Abstract

The question of how multinational enterprises (MNEs) respond to local corporate social responsibility (CSR) expectations remains salient, also in the context of many African governments’ attempts to define and regulate business responsibilities. What determines whether MNEs respond to such local, state-driven expectations as congruent with their global commitment to CSR? Adopting an institutional logics perspective, we argue that a higher global CSR commitment will lead to higher local responsiveness when regulatory distance is low, but it will lead to lower local responsiveness when regulatory distance is high. We find support for our hypothesis using data on 93 MNEs’ responses to the South African state’s Broad-Based Black Economic Empowerment policy. We thus contribute to the global–local CSR literature and show how MNEs’ local CSR responsiveness will be shaped by not only the local context but also their home country and firm-internal environments.

Keywords

Multinational enterprises (MNEs) face significant institutional complexity (Kostova & Zaheer, 1999), especially when managing corporate social responsibility (CSR) in different contexts. CSR requires companies to respond to universal, “global” principles of human rights and sustainable development (such as those highlighted by the United Nations Global Compact; United Nations, 2011), as well as more particular, “local” societal and cultural expectations and state regulations (Husted & Allen, 2006; see also Campbell, 2007; Donaldson & Dunfee, 1994; Matten & Moon, 2008). Motivated also by prominent cases of MNEs’ failure to respond to such local versions of CSR, this gives rise to researchers’ interest in what influences MNEs’ responsiveness to the local context of host countries (Husted & Allen, 2006).

One might expect MNEs with a strong corporate commitment to CSR to have the motivation and capabilities to also respond proactively to local variants of CSR, and this is supported by some studies (Cruz & Boehe, 2010; Kolk, Hong, & Van Dolen, 2010). However, a strong CSR commitment may lead to global CSR approaches becoming institutionalized and “ingrained” throughout the firm’s structure, with little allowance for local responsiveness (Bondy & Starkey, 2014; Husted & Allen, 2006; Muller, 2006; Tan & Wang, 2011). This uncertainty in the literature is mirrored in anecdotal queries by African stakeholders about why some MNEs seem disinterested in or even adversarial toward local CSR-related expectations, despite prominent corporate CSR commitments. It is also reflected in MNE managers’ doubts about how their global CSR strategies are related to local variants, such as South Africa’s Black Economic Empowerment (BEE 1 ) policies (Chahoud, Kneller, Krahl, Rieken, & Riffler, 2011).

Indeed, the global–local CSR debate is particularly salient in the African context, due to these countries’ distinctive economic and institutional circumstances (Ackah-Baidoo, 2012; Asiedu, 2002; Kolk & Van Tulder, 2010; Pratt, 1991). Particularly prominent in numerous African economies have been government policies and regulations focused on “indigenization” or “BEE,” seeking to address colonial or apartheid legacies of Africans’ exclusion from the control or benefit of economic activity (Bellema, 2010; Beveridge, 1974; Nwosu, Nwachukwu, Ogaji, & Probert, 2006; Ukiwo, 2008; Wilson, 1990). In the African historical and socio-economic context, such policies have important overlaps with the global CSR movement (Arya & Bassi, 2009; Hamann, Agbazue, Kapelus, & Hein, 2005; Littlewood & Holt, 2018; Muthuri & Gilbert, 2011; Mzembe & Meaton, 2013), yet there are also idiosyncrasies associated with their thematic content and regulatory provenance. In this article, we focus on how MNEs respond to these “home-grown,” state-driven African versions of CSR. More specifically, what determines whether MNEs respond to local, state-driven African expectations as congruent with their global commitment to CSR?

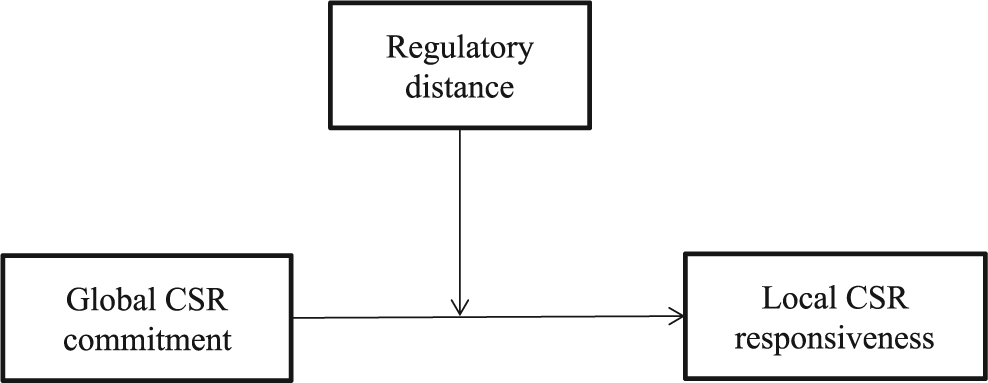

Building on the literature, we argue that the relationship between an MNE’s CSR commitment and its local responsiveness is moderated by the regulatory distance between host and home countries. We focus on regulatory distance because we expect this to play an important role given the regulatory provenance of the local African CSR variants in question. This builds on Matten’s and Moon’s (2008) arguments about the institutional embeddedness of CSR, including in particular the disparate roles of the state in different national business systems and corresponding differences in how CSR is manifested. We apply an institutional logics lens to theorize how global CSR commitment and regulatory distance interact to determine local responsiveness. We argue that high global CSR commitment will lead to high local responsiveness when regulatory distance is low, but it will lead to lower local responsiveness when regulatory distance is high.

This hypothesis is tested using data on 93 MNEs operating in the strategic research setting provided by the South African state’s BEE policy (Arya & Bassi, 2009; see also Littlewood & Holt, 2018). Our research is exploratory given limitations in our methods and data, but we consider our findings and arguments to be helpful in the context of sparse research on CSR and the role of state regulation in Africa.

We contribute to the literature on global–local CSR and extend the analysis by Campbell, Eden, and Miller (2012) by focusing on regulatory distance and explaining its moderating influence on the role of MNEs’ CSR commitment. Applying an institutional logics perspective to the global–local CSR debate, we contend that the MNE internal institutional environment “carries” the state logic so as to influence MNEs’ responsiveness to local, state-driven CSR variants. This allows us to extend Matten and Moon’s (2008) characterization of different institutionalized approaches to CSR to the context of MNEs straddling different institutional business systems, showing how MNEs’ local CSR responses are shaped not only by the complexities of the local context but also by their home country and firm-internal environments.

We commence with a literature review on the global–local CSR debate and institutional logics to develop our hypothesis. In the “Method” section, we devote attention to our research setting to explain both the similarities and tensions between universal conceptions of CSR and BEE as a particular regulation-driven variant of CSR. We test our hypotheses empirically and then discuss contributions, limitations, and further research.

Theory

MNEs’ Responsiveness to Local CSR

In addressing the question of what influences MNEs’ responsiveness to local CSR, some scholars have focused on firm-specific aspects, including in particular their global CSR commitment, whereas others have focused on firm-external aspects, especially the institutional differences between home and host countries. On neither of these dimensions, however, is there much agreement.

It has been suggested that MNEs with high global CSR commitment have both the motives and capabilities necessary for locally responsive CSR investments in host countries. In their study of retail companies’ CSR priorities in China, Kolk et al. (2010) found that those companies with high global CSR commitment—Carrefour and Wal-Mart—not only implement some aspects of their global CSR strategy but also show significant local responsiveness. Similar evidence of local responsiveness facilitated and motivated by a corporate commitment to CSR is found in the case of two French multinational retailers’ operations in Brazil (Cruz & Boehe, 2010).

However, a high level of global CSR commitment may lead to such global policies and practices being “ingrained,” and thus local responsiveness is diminished to maintain internal legitimacy and reduce internal co-ordination costs (Tan & Wang, 2011). Bondy and Starkey (2014) investigated the local CSR practices of 37 MNEs and found that they emphasize their global commitments and give surprisingly little attention to local cultures or circumstances. Similarly, Muller (2006) explored the CSR practices among Mexican subsidiaries of seven European MNEs in the automotive industry and showed that these firms tend to prioritize themes and practices associated with their global approach. Barkemeyer and Figge (2014) referred to the “headquartering effect” brought about by the increasing professionalization of CSR, which also prioritizes internal coherence and legitimation of CSR at the expense of local responsiveness.

With regard to firm-external factors, Yang and Rivers (2009) proposed that MNEs’ subsidiaries will adapt to local practices to legitimize themselves if they operate in host countries with institutional environments different from the firms’ home countries. By imitating the strategy of local firms, MNE subsidiaries may acquire legitimacy and thereby reduce their liability of foreignness (Gardberg & Fombrun, 2006; Salomon & Wu, 2012). CSR is thus viewed as a strategic investment comparable with research and development (R&D) and advertising (Gardberg & Fombrun, 2006), and this is especially pertinent when home and host countries are institutionally different.

However, building on the literature on institutional, cultural, and geographic “distance” as a significant challenge to MNEs (Ghemawat, 2001; Ionascu, Meyer, & Estrin, 2004; Kostova, 1996), Campbell et al. (2012) argued that administrative distance—which includes not only regulations but also other aspects, such as political stability and government effectiveness—will make MNEs’ managers less empathetic to local constituencies and thus less motivated to adapt to local expectations, and it also makes local CSR responsiveness more difficult and costly. They confirm their hypothesis that increased administrative distance diminishes MNEs’ local CSR responsiveness with data on multinational banks’ responses to the U.S. government’s Community Reinvestment Act.

Regulatory Distance as a Moderating Variable

We seek to respond to these conflicting arguments and findings in two steps. First, we suggest that an MNE’s global CSR commitment and the “distance” between host and home country institutions interact when influencing the MNE subsidiary’s local CSR responsiveness, and thus they need to be considered together. Specifically, we expect differences between host and home countries to influence the relationship between high CSR commitment and local responsiveness.

Furthermore, whereas Campbell et al. (2012) identified a significant role for the broad construct of administrative distance, we focus on the more specific issue of regulatory distance. In doing so, we follow calls for disaggregated analyses of institutional differences (Jackson & Deeg, 2008; Xu & Shenkar, 2002). Furthermore, we are motivated by our conceptual and empirical interest in African, state-driven variants of CSR, and specifically the anecdotal observation in South Africa that some MNEs with high explicit CSR commitment seem surprisingly unresponsive to state-driven CSR variants as part of their CSR strategies and reporting. This has broader relevance in the context of the widespread adoption by many African governments of regulations focused on enhancing Africans’ ownership of, and inclusion in, economic activity, as well as increasing calls for state regulation to improve CSR uptake in Africa (Muthuri & Gilbert, 2011; Mzembe & Meaton, 2013).

Our focus on regulatory distance is also motivated by an ongoing tension in scholarly and policy debates surrounding the degree to which the definition and implementation of CSR is discretionary or may involve state regulation. As noted by Matten and Moon (2008), “In its very name, CSR presumes corporate choices . . . yet it also entails conformance with the law” (p. 407; see also Vogel, 2010). The role of regulations in defining CSR in diverse institutional settings is thus an important issue in our understanding of CSR, and it is particularly salient in the African context. To our knowledge, there are no prior studies focusing on the role of regulations in CSR in Africa, so we aim to address this gap with this article.

As a result of the above arguments, we arrive at a model in which the effect of MNEs’ CSR commitment on local responsiveness is moderated by the regulatory distance between the MNE’s home and host countries. This is illustrated schematically in Figure 1.

Conceptual model showing moderating role for regulatory distance in the global–local CSR relationship.

The Role of the State Logic

In our second step, we seek to respond to the ambiguities in the global–local CSR literature by theoretically explicating the relationships in Figure 1 using an institutional logics perspective. In adopting this lens, we build on Kostova, Roth, and Dacin (2008), who point out the limitations of neo-institutional theory and its emphasis on isomorphism in explaining MNEs’ responses to complex and dynamic institutional environments in diverse host countries, within the MNE itself, and in the MNE’s global, meta-institutional field. An institutional logics perspective, however, lends itself well to an analysis of such heterogeneity (Greenwood, Diaz, Li, & Lorente, 2010; Thornton, Ocasio, & Lounsbury, 2012). We also follow Tan and Wang (2011) in applying this perspective to MNEs’ approaches to CSR, but do so in a different way. The institutional logics literature focuses on how macro-level, socially constructed assemblages of practices, beliefs, and values shape individual and organizational behavior (Thornton et al., 2012; see also Alford & Friedland, 1985; Besharov & Smith, 2014; Friedland & Alford, 1991; Jackall, 1988; Joseph, Ocasio, & McDonnell, 2014; Lounsbury, 2007; Meyer & Hammerschmid, 2006; Thornton & Ocasio, 1999).

Many of the early texts in the institutional logics literature emphasize the inconsistencies, contradictions, and incompatibility of institutional logics (Friedland & Alford, 1991; Thornton & Ocasio, 1999), with the result that analyses of organizations’ responses to numerous logics in situations of institutional complexity generally emphasize conflict and difficulty as outcomes (Greenwood, Raynard, Kodeih, Micelotta, & Lounsbury, 2011). Yet, according to Besharov and Smith (2014) logic multiplicity can take diverse forms, as logics have varying degrees of compatibility with each other and also varying degrees of relevance to an organization’s mission and identity. Furthermore, people do not always passively or uniformly react to institutional scripts; they can also bring agency to the process of responding (McPherson & Sauder, 2013; Thornton et al., 2012). For instance, Binder (2007) found that numerous logics can be combined in a process of bricolage or what Besharov and Smith (2014) referred to as blending.

Yet, for logics to be combined or blended by organizational actors, they need to be available and salient. The implication is that MNE subsidiary managers will create their responses to CSR depending on the logics that are available and salient to them, as they emanate from the host country environment, the firm-internal environment, and the global meta-institutional field (Kostova et al., 2008; Kostova & Zaheer, 1999). To identify which logics are salient for our purposes, we relate logics highlighted by Thornton et al. (2012) to the variables in our model in Figure 1.

Building on Besharov and Smith (2014), MNEs’ CSR commitment will be characterized by the blending of the market logic with what Thornton et al. (2012) called the “community logic” (p. 73), or what Besharov and Smith (2014) referred to as “social welfare, development, or sustainability logics” (p. 376). Committed CSR strategies emphasize cooperation and mutuality between the company and its stakeholders, they are informed by the community logic, which implies a belief in trust, reciprocity, cooperation, and transparency toward stakeholders. An implication is that, as an MNE’s CSR commitment increases, the pertinence of the community logic in the firm-internal institutional environment will increase for subsidiary managers. This logic’s emphasis on stakeholder engagement and mutuality would thus suggest that responsiveness to local approaches to CSR would also increase. This dynamic would explain findings by Kolk et al. (2010) and Cruz and Boehe (2010), but it is contradicted by findings by Muller (2006) and Bondy and Starkey (2014).

As noted above, we suggest such contradictions can be explained by the moderating role of regulatory distance and a corresponding, second logic. More specifically, given our interest in MNEs’ responses to local, state-driven variants of CSR, a key role is played by the state logic, which emphasizes the state’s role and hierarchical capacity to enforce commonly binding rules for the public benefit (Thornton et al., 2012, p. 73). In host countries such as South Africa, local CSR variants involve an explicit, prominent role of the state in defining and motivating CSR, and so the state logic is pertinent. If regulatory distance is low, the MNE’s home country environment also provides for a significant role for the state logic in defining CSR. Building on Matten and Moon’s (2008) framework, this will be the case if the MNE’s home country is one of the coordinated market economies, such as many European countries, in which actors are more likely to expect and legitimize a role for government that is “more engaged in economic and social activity” (Matten & Moon, 2008: p. 407). Given that the MNE internal institutional environment is influenced materially by its home country—due to head office policies and subsidiaries’ reliance on firm-internal resources (Hillman & Wan, 2005; Kostova & Zaheer, 1999; Tan & Wang, 2011)—this MNE internal environment will also “carry” the state logic as appropriate in defining and implementing CSR policies. As long as regulatory distance is low, there is thus an alignment between the MNE internal environment and the host country environment with regard to the role of the state logic in CSR. An increase in CSR commitment will thus elevate the pertinence of the community logic and an increase in local responsiveness, unperturbed by the state logic.

However, if regulatory distance is high, the home country environment is characterized by a voluntaristic approach to CSR, which allows for only a very limited role for the state in defining and motivating CSR. This will be the case, building again on, for MNEs headquartered in liberal market economies, such as the United States, which are characterized by a logic that emphasizes “corporate discretion” in the context of a “less active” government (Matten & Moon, 2008, p. 407). This gives rise to a potentially significant contradiction for the MNE subsidiary manager, because the host country environment expects a prominent role for the state logic in CSR, but the MNE internal environment—which, again, is shaped materially by the home country—prioritizes a voluntaristic approach to CSR. The MNE internal environment will be particularly influential, given the role of hierarchical structures, headquarters’ efforts to create firm-internal coherence, and subsidiaries’ reliance on MNE resources (Kostova et al., 2008; Kostova & Zaheer, 1999). This contradiction is particularly salient if there is a strong commitment to CSR, because this commitment is associated with a voluntaristic conception of CSR. Hence, if regulatory distance is high, increases in MNE’s CSR commitment will give rise to lower local responsiveness.

Summarizing the arguments above, we hypothesize as follows:

Method

The Research Setting: South Africa’s BEE Policy as Local, State-Driven CSR

South Africa’s industrialization relied on cheap labor to, among other things, make the extraction of underground resources feasible. This was supported by a range of measures including the 1913 Natives Land Act and formal “apartheid” policies after 1948 (Sparks, 2011; Terreblanche, 2002). The result of these colonial and apartheid policies has been a deeply divided and unequal society, a legacy that has been very difficult to address by the democratic governments since 1994. South Africa has one of the world’s highest Gini coefficients (a measure of socio-economic inequality). 2 Black South Africans continue to be largely excluded from control and ownership of the formal economy. Although the pertinent statistics depend on the definition of measures and the data used, it is estimated that direct Black ownership of publicly traded South African countries has remained below 10%, whereas about 10% is owned indirectly by Blacks through unit trusts and the like (Johannesburg Stock Exchange, 2011). Blacks occupied just more than 12% of top management positions in 2012 compared with 10% in 2002 (“Whites Still Dominate South African Management,” 2013).

This duality and continued racial characteristics of the rich, formal economy and the poor, informal economy have been prominent features of the post-apartheid government’s rhetoric and policy making. In 1998, South Africa’s then Deputy President, Thabo Mbeki, described South Africa as “two nations” 3 (Mbeki, 1998; Nattrass & Seekings, 2001). The most prominent government response has been its BEE policy framework, which found expression in a number of sector-specific, negotiated “transformation charters” (Hamann, Khagram, & Rohan, 2008), as well as an overarching BEE Act (53 of 2003) and subsequent “codes of good practice” (Arya & Bassi, 2009). They provide for a so-called BEE scorecard that assesses companies’ performance in four areas: (a) direct empowerment of Black people through ownership and control of enterprises and assets; (b) management by Black people at senior level; (c) human resource development and employment equity, to ensure access by Black people to job opportunities and career advancement; and (d) indirect empowerment through preferential procurement (prioritizing BEE companies), enterprise development (supporting small, Black-owned companies with training or access to finance), and “socio-economic development” focused on health, education, housing, or other social domains. Compliance has been sought primarily through two means. In some sectors, notably mining, companies’ access to necessary government licenses depends on their ability to show progress in improving their BEE scores. The second mechanism is through the government’s procurement system, which gives preference to BEE compliant companies. These two pressures are particularly pertinent to relatively large firms; but through the preferential procurement element in the BEE scorecard, they are implemented indirectly along supply chains throughout the economy.

Importantly, rather than being a national idiosyncrasy, South Africa’s BEE policy and the debates that have been surrounding it (Alessandri, Black, & Jackson, 2011; Ponte, Roberts, & van Sittert, 2007; Shubane & Reddy, 2005, 2007) can be seen as an expression of prominent debates, tensions, and state strategies in numerous African countries seeking to translate political independence from colonial powers into economic benefits for their African population. For instance, Zambia’s first President, Kenneth Kaunda, bemoaned the lack of businesses owned or managed by Zambians in the years following independence in 1965 (Kaunda, 1968, quoted in Beveridge, 1974). A common response by newly independent African states—including Zambia, for instance—has been nationalization, often precipitating a deleterious nationalization–privatization cycle (Chua, 1995). The alternative strategy has been to foster “indigenization,” which involves state policies requiring that companies involve locals as owners, managers, and suppliers. The tension between nationalization and indigenization has been prevalent in many African countries after independence (Wilson, 1990), especially in resource industries such as Nigeria’s oil sector (Ukiwo, 2008). Also in South Africa, critics of the government have complained that BEE is primarily about “elite enrichment” with little benefit for the poor (Freund, 2007; Ponte et al., 2007), and some have argued for nationalization of mines and banks as the preferred alternative (see Bond, 2013).

Given that BEE is premised on state regulation, why or how might it be interpreted as a form of CSR, as has been the case in a number of contributions to the CSR literature (Alessandri et al., 2011; Arya & Bassi, 2009; Juggernath, Rampersad, & Reddy, 2011)? Most of these contributions explicitly or implicitly argue for a link on the basis of a thematic overlap. For instance, Arya and Bassi (2009) explained as follows:

The Codes of Good Practice take a broad approach to CSR as they focus on increasing the incidence of principled behavior by South African organizations by altering organizational practices toward employees and by increasing corporations’ overall impact on society—yet they do not cover all areas of CSR. Instead, they focus on one area of CSR, namely, social issues directed at direct and indirect empowerment of historically disadvantaged people and building a diverse workforce. (pp. 677-678)

Focusing on this thematic overlap between BEE and CSR means that those thematic aspects of BEE that are outside the global CSR discourse—specifically the transfer of ownership to Black South Africans—are conveniently ignored. At least it may be argued that these aspects are not irreconcilable, given that international human rights law allows such “special measures” as long as they are not implemented indefinitely (e.g., de la Vega, 2010); though note there are no provisions in BEE policies specifying their end just yet). In addition, the ownership transfer elements of the BEE scorecard have been somewhat diluted for MNEs. This is because sharing control and equity with local Blacks has been the most contentious issue for MNEs. 4

Aside from the thematic alignment between BEE and CSR, however, an additional concern regarding these concepts’ commensurability may be related to BEE’s regulatory provenance. This would be premised on the assumption that CSR is primarily or even only about voluntary business actions that go beyond what is required by state regulation. Such a perspective is represented in the scholarly literature (McWilliams & Siegel, 2001) and has been identified as prominent especially in the U.S. context (Matten & Moon, 2008). Whereas early, draft European policies on CSR also emphasized its voluntary aspects (European Commission, 2001), more recent policies identify a close interrelationship between CSR and government regulation (European Commission, 2011; see also Vogel, 2010). The assumption of CSR as a voluntary business pursuit has thus diminished and CSR is a prominent theme in diverse public policies (Arya & Bassi, 2009; Campbell, 2007; Fox, 2004; Knudsen, Moon, & Slager, 2014; Matten & Moon, 2008; McBarnet, Voiculescu, & Campbell, 2007; Moon & Vogel, 2008; Steurer, 2010). This broadened conception of CSR is thus able to include state-driven policy frameworks, such as BEE in South Africa. A prominent role for the state in delineating CSR has also received dedicated attention among scholars focused on South Africa and other African countries (Hamann et al., 2005; Muthuri & Gilbert, 2011; Mzembe & Meaton, 2013).

A second aspect worth noting is that despite its regulatory provenance, business responses to BEE are characterized by significant diversity in terms of motives and commitment. In terms of implementation, some of this variance is related to the BEE codes themselves, which allow for varying degrees of performance. There is thus some strategic discretion provided for companies with regard to the level of their BEE commitment. In terms of motivation, some companies have interpreted BEE as an onerous regulatory burden, a tax, or even an infringement of bilateral trade agreements. 5 Others have highlighted its normative appropriateness (Chabane, Roberts, & Goldstein, 2006) or the longer term business benefits, including access to a broader skills base and mitigating the risk of populist government policies, such as nationalization. 6 In sum, these various factors—thematic overlaps between BEE and CSR, a broadening of CSR conceptions to include state regulation, and variations in strategic commitment and motivation to respond to BEE requirements—combine to make BEE a prominent local variant of the global CSR movement. They also highlight the pertinence of considering why some MNEs may give more attention to BEE than others.

Measures and Data Collection

Our unit of analysis is the foreign-based MNE operating in South Africa. We collected data on MNEs’ BEE scores and CSR performance focusing on environmental and on human rights criteria. All in all, we assessed the BEE and CSR performance of 93 publicly listed companies with significant operations in South Africa. 7 These companies were identified by choosing the largest investors in operations in South Africa from each of the three most prominent areas of origin: Europe (36 companies), Asia (27 companies), and North America (30 companies). The data were collected during 2010 from these companies’ public reports, including company websites, annual reports, and sustainability reports for the year 2009. The content analysis of these texts gave rise to quantitative data representing our independent and dependent variables.

Global CSR

This is our key independent variable measuring MNEs’ global CSR commitment. We opted to measure MNEs’ CSR commitment through a content analysis of their public reports so as to ensure a coherent approach that covers a broad array of CSR themes. An alternative might have been to consider third-party assessments by stock exchanges or analysts. But, we worried that available assessments of this sort do not include MNEs from different regions and/or do not cover a broad array of CSR themes.

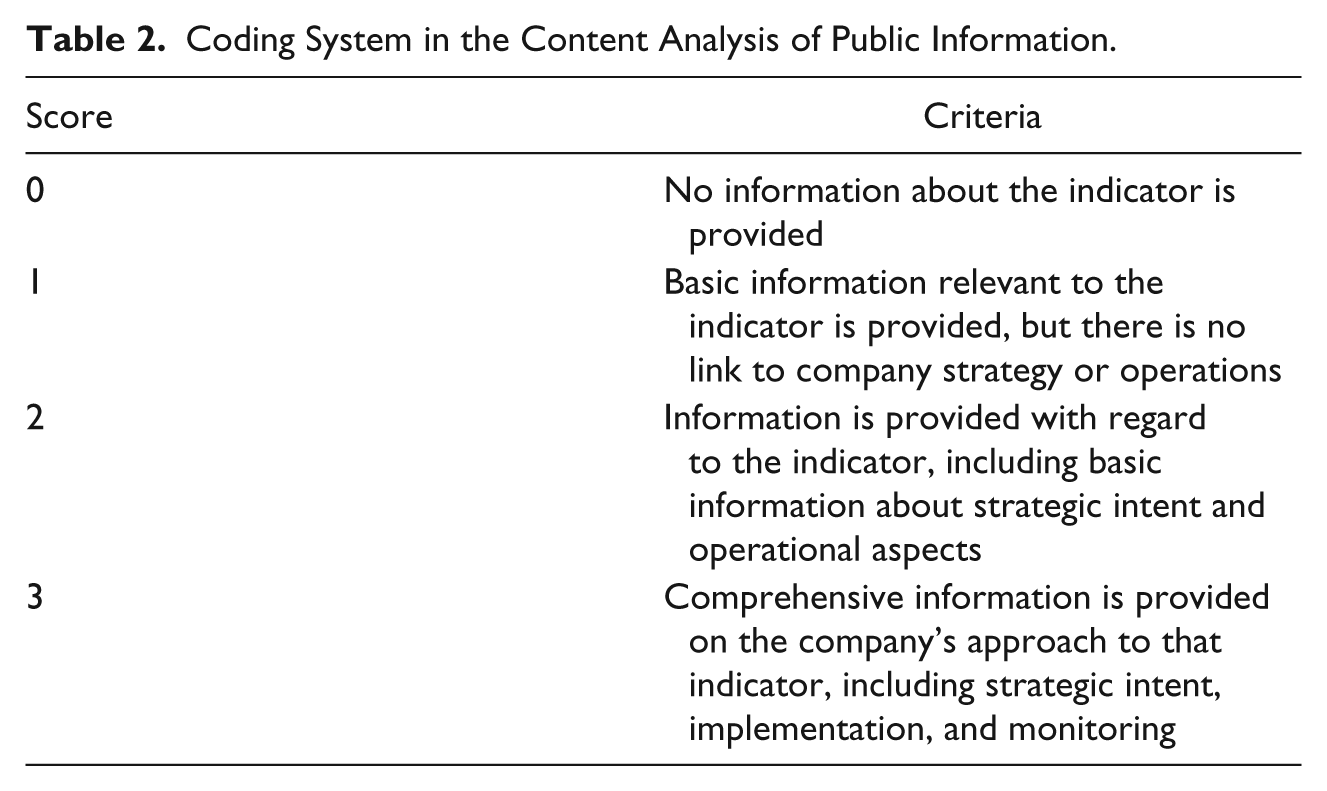

We measured the Global CSR variable by means of 13 items focused on the extent to which human rights and environmental issues were addressed in firms’ policies, practices, and management structures, and the extent to which such efforts were motivated explicitly with reference to competitiveness, ethics, or compliance. These items are listed in Table 1. Each item was given a score between 0 and 3 depending on how systematically and rigorously it was addressed by the firm, as described in the public reports. We adapted our coding schematic from Hamann, Sinha, Kapfudzaruwa, and Schild (2009); and, a similar 4-point scale was applied in an analysis of corporate reports by Dawkins and Ngunjiri (2008). Based on methodological recommendations for content analysis (Krippendorff, 1980), the coding process was guided by a scoring schematic, as provided in Table 2. We checked for item correlations against the rest of items in the scale and removed those items with correlations less than .5. Our standardized scale resulted in a Cronbach’s alpha value of .90.

Global CSR Items.

Note. CSR = corporate social responsibility.

Coding System in the Content Analysis of Public Information.

Local CSR (BEE)

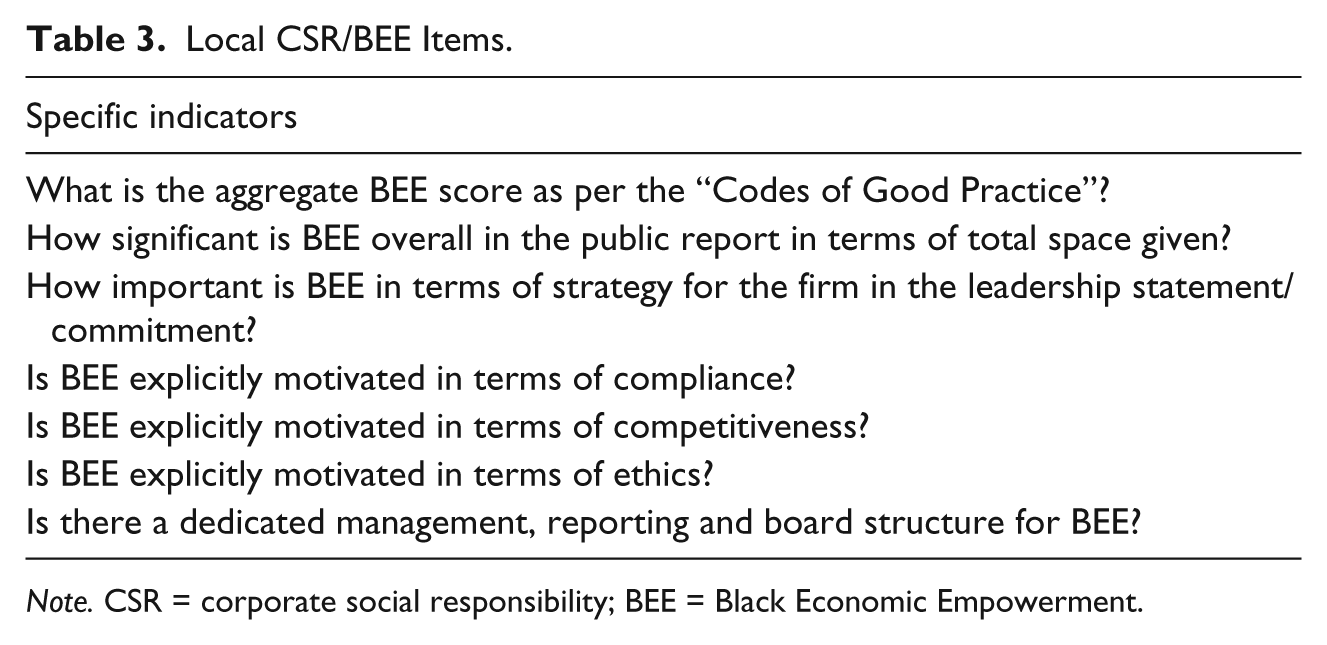

This is our dependent variable. MNEs’ local CSR efforts, through BEE, were also assessed by examining public reports using the content analysis scoring schematic provided in Table 2. The specific items are listed in Table 3 and generally focus on the extent to which BEE-specific themes are addressed in firms’ policies, practices, and management structures, and the extent to which they are motivated explicitly. One of the items focuses on the company’s formal BEE score, which is generally calculated and assured by third-party verification agencies, based on criteria established in the government’s “Codes of Good Practice” (see also Arya & Bassi, 2009). It could be argued that we should rely entirely on this externally assured measure, but we assessed this as part of the content analysis schematic and together with other items for two reasons. First, not all 93 MNEs reported their formal BEE scores and efforts to obtain these data from the South African government were unsuccessful. We thus gave companies that did not report their formal BEE score a 0 for this item and companies that did report the formal BEE score were coded in correspondence with this score. Second, our research question is focused on the degree to which firms respond to local CSR expectations as being congruent with their broader CSR approach, so we wanted to measure not just firms’ BEE performance per se, but also the extent to which they publicly reported on this as part of their CSR-related communication to stakeholders. The Cronbach’s alpha value for our resulting scale of seven items is .85.

Local CSR/BEE Items.

Note. CSR = corporate social responsibility; BEE = Black Economic Empowerment.

A number of additional means were implemented to enhance the reliability of the coding process. For a start, the definition of hypotheses and the coding process were undertaken by different members of the research team. The coding was thus done without any knowledge of the hypotheses. In addition, an inter-coder reliability test was conducted. Ten companies (representing 10% of the original sample of 100 companies) were coded by two researchers simultaneously. We calculated the Krippendorff alpha (Hayes & Krippendorff, 2007) to measure the degree of agreement between these coding sets, with alpha scores between .67 and .80 representing sufficient reliability (Krippendorff, 1980). The average alpha score for our sub-set of companies was .71, with none of the companies in our sub-set having a score below .60. We are thus reasonably confident in the reliability of the data for our Global CSR and Local CSR variables.

We are cognizant of the limitations associated with a cross-sectional design based on data that were largely collected from companies’ public reports. It may thus be argued that we are measuring CSR and BEE disclosure, not performance itself. However, many of the indicators, though based on public disclosure, intentionally include aspects of performance beyond the existence of policies and programs (this is an explicit intention of the Human Rights Compliance Assessment, on which our CSR and some of the BEE indicators are based—see Danish Institute for Human Rights, 2006, 2008, and Hamann et al., 2009). Furthermore, our focused research question is specifically about the degree to which local, state-driven variants of CSR are seen by MNE subsidiaries as connected to global CSR and communicated as such. That is, disclosure is an important aspect of what we are measuring in both the independent and dependent variables. Nevertheless, we recognize this as a constraint in our methodology (on the role of reporting and its links to performance and accountability, see Dawkins & Ngunjiri, 2008, and Kolk, 2008).

We also recognize possible risks associated with the fact that both our dependent and independent variables arise, in the main, from the same secondary data source; that is, common methods bias. We mitigate possible problems associated with a common rater (Podsakoff, MacKenzie, Lee, & Podsakoff, 2003) by means of the efforts to enhance coding reliability mentioned above. We also ensured that our measures included at least five items. Finally, our interaction model is complex and thus difficult to visualize, which further reduces common method bias (Chang, Van Witteloostuijn, & Eden, 2010).

Regulatory distance

To measure regulatory distance between host and home countries, we used data from the World Economic Forum Global Competitiveness Report for 2006-2007 (World Economic Forum, 2006). The report measures a range of economic, infrastructural, and political variables in 148 nations, grouped into nine pillars that are considered “critical to driving productivity and competitiveness” (World Economic Forum, 2006, p. 5). One of these pillars is “institutions,” and one of the measures most directly related to governments’ efforts to regulate economic activity focuses on respondents’ perception of regulatory burden. We focus on this particular measure because regulatory requirements specifying social obligations are often perceived as burdens by managers (Porter, Schwab, Sala-i-Martin, & Lopez-Claros, 2004). Specifically, the question posed to business leaders was, “In your country, how burdensome is it for businesses to comply with governmental administrative requirements (e.g., permits, regulations, reporting)?” Responses were on a scale from 1 to 7. The average number of respondents per country was 90 (World Economic Forum, 2006, p. 59). 8

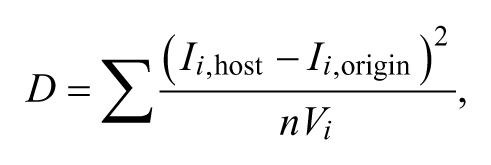

To estimate the “distance,” we use the Kogut and Singh (1988) formula below:

where Ii,host (Ii,origin) is the ith dimension of the index for the host country (country of origin) and Vi is the variance of the ith dimension and n is the number of dimensions used. In our case, n was equal to one.

Control variables

To control for competing explanations, we included a number of other variables considered significant. Because our dependent variable is BEE performance, we control for factors that could systematically affect BEE performance. Responses to institutional idiosyncrasies may be affected by organizational attributes such as size, age, or industry segment (Henisz, 2003). Accordingly, we control for market capitalization of the MNE, the number of years that the MNE has been operating in South Africa, and the economic sector of the MNE. Market capitalization was used as a proxy for size, which has been shown to influence an enterprise’s CSR performance particularly for North American MNEs (McWilliams & Siegel, 2001; Sotorrío & Sánchez, 2008). We also expect that an MNE that has been operating in SA for a long period will have had more opportunities to respond to the local institutional context and its stakeholders.

We expect MNEs in those sectors that are dependent on government licenses and procurement to experience greater pressure to implement BEE. MNEs within the mining and oil and gas sectors rely on the state to grant them licenses to operate. Other MNEs in service type sectors (e.g., consulting, finance, and information technology hardware and software) rely on the state procurement for a significant amount of their revenue. Public hospitals and clinics also procure a significant amount of pharmaceuticals. We use a dummy variable labeled “procurement and license pressure” where 1 represents those sectors relying on state licenses and/or procurement and 0 represents those that do not.

Analysis

We use multiple regression to test the significance of global CSR, regulatory distance, and respective interaction terms. This interaction term was necessary to model the contingency effect of regulatory distance on the global CSR–local CSR relationship (Cohen, Cohen, West, & Aiken, 2013). We tested for an interaction effect by observing the significance of the interaction term. Bearing in mind our hypothesis on the nature of the interaction, the significance of the interaction term signaled the importance of examining the particular interaction further. We plotted the slopes (Dawson & Richter, 2006) to examine the nature of the interaction.

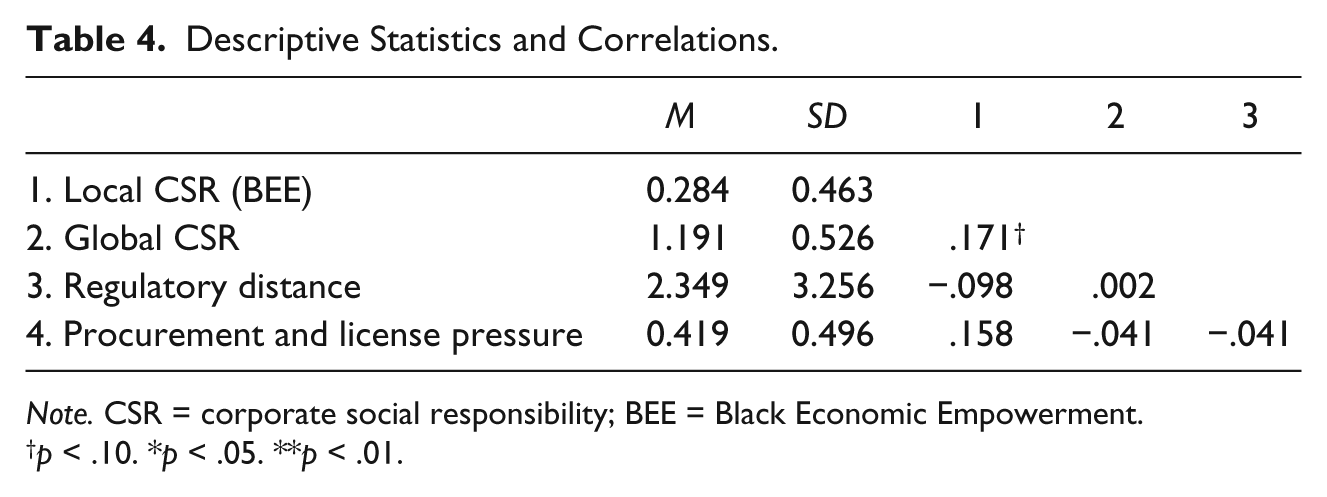

To simplify the model, we removed those control variables that turned out to be not significant. These were size (market capitalization) and the time spent by the MNEs in South Africa. We suggest that although size may influence CSR performance (McWilliams & Siegel, 2001; Sotorrío & Sánchez, 2008), and although duration of local presence may influence local responsiveness, per se, these variables need not markedly influence our hypothesized interaction between CSR commitment and regulatory distance. Once these control variables were removed, the model’s interaction term remained statistically significant and did not change sign from the original model with all control variables. We therefore, removed these variables from our correlation matrix in Table 4 and the final models shown in Table 6. We attribute the relatively large difference between adjusted r2 and r2 to our small sample size of 93 MNEs.

Descriptive Statistics and Correlations.

Note. CSR = corporate social responsibility; BEE = Black Economic Empowerment.

p < .10. *p < .05. **p < .01.

Results

The means, standard deviations, and correlations of the variables are displayed in Table 4. Although there are no high correlations between independent variables, we mean centered the variables before creating the interaction terms to ensure that multicollinearity was not an issue (Aiken & West, 1991). 9 Resultant variation inflation factors were less than 5.

Table 5 characterizes the cases across the four possible idealized combinations of our independent variable (global CSR commitment) and the moderating variable (regulatory distance). It shows that each of these four types was represented relatively equally in our sample, which is helpful for our statistical analysis. Although there is no clear differentiation of industries, home countries with relatively low regulatory distance were China, France, Germany, India, and the United Kingdom, whereas the home countries with relatively higher regulatory distance included in particular Japan and the United States. (This is broadly in line with analyses of national business systems; Witt & Redding, 2013; see also Note 8.)

An Overview of Cases in Our Sample in Terms of Combinations of Independent and Moderating Variables.

Note. CSR = corporate social responsibility; IT = information technology.

Table 6 presents the results of the regression analysis. Model 1 includes all variables without the interaction term. Note that the relationship between global CSR and local CSR is significant only at the 10% level, supporting our argument that there is no universal effect of global CSR on local CSR.

Regression Results.

Note. CSR = corporate social responsibility; BEE = Black Economic Empowerment.

p < .10. *p < .05. **p < .01. ***p < .001.

Our hypothesis suggests that the moderating effect of regulatory distance would be significant. Our results displayed in Model 2 (β = –.140, p < .01) support this. The negative sign of the interaction term supports our hypothesis with regard to the directionality of the moderating effect of regulatory distance on the global CSR–local CSR relationship. We also use a graph to confirm this, as depicted in Figure 2. It shows that increases in global CSR commitment have a positive effect on local CSR responsiveness when regulatory distance is low. In contrast, increases in global CSR commitment have a negative effect on local CSR responsiveness when regulatory distance is high.

Moderating effect of regulatory distance on the global CSR–local CSR responsiveness relationship.

Discussion

Our study set out to understand how MNEs respond to local, state-driven versions of CSR common in many African countries. Such “indigenization” or “Black empowerment” policies have been and still are common in Africa, as governments seek to translate political independence from colonial or apartheid powers into economic benefits for the local African population. They commonly require domestic and multinational companies to give preference to designated groups in the company’s ownership, employment, and procurement, and also to contribute to broader social development initiatives. In our empirical analysis, we focused in particular on South Africa’s BEE policy, which we described as a prominent local variant of the global CSR movement despite its thematic idiosyncrasies and regulatory provenance. Although we see BEE as an example of African governments’ attempts to define legitimate corporate behavior in a post-colonial context, there are differences in kind and in degree between these attempts, so pan-African generalizations will need to be made with caution.

The extant literature on global–local CSR could not provide clear predictions for how MNEs would respond to state-driven, local CSR variants such as BEE. Some suggest that high global CSR commitment provides firms with the motivation and ability to respond to local CSR variants (Cruz & Boehe, 2010; Kolk et al., 2010), whereas others argue that it leads to managers prioritizing internal legitimacy at the expense of local responsiveness (Barkemeyer & Figge, 2014; Bondy & Starkey, 2014; Kostova et al., 2008; Muller, 2006; Tan & Wang, 2011). We noted that these uncertainties about the relationship between global CSR commitment and local responsiveness are reflected in doubts and queries voiced by practitioners in both public and private sectors (see also Chahoud et al., 2011).

We responded to these uncertainties in theory and practice by proposing that the relationship between global CSR commitment and local responsiveness is moderated by regulatory distance. We focused on regulatory distance instead of a broader, aggregate construct of institutional distance because of our interest in African, state-driven CSR variants and to develop a more specific argument. We then predicted the outcomes of this interaction using an institutional logics perspective. Specifically, we argued that for MNEs from a home country, in which the state is expected to play a more interventionist role in defining CSR, an increase in global CSR commitment will lead to a greater responsiveness to local, state-driven CSR such as BEE. For such firms, the local, state-driven variant is seen as compatible with their global CSR commitment. However, in the case of MNEs from a home country, in which CSR is seen in voluntaristic terms and where the state is not expected to be involved in defining or even regulating CSR, an increase in global CSR commitment will lead to a widening gap between the firm’s conception of CSR and local, state-driven CSR. This gap leads to resistance to connecting state-driven variants of CSR such as BEE to the firm’s global CSR efforts. Our analysis of data collected from 93 MNEs from diverse home regions operating in South Africa supported these hypotheses.

Contributions and Implications

Our primary contribution is to the literature on global–local CSR (Barkemeyer & Figge, 2014; Bondy & Starkey, 2014; Campbell et al., 2012; Cruz & Boehe, 2010; Gardberg & Fombrun, 2006; Kolk et al., 2010; Kostova et al., 2008; Muller, 2006; Salomon & Wu, 2012; Tan & Wang, 2011; Yang & Rivers, 2009). We build on Campbell and colleagues’ (2012) argument on the important role of administrative distance, first, by contextualizing and focusing the analysis on state-driven local CSR variants (implied in their study) and on regulatory distance as a more specific dimension of institutional distance. We extend their analysis by using regulatory distance not as an independent variable, but as a moderator of the role of firms’ global CSR commitment.

Furthermore, we theorize the impact of this interaction using an institutional logics perspective. We use this theoretical lens to argue that the MNE internal institutional environment (the importance of which has been emphasized by Kostova et al., 2008, and Kostova & Zaheer, 1999) “carries” the state logic so as to influence MNEs’ responsiveness to local, state-driven CSR variants. Our second contribution is thus to illustrate the potential of the institutional logics perspective in the global–local CSR debate (building on Tan & Wang, 2011).

Our model allows us to make the counter-intuitive argument that MNEs with greater global CSR commitment will be more or less responsive to local, state-driven CSR variants depending on their origin. This aids our nascent understanding of CSR in the African context, where many governments have policies focused on enhancing Africans’ ownership of and inclusion in economic activity. This is likely to be an enduring characteristic of CSR in Africa, also considering calls for state regulation to improve CSR uptake in Africa (Muthuri & Gilbert, 2011; Mzembe & Meaton, 2013).

So, even while the “explicit” CSR approach that emerged in the United States—which generally expects only a minor role for the state in defining business responsibilities—is becoming increasingly globalized (Matten & Moon, 2008), CSR in Africa will develop with a strong role for the state in defining at least some dimensions of CSR. This prominent role for the state is juxtaposed paradoxically to the relative weakness of many African states, which creates rather different motivations for CSR as a way to fill gaps in the provision of public goods (Börzel & Hamann, 2013; Scherer & Palazzo, 2011). The African context thus gives rise to diverse motives for CSR, which in turn will give rise to novel hybrids between “explicit” and “implicit” CSR (Matten & Moon, 2008). Our third contribution is thus to extend Matten and Moon’s (2008) framework to the context of MNEs straddling different institutional business systems. This allows us to show that CSR in Africa will be shaped by not only the complexities of the local institutional context but also MNEs’ home country institutions.

We have argued that MNEs’ responses to local, state-driven variants of CSR will not be uniform, as might have been expected from neo-institutional theory, or as is commonly assumed by policy makers. Also, such responses will not be easily predicted with regard to the MNEs’ global CSR commitment. This has implications for policy makers, who will need to recognize that MNEs’ narratives about CSR are not uniform. In particular, although some companies’ global CSR commitments may give rise to a proactive approach to local, regulation-driven versions of CSR, similar commitments from other MNEs will in fact have the opposite effect. A policy implication of this might be that quasi-discretionary aspects of policies such as South Africa’s BEE policy might need to be backed up with clearer and more explicit compliance-driven expectations. For managers in MNEs, our analysis suggests that their firm-internal expectations of the role of the state might predispose them to resistance to local, state-driven approaches to CSR, thus preventing the kind of response hoped for by the local state and possibly leading to acrimony in the political process of negotiating legitimacy (Kostova et al., 2008).

Limitations and Further Research

Our study has the following limitations. First, our model focuses on the global–local CSR relationship in those instances, when the local variant is state-driven. We motivated this focus with reference to our particular interest in the African context, where state-driven local CSR variants are prominent. This means, however, that our model will not necessarily apply in instances where the defining differences between host and home country institutions are not regulatory in nature. Further research may want to consider other disaggregated aspects of institutional differences (Jackson & Deeg, 2008; Xu & Shenkar, 2002), such as cognitive structures or cultural norms, and how they influence the relationship between firms’ global commitments and local responsiveness. Furthermore, we do not empirically address the substantive differences between ostensibly global standards for CSR, such as the United Nations Global Compact, and what Tan and Wang (2011) called idiosyncratic ethical pressures prominent in local institutional contexts. Focusing on the role of local CSR variants’ substantive content, over and above their regulatory provenance, is an additional avenue for further research.

A second limitation relates to our methods and data. Our sample is limited to 93 observations. As a result, we chose a simple model with only a single control focusing on “procurement and/or license pressure” faced by MNEs to implement BEE. We were able to remove the controls for size (market capitalization) and the time spent by the MNEs in South Africa from the final model, because the interaction term—on which we rely for empirical support of our argument—remained statistically significant and did not change sign in this process. We also reiterate possible limitations related to our reliance on companies’ public reports for many of our measures, as well as the imperfect proxy relied upon for regulatory distance. However, we have sought to mitigate the limitations of our sample and of our data sources by making the model as simple as possible and through a range of other efforts, as outlined in our “Method” section. We also highlight the exploratory nature of our study as part of a nascent literature on CSR in Africa. Subsequent research will need to develop these ideas in other contexts and with larger, more diverse, and more nuanced data sets.

Finally, attentive readers may have noticed the striking fact that the lines in Figure 2 cross. That is, our findings not only show that an increase in global CSR commitment gives rise to increasing or decreasing local CSR commitment, depending on regulatory distance but also suggest that among those companies that have a low global CSR commitment, those with high regulatory distance are more locally responsive than those with low regulatory distance. This was a significant surprise for us that could not be explained by our theoretical reasoning (though it may well have to do with the “distance paradox” identified by O’Grady and Lane, 1996). We also do not feel confident in using our data and analysis to explicate this post hoc. This surprising finding will thus need some further attention.

Conclusion

The question of how MNEs respond to local variants of CSR is of scholarly and practical interest. In many African countries, CSR is partly defined by governments’ attempts to regulate and incentivize companies’ behavior to enhance indigenous Africans’ access to economic opportunities. We argued that despite some areas of thematic divergence and the regulatory provenance of such policies, such as BEE in South Africa, their link to global CSR is nevertheless relevant due to thematic overlap, a broadening of CSR conceptions, and some degree of discretion in firms’ responses. It is this juxtaposition of distinctiveness and similarities that makes state-driven CSR such as BEE such an interesting local variant of the global CSR movement. Yet, some MNEs laying claim to global leadership in CSR and sustainable development are nevertheless resistant to BEE. This has been puzzling to local policy makers, but is explained in our analysis. We show that MNEs’ local responsiveness is influenced by the regulatory distance between home and host countries, and specifically the degree to which an MNE’s firm-internal conception of CSR allows for a prominent role for the state in defining CSR. For MNEs from home countries with a weak state logic, an increase in global CSR commitment leads to diminished willingness to engage in local, state-driven business responsibilities as part of the firm’s global CSR. CSR in Africa is thus shaped by not only complex local contexts but also MNEs’ home environments and their effect on firm-internal environments.

Footnotes

Acknowledgements

The authors are grateful for comments and guidance from three anonymous reviewers and the guest editors Miguel Rivera-Santos and Ans Kolk. Helpful comments were also received from reviewers for the Academy of Management Annual Meeting 2015. The authors are very thankful to Ted Baker and Stephanie Bertels for important help in later stages of this project.

The article was accepted during the editorship of Duane Windsor.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Research leading to this article was supported by the Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ; German development cooperation), the National Research Foundation of South Africa, and the UCT African Climate and Development Initiative.