Abstract

Recently, international funding agencies and practitioners in the area of corporate social responsibility (CSR) and small and medium enterprises (SMEs) have argued that microfinance institutions (MFIs) could promote the adoption of environmentally friendly business practices in microenterprises in developing countries. This article explores the potential and limitations of MFIs in promoting the spread of environmental risk management techniques and practices in microenterprises using a case study of an MFI-sponsored pilot program in this area in El Salvador. The author argues that caution should be exercised about the role that MFIs can play in relation to inducing change to the environmentally harmful practices of micro-entrepreneurs. In fact, this study reveals that the MFI had some difficulties in building internal skills and reconciling its environmental and performance objectives, limiting its ability to assist microenterprises in the area of environmental management. Furthermore, the pilot program, as it was designed, did not sufficiently take into account the psychological and financial barriers that constrain micro-entrepreneurs’ capacity to engage in any meaningful environmental behavior change. Finally, factors such as the lack of an adequate legal framework and local infrastructure also countered the effort of the MFI and limited the potential of microenterprises for effectively engaging in environmental risk management practices. The article concludes by outlining the implications of this analysis for future research, policy, and practice in this area.

Keywords

Small and medium enterprises (SMEs) account for more than 90% of all companies in the developing world (Mir & Feitelson, 2007). In fact, most SMEs are microenterprises with less than 10 employees that operate in the informal economy. 1 Microenterprises include a diversity of business entities such as small-scale manufacturers, traders, service providers, artisans, and farmers. Although these enterprises often generate a large part of the gross domestic product (GDP) and employment of developing countries, 2 microenterprises are usually “overlooked” in government policies and programs. Very little attention is paid to their social and environmental performance as corporate social responsibility (CSR) tends not to be perceived as a priority for microenterprises. Even if micro-entrepreneurs were interested in engaging in CSR, many of them have received very little, if any, formal education and are thought to lack the financial resources to engage effectively in CSR (Hillary, 2004; Mir & Feitelson, 2007; Shi, Peng, Liu, & Zhong, 2008). At the same time, the environmental impacts of microenterprises are sometimes seen as negligible in the literature. Yet several studies have demonstrated that some microenterprises adversely affect the environment through their use of chemicals, and because they generate a lot of solid and liquid waste (Wenner, 2002). Moreover, microenterprises may also exploit natural resources in unsustainable ways that lead to deforestation and soil degradation (Blackman et al., 2006; Crow & Batz, 2006; Lahiri-Dutt, 2008).

Although exact figures relating to the environmental impacts of microenterprises are not available, estimates indicate that 10% to 25% of microenterprises create environmental risks through their operations that represent direct threats to the health and livelihoods of micro-entrepreneurs and local communities in developing countries (Pallen, 1997). 3 Solutions exist to mitigate these risks such as energy-efficient machines, waste treatment and recycling, and agro-ecological practices, but conventional environmental management strategies have largely failed to promote their adoption in microenterprises (Blackman & Kildegaard, 2010).

Recently, some donors and experts have called for the involvement of a new actor, microfinance institutions (MFIs), in the promotion of CSR in microenterprises in developing countries (Schuite & Pater, 2008; Van Elteren, 2007). According to these authors, MFIs are well placed to promote CSR among microenterprises as they are in direct contact with thousands of microenterprises on a daily basis. In particular, MFIs are thought to embody the potential for acting as intermediaries that help raise the social and environmental awareness of micro-entrepreneurs through information dissemination (Hall, Collins, Israel, & Wenner, 2008; SEEP Network, 2008). Several MFIs have already been active in promoting CSR among their microenterprise clients in areas such as compliance with sanitary or labor laws, awareness of HIV/AIDS, and the improvement of human resources management (Dunford, 2001; Hall, 2006; Simanowitz, 2008).

As part of their social mission, MFIs could also, at least in theory, promote environmental management in microenterprises. Authors such as Blackman and Bannister (2006) have argued that MFIs could help microenterprises overcome two main barriers to environmental behavior change if they started combining tailored informational messages related to environmental management with their more traditional financial services. These two barriers are micro-entrepreneurs’ lack of environmental awareness and lack of financial resources. In practice, however, doubts remain as to whether MFIs would really have the capacity to implement environmental risk management programs among microenterprises, and whether such programs would change the environmental behavior of micro-entrepreneurs. For example, can MFIs reconcile such awareness-raising activities with their financial performance objectives? This study thus seeks to explore two interrelated research questions as follows:

The article makes two contributions to the emerging literature on CSR in SMEs in the developing world. First, through a literature review on MFIs, microenterprises, and environmental management, the article highlights our current knowledge of the factors that enable and constrain MFIs in relation to the promotion of environmental risk management among their microenterprise clients in the developing world. Second, in terms of its empirical contribution to knowledge, the article uses this literature review as a basis for analyzing a case study of an MFI in El Salvador that was one of the first to attempt to promote environmental risk management among its microenterprise clients. The article is likely to be the first of its kind that investigates the potential and limits of MFIs in relation to promoting CSR in microenterprises in this particular area.

The rest of the article is structured as follows: The second section introduces the rationale, assumptions, and questions behind the involvement of MFIs in promoting environmental risk management among their microenterprise clients. “A Pilot Program in El Salvador” section presents the case study in El Salvador. “Method” section describes the methodology used for this research. “Findings” section outlines the results of the pilot program and analyzes the internal and external challenges faced by Integral, the case MFI, in the implementation of this pilot program. The final section summarizes the main conclusions of the study and reflects on its implications for future research and policy in this area.

Literature Review

Involving MFIs in Environmental Risk Management Among Microenterprises: A Promising Approach?

Microenterprises and environmental risks

Most microenterprises do not generate significant environmental impacts. However, several academic studies have shown that some microenterprises in specific industries produce environmental risks through their core business operations (Wenner, 2002). 4 Such risks are primarily generated by microenterprises operating in industries such as leather tanning, metal working, electroplating, mining, painting, printing, textile dyeing, auto-repair, brick and tile making, wood processing, charcoal making, crop growing, animal husbandry, fisheries, food processing, and transportation (Blackman, 2006a; BRAC Bank, 2006; FMO Entrepreneurial Development Bank, 2008; Green Microfinance, 2007; Pallen, 1997; SEEP Network, 2008). As illustrated in Table 1, the environmental risks of these business activities are linked to inefficiency of production processes, inadequate chemical use, or inappropriate waste management. In fact, microenterprises are more likely to use older equipment and apply inadequate production techniques than many larger enterprises (Lanjouw, 2006).

Environmental Risks of Business Activities.

Source. Based on FMO Entrepreneurial Development Bank (2008).

Environmental impacts of microenterprises tend to be highly local in nature but still significantly affect mortality rates in the communities residing near production sites. After conducting a cost–benefit analysis, Blackman et al. (2006) even showed that there would be more benefits from reducing pollution in small-scale brick kilns than in larger brick-making firms. Similarly, Crow and Batz (2006) studied the environmental impact of small bleachers and dyers in India. They found that water effluents from these enterprises were loaded with chemicals and heavy metals that contaminated the groundwater and local rivers, reduced soil fertility, decreased fish stocks, produced skin diseases, and caused a shortage of drinkable water. Another study by Lahiri-Dutt (2008) demonstrated that people working in small-scale mining activities were more prone to developing respiratory problems, arthritis, and tuberculosis because of poor sanitation, constant exposure to dust, and limited access to clean drinking water. Poor people were thus disproportionately affected by the environmental risks generated by the microenterprises (Blackman, 2006a).

However, in most microenterprises, environmental risks can be mitigated by enhancing production efficiency, using filters to reduce water contamination, or integrated pest control. Changing the behavior of managers and workers by making them use chemicals, masks, and gloves in a rational way, as well as encouraging them to engage in recycling, may also help in this regard (Blackman, 2006c; Crow & Batz, 2006; FMO Entrepreneurial Development Bank, 2008). According to FMO Entrepreneurial Development Bank (2008), this change would benefit micro-entrepreneurs and the communities affected by their enterprises by reducing occupational hazards and environmental contamination. Yet the voluntary adoption of such solutions is not always easily accomplished.

Barriers to environmental behavior change in microenterprises

The literature identifies several barriers to environmental behavior change in microenterprises (Hillary, 2004). These barriers can be divided into structural and psychological barriers (Swim et al., 2010). Structural barriers refer to access to information and financial resources, infrastructure limitations, and inadequate market regulation. In fact, micro-entrepreneurs often lack awareness of the environmental, health, and sanitation risks linked to the running of their enterprises as well as information on how to mitigate these risks (Blackman, 2006a, 2006c; Hilson, Hilson, & Pardie, 2007; Mir & Feitelson, 2007). Access to information thus seems to be a first significant barrier to the voluntary adoption of environmentally friendly technologies in microenterprises (Hillary, 2004; Lanjouw, 2006; Pimenova & Van der Vorst, 2004). A second structural barrier often cited in the literature is the lack of financial resources that prevents a microenterprise from upgrading to cleaner production processes (De Almeida, 1998; De Canio, 1998; Lanjouw, 2006; Pimenova & Van der Vorst, 2004; Swim et al., 2010). As highlighted by Mir and Feitelson (2007), microenterprises already struggle to survive in the short-term. They are often unable to access the banking system as they cannot provide sufficient collaterals. This lack of collaterals prevents them from accessing finance that might help them upgrade their enterprises in technological terms (Blackman & Bannister, 2006). Lack of adequate infrastructure is also seen in the literature as a barrier to changing environmental behavior of microenterprises. For instance, the absence of local technology suppliers or recycling facilities may hinder the adoption of clean technologies (De Almeida, 1998; Steg & Vlek, 2009). Finally, inadequate public regulation such as high taxes on clean technologies may also be a structural barrier that leads to price distortions (De Almeida, 1998; Swim et al., 2010).

In addition to these structural barriers, the literature on environmental behavior change discusses how human habits, social norms, or emotions may constitute barriers to environmental change (Henrich et al., 2001; Jager, 2003; Maréchal, 2009; Steg & Vlek, 2009; Swim et al., 2010). In fact, many authors describe how human beings are locked into particular “habits,” repeating the same actions without much deliberation. These actions become the norm (Jager, 2003; Maréchal, 2009; Steg & Vlek, 2009; Van den Bergh, Faber, Idenburg, & Oosterhuis, 2006). Moreover, various studies show that human beings may be reluctant to adopt new forms of behavior when their peers are locked into the same habit (Barnes, Gartland, & Stack, 2004; Henrich et al., 2001; Maréchal, 2009; Swim et al., 2010). Finally, the decision to change habits also relates to the emotions associated with the habit in question. As Swim et al. (2010) argued, emotions can be a stronger driver of particular types of behavior than rational decision-making processes.

When it comes to overcoming barriers to environmental change, Steg and Vlek (2009) identified two approaches that may be helpful: informational and structural strategies. Informational strategies seek to address the lack of awareness of the target population (in this case, microenterprises). However, many studies have shown that the mere provision of information does not systematically translate into behavioral change (De Almeida, 1998; Swim et al., 2010). Therefore, Steg and Vlek emphasize that informational strategies should also address the psychological barriers to behavior change. It is not only the content of the information which counts but also the question of who, when, where, and how the information is provided. In a case study, McKenzie-Mohr (2000) found that people were more likely to change their behavior in relation to watering their lawns when they had been visited by a student on an individual basis than people who were just given a flyer. Jager (2003) thus argued that human beings are also more likely to change their behavior when new information is provided at the same time as the concerned behavior is performed. This argument also rings a bell with Steg and Vlek, who debate how environmental behavior change is more likely to occur when awareness-raising information is tailored to the needs, wants, and perceived barriers of individual segments of a given population. This approach is also known as individualized social marketing in the literature (Kollmuss & Agyeman, 2002; McKenzie-Mohr, 2000; Steg & Vlek, 2009).

In addition to informational strategies, structural programs may also be helpful in relation to encouraging pro-environmental behavior (in this case, among micro-entrepreneurs). For instance, by promoting local market development for clean technologies, investing in recycling infrastructure, facilitating access to payment facilities, or setting up fiscal and financial incentives for technology change (Steg & Vlek, 2009). The exact choice of strategy will depend on the specific barriers and solutions to environmental behavior change in microenterprises identified in a given context. Table 2 identifies these barriers and solutions.

Barriers to and Solutions for Introducing Environmental Behavior Change in Microenterprises.

The need for alternative actors to foster pro-environmental behavior

Public agencies have tried to promote environmental responsibility through informational and structural strategies, by implementing national awareness-raising campaigns, providing subsidies, or offering tax incentives programs to SMEs. However, these interventions have largely failed to improve the environmental performance of microenterprises (Blackman & Kildegaard, 2010). The present study’s review of the literature in this area indicates that two main reasons explain this lack of performance.

First, public sector interventions tend to fail as they do not adapt their environmental messages to the particular contexts in which they are promulgated. While low awareness and lack of technical information are identified as some of the main barriers to the adoption of pro-environmental behavior in microenterprises, national awareness-raising campaigns have a limited effect on microenterprises as messages are often not adapted to the concerns and educational levels of micro-entrepreneurs. At the same time, they tend not to be broadcast through media accessible to this target population (Blackman, 2006a, 2006c; Mir & Feitelson, 2007). This circumstance is related to the general challenges faced by public sector agencies in reaching out to microenterprises. Command-and-control strategies are often ineffective, because public agencies lack the human and financial resources to enforce those (Wenner, Wright, & Lal, 2004). Most microenterprises are informal, and geographically dispersed, making it complicated and costly for public agencies to control and sanction them according to existing environmental laws (Blackman, 2006a, 2006b). Positive strategies based on subsidies or fiscal incentives also have limited effects as they are designed for legal companies and do not reach micro-entrepreneurs who mostly operate in the informal economy (Hilson et al., 2007; Vincent & Sivalingam, 2006).

Involving microfinance: The promise of an integrated approach?

Nevertheless, several recent studies have pointed that a promising approach could be to involve MFIs in the promotion of environmental responsibility among microenterprises (Blackman, 2006a, 2006c; Hall et al., 2008; Schuite & Pater, 2008; Van Elteren, 2007). A donor, the Dutch development bank FMO, has been particularly active in promoting environmental risk management within MFIs. Through the development of specific tool kits 5 and the organization of international workshops, the FMO has sought to encourage its partner MFIs in developing countries to assess the environmental risks of their clients’ activities and raise these micro-entrepreneurs’ awareness of mitigation solutions.

At first, this approach seemed promising. MFIs were thought to have a first-mover advantage in promoting pro-environmental behavior in microenterprises as they closely interacted with thousands of micro-entrepreneurs and could influence micro-entrepreneurs’ decision-making processes as investors (Coulson & Dixon, 1995; Wenner et al., 2004). Some MFIs believed that their close relationship with their clients could help them raise their clients’ awareness of different issues such as family planning or HIV/AIDS prevention (Dunford, 2001). Similarly, MFIs might be in a position to raise their microenterprise clients’ awareness of environmental risk mitigation through their loan officers as these had face-to-face interactions with the micro-entrepreneurs and were able to tailor their messages to the needs of these clients.

The second advantage of MFIs was seen to be their ability to provide access to financial resources for micro-entrepreneurs that would otherwise be excluded from the mainstream banking system. The difficulties that microenterprises face in accessing the “mainstream” banking system were often portrayed as a key factor that hindered technological change in micro-, small-, and medium-sized enterprises (Blackman & Bannister, 2006). An integrated approach whereby MFIs combined their financial and informational services might thus lead to synergies in the promotion of pro-environmental behavior in microenterprises. Yet, as environmental risk management was still a very new issue for MFIs to take on, they were also likely to face important challenges in encouraging their microenterprise clients to engage in environmental risk mitigation.

Challenges linked to MFIs’ involvement in environmental risk management

Drawing on the literature on microfinance and environmental behavior change, it seems that MFIs may face at least three significant challenges in the promotion of environmental responsibility among their microenterprise clients. First, MFIs specialize in the provision of financial services, but they do not have a priori the skills and expertise needed to assess the environmental risks of their clients and help them mitigate those risks. The practitioner-oriented literature also highlights that the provision of non-financial services may conflict with the MFI’s financial objectives (Ahmad, 2003; Lensink & Mersland, 2009; Lensink, Mersland, & Nhung, 2011). In fact, some studies show that loan officers sometimes fear that they will lose their bonus or even their job if they are not performing well in financial terms. Therefore, they are likely to prioritize the activities on which they are evaluated—usually portfolio development and quality—at the expense of other activities (here environmental risk mitigation; Ahmad, 2003; Bazoberry, 2001; Dixon, Ritchie, & Siwale, 2007).

Second, it seems questionable whether MFIs can address the psychological and structural barriers to environmental behavior change among their microfinance clients. In theory, MFIs could provide individually tailored messages to their clients through their loan officers during face-to-face interaction at the micro-entrepreneurs’ workplace (Jager, 2003; Kollmuss & Agyeman, 2002; McKenzie-Mohr, 2000; Steg & Vlek, 2009). Nevertheless, even if it takes the shape of individualized, social marketing, using an informational approach may be insufficient to change people’s (in this case micro-entrepreneurs’) environmental behavior. In fact, they might already be locked into particular forms of behavior or habits (Verplanken & Wood, 2006). 6

Third, the lack of financial resources to upgrade to cleaner production processes is another key barrier to environmental behavior change in microenterprises (De Almeida, 1998; De Canio, 1998; Swim et al., 2010). As mentioned earlier, MFIs are well positioned to provide the financial resources needed to invest in clean technologies. However, this positioning implies that alternatives that can upgrade production processes are available on the local market (Millard, 2002) and that these alternatives bring clear economic benefits to the micro-entrepreneur to be adopted on a voluntary basis (De Canio, 1998; Srinivasan, 2008). Even if they manage to implement an environmental risk management program, MFIs may not be able to address other structural barriers to behavior change such as pricing, inadequate infrastructure, and the absence of proper legal framework for environmental pollution control (Blackman, 2000; Steg & Vlek, 2009; Swim et al., 2010). An MFI willing to promote environmental responsibility among its microenterprise clients may thus face significant external challenges in addressing psychological and structural barriers to behavior change among microenterprises.

The next section introduces the case study of how an MFI sought to overcome both internal and external challenges to promoting environmental risk management among microenterprises in El Salvador.

A Pilot Program in El Salvador

El Salvador, a small country with around seven million inhabitants in Central America, faces several major environmental challenges including water contamination, outdoor air pollution, and deforestation (Ministry of Environment and Natural Resources [MARN], 2011; World Bank, 2006). However, the agency charged with handling environmental affairs in El Salvador, the MARN, has neither adequate financial nor human resources to address these environmental challenges. Apart from nation-wide awareness-raising campaigns on specific issues (such as turtle protection, organic composting, and energy savings), the Ministry tends not to be involved in implementing prevention and support programs that foster the adoption of pro-environmental behavior within El Salvador.

As far as micro and small enterprises are concerned, they are required to comply with the national Environmental Code and obtain Environmental Licenses from MARN. However, MARN focuses on large companies through a system of complaints and sanctions instead because the Ministry does not have the means to enforce the Code at the level of micro and small enterprises. Yet, the National Committee for Micro & Small Enterprises (CONAMYPE) identifies environmental management as a key issue for micro and small enterprises in the country. In 2009, CONAMYPE decided to include environmental objectives in its vision and mission. At the time of this fieldwork, the agency considered initiating programs to help micro and small enterprises, but lacked the means to enable them effectively to comply with the Environmental Code. The context in El Salvador was therefore favorable to the involvement of MFIs in promoting environmental responsibility among microenterprises in the country. Hence, in 2009, the Salvadorian Microfinance Network ASOMI, comprising 11 MFIs, organized a series of workshops to raise MFIs’ awareness of their ecological footprint.

As the MFI with the largest outreach and more than 45,000 active borrowers in El Salvador, 7 Integral initiated a pilot environmental risk management program in October 2009 that continued throughout 2010 and 2011. This initiative stands out as an interesting case study for several reasons. First, Integral is one of the very few MFIs that have taken up the challenge of engaging in environmental risk management. As a pioneer in this field, Integral gives us the opportunity to identify the achievements and challenges that MFIs are likely to face in implementing this type of program. The case is furthermore interesting in that Integral is a large and very professional MFI, which has performed well in financial terms. The issues that Integral faces when implementing an environmental risk management program may therefore be indicative of the challenges that other MFIs might encounter in undertaking such a program. Finally, the case is worth studying, because Integral decided to undertake the pilot on the recommendation of one of its donors, the Dutch development bank FMO. Integral opted for a positive approach—raising their clients’ awareness of environmental risks—instead of only adopting an environmental exclusion list as some MFIs did to respond to donors’ expectations (Allet, 2014).

Integral’s pilot program targeted three areas that Integral considered as environmentally risk prone.

Food production and sale: Bakeries, food stalls, small restaurants, tortillerías, or pupuserías 8 may be associated with environmental risks depending on their cooking energy source. In fact, using wood for cooking might be related to deforestation and air pollution.

Manufacturing workshops: Metal workshops, aluminum workshops, auto-repair workshops, brick making, carpentry, and sewing can involve environmental risks linked to chemical use and waste management.

Agriculture: Farming can also entail environmental risks due to inadequate use of chemicals and unsustainable natural resources management.

In June 2008, two representatives of Integral participated in a workshop on environmental risk management in Quito, Ecuador, which was organized by FMO for its partner MFIs. During the workshop, the FMO introduced a methodology to assess and mitigate the environmental risks of microfinance clients. 9 Integral decided to test this approach in six branches before rolling out the program to all 25 branches in El Salvador. The six pilot branches were selected because their client portfolios were seen as the most environmentally risk prone. The Housing Loan Manager of Integral was appointed as the Social and Environmental Issues focal point, taking charge of the coordination of the pilot. Initially, Integral worked on adapting and simplifying FMO’s tools, and organized a training session on environmental risk management for MFI staff (loan officers, branch manager, and operation manager) from the six pilot branches in October 2009. Loan officers were asked to identify environmentally risky activities in their portfolio and discuss environmental risks and mitigation solutions with clients. Loan officers then had to fill in a specific form for each client wherein they would write down the environmental risks that they had identified in the client’s activity and the mitigation solution that they suggested to the client. Finally, they were instructed to conduct follow-up visits to monitor and write down changes in practices linked to environmental risks among microenterprise clients. Integral thus decided to promote environmental risk mitigation in microenterprises through an innovative individualized informational approach.

Method

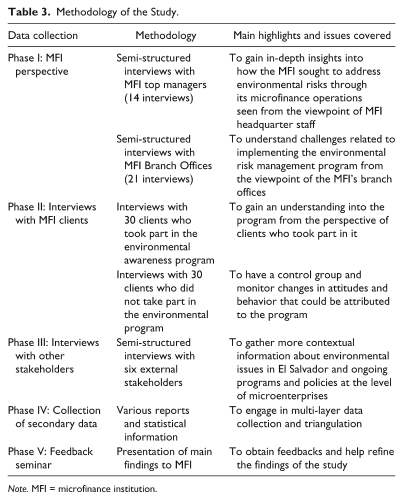

This study of Integral’s environmental risk management program is based on data gathered during 6 weeks of fieldwork in May and June 2011 in El Salvador. The author interviewed 95 people with a view to understanding the outcomes of Integral’s environmental risk management program. To grasp the challenges faced by Integral in the implementation of the pilot program, the author first conducted 35 semi-structured interviews with a wide range of managers and employees of the MFI. The author then interviewed 14 top managers working at Integral’s headquarters. 10 The author also conducted interviews at Integral’s branch offices. The interviews included two branch managers and nine loan officers in three branches that were involved in the pilot program (at Apopa, Ahuachapán, and Flor Blanca), as well as two branch managers and eight loan officers in two branches that were not part of the pilot (at Centro and Santa Ana). An open, semi-structured protocol guided these interviews, focusing on the importance of environmental issues and risks in the portfolio, the clients’ awareness of and capacity to mitigate environmental risks, and the role of loan officers in tackling environmental issues. The interviews also touched upon the willingness and capacity of loan officers to promote pro-environmental behavior among their clients. Moreover, when loan officers had participated in the pilot, the author probed their views on the training and tools used, the implementation of pilot activities, and the challenges that microenterprises faced in the implementation process.

Furthermore, an experimental group of clients (pilot branches’ clients) was compared with a control group (other branches’ clients) to identify the achievements by Integral’s environmental risk management program. In doing so, the author conducted 60 semi-structured interviews, with 30 clients in the pilot group and 30 clients in the control group, in four different branches. A matching approach was used to select a valid control group. This approach consists in pairing each observation with a control one that shares characteristics as similar as possible (Frondel & Schmidt, 2005; Girma & Görg, 2007; Hujer, Caliendo, & Thomsen, 2004; Hulme, 2000; Wagner, 2002). Sample selection was thus made in two steps: (a) selecting pilot and control branches, and (b) pairing pilot clients with control clients.

Out of the six branches that were involved in the pilot program, the author decided to focus on two branches that have proved to be the most active in implementing the pilot program: Apopa whose portfolio is mostly urban and peri-urban, and Ahuachapán whose portfolio is more rural. On the basis of information provided by Integral, the author then identified Centro and Santa Ana as suitable control branches, because they are similar to Apopa and Ahuachapán in terms of their portfolio size, number of clients and loan officers, average loan amount, gender, and urban/rural distribution. Centro and Apopa are located in the San Salvador area whereas Santa Ana and Ahuachapán are in the western part of the country.

In the two pilot branches, the objective was to interview as many microenterprises from the pilot program as possible. Some of the microenterprises could not be interviewed as some had dropped out from Integral’s program; were located in areas with high security risks; or could not be reached in spite of many field visits. The author managed to interview a total of 30 clients (14 in Apopa and 16 in Ahuachapán) out of the 58 microenterprises that were involved in the pilot program in these branches. The author then paired each pilot microenterprise with a control client sharing similar characteristics (14 in Centro and 16 in Santa Ana) using the Monitoring and Information System data and loan officers’ knowledge. The first criterion was to match activities because environmental risks are inherently linked to production in particular industries. For example, if the author had interviewed two metal workshops in Apopa, she tried to find two metal workshops in Centro. Moreover, when there was enough choice, the author sought to find control clients with similar gender, geographical location (rural/urban), education levels, and age brackets as all of these variables could influence their environmental awareness and behavior. A summary of the methodology deployed for this study is found in Table 3 below and the characteristics of the sample are presented in Table 4.

Methodology of the Study.

Note. MFI = microfinance institution.

Client Sample Characteristics.

The interviews were conducted in Spanish directly by the author with each client interview lasting between 30 and 60 min. Loan officers or representatives of Integral were not allowed to stay during the discussion as their presence might affect their clients’ answers. The interview guide focused on topics such as clients’ credit history and level of satisfaction with Integral’s services, their awareness of and capacity to reduce environmental risks, and their relationship with their loan officer. The author also talked to them about their previous and actual environmental behavior, and the environmental management suggestions given by the loan officer. The author looked at both self-reported and observed behavior to identify the actual environmental behavior of the microenterprises. The author relied on their self-reported behavior and the environmental risk forms that had been filled by loan officers in 2009-2010 to establish the previous environmental behavior and identify possible changes in the behavior of these microenterprises that might have occurred later on.

In addition, the author reviewed all documentation available on the pilot project including the guidelines that loan officers had received regarding the pilot program, the training tools that were used, the environmental risk forms that had been filled by loan officers, and the few reports and statistics that had been compiled at the headquarters level regarding the project. The author looked at the manual of procedures and the Monitoring and Information System of Integral to have a better understanding of current procedures. These multiple data sources enabled the author to triangulate information, identify contrasting opinions, and therefore obtain a better understanding of the factors that played a role in producing particular outcomes of the pilot program.

Collected data were first analyzed using an inductive approach before placing the results in the context of the literature on environmental behavior among microenterprises. Specific attention was given to the triangulation of information (Guérin, Morvant-Roux, Roesch, Moisseron, & Ould-Ahmed, 2011), which was possible due to the different interviews conducted with top management, branch managers, loan officers, and microenterprise clients. 11

Finally, at the end of the field visit, the author had the opportunity to present preliminary results to some of Integral’s top managers, including the Executive Director, the Operations Manager, the Finance Manager, the Human Resources Director, the Legal Department Manager, and the Environmental Management Officer. They broadly considered that the findings were valid and provided some feedback that helped refine the analysis.

Findings

The findings show that the pilot program only had modest results. In fact, the outreach of the pilot program was limited in terms of the number of clients sensitized. From December 2009 until May 2011, the program reached a total of 149 clients that represented only 1% of the portfolio of the six pilot branches and 0.3% of the Integral’s clients. This lack of outreach is surprising because interviewed branch managers and loan officers estimated that environmentally risky activities represented between 10% and 40% of their portfolio clients. Out of the 149 clients reached, 70 were visited by the loan officers from the six pilot branches after they had been trained in late 2009 and early 2010. Loan officers conducted a follow-up visit in early 2010 for 40 out of these 70 clients. However, they did not assess the environmental risks of other clients later in 2010 and 2011 until someone from Integral’s headquarters came for this purpose, visiting 79 additional microenterprises in March 2011. The number of sensitized microenterprises was also different from one pilot branch to another. Two branches did not asses the environmental risks of their clients after receiving the training whereas one of them raised awareness of approximately 36 clients. Even if the program was first implemented as a pilot, outreach appears to have been very limited.

Moreover, the impact of the pilot program also seemed to be rather modest. Among the clients who were reached by the pilot, 40% remembered that someone from Integral came to discuss environmental and sanitary issues. Only 23% actually recalled what the loan officer recommended to reduce environmental risks and health hazards. In addition, almost 23% of the clients who remembered the loan officer’s advice stated that they already knew of these environmental risks and the recommended mitigation strategy. Finally, the pilot program did not seem to foster any change in the environmental behavior of microenterprise clients. None of the interviewed micro-entrepreneurs from the pilot program reported a change in behavior following the loan officers’ advice between 2009 and 2011.

One might ask why Integral’s pilot program for environmental risk management was only able to achieve these relatively modest results. The next sub-section provides answers to this question as the author first identifies the internal challenges linked to initiating an environmental risk management program within Integral and then analyzes the external challenges that Integral faced in relation to promoting environmental risk management among its microenterprise clients.

Internal Challenges in Implementing the Program

High motivation, low technical knowledge

The limited outreach of the pilot program cannot be attributed to a lack of motivation on the part of loan officers. On the contrary, loan officers and branch managers expressed a keen interest in the topic. They asserted that 10% to 40% of their portfolio clients were affected by environmental risks, and that it would be important to reduce these risks. In Integral, loan officers who managed rural portfolios were recruited, in part, due to their background as agro-economists or agro-engineers. This background seemed to make them inclined to analyze the environmental risks of their microenterprise clients’ activities. Several of them clearly defined environmental assessment as part of their job and mission. In Integral, loan officers are called asesores, which can be translated into English as “advisors.” As asesores, many felt that it was their job to advice their clients on how they improve the financial management, marketing, productivity, and even environmental risk management of their microenterprises. The loan officers identified a clear link between environmental management and their social mission of financial inclusion and poverty reduction. In the view of many loan officers, Integral might fail to help micro-entrepreneurs improve their livelihoods if the MFI did not address the issue of environmental risk mitigation. In addition, they mentioned that supporting microenterprise clients in reducing their environmental risks could be beneficial to Integral. Such reduction could improve Integral’s reputation and prevent credit risk in some cases as a baker who gets sick from fire smoke or a farmer who suffers from chemical intoxication might stop repaying loans.

However, loan officers felt that they were not well placed to assist their clients in mitigating environmental risks, because they still lacked the required technical knowledge and tools. Loan officers and branch managers were interested in the training that they received about environmental risk management. Yet they believed that the training was too theoretical and short—training lasted only half a day. In addition, they were not provided with more specific tools and technical information on solutions to mitigate environmental risks. As they were not environment or energy practitioners, they found it difficult to provide their microenterprise clients with information that would actually promote pro-environmental behavior.

Conflicting priorities within the MFI

Another barrier to the effective implementation of the pilot program was related to the internal strategy of the MFI. The activities of the pilot program were to some extent in conflict with the financial objectives of Integral. Similar to what the author found in the literature (Ahmad, 2003; Bazoberry, 2001; Dixon et al., 2007), all loan officers mentioned that they were overloaded with work and had strict financial objectives to reach in terms of portfolio size, number of clients, and portfolio quality, which partly determined their monthly salary. The loan officers’ job description had not been revised with a view to making it compatible with the new tasks required by the pilot program. Consequently, loan officers found it difficult to find time to both achieve their financial performance requirements and raise clients’ awareness on environmental issues:

It is difficult with the workload we have. (Loan officer at Apopa) There is a lot of pressure with our other goals. We lack time. We have many other things to do. (Loan officer at Ahuachapán) It could be conflicting with our objectives, because we sometimes run against time. (Loan officer at Santa Ana)

Moreover, assessment of environmental risks had not been integrated in the credit methodology or the MFI manual of procedures. Environmental risk assessment was performed after the provision of the loan outside of the regular field visits that loan officers would conduct. Had environmental risk assessment been included as one of the tasks to be completed by loan officers during their regular field visits (when they assessed the capacity and willingness of micro-entrepreneurs to pay for a loan), the additional burden of attending to the new task would have been reduced. Despite the willingness of the person in charge of the pilot program, data collected by loan officers on environmental risks were not included in the Monitoring & Information System. These data were processed manually which entailed a higher risk of incomplete or incorrect data being recorded, making it more difficult to ensure follow-up and progress monitoring with microenterprise clients. Some loan officers also mentioned that they lost motivation in manually sending data to the headquarters, because they never received feedback on how the data were analyzed.

Another issue was the lack of regular training. Loan officers in the pilot branches only received training at the beginning of the program. However, out of the 21 loan officers trained in Apopa and Ahuachapán in 2009, only 8 were still working for Integral in 2011. Loan officer turnover would have required more regular training sessions in environmental risk management among microenterprises. Yet this step did not occur, because training on environmental risk assessment had not been included in the regular training curriculum provided to every new loan officer. For these reasons, the pilot program was perceived by several branch managers and loan officers as a very specific, time-bound initiative. Some loan officers thought that they had to perform environmental risk assessment only once for a specific set of clients. They perceived the exercise as a requirement from the headquarters, conflicting with their regular job description.

Integral’s experience thus confirms that an MFI willing to implement an environmental risk management program is likely to face important challenges in developing its internal skills and procedures in this area while reconciling its different performance objectives (financial, social, and environmental). In fact, pursuing these different objectives simultaneously may in the end compromise the effectiveness of such a program. To improve its impact in promoting environmental responsibility among microenterprises, an MFI needs to pay attention to the integration of environmental risk management into its daily operations. This integration has to start with the inclusion of environmental management into its mission, defining performance objectives for loan officers and managers that are consistent with the time and resources needed for promoting environmental responsibility, developing integrative procedures that builds on synergies, and providing staff with the adequate training, skills, support, incentives, and resources to implement these new activities. When the environmental issues are too complex to be managed by loan officers or when the MFI is not willing or able to perform awareness-raising activities itself, an option might be to establish a partnership with another organization specialized in environmental risk management. The MFI then acts as a facilitator to reach the target microenterprise population and contributes to the promotion of environmentally responsible behaviors without having to compromise its different objectives or to build technical skills internally.

Challenges in Addressing External Barriers to Environmental Behavior Change

In addition to internal management issues, the case study also revealed that Integral faced a number of external challenges in promoting environmental risk mitigation among their micro-entrepreneur clients. This section deals with each of these psychological, economic, and financial or other structural barriers.

Psychological barriers

Integral opted for an approach very close to individualized social marketing by asking loan officers to discuss environmental risks with their clients during field visits, assuming that face-to-face discussion would be efficient to promote pro-environmental behavior. However, this study revealed that this approach did not appear to be efficient when it came to addressing some of the psychological barriers to behavior change mentioned in the literature (Jager, 2003; Maréchal, 2009; Steg & Vlek, 2009; Swim et al., 2010). In fact, the author observed how some microenterprise clients ignored the advice provided by loan officers, because they did not always perceive loan officers as legitimate “messengers” of pro-environmental practices; and because these microenterprise clients appeared to be locked into habits that could not be altered by the mere provision of information.

Involving microfinance in raising clients’ awareness of environmental risks was based on the assumption that loan officers were in a good position to influence the decisions of their clients regarding business management. Loan officers themselves seemed to be conscious of this power:

As loan officers, we could have a bigger impact because there is trust, clients listen to us. (Loan officer at Ahuachapán) We could be a good channel of awareness-raising since clients see their loan officer as the “Dios Dinero.”

12

(Loan officer at Santa Ana)

A significant majority of interviewed clients (84%) said that they would be interested in receiving some advice from their loan officers on environmental risks. However, this study clearly revealed that not all microenterprise clients would actually trust the capacity of the loan officer to provide adequate recommendations. Here, the quality of the relationship between the loan officer and the client was directly linked to how the client perceived the loan officers’ capacity to provide environmental advice. Some loan officers were conscious of this limitation:

It only works with clients who already trust us. (Loan officer at Apopa)

In the sample, some clients stated that they had a good and trustful relationship with their loan officers. In fact, 71% of the interviewees in this category indicated that their loan officer had the capacity to provide environmental advice. As they were already used to discussing their situation with their loan officers, they expressed an interest in also receiving such advice from them,

I know her well. I really trust her. Any time I need some advice, I go and find her. (Pupusería at Apopa) He is smart and nice. Every time I need some help, I go and find him. (Pupusería at Centro)

In addition, 50% of those stating that they had a medium level of trust in their loan officers indicated that the loan officer had the capacity to provide environmental advice. However, some of the microenterprise clients in the sample revealed that they did not have a good relationship with their loan officers. In fact, only 20% of the clients who had low trust in their loan officers believed that their loan officers had the capacity to provide them with environmental advice. Hence, most clients in this category believed that the loan officers could not act with any credibility in this role, because they primarily focused on financial considerations, including repayment imperatives,

Loan officers are only interested in economic aspects. They don’t take time to talk. (Carpenter at Santa Ana) Loan officers do not have the knowledge. They only know about finance. (Pupusería at Centro) I do not have so much trust. They put too much pressure. . . . I don’t think it should be their role to give advice on environmental risks. They do not know anything about occupational hazards. (Metal workshop at Apopa) They put too much pressure when one is just two or three days late. I want to get out of here. . . . It is important to give advice, but loan officers are not interested in clients’ well-being. (Workshop at Santa Ana)

This study thus revealed that microfinance clients did not uniformly perceive loan officers as legitimate when it came to providing advice on environmental risk management. As a consequence, they might have ignored any advice provided by their loan officer.

As emphasized in the literature, the tendency to dismiss new information is even stronger when people are locked into particular habits (Jager, 2003; Maréchal, 2009; Steg & Vlek, 2009; Van den Bergh et al., 2006). This tendency was the case for some of the microfinance clients interviewed. The sample micro-entrepreneurs seemed to be relatively aware of the environmental risks linked to their activity. Very few of them identified these risks as “environmental” or related those risks to ecological issues such as deforestation or biodiversity loss. They were instead concerned with the health consequences of risks such as asthma and lung disease generated by daily exposure to smoke (for food-related activities using wood as a cooking energy source 13 ), wood dust (for carpenters), clothe dust (for sewers); intoxication from chemicals (for farmers); and water contamination from inappropriate waste management. However, very few micro-entrepreneurs decided to decrease their use of chemicals or at least use protective gear even if they were aware of health hazards linked to chemicals. Two of the farmers interviewed had been seriously intoxicated, but they were still using chemicals without wearing any mask or gloves. Many micro-entrepreneurs kept using wood as a cooking energy source even if they did not like smoke emissions.

I could use protective gear. It is not a question of cost. It is just a question of habit. (Farmer at Santa Ana) It is a question of habit. I never used protective gear when I was working with muriatic acid with my father. (Aluminum workshop at Santa Ana) I would not listen to the loan officers’ advice regarding the use of chemicals, because my grandparents have always done it this way. We are used to it. (Farmer at Apopa)

Loan officers identified this barrier as part of the “culture” of the people. Clients explained their behavior with reference to what they and their peers were already or used to doing. The literature on environmental behavior identifies some specific strategies that address this psychological barrier and prove more efficient in fostering behavioral change. These strategies include providing the target population with the opportunity to directly experience the promoted technology or behavior (Duerden & Witt, 2010), providing comparative feedback (Steg & Vlek, 2009; Swim et al., 2010), promoting role models (Steg & Vlek, 2009), giving positive feedback on what people do well or could do well instead of negative criticism of their actual behavior (Jager, 2003; Maréchal, 2009; Steg & Vlek, 2009; Swim et al., 2010), and challenging people to commit to a change in their environmental behavior (Maréchal, 2009; Steg & Vlek, 2009; Wood, Tam, & Guerrero Witt, 2005). For instance, some loan officers suggested that pro-environmental behavior could be promoted by organizing a “competition” between their clients with an award granted to the micro-entrepreneur with the best environmental behavior. However, at the time of the study, the approach implemented by Integral was only based on a discussion about actual practices and potential mitigation solutions. Furthermore, discussions about environmental risk mitigation between the loan officer and the microenterprise client only happened once or twice in 18 months whereas breaking habits would require longer term interventions to overcome the psychological barriers identified above (Verplanken & Wood, 2006).

Economic and financial barriers

In addition, Integral’s pilot program did not lead to environmental behavior change among its microenterprise clients, because the MFI did not demonstrate how the use of particular technologies would result in economic benefits for its clients. For instance, in a context where the Government of El Salvador had removed most gas subsidies in March 2011, loan officers could not expect their clients involved in food-related activities to reduce their wood consumption and use more gas just because they advised them to do so. Loan officers might play a more effective role if they started to raise clients’ awareness on the existence of energy-efficient cook stoves. Thirty-six percent of the microenterprise clients involved in food production and sale had already heard about efficient cook stoves—mostly on television. However, only one had already seen such a cook stove, and most microenterprises did not know anything about the actual financial and health benefits or costs of using this technology. Forty-seven percent said that they would be interested in investing in such an efficient cook stove, provided they could obtain a microcredit loan for the purchase.

Integral had been working on developing specific credit lines for investing in efficient cook stoves, solar panels, and solar lanterns. Yet, when this study was conducted, the institution was still in an initial phase and had not yet developed marketing and communication tools for these technologies. Other initiatives in the microfinance sector had shown the importance of linking awareness-raising to the provision of microcredit. This linking was the case for Grameen Shakti for instance (Barua, 2001). However, within Integral, the pilot program was implemented without taking advantage of the synergies that could be created by linking the informational approach to the access to credit for investing in clean technologies.

Structural barriers beyond the MFI’s reach

Had it tailored its informational approach and coupled it with the provision of adapted loans, Integral might have been able to better influence the environmental behavior of its clients. However, there were still some structural barriers to behavior change that were beyond the reach of Integral.

A first barrier was the lack of local infrastructure. Several clients living in rural areas mentioned that they did not have any choice but to burn their waste or throw it into the nearby river, because there was no garbage collection in their area. One of the carpenters asserted that he would rather buy timber from sustainably managed forests, but that his suppliers did not use any certification that could help him know the exact origin of the timber. Lack of such infrastructure constrained the ability of micro-entrepreneurs to mitigate environmental risks.

A second structural barrier was linked to public policies (De Almeida, 1998; Swim et al., 2010). In March 2011, a month before this fieldwork commenced, the government of El Salvador drastically decreased subsidies on gas bottles. The price of gas bottles almost tripled for microfinance clients, increasing from US$7 to around US$20. The economic shock compelled some microenterprises to decrease their use of gas and replace it with wood, which went counter to Integral’s efforts aimed at promoting gas as a cleaner cooking fuel. 14

Finally, 63% of the microenterprise clients in the sample stated that they were affected by the global economic crisis. Forty-six percent clearly mentioned that they were not ready to make any new investments even if they could obtain a microcredit loan for this purpose. The inhabitants of El Salvador were even more reluctant to invest in upgrading their businesses as investment might attract the attention of maras (armed gangs) who would ask them to pay rentas (extortion). Environmental risk management initiatives undertaken by MFIs might thus encounter structural barriers that cannot simply be addressed by the MFI or the provision of information alone.

Conclusion

In this article, the author explored the potential and limitations of MFIs in promoting environmental risk management in microenterprises using a case study of an MFI-sponsored pilot program in El Salvador. In theory, MFIs might be in a good position to promote pro-environmental behavior in microenterprises. As highlighted in the international literature on the topic, this promotion might happen due to their embeddedness at the grassroots level and the synergies that could be created by combining their use of information and financial services. At the same time, analysis of the pilot program in El Salvador showed that it had very limited outreach and impact. Basing analysis on 95 interviews with microfinance clients and staff, the author identified two factors that could explain these modest achievements: (a) internal challenges faced by MFIs in implementing an environmental risk management program; and (b) external challenges faced by MFIs in addressing barriers to environmental behavior change among micro-entrepreneurs.

First, this study showed that the MFI was not able to develop its internal skills/procedures in ways that would have made it possible to implement effectively the pilot program. Loan officers also had to deal with conflicting priorities within their institution. This conflict happened as they were asked to raise clients’ awareness on environmental issues but were pressurized to reach tough financial targets.

Second, even if awareness-raising activities were essential to promoting pro-environmental behavior in microenterprises, the study found that the effects of awareness-raising activities were limited by psychological, economic, and other structural factors that the pilot program was not able to address fully. In particular, microenterprise clients were not always receptive to awareness-raising messages—either because they did not perceive loan officers as legitimate advisors or because the pilot program did not include more innovative strategies that would have encouraged them to break their habits. Moreover, the MFI did not create the synergies between its awareness-raising activities and its financial services that would have helped its microenterprise clients overcome their financial and psychological barriers to behavior change. Finally, Integral’s efforts were in some cases undermined by external factors such as a change in national policies that the MFI could not directly influence.

In terms of policy implications, the author recommends that MFIs integrate environmental risk management in their objectives, procedures, and daily work processes at all levels. This integration would reduce the tensions between the financial and environmental bottom lines of MFIs when undertaking environmental risk mitigation programs. Second, MFIs could have a greater impact on their clients’ environmental behavior if they took advantage of the synergies created by an integrated approach to environmental risk mitigation. On one hand, the MFI could raise awareness on a mitigation solution that could bring financial benefits to their clients. On the other hand, the MFI could provide microenterprises with access to credit that would enable them to invest in this solution. Third, the impact of the informational message could be improved by adopting strategies that addressed the psychological barriers to behavior change among microenterprise clients such as comparative feedback, direct experience, and commitment strategies. Finally, developing partnerships with technical support organizations would be key in making environmental risk mitigation programs more effective in the future. This approach might help MFIs in overcoming environmental management skill gaps internally within their organization and the lack of external legitimacy of loan officers in the eyes of some microenterprise clients.

This study also showed that caution should be exercised about the role that MFIs can play in the promotion of environmentally responsible behavior among microenterprises in developing countries. MFIs have the means to contribute to environmental risk management to a certain extent, but MFIs are financial institutions above all. Their role will always be limited, and they will never replace other actors in environmental protection. One should thus be cautious when promoting MFI involvement in environmental management. Especially at a time when we still lack knowledge on the relative effectiveness of the environmental strategies they implement. This question is even more crucial as many microfinance programs are subsidized. In fact, one might question whether supporting MFIs in developing environmental risk management programs is the most effective and efficient way to use public funds to promote environmental responsibility within microenterprises. It could be more relevant to provide support directly to producers’ organizations, which have long-term relationships with their members to promote agro-ecological farming practices as already done by some socially responsible investors. It could be more efficient to finance-specific industry unions to promote and facilitate access to clean production technologies as is suggested by Blackman (2006a). Further research is thus needed to assess whether MFIs have a comparative advantage in undertaking environmental risk management programs. Scholars also need to assess whether these programs are cost-efficient in comparison with other approaches aimed at fostering pro-environmental behavior in microenterprises in developing countries.

Footnotes

Appendix

Acknowledgements

The author would like to thank Peter Lund-Thomsen, Dima Jamali, and Søren Jeppesen for their significant support and contributions in improving and finalizing this article. I am also thankful to Isabelle Guérin, Marek Hudon, Marc Labie, Jean-Yves Moisseron, and Ariane Szafarz for their valuable comments on earlier versions. I am very grateful to Integral, which opened its doors and shared its pilot experience in a very transparent way. I am thankful to all Integral managers and employees who supported my research and answered all my questions, especially Carlos Viteri, Silvia de Melendez, Tony Castillo, and Karina Henriquez, as well as the loan officers and branch managers of Ahuachapán, Apopa, Centro, and Santa Ana. I also express many thanks to all 60 clients who dedicated some of their time to the interviews, and to my guides Carlos, Marcos, and Mauricio. Finally, I am thankful to Lisa Petzold for her logistical support and to Christine Dunlap for her proof reading of the article.

The article was accepted during the editorship of Duane Windsor.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article was financially supported by University Meets Microfinance program, PlaNet Finance, and ANRT (Association Nationale de la Recherche et de la Technologie).