Abstract

This dissertation abstract and the reflection commentary present the work of Dr. Rieneke Slager. The dissertation addresses the influence of Corporate Social Responsibility (CSR) metrics on responsible corporate behavior, through a case study of a prominent metric in the Socially Responsible Investment (SRI) market, namely, the FTSE4Good Index. This extended dissertation abstract introduces the research questions, theoretical framework, methods, and findings. The author’s views on successful completion of a PhD are discussed in the appendix.

Keywords

In recent years, a large number of rankings, ratings, and indices have been developed that attempt to measure the Corporate Social Responsibility (CSR) of companies. Substantive growth in the Socially Responsible Investment (SRI) market in the last two decades plays a major role in this development (Déjean, Gond, & Leca, 2004). To be able to invest in responsible companies, investors need to have a standard of measurement, or what the author terms a metric, which can be consistently applied in their decision-making process. Likewise, many academics interested in issues related to business and society have used CSR metrics to study the relationship between CSR and corporate financial performance. While most CSR metrics have attracted criticism on methodological grounds such as on issues related to their reliability and validity (Chatterji & Levine, 2006), they are nevertheless widely used by both academics and investors. However, little is known about the extent to, and ways in which, the metrics developed for the SRI market may contribute to improvements in CSR. Do these metrics simply measure CSR, or can they influence underlying responsible corporate behavior? How do those organizations being measured use these metrics themselves?

CSR metrics are often being dismissed as “box-ticking exercises” by critics, but they may be as powerful as they are controversial (Power, 2004). Research on rankings and league tables in higher education suggests metrics have a strong and lasting impact on organizational behavior and even on work content (Minzberg, 2004; Starkey & Tiratsoo, 2007). As the number of rankings increases, management scholars and sociologists have started to explore how such external metrics structure organizational fields (Sauder, 2008; Wedlin, 2007) and trigger organizational responses (Elsbach & Kramer, 1996; Sauder & Espeland, 2009). This research shows metrics induce reactivity: Organizations and individuals adjust their behavior in response to being measured and evaluated on aspects of their performance (Espeland & Sauder, 2007). Metrics elicit responses that may lead to them becoming constitutive of what is being measured. Due to the proliferation of metrics in organizational life and their capacity to produce intended or unintended organizational change, metrics deserve much closer attention (Espeland & Sauder, 2007). The study of CSR metrics is particularly pertinent. The rankings in higher education were never designed with the objective to change organizational behavior (Espeland & Sauder, 2007).

The stated aims of many SRI metrics however are not only to measure but to improve responsible corporate behavior (Sustainability, 2010). The author examines whether and how this improvement can be done by studying the FTSE4Good index, an SRI index launched in 2001 by FTSE Group, a major index provider in the global financial market with its headquarters in the United Kingdom. This study uses the institutional work perspective (Lawrence & Suddaby, 2006; Lawrence, Suddaby, & Leca, 2009) to study the practices of FTSE and related organizations aimed at creating and maintaining the institution of CSR through the development of the Index criteria. Using a mixed-methods approach, the author first examines how FTSE Group developed the FTSE4Good Index into a de facto standard for good CSR, showing how the Index becomes an integral part of international accountability standards that have emerged in the CSR field (Waddock, 2008). Three types of activities underpin this trend: first, the work by FTSE and social rating agency EIRIS to frame the index inclusion criteria and measure compliance; second, the process of engagement and dialogue with companies and third parties (e.g., Non-Governmental Organizations) by the FTSE Responsible Investment (RI) team; and third, the valorizing by companies and third parties of the index as a de facto CSR standard (Slager, Gond, & Moon, 2012).

The second part of the research examines the influence of the Index on the responsible corporate behavior of included companies. The engagement dialogue between the FTSE Responsible Investment (RI) team and the included companies is one of the main mechanisms to create reactivity, as it provides companies with an opportunity to obtain advice and guidance about the Index inclusion criteria. Archival data related to the engagement process, obtained through unique access to the FTSE Group archives, is collected and supplemented with interview, media, and quantitative data. This data set is analyzed using inductive qualitative, fuzzy-set Qualitative Case Analysis (QCA), and multivariate quantitative methods in a stepwise approach. The research findings show that, as the bar for inclusion in the FTSE4Good Index is continuously raised, the commensurate improvement in responsible corporate behavior depends on the level of engagement and symbolism used by affected companies, as well as the sophistication of their CSR measurement and reporting routines.

The study provides a fresh perspective on the measurement of CSR by highlighting the sociological elements involved in measurement processes. The study shows that the institutional work of different actors and organizations is related, and leads to differences in organizational responses. Furthermore, the author theorizes the influence of material artifacts on reactivity, highlighting a gap in current studies of metrics. The study has implications for those seeking to govern by metrics (Miller & Rose, 1990), as it shows how striking a balance between what can be measured and what ought to be measured is complicated and requires a lot of work. Last, the research opens up a number of venues for future research into CSR, SRI, and institutional work.

The abstract is structured as follows. The next section will briefly describe the core theoretical underpinnings of the research and its key research questions. The subsequent section introduces the mixed-methods methodological approach used in the study. Finally, the author describes the findings in two sections, concluding with implications for future study.

An Institutional Work Perspective on SRI Indices

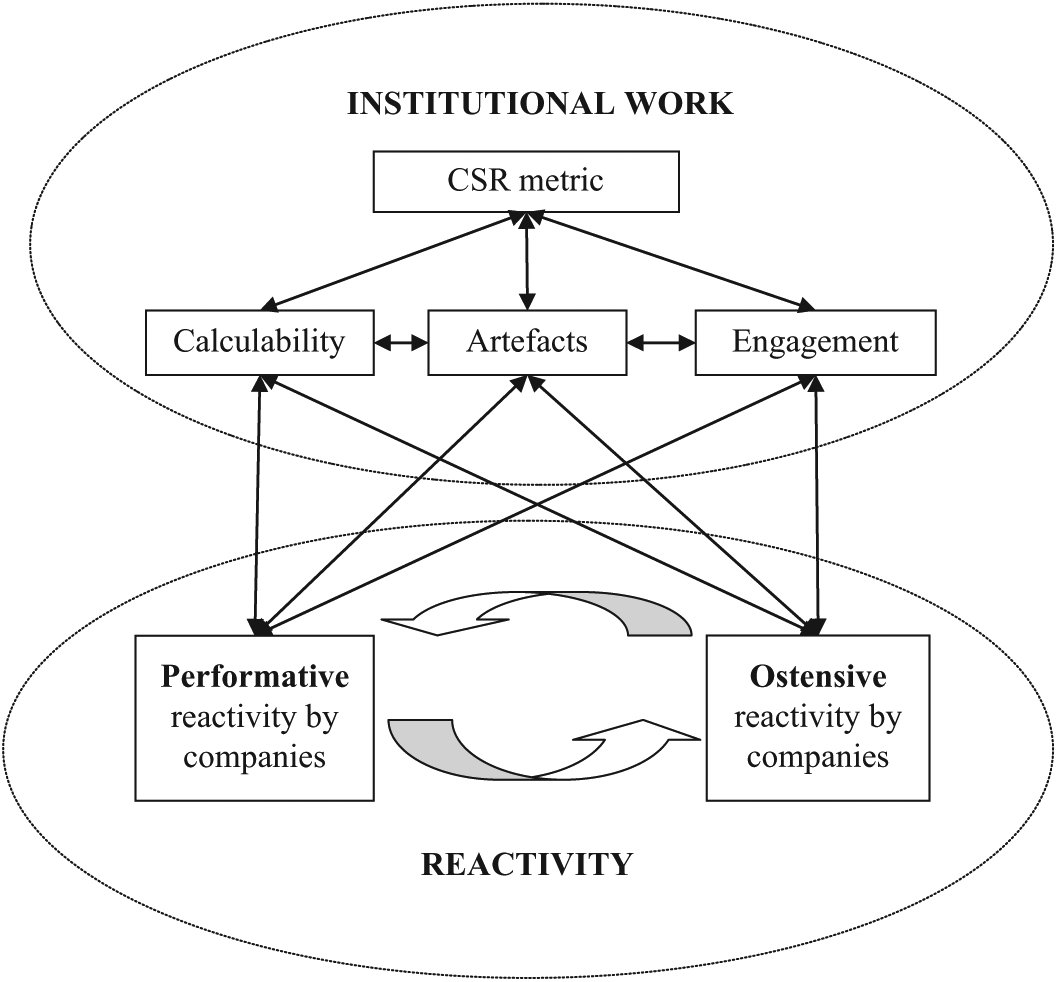

The research uses a theoretical perspective that is anchored in institutional theory, which provides the opportunity to examine the interaction of organizations with their environments, thus providing a more holistic picture of CSR (Campbell, 2007). Specifically, the research draws on theoretical concepts that have been specified in recent studies on institutional work (Lawrence & Suddaby, 2006; Lawrence et al., 2009). The concept of institutional work allows for an examination of the dynamic nature of institutions and the recursive relationship between institutions and organizational practices (Lawrence, Suddaby, & Leca, 2011). Additional theoretical perspectives stemming from the social studies of finance (Callon & Muniesa, 2005; MacKenzie, 2009) and organizational routines (Feldman & Pentland, 2003; Pentland & Feldman, 2005) are also used. Last, the research draws on evidence provided by studies of rankings in the field of education, which, in contrast to SRI indices, have attracted critical examination in a number of studies (Espeland & Sauder, 2007; Sauder & Espeland, 2009). Figure 1 depicts the key theoretical concepts used in the study and their interactions. The following section will discuss each concept and their application in the research.

Institutional work for reactivity.

To study the work underlying the creation and maintenance of CSR metrics, the author relies on the concept of institutional work, which aims to study the purposive action of individuals and collective actors aimed at creating, maintaining, or disrupting institutions (Lawrence et al., 2009, 2011; Lawrence & Suddaby, 2006). The umbrella concept of institutional work allows for a study of different types of work that draws in closely related theoretical perspectives. The relative flexibility of the concept of institutional work allows for an integration of theoretical perspectives that pay more attention to the interaction between cognitive aspects of institutions, material objects, and organizational practices. Institutionalization depends to a large extent on “mundane administrative arrangements” and routine practices that can accommodate institutionalized norms and values (Kraatz, Ventresca, & Deng, 2010; Selznick, 1957). Similarly, artifacts and material objects have received relatively little attention in the literature on symbols and rituals in institutionalization, which has relied in the main on the linguistic approaches to study symbolism. However, institutions are material as well as symbolic, and integrating a more nuanced perspective on artifacts will illuminate their interaction with institutionalized practices (Sillince & Barker, 2012).

Calculability forms a key part of the institutional work underlying CSR metrics. Calculability is broadly defined as a process of “isolating objects from their context, grouping them in the same frame, establishing original relations between them, classifying them and summing them up” (Cabantous & Gond, 2011; Callon & Muniesa, 2005, p. 1232). Thus, calculability refers not only to the nature or content of mathematical calculations but also to the human interaction, cognitive models, and material objects needed to ensure the circulation of calculated numbers in markets. It is a constructivist, situated notion that acknowledges the truth of numbers is constructed in an interactive process, but that the efforts of the calculative work become invisible when numbers become widely diffused and taken-for-granted.

Calculability also has a material dimension. Metrics are likely to become taken for granted as commensuration gets built into practical organizational structures of labor and resources (Espeland & Stevens, 1998, p. 329). Artifacts are thus likely to play an important role in the institutional work underlying CSR metrics. Last, calculation is viewed as a type of institutional work that is distributed between individuals and organizations that co-operate in creating and maintaining a metric. This is a potentially powerful form of institutional work. In their study of the French SRI market, Déjean et al. (2004) attribute a central role to the organization, which sets the measurement criteria and undertakes calculation based on the supplied information, because of its systemic power to set (and change) the categories and criteria for measurement. The concept of engagement is used to study the interactions between the organization creating the metric and the organizations that are rated through the metric.

The application of the concept of reactivity to the study of metrics shows that reactivity could potentially be harnessed to achieve changes in organizational behavior (Espeland & Sauder, 2007). It focuses the attention on the intended and unintended consequences of the rise in measures that hold organizations accountable, which are increasingly public in nature (Power, 1997). In this research, the concept is used to examine the changes in organizational behavior that are made to conform with, or even excel in, the evaluation as carried out by an external agency, such as those agencies that provide information on which SRI indices are based. Viewed from an institutional perspective the effects of reactivity may range from a symbolic response that emphasizes gaming strategies to a more substantive response that sees internalization in organizational routines. Little is known however about the organizational practices that mediate the tension between these two extremes (Ansari, Fiss, & Zajac, 2010). While studies of metrics and reactivity have shown that the redistribution of resources and reorganization of work are consequences of reactivity (Power, Scheytt, Soin, & Sahlin, 2009; Sauder & Espeland, 2009), these studies have not generally examined in detail the work that is needed to participate in ratings, or the work that the rating organizations undertake to engage rated organizations.

To examine the impact of institutional work on organizational behavior, the concept of reactivity provided by Espeland and Sauder (2007) is extended based on dynamic routine theory (D’Adderio, 2008; Rerup & Feldman, 2011). Recent insights in routine theory suggest that routine practices consist of artifacts, ostensive, and performative elements (Feldman & Pentland, 2003, p. 95). The ostensive element relates to the overarching structure and pattern of activities; the performative element is the performance of routine practices by organizational actors (Feldman & Pentland, 2003; Pentland & Feldman, 2005). The difference between the ostensive (abstract pattern) and performative (specific actions) creates dynamism. Viewed in this way, the routine practices that mediate between symbolic management of institutional pressure (performative routine activity that might not be embedded into ostensive reactivity) and substantive management (where performative and ostensive elements are in balance and aligned) can be studied.

The research aims to answer two sets of research questions. The first set of questions focuses on the institutional work underlying the creation and maintenance of CSR metrics. How did FTSE, as a traditional index provider, manage to establish and maintain an SRI index? What practices did FTSE use, and which other organizations and actors were involved? Why have SRI indices become so popular, especially among companies listed on them? This set of research questions looks at the institutional work (Lawrence & Suddaby, 2006; Lawrence et al., 2009) undertaken by various actors. This study of the FTSE4Good index allows for an examination of the work done by various organizations that might result in reactivity on the part of the companies included in the Index.

The next set of research questions focuses on the impact of this institutional work on organizational behavior. How and to what extent does being listed on the FTSE4Good Index affect responsible corporate behavior? What type of changes, if any, do companies make in reaction to being measured and included in the Index? What are the mechanisms whereby this impact is channeled? Grounded in the theory and data of the case, the concept of reactivity is further developed to encompass both the actions of companies as they adjust CSR practices to comply with the FTSE4Good inclusion criteria, and the development of deeper shared understandings of the importance of good CSR practices that are mediated through index inclusion and engagement by the FTSE RI team. The research takes a comparative approach to capture the differences in the organizational responses to Index inclusion and hypothesizes the main mechanisms by which reactivity is channeled.

Method

The main concern of the research lies with the way in which the activities related to SRI indices influence organizational behavior; therefore, it does not seek to answer questions of a more technical nature, such as those related to whether SRI indices effectively measure CSR. A definition of CSR is context dependent (Matten & Moon, 2008). As such, this research will not attempt to define what CSR is but take as a starting point the measurement process by the FTSE4Good index. This approach is justified on pragmatic and conceptual grounds. Most SRI indices continue to measure different aspects of CSR. This variability is unlikely to change in the near future as the differentiation of the various SRI indices in the market depends on their distinctive inclusion criteria and ways of measuring CSR. At a more conceptual level, the research on university rankings and league tables has shown that these external metrics shape organizational perceptions and identities, regardless of questions regarding the quality and content of their underlying methodology (Sauder, 2008). Even flawed metrics still have an impact on organizational behavior, as long as they are credible: “It is critical to acknowledge that we often choose measures based on their credibility more than their efficiency or validity. It matters not if we have valid measures if no one believes them” (Mitnick, 2000, p. 420). Therefore, the definition of CSR or responsible corporate behavior is grounded in the process of creation and maintenance of the FTSE4Good Index, and not given a priori.

Case selection

The term SRI refers to investments made based on considerations of financial returns, as well as extra-financial considerations, such as concerns regarding the ethical, religious, social, governance, or environmental impacts of the entities that investors are looking to invest in (Kurtz, 2008). SRI investors need metrics that allow them to make a judgment of the CSR “quality” of corporate stocks. An SRI Index is a weighted listing of stocks that is constructed by filtering a broader universe of stocks according to a set of social, environmental, or corporate governance criteria. Common examples include the Dow Jones Sustainability Index (DJSI), the Domini 400 Social Index, and the FTSE4Good Index.

The FTSE4Good Index was launched in 2001 to measure up the environmental and social performance of companies listed on stock exchanges worldwide. The data regarding social and environmental performance were provided by the social research agency EIRIS during the period under study. The information is collected based on publicly available information in company reports and webpages, and supplemented with information directly provided by companies. The Index is managed on a day-to-day basis by a specialized team of FTSE staff members, named the Responsible Investment (RI) team, in collaboration with a number of third parties. The FTSE4Good Index uses a dual strategy of continuously raising the bar for company inclusion through the introduction of new inclusion criteria, followed by an invitation for dialogue and engagement that is extended by the FTSE RI team to companies under threat of exclusion. In the engagement process, companies have the chance to provide evidence to show they are working toward meeting the criteria. The FTSE4Good Policy Committee ultimately decides whether a company should be removed from the Index after this period of dialogue and engagement.

The creation of the FTSE4Good Index series in 2001 can be seen as an extension of the general FTSE brand into the SRI market. The concept of institutional work is particularly suited to study the legitimization process that takes place when an organization wants to extend its activities to a new field (Durand & McGuire, 2005). The FTSE4Good Index presents an ideal case to observe the emergence of an index and is a window on institutional work “in the making” due to the objective to develop continuously new inclusion criteria to cover an increasingly wide array of aspects related to responsible corporate behavior (FTSE, 2010). This condition effectively creates a moving target for included companies. It also means the Index is almost constantly in flux, which provides a unique opportunity to study the dynamics of institutional work in practice. The engagement undertaken by the FTSE RI team is another distinguishing feature of the FTSE4Good Index. These features of the Index and its relative longevity in the SRI market present significant research opportunities that make the FTSE4Good an ideal case for the case study.

Data collection and analysis

The mixed-methods approach in the study is well suited to the two sets of research questions. The first set of research questions requires a qualitative study of actors’ understanding of the context in which the FTSE4Good Index was created and continues to develop. This qualitative understanding is used to develop and enhance the theoretical framework that is outlined in Figure 1, so that it is grounded in theory and data. The framework is then tested in a larger sample of corporations included in the FTSE4Good Index. The research relies on unique access to multiple data sources: interview data, in situ observations, archival material from FTSE, several secondary data sources, and a database provided by research agency EIRIS.

Observations

The FTSE premises were visited several times a year to conduct observations of Policy Committee meetings, and to gather data. In total, around 12 weeks were spent at the FTSE Group over a period of 3 years, during which frequent informal conversations with the FTSE RI team members confirmed many of the insights of the interviews and helped weigh the value of interviews and archival data during the data-coding process.

Interviews

Four categories of informants have been interviewed: those involved with day-to-day management of the Index, those involved with the research underlying the Index, external CSR consultants, and managers of 30 companies included in the Index. Several informal follow-up interviews were conducted throughout the research period with FTSE RI team members, to test and confirm emerging insights. In addition, interviews with four members of the Policy Committee, which oversees the governance of the Index, and two interviews with EIRIS researchers were conducted.

Archival material

Four categories of archival material were consulted. First, publicly available information published by FTSE was consulted, including several progress reports and semi-annual updates of company exclusions and inclusions from the Index. Second, the minutes and papers of the Policy Committee meetings were reviewed. Papers proposing changes to the Index criteria and its constituents are prepared by the RI team for assessment by the Policy Committee and voted on in the semi-annual index review meetings. These materials were studied for the period from 2001 through to the end of 2010 (totaling more than 650 pages). As noted above, the Policy Committee meetings were observed from 2008 to 2011, which helped contextualize the archival material. Third, correspondence between the FTSE RI team and corporate managers was studied. This included 239 letters for the period from 2003 to 2010, and more than 500 emails that were examined in detail. Fourth, a database was created that listed company scores on the inclusion criteria for the period 2001 to 2010. These data were gathered from the FTSE archives.

EIRIS database

A database containing research on CSR performance of companies worldwide was purchased from research agency EIRIS. The database represents an unbalanced panel of between 2,300 and 2,900 companies for the period 2003 to 2010. In addition to the research on which the FTSE4Good index is based, this database contains information on a wide variety of other CSR issues. The information related specifically to corporate systems and policies for countering bribery and corruption is analyzed in the final part of the research.

The collected data are analyzed with a stepwise approach, moving from qualitative, inductive analysis methods to increasingly structured, comparative, and quantitative methods. The first step is familiarization with the research setting, to understand the main processes and activities taking place in the setting, and to elicit perspectives and viewpoints from the various research participants. Triangulation is achieved by moving between the different sets of data. In a second step, the data set is coded and analyzed through Qualitative Case Analysis (QCA), a comparative method, used here to analyze different response of companies included in the Index. A final step uses multivariate analysis to test whether the conditions and concepts identified through the qualitative and QCA analysis are significant for a larger number of companies.

The research sets out to answer two core research questions. First, what is the institutional work that is needed from all involved parties to create and maintain the FTSE4Good Index? Second, how and to what extent does this institutional work channel reactive organizational responses to the Index? In the following two sections, the research findings related to these two questions are discussed.

Findings 1: The FTSE4Good Index as a Standard for Responsible Corporate Behavior 1

The analysis of the institutional work of Index creation and maintenance shows that a wide range of political, normative, cognitive, and material practices are involved in turning the FTSE4Good Index into a standard for responsible corporate behavior. These practices are clustered into three types of institutional work: calculative framing, engaging, and valorizing.

The work of calculative framing involves defining and calculating the rules that frame the practices of eligible members of the Index. It entails defining the appropriate attributes of “good CSR,” rendering these aspects visible to external inspection and opening up the possibility of sanctioning non-compliance (Brunsson & Jacobsson, 2000). The research findings show how a system of measurement can play a key role in institutionalization processes (Hasselbladh & Kallinikos, 2000). By building on existing international standards regarding aspects of CSR such as human rights or labor standards, the FTSE4Good Index standardizes and diffuses prevailing norms regarding what constitutes responsible corporate behavior in the international domain.

Engaging is summarized as work that serves to create the knowledge and expertise needed to legitimate the Index and monitor the behavior of the included companies. The engaging work is constituted of the work of acquiring expertise on subject matters related to CSR, labeled here as convening, as well as the work needed to disseminate the acquired knowledge to the companies in the Index, labeled here as educating. The engaging work serves an important role in the institutionalization of new CSR practices that are framed through the Index, as it provides companies with the resources and support that are needed to implement new practices (Lounsbury, 2001). The research findings confirm that organizations which create metrics may also aid diffusion processes (Sauder, 2008; Wedlin, 2007). However, the findings also point to the fact that calculative framing needs to be accompanied by engagement work to be successful.

Valorizing is the third type of institutional work identified, and refers to the infusion of values beyond the technical requirements (Selznick, 1957) of the Index. The normative associations of third parties and companies have shifted from regarding the Index as purely a market instrument for SRI investors to it also being a standard for good CSR. The shift in normative associations related to the FTSE4Good Index is supported and encouraged through the creation and circulation of artifacts such as the FTSE4Good logo and certificate of inclusion. Of the various groups of actors involved in valorizing work, companies in particular welcomed the creation of SRI indices such as the FTSE4Good and the Dow Jones Sustainability Index. They recognized that the SRI indices would be able to provide signals to investors regarding the quality of CSR practices, an area in which corporate capabilities are hard to evaluate and company self-assessment is often regarded as not credible. As such, the SRI indices have become part of the assortment of codes, standards, and governance initiatives that Gilbert, Rasche, and Waddock (2011) refer to as “international accountability standards”: voluntary predefined rules, procedures, and methods to systematically assess, measure, audit, and/or communicate the social and environmental behavior and/or performance of firms (Gilbert et al., 2011, p. 25).

The research findings show that multiple types of institutional work are needed in the creation stages as well as the maintenance stages. This multiplicity is particularly pertinent in the case of the FTSE4Good Index due to its objective to raise continuously the bar for inclusion. The dynamic created by the different types of institutional work shapes the reactivity of companies included in the Index. This dynamic process of institutional work is never completely finished, as it relies on constant innovation in criteria and the continuous interaction between the different types of work. As such, participation in the institutional work on the part of companies will also be dynamic. The next section discusses the findings related to corporate participation in the institutional work and the impact of this participation on the reactivity toward the Index inclusion criteria.

Findings 2: Dynamic Reactivity Toward the FTSE4Good Index

The research shows that while the institutional work of calculative framing requires significant resources on the part of FTSE and involved third parties, it is also dependent on the calculative work undertaken by companies with regard to measuring and reporting their CSR performance. This calculative work relates to the routine intra-organizational practices of collecting relevant information, aggregating it in accordance with commonly accepted metrics, and reporting the results to interested parties both within and outside of the company. The calculative work that precedes the reporting may be largely hidden from view but may nevertheless be shaped by, and respond to, external calculative framing such as that underlying the FTSE4Good Index. External metrics create the need to establish within organizations a “calculative infrastructure” (Cabantous, Gond, & Johnson-Cramer, 2010) that may involve new routines or the transformation of existing routines for calculation. This powerful effect has been referred to as “action at a distance” in governmentality studies (Latour, 1986; Miller & Rose, 1990): a form of action that is brought about through seemingly mundane practices such as calculation, which allows information to be gathered through intricate networks of participating organizations and individuals. Participation in these networks relies neither on brute force nor on persuasion, but on the gradual alignment of interests through the use of shared frames of reference, metrics, and language among participants.

The results show that reactivity may take place at the performative and ostensive level. Performative reactivity refers to the creation or adjustment of CSR policies, management systems, or reporting practices that are in line with the inclusion criteria. Ostensive reactivity refers to the creation or adjustment of shared understandings on the meaning of those CSR practices. The tension between these two levels of reactivity may be mitigated through symbolic work, for example, using the FTSE4Good logo to signal the quality of CSR practices to various audiences (expressive symbolic work) or to create leverage to change or improve CSR practices internally (instrumental symbolic work).

The research findings show how inclusion in the FTSE4Good index requires routine connections (Feldman & Rafaeli, 2002) between companies, FTSE, and rating agency EIRIS, as well as connections between different departments within the included companies, to collect and monitor data on CSR practices. These routine connections may be firmly embedded within corporate systems and structures in some cases, to the extent that they become integrated in other organizational routines such as personal performance measurement. In other cases, the lack of fit between existing corporate calculative routines and the calculative framing of the index triggers responses ranging from adaption of corporate practices to highly resistant and reflexive attitudes. The artifacts created by Index inclusion, such as the FTSE4Good logo, may be used simply to summarize CSR practices and signal its quality, or may be used more extensively and instrumentally to achieve fit between corporate practices and the index inclusion criteria. The potential for (mis)fit between organizational calculative practices and the external framing of the index is dynamic (Ansari et al., 2010), in that it may change over time due to learning effects and may vary across the specific areas that are being measured, for instance, calculations of environmental performance versus social areas of concern.

The engagement work by the FTSE RI unit provides a platform for information exchange that leads to shared understandings about the importance of “good CSR.” The results of the QCA analysis confirm that engagement, symbolic work, and calculative routines are important elements of the institutional work that maintain the index as a standard for good CSR. Fuzzy-set QCA is used to the data related to the 30 case companies to analyze the conditions under which reactivity occurs. The reactivity toward the Index inclusion criteria is most prevalent for companies that have been in engagement and undertake the symbolic work that is associated with being included in the index, such as display of the FTSE4Good logo. Tracking improvements in CSR scores in the database of social rating agency EIRIS, the results show that companies that are in engagement with the FTSE RI team and also use symbolic work show reactivity toward the Index criteria—they improve their CSR scores in line with the criteria. This action ensures they do not get deleted from the Index. There are various paths to reactivity though, as some companies react without being directly engaged and others resist engagement and show no or limited reactivity. As the Index sets its criteria at the level of “good practice” rather than “best practice,” the CSR practices of some companies exceed the benchmark set by the criteria, and the Index has limited influence in these cases.

The final step uses multivariate analysis to test whether the conditions and concepts identified through the qualitative and QCA analysis hold for a larger number of companies. The author studies the effects of the introduction of new Index criteria on countering bribery in 2006. 2 Data are collected from FTSE and EIRIS databases, as well as corporate documents. The sample includes 254 companies operating in environments with a high risk of corruption. The findings show that, even when controlling for various aspects of firm financial performance, companies in engagement are more likely to have high-quality corporate practice for countering bribery and corruption, in the year following engagement. These effects are strongest for engagement that has a medium level of intensity, taking place over a period of 7 to 15 months. Companies that use the logo of the FTSE4Good index to signal the quality of CSR practices to external audiences, and companies that use Global Reporting Initiative (GRI) reporting guidelines (as a proxy for calculative routines), are also more likely to have good countering bribery practices.

Conclusion

While engagement has become a more popular strategy for responsible investors in recent years, there is limited academic research on the impacts of engagement on organizational behavior. In addition, little is known about how metrics for responsible investment, such as SRI indices, are used within companies to achieve organizational change. The research has filled these gaps in the literature through a mixed-methods case study of the FTSE4Good index. The research findings show how a system of measurement can play a key role in institutionalization processes (Hasselbladh & Kallinikos, 2000). By building on existing international standards regarding aspects of CSR such as human rights or labor standards, the FTSE4Good index standardized and diffused prevailing norms regarding what constitutes responsible corporate behavior in the international domain. The engaging work serves an important role in the institutionalization of new CSR practices that are framed through the Index, as it provides companies with the resources and support that are needed to implement new practices (Lounsbury, 2001). The research findings show the supporting role of material artifacts in symbolic work and highlight that symbols may be used not just to represent commonly shared meanings but also to influence patterns of action (Gioia, Thomas, Clark, & Chittipeddi, 1994).

Several distinct contributions are made. First, the analysis shows behavioral, cognitive, and material aspects all play a role in reactivity. Guided by concepts developed in dynamic routine theory (D’Adderio, 2008; Pentland & Feldman, 2005), a more dynamic theorization of reactivity is developed. This dynamic theorizing allows exploration of reactivity in further detail, because it points to the practices that constitute reactivity over time and their connection to cognitive ideas and material artifacts. Furthermore, the results show that organizational responses to ratings, metrics, and certification are not as homogeneous as is often assumed (Graffin & Ward, 2010). Second, the research has also provided insights into the measurement of CSR, by providing a fresh perspective based on a sociological model of measurement and its effects. It reinforces the view of Mitnick (2000) that it does not matter whether metrics such as SRI indices effectively measure CSR, but what is important is that they are credible measures. The analysis shows how a metric may become valorized as setting a standard for good CSR. Third, the study contributes to the understanding of embedded agency and its relationship with institutional work, by highlighting the interaction effects between different types of institutional work, and by reconceptualizing agency to include sociomaterial artifacts.

Previous studies of metrics, such as law and business school rankings, have often emphasized the negative effects of rankings on organizational practices, such as gaming strategies (see Gioia & Corley, 2002). In contrast, rather than emphasizing only the constraints exerted by metrics, this study has focused on the way the disciplining force of metrics may be used as a force for good. The results show how metrics such as SRI indices may be used to incentivize and encourage responsible corporate behavior. Several caveats need to be taken into account by organizations and public policy makers seeking to make more use of metrics in governing organizational behavior. The study shows creating and maintaining a metric is not a simple task. It requires the careful balancing of different types of activities and their consequences for governing behavior. The credibility of the metric relies on the participation of the organizations being measured and is therefore often reliant on what can be measured as much as what ought to be measured. This problem is particularly relevant for metrics in the area of CSR where what can be measured is still very much determined at the discretion of companies. Governing by metrics should take a longitudinal approach, which encourages incremental movements from what can to what should be measured.

Footnotes

Appendix

Rieneke Slager—Reflections on Successful Completion of a PhD

Being asked to reflect on and provide guidance for successful completion of a dissertation is tricky; it is hard not to spout a whole lot of truisms of the “That’s easy for you to say” kind. And while it may be due to post hoc rationalization on my part, I would say I thoroughly enjoyed the experience of undertaking research and writing a dissertation. So much so that I changed my career aspirations mid-way through, having been enticed by the idea of becoming an academic, especially by the intellectual stimulation and relative flexibility to shape your own activities that come with the job. Along the way I (sometimes) listened to advice of senior colleagues, and what follows is really an amalgamation of guidance and tips that have stuck in my mind as being useful at various points in time. Perhaps this reflection may also be helpful to others in some way.

Early on in the PhD program, we were asked to present the contributions of our planned research in four slides. The idea of the exercise was of course to be able to communicate concisely your ideas, without losing your audience in complicated, long-winded theoretical or methodological arguments. The suggestion was to identify the “conversation” that was ongoing in your field of study and to which you wanted to contribute with your research findings. 3 As I had come from a different field of study, I found this approach a useful way of familiarizing myself with the literature, arguments, and evidence being talked about in management and organizations studies broadly, and the field of business and society in particular. Reading widely, and attending conferences where these different “conversations” were going on, helped me feel more confident about crossing disciplinary boundaries. Crucially, it also reminded me to construct carefully my ideas in the language appropriate for the different audiences with which I was engaging.

Speaking to different audiences formed an important part of my research due to its (at the time) novel set-up through a funding scheme by the Economic and Social Research Council (ESRC) in the United Kingdom, aimed at promoting closer collaboration between business and academia. The scheme funded 3 years of doctoral research at the International Centre for Corporate Social Responsibility (ICCSR) at Nottingham University Business School, with FTSE Group providing in-kind support through access to data as well as supporting teaching on responsible investment topics at the ICCSR. This collaborative set-up provided me with great access to the field but also meant the balance between the demands for rigor in academic research and requirements for timely results in business had to be carefully managed. I was fortunate enough that the team at FTSE was very understanding of the academic demands. I would encourage any doctoral student to seek out opportunities for such fieldwork (where appropriate in terms of research methodology), as it greatly enhances understanding of the field, contributing to more grounded theory building, while providing opportunities for teaching “real-life” cases.

Joining the conversation in your field of study also means a reciprocal sharing of ideas, at conferences, workshops, and seminars, and so on. As a doctoral student, you might be drilled on perfecting the novelty of your contribution to research, and one of the worst fears is finding that recently published article that addresses similar research questions or ideas to your own. This possibility makes some people wary of sharing ideas pre-publication. While I am under no doubt that copy-cats exist in academia as in other walks of life, there are too many important questions remaining to stop us from having meaningful conversations about issues related to business and society. And, as a senior academic commented at a Social Issues in Management (SIM) Doctoral Consortium, in response to a question from a doctoral student about the dangers of sharing research ideas, “If you are only going to have one idea, you are not going to have a very fruitful or successful academic career.” Take the time and space you have during doctoral studies to think about ideas and topics that are related to your research interest, and which you may be able to develop once the dissertation is finished, when initial teaching and administrative responsibilities may impede your capacity for coming up with fresh research ideas. While the best dissertation is a finished dissertation (speaking about truisms) hopefully your research ideas and interest are never ending and the completion of a dissertation will have given you the stimulation and confidence to continue to pursue them. Is not that what it is all about in the end?

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research was funded by the Economic and Social Research Council (ESRC) and the International Centre for Corporate Social Responsibility (ICCSR) with support from FTSE Group.

The article was accepted during the editorship of Duane Windsor.