Abstract

This study examines the degree of state ownership on corporate bribery. Integrating the theories of state ownership and corporate corruption, we propose that state ownership influences bribery propensity and bribery intensity in different ways; it lowers a firm’s tendency to pay bribes but increases the relative amount of bribery payment. Building on the control rights/bargaining hypotheses, we demonstrate that state ownership shields firms from bribery demands by reducing administrative hurdles that include bureaucratic requirements of obtaining licenses or settling taxes in business operations. However, state ownership elevates the level of bribes by weakening their capital mobility. Using a sample of 23,018 firms from 54 countries covering 2006 to 2013, we find evidence to support our hypotheses. This article contributes to corruption research by drawing attention to an important channel of corruption and by highlighting the importance of considering not only the propensity but also the intensity of bribe payments.

The issue of corporate bribery forms a central topic in the corruption literature (Fleming & Zyglidopoulos, 2009). Bribing public officials to obtain and retain business not only poses threats to the stability of societies but also undermines moral and ethical values in organizations (Lennerfors, 2009; Sanyal, 2005). Therefore, a large body of corruption research focuses on the antecedents of corporate bribery in a variety of organizational and industry contexts (Y. Chen et al., 2008; Collins et al., 2009; Jeong & Weiner, 2012).]. Although many previous studies control for the effect of state ownership in investigating the firm-specific causes of bribery (Martin et al., 2007), research is silent on when, why, and how much state ownership affects bribery behavior. The Organisation for Economic Cooperation and Development (OECD, 2019) State-Owned Enterprises (SOEs) and Corruption Report particularly calls for further investigation into the bribes paid by SOEs. Previous research has indicated that SOEs are also prone to bribe payments in certain circumstances, stressing the need for a deeper investigation of specific mechanisms that how state ownership shapes bribery behaviors (Shaheer et al., 2019). In this article, we respond to the recent calls for deepening research on state ownership and bribery behavior by theorizing some important mechanisms behind bribery behavior of firms with state ownership.

We extend the control rights/bargaining hypotheses by Svensson (2003) to develop a theoretical framework that may explain the mechanisms behind bribery behavior of firms with state ownership. The seminal article by Svensson (2003) in the economics of corruption research reveals the subtle distinction behind mechanisms that may shape the likelihood of bribe payment and the amount paid in bribes. However, the extant research rarely clarifies whether a given factor influences both bribery propensity and bribery intensity in the same fashion, partly because it is often less than obvious, a priori, why a line of argument would apply to only one dimension of bribery behavior but not the other. We address this theoretical gap in the novel context of firms with state ownership. In particular, we theorize that the control of corrupt officials on a firm’s business, as determined by the firm’s required dealings with public officials, may enhance the firm’s bribery propensity while the firm’s bargaining position vis-à-vis corrupt officials, as determined by firm ability to relocate its business, may influence the firm’s bribery intensity. Accordingly, we suggest that state ownership in a firm may lead to a lower bribery propensity by reducing the firm’s dealing with public officials but may result in a high bribery intensity for bribe-paying firms due to restricting firm mobility to other sectors. Hence, we propose the divergent effects of state ownership on a firm’s tendency to pay bribes versus the relative amount a bribe-paying firm pays.

Using a sample of 23,018 firms from 54 countries, we find empirical support for our hypothesis that the degree of state ownership reduces the incidence of bribery, yet raises the payment size should the firm engages in bribery. We further test the specific mechanisms in our theoretical framework. We find that the degree of state ownership shields firms from bribery demands by reducing administrative hurdles but elevates the level of bribes by weakening their capital mobility.

We make some important contributions to the literature on corruption and state ownership. First, our study extends the understanding of the persistent phenomenon of public corruption by distinguishing the mechanisms of bribery propensity and intensity. Although researchers have paid considerable attention to the determinants of corporate bribery, most studies focus on either the incidence (C. W. Chen et al., 2015; Y. Chen et al., 2008; Clarke & Xu, 2004; Collins et al., 2009; Martin et al., 2007; Shaheer et al., 2019; Wu, 2009) or the intensity (Lee et al., 2010; Zhou & Peng, 2012) of making illicit payments. In our study, we focus on both incidence and intensity to fill the research gap. We corroborate the control rights/bargaining hypotheses to show that the impacts of state ownership on bribery propensity and intensity are driven by different mechanisms. The use of two-stage Heckman analysis to alleviate sample selection bias may further help future research explore other mechanisms. Our findings imply that the research on corporate bribery may produce a more comprehensive analysis by recognizing not only the incidence but also the intensity of unethical practices. Besides, other studies have focused on the macro causes of corruption, primarily revolving around the national and cultural contexts in which supplying bribes by the firm and demanding bribes by the official is the most likely (C. W. Chen et al., 2015; Y. Chen et al., 2008; Clarke & Xu, 2004; Husted, 1999; Jeong & Weiner, 2012; Sanyal, 2005; Shaheer et al., 2019; Shleifer & Vishny, 1993; Wu, 2005, 2009; Zhou & Peng, 2012). Article sheds new light on the intrinsic firm-specific causes of corruption and provides implications for regulators striving to curb bribery.

Second, we contribute to the literature on firms with state ownership by highlighting some of their distinctive characteristics that may influence their ethical behaviors. Although firms with state ownership are becoming more important in the global marketplace, the theoretical development of such firms still lags. Various theoretical mechanisms have been proposed in the literature as to how state ownership shapes various firm behaviors (Bruton et al., 2015; Cuervo-Cazurra et al., 2014). Among the most common are soft budget constraints (Tan & Peng, 2003), political connections (Jia, 2014; Shi et al., 2014), political legitimacy (Meyer et al., 2014), and agency problems (Shleifer & Vishny, 1994). These studies emphasize one or another characteristic of state ownership based on the different contexts in which firms are embedded (Cui & Jiang, 2012; Pan et al., 2014). Yet what exactly state ownership contributes to firm ethical behavior, particularly bribery decisions, is neglected in the corruption literature (Liang et al., 2015; Xia et al., 2014). We build on previous theorizations about state ownership to uncover the reasons behind the varied state ownership effects on bribery propensity and intensity. Hence, we provide a context to the theories of state ownership for developing a better understanding of how state ownership functions to shape ethical behaviors, which is the critical first step toward formulating effective strategies for improving their ethical behaviors (Inoue et al., 2013).

Third, we contribute to literature on bribery mechanisms of state ownership in developing economies by examining the mechanisms in a sample with developing countries. Previous studies mostly focus on the factors that determine the level of bribery in a general context (Lee et al., 2010; Wu, 2009). In this study, the findings of distinguished mechanisms of bribery propensity and intensity of state ownership may trigger the attention for the role of state ownership in controlling corruption in development countries. Despite the low incidence of bribing, firms with state ownership are in fact a salient vehicle by which valuable public funds can be drained, subsequently compromising the effectiveness of state-led growth and jeopardizing national competitiveness, especially for resource-scarce developing economies.

Theory and Hypotheses

Bribery refers to “the offering, promising, or giving something in order to influence a public official in the execution of his/her official duties” (Sanyal, 2005, p. 139). Bribery is a specific form of corruption that is considered both illegal and unethical; it not only violates widely accepted moral norms but is criminalized in most national as well as international legislations (Gorsira et al., 2018; Husted, 1994; Lennerfors, 2009; Pendse, 2012). As corrupt behaviors like bribery are found to have severely negative impacts on countries, organizations, and individuals (Burke & Tomlinson, 2016; Lounsbury & Hirsch, 2010), the issue of corporate bribery draws substantial research attention by scholars.

State Ownership and Bribery Propensity: Control Rights Perspective

Although a large body of ethics literature focuses on country-level causes of corruption, there are notable variations in bribery among firms from same institutional environment (Lee et al., 2010). Assigning explanatory primacy to the firm, research on the economics of corruption provides a useful framework—the control rights/bargaining hypotheses—to account for firm-specific determinants of bribery (Svensson, 2003). The framework rests on the premise that firms do not equally need to pay bribes, and also systematically differ in the amount of bribes paid. Bribery propensity is a function of the control rights that public officials have over the firm. In general, required dealings with the public officials expose the firm to officials’ demand for money and increase the likelihood of the firm submitting to bribery requests to continue operations. Put differently, when a firm cannot avoid the extensive interactions with government officials in acquiring administrative approvals for business survival, it would be under greater control of corrupt officials, and thus more likely to pay bribes. Given the multiple intrinsic characteristics associated with state ownership (Bruton et al., 2015; Cuervo-Cazurra et al., 2014), some features of state ownership may reduce the control rights that officials could wield. Therefore, we expect the bribery propensity mechanism as:

In the following section, we draw insights from the theories of state ownership to identify and investigate characteristics that may explain the reasons behind the propensity mechanism hypothesis.

The Mediation Mechanism of Bribery Propensity: Administrative Hurdles

The control rights hypothesis (Svensson, 2003) suggests that bribery propensity is a function of a firm’s need to interact with public officials for overcoming administrative requirements. Below, we build upon the previous literature and argue that administrative hurdles mediate the effect of state ownership on bribery propensity.

Administrative barriers, such as obtaining government approvals or dealing with regulatory agencies, increase a firm’s dependence on government officials, which effectively brings the firm under officials’ control and opens opportunities for officials to extract bribes from businesses.

We argue that firms with state ownership may face lower administrative hurdles mainly because of their greater political legitimacy than firms without state ownership. As suggested in the literature, the existence of state ownership centers on the ideology and political strategy of the government (Bös, 1986; Whelan & Muthuri, 2017). This perspective posits that government forms state ownership to achieve various political objectives. For instance, firms with majority state ownership may serve to promote industrial development of the country by investing in large-scale projects that have long payback periods but can contribute to economic activities across a range of upstream and downstream industries, which private enterprises do not have the interest or risk-bearing capacity to initiate (Lawson, 1994). Other political objectives include maximizing social welfare through the redistribution of income, and controlling industries of strategic importance (Cuervo-Cazurra et al., 2014). Serving as the vehicle for attaining state objectives may grant higher political legitimacy to firms with state ownership, conferring on them preferential treatment from political and bureaucratic authorities.

We propose two channels through which the political legitimacy of firms with state ownership may alleviate their burden of dealing with various bureaucratic requirements. First, whether these political objectives can be served as desired depends on the continued operations of firms with state ownership. Increased state ownership signals strong vested interests of the government in the successful operations of the establishment (Whelan & Muthuri, 2017), so that more state ownership is less subject to administrative hurdles in obtaining necessary licenses, permits, and government approvals related to their businesses. In some cases, licenses may be created specifically for firms with more state ownership to raise revenue for the state or discretionary use by politicians (Lawson, 1994). Therefore, firms with more state ownership should face less difficulty, and in fact fewer chances of dealing with government agencies, in securing vital sanctions for business operations.

Second, the activities of firms with state ownership are also perceived as politically more legitimate because some of their business operations, such as production arrangements and corporate policies, are governed by the government through direct ownership (Sappington & Stiglitz, 1987). Although compliance with various state regulations may impose a considerable hurdle to other enterprises, being controlled by the government may reduce the necessity for other state authorities to strictly monitor firms with state ownership’s compliance with regulatory standards such as taxation. In other words, firms with more state ownership are less likely to face the need for extensive interactions with government agencies in attempts to prove their compliance with various legal requirements. Therefore, we hypothesize that

Next, we extend the control rights hypothesis to argue that attenuated intervention in the firm’s operation by government agents may restrict the opportunity for individual officials to extract bribes from the firm. Increased interaction with government officials for overcoming administrative hurdles may impose various costs on businesses. Firms may face the cost of managerial time consumed in engaging with authorities, and compromise business efficiency due to delayed approvals, licenses, and permits (Svensson, 2003). These costs and required dealings confer on public officials substantial control over business enterprises, as officials may threaten to increase administrative hurdles during the interactions with firms and can force firms to pay bribes for minimizing these costs. Therefore, we propose that

As we argue above, the political legitimacy of firms with state ownership may reduce their reliance on individual officials’ discretion in issuing administrative approvals such as business licensees or permits or attesting their compliance with burdensome administrative obligations. Officials’ dampened control over firms with state ownership in this respect implies that the latter may avoid paying bribes without any major negative impact on their business operations. This serves as an important mechanism to explain why firms with more state ownership have a lower level of bribery propensity, which are more likely to encounter various regulatory inspections and delayed administrative approvals should bribery requests be not satisfied.

Taken together, bribery propensity mechanism is mainly rooted at the institutional pressure, which provides political legitimacy and conducts control rights for SOEs. Therefore, the mediation hypothesis of bribery propensity is proposed:

State Ownership and Bribery Intensity: Bargaining Position Perspective

We propose that bribery propensity and intensity are likely to be driven by two separate mechanisms. Once the firms decide to bribe, the amount a firm needs to transfer depends on the firm’s bargaining position against the rent-maximizing officials, which is in turn affected by its ability to pay bribes (Clarke & Xu, 2004) and the “ability to walk away from the table” (Lee et al., 2010, p. 776). Officials will demand a bigger payment for a given service when the firm can afford it, or has weaker refusal power due to its high cost to exit.

Extending the control rights/bargaining hypotheses, we argue that state ownership shields a firm from bribery requests through strong relationships and shared interests with government bodies. Different from private firms that need to deal with the public sector for survival, state ownership may obviate dealings with corrupt officials for survival and weaken individual officials’ discretionary power (Clarke & Xu, 2004; Shaheer et al., 2019). On the other hand, should firms with state ownership need to pay bribes, they may have a weaker ability to walk away from the table because of their lower capital mobility, which increases their cost of exiting from the market or reallocating their resources to other sectors. Thus, we propose the bribery intensity mechanism:

Next, we draw insights from other characteristics that may affect officials’ bargaining power, which induce that divergent effects on bribery propensity and intensity.

The Mediating Mechanism of Bribery Intensity: Capital Mobility

The bargaining hypothesis (Svensson, 2003) suggests that bribery intensity is a function of a firm’s ability to walk away from the table (Lee et al., 2010). To understand the intrinsic bargaining power associated with state ownership, we draw insights from the positive theories of state ownership. It has been posited that the distinguishing characteristic of state-owned firms vis-à-vis private firms lies in the constraints the former face and the managerial behavior in response to these constraints (Lawson, 1994). Below, we argue that capital mobility mediates the effect of state ownership on bribery intensity.

Capital mobility—an important determinant of a firm’s cost of relocating its production to another sector/location—may have important ramifications for bribe payouts. Higher capital mobility improves a firm’s bargaining power against corrupt officials as the firm can walk away from the negotiation table and relocate its business to other sectors if officials demand too excessive a bribe payment.

We argue that firms with more state ownership tend to have lower capital mobility from two aspects (i.e., the management and the government). First, a unique feature of the firms with state ownership is receiving conflicting parallel commands from multiple factions of principals within the government (Aharoni, 1982). Different government bodies may intervene, at any point, in attempts to align the priorities of the firm’s objectives to the favored ones from their particular vantage points, as opposed to the preferences of management. This dampens managers’ willingness to manage the enterprise actively vis-à-vis following governmental mandates and ascribing any losses to these mandates (Levy, 1987). As a result, unlike private firms that adapt to the environment by searching for alternative courses of action (Cyert & March, 1963; Luo, 2011), managers of firms with state ownership are less motivated to devote search efforts and evaluate the value of outside options.

Second, the state deliberately or inadvertently raises the barriers to exit for firms with state ownership. Divesting from certain state-dominated sectors is usually barred (Lin et al., 1998). The same is true for relocating capital investments to other provinces when the local government takes majority equity position or has minority but “golden shares” that come with veto rights (Cuervo-Cazurra et al., 2014). On the other hand, obtaining capital at subsidized rates induces firms with state ownership to employ capital-intensive production techniques (Lawson, 1994), leading to less salvage value of the production equipment and lower likelihood of closure (Colombo & Delmastro, 2001). Given the barriers to exit and managers’ lack of search efforts, firms with more state ownership may be less concerned with the extent to which the invested capital can be reallocated, and would organize production accordingly—in such a way that diminishes capital mobility relative to other firms.

Taken together, other things being equal (i.e., firm ability, profitability, and strategy flexibility), the prominent feature of state ownership with the government reduces the capital mobility of firms with state ownership. Thus, the hypothesis is proposed:

Then we extend the bargaining hypothesis to argue that bribe-paying firms may exhibit higher bribery intensity because of their reduced capital mobility, which weakens their ability to “walk away from the table” while negotiating the amount of illicit payments with rent-maximizing officials (Husted, 1994). As explained by Svensson (2003), once the firm submits to bribery requests, the amount of bribes is the outcome of the bargaining process between the bribe-paying firm and bribe-seeking public officials. Officials aim to extort the highest possible bribes, to the extent that non-complying firms may exit from the market altogether.

As discussed above, firms with lower capital mobility indicate that they already put most of their capital in certain sectors. Due to low level of flexibility, the firm needs to protect itself from other competitors and new entrants, which lead to the increase in their bribe payments. On the other side, firms with higher capital mobility are actively engaged in innovative businesses, they can quickly transfer their business sectors with low governmental intervention or bribery requests. Thus, the hypothesis is proposed:

Taken together, we argue that state ownership may make firms less capable of reallocating their production to other sectors or locations. Therefore, when firms with state ownership have to pay bribes, they may suffer from weaker bargaining power vis-à-vis officials due to the lack of capital mobility. Taking advantage of the diminished “refusal power” of firms with state ownership, predatory public officials may seek to, and in fact can, extract higher bribes from firms with more state ownership. This may be an important reason why firms with state ownership exhibit a higher level of bribery intensity than others, should they engage in grafting. Therefore, the mediation mechanism of bribery intensity is proposed:

Method

Sample

We draw upon the recent World Enterprise Survey (WES) conducted by the World Bank from 2006 to 2013. 1 WES is a cross-sectional survey of more than 94,000 firms from over 120 countries. In the WES project, the World Bank periodically collects worldwide firm-level data through several rounds of surveys across years to develop a comprehensive database of various firm and business environment-specific characteristics. The survey is answered by business owners and top managers, sometimes managers in human resource and financing department involvement in the response. 2 WES contains items regarding the percentage of sales firms pay to bribe public officials for obtaining various public services. Recent research (Uhlenbruck et al., 2006) has confirmed the validity of the bribery items in the survey. Another advantage of the WES data is that it applies a stratified sampling approach to select the surveyed firms from the complete population of registered companies. 3 Firms included in the survey exhibit sufficient heterogeneity in terms of size, ownership, industry membership, and country of origin, which alleviates the problems associated with unrepresentative samples encountered in many cross-country studies (Beck et al., 2006). Therefore, our sample is cross-sectional and cross-country data.

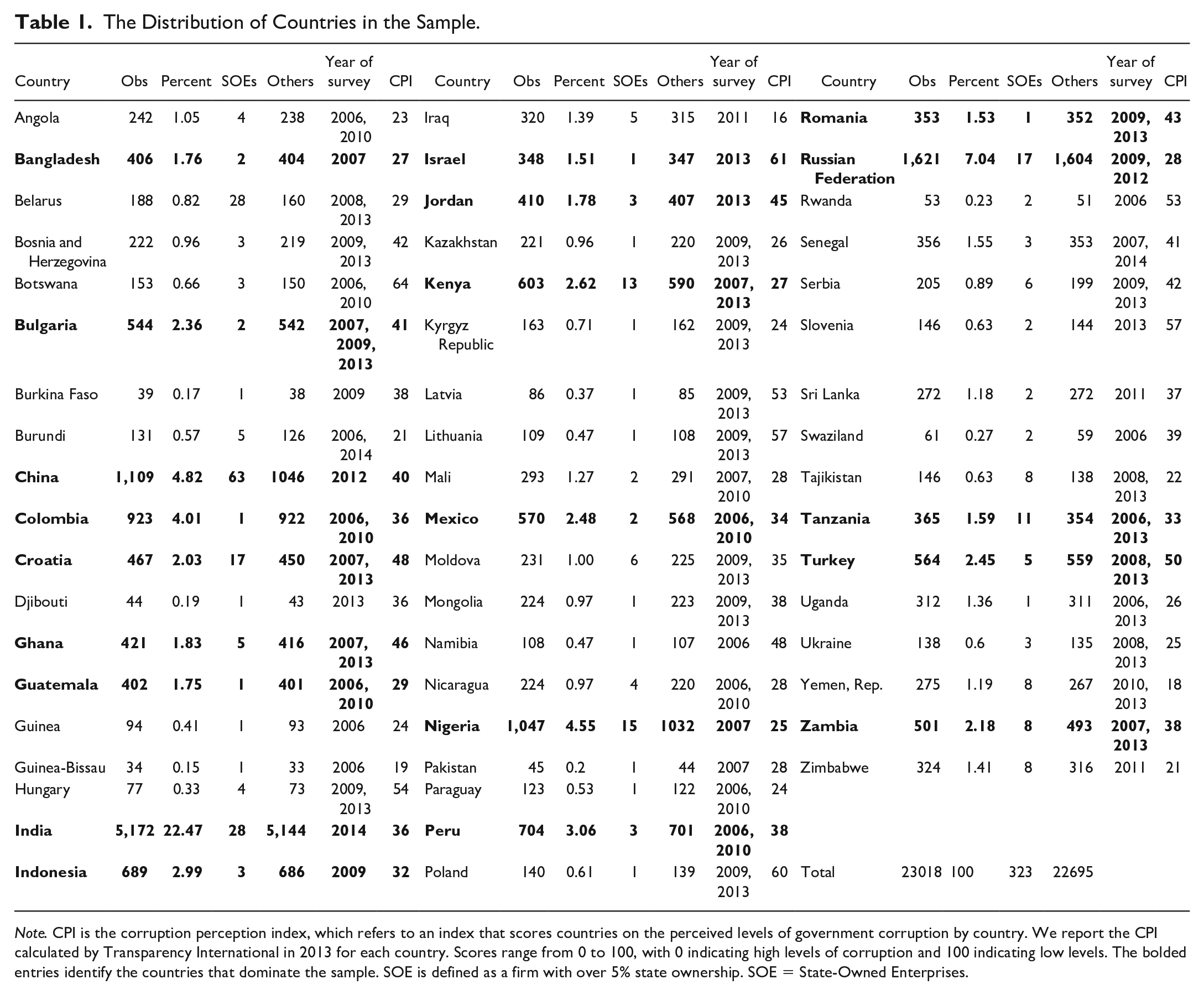

We construct our sample in three steps. First, we follow the normal practice to exclude observations with missing information for our main variables of interest (i.e., bribery and firm ownership; Birhanu et al., 2016; Luo & Han, 2009). We also conduct robustness checks on common method bias to ensure that missing observations across bribery analyses are not likely related to any systematic pattern. Second, we exclude all observations from countries for which no SOEs were surveyed by the WES. Finally, we merge WES data with World Bank’s World Governance Indicators (WGI). By applying the above criteria and deleting observations with missing values, our final sample consists of 23,018 firms from 54 countries. The sample distribution of countries is shown in Table 1.

The Distribution of Countries in the Sample.

Note. CPI is the corruption perception index, which refers to an index that scores countries on the perceived levels of government corruption by country. We report the CPI calculated by Transparency International in 2013 for each country. Scores range from 0 to 100, with 0 indicating high levels of corruption and 100 indicating low levels. The bolded entries identify the countries that dominate the sample. SOE is defined as a firm with over 5% state ownership. SOE = State-Owned Enterprises.

We perform statistical tests to rule out systematic correlations between the main variables that could arise from the measurement method. First, we apply the Kolmogorov–Smirnov test (Siegel & Castellan, 1988) to assess the impact of nonresponse bias by comparing the observable characteristics of bribe-paying firms against other firms. We find no evidence of significant differences between firms reporting that they engage in bribery and firms that do not. Second, we perform a confirmatory factor analysis to test for the effect of a single unmeasured latent method factor. We compare the fit of a model that includes the latent method factor with a model that does not (Podsakoff et al., 2003). We do not find evidence of common method bias.

Measures

Dependent variables

We follow prior research (Lee et al., 2010; Lee & Weng, 2013; Zhou & Peng, 2012) to obtain the measures of our two dependent variables, bribery propensity and bribery intensity from the WES. Participants in the WES are requested to indicate the percentage of annual sales paid to public officials in informal payments for getting things done. The responses to this question are reported in terms of percentages.

Our first dependent variable, bribery propensity is defined as the likelihood of participation in bribery by a given firm. To measure this variable, we code those firms that reported bribery activities in a given year as 1, and 0 otherwise. The resulting binary measure of bribery propensity has a theoretical basis similar to those used in previous studies (Morgan, 1993; Zhou & Peng, 2012). Our second dependent variable, bribery intensity, is a continuous variable measured by the percentage of total sales paid as bribes. This is also consistent with various previous studies (Lee et al., 2010; Lee & Weng, 2013; Wu, 2009).

Independent variable

As any shareholding by the government may indicate government interference and interest in an organization (Meyer et al., 2014; Zheng et al., 2013), we measure our main independent variable, state ownership, as a continuous variable representing the percentage of firm shares owned by the government, ranging from 0 to 100. This variable is also provided in the WES survey. We also run robustness tests using a set of binary variables that equal 1 if the government owns more than 5%, 30%, or 50% shares in a firm and 0 otherwise, 4 in which we can distinguish the comparisons between majority-state-owned versus private firms.

Mediating variables

For our H1 and H2, we test the mediating effects of administrative hurdles and capital mobility on the relationship between state ownership and bribery propensity or bribery intensity. First, we follow previous research which indicates that bureaucratic requirements of obtaining licenses or settling taxes impose considerable administrative barriers to business operations, and influence the likelihood that a firm will encounter the demand for bribes (Cuervo-Cazurra, 2008; Svensson, 2003; Uhlenbruck et al., 2006). Therefore, we use two variables business licensing and permits, and tax inspection to test the mediating effect of administrative hurdles.

Consistent with prior research (Khalil et al., 2015; Ma et al., 2010), we obtain our first variable, business licensing and permits, from the WES question “Is business licensing and permits No Obstacle, a Minor Obstacle, a Major Obstacle, or a Very Severe Obstacle to the current operations of this establishment?.” We code this variable as a binary one, which equals 1 if access to business licensing and permits is a major or a very severe obstacle for the firm indicating that the firm enjoys lower administrative hurdles, and 0 otherwise. Our second variable to operationalize administrative hurdles is tax inspection, which we also obtain from the WES. Following previous research (Hellman et al., 2000; Knack, 2007; Wu, 2009), this variable is based on the WES question, “Over the last 12 months, was this establishment visited and/or inspected by tax officials?” We code tax inspection as a dummy variable that equals 1 if the firm was visited and/or inspected by tax officials in the year, and 0 otherwise. 5

To capture capital mobility, we follow Svensson (2003) to use the alternative return on the firm’s capital stock. As argued by Svensson (2003), a firm's cost of refusing to pay is determined by the alternative return on the firm's capital stock, assuming that firm’s refusal to pay bribes may force it to exit from the current market. The relative cost or benefit of exiting from the market is reflected in the difference between the forgone profits (gross profit after paying bribes) and the expected profits the firm could make elsewhere. Accordingly, we calculate alternative return on the firm’s capital stock as the residual from the regression of the ratio of resale to replace values of the capital stock to the average age of the capital stock and a constant (Svensson, 2003). 6 The rationale of alternative return to proxy capital mobility is that higher alternative return indicates higher expected profits the firm could make elsewhere thus increases the capital mobility of the firm.

Control variables

We follow prior research to control for various firm-level determinants of bribery behavior. First, the link between firm size and bribery behavior is well documented (Martin et al., 2007). Small firms lack the power to resist predatory bribery requests (Svensson, 2003), and may appear to pay a higher proportion of their revenues than large firms due to the same equilibrium rate of bribery across firms of all sizes (Wu, 2009). Therefore, we include firm size as a continuous variable measured by the logarithm of the total employees of a firm. As sales were reported in local currencies, we convert all sales to U.S. dollars by using the exchange rate for the year in which WES collected data for that particular firm. In addition, Amato and Amato (2007) and Tilley (2000) suggest that firm age is relevant in predicting ethical behavior, in that younger firms tend to focus more on survival and growth and are less likely to become involved in unethical and fraudulent activities. We control for firm age, as measured by the logarithm of the number of years since the establishment of a firm.

We also account for the role of manager’s experience, measured as the logarithm of the number of years that the top manager worked in their firms’ current sectors (Birhanu et al., 2016). In addition, given that listed firms face more effective and intensive monitoring regarding corporate misconduct, we include public listing, a dummy variable that equals 1 if the firm is publicly listed, and 0 otherwise. Moreover, firms concentrating on the domestic market may have stronger incentives to bribe in order to obtain the local market privileges, whilst it is arguably less necessary for firms focusing on international markets to pay bribes (Y. Chen et al., 2008). We control for this effect by including international market, a dummy variable that equals 1 if the firm’s main markets are international, and 0 otherwise.

(Wu, 2009) suggests that the use of external auditors represents one of the most important obstacles to corruption. We include external audit, a dummy variable that equals 1 if the establishment has its annual financial statement checked and certified by an external auditor, and 0 otherwise. We control for, profitability, as the ratio of total profits to total sales. We also control for foreign firm to consider the potential differences due to different ownership, which takes the value of 1 if more than 50% of a firm is owned by foreign investors. We also control for the corruption perception index (CPI) in each country, which ranges from 0 to 100, with 0 indicating high levels of corruption and 100 indicating low levels.

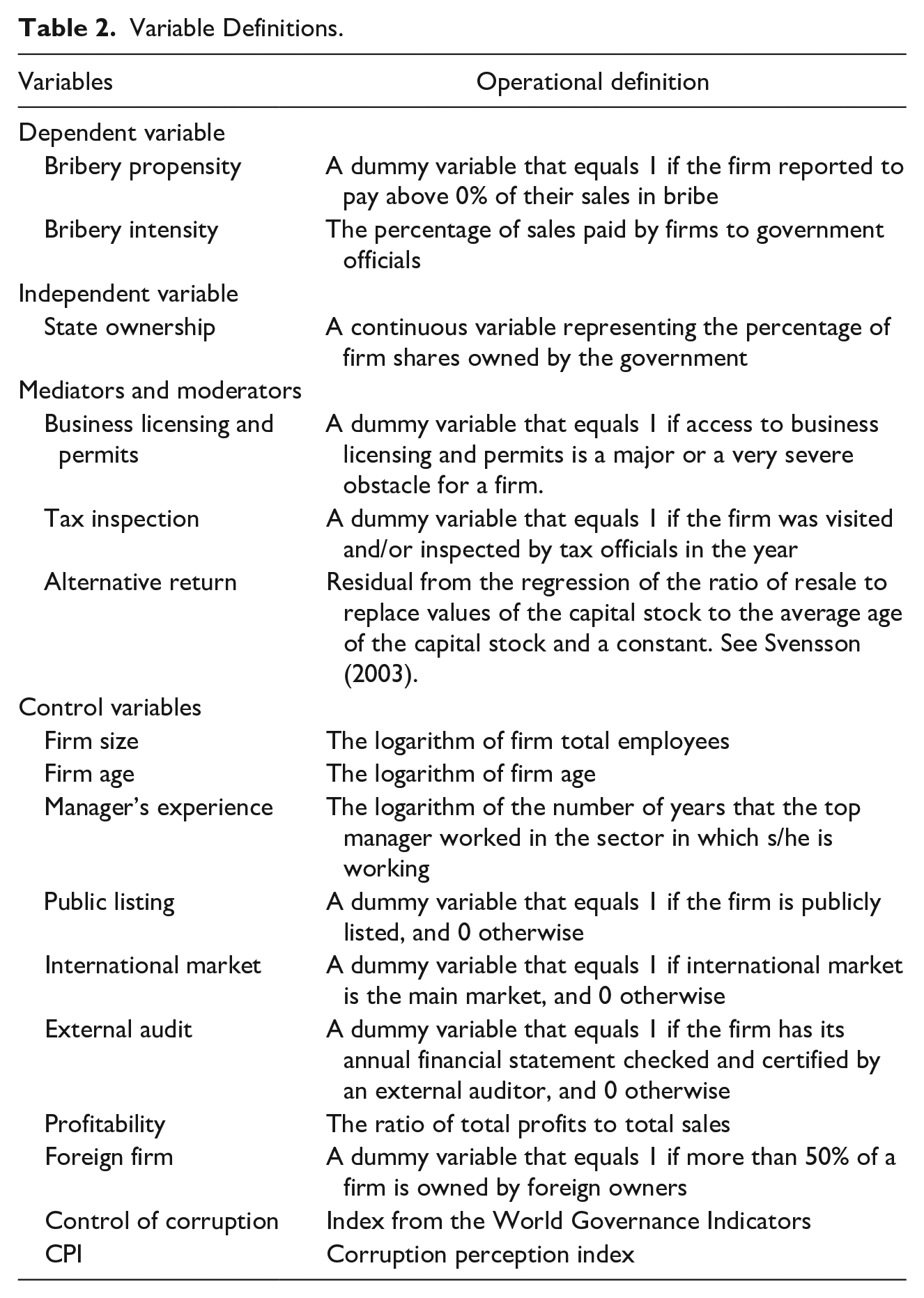

Finally, we use dummy variables to control for potential country, industry, and time effects. We summarize the variables and their operational definitions in Table 2.

Variable Definitions.

Statistical Approach

Following previous studies that empirically test the difference between propensity and intensity of firm behavior (Estrin et al., 2008; Ganotakis & Love, 2012), we need to employ a two-stage analysis to test our baseline hypothesis. Thus, we employ a two-stage Heckman selection model because unobserved omitted variables such as the firm’s ability to extract benefits from corrupt transactions may introduce a sample selection bias (Certo et al., 2016).

In the first stage of Heckman selection model, we adopt a Probit model to regress our first dependent variable, bribery propensity, on all the explanatory variables. We also include an additional variable, control of corruption, to meet the exclusion restrictions’ requirement for the first stage regression (Sartori, 2003). Our exclusion restriction variable is sourced from the World Governance Indicators and defined as the quality of country-specific governance with respect to anti-corruption. It ranges from −2.5 (weak governance performance) to 2.5 (strong governance performance). As control of corruption focuses on the prevention mechanisms that a society develops against corruption, it may lessen the average firm’s likelihood of undertaking corruption activities in its normal interactions with public officials (Roy & Oliver, 2009). However, once firms have decided to engage in bribery even though there is high punishment for bribery, control of corruption may not affect their decision on the amount of bribery. Empirically, our results showed that control of corruption significantly influence the bribery propensity (probability of an observation’s appearing in the second stage) but do not influence bribery intensity (the ultimate dependent variable of interest in the second-stage model), which fits the requirements for exclusion restriction in a sample selection model (Certo et al., 2016). Taken together, control of corruption is an appropriate exclusion restriction both conceptually and empirically. We estimate the inverse Mills ratio from the first stage regression, which is then included in the second stage.

In the second stage model, we regress our second dependent variable, bribery intensity, on the explanatory variables only for bribe-paying firms. Since bribery intensity is a censored variable in the second stage of the procedure, we apply a Tobit model in the context of censored dependent variables. In addition, the two-stage model specification allows the explanatory variables to have varying effects on bribery propensity and bribery intensity respectively, which is appropriate to test our hypotheses. Moreover, we test the significance of control of corruption as the exclusion restriction variable in the second stage. The insignificant result in the second stage confirms the validity of control of corruption as an exclusion instrument for the first stage regression. Finally, the significant findings of the inverse Mills ratio in the second stage for most model specifications confirm the appropriate use of the Heckman selection model.

We use a mediation model to test our hypotheses, following the criteria suggested by Baron and Kenny (1986): (a) the initial explanatory variable must be correlated with the mediator and the outcome variable, (b) the mediator must be correlated with the outcome variable, and (c) the effect of the explanatory variable on the outcome variable in a model that includes the mediator should be significantly smaller than in a model that does not include the mediator. To test the mediation effects of business licensing and permits and tax inspection on bribery propensity, we use the first stage Probit model. To test the mediation effect of alternative return on bribery intensity, we use the second stage Tobit model. In both Probit and Tobit models, we include country, industry, and year fixed effects to control for unobserved country, industry, and year characteristics and thus get unbiased estimates. Fixed country effect indicates that the estimates are estimated from within country, and the overall conclusions are consistent across countries.

Results and Robustness Checks

Results

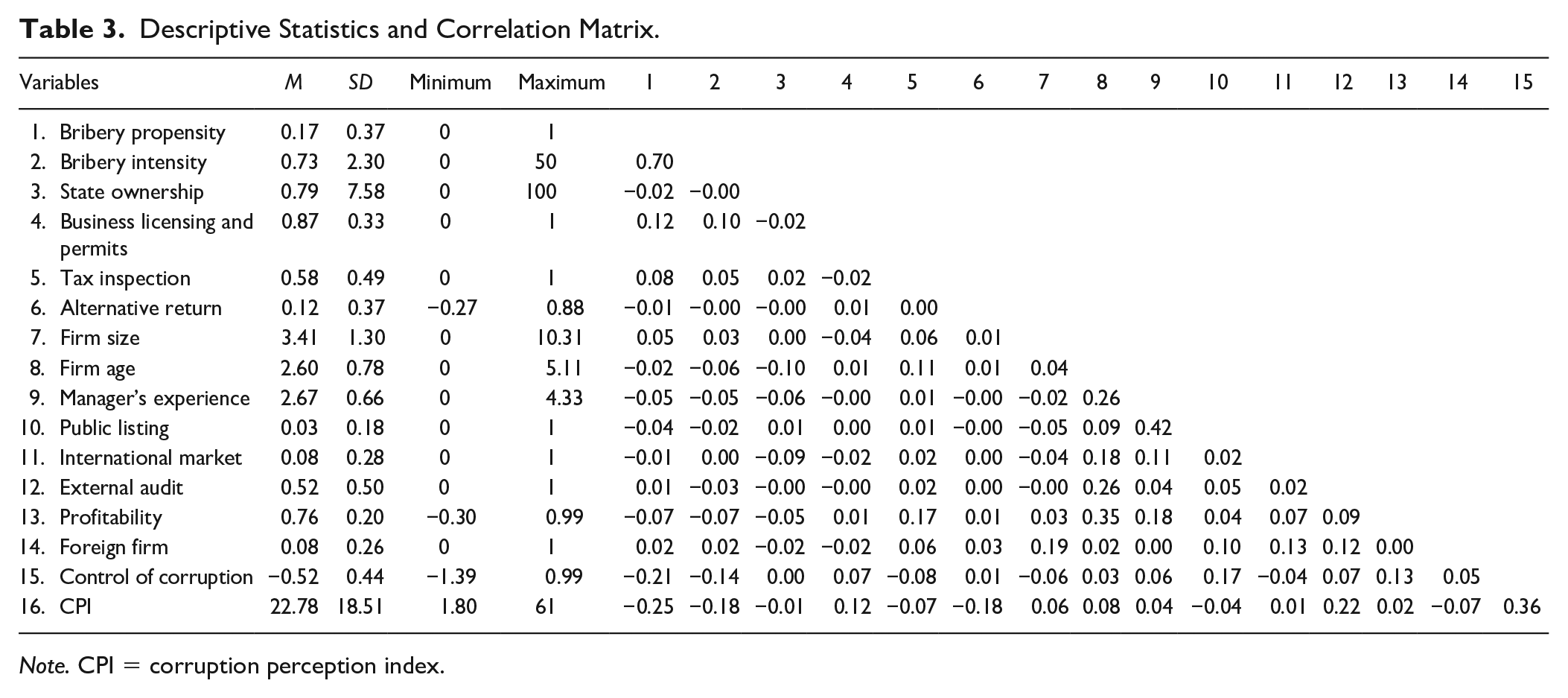

Table 3 provides the descriptive statistics and the correlation matrix for all our variables. Our sample indicates that 16.57% of firms engaged in bribery during our study period and these bribe-paying firms, on average, paid 0.73% of their sales revenues in bribes. In addition, considering any firm with at least 5% state ownership as SOE, we find 13.31% of SOEs engaged in bribery whereas 16.61% of other firms paid bribes. Among bribe-paying organizations, however, SOEs paid a higher proportion, 1.03% of their sales, in bribes as compared with other firms that paid only 0.72% of their sales in bribery. These sample statistics confirm our initial assertion about differences in bribery propensity and bribery intensity. 7 With regard to multicollinearity, we use the SAS linear regression collinearity diagnostics to check the value of the variance inflation factor (VIF) for all independent variables and interaction terms. We find that VIF ranges between 1.00 and 1.32, which is much lower than the threshold value of 10 (Hsieh et al., 2003). These results suggest that multicollinearity may not be a problem in our estimation.

Descriptive Statistics and Correlation Matrix.

Note. CPI = corruption perception index.

Tables 4 and 5 report the results for our two-stage model and also test our H1 and H2 about bribery propensity and bribery intensity. Model 1 in Table 4 presents the results for the first stage with bribery propensity as the dependent variable, although Model 1 in Table 5 reports the results for the second stage—where only firms engaged in bribery are included—with bribery intensity as the dependent variable. We find the coefficient of the main variable, state ownership, to be negative and significant (β = −0.01, p<.001) in the first stage, but positive and significant (β = 0.07, p<.001) in the second stage. Hence, H1 and H2 are supported, in that state ownership tends to reduce the propensity to bribe, but raises the relative amount of illicit payments once the firm engages in bribery. We assess the economic significance of our results by calculating the marginal effects of our coefficients in Model 1 of Tables 4 and 5. We find that one standard deviation increase in state ownership reduces the probability of the bribery by 1.32%, and one standard deviation increase in state ownership increases the intensity of the bribery by 5.67%.

The Impact of Causal Mechanisms on Bribery Propensity.

Note. Standard errors are reported in parentheses. CPI = corruption perception index.

p < .10. *p < .05. **p < .01. ***p < .001.

The Impact of Causal Mechanisms on Bribery Intensity.

Note. Standard errors are reported in parentheses. CPI = corruption perception index.

p < .10. *p < .05. **p < .01. ***p < .001.

Among the control variables, we find firm size increases bribery propensity (β = 0.04, p<.001) but reduces bribery intensity (β = −0.32, p<.001). CPI decreases bribery propensity (β = −0.01, p<.001) and bribery intensity (β = −0.05, p<.05). In addition, we do not find statistically significant impacts of firm age, manager’s experience, public listing, international market, profitability, and foreign ownership on bribery propensity. However, manager’s experience (β = 0.23, p<.1) tends to increase bribery intensity international market (β = −0.68, p<.05) appears to reduce it. Moreover, we do not find statistically significant impacts of external audit on both bribery propensity and intensity. In addition, we find that the exclusion restriction variable, control of corruption, tends to reduce bribery propensity (β = −0.75, p<.001). Finally, we find statistically significant inverse Mills ratio in the second stage, lending support to the use of the Heckman selection model (Heckman, 1979).

Models 2 to 5 in Table 4 test our H1a, H1b, and H1c. Model 2 shows that the effect of state ownership on business licensing and permits is negative and significant (β = −0.01, p<.05), implying that state ownership reduces the firm’s reliance on individual officials’ discretion in issuing business licenses and permits (H1a). Next, Model 3 shows that the effect of state ownership on bribery propensity, which appears significant in Model 1, becomes statistically insignificant after controlling for business licensing and permits. These results show that business licenses and permits mediate the effect of state ownership on bribery propensity. Similarly, Model 4 in Table 4 shows that the effect of state ownership on tax inspection is negative and significant (β = −0.01, p<.001), implying that state ownership reduces the firm’s dealings with tax officials (H1a). Furthermore, Model 5 in Table 4 indicates that the effect of state ownership on bribery propensity becomes insignificant after controlling for tax inspection. These results show that tax inspection also mediates the effect of state ownership on bribery propensity. Overall, we find both measures of administrative hurdles to mediate the effect of state ownership on bribery propensity, providing support for our H1b and H1c.

We test our H2a, H2b, and H2c in Models 2 and 3 of Table 5. Model 2 shows that the effect of state ownership on alternative return is negative and significant (β = −0.01, p<.05), implying that state ownership diminishes the alternative return on the firm’s capital stock (H2a). Model 3 shows that the effect of state ownership on bribery intensity becomes insignificant after controlling for alternative return. Therefore, H2b and H2c are supported, confirming that capital mobility mediates the effect of state ownership on bribery intensity.

Robustness Checks

To ensure the robustness of our results to alternative measures and specifications, we perform several robustness tests. First, to confirm that the results that are not driven by our specification of state ownership, we run robustness tests using a set of binary variables of SOE that equals 1 if the government owns more than 5%, 30%, or 50% of shares in a firm respectively, and 0 otherwise (Meyer et al., 2014; Zheng et al., 2013). As the results remain qualitatively unchanged, we only report the main specification.

Second, to confirm that the results are robust to different combinations of countries. First, we test for the results are not driven by the behavior in particular emerging countries (e.g., China, India, and Russia), we run robustness tests using the sample excluding particular emerging countries. We also run robustness tests on the large proportion (in relatively larger proportion to Turkey) and small proportion countries (in relatively smaller proposition to Turkey) separately. The results are consistent with the main results, `` which indicate that our results are robust and that our conclusions are generalizable.

Third, we perform the likelihood ratio test to check the validity of the two-stage model specification. Since bribery intensity is a limited variable within the range of 0 and 1, we could apply either a Tobit model in the context of censored dependent variables, or a fractional logit model in the context of fractional dependent variables (Papke & Wooldridge, 1996). However, this line of modeling approach has the implicit assumption of equality in the signs and magnitudes of the coefficients of explanatory variables in both stages (Ganotakis & Love, 2012). We employ the likelihood ratio test for the restriction assumption of equality against the unrestricted form. In the procedure, we conduct a Probit regression for bribery propensity followed by a truncated Tobit regression for bribery intensity using only the subsample of bribe-paying firms and perform a likelihood ratio test against the restricted Tobit or fractional logit model for the full sample. The test suggests rejecting the restriction assumption of equality of coefficients at the 1% significance level, which shows the two-stage model specification is appropriate.

Fourth, given that the dependent variable in the second stage is proportion variable. We further performance negative binominal specification model and beta regression to test for the robustness of the conclusions (Baum, 2008; Douma & Weedon, 2019). The results are consistent with our results with Tobit models.

Finally, given that size is controlled in the second stage, measuring bribery intensity as percentage of sales introduces size a second time in the equation. We run a robustness check using the logarithm of the absolute amounts of bribes as the dependent variable and alleviate the concern for double control of the firm size. The results are robust to our conclusions.

Discussion

In this study, we cross-fertilize two important inquiries—firm-level causes of corruption and state ownership—to examine the influence of state ownership on bribery. By drawing upon the control rights/bargaining hypotheses, we argue that state ownership reduces firms’ tendencies to pay bribes, yet increases the relative amount of bribes paid by graft-paying firms to public officials. We also propose the mechanisms behind the seemingly conflicted phenomenon, which include that the lower administrative hurdles for firms with state ownership diminish their required dealings with public officials and thus make them less likely to bribe than others. Meanwhile, state ownership induces the firm to organize production in a way that lowers its capital mobility. Should the firm need to pay bribes, this weakens its bargaining power against corrupt officials over the amount to pay. Utilizing a large sample from the WES, our empirical results support our hypothesis.

Our study makes some important contributions to the literature related to corruption. By drawing upon the control rights/bargaining hypotheses, we not only trace the cause of bribery to an intrinsic firm characteristic but also highlight the fact that bribery propensity and intensity are determined by different sets of mechanisms. On one hand, our analysis offers new theoretical perspectives to this stream of research. On the other hand, the use of two-stage Heckman analysis to alleviate sample selection bias may help other research to further explore other mechanisms. In practice, our analysis yields a nuanced understanding of possible strategies to regulate corporate bribery. A corrective policy aimed at attenuating the firm tendency to pay bribes may unwittingly lead to bigger amounts of illicit payments and a greater extent of corruption. By providing the theoretical foundation to the significant yet divergent effects of an organizational feature (i.e., state ownership) on bribery propensity and bribery intensity, we call on future research to consider them simultaneously.

We also extend the state ownership literature to the context of illicit behavior. A firm with state ownership is a hybrid organization as it earns revenues by selling products in open markets while taking mandates from the government and operating under different constraints. A notable challenge in accounting for the effect of state ownership in strategy research is the high degree of variability in the behavior of firms with state ownership in general (Cuervo-Cazurra et al., 2014; Levy, 1987). A variety of theoretical explanations have been proposed as to why state ownership matters from the general theories of firm behavior. Yet previous studies cannot explain the reasons and mechanisms of how state ownership affects bribery behavior. We aim to integrate the inquiries of state ownership by ascribing explanatory primacy to the intrinsic features associated with state ownership and the common constraints under which firms operate. Testing these mechanisms allows us to disentangle what exactly state ownership contributes. Although recent research highlights the distinctiveness of state ownership in circumventing the barriers that private firms confront (Cuervo-Cazurra et al., 2014), we extend the literature to the context of illicit behavior, leading to a better understanding of how state ownership affects firm strategy and actions.

We also acknowledge some important limitations of our study, which may nevertheless pave the ground for future research. First, an important limitation of our study is in good part related to the challenge of obtaining good data on a sensitive topic like bribe payments. WES measures bribe payment with an indirect question, a common strategy to solicit responses about delicate issues. The bribery item in the WES survey has been extensively employed in various corruption-related research studies (Birhanu et al., 2016; Lee & Weng, 2013; Martin et al., 2007 to name a few) and scholars have confirmed the validity of WES in research studies (Uhlenbruck et al., 2006). We acknowledge that a structured questionnaire may not fully reveal the nuances regarding organizational bribery behavior. Besides, the mixed interdependencies between bribery propensity and intensity, and the frequency of the bribery behavior should be considered in future research. Another limitation is that we do not know the details to whom the firms bribe. It would be more meaningful if one can explore the bribe demand from different levels of officials. Therefore, we encourage future research to employ in-depth interviews and other data collection approaches to uncover various dynamic and context-specific features of bribe payments (Lee & Weng, 2013). Besides, we also call for future research to investigate the heterogeneous effects of state ownership across countries, industries, and different levels of government involvement.

Due to the fact that WES uses the stratified sampling methodology to make sure that the sample is representative of the population, the proportion of SOEs in our sample is relatively small. Thus, we encourage future studies to investigate the effects of state ownership on bribery with a larger sample with higher proportions of SOEs. Even though we have a few hundred SOEs in our sample, the SOEs population is huge and it is more concentrated in countries where we observe bribery incidences. Most countries where we find bribe payments are the same economies where SOEs are wasting money on bribery. We encourage future studies to consider institutional factors that may influence SOE bribery in some specific countries.

Furthermore, we test only a subset of possible mechanisms that may explain the conceptual conflation between bribery propensity and bribery intensity of state-owned firms. Our research is, by no means, conclusive on the topic as several studies have hypothesized a number of factors affecting behavior in general, such as the agency problem, political connections, and government intervention (Meyer et al., 2014; Shi et al., 2014; Shleifer & Vishny, 1994; Tan & Peng, 2003). Limited by our data, we are not able to disentangle the impact of all these mechanisms on bribery behavior, and we are unable to rule out other sets of different mechanisms in different bribery stages. It would also be interesting to explore the interactions among the mechanisms (i.e., soft budget, agency issues, divergent managerial experience, institutions, etc.). Besides, it would be valuable to explore the interaction and complementation of two mechanisms (i.e., control rights and bargaining power in different stages) if there is more in-depth data.

Despite these limitations, our study addresses an important gap between academic research and public concerns. The media has increasingly cast spotlight on illegal deals involving heavy amounts paid by SOEs. Damning examples include the recent anti-corruption campaign by the Chinese government on corruption, which has uncovered enormous bribes paid by SOEs to public officials and politicians (South China Morning Post, 2012). The research to investigate the mechanisms of how state ownership affects bribery has been lately called upon since state ownership remains important and distinct after pro-market reforms and emerge as a notable force in today’s world economy (Bruton et al., 2015; Cuervo-Cazurra et al., 2014). We fill this gap by investigating the bribery propensity and intensity of firms with state ownership. Figuring out the mechanisms of state ownership and bribery, our research call for attention to control SOE bribery. As an answer to the recent call for research (OECD, 2019, State-Owned Enterprises and Corruption Report), our study provides important policy implications for regulators promoting transparency and fair competition.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China (Grant Number 71873136) and University of South Carolina CIBER grants.