Abstract

Theoretical evidence suggests that corporate social irresponsibility (CSI) should produce long-lasting negative influences on firm performance. Yet, little empirical evidence exists in the literature to support this time-embedded research frame. This research was conducted by collecting a large set of firm data and by employing a series of vector autoregressive models to map out the longitudinal dynamic relationships between CSI and firm value under high versus low levels of two external factors, environmental dynamism and competition intensity, and one internal factor, firm capability. The results show that CSI’s negative influences endure in scenarios such as high dynamism, high competition intensity, and low capability, but it has only a short-term impact on low-dynamism markets and does not produce significant effects on firm value under low-competition or high-capability conditions. These findings yield useful implications for CSI, resource-based theory, and environment theories as well as for managerial effectiveness of coping with social negativities.

Keywords

Corporate social responsibility (CSR) represents the firm actions aiming for social welfare that goes beyond the core business targets of the firm (Djelic & Etchanchu, 2017; McWilliams & Siegel, 2001), and it has captured considerable attention in the past decades from both academic researchers and business practitioners regarding its roles in influencing a large array of firm performance outcomes (Barnett, 2007; Orlitzky, 2011; Székely & Knirsch, 2005). It has been widely acknowledged that CSR has the power to positively drive firm strengths of appealing to its customers, employees, investors, and other stakeholders and therefore provides an “insurance-like” protection for the firm’s competitive positions (Brammer & Pavelin, 2004; Glavas & Kelley, 2014; Peloza, 2006; Sen et al., 2006; Soundararajan et al., 2018). Although CSR has received significant attention, the understanding of the CSR’s counterpart, corporate social irresponsibility (CSI), is markedly deficient. CSI, in its earlier form, was defined as the firm decisions which are seeking gains at the expense of other parties or the total system (Armstrong, 1977), and later its conceptualization further incorporates firm behaviors incurring harmful effects on related or unrelated entities (Kang et al., 2016; Mena et al., 2016; Soundararajan et al., 2018). Recent theorists have called for more research focus directed to CSI because in many aspects it is even more important than CSR in terms of the impact on firms (Lange & Washburn, 2012; Lin-Hi & Müller, 2013). For instance, CSI naturally captures more media attention because of the negativity and yields a higher magnitude of impact than positive CSR activities (T. Wagner et al., 2008). In addition, CSI produces more complicated implications on firm performance because, on one hand, it may bring detrimental effects on business performance, but, on the other hand, it may ease firm financials due to its cost-saving functions (e.g., avoiding budgets on community relations, or cutting cost on employee caring or environmental protection programs) and/or additional revenue benefits (e.g., sales from unethical practices; McClaren, 2000). A more crucial nature of CSI that differentiates it from CSR is that the former’s impacts on the firm may last longer than those of the latter (Allsop et al., 2007). This creates an interesting avenue for exploring CSI’s time-related implications on firm performance. Moreover, CSI involves firm crisis management and responding vehicle that are not applicable for CSR. These coping activities intertwine with the CSI spread and make it a challenge to trace the true role of CSI under traditional research frames.

The distinctive nature of CSI provides strong motivations for this article to pursue an in-depth knowledge set in this domain. A further literature review on the CSR and CSI topics reveals several notable theoretical gaps as well as empirical vacancies. Foremost, although numerous academic researchers strongly advocate the longitudinal influences of firm social activities (Jamali & Mirshak, 2007), the theoretical development and empirical work targeting this direction are rare. Hamann (2019) calls for that CSR studies should focus more on the dynamic interactions rather than “static” images. Specifically, to the best of our knowledge, there is no existing research that explicitly explores CSI’s longitudinal effects disregarding the importance of this area. Furthermore, the extant knowledge about CSI is largely limited to the fields such as consumer metric and market performance, and a link between CSI and firm value is surprisingly absent. Filling this gap is critical because firm value is the ultimate goal of business firms and is a fundamental performance gauge that signifies the firm’s multifaceted managerial effectiveness (Godfrey et al., 2009). In addition to the vacancies of these direct relationships, incorporating contextual factors may be equally important (Djelic & Etchanchu, 2017). Given the complexity of firm environments, it is necessary to consider those factors when examining CSI’s roles because a firm’s social activities occur in a wide array of external contingencies and involve a broad base of outside stakeholders (Morsing, 2006). However, there is little existing evidence showing the interactions between CSI and environmental factors. Internally, firms differ in their strengths of controlling and deploying resources, which logically affects the impact of CSI because a firm’s coping strategy effectiveness largely determines the scope and depth of the negative results of CSI. Thus, firm capability must be considered when CSI is a research focus. However, this meaningful association has not been either theoretically proposed or empirically examined.

This research is developed to bridge these notable gaps. We took the first attempt in this research stream to use a time-series analysis, tracking CSI’s influences on firm value. More importantly, we incorporated two variables, dynamism and competition intensity, to trace the long-term effect paths of CSI under different external conditions. In addition, we included firm capability, a central factor that represents the firm’s inherent strength, to explore CSI’s long-term effects under high and low firm abilities of deploying resources. We collected a large set of data covering firms from a comprehensive industry spectrum, and we applied a panel data vector autoregressive model with exogenous variables (VARX) to empirically estimate the models. With these new theoretical links, our research is expected to generate a set of meaningful contributions to both the theories and business practices. First, adopting a new approach in which CSI is viewed as a factor that may continuously exert its influence on firm performance enriches the understanding of the stakeholder view of CSR that has been mainly focused on cross-sectional relationships. The addition of the time factor maps out the long-lasting performance impact of CSI and more realistically reflects the roles of firm social activities in practice (Nevins et al., 2007). Second, our research should contribute significantly to the application of the notion of sustained competitive advantages in the CSR literature (Greening & Turban, 2000; McWilliams & Siegel, 2001) because it extends the scope of this research field by illustrating the importance of the socially responsible activities of the firm from a new perspective. Third, linking CSI to firm value in a time-series framework yields new knowledge sets for understanding the dynamic relations between firm social activities and shareholder value (Godfrey et al., 2009). The varying impacts on shareholder value can be traced in a longitudinal manner and thus reveals a clearer pattern of shareholder value drivers (or hindrances) that will allow researchers to get more in-depth information about protecting firm value. This time-based notion of CSI paves the way for more realistically understanding firm activities and their influences, which should be looked as continuous concepts and should have long-lasting rather than short-term implications. Fourth, our research is designed to enrich environmental studies in the business domain that have been largely directed to the short-term moderating effects. Our research takes a different angle and tracks these moderating functions in expanded time durations. In this regard, our research further extends the contingency theories and their applications in the CSR/CSI research scheme. Fifth, the incorporation of firm capability brings together the CSI literature and dynamic capability theories in a way that has not been employed before. CSI and firm capability have largely been treated as separate entities in the literature. CSI studies are primarily focused on its implications for firm social performance and resulted financial gains/losses (Kang et al., 2016; Lange & Washburn, 2012), whereas capability studies are more constrained to the firm functional and operational units that drive firm outcomes (Krasnikov & Jayachandran, 2008; Stoel & Muhanna, 2009). A combination of these two streams is surprisingly missing. Their joint effects, therefore, reveal important insights into how firms may use managerial competencies to cope with undesirable social impacts (Luo & Bhattacharya, 2006).

Theoretical Framework

CSI and Its Influences on Firm Value

CSI as a distinctive construct beyond being the counterpart of CSR

Scholars have raised attention toward CSI and suggest that it should not be merely looked at as in opposition to CSR. Rather, it has a number of distinctive characteristics that have unique implications for firm performance (Kang et al., 2016). The most prominent nature of CSI is that the magnitude of its negative impact exceeds the positive impact of CSR (Frooman, 1997; Muller & Kräussl, 2011). Consumers are more sensitive to negative news, and the willingness to punish is significantly higher in magnitude than the willingness to support that results from CSR activities (Williams & Zinkin, 2008). More importantly, the media tends to focus more on CSI news than on CSR news. People are naturally assumed to behave ethically, and thus CSI’s contradictory effect to this hidden assumption captures more attention from media agencies. Therefore, a firm’s CSIs tend to capture a broader exposure than CSRs and incur significant damages on the firm’s market performance, which in turn reduces firm value. Furthermore, similar to media propensity, the business ethics literature documents that consumers are inclined to spread more CSI than CSR through word of mouth (Baumeister et al., 2001; Sen & Bhattacharya, 2001). This channel is deemed to be more credible and more powerful than classic media channels (Keller, 2007), and thus it is situated to further reduce customer loyalty, resulting in worse shareholder value. Another key point is that although CSR projects are purposefully developed for serving firms’ social or business goals, CSI can be categorized into either intentional or unintentional activities (Lin-Hi & Müller, 2013). Intentional CSI is particularly detrimental to firm performance because it not only ruins the reputation through its negative consequences but also causes the stakeholders to question the fundamental ethical basis of the firm; it thus produces a double-fold negative impact on firm business outcomes (Frooman, 1997). On the other hand, CSI is not solely associated with the downside effects on a firm, but it may have positive functions for the firm from a purely financial perspective. For example, CSI is often the result of a firm that pursues certain self-interest goals such as more sales, cost saving, or using unethical ways to realize competitive advantages (M. F. Chen & Mau, 2009). In this sense, CSI may yield support for the financial outcomes even though theorists argue that these gains cannot be sustained in the long term (Lin-Hi & Müller, 2013). This exactly echoes the motivation of this article in developing the contingency-based longitudinal research setting that may better capture the dynamic nature of CSI.

CSI and firm valuation

CSR has been found to generate a firm’s “moral capital” that stands for a firm’s desirable resource type and positively drives firm value. Conversely, CSI not only signifies the absence of this resource but also creates negative messages to the market and undermines the firm’s reputational assets (Lin-Hi & Müller, 2013). This loss of assets has been found to be strongly decreasing a firm’s value (Lucas & Noordewier, 2016). Furthermore, although it is widely recognized that firm valuation is performed by shareholders, the valuation process will include a number of stakeholders (Bhattacharya et al., 2009). The instrumental stakeholder theory of social responsibility holds the notion that a firm’s social negativities will be likely to undermine its relationships with stakeholders and thus negatively affect the shareholder’s assessment (Kang et al., 2016), resulting in firm value decrease. More fundamentally, CSI is likely to create undesirable functional issues such as operational difficulties (Arora & Lodhia, 2017). For example, channel members may cease to cooperate with firms that have CSI and this will result in immediate operational disorders due to the disruption of the channel system. These disorders will affect revenue flows and also augment firm performance uncertainty, which have been found to be central to shareholders’ value assessment (Srivastava et al., 1998). Equally important, CSI’s impacts on firm value are reflected by the worsened microenvironment of the firm in its geomarkets. Local government and interest groups may set barriers for a CSI firm as well as execute sanctions for its CSI behaviors and consequences. These factors of supportiveness of the environment are essential in a firm’s valuation (Gaur et al., 2018). Thus, CSI will be negatively related to firm value.

CSI’s long-term effects

Although CSR’s power on business performance is well documented, either the theoretical pattern or empirical evidence about CSI’s longitudinal function has not yet been adequately determined. The long-term effects, in contrast to the short-term ones, mean that the results of firm actions go beyond the current or immediate business cycles and exert extended influences on the firm’s future operations as well as performance outcomes (Mascarenhas & Aaker, 1989). Although the immediate outcomes of firm actions are more observable and traceable, the long-term effects are often blurred due to the overflow of incoming influential factors over time (Kale et al., 2002). However, ample evidence can be found in the literature to support these long-term effects. Reputation theories propose that a firm’s reputation is an enduring factor that continuously protects the firm from competitive threats (Roberts & Dowling, 2002), and conversely an undesirable firm image makes the firm more vulnerable (Rose & Thomsen, 2004). CSI thereby exposes the firm to risks by undermining the reputation assets that are unlikely to recover in a short period (Lange & Washburn, 2012). For instance, Toyota’s accelerator pedal problem had a long-lasting continuous media exposure and analysts’ references. One example is that, even in 2016 (7 years after the occurrence), media still cited Toyota’s case (Parrish, 2016), not to mention the numerous case studies adopting it as a negative example (Austen-Smith et al., 2017; Hsu & Lawrence, 2016). These negative publicities, as shown in the literature, will create enduring negative influences on firm brand image and thus on shareholders’ value assessment (Y. Chen et al., 2009; Monga & John, 2008; Pullig et al., 2006). In addition, a firm’s social activities reflect a firm’s internal management structure, policies, and market orientation toward a better synergy with the external environment that is formed with key stakeholders (Gond et al., 2011; Nielsen & Thomsen, 2009). However, CSI signifies that the firm’s internal management and orientation deviate from the synergy with external parties (Lange & Washburn, 2012), and this synergy is unlikely to be restored in a short duration (R. Sims, 2009). This mechanism supports the proposition of the long-term impact of socially irresponsible behaviors. More profoundly, CSI negatively affects consumer attitude toward the firm. In marketing theories, attitude is a notion that has a salient long-term existence once established (Amine, 1998). Firms have to spend considerable time and effort to reverse unfavorable attitudes. On the other side, potential and existing investors use a firm’s social image in their valuation (Luo & Bhattacharya, 2006). This valuation is forward-looking, and therefore the occurrence of CSI will reduce the firm value to the firms in an extended time span rather than over the short term.

The Moderating Role of Environmental Dynamism

Environmental dynamism is one of the necessary considerations when business managers are seeking opportunities from outside. Dynamism is defined as the uncertainty in an industry regarding the business potential and volume (Simerly & Li, 2000). It measures the unpredictability a firm has to face when it is operating under a changing external condition (Husted, 2000; Priem et al., 1995). This uncertainty of industry by nature is originated from and, in many cases, driven by a broad scope of entities including consumers, investors, governments, and/or macroeconomic conditions (T. S. Chung & Low, 2017; Harrington et al., 2005; Mason, 2008). The literature notes that environmental dynamism has been widely recognized as a powerful moderator that changes the strength and direction of the influences of firm strategic elements such as management competency, new product capability, or social activities (Goll & Rasheed, 2004; Hough & White, 2003; Schilke, 2014). Incorporating dynamism into the interaction with CSI is of particular significance because CSI is deeply embedded in and affected by external environments (Lin-Hi & Müller, 2013). One salient feature of a turbulent industry is that no consistent patterns exist in the market. Situational factors such as consumer trends, resource composition, and business networks shift at a high speed (Hough & White, 2003). This condition generates several obvious influences on the link between CSI and firm value. Finance researchers explicitly advocate that investors find all possible factors to assess a firm’s potentials (Hoffmann & Fieseler, 2012). However, in an unstable market, the information acquisition process becomes challenging so that the most salient occurrences will naturally gain higher weight in investors’ valuation system (Hough & White, 2004). Desai (2014) also indicates that the negative media coverage about a firm’s issue will soon be an alert for the environment, leading to changes in the competition that are unfavorable for the firm’s public image. Other stakeholders such as consumers behave in a similar way. Consumers’ decision-making is a process of information collection and analysis (Ariely, 2000; T. Wagner et al., 2008). When there are less reliable and consistent factors to consider, CSI will play a more vigorous role in the purchase decisions and the undermined social identity will reduce consumers’ patronage likelihood and eventually affect firm value.

Furthermore, the dynamic capability theory clearly outlines that the fast-changing environment may create challenges for a firm’s strategy making because a turbulent market sets barriers for a firm to smoothly acquire resources and optimally deploy assets (Eisenhardt & Martin, 2000; Teece et al., 1997). Under these conditions, external resource configurations are unpredictable and the needs for stronger capability become more imperative (Paladino, 2008; Pavlou & El Sawy, 2011; Priem et al., 1995; Teece et al., 1997). CSI, in this type of environment, is less likely to be controlled and remedied by the firm due to the resource constraints. For example, a product failure requires the firm to adjust its production system by updating the old component specifications. However, in a fast-changing environment, this type of attempt for incremental update is often not supported any longer because the market has switched to a radically new platform. In this case, the dynamism of environment makes it harder for a firm to correct its problems, and this will result in lower responsiveness to the market and harm long-term firm value (Joshi & Campbell, 2003).

Nevertheless, there is an alternative logic supporting that, in highly dynamic environments, CSI’s effects may diminish at a higher rate. This view is built upon the rationale that the changing environment may quickly eliminate the negative impact of CSI. For example, a fast-changing environment incurs information processing complexity (Boisot & Child, 1999), which has the potential to reduce the magnitude of negative exposures. Overall, the evidence is somewhat mixed but it seems to have more weight on the CSI’s longer-term effects in highly dynamic environments. Therefore, we tentatively hypothesize the following:

The Moderating Role of Competition Intensity

Competition intensity indicates in an industry how the competitors are distributed regarding their numbers and market strengths. A high-competition-intensity industry is characterized as many firms having similar power in controlling or influencing the market, and therefore customers have more freedom to choose from an extended volume of selections (Auh & Menguc, 2005). In this type of environment, firms are particularly interested in maximizing their advantages as well as minimizing disadvantages because imperfections will incur significant vulnerability in the competition (Ang, 2008). Consumers are sensitive to this type of comparative media content, and thus these strategies give them clearer and more vivid information that directs their purchase decisions (Siomkos et al., 2010). This disadvantage of CSI in competition impacts the firm value assessment via the decrease of brand equity (Creyer & Ross, 1996).

From a shareholder’ perspective, investors are more sensitive to negative activities such as CSI in competitive markets. Several reasons explain this condition. For example, Luo et al. (2010) found that negative information affects analyst recommendations, which in turn affect investment choices. Also, negative information directly triggers investors’ uncertainty about the firm’s future earning ability, and therefore they adjust their valuation accordingly (Luo, 2007). In addition, corporate unethical behaviors indicate caution to investors about the credibility of other information disclosed by the firm and further deteriorate confidence in the firm (Renneboog et al., 2008). Moreover, when a number of similar firms are in a competitive industry, investors have more choices regarding investment targets, and they become more stringent given the extended choice set. In this case, CSI firms will have a particularly negative position within this choice set regarding firm value assessment.

The Moderating Role of Firm Capability

Firms’ dynamic capability is defined as their competency of acquiring, controlling, and deploying firm resources to achieve competitive advantages that lead to the best possible shareholder value (Makadok, 2001). Several key traits of firm capability distinguish it from other strategic aspects of the firm. In the framework of dynamic capability theories (DCTs), capability is dynamic in nature in that it captures the firm’s strengths for coping with fast-changing internal and external environments (Teece et al., 1997). Capability is an inherent trait of the firm and is not simply and easily acquired from the outside. Rather, firm capability is the result of corporate learning from business practice and resource configuration, and thus it is deeply embedded in the whole firm’s activities (Teece et al., 1997). More importantly, DCT describes the goal of having high firm capability beyond the traditional scope of competitive advantages. The competitive advantage in the DCT domain has a salient time-related nature and is termed as a “sustained” competitive advantage (Barney, 2001). If and only if a firm realizes the sustained superior positions in the competition can it benefit shareholders in the long term (Srivastava et al., 1998). Along with that, the DCT also explicitly emphasizes the moderating roles of firm capabilities. For example, Dutta et al. (1999) demonstrate how firm marketing side capability may strengthen the technological competency. Similarly, Kotabe et al. (2002) document the strong moderating effects of firm capabilities on the relationship between market expansion and firm performance. Given the importance of firm capability, it is worthwhile to consider its moderating role on the link between CSI and shareholder value.

In the aforementioned CSI theories, one of the most serious concerns of CSI for a business firm is that it negatively affects brand image and therefore affects shareholder value (Sweetin et al., 2013). However, strong firm capability may mitigate this negative impact because a firm can use its resources to offset or remedy the impact of CSI (Desai, 2014). For example, a properly deployed market-based assets bundle can effectively help a firm in adverse situations (M. F. Cheng & Kesner, 1997). The social network assets of a firm can function in a similar way (Uzzi, 1997). The systematically configured channels can also jointly assist the firm to deal with unfavorable conditions (Liu et al., 2008). Moreover, firms may further improve its internal learning features in the face of the negative disclosure and alleviate the negative impacts (Desai, 2014). This means that a firm with strong capability to organize its resources is likely to bear a lower loss from CSI because of its well-structured learning capacity and coping mechanisms. Firm capability has another valuable trait, which is responsiveness (Teece et al., 1997). A firm with strong capability is able to quickly sense the market information, collect and analyze the information, and promptly launch coping implementations. This nature of capability is especially meaningful for remedying CSI occurrences, which are often neglected by firms at the early stages. Barnett (2014) proposes that media sources largely determine whether and how strongly the audience notices and judges the misconduct of a firm, and meanwhile Trainor et al. (2014) indicate that a firm with strong capability can detect the source of publicity and more promptly launch coping actions and yield better results. Thus, a firm’s capability set is looked as a quick responding mechanism that enables the firm to mitigate the impact of CSI and therefore protects shareholder value in the best possible manner.

Data and Measures

We collected the data from multiple sites such as Compustat, Kinder, Lydenberg, and Domini (KLD), Business Segment database, and firm annual reports. Merging all of the data items from these sites resulted in an unbalanced dataset that contains 4,210 observations from 516 firms that ranged from 1996 to 2015. A number of advantages can be obtained with this data approach. For example, these data are widely known to business researchers and have been adopted in numerous research settings (El Ghoul et al., 2011; Godfrey et al., 2009; Kang et al., 2016). Their reliability has been sufficiently documented and thus the quality of empirical studies can be supported. Furthermore, this dataset comprehensively includes a large number of firms from almost all major industry sectors such as mining and oil, transportation, manufacturing, professional services, retail trade, and wholesale firms. This comprehensive selection, instead of focusing on a limited firm scope, ensures the external validity of this research. Furthermore, this dataset covers the firms’ information over an extended time span that adequately reflects the longitudinal variation of the relationships. This nature is particularly relevant to the main goal of our research. Another advantage is that the panel data structure provides additional benefits for obtaining more precise estimators (Hsiao, 2014). Furthermore, and importantly, these data sources involving Compustat are deemed to have higher objectivity than the data approach based on perceptual answers such as surveys. Over a long-term period, survey data become more difficult to manage and errors may escalate significantly. Table 1 summarizes the descriptive information about the variables. The operationalization methods of each variable are discussed below.

Descriptive Information on Variables and Their Correlations.

p < .1. **p < .05. ***p < .01.

CSI

We collected CSI data from the KLD database. KLD is a large database that annually gathers information from professionals in each industry regarding firms’ strengths/concerns in terms of socially beneficial activities. The KLD rating in this database provides useful information for various business research domains because it has several key advantages such as comprehensive firm type coverage, collective expert opinions, and rich measure items covering different facets of social activities (Dawkins, 2012; Ruf et al., 2001; M. Wagner, 2010). Another notable trait of KLD data is that they clearly distinguish CSR and CSI as reflected by strengths and concerns. We followed Kang et al. (2016) and Mattingly and Berman (2006) to summate the total number of concerns of a firm in a specific year to be the CSI score. The concern items include community relations, corporate governance, diversity, employee relations, environment, human rights, and product for each firm and this measure approach seamlessly matches the conceptualization of CSI because it not only fully recognizes the multifaceted nature of CSI occurrences of various firms but also explores the depth of firm managerial behaviors into functional areas. This match between CSI conceptualization and measure operationalization has been widely recognized by previous studies (Muller & Kräussl, 2011; Strike et al., 2006). However, KLD data items may vary over time, so we addressed this issue by normalizing the raw CSI score against the total maximum number of concerns in each year. This transformation makes the scores comparable across different years and safe to merge for analysis (Kang et al., 2016).

Firm Value

Tobin’s q is frequently used in finance, management, and marketing research as the measure of firm value (Daines, 2001; Jo & Harjoto, 2011). It measures the forward-looking value to investors against book value of firm assets. K. H. Chung and Pruitt (1994) proposed a popular operationalization of Tobin’s q using firm financial data. The formulation is specified as

where DEBT means the difference between short-term liabilities and assets plus book value of inventories and long-term debt. The outcome Tobin’s q from this model is a unitless measure and is consistently comparable across different firms. We collected the component data items from Compustat.

Environmental Dynamism and Competition Intensity

Environmental dynamism reflects the turbulence rate of each industry (Keats & Hitt, 1988). We followed previous research to measure dynamism using the coefficient of variation of sales volume in each industry for every 5-year moving window. To capture the seasonal variation, we used quarterly data as suggested by Sridhar et al. (2014). For competition intensity, the Herfindahl–Hirschman index (HHI) indicates the concentration ratio of firms in an industry, and 1-HHI becomes a preferred measure of competition intensity (Flammer, 2015).

Firm Capability

The fundamental notion of firm capability is to what degree a firm is capable of transforming its resources to business outcomes. In this sense, an input–output approach of measuring capability is desirable. The same approach can be seen in various resource-based view (RBV) and DCT studies (Dutta et al., 2005; Mahmood et al., 2011). In this input–output frame, the stochastic frontier model (SFM) is adopted to generate capability scores. The SFM gauges the distance between each firm and the best performer in the same group regarding the efficient use of input variables to achieve outputs. This method pinpoints the nature of firm capability, and its validity is confirmed by numerous previous works in this stream (Dutta et al., 2005; Lieberman & Dhawan, 2005). To obtain the input variables, we collected an extended list of items from Compustat. Each of these items has been supported by previous research to represent specific input resources. We collected data on selling, general, and administrative (SG&A) expense to measure management and marketing inputs (Bahadir et al., 2008). We collected R&D expenditure data to measure the input in innovation and technological development. Cost of goods sold was collected to reflect the procurement and production inputs (Dutta et al., 1999). The number of employees was used to measure the human resource. In addition to that, we also collected receivables to proxy the customer relationship stock as it reflects the willingness to extend credits to customers (Dutta et al., 1999). We collected balance sheet intangibles to represent the intangible assets of a firm. We also input slack resource, which was obtained by generating a principal component from working capital and retained earnings (Fang et al., 2008). Slack resource is important because it represents the resource abundance of a firm. For the outcome variables, we used return on assets (ROA) as well as market share to reflect the multifaceted nature of firm business outcomes in relation to both profitability and market position achieved in competition.

Other Control Variables

Because we used a panel data VARX, we included several additional control variables. We used firm size to control the size effect on firm value. We collected total assets from Compustat and applied a log transformation on it (Maury & Pajuste, 2005). Because product market diversification may affect firm value, we controlled for firm diversification by collecting the number of firm product segments from the Business Segment database (Hyland & Diltz, 2002). We also included industry munificence, measured by the growth rate of each industry in the 5-year moving windows as proposed by Keats and Hitt (1988), to be an additional environmental factor to control the industry growth effect.

Empirical Estimation Method

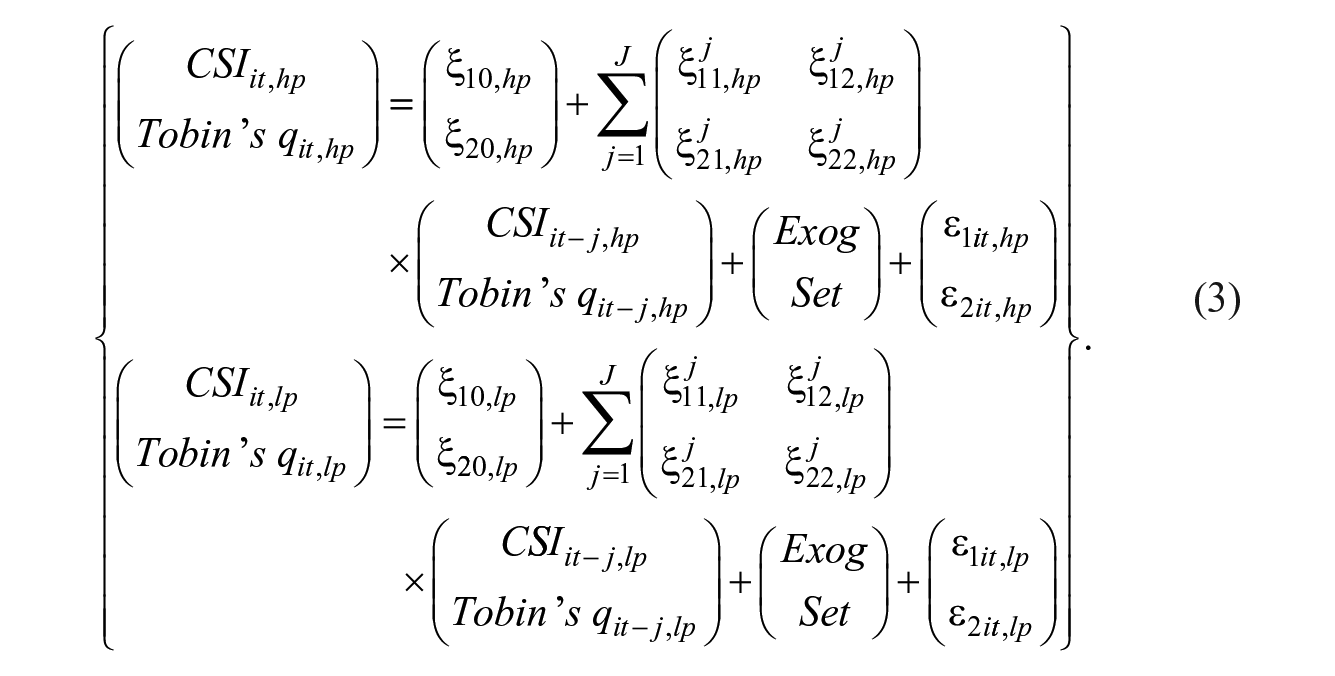

Given the special goal for long-term dynamic relationships, traditional cross-sectional methods are no longer applicable. In our empirical work, we chose the panel data VARX to estimate the proposed framework. Business research has been increasingly using VARX to track time-series relationships. For example, it has been used to examine the long-term effects of new products, social networks, and user contents on firm performance (Pauwels et al., 2004; Stephen & Toubia, 2010; Tirunillai & Tellis, 2012). The basic format of VARX is constituted by a system of equations in which each variable is regressed against its own lag terms and also against the lag terms of other endogenous variables. Therefore, the time-related impacts can be estimated in the VARX system. Because the main interest of this article is to examine the long-term effects of CSI under the moderating factors, dynamism, competition, and capability, we median-split the dataset into high and low scenarios of each of the three moderators and then ran VARX for each subset. Researchers such as Lim et al. (2005) and Sismeiro et al. (2012) have explicitly called for this form of segmented vector autoregressive model because it demonstrates how the same proposed theoretical relationship can vary in different groups and therefore yield more detailed and more in-depth insights. Showing the significance between the results of the high versus low scenarios cannot be accomplished by the traditional interaction term in the cross-sectional research. Testing this difference is achieved by the holdout sample method. We randomly retained half of the data for the VARX analysis and retained another half as the holdout sample to test the differences between the high versus low scenarios after the estimators were obtained. The systems of equations are formulated as follows:

In these equations, t denotes time periods, i denotes firms, j means lags, hd/ld means high and low dynamism, respectively, hc/lc means high and low competition intensity, respectively, and hp/lp means high and low capability, respectively. “Exog Set” means the control variables including environmental factors (munificence, dynamism, and competition), firm size, and diversification. This model formulation has several preferable traits. First, the equation system extends the traditional dynamic panel data model into a more realistic structure in which the relationships are looked as two-way along the timeline (Tirunillai & Tellis, 2012). Second, the set of control variables covers both firm nature as well as the multiple aspects of the environment and considers the balance between model complexity and parsimony. Third, the dynamic system equation makes further forecast studies more precise than traditional VAR models because the information set has been extended to incorporate other variables’ histories (Verbeek, 2004). Fourth, the mirrored dynamic terms between CSI and firm value avoid the task of identifying “a priori” endogenous and exogenous roles in the pair, and therefore the arbitrary constraints that are used to ensure identification are not required (C. A. Sims, 1980).

A necessary condition for running VARX is that each endogenous variable should be stationary. The existence of unit root will make VARX no longer appropriate; therefore, unit root tests will be applied first. Because the dynamic panel data model has the threat of fixed effect, we sought to remove that fixed effect by choosing a Helmert transformation for the variables. This transformation applies a forward mean-difference method and is more desired than the traditional mean differencing because the Helmert transformation works better to retain the orthogonality in between the new transformed variables and the lags of original variables. This feature allows researchers to use more efficient estimation methods such as generalized method of moments (GMM) that enclose lagged endogenous variables as instrument variables (Love & Zicchino, 2006). We chose the system GMM to estimate the VARX because it has special strengths for handling this type of dynamic panel data. For example, it is robust on the distributional assumptions and is heteroscedasticity consistent in addition to its ability to handle endogeneity.

To seek the useful inferences from VARX, impulse response functions (IRFs) based on VARX should be employed (Love & Zicchino, 2006; Luo, 2009; Pauwels et al., 2004; Stephen & Toubia, 2010). IRF traces the dynamic movement of the impact of one variable on another into multiple-period time frames. It estimates how much changes on the response variable at each time period can be traced back to one standard deviation change of the impulse variable at the start point. The significance level of IRF is achieved by applying Monte-Carlo simulations of the IRFs (Tirunillai & Tellis, 2012).

Results and Discussion

To check the appropriateness of using VARX, we first adopted a series of unit root tests on CSI and Tobin’s q in each of the six scenarios (high vs. low on dynamism, competition, and capability). To ensure the robustness of the test, we used four unit root test methods: Im, Pesaran, and Shin test; ADF-Fisher test, Phillips–Perron–Fisher test, as well as the Levin, Lin, and Chu test. The results are presented in Table 2. Both of the variables display stationarity in all the six scenarios, and therefore VARX can be safely used. We used Hansen’s J test to examine the overidentification of the scenarios, and no threats were found. As mentioned in the “Empirical Estimation Method” section, to obtain the significance band of IRFs, Monte-Carlo simulation was employed. We ran the simulation 500 times and constituted the 95% significance level for the IRFs in each of the scenarios. The results are presented in Tables 3 to 5. To more clearly present the relationships, we graphed the results in Figures 1 to 3.

Unit Root Tests on the Endogenous Variables.

Note. Null hypothesis: unit root.

p < .1. **p < .05. ***p < .01.

CSI’s Longitudinal Effects on Firm Value Under High Versus Low Environmental Dynamism.

Note. The bold numbers are significant estimators at the 95% significance level based on 500 times Monte-Carlo simulation of the impulse response functions. CSI = corporate social irresponsibility.

CSI’s Longitudinal Effects on Firm Value Under High Versus Low Competition Intensity.

Note. The bold numbers are significant estimators at the 95% significance level based on 500 times Monte-Carlo simulation of the impulse response functions. CSI = corporate social irresponsibility.

CSI’s Longitudinal Effects on Firm Value With High Versus Low Firm Capability.

Note. The bold numbers are significant estimators at the 95% significance level based on 500 times Monte-Carlo simulation of the impulse response functions. CSI = corporate social irresponsibility.

CSI’s longitudinal effects on firm value under high versus low environmental dynamism.

CSI’s longitudinal effects on firm value under high versus low competition intensity.

CSI’s longitudinal effects on firm value with high versus low firm capability.

CSI and Firm Value Under High Versus Low Environmental Dynamism

Table 3 and Figure 1 show the IRFs of CSI on firm value under high and low dynamism. Several important findings emerge in the results. One can observe that, when the environment is highly turbulent, CSI has a 5-year influence on firm value. However, in the low-dynamism environment, CSI’s influence only lasts for 1 year. Beyond that, CSI’s impact strength on firm value is much higher in the high-dynamism environment (average IRF = −0.175 in the 5 years of high-dynamism environment vs. IRF = − 0.099 in the low-dynamism environment). This means that, practically, a 0.116 (one standard deviation) increase in a firm’s CSI will lead to the drop of 0.275 and 0.155 in firm value (as reflected by Tobin’s q) in high- versus low-dynamism industries. These two findings jointly indicate that CSI places a more enduring and more powerful negative influence on firm value in turbulent markets. Thus, H1 is strongly supported. The finding of CSI’s short-term impact on a low-dynamism environment also echoes the findings of Sudhir (2001) that a stable market has an equilibrium that is hard to break once it is established. However, in turbulent markets where the resources, relationships, and information patterns are constantly changing, CSI exerts a significant effect as it influences investors’ decisions in a negative direction. Another interesting finding is that only in Year 1 the IRF strength of CSI is lower in the high-dynamism environment (IRF = −0.086 vs. IRF= −0.099). This finding is in line with business environment theories that a stable environment could make the information collection easier (Song et al., 2009) so that CSI can have a quicker and stronger impact at the beginning. However, in a turbulent market, it takes more time and effort to collect and absorb external information. The results also show that in the concurrent year (Year 0) CSI does not impact firm value in either of the environment conditions. This is supported by the reality that a burst of public exposure often has a time lag after the actual CSI occurrence. This also explains that, in the CSR/CSI literature, insignificant results are often found regarding social activities of the firm. Many of the results may simply be due to the insufficient consideration of the time-related effects. However, there is an alternative reasoning in that a dynamic environment may also make stakeholders such as consumers and investors more easily forget the negative news due to information overflow, and then the negativity of CSI may travel shorter time in a dynamic market. Our empirical work demonstrates that this effect is in general outweighed by the enduring mechanisms of CSI and the overall pattern shows its longer-term effects in high-dynamism conditions.

CSI and Firm Value Under High Versus Low Competition Intensity

In our theoretical development, we expected that CSI should have a stronger harming effect on firm value. The empirical results confirm such a proposition (Table 4 and Figure 2). When the competition intensity is high, CSI’s effect remains significant for 7 years. In contrast, in a low-competition market, CSI does have a significant influence, supporting H3. These findings reveal several key insights that have not been deciphered by previous researchers. Although the literature has provided evidence about the moderating role of competition on CSR, the long-term impact of CSI has never been clearly demonstrated. Due to the challenge of finding the precise cutoff points between the long term and the short term, we, in general, use the first 3 years to denote the short term and the following years as the long term. This cutoff point is chosen because a business cycle is more likely to be concentrated in an approximate 3-year time frame. Firms tend to use 1 or 2 years as their planning phase and use the third year as the evaluation or auditing stage (Groenveld, 2007). A similar notion of time can be found in other studies such as Doukas and Lang (2003) and López et al. (2007). In a competitive market, CSI seems to be a strong and long-lasting factor that decreases firm value (average IRF = −0.115, p < .05). This reflects the fundamental nature of CSI in a firm’s business operations in that, under those demanding environments, investors allocate more weight to CSI in their valuation formulas. This reinforces the social responsibility theory that advocates that social irresponsibility is related to competitive disadvantages, but our research further shows that it is even more meaningful and indicative for the “sustained” competitive disadvantages.

Another finding is equally noteworthy

The IRF of CSI in a high-competition-intensity market displays a salient “buildup” and “decay” pattern. The negative response increases (we use “increase” to discuss magnitude rather than signs) from 0 to −0.134 for Year 0 to Year 3 and then decreases to Year 7. The finding of this pattern significantly enriches the CSI theories. Traditional thinking about the negative influences of firm activities may be a unidirectional curve, with the highest impact at the beginning. However, our research provides empirical evidence showing that the impact of these activities may take time to build until they reach a peak.

CSI and Firm Value With High Versus Low Firm Capability

In contrast to dynamism and competition, firm capability represents the intrinsic competency of the firm. We expected that, for low-capability firms, CSI will have a more severe influence on firm value (H3). Our empirical findings confirm this hypothesis and go further beyond this theory scope. The VARX and IRF analyses show that, for low-capability firms, CSI exerts a negative impact for 6 years with a largely decreasing strength pattern (IRF = −0.181, p < .05 at Year 1 and IRF = −0.040 p < .05 at Year 6). However, it is interesting to find that, for high-capability firms, CSI does not display any significant effect on firm value (Table 5 and Figure 3). These findings generate several key insights that are generally missing in either CSR/CSI or RBV/DCT theory streams. The extant capability literature is mainly limited to the role of capabilities of assisting other firm factors to achieve performance, but to date there is little knowledge about how capability may play a role in remedying a firm’s negative aspects such as CSI. Our finding thus explores such a direction and shows that firms’ CSI can be offset by having superior capabilities. Furthermore, it has been found that high-capability firms may perform better in managing shareholder relations including informing, assuring, and communicating with them (Hockerts & Moir, 2004). Our results echo this reasoning from the CSI’s insignificant impact. Another interesting finding is that CSI’s effect for a low-capability firm is largely a decay trend, which means that the negative impact quickly reaches its peak. This finding is critical in that it is in line with the root of DCT that firms are vulnerable to immediate shocks when they lack the protection from capability (Dutta et al., 1999). Finally, DCT emphasizes the time-related nature of capability, which is theoretically suggested to have long-term effects but empirically has little evidence. In our research results, the long-term insignificant relationship between CSI and firm value for high-capability firms sufficiently demonstrates an enduring nature of firm capability for not only facilitating firm strategies as proposed in the literature but also saving firms from crisis.

Additional Studies and Robustness Checks

As we compared the high–low scenarios, we used the IRFs from our research results, applied them to another half of the data, and compared the differences between the scenarios. Using holdout samples may further validate our results obtained from the main model. The results show that all the differences are significant at the .05 level. To further ensure the robustness of the model formulation, we also included CSR and ROA into the control variables, and the results are largely consistent. We also conducted a series of robustness checks by measuring the variables using alternative approaches. For example, in addition to measuring dynamism as the coefficient of variations, we also used the measure proposed by Keats and Hitt (1988) from a series of time-series regression coefficients’ standard errors of the industry sales. We also changed the quarterly data to yearly data and tested the industry definition from four-digit SIC codes to three-digit SIC codes. For measuring capability, we used a normal–half normal distribution assumption and also tested other assumptions such as normal–exponential and normal–truncated distributional assumptions; the results and the inferences were largely consistent.

Implications

Implications for Theories

Although the major focus of the current corporate societal activities is largely limited to CSR, our research takes the first attempt to explore the in-depth understanding of CSI’s longitudinal effects on firm value under the moderations of a firm’s environmental factors, dynamism and competition, as well as a firm intrinsic nature variable, firm capability. This research framework generates a number of useful implications for theories such as CSR research, RBV and DCT streams, shareholder value maximization, business environment, and contingency theories.

In the social responsibility research domain, CSR and CSI have been found to have mixed results on firm performance, and the understanding of their true roles is rather confusing because of the contradictory evidence. Our research of the longitudinal study based on moderations reveals some fundamental clarifications. For example, the effect of firm social activities such as CSR and CSI is well known to vary under different conditions. Our research shows that different industries as grouped by turbulence rate and competition intensity create salient differences in terms of CSI’s role on firm value. Furthermore, firms with high and low capability also yield varying power on performance. These moderating models partially explain the mixed findings in the literature. In addition to that, our research also demonstrates that these social activities do not have an immediate or concurrent impact on firm performance as reflected by firm value. In this sense, researchers who fail to consider the lag effects of these factors might find weak or insignificant relationships. Our research thus provides additional explanations of the mixed pattern in regards to the time dimension. The buildup and decay pattern of CSI’s influence in our results further illustrates the dynamic nature of these social factors. Researchers should consider both cross-sectional and longitudinal models to fully account for their influences. The same logic set can be further leveraged to other firm strategies or factors when researchers are tracing their performance implications. Firm strategies may show varying strengths along the timeline, and researchers should capture such an evolving route to generate meaningful insights.

Our research also more deeply enriches the CSI literature, which is almost solely focused on its negative aspects and therefore gives a prevailing perception that CSI should be detrimental in all situations. However, our results demonstrate that in certain conditions such as low competition or high firm capability, CSI may not have the expected negative impacts on performance. Researchers in this stream should be more aware of both the internal mechanism of CSI regarding its possible positive impacts on financial outcomes as well as the external conditions that might not grant sufficient penalty on firms’ CSI activities. More importantly, during and after CSI occurrence, high-capability firms are skilled to detect and analyze situations, and they can quickly launch coping strategies to recover the loss. In this sense, researchers in the CSI area should be informed of the joint effects of positive and negative factors about CSI along with firm competency levels before they attempt to explain its relations with outcomes.

The focus of firm value in this research carries special merits in that the stakeholder view of CSR has long been advocating the importance of social investment for shareholders’ valuation. Firm value stands for the ultimate goal of running a firm and researchers have invested massive efforts in exploring and sorting out effective firm factors that influence this outcome. However, CSI has been largely missed in this scheme. Yet, this construct deserves much more attention because in theory it is fairly different from CSR, and more importantly CSI reflects a number of firm’s inherent operational weaknesses and/or orientational problems that may have the potential to generate more profound effects on firm value. Our research thus raises this issue that may benefit future research in this direction.

Our study also responds to the special calling for the long-term effects of firm social activities. Researchers have been sufficiently aware of the importance of tracing these types of influences, but little knowledge exists. Knowing these longitudinal patterns is particularly important for several reasons. CSI studies are characterized as a continuous strategic area in which firms are looking for long-term engagement of these activities. Moreover, management teams are interested in the long-term potential of these activities rather than the immediate impact, and therefore tracing the time-related paths will give firms a solid motivation for launching CSR and avoiding CSI. Equally importantly, firm operations are a function of time, and its effectiveness is also dynamic along the timeline. Considering the time factor, therefore, yields more meaningful explanations. Similarly, as our results demonstrate, the stakeholders’ acceptance or rejection of firm activities may also be a function of time. For example, shareholders may initially be less sensitive about CSI. However, over time, their concerns escalate when in a competitive market, as shown in our results. Finally, firm management and strategy are forward-looking notions; shareholders’ valuation is also a forward-looking process. Therefore, studying the long-term dynamic relationships becomes a necessary avenue.

Our research also helps further extend DCT because the traditional view of firm capability is usually limited to its beneficial role of assisting firm factors such as strategies, operations, and innovations to achieve performance, and few studies explore its function in offsetting, correcting, or remedying the firm’s negative factors such as CSI. Yet, this new direction is crucial because firms constantly face uncertainties and risks and there are always management and marketing imperfections. Thus, how to use firm capability in those negative situations becomes an equally or even more important area. Furthermore, although capability is a result of the entire firm’s learning and practicing activities, CSI often happens to a single functional area of a firm, and thus they may be treated as two conceptually distant constructs. However, our research demonstrates that there might be more profound links between them, especially in a longitudinal research framework.

Implications for Managers

Our research first guides managers to consider strategic emphasis and resource allocation for crisis management after CSI incidents. In practice, managers tend to focus on the immediate needs for addressing negative impacts, for example, immediate customer care or advertising budgets are made to assure consumers; immediate press meetings are held to inform investors. However, those solutions often lose momentum in the long term. Our research provides clear evidence, showing that managers should have a long-term view when coping with the CSI exposure, especially when they are in turbulent, intensively competitive market environments and when their firms lack strong capabilities. This long-term view of CSI has enduring effects on firm performance such as shareholder value because of the persistent nature of CSI that is associated with competition threats, negative information spread, and stakeholders’ confidence. Managers, therefore, should launch their coping strategies in a forward-looking approach rather than a “one-time-for-all” solution.

After CSIs occur, managers are often wondering how much negative impact those activities will bring to the firm. More often than not, they do not see immediate adverse business results, and this leads to an underestimation of the seriousness of CSIs. The “buildup and decay” pattern of CSI’s shock answers the puzzling question and cautions managers to realize that the effects of CSIs on their business performance exhibit time lags and will have a postponed peak. Therefore, our research suggests the full managerial engagement once CSIs occur rather than keeping waiting until the maximum damage is detected.

Our research also yields implications for proactively establishing effective corporate procedures to minimize CSI. In business practice, managers consistently encounter dilemmas involving benefits and costs, and preventing CSI is one of these tradeoffs. Although managers can fully recognize the detrimental force of CSI on their performance and they are motivated to take proactive preparations, they also have to redirect a large amount of their key resources away from their business cores to social activities, which may dilute the firm’s strengths. However, our research provides support for an adequate engagement in proactive preparation and particularly in highly competitive markets and fast-changing environments because, in these types of environments, CSIs may create strong and long-lasting negative results for firm performance.

Along with business domains, our research may also find its use in a broader scope such as public policymaking in the society. Firms’ irresponsible behaviors not only affect their own performance but also may produce spillover or chain effects and yield more profound impacts on the public (e.g., the BP’s oil spill crisis created significant public concerns). This enduring nature of CSI, as shown in our results, gives special caution for the policymakers to understand the industry characteristics and track the possible route of the negative impacts over time. Ample evidence demonstrates that the social and psychological impacts on pubic resulted from firms’ CSIs. Regulators and policymakers, therefore, need to pay particular attention to the industries that are highly turbulent and competitive to more effectively and efficiently deploy public remedial programs because CSI’s detrimental effects are more severe in these industries. Also, when they observe that the focal firm(s) lacks resources or capabilities of handling the crisis, early intervention may be more important to avoid the escalation of negative consequences.

Limitations and Future Research Ideas

This research uses two external factors (dynamism and competition) and one internal factor (capability) as moderators to decode the longitudinal effects of CSI on firm value. However, there are more influential sources that future researchers could consider. For example, CSI and CSR in reality may coexist in business firms and thus an interesting future research idea is to adopt CSR as an additional moderator. CSR’s strong or weak presence may function very differently on levitating the negative impacts of a firm’s CSI. Another idea with potential is to consider financial strengths such as ROA as a moderator. This direction is rewarding because financial strengths will largely determine the readiness for launching coping mechanisms for remedying CSI and represents a firm’s capacity of acquiring external resources and solutions. Furthermore, nonmarket environmental factors such as private politics and corporate political activities, publicity, and media attention will be another powerful portfolio of moderators that will further contribute to this research stream. The combination of market and nonmarket may be even more critical for firm managers to more precisely and effectively handle social activities and aim at better firm outcomes.

In this research, we only used firm value as the outcome variable, and thus this article is mainly positioned to understand CSI from the shareholder’s view. However, as the vast body of extant CSR/CSI research demonstrated, other stakeholders are of similar interest. For example, future researchers can further target the CSI’s long-term influences on consumer metrics such as satisfaction, brand equity, and switching behaviors. Organizational behavior researchers, on the other hand, can explore more of how CSI may affect internal stakeholders such as employees. This extended version of outcome variables, collectively, should yield a more comprehensive pattern that assists academic researchers as well as business practitioners.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.