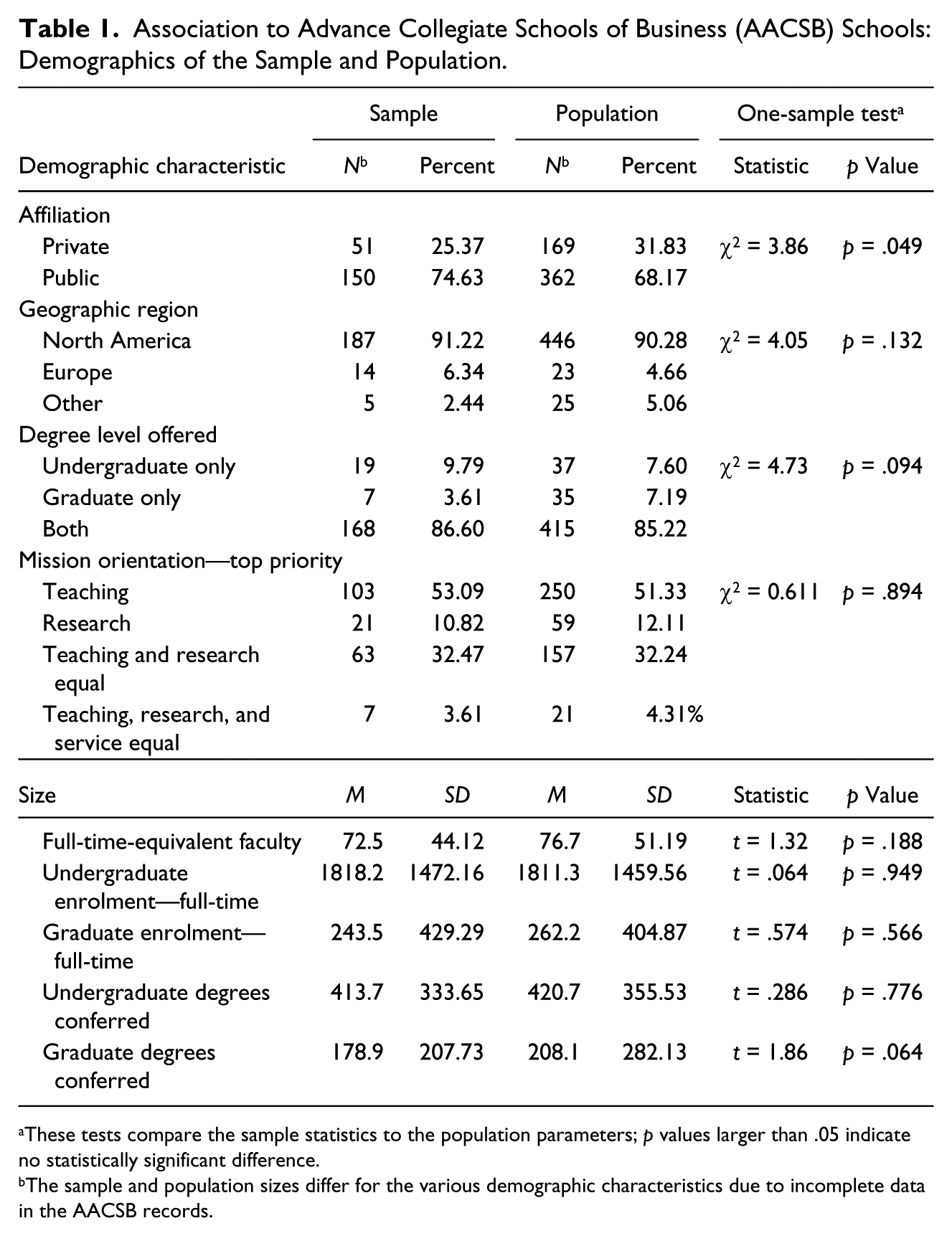

For the current study, IDJ lists that were formally used at AACSB-accredited business schools to assess faculty research were collected through the use of an email survey sent to the office of the business school dean or department head. Each AACSB-accredited school was asked to submit the IDJ list used for evaluating faculty publications at their school, if such a list existed, or to indicate that their school did not have a list. At the time of the survey, 545 institutions from around the world held AACSB accreditation, and 206 (38%) of these institutions responded to the request. The demographics of the responding schools are reported in Table 1 and are based on AACSB records. These records, however, had occasional omissions of data, and consequently, the population and sample sizes enumerated in Table 1 do not add to 545 and 206, respectively, in all circumstances. These sample demographics were compared to those of the population of all AACSB-accredited schools in order to determine the representativeness of the sample (see Table 1). One-sample chi-square tests were employed on the categorical demographic measures (affiliation, geographic region, degree level offered, and mission priority) to determine whether the sample differed from the population. Only one of these tests, on public/private affiliation, was significant at the .05 level, and only marginally so. For the continuous variables, which essentially relate to school size, one-sample t tests were utilized for the same purpose; no significant differences were found at the .05 level. Correspondingly, the sample appears to exhibit similar demographic characteristics to the population and is thus representative of the population.

Association to Advance Collegiate Schools of Business (AACSB) Schools: Demographics of the Sample and Population.

These tests compare the sample statistics to the population parameters; p values larger than .05 indicate no statistically significant difference.

The sample and population sizes differ for the various demographic characteristics due to incomplete data in the AACSB records.

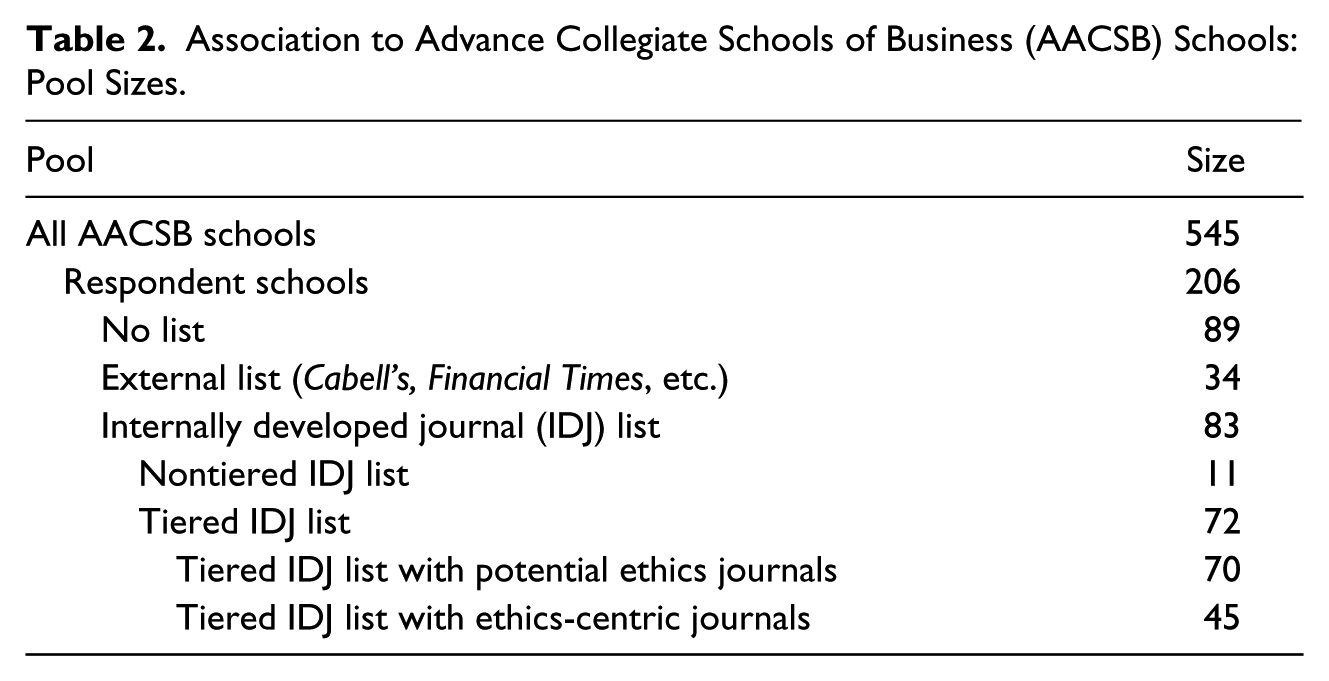

Of the 206 responding schools, 83 (40%) provided their departmental or school IDJ lists that those schools utilized in evaluating faculty research across all business disciplines, including business ethics. The remainder of the respondents included 89 schools (43%) that indicated they did not utilize any sort of journal list, 22 (11%) that employed Cabell’s Directory of Publishing Opportunities, and 12 (6%) that stated that they used external lists. Of these 12 schools that used external lists, 3 used the Financial Times list, and the other 9 used lists from other schools, such as Vienna University, or other published lists, such as the Harzing list. None of these external lists were used in classifying or assessing the relative standing of business ethics journals in this study (see Table 2 for a quantitative breakdown of the groups of schools used in this study).

Association to Advance Collegiate Schools of Business (AACSB) Schools: Pool Sizes.

Metrics Derived From the AACSB School Journal Lists

When IDJ lists are used by business schools, journals are often categorized in tiers based on their perceived quality. These school lists depict how journals are actually considered in practice at universities for decisions regarding tenure, promotion, annual review, and research awards, and so on. Given that journals are generally categorized at individual schools by their perceived value, the metrics derived from school IDJ lists serve as a reasonable depiction of journal standing from an operational standpoint (Van Fleet et al., 2000).

Of the 83 IDJ lists from the survey of AACSB-accredited schools, 11 did not present the journals in tiers (i.e., categories based on assessed quality), whereas 72 school IDJ lists did employ tiers (see Table 2). Using these tiered IDJ lists, four scores for each business ethics journal were computed: (a) the percent of times the journal was listed in the top tier across schools, (b) the percent of times the journal was listed in the top two tiers across schools, (c) the percent of times the journal was listed in any tier across schools, and (d) the weighted average mean percentile for the journal. The first three of these metrics are percentages based on simple frequency counts. Since the number of graded tiers differed among the schools in the sample, a mean percentile score was also computed for each journal at each school based on its assignment in the school’s graded tiers. This score took into account the number of tiers at the school, the total number of journals in that school’s tiers, and the tier placement of the given journal. All journals in the same tier at a given school were given the same mean percentile score for that school. These mean percentile scores were then aggregated across the schools in the sample by creating an average of the mean percentiles for each journal. The final weighted average mean percentile score was calculated by multiplying the average mean percentile by the number of schools listing that journal in one of their tiers (see the Appendix for a detailed description and example of this calculation).

The weighted average mean percentile may be the most comprehensive of the metrics derived from the school lists in that it considers a given journal’s tier placement at each school, the number of tiers at the school, the number of journals graded by the school, and the number of schools listing that journal. This metric may be the most appropriate metric for depicting actual journal standing in that it encompasses the most relevant information. As such, the journal rankings of the current project were determined from this weighted average mean percentile metric.

Potential Business Ethics Journals

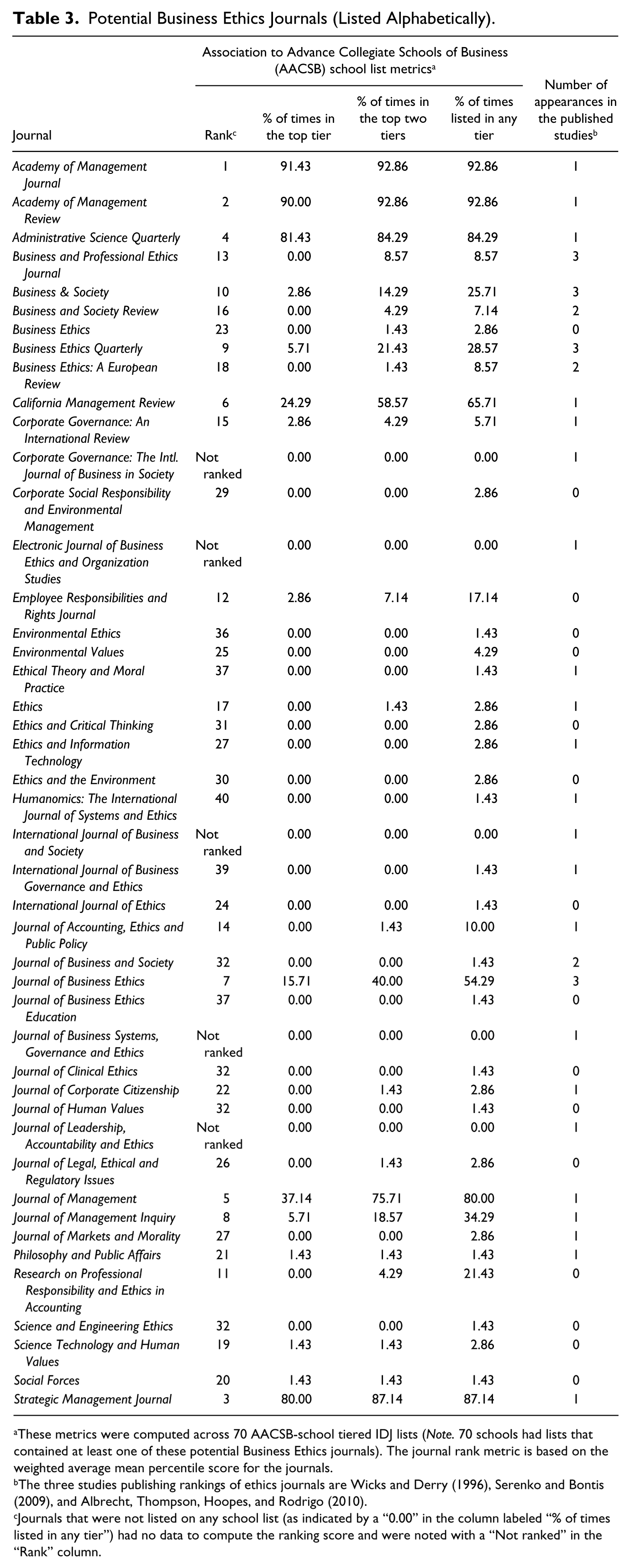

To establish whether a journal should be classified as a potential ethics journal, the following three criteria were applied: The journal was categorized specifically as an ethics journal on any of the AACSB school lists, the journal was included in either of the three published studies that ranked business ethics journals (Albrecht et al., 2010; Serenko & Bontis, 2009; Wicks & Derry, 1996), or the title of the journal, as listed in any category or discipline of the AACSB school journal lists, contained any one or more of the following keywords: ethic, moral, value, citizen, or “responsib.” The last keyword “responsib” was included to capture journals with the words “responsible” or “responsibility” or variations in the title. These keywords were derived by content analysis of the titles of journals listed by the following sources: the articles by Albrecht et al., Paul (2004), Sabrin (2002), Serenko and Bontis, and Wicks and Derry; the web sites for the Business Ethics Institute (BEI) and the Society for Business Ethics (SBE); and the ethics categories on the websites of the ISI Social Science Index and Springer Publishing.

If any one of these three criteria was met, the journal was considered to be a potential business ethics journal. In all, 70 tiered school lists contained journals that met these criteria (see Table 2). The resulting 45 journals that were classified as potential business ethics journals were then ranked based on their weighted average mean percentile score. Five of these journals did not appear on any of the school lists; therefore, no weighted average mean percentile score was available and they were not ranked (noted as “Not ranked” in Table 3). The results from this first phase are presented in Table 3.

Potential Business Ethics Journals (Listed Alphabetically).

These metrics were computed across 70 AACSB-school tiered IDJ lists (Note. 70 schools had lists that contained at least one of these potential Business Ethics journals). The journal rank metric is based on the weighted average mean percentile score for the journals.

The three studies publishing rankings of ethics journals are Wicks and Derry (1996), Serenko and Bontis (2009), and Albrecht, Thompson, Hoopes, and Rodrigo (2010).

Journals that were not listed on any school list (as indicated by a “0.00” in the column labeled “% of times listed in any tier”) had no data to compute the ranking score and were noted with a “Not ranked” in the “Rank” column.

BEC Journals

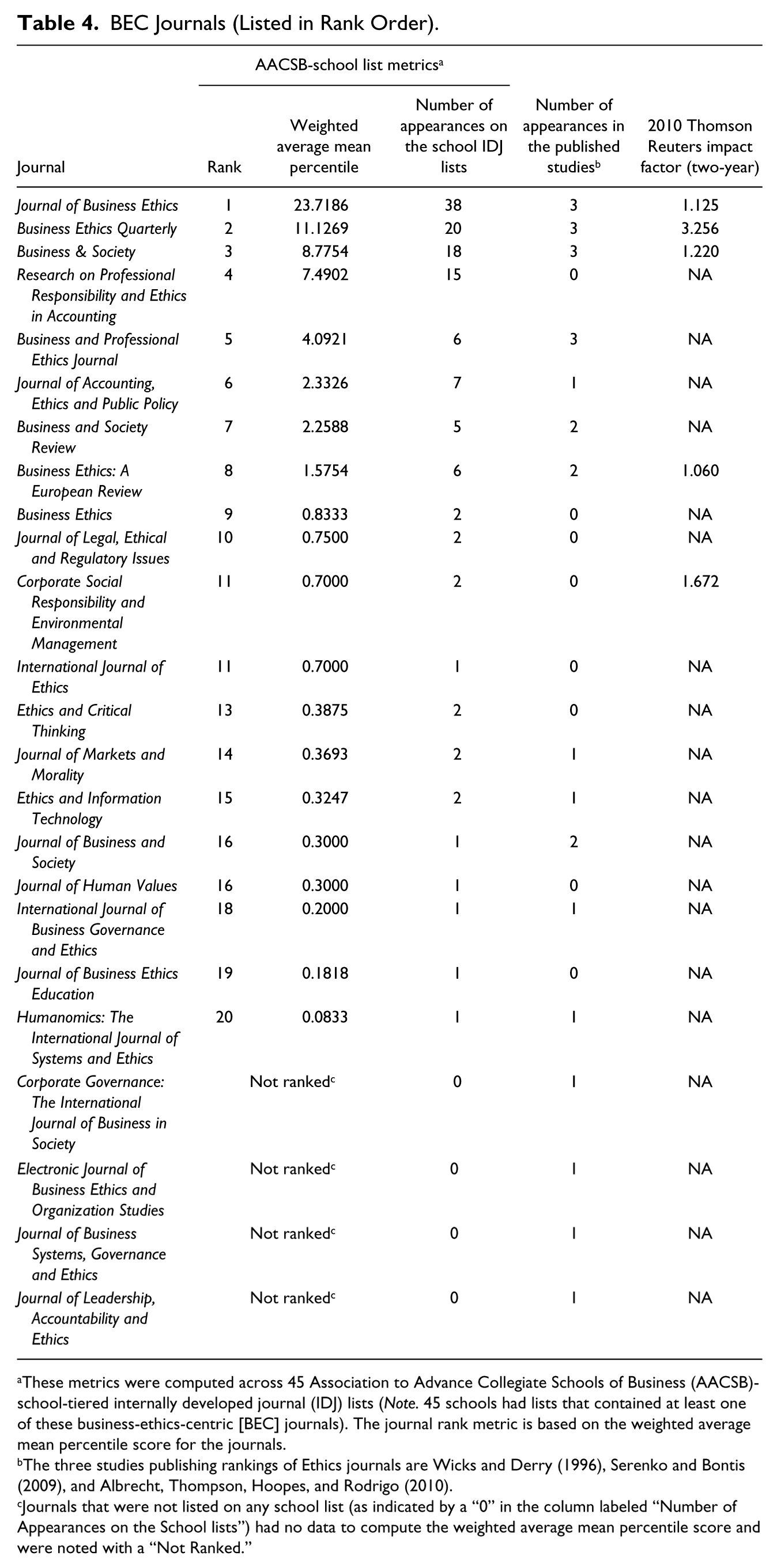

In the second phase of the methodology, the BEC journals were determined. Beginning with the list of potential business ethics journals, each journal was further scrutinized to establish whether it dealt predominantly with business ethics topics. To be considered a BEC journal, the authors decided that two criteria had to be met: (a) the mission statement of the journal reflected a primary concern with business ethics subjects, and (b) at least 20% of the published articles of the prior 3 years were about business ethics issues. Correspondingly, the mission statements of the 45 potential business ethics journals were examined as well as each issue of these journals for a 3-year period.

Twenty-four of the potential business ethics journals met both of the established standards and were classified as BEC journals. These 24 journals appeared on 45 of the IDJ lists from the survey of AACSB-accredited schools (see Table 2). The weighted average mean percentile scores of these journals were then ranked. Since four of these journals did not appear on any school list, there were no data to compute their weighted average mean percentile score and they were not ranked (noted as “Not ranked” in Table 4). The outcomes of this second phase are reported in Table 4.

BEC Journals (Listed in Rank Order).

These metrics were computed across 45 Association to Advance Collegiate Schools of Business (AACSB)-school-tiered internally developed journal (IDJ) lists (Note. 45 schools had lists that contained at least one of these business-ethics-centric [BEC] journals). The journal rank metric is based on the weighted average mean percentile score for the journals.

The three studies publishing rankings of Ethics journals are Wicks and Derry (1996), Serenko and Bontis (2009), and Albrecht, Thompson, Hoopes, and Rodrigo (2010).

Journals that were not listed on any school list (as indicated by a “0” in the column labeled “Number of Appearances on the School lists”) had no data to compute the weighted average mean percentile score and were noted with a “Not Ranked.”

Discussion

The survey of AACSB schools that served as the basis for the journal rankings in this study also offers insights into the use of IDJ lists among AACSB-accredited schools. In the sample responses, 57% of the schools reported that they employed a journal list of some sort: 40% used IDJ lists, 11% used Cabell’s, and 6% used lists from other external sources. All of the schools employing Cabell’s were located in the United States. Of the 12 schools that utilized external lists, 3 used the Financial Times list; 2 of these were U.S. schools and 1 was Norwegian. Fourteen of the 19 schools outside of North America (74%) employed IDJ lists. Of the 45 schools that rated the BEC journals (Table 4), 8 were from outside of North America. The three top journals based on data from these eight non–North American schools were the same as for the overall study; however, BAS was ranked as second among these eight schools, ahead of BEQ.

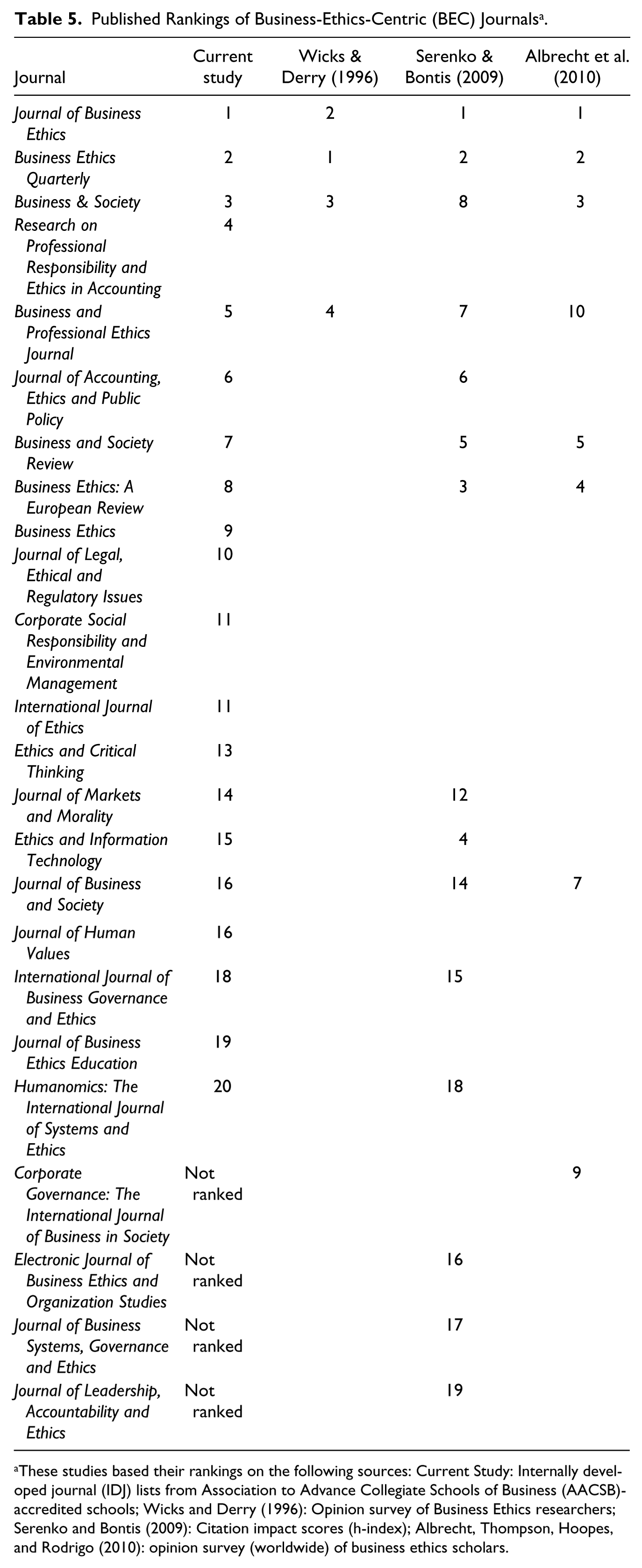

This study’s novel measure of publication quality yields several notable comparisons with prior rankings and assessments of research quality. First, Table 5 displays a comparison of rankings from three previous studies (Albrecht et al., 2010; Serenko & Bontis, 2009; Wicks & Derry, 1996) and the current study’s measure of journal quality. Of the three previous business ethics rankings studies, two are opinion surveys of business ethics researchers, and results of both of these studies indicated that respondents considered BEQ, BAS, and JBE to be the highest quality journals in the discipline (Albrecht et al., 2010; Wicks & Derry, 1996). Table 5 also includes a third previous study that utilized citation index analysis and found JBE, BEQ, and Business Ethics: A European Review to have the highest impact of business ethics journals (Serenko & Bontis, 2009). Since that publication, Thomson Reuters updated the impact factors of the most-cited journals of the social sciences in 2010, and these factors are included in Table 4 for the BEC journals. Only 5 of the BEC journals have an impact factor suggesting that the others were not among the 2,731 most-cited journals of the 2010 update. Notably, JBE, the BEC journal with the highest ranking in the 2009 study of impact factors, had the fourth highest impact factor of the BEC journals in the 2010 update. Three of the five BEC journals that had 2010 impact factors, including BAS and BEQ, had higher impact scores than JBE.

Published Rankings of Business-Ethics-Centric (BEC) Journals a .

These studies based their rankings on the following sources: Current Study: Internally developed journal (IDJ) lists from Association to Advance Collegiate Schools of Business (AACSB)-accredited schools; Wicks and Derry (1996): Opinion survey of Business Ethics researchers; Serenko and Bontis (2009): Citation impact scores (h-index); Albrecht, Thompson, Hoopes, and Rodrigo (2010): opinion survey (worldwide) of business ethics scholars.

With the exception of the Serenko and Bontis study, BEQ, BAS, and JBE have been consistently found by previous rankings studies and the current project to be the premier business ethics journals. This includes the Paul’s (2004) citation study discussed previously, which did not rank these three journals but presumed that they were the preeminent business ethics journals. Table 5, however, demonstrates that journal rankings after these top three journals vary widely from study to study (Albrecht et al., 2010; Serenko & Bontis, 2009; Wicks & Derry, 1996).

Considering possible quality differences among the three premier business ethics journals, BEQ, BAS, and JBE, an analysis of variance test on the tier averages and mean percentile scores from the school IDJ lists of the current study showed no statistical difference at the .05 level among these top journals. The top ranking for JBE in this study is primarily due to the large number of schools that included JBE on their IDJ lists. Notably, however, the presence of JBE as the only business ethics journal on the Financial Times list may have enhanced the visibility of JBE and introduced bias in its inclusion and ratings on the IDJ lists of the surveyed AACSB-accredited schools.

The analysis of this study, however, provides more than simply a third measure of journal quality. In a sense, this novel methodology helps to normalize the biases that limit the other two ranking methodologies. The quality assessment technique utilized in this article goes beyond ideological perspectives about quality to actual operationalization. The methodology of this study captures how the decision makers in many AACSB-accredited schools assess quality and operationalize it in their academic communities. Although deans, promotion and tenure committees, and other colleagues may be biased in some way, one of the ostensible reasons for constructing departmental lists of preferred journals is to minimize the effects of the biases of individual researchers and administrators.

A second stream of inquiry emanating from these results is whether to consider a broad array of journals, some of which occasionally publish business ethics research, or to limit assessment to BEC journals. A comparison of Tables 3 and 4 may inform this dialogue, as BEQ, BAS, and JBE are identified as the three premier BEC journals. These three journals, however, rank 9th, 10th, and 7th, respectively, when included in a list of broader business ethics publication outlets. Consequently, as some schools may limit recognition of quality research to publications in the top five, or even the top three, journals in a field, BEC journals may be dramatically undervalued when they are included in broader journal rankings (Serenko & Bontis, 2009). Clearly, promotion, tenure, and recognition decisions may be strongly influenced by the difference between publishing in a journal ranked 3rd in one’s field as compared to a journal ranked 10th. Understandably, deans and colleagues from other disciplines may rely heavily on journal lists to comprehend research quality when they are unfamiliar with journals outside their own area of expertise. Unfortunately, such broad journal lists that encompass multiple disciplines may be conveniently overutilized in evaluation of faculty research contributions by administrators and colleagues who cannot or do not take the time to read faculty research in the context of an entire publication stream or record (Serenko & Dohan, 2011; Suchan, 2008). Correspondingly, a lack of recognition of business ethics journals may cause misunderstandings of journal quality and unjust and inequitable results in decisions regarding annual evaluations, tenure, and promotions.

The results of this study also indicate that the rigor and visibility of BEC journals may be comparable or even superior to journals in other business concentrations such as accounting, management, marketing, or systems. In fact, if visibility and professional influence are a publication objective, BEC journals may be the preferred outlets. An examination of Table 3 reveals the inclusion of journals of several business disciplines. This inclusivity raises concerns that scholars conducting research about ethics issues in one discipline may be less likely to review resources outside their discipline than they may be to review articles in BEC journals which focus on ethics issues. Management scholars, for example, may be less likely to examine relevant, published ethics research in accounting journals, whereas scholars from all business disciplines may examine published research in premier BEC journals. BEC publications, therefore, that cross over business disciplines and influence interdisciplinary thinking about business ethics may be more visible and influential than journals focused solely on one other business discipline. This influence, consequently, may be the primary role of BEC journals. Correspondingly, if a school is relying on journal quality as an indicator of visibility and influence, BEC journals should be considered separate and apart from broader journal lists.

Previous research strongly advocated the development and utilization of a list of BEC journals and argued that such a list would signal maturity in this field of study (Paul, 2004; Serenko & Bontis, 2009; Wicks & Derry, 1996). In her review of the history of business ethics publications, Paul contended that business ethics became a clearly defined field of study beginning in the 1980s. Prior to that point, the discipline could be characterized as a diverse collection of scholars and their work from varied perspectives, including philosophy, sociology, and religion, as well as business concentrations such as marketing, accounting, and management. Since that time, the development and growth of several organizations and societies dedicated to business ethics and recent high-profile corporate scandals have fostered considerable growth in business ethics publications. The current study identified 24 BEC journals, and one of the contributions of this article is the methodical process used to develop this comprehensive list.

Due to the distinction of business ethics from other business fields, the depth of quality and influence in the discipline, and the broad readership and interest in business ethics, BEC journals should be designated on their own separate list and valued in the same way that business schools value other domains. This may be particularly necessary as the current study has revealed that BEC journals were less recognized in broader lists. Accordingly, the BEC journal list provided by this study and enumerated in Tables 4 and 5 may be an appropriate adoption of business schools that utilize such lists.

Limitations

Although this study introduces a new method of evaluating business ethics publications and utilizes a diverse sample, the population examined was limited to AACSB-accredited schools, which may not be representative of all schools in their assessments of journal quality. Furthermore, Table 1 demonstrates that this project included proportionately more public than private schools, and the latter may use somewhat different criteria to judge publication quality than public schools.

In addition, although journal rankings are not always significantly affected by region or geography (Serenko & Dohan, 2011), the global relevance of the current study is restricted, since slightly more than 90% of AACSB-accredited schools are located in North America. Although the sample of this project is representative of the AACSB population, the current study did not test for geographical differences.

A final limitation of the present study is the self-reporting of the surveyed schools. Business school representatives were asked whether or not they had a list for assessment of publication quality and, where they did, to provide that list. In response to this request, however, a dean or representative may have shared the internal list that a school espouses to use, but in actuality, other stated or unstated criteria may be utilized in tenure, promotion, review, and award decisions. The data used in this project, consequently, are limited to the espoused journal quality assessments of the surveyed schools that may or may not reflect the reality of how publications were actually assessed at those institutions.

Conclusion

Previous research regarding the comparative quality of business ethics journals utilized one of two methodologies: citation analysis or opinion surveys of active business ethics researchers. This article introduces a new approach to assessing business ethics journal quality, which uses publication quality metrics that are actually used by business schools in decision making about promotion, tenure, and faculty evaluation.

A second significant contribution of this article is a comprehensive list and ranking of BEC journals, which may be appropriately used to evaluate the quality of journals specifically dedicated to business ethics. This list was the product of a methodical process that yielded a ranking of 24 BEC journals. The study results support previous calls to utilize such a list in the assessment of business ethics research quality (Paul, 2004; Serenko & Bontis, 2009; Wicks & Derry, 1996).

Footnotes

Appendix

Acknowledgements

The support of the Association to Advance Collegiate Schools of Business (AACSB) during the data collection stage of this study is greatly appreciated.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.