Abstract

Research on corporate political activity has considered a number of antecedents to a firm’s engagement in politics. The majority of this research has focused on either industry or firm-level motivations that lead to corporate political activity, leaving the role of the firm’s leader noticeably absent in such scholarship. This article combines ideas from Upper Echelons Theory with research in corporate political activity to bridge this important gap. More specifically, this research utilizes CEO demographic characteristics to determine (a) whether a firm will invest in political activity and (b) how these characteristics influence the particular approach to political activity the firm undertakes. Considering 27 years of data from large U.S. firms, we find that a CEO’s age, tenure, functional, and educational backgrounds influence whether and how the firm invests in political activity.

A core function of the firm’s CEO is to manage the interface between the firm and its external environment (Finkelstein & Hambrick, 1996). As a result, a considerable amount of scholarship from Upper Echelons Theory (UET) has considered the actions that CEOs take to manage the firm’s success in the market environment (see Finkelstein, Hambrick, & Cannella, 2009, for a review of this literature). However, firms also operate in the nonmarket environment which Baron (1995) described as firm interactions with the government, media, or public institutions with the intent of improving corporate performance. Recent scholarship has considered the CEOs impact on the firm’s decision to engage the nonmarket environment. For example, Borghesi, Houston, and Naranjo (2014) found that female and younger CEOs were more likely to invest in corporate social responsibility (CSR) initiatives. Chin, Hambrick, and Treviño (2013) found that CEO political ideology influences firm investment in CSR initiatives as well as political action committee (PAC) contributions. Although this research explores the relationship between the CEO and firm nonmarket action, we still know little about the influence that CEOs have on the corporate political activity (CPA) undertaken by the firm. Yet, research has found that CEOs have become increasingly focused on the firm’s government affairs activity, in many cases even engaging policy makers themselves (Foundation for Public Affairs, 2008).

Extant research has found that firms engage in CPA for a number of reasons. For example, scholars have identified firm size (e.g., Hillman, 2003; Meznar & Nigh, 1995), slack resources (e.g., Meznar & Nigh, 1995; Schuler, 1996), firm age (e.g., Hillman, 2003; Keim & Baysinger, 1988), and market share (e.g., Schuler, 1996) as all positively related to a firm’s propensity to invest in political activity (see Hillman, Keim, & Schuler, 2004, for a review of this research). Furthermore, research utilizing agency theory has found that different ownership structures influence firm CPA (e.g., Hadani, 2012; Ozer & Alakent, 2013). Despite this extensive line of research, little has been done to examine the relationship between the individual characteristics of the CEO and firm investment in CPA. Therefore, in this study, we seek to answer a two-part research question. First, we ask “To what extent do CEO characteristics affect the firm’s investment in political activity?” Within this first question, we ask a second: “How do CEO characteristics affect the approach that a firm takes when investing in political activity?”

Hambrick and Mason (1984) argued that organizational outcomes can be viewed as reflections of the values and cognitive perspectives of top managers in the organization. In this research, we follow UET and argue that characteristics of the firm’s CEO have predictable relationships with a firm’s investment in political activity. However, Hillman and Hitt (1999) distinguished between two approaches firms take to political activity: relational and transactional CPA. Relational CPA is proactive and associated with a long-term and continuous interaction with policy makers that occurs through the firm’s Washington, D.C. office. Transactional CPA is reactive and described as occurring only when the firm identifies an issue which demands its attention. As a result, firms hire outside lobbying organizations to undertake transactional CPA. This distinction between relational and transactional CPA allows us to go substantially beyond a traditional UET study on the effects of CEO characteristics on the firm’s use of CPA; this research considers how CEO characteristics impact the approach to CPA that the firm undertakes.

This article seeks to make a number of contributions. First, we highlight the importance of the CEO in the firm’s strategic decision to engage in CPA. CPA investment represents a firm’s engagement in the nonmarket environment to gain competitive advantage and such investment can have important performance outcomes for the firm (e.g., Boddewyn, 2003; Bonardi, Holburn, & Vanden Bergh, 2006; Hillman, Zardkoohi, & Bierman, 1999; Shaffer, Quasney, & Grimm, 2000). However, we go beyond the question of “whether” specific CEO characteristics effect a firm’s investment in CPA and consider the influence of these characteristics on “how” the firm chooses to engage in CPA. In exploring this question on “how” firms choose to engage in CPA, we make an important contribution to the nonmarket strategy literature by providing a nuanced understanding of the critical individual-level drivers that motivate specific approaches to firm CPA.

Second, we seek to contribute to the ongoing debate between the role of the top manager in the firm and organizational outcomes (cf., Lieberson & O’Connor, 1972; Thomas, 1988; Weiner & Mahoney, 1981). By considering how a CEO’s demographic characteristics differentially impact a firm’s investment in CPA, an investment that has primarily been explained in the past by industry and firm-level attributes, we provide new evidence of the importance of top executives within the firm. Furthermore, by exploring how CEO characteristics impact the firm’s likelihood of investing in specific approaches to CPA, we offer a link between individual-level characteristics and the firm’s propensity to invest in political capabilities that can influence the long-term success of the firm.

Finally, we note that CPA scholarship has often utilized an agency perspective to explain a firm’s political investments (e.g., Getz, 1993; Hadani, 2012; Mitnick, 1993; Ozer & Alakent, 2013). This research has argued that CEOs seek to gain personal benefits from the firm engaging in CPA and hence predicts uniform political activity from the firm when certain ownership structures are present. Although this approach makes sense from a corporate governance perspective, we believe that the UET approach utilized in this research has the ability to go beyond such homogeneous predictions by tapping into the unique perspectives of the firm’s leaders. Put differently, while previous scholarship has theorized that CPA is the result of the firm’s managers seeking to maximize managerial benefits such as compensation or employability (Aggarwal, Meschke, & Wang, 2012; Arlen & Weiss, 1995), we provide a more direct assessment of the specific types of CPA in which a firm invests and link it to the unique characteristics of the firm’s CEO. In so doing, we hope to provide a more complete picture of the motivations driving a CEO to invest in CPA.

In the next section, we provide an overview of the literature on CPA, focusing in particular on the different approaches to CPA that firms undertake. The subsequent section offers arguments for how different CEO characteristics impact a firm’s investment in different types of political activity. The methodology used to test our hypotheses and results are then presented. Finally, a discussion of the results and implications for future research are offered.

CPA

The field of CPA has been described in a number of ways. Baysinger (1984) characterized CPA as efforts by firms to shape public policy in ways that are favorable to the firm. Oliver and Holzinger (2008) defined strategic political management as “the set of strategic actions that firms plan and enact for the purpose of maximizing economic returns from the political environment” (p. 496). These two definitions are linked by the idea that firms take strategic action in the nonmarket environment, which is comprised of legal rules and governmental actors, in the pursuit of competitive advantage (Baron, 1995).

Firms may choose to engage the government for a number of different reasons. For example, Baysinger (1984) developed the ideas of domain management, domain defense, and domain maintenance. He described domain management as a firm-specific improvement resulting from political action, domain defense as a set of political activities designed to maintain a stable environment via challenging proposed legislative changes, and domain maintenance as a defense against threats “to the methods by which organizational goals and purposes are pursued” that firms undertake in the political arena (Baysinger, 1984, p. 249). Oliver and Holzinger (2008) dichotomized CPA into defensive political strategies and proactive political strategies. Defensive political strategies seek to maintain the status quo of the firm’s competitive environment. Alternatively, proactive political strategies seek to create value for the firm by shaping the rules that govern the firm’s competitive environment. There are also a number of specific activities in which firms may choose to engage as part of a defensive or proactive political strategy (Hillman & Hitt, 1999). Corporate lobbying, PAC contributions, constituency building, and grassroots efforts have all been identified as viable corporate tactics for firms engaging in the political process (Baysinger, 1984; Epstein, 1969; Keim, 1981).

A firm’s approach to CPA is perhaps as important as its motivation for engaging in CPA. Hillman and Hitt (1999) developed a model that distinguishes between relational and transactional approaches to CPA. A relational approach to CPA occurs when firms “pursue political strategies over the long-term, rather than on an issue-by-issue basis” (Hillman & Hitt, 1999, p. 828). Relational CPA tends to be associated with the firm’s employment of individuals that are housed within the firm’s government affairs office, typically in Washington, D.C. As a result, a relational approach to CPA tends to be costly. Such an approach is also more likely to align the firm’s political strategies with its broader competitive strategy (Kollman, 1998). Thus, relational approaches to CPA are characterized as long-term focused and costly which firms utilize when public policies are deemed to be sufficiently important to the firm’s competitive position (Levine, 2009).

In contrast, transactional approaches to CPA tend to be more short-term focused and less costly (Hillman & Hitt, 1999). Firms using a transactional approach are more likely to contract with external lobbying organizations to engage policy makers on their behalf. Kersh (2002) suggested that this is because external lobbyists are highly capable of “navigating through agencies and offices based upon their personal knowledge and personal connections” (p. 240). Engaging in transactional CPA is more likely to occur when a firm only has intermittent dealings with the government and thus it does not make sense to establish and staff a full-time government affairs office in Washington, D.C. As a result, firm engagement in transactional CPA tends to require lower resource commitments.

Research has sought to understand why firms would choose to engage in relational or transactional political activity (e.g., Gais & Walker, 1991; Hojnacki & Kimball, 1999; Ozer & Alakent, 2013). In general, this research has proposed that the internal government affairs employees associated with relational CPA are more akin to “watchdogs monitoring the day-to-day activity of Congress flagging potential issues of interest for their company” while external lobbyists employed in transactional CPA tend to be specialists utilizing their unique connections when called upon by firms (Bertrand, Bombardini, & Trebbi, 2011, p. 11). Thus, engaging in relational CPA, while costlier and more time-consuming than transactional CPA, can also result in the firm developing political capabilities that can be utilized to improve not only the firm’s performance in the nonmarket environment but also its overall competitive advantage.

Our main proposition is that a firm’s investment in CPA is influenced by the characteristics of its CEO. More specifically, we propose that a firm will invest in one of two different approaches to CPA, relational or transactional, based on its CEO’s unique demographic characteristics. This proposition is based on three assumptions. First, we assume that CPA is an investment that top executives have the discretion to control in firms. Because government affairs is an activity that falls under the control of many top executives (Foundation for Public Affairs, 2008), we expect that top managers monitor CPA investment and adjust its level based on their preferences. Second, we assume that CEOs have the greatest organizational power to influence investment in CPA as the CEO is often the central strategic decision maker and can even control the composition of the organization’s top strategy-making group (e.g., Zahra & Pearce, 1989). Extant research has suggested that even in heavily regulated environments, with inherently low levels of discretion, political activity is considered to be one area where decision makers do have managerial discretion (Dahan, Hadani, & Schuler, 2013; Finkelstein & Peteraf, 2007; Peteraf & Reed, 2007). Finally, following the UET perspective (e.g., Hambrick & Mason, 1984), we assume that a CEO’s preferences for various levels of CPA investment are associated with observable CEO characteristics such as age, tenure, functional background, and educational background. Although this demographic approach is not without its limitations (see Lawrence, 1997), we believe it is an excellent initial approach for examining whether relationships between CEOs and firm CPA exist in a large sample of firms, especially given the paucity of empirical studies on this topic.

In the next section, we combine ideas from UET with the choice of firms to invest in political activity in general as well as in relational and transactional political activity. Research has yet to consider the role of the CEOs selective perception on why firms would choose to invest in political activity. We develop a set of novel hypotheses which explore this relationship.

Theory and Hypotheses

CEO Characteristics and Firm Investment in Political Activity

Hambrick and Mason (1984) argued that top executives act on the basis of their strategic interpretations of the external environment and that these interpretations are driven by the executive’s experiences, values, and personality traits. Gaining an understanding of the relationship between demographic characteristics of executives and the strategic decisions they make has resulted in a better understanding of organizational actions and performance outcomes (Hambrick, 2007). Extant UET research has considered a variety of demographic characteristics that influence strategic actions within the firm such as age (e.g., Child, 1974; MacCrimmon & Wehrung, 1986), tenure (e.g., Grimm & Smith, 1991; Henderson, Miller, & Hambrick, 2006), functional background (e.g., Bantel & Jackson, 1989; Cannella, Park, & Lee, 2008; Carpenter & Fredrickson, 2001; Michel & Hambrick, 1992; Wiersema & Bantel, 1992), and educational background (e.g., Cannella et al., 2008; Carpenter & Fredrickson, 2001; Wiersema & Bantel, 1992). This work has empirically justified the importance of the relationship between demographic characteristics of top executives and the strategic decision making that follows.

Despite the substantial work that has taken place to understand the relationship between CEO characteristics and the strategic decisions made by the firm, little work has sought to understand how these variables influence a firm’s propensity to engage in CPA. In the next section, we seek to answer our first research question regarding the extent to which CEO characteristics affect whether the firm engages in political activity. To answer this question, we combine ideas from UET with research on CPA to develop a set of novel hypotheses linking the two research streams together. Our primary argument is that certain CEOs will possess characteristics that predispose them to be more aware of the firm’s nonmarket environment and as a result will be more likely to engage that environment via political activity.

CEO age and tenure

CEO age and tenure are foundational demographic characteristics in UET scholarship. Although scholars have considered a number of psychological traits that are associated with older and longer tenured CEOs, most important to our initial research question regarding CEO characteristics that affect whether a firm invests in political activity is the fact that older and longer tenured CEOs are more likely to have a greater breadth and depth of experiences than their younger and less tenured colleagues (Hambrick & Fukutomi, 1991). As a result, these older and longer tenured CEOs are more likely to be aware of the firm’s nonmarket environment as well as the use of CPA to engage it. In addition, older and longer tenured CEOs are likely to have developed their own perspectives on the value of engaging in political activity. Scholars have established that CPA is particularly well suited for maintaining the status quo in the firm’s competitive environment (e.g., Baysinger, 1984; Oliver & Holzinger, 2008; Rudy & Johnson, 2016). UET research (e.g., Hambrick, Geletkanycz, & Fredrickson, 1993) argues that CEOs are likely to show a stronger commitment to the status quo than others in the organization, as strategic change can be risky (Henderson & Fredrickson, 1996) with highly unpredictable performance outcomes (Eisenhardt, 1989). This research suggests that older and longer tenured CEOs are more likely than their younger and shorter tenured counterparts to possess a strong commitment to maintaining the status quo, both in regard to the firm’s current strategy and its competitive environment (Hambrick et al., 1993; McClelland, Liang, & Barker, 2010). Thus,

CEO functional background

The varied job demands placed upon a CEO suggests that a broader view of the world is a prerequisite for job effectiveness (Hambrick, Finkelstein, & Mooney, 2005). Yet each CEO brings a perspective driven largely from experiences in the primary functional area through which they ascend. Although this functional track may not drive all of the strategic choices made by the CEO, it is expected to influence their decision making (Hambrick & Mason, 1984). For example, Dearborn and Simon (1958) found that when CEOs were asked to complete a task, they relied heavily on problem-solving skills developed in their functional area of expertise in framing the task and the actions that should be undertaken.

Functional tracks have been classified in a number of different ways. Hambrick and Mason (1984) argued that “throughput functions” such as operations, production, and distribution would result in the CEO being focused on increasing the firm’s efficiency. “Output functions” such as marketing, sales, engineering, and R&D would drive the CEO to be focused on the growth aspects of the firm. Finally, “peripheral functions” such as accounting and finance, law, human relations, and general management positions would be associated less with the core activities of the firm, but rather the administrative functions required for the firm to operate within the larger institutional environment.

These functional background distinctions of the CEO are useful to understanding whether a firm might engage in political activity. CEOs from a peripheral functional background (i.e., accounting, finance, law) are believed to have a different perspective on the determinants of the firm’s success when compared with CEOs from output and throughput functional backgrounds (Hambrick & Mason, 1984). Peripheral function CEOs are accustomed to dealing with the firm’s external environment and the laws and rules which define it. As such, they are more likely to recognize that the external environment is not so much a set of “fixed” rules, but rather an environment comprised of rules of competition which can be influenced by the firm. Thus,

CEO educational background

The choice of curriculum of study is indicative of a CEO’s cognitive strengths and the curriculum pursued can shape their perspectives and outlooks (Holland, 1973). For example, Hitt and Tyler (1991) found that a firm’s strategic decision making was influenced by the college degrees of its executives. Furthermore, Wiersema and Bantel (1992) argued that certain academic fields are more likely to be oriented toward change, suggesting that CEOs with specialized degrees in engineering and science would be more likely to be associated with strategic change actions in the form of invention and innovation. In contrast, CEOs with degrees in business, economics, and law may be less likely to only focus on these market-oriented strategic change actions, relying also on maximizing the firm’s underlying value by influencing the rules that define the firm’s competitive environment.

Similar to the relationship between CEOs with peripheral functional backgrounds and engagement in political activity, we also expect CEOs that have more generalized degrees in business, economics, and law to lead their firms to engage in greater amounts of political activity. This is because CEOs who followed generalized degree curriculums are likely to possess a perspective which takes into account a greater variety of possible strategies, especially when compared with CEOs with specialized educational backgrounds who may think in terms of the specific strategic actions that their educations provided them. For example, scholars have demonstrated the importance of a decision maker’s scientific and technical knowledge to understanding the changing industry conditions in the pharmaceutical, biotechnology, and medical device industries (e.g., Castanias & Helfat, 2001; Cooper, Gimeno-Gascon, & Woo, 1994; Gimeno, Folta, Cooper, & Woo, 1997; Pukthuanthong, 2006). Thus, a CEO with an educational background in business, economics, or law with their more detailed knowledge of the nonmarket environment, would be expected to invest in political activity to protect the firm’s competitive position in the marketplace. Thus,

CEO Characteristics and Firm Investment in Relational Political Activity

In this section, we begin to explore our second research question and seek a deeper understanding of the relationship between CEO characteristics and the firm’s investment in political activity. More specifically, we seek to gain an understanding of the relationship between CEO characteristics and whether the firm invests in relational or transactional forms of political activity.

As previously discussed, relational political activity can be characterized by a number of distinct features. First, relational CPA is thought to be associated with a long-term and continuous approach to political activity by the firm (Hillman & Hitt, 1999). Establishing and maintaining a government affairs department in Washington, D.C., takes a substantial amount of time. Thus, firms that establish such offices are thought to possess a long-term focus on the role that political activity plays in the firm’s broader strategy. Second, relational political activity is costly. In addition to establishing a Washington, D.C. office, employing a full-time staff represents a substantial investment, especially when compared with the alternative of hiring outside lobbyists. In addition to the long-term and costly nature of engaging in relational political activity, firms making this investment are thought to position themselves for better returns on their investment as the firm’s relations with critical policy makers will be strengthened (Hillman & Hitt, 1999). Thus, while investing in relational political activity may be higher risk for the firm, it also represents the potential for higher long-term returns because the firm is developing distinct political capabilities.

CEO age

In contrast to our general arguments above that suggest older CEOs are more aware of the firm’s nonmarket environment and thus more likely to engage it, we believe that firms led by younger CEOs will invest in relational political activity. To engage in relational political activity, a firm must establish and staff its Washington, D.C. office (Hillman & Hitt, 1999). Although costly and time-consuming, this represents an investment in the development of political capabilities with the goal of gaining a competitive advantage in the nonmarket environment. Child (1974) told us that younger CEOs are more open to all strategic options available to the firm, such CEOs would be likely to be open to making the investments to build the long-term political capabilities to compete in the firm’s nonmarket environment. Younger CEOs have also been characterized as more likely to take strategic risks than older CEOs (Hambrick & Mason, 1984). As discussed, a firm’s investment in relational political activity is a higher risk investment than investing in transactional political activity. Thus,

CEO tenure

Simsek (2007) suggested that longer CEO “tenures are conducive to the accumulation of knowledge, learning, and power” (p. 654). As such, we believe that firms led by longer tenured CEOs will not just engage in political activity but focus on the development of political capabilities associated with relational political activity. Developing such capabilities is expensive and time-consuming and longer tenured CEOs are more likely to have both the power and reputation within the firm to undertake such an investment. Furthermore, with greater experience within the firm, the CEO is more likely to recognize the long-term benefits to the firm of engaging in relational political activity. Although investing in relational political activity does not preclude the firm from also investing in transactional political activity, longer tenured CEOs are better positioned to understand the strategic advantages of each as well as have the perspective to develop the firm’s internal political capabilities. Thus,

CEO functional background

As previously discussed, CEOs from peripheral functional backgrounds tend to be more weakly linked to the firm’s core strategic capabilities (Hambrick & Mason, 1984) and are therefore more likely to consider a wider set of strategic options (Hambrick & Finkelstein, 1987). However, beyond simply engaging in political activity, we expect CEOs with peripheral functional backgrounds to invest in relational CPA. Because such CEOs are already aware of the firm’s nonmarket environment, they are also more likely to understand the competitive benefits of developing the internal political capabilities to effectively engage in relational CPA. Government affairs employees’ act as policy watchdogs possessing political capabilities aligned with the firm’s strategic goals. CEO’s from peripheral functional backgrounds, possessing a strategic perspective which takes into account the malleability of rules which define the firm’s competitive environment, will be more likely to build political capabilities in-house and actively engage the nonmarket environment in search of competitive advantage. Thus,

CEO educational background

As described above, CEOs that pursued a more generalized program of study are thought to be more likely to possess a perspective which views the firm’s nonmarket environment as an area within the scope of strategic action. The cognitive preference for CEOs with generalized educational backgrounds to invest in relational political activity stems from Hambrick and Mason’s (1984) argument that these executives tend to be “organizers and rationalizers” (p. 201) who emphasize more complex organizational systems of the firm. Manner (2010) argued that such CEOs are less cooperative in nature than their counterparts and more focused on their firm’s own narrow self-interest. Thus, CEOs with educational backgrounds in business, economics, and law would also be more likely to invest in internal political capabilities to engage in relational political activity because building a government affairs operation represents an opportunity to implement the complex administrative systems toward which such CEOs gravitate. The investment in the development of such internal political capabilities is also consistent with the CEOs preference to focus on maximizing the firm’s self-interest. Thus,

CEO Characteristics and Firm Investment in Transactional Political Activity

In contrast to relational political activity’s focus on long-term and continuous engagement in political activity, transactional political activity can be characterized as having a more short-term focus (Hillman & Hitt, 1999). Firms invest in transactional political activity only when issues arise that force such engagement. As a result, transactional political activity can be described as more reactive than relational political activity because it is relatively quick and easy to contract with an external lobbying organization that is politically well-connected to represent the firm. Also, transactional political activity is less costly than relational political activity. Engaging in transactional political activity does not require the large resource commitments necessary to establish a Washington, D.C. office and employ a full-time staff. Perhaps not surprisingly, firms that engage in transactional political activity are less likely to enjoy performance gains when compared with firms that invest in relational political activity (Hillman & Hitt, 1999). Thus, investing in transactional political activity can be characterized as shorter term, lower risk, and less costly for the firm.

CEO age

UET posits that older executives tend to be more conservative in their decision-making than their younger colleagues (Hambrick & Mason, 1984). Child (1974) found that older executives were more likely to follow lower growth strategies than their younger peers, and MacCrimmon and Wehrung (1986) found that these older managers tend to be more risk averse. Investing in transactional political activity is less risky than investing in relational political activity. Furthermore, investing in transactional political activity is well suited for dealing with short-term issues within the firm’s nonmarket environment (Hillman & Hitt, 1999). Thus, firms led by older CEOs would be expected to invest in transactional political activity to protect the firm’s existing competitive environment rather than engage in riskier, longer-term relational political activity.

In addition to these psychological explanations, scholars utilizing agency theory have argued that CEOs may be more likely to engage in transactional political activity because they are incentivized to maximize the firm’s current profitability which, in turn, will maximize their short-term compensation (Gerhart, Rynes, & Fulmer, 2009). Older CEOs who may be nearing retirement would therefore be expected to engage in greater amounts of transactional political activity to protect the firm’s short-term profits and hence their personal compensation packages. Thus,

CEO tenure

In contrast to the arguments laid out above regarding the relationship between CEO tenure and a firm’s investment in relational political activity, we believe firms led by shorter tenured CEOs will be more likely to invest in transactional political activity. CEOs with shorter tenure in their position as CEO would be expected to focus on the challenges facing the firm in the market environment. As such, shorter tenured CEOs are more likely to align their firms with powerful external lobbying firms to overcome challenges in the nonmarket environment that may arise. Because external lobbying firms tend to be comprised of former legislators (Smith, 1988), these firms provide an attractive means for shorter tenured CEOs to quickly and effectively engage in political activity. CEOs with shorter tenure will therefore be more likely to seek out powerful external lobbyists in an effort to gain information and reduce uncertainty in the firm’s nonmarket environment to overcome their liability of newness within the firm. Thus,

Method

Data

The sample utilized for this study was large, publicly held firms based in the United States. This sample was derived from the largest 100 firms (by revenue), as ranked by Fortune in 1980. Data on these firms were collected through 2006; after accounting for firm deaths and missing data, the sample consisted of 1,955 firm-year observations.

There are a couple of reasons why we chose to create a sample based on large firms. First, extant research has consistently found that larger firms are more likely to engage in political activity than smaller firms (e.g., Masters & Keim, 1985; Meznar & Nigh, 1995; Schuler, 1996). Second, Fligstein (1990) argued that large firms are a group classification unto themselves because larger firms are often considered industry leaders (Fligstein, 1990) whose actions are more visible which attracts greater media coverage and as a result are more likely to be observed by stakeholders (Rao, Davis, & Ward, 2000). Thus, in considering a sample comprised of larger firms, this research seeks to explore more nuanced drivers of CPA.

Dependent Variables

All dependent variables were collected and coded by one of the authors. Investment in political activity was assessed using data collected from the publication Washington Representatives by Columbia Books. Washington Representatives is a directory of corporations and lobbying firms engaged in political activity in Washington, D.C., published annually. For each year, Washington Representatives collects information on the names of employees working in corporate government affairs offices in Washington, D.C., as well as the names of external lobbying organizations retained by firms to lobby on their behalf in Washington, D.C. The publisher, Columbia Books, collects these data using “a variety of sources including federal lobbying registrations filed with the Clerk of the House and Secretary of the Senate; FARA (Foreign Agents Registration Act) registrations at the Department of Justice; press releases; and the responses to annual questionnaires” (Columbia Books, Inc., 2006, p. i).

Investment in political activity

The dependent variable for Hypotheses 1a through 1d is a dummy variable coded 1 if the firm was listed in Washington Representatives in a given year and 0 otherwise. More specifically, if a firm in the sample employed a government affairs employee in their Washington, D.C. office, contracted with a lobbyist from an external firm or did both, we coded investment in political activity for that firm-year observation as 1. Data on investment in political activity were collected for each year using the Client section of Washington Representatives.

Investment in relational political activity

Utilizing Hillman and Hitt’s (1999) distinction between relational and transactional CPA, we followed Hadani (2007) and Ozer and Alakent (2013) and determined a firm’s relational approach to CPA depending on whether it utilized a government affairs office in Washington, D.C. Thus, the dependent variable for Hypotheses 2a through 2d is a dummy variable coded 1 if the firm was listed as employing a government affairs employee in their Washington, D.C. office in a given year and coded 0 otherwise. Data on investment in relational political activity were collected for each year using the Client section of Washington Representatives.

Investment in transactional political activity

Hillman and Hitt (1999) described transactional CPA as a short-term, contracting approach to political activity. Thus, we follow Hadani (2007) in assessing our dependent variable for Hypotheses 3a and 3b as a dummy variable coded 1 if the firm was listed as contracting with an external lobbying firm in a given year and coded 0 otherwise. Data on investment in transactional political activity were collected for each year using the Client section of Washington Representatives.

For all dependent variable data collected from Washington Representatives, a series of random spot checks were employed by one of the authors to assess accuracy in the data collection procedure. The initial spot check resulted in 96% agreement between the two authors. It was determined that the discrepancy in agreement was the result of sample firm name changes over the window of observation. To correct this discrepancy, all firm-year observations were reassessed using multiple search strings (e.g., shortened name, removal of “inc.” or “corp.” from name); 100% agreement between the authors was achieved.

Independent Variables

The independent variables for this study were composed of a number of CEO demographic variables. We obtained these data from a variety of resources including the Reference Book of Corporate Management; Standard & Poor’s (S&P’s) Register of Corporations, Directors, and Executives; Who’s Who in Finance and Industry; and corporate annual reports and proxy statements filed with the Securities and Exchange Commission.

CEO age was measured in years. CEO tenure was measured as the number of years since being appointed CEO. To assess the CEO’s functional background, we followed a number of scholars who have studied functional diversity within the firm’s top management team (TMT; that is, Bantel & Jackson, 1989; Cannella et al., 2008; Carpenter & Fredrickson, 2001; Michel & Hambrick, 1992; Wiersema & Bantel, 1992). The dominant functional career track was defined as the functional area through which a CEO rose to power within the organization. In this study, functional background took on the values 1 to 11, representing the following functional tracks: (1) production or operations, (2) distribution, (3) research & development, (4) engineering, (5) marketing, (6) sales, (7) accounting & finance, (8) law, (9) personnel & labor relations, (10) management & administration, and (11) general or other. Following Hambrick and Mason (1984), the higher the value for the functional background variable, the more likely the CEO was to have had a peripheral functional background.

To assess the CEO’s educational background, we followed Cannella et al. (2008), Carpenter and Fredrickson (2001), and Wiersema and Bantel (1992). We classified each CEO into one of five categories based on the highest degree awarded: (a) sciences, (b) engineering, (c) arts, (d) business and economics, and (e) law. Following these scholars, the higher the value for the educational background variable, the more likely the CEO was to have had a more generalized educational experience.

Control Variables

All models contain a number of control variables. Firm age has been argued to positively effect a firm’s likelihood of engaging in CPA as it is thought to act as a proxy for “reputation” (Baron, 1995; Boddewyn & Brewer, 1994) and political “experience” (Hillman & Hitt, 1999). Firm age was measured as the number of years since the firm’s founding year. Firm size may act as a proxy for a firm’s ability to become engaged in political activity because larger firms are thought to represent more stakeholders and hence more voters (Hillman et al., 2004). Firm size was measured using the firm’s assets provided by Compustat. This variable was highly skewed, however, so we took the natural log of firm size to attain an approximately normal distribution. Firm slack has also been argued to influence a firm’s CPA, as it provides the necessary resources to engage in such behavior (Meznar & Nigh, 1995). We followed Bourgeois and Singh (1983) and Bromiley (1991) to measure firm slack as an index of multiple accounting measures (all obtained from Computstat). We used the current ratio (current assets divided by current liabilities) to assess available slack, working capital-to-sales ratio to measure recoverable slack, and equity-to-debt ratio to measure potential slack. We then standardized these three proxies of slack and summed them to create a firm slack index.

A firm’s market share may also influence its investment in politics. Yoffie (1987) argued that firms with the largest market share in their industry are more likely to take leadership roles in political activity as they are more likely to be impacted by policy decisions. Market share was calculated by dividing each firm’s annual sales by the total sales for the firm’s industry using the primary three-digit Standard Industrial Classification (SIC) code. Data for market share came from Compustat. Year dummies were also included to control for unobserved systematic period effects, such as the effects of an election year, on each firm’s political activity. Finally, a firm’s industry is likely to influence whether it engages in political activity (Schuler, 1996; 1999). Therefore, industry dummies were also included in our analysis using the three-digit primary SIC code listed for each company in Compustat.

Analysis

The dependent variables in this study are dichotomous variables; thus, we use probit analysis to estimate our models. Furthermore, to account for unobserved heterogeneity, we used a random-effects approach. As a robustness check, we also tested our hypotheses using a random-effects logit analysis. All of the results from the logit models were similar to those of the probit models, and the results based on the random-effects probit analysis are reported.

Results

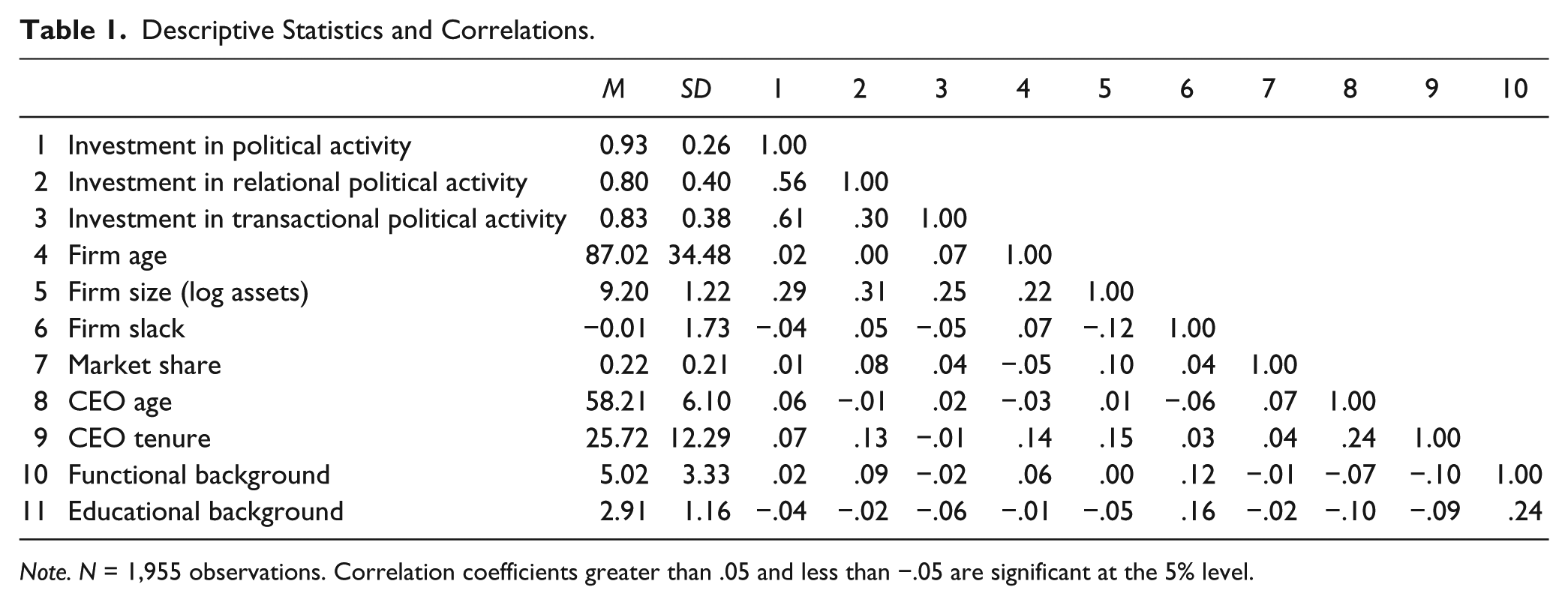

Table 1 provides descriptive statistics and correlations for the variables used in this study. The significant correlations between firm size and firm political activity are consistent with extant scholarship and support its use as a control variable. To ensure that collinearity did not affect the results, we assessed the variance inflation factor (VIF) and condition indices for all models using the collin function in Stata. The highest value across all models was 1.21, and the highest average VIF was 1.11, both well below the recommended cutoff value of 10, thus multicollinearity does not appear to be a concern in the results (Chatterjee, Hadi, & Price, 2000; Neter, Kutner, Wasserman, & Nachtsheim, 1996).

Descriptive Statistics and Correlations.

Note. N = 1,955 observations. Correlation coefficients greater than .05 and less than −.05 are significant at the 5% level.

CEO Characteristics and Firm Investment in Political Activity

Table 2 reports the results of the test of Hypotheses 1a through 1d. Model 1 reports the results for the control variables. Firm size was positively related to investment in political activity undertaken by the firm while market share was negatively related. Models 2 through 6 include the CEO demographic characteristics hypothesized to impact the firm’s investment in political activity. Regarding CEO age, Hypothesis 1a predicted that a firm would be more likely to invest in political activity if it were led by an older CEO. As reported in Model 2, the positive and significant effect of CEO age (b = 0.027, p < .05) provides initial support for this hypothesis. Hypothesis 1b predicted that firms with longer tenured CEOs would be more likely to invest in political activity. Model 3 shows a nonsignificant result for CEO tenure (b = 0.016, p = n.s.). In Hypothesis 1c, we predicted that a firm would be more likely to invest in political activity if it was led by a CEO whose functional background was in the peripheral areas of the firm. As reported in Model 4, the positive and significant effect of functional background (b = 0.054, p < .05) provides initial support this prediction. Hypothesis 1d predicted that a firm would be more likely to invest in political activity if it was led by a CEO whose educational background was in generalized fields of study. As reported in Model 5, the positive and significant effect of educational background (b = 0.203, p < .10) provides initial support this prediction. Reviewing the full model (Model 6), only CEO age maintained significance (b = 0.088, p < .01), thus we find full support for Hypothesis 1a, partial support for Hypotheses 1c and 1d and no support for Hypothesis 1b.

Random-Effects Probit Analysis of the Likelihood of Investment in Political Activity.

Note. Numbers in parentheses are standard errors; Year and industry dummies not shown to conserve space.

p < .10. *p < .05. **p < .01. ***p < .001.

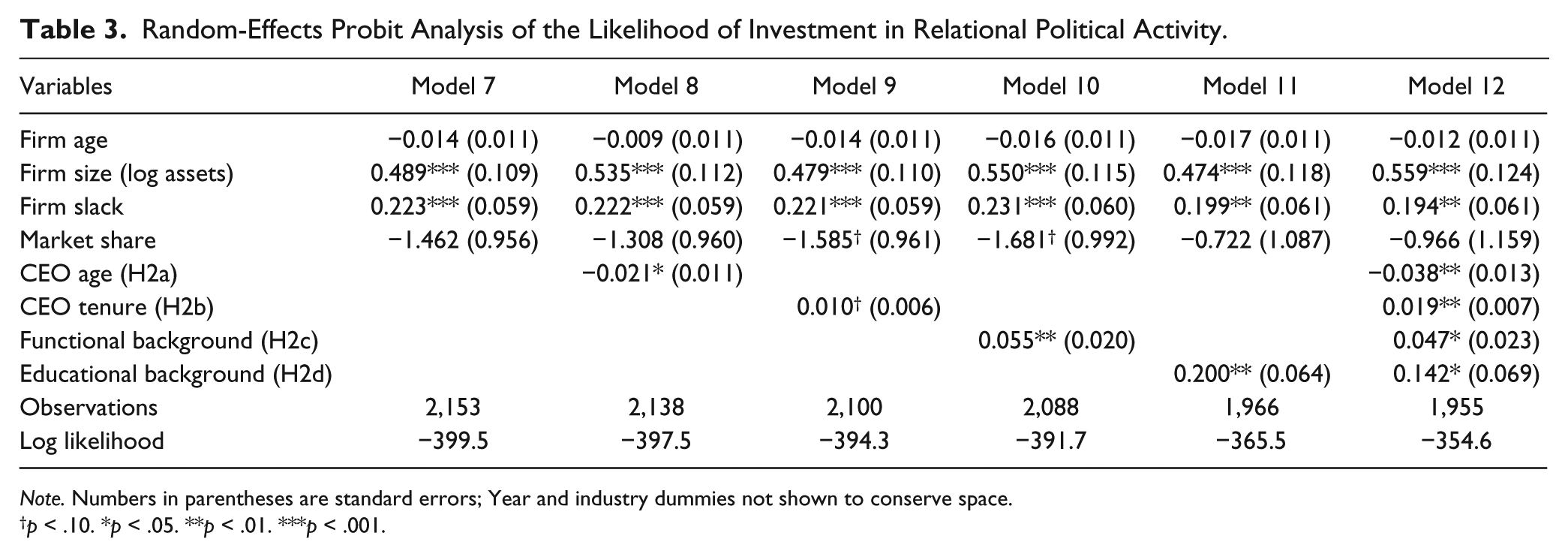

CEO Characteristics and Firm Investment in Relational Political Activity

Table 3 reports the results of the test of Hypotheses 2a through 2d. Model 7 reports the results for the control variables. Firm size and slack were both positively related to the firm’s investment in relational political activity. Models 8 through 12 include the CEO demographic variables from our hypotheses. Regarding CEO age, in Hypothesis 2a, we predicted that a firm led by a younger CEO would be more likely to invest in relational political activity. As reported in Model 8, CEO age was found to be negative and significant (b = −0.021, p < .05) providing initial support for this prediction. Hypothesis 2b argued that firms would be more likely to invest in relational political activity if they were led by longer tenured CEOs. In Model 9, the variable CEO tenure was found to be positive and significant (b = 0.010, p < .10) providing initial support for Hypothesis 2b. Hypothesis 2c predicted that a firm would be more likely to invest in relational political activity if it was led by a CEO whose functional background was in the peripheral areas of the firm. As reported in Model 10, the positive and significant effect of functional background (b = 0.055, p < .01) provides initial support this prediction. Hypothesis 2d predicted that a firm would be more likely to invest in relational political activity if it was led by a CEO whose educational background was in generalized fields of study. As reported in Model 11 the positive and significant effect of educational background (b = 0.200, p < .01) provides initial support this prediction. Reviewing the full model (Model 12), CEO age (b = −0.038, p < .01), CEO tenure (b = 0.019, p < .01), functional background (b = 0.047, p < .05) and educational background (b = 0.142, p < .05) all maintained significance, thus Hypotheses 2a through 2d are fully supported.

Random-Effects Probit Analysis of the Likelihood of Investment in Relational Political Activity.

Note. Numbers in parentheses are standard errors; Year and industry dummies not shown to conserve space.

p < .10. *p < .05. **p < .01. ***p < .001.

CEO Characteristics and Firm Investment in Transactional Political Activity

Table 4 reports the results of the test of Hypotheses 3a and 3b. Model 13 reports the results for the control variables. Only firm slack was negatively related to the firm’s investment in transactional political activity. Models 14 through 18 include the CEO demographic characteristics. Regarding Hypothesis 3a, we predicted that a firm would be more likely to invest in transactional political activity if it was led by an older CEO. As reported in Model 14, the positive and significant effect of CEO age (b = 0.009, p < .05) provides initial support for this prediction. Hypothesis 3b predicted that a firm would be more likely to invest in transactional political activity if it was led by a CEO with less tenure in the firm. As reported in Model 15, the negative and significant effect of CEO tenure (b = −0.008, p < .05) provides initial support for this prediction. We include in Models 16 and 17, analyses of the relationship between a firm’s investment in transactional political activity and the CEOs functional background and educational background, respectively. We do not formally hypothesize about these relationships, but rather include them in the model to demonstrate that they are not significantly related to the firm’s investment in transactional political activity. Reviewing the full model (Model 18), CEO age remains significant (b = 0.015, p < .05), thus Hypothesis 3a is fully supported. CEO tenure also continues to be significant as well (b = −0.015, p < .01), thus Hypothesis 3b is fully supported. We provide an overview of all of our Hypotheses and our findings in Table 5.

Random-Effects Probit Analysis of the Likelihood of Investment in Transactional Political Activity.

Note. Numbers in parentheses are standard errors; Year and industry dummies not shown to conserve space.

p < .10. *p < .05. **p < .01. ***p < .001.

Summary Findings.

Discussion

This article considers the relationship between the characteristics of the firm’s CEO and the likelihood of the firm investing in political activity. Combining ideas from UET and CPA, we proposed that individual characteristics associated with the CEO’s age, tenure, functional background, and educational background were likely to result in the firm’s investment in political activity. We then went beyond this traditional UET-based argument and predicted that these characteristics would motivate the firm’s CEO to make specific types of investments in either relational or transactional CPA.

Analyzing data from large publicly traded firms in the United States between 1980 and 2006, we found that firms led by older CEOs were more likely to invest in political activity (H1a). We also found partial support for our predictions that CEOs from peripheral functional backgrounds (H1c) and generalized educational backgrounds (H1d) would invest in political activity. However, when we considered whether CEO characteristics were related to the firm’s investment in relational and transactional political activity, our results became much more interesting and robust. We found that younger CEOs, CEOs with longer tenures within the organization, CEOs with peripheral functional backgrounds, and CEOs with generalized, educational backgrounds in business, economics, and law were more likely to lead organizations to invest in relational political activity (Hypotheses 2a through 2d). In contrast to these findings, we found that firms led by older CEOs and CEOs with shorter tenure were more likely to direct their firms to invest in transactional political activity (Hypotheses 3a and 3b).

In general, the findings from this study suggest that different relationships exist between the characteristics of the firm’s CEO and the firm’s choice to invest in political activity. What is particularly interesting in our findings is the fact that while we only find strong support for CEO age as a driver of whether a firm invests in political activity (Hypothesis 1a), we find strong support for all of our hypotheses that relate CEO characteristics to the approach the firm takes to invest in CPA (Hypotheses 2a-2d and 3a-3b). This suggests that CEO characteristics have less of an impact on “whether” a firm engages in CPA, but once a firm decides to engage in CPA, CEO characteristics have an important impact on “how” the firm chooses to invest in CPA.

This research seeks to contribute to our theoretical understanding of the determinants of CPA. The majority of the research that has considered the antecedents to CPA has focused on either industry-level characteristics such as regulations (Grier, Munger, & Roberts, 1994) or firm-level characteristics such as size (Schuler, Rehbein, & Cramer, 2002) and slack resources (Meznar & Nigh, 1995). This article goes beyond these studies by suggesting and finding support for the idea that firms engage in political action as a result of the unique perspectives held by the firm’s CEO. As a result, this research provides important insights into a driver of nonmarket activity that has, up to now, only been considered in traditional, market-related strategic management research.

Furthermore, this research demonstrates an important distinction within UET. That is, we show that specific characteristics of a firm’s CEO leads to a distinct approach to how it engages the nonmarket environment (i.e., via investment in relational or transactional political activity). Most notably, we find that certain characteristics are more likely to motivate the CEO to make investments in the political capabilities which comprise relational CPA. We believe that this finding, as well as demonstrating the relational–transactional CPA distinction, represent important contributions to UET. Not only does it show that the nonmarket environment is an important outlet for the firm’s strategic actions, but also that specific CEO characteristics impact the firm’s investment in developing capabilities that scholars have suggested are crucial for the long-term competitive advantage of the firm (e.g., Eisenhardt & Martin, 2000; Teece, Pisano, & Shuen, 1997).

Finally, CPA research using an agency theory perspective has theorized that the firm’s management is likely to engage in CPA to maximize managerial benefits such as compensation or employability (Aggarwal et al., 2012; Arlen & Weiss, 1995). In this study, we are able to show a direct relationship between a firm’s leader and its investment in CPA. Thus, while corporate governance scholars utilize agency theory to suggest CEOs engage in CPA in uniform ways to gain benefit for themselves, this research provides a more complete picture of the motivations driving the firm’s leaders to engage in CPA.

Limitations and Future Research

Like all research, this article carries with it some limitations. First, to assess investment in political activity, as well as relational and transactional political activity, this research considers whether the firm had employees in their Washington, D.C. office or whether the firm contracted with external lobbying organizations. However, this article does not specifically measure the amount of political investment undertaken. Thus, the measures in this research represent the presence of political activity but not a specific investment in political activity by the firm. Furthermore, firms may engage in many different forms of CPA (e.g., PAC contributions, advocacy advertising, grassroots coalition building). Future research needs to look more broadly across these different forms of CPA to assess whether the relationships proposed herein hold.

Scholarship from CPA has also identified a number of drivers of a firm’s investment in political activity for which we were unable to control. Issue salience is one such driver of CPA with scholars predicting that there will be increased firm political activity surrounding important political issues for firms (e.g., Bonardi & Keim, 2005; Hillman & Hitt, 1999). Another driver of firm CPA is related to institutional characteristics like congressional structure. For example, Schuler and colleagues (2002) found that firms within industries represented by congressional caucuses were more politically active. Such external factors can impact a firm’s investment in CPA, and future research should consider how these factors might interact with the CEO characteristics studied here.

Scholarship from UET has also identified a number of CEO demographics that were not included in this study. CEO gender and CEO power are two of the more common CEO characteristics in extant literature. We chose not to study CEO gender because of the lack of variance in this measure during the sample window. Regarding CEO power, one of our core assumptions in this article was that the CEO had the power to engage the firm in CPA. Future studies will need to assess the validity of this assumption. Also, this research only considers CPA in the United States by large, publicly traded firms. These firms are likely to engage in political activities in most if not all countries in which they operate. Yet, this article does not capture whether the CEO characteristics identified to influence investment in political activity also drives similar investments in other countries. Therefore, future research should consider questions surrounding CEO characteristics and nonmarket activity in international contexts.

Going forward, research integrating UET with CPA has the potential to yield exciting opportunities and important insights. In addition to addressing the limitations discussed above, future studies might also consider expanding CEO characteristics to broader TMT characteristics. UET research that considers the TMT has generated important findings such as the impact of heterogeneity of the firm’s TMT on firm-level outcomes like performance (e.g., Carpenter, 2002). Such relationships are likely to be present in regard to the firm’s choice to engage in CPA as well. Similarly, the impact of the firm’s Board of Directors (BOD) on the CEO and the firm’s investment in CPA should also be considered. Extant research has found relationships between politicians on the BOD and the firm’s engagement in CPA (e.g., Hillman, 2005), but future research should consider how the BOD influences the firm’s CEO to engage in CPA. This line of research would also augment our existing understanding of the corporate governance research described in this article that uses agency theory to predict firm CPA. Finally, future research also needs to consider the performance outcomes of the firm’s investment in CPA. Although this study found that CEO characteristics are related to different types of investments in political activity, what these firms gain by undertaking these distinct relational and transactional investments in political activity remains an open question.

Conclusion

Nonmarket strategic action undertaken by firms led by CEOs with unique perspectives is an unexplored area of research in strategic management. Utilizing ideas from UET, we sought to gain insight into the CEO characteristics that motivate the firm’s investment in, and the approach to, political activity. In so doing, this article establishes the importance of such characteristics in motivating different types of firm nonmarket strategic actions.

Footnotes

Acknowledgements

The authors thank Stewart Miller and Michael McDonald for their helpful comments and suggestions on earlier versions of this article. The authors also thank participants at the annual Academy of Management conference for their comments. Finally, the authors greatly appreciate the constructive guidance of Kathleen Rehbein and the three anonymous referees at Business & Society. Any remaining errors are our own.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.